Accounting Standard Updates - HFMA Spring Conference 2018 - PPT Presentation

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Accounting Standard Updates HFMA Spring Conference 2018 Presented by: Kimberly Sokoloff, Health Care Assurance Services Senior Manager Elizabeth Lasnier, Health Care Assurance Services Manager

Presenters

HFMA 2018 Spring Conference

Kimberly Sokoloff, CPA

Senior Manager – National Health Care Practice

Kimberly.Sokoloff@mossadams.com

1

Elizabeth Lasnier, CPA

Manager – National Health Care Practice

Elizabeth.Lasnier@mossadams.com

Agenda

• Revenue Recognition

HFMA 2018 Spring Conference

• FASB Grants and Contracts Project

• Leases

• NFP Financial Statements

• Financial Instruments

2

• Other Recent ASUs

• Q&ARecently Issued FASB Standards

Upcoming Effective Dates: The “Big Three” for NFP

Healthcare (Annual FS)

HFMA 2018 Spring Conference

Not-for-Profit

Financial Revenue Leases

Statements

4

CY 2018* (All) CY 2018* (Public) CY 2019* (Public)

CY 2019* (Non-public) CY 2020* (Non-public)

*or FYs beginning in those years

NOTE: “Public” for Revenue and Leases includes NFPs with public debt (conduit or direct)Revenue Recognition

Revenue Recognition – Scope

• Lease contracts

• Insurance contracts

HFMA 2018 Spring Conference

• Financial instruments

All contracts • Guarantees

with customers, • Nonmonetary exchanges in the same line of business to facilitate sales

except to customers

6

• Contributions

Contracts not • Collaborative arrangements

with customers

are excludedRevenue Recognition – Model

Core principle:

HFMA 2018 Spring Conference

Recognize revenue to depict the transfer of promised goods or services to

customers in an amount that reflects the consideration to which the entity

expects to be entitled in exchange for those goods or services.

Steps to apply the core principle:

7

5.

1. Recognize

2. 3. 4. revenue

Identify Determine when (or as)

Identify Allocate

contract(s) transaction a

performance transaction

with the price performance

obligations price

customer obligation is

satisfiedRevenue Recognition – Disclosures

• Revenue recognized from contracts with

HFMA 2018 Spring Conference

customers vs. other revenue sources

Contracts with Customers

• Impairment losses recognized on

receivables or contract assets

• Performance obligation timing*

• Significant payment terms*

Performance Obligations • Nature of promised goods or services*

• Obligations for returns, refunds, warranty*

8

• CY revenue for PY obligation*

• Significant financing component*

• Cost of obtaining a contract*

• Portfolio approach

Practical expedients and accounting • Invoice method

policy elections • Immaterial promises

• Shipping and handling

• Sales taxes

• Loss contract unit of account

* Mostly optional for nonpublic entitiesRevenue Recognition – Disclosures

• Qualitative and quantitative*

HFMA 2018 Spring Conference

disaggregation of revenue into categories

Disaggregation of revenue

that depict how revenue and cash flows

are affected by economic factors

• Opening and closing balances

• Amount of revenue recognized from

contract liabilities*

Information about contract balances

9 • Timing of performance obligation vs. pay*

• Explanation of significant changes in

contract balances*

• Transaction price allocated to remaining

performance obligations*

Remaining performance obligations • Quantitative or qualitative explanation of

when amounts will be recognized as

revenue*

* Mostly optional for nonpublic entitiesRevenue Recognition – Disclosures

• Short-term contract exemption

HFMA 2018 Spring Conference

• As-invoiced exemption

Remaining performance obligations:

• Sales- or usage-based royalty exemption

Optional exemptions

• Directly allocable variable consideration to

wholly unsatisfied obligation exemption

• Optional disclosures elected, nature of

Optional exemption disclosures obligation, remaining contract direction,

10 additional consideration details

• Timing of satisfaction of performance

obligations*

Significant judgments

• Transaction price and amounts allocated

to performance obligations*

Contract costs • Contract cost assets and changes*

Interim requirements • Quantitative disclosures*

* Mostly optional for nonpublic entitiesConsiderations for Disaggregation of Revenue

Timing of transfer of

HFMA 2018 Spring Conference

Payor category goods or service

(Medicare, Medicaid,

Commercial, Self-

Pay, etc.)

Example Service type

11

categories (inpatient, outpatient,

home health, etc.)

Contract type (fee for

service, capitation,

etc.)

GeographyDisclosure Requirements – Disaggregated Revenue

Revenue Disaggregation by Payor

HFMA 2018 Spring Conference

The composition of patient care service revenue by primary payor for the years ended December 31 is as

follows:

20x2 20x1

Medicare $16,000 $15,000

Medicaid 6,000 5,000

12 Managed care 11,000 10,500

Commercial insurers 4,000 3,500

Uninsured 1,800 1,900

Other 1,000 1,000

$39,800 $36,900

Source: AICPA Health Care Entities Revenue Recognition Implementation Issue Paper #8-6 – Presentation and Disclosure.

As of January 2018, this paper has not been finalized in the AICPA Audit & Accounting Revenue Recognition Guide.Disclosure Requirements – Disaggregated Revenue

Revenue Disaggregation by Region, Service Line, Reimbursement, Timing

20x2

HFMA 2018 Spring Conference

Northeast Central Southeast Total

Services lines:

Hospital-inpatient $ 3,500 $ 1,000 $ 3,000 $ 7,500

Hospital-outpatient 4,500 2,000 2,000 8,500

Physician services 3,000 3,000 5,000 11,000

Home health and hospice 1,000 800 2,000 3,800

Retail sales 2,000 2,000 4,000 8,000

Other 400 200 400 1,000

13

$ 14,400 $ 9,000 $16,400 $39,800

Method of reimbursement:

Fee for service $ 8,900 $ 5,300 $ 6,000 $ 20,200

Capitation and risk sharing 3,100 1,500 6,000 10,600

Other 2,400 2,200 4,400 9,000

$ 14,400 $ 9,000 $ 16,400 $39,800

Timing of revenue and recognition:

Health care services transferred over time $12,400 $ 7,000 $12,400 $31,800

Retail pharmacy and equipment sales at point in time 2,000 2,000 4,000 8,000

$ 14,400 $ 9,000 $ 16,400 $39,800

Source: AICPA Health Care Entities Revenue Recognition Implementation Issue Paper #8-6 – Presentation and Disclosure.

As of January 2018, this paper has not been finalized in the AICPA Audit & Accounting Revenue Recognition Guide.List of AICPA Papers on the Issues

• Final (included in Revenue Recognition Guide): AICPA Revenue Recognition homepage

HFMA Spring Conference 2018

for Health Care:

- Self-pay patient balances (Issue 1)

https://www.aicpa.org/interestareas/frc/ac

- Applying a portfolio approach (Issue 2)

countingfinancialreporting/revenuerecogn

- Presentation and disclosures (Issue 6) ition/rrtf-healthcare.html

• Exposure period ended, to be finalized soon:

- Third-party settlements (Issue 8)

- Risk sharing arrangements (bundled payments) (Issue 9)

14

- Performance obligations (Issue 10)

• Currently or soon to be out for exposure:

- Various issues fully or largely related to CCRCs (Issues 3,4,5)

- Accounting for contract costs (Issue 7)Identify the Contract(s) with a Customer

A contract is an agreement between two or more parties that creates enforceable rights and obligations.

HFMA 2018 Spring Conference

ASC 606 says: “Enforceability of the rights and obligations in a contract is a matter of law. Contracts can

be written, oral, or implied by an entity’s customary business practices.”

Additionally:

…collection of substantially …rights of parties and

all consideration is payment

15

probable terms can be

identified

A contract

exists if…

…it has approval and

…it has commercial commitment of the parties as

substance to their obligationsPrice Concessions

• Explicit Price Concessions • Implicit Price Concessions

HFMA 2018 Spring Conference

- Contract discounts - EMTALA – Role of Medical Screening Exam (MSE)

- Cash pay schedules • Implicit Price Concession Based on Portfolio

- Letter of agreement Approach

- Risk-based contract - Emergency vs Direct Admits

- Contract denials

16

- Charity care

- Uninsured

- Pending Medicaid eligibility

- Dual eligible patientsBad Debt Expense – Not Going Away, But Reduced

• Bad Debt Expense: When a health care entity performs a credit assessment prior to providing services

HFMA 2018 Spring Conference

to a patient and expects to collect substantially all of the discounted charges.

• For example, an elective procedure in which historical experience supports collection of substantially

all of the discounted charges.

17

Many health care providers believe their provision for bad debts for services provided

to uninsured and insured patients with co-payments and deductibles will be

significantly reduced, in comparison to current U.S. GAAP.Portfolio Approach

The standard is generally applied on a contract-by-contract basis with a customer.

HFMA 2018 Spring Conference

Portfolio Approach

18

Health care entities may use a portfolio approach as a practical

expedient, whereby the revenue guidance is applied to a portfolio

of contracts with similar characteristics.

The portfolio approach is allowed if the entity reasonably expects

that the financial statement effects of applying the standard to the

portfolio would not be materially different from applying the

standard to individual contracts within that portfolio.Application of the Portfolio Approach to Contracts with

Patients

• Considerations for a health care entity to determine in grouping contracts with similar characteristics

HFMA 2018 Spring Conference

for inclusion in a portfolio

- Type of service – inpatient, outpatient, skilled nursing, home health, emergency room, elective procedure, etc.

- Type of payors – insurance contract, insurance contract with patient responsibility, governmental programs, uninsured

self-pay, etc.

- Dates when contracts are entered into are close to each other

19

Using a portfolio of similar transactions to make certain estimates and judgments is not the

same as applying the portfolio approach practical expedient.Third-Party Settlements

• Medicare/Medicaid –Variable consideration

HFMA 2018 Spring Conference

• Complex rules

• Timing

• Patient is the Customer

- Payor contract affects variable consideration

20Third-Party Settlements

• Variable consideration should be estimated using on of the approaches below

HFMA 2018 Spring Conference

• Reminder: The selected method should be applied consistently throughout the contract

Expected value Most likely amount

• Sum of probability-weighted amounts in a • The single most likely amount in a range

21

range of possible consideration amounts of possible consideration amounts

• Most utilized when there are a large • Most utilized when there are two possible

number of possible outcomes outcomesThird-Party Settlements

• When determining variable consideration amounts, think about:

HFMA 2018 Spring Conference

• Historical and current reimbursement information, including third-party settlements

• Historical and current experience with the fiscal intermediary

• Current charges, allowable costs, and relevant patient statistics

• Consider all information (historical, current and forecasted) that is reasonably available

• Update estimates each reporting period

22

• Apply one method consistently throughout the contractThird-Party Settlements

• Evaluate the “constraint” of variable consideration revenue

HFMA 2018 Spring Conference

• When assessing whether it is probable that a significant revenue reversal will not occur when the cash

collections or payments are made based on final settlement, consider the following:

• Whether settlement is outside of entity’s control (third-party payor controls settlement process)

• Entity’s experience in estimating third-party settlements with government payors

• Length of time before final settlement is known

23

• Whether payment terms may be changed

• The number of possible consideration amounts – consider range of outcomes and whether there have been

significant differences from reporting period to reporting periodRisk Sharing Arrangements

• Arrangements with third-party payors should be considered in determining the transaction price for

HFMA 2018 Spring Conference

services provided to a patient

• Customer is the patient

• Different types of risk sharing arrangements

• Bundled payment arrangements

• Pay for performance contracts

24

• Contracts with shared savings or shared losses

• Risk pool contracts

• Capitation arrangementsRevenue Considerations for CCRCs

• The following key issues related to CCRCs are still under review by the AICPA Healthcare

HFMA 2018 Spring Conference

Revenue Recognition Task Force:

• Recognizing monthly/periodic fees and nonrefundable entrance fees under different contract types

• Calculating the obligation to provide future services and use of facilities

• Assessing whether a significant financing component exists for refundable and nonrefundable

entrance fees

25

• Accounting for contract acquisition costsGrants and Contracts Project: Clarifying the Scope and Accounting Guidance for Contributions Received and Contributions Made

Scope

• Applies to all entities (NFPs and business entities) that receive or make contributions

HFMA 2018 Spring Conference

unless otherwise indicated.

• Excludes transfers of assets from the government to business entities.

• Applies to both contributions received by a recipient and contributions made by a

resource provider.

27 • The term used in the presentation of financial statements to label revenue (for example,

contribution, grant, donation) that is accounted for within the Scope of Subtopic 958-605

is not a factor for determining whether an agreement is within the scope of that

guidance.Grants and Contracts – Background

HFMA 2018 Spring Conference

Project added to FASB’s Technical Agenda to improve and clarify

existing guidance

ASU 2014-09, Revenue from Contracts with Customers, including related

disclosures, heightened the issue

28 Raised question as to whether grants and contracts are in scope of that guidance

(reciprocal or nonreciprocal)

Long-standing diversity in practice in classifying grants and contracts,

particularly from governmental entities

Issue 1: Reciprocal Versus Issue 2: Conditional Versus

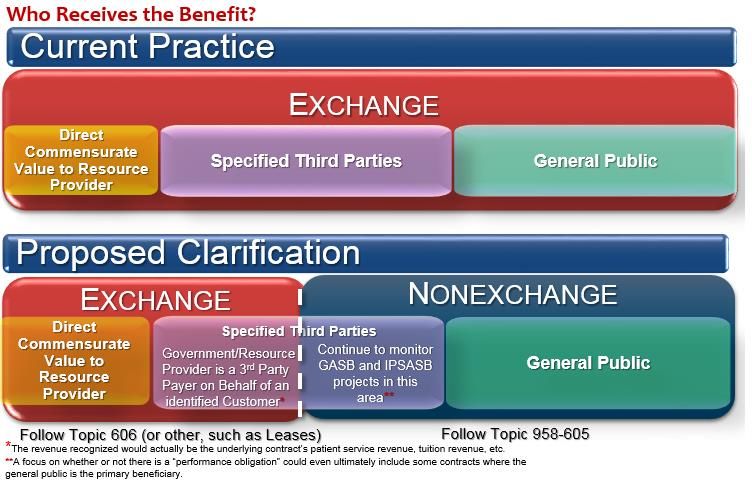

Nonreciprocal UnconditionalIssue 1: Reciprocal (Exchange) vs. Nonreciprocal

(Nonexchange/Contribution) Transactions

HFMA 2018 Spring Conference

29Issue 1: Reciprocal vs. Nonreciprocal Transactions:

Key Clarifications to the Scope of Subtopic 958-605

The proposed ASU would clarify and refine existing guidance in Subtopic 958-605 by adding

HFMA 2018 Spring Conference

paragraphs that would clarify the scope of the Subtopic as well as illustrative examples.

• The resource provider is not synonymous with the general public, even a governmental

entity. If a resource provider receives value indirectly by providing a societal benefit, this

would be considered a nonreciprocal transaction.

30 • If the primary beneficiary of a grant or contract is a third party, an NFP must use

judgment to determine if the transaction is reciprocal or nonreciprocal.

• Furthering a resource provider’s mission or “feel good” sentiment does not constitute

commensurate value received.

• The type of resource provider should not override the substance of the transaction.Issue 2: Conditional vs. Unconditional Contributions

20th HFMA Western Region Symposium

For a Donor-Imposed Condition to Exist:

Proposed Alternative

ASU Rejected

A right to A right to

return/release must return/release must

31

exist; and exist.

The engagement Would have required

must include a barrier a probability

• Indicators and examples assessment about

to help in determination

whether it is likely a

recipient NFP will

fulfill the stipulationsIndicators to Determine a Barrier

HFMA 2018 Spring Conference

To determine what is a barrier, an NFP would consider indicators,

which would include, but are not limited to, the following:

The inclusion of a measurable performance-related barrier or

other measurable barrier.

32 Whether a stipulation is related to the purpose of the

agreement.

The extent to which a stipulation limits discretion by the

recipient.

The extent to which a stipulation requires an additional action

or actions.NFP Revenue Recognition Decision Process HFMA 2018 Spring Conference 33

Transition Approach

• Modified prospective

HFMA 2018 Spring Conference

- Apply to all agreements

o Existing at the effective date (only apply to the portion

of existing agreements not previously recognized)

o Entered into after the effective date

• No restatement of prior amounts recognized

34

• Retrospective application permittedEffective Date

The effective date is the same as the new Revenue Recognition standard (Topic 606), but

HFMA 2018 Spring Conference

allows for early implementation.

Annual periods beginning after December 15, Annual periods beginning after December 15,

2017, including interim periods: 2018, and interim periods beginning after

• Public Business Entities December 15, 2019:

• All other entities

• NFP that has issued, or is a conduit bond

35

obligor for, securities that are traded, listed,

or quoted on exchange or an over-the-

counter marketTimeline of the Project

HFMA 2018 Spring Conference

Issued

Proposed Comment

Update Period Deadline Final ASU

36

August 3, 2017 November 1, 2017 Q2 2018Leases

ASU 2016-02: Leases (Topic 842)

HFMA 2018 Spring Conference

A lease contract conveys the right to use an asset (the underlying asset) for a period of time in

exchange for consideration.

38Identifying a Lease

(The new primary determinant for on/off balance sheet treatment)

HFMA 2018 Spring Conference

That is explicitly or

implicitly specified

An identified asset

Supplier has no practical

ability to substitute and

would not economically

benefit from substituting

39 Lease contracts in the the asset

scope of Topic 842

involve

Decision-making authority

over the use of the asset

The right to control the

use during the lease term

The ability to obtain

substantially all economic

benefits from the use of

the assetLessee Accounting Overview

Balance Income Cash Flow

Sheet Statement Statement

HFMA 2018 Spring Conference

Right-of-use Cash paid for

Amortization

(ROU) asset principal and

expense

Lease interest

Finance Interest expense

liability payments

Right-of-use Single lease Cash paid for

40

Operating (ROU) asset expense on a lease

Lease liability straight-line basis payments

Classification is similar to that in Topic 840, Leases

Recognition and measurement exemption for short-term leases

Other than public business entities may use risk-free rates for measurement of all lease

liabilitiesLessor Accounting Overview

HFMA 2018 Spring Conference

Balance Sheet Income Statement Cash Flow Statement

Cash

Net Interest income and

received for

Finance investment in any profit on the

lease

the lease lease

payments

41 Continue to Lease income, Cash

recognize typically on a received for

Operating underlying lease

straight-line basis

asset paymentsLeases – Getting Ready

HFMA 2018 Spring Conference

Inventory of leases – What’s out there? Know your leases.

42

Materiality – How modern is your capitalization policy?

Debt covenants – To what extent will capitalizing your

operating leases affect covenants based on leverage

ratios?Leases – Getting Ready

HFMA 2018 Spring Conference

Review FASB updates – Proposed ASU issued in January

2018 would provide transition relief

43 IT systems – Does your current system capture all required

information?

Consider required assumptions and inputs – Have you

started considering your discount rates, likelihood of

exercising options, etc?Not-for-Profit Financial Statements

NFP Financial Statements ASU – Key Objectives

(recommended by FASB’s NFP Advisory Committee (NAC))

HFMA

Spring

HFMA 201820th Western Region Symposium

Conference

Improve information

in financial

Update, not Improve net asset statements and Better enable

overhaul, the classification notes about: NFPs to “tell their

current model scheme financial financial story”

performance, cash

flows, and liquidity

45

Issued August 18, 2016, ASU No. 2016-14Net Asset Classification

HFMA 2018 Spring Conference

Current Temp. Perm.

Unrestricted

GAAP Restricted Restricted

GAAP Without Donor

46 Restrictions With Donor Restrictions

+ Amount,

Disclosures

purpose, and Nature and amount

type of board of donor restrictions

designations *

* New disclosure requirementExamples

Net assets:

Net assets without donor restriction:

Minimum

HFMA 2018 Spring Conference

Community Health Care $ 2,449

Noncontrolling interests 20 presentation

2,469 required

Net assets with donor restriction: 585

Total net assets $ 3,054

Net assets:

Net assets without donor restriction:

47 Community Health Care:

Undesignated $ 2,000

Designated by Board for capital prospects 449

2,449

Noncontrolling interests 20

Alternative 2,469

disaggregation Net assets with donor restriction:

allowed Time restrictions 50

Purpose restrictions 235

Endowment funds 300

585

Total net assets $ 3,054Net Assets and Related Disclosures

• Presentation of changes is similar to current guidance except that there are now two

HFMA 2018 Spring Conference

classes of net assets as opposed to three.

• Consistent with current guidance, an NFP will provide information about the nature and

amounts of donor restrictions either on the face of the financial statement or the notes.

• An NFP will now be required to disclose the amounts and purposes of board-designated

net assets either on the face of the financial statement or the notes.

48

• Underwater endowment funds will be classified within net assets with donor restrictions,

as opposed to current guidance, which requires them to be classified within unrestricted

net assets.

• Expanded from current guidance for underwater endowments, an NFP will be required

to disclose the aggregate of the original gift amounts (or level required by law or donor),

fair value, the aggregate amount of the deficiencies and any governing board policy

decision to reduce or not spend from such funds.Expenses

• Requires all NFPs to present information about their expenses by nature and function

HFMA 2018 Spring Conference

either:

- In the statement of activities,

- As a separate statement, or

- In the notes to the financial statements.

49 • NFPs required to provide qualitative disclosures about methods used to allocate costs

among program and support functions.Expenses Disclosure Example 1 – Draft

Health Care Services Support Services

Acute Ambulatory Physician Post Acute Health Plan Research MG&A Fundraising Total

HFMA 2018 Spring Conference

Salaries and benefits $ 1,742 $ 321 $ 688 $ 459 $ 229 $ 229 $ 688 $ 229 $ 4,585

Purchased services 885 163 349 233 116 116 349 116 2,329

Supplies 428 79 169 113 56 56 169 56 1,125

Depreciation and amortization 214 39 85 56 28 28 85 28 564

Capitated purchased services - - - - 246 - - - 246

Rentals and leases 57 11 23 15 8 8 23 8 151

Interest 35 7 14 9 5 5 14 5 93

Insurance 5 1 2 1 1 1 2 1 14

Other 241 44 95 64 32 32 95 32 635

50

$ 3,608 $ 665 $ 1,424 $ 950 $ 721 $ 475 $ 1,424 $ 475 $ 9,742

The financial statements report certain expense categories that are attributable to more than one health care service or

support function. Therefore, these expenses require an allocation on a reasonable basis that is consistently applied.

Costs not directly attributable to a function, including depreciation, amortization, interest and other occupancy costs, are

allocated to a function based on a square footage or units of service basis. Allocated health care services cost not

allocated on a units of service basis are otherwise allocated based on revenue.Expenses Disclosure Example 2 – Draft

Health Care Services Support Services

North Region Central Region South Region MG&A Fundraising Total

HFMA 2018 Spring Conference

Salaries and benefits $ 1,376 $ 917 $ 1,376 $ 688 $ 229 $ 4,585

Purchased services 699 466 699 349 116 2,329

Supplies 338 225 338 169 56 1,125

Depreciation and amortization 169 113 169 85 28 564

Capitated purchased services 74 49 74 37 12 246

Rentals and leases 45 30 45 23 8 151

Interest 28 19 28 14 5 93

Insurance 4 3 4 2 1 14

51

Other 191 127 191 95 32 635

$ 2,923 $ 1,948 $ 2,923 $ 1,461 $ 487 $ 9,742

The financial statements report certain expense categories that are attributable to more than one health care service or

support function. Therefore, these expenses require an allocation on a reasonable basis that is consistently applied.

Costs not directly attributable to a function, including depreciation, amortization, interest and other occupancy costs, are

allocated to a function based on a square footage or units of service basis. Allocated health care services cost not

allocated on a units of service basis are otherwise allocated based on revenue.Investment Return

• The ASU requires investment return to be reported net of external and direct internal

HFMA 2018 Spring Conference

investment expense.

• NFP’s are no longer required to disclose investment expenses that have been netted.

• An NFP will be precluded from including these investment expenses in the nature-by-

function expense analysis.

52Year 1 Presentation of Net Investment Return

Format 1: Format 2:

HFMA 2018 Spring Conference

Revenue $ X,XXX Revenue $ X,XXX

Expenses XXX Expenses XXX

Operating income XXX

Operating income XXX

Investment return, net excluding

Investment return, net XXX unrealized gains (losses) on other than

Less: trading securities excluded from

Unrealized gains (losses) on other performance indicator XXX

than trading securities excluded from

Performance indicator XXX

53 performance indicator (200)

Unrealized gains (losses) on other

Performance indicator XXX than trading securities excluded from

Add: performance indicator 200

Unrealized gains (losses) on other Change in net assets without donor

than trading securities excluded from restrictions $ XXX

performance indicator 200

Change in net assets without donor

restrictions $ XXXCash Flows and Liquidity and Availability Disclosures

• Cash Flow Statement

HFMA 2018 Spring Conference

- Allow free choice between the Direct Method and the Indirect Method

o Indirect reconciliation no longer required for Direct Method

• Liquidity and Availability Disclosures

- Qualitative information about how a NFP manages its liquid resources and liquidity risk

54

- Quantitative information about the availability of a NFP’s financial assets to meet those cash needs for

general expenditures within one year of the balance sheet dateLiquidity Example Disclosure – Draft

HFMA 2018 Spring Conference

55

The System has certain board-designated and donor-restricted assets limited to use which are available for general expenditure within one year

in the normal course of operations. Accordingly, these assets have been included in the qualitative information above. The System has other

assets limited to use for donor-restricted purposes, debt service and for the professional and general liability captive insurance program.

Additionally, certain other board-designated assets are designated for future capital expenditures and an operating reserve. These assets limited

to use, which are more fully described in Notes ___ and ___ are not available for general expenditure within the next year and are not reflected in

the amounts above. However, the board-designated amounts could be made available, if necessary.

As part of the System’s liquidity management plan, cash in excess of daily requirements are invested in in short-term investments and money

market funds. Occasionally, the Board designates a portion of any operating surplus to an operating reserve, which was $1,200,000 as of

December 31, 2016. This fund established by the board of directors may be drawn upon, if necessary, to meet unexpected liquidity needs.

Additionally, the System maintains a $5 million line of credit, as discussed in more detail in Note ___. As of December 31, 2016, $5 million

remained available on the System’s line of credit.Financial Instruments

ASU No. 2016-01 (Topic 825), Financial Instruments –

Classification and Measurement Amendments to Current GAAP

Targeted improvements, effective for CY 2019 (FY 2019-20); one year earlier for PBEs

HFMA 2018 Spring Conference

Financial Assets

• Equity investments (other than those under the equity method) measured at each

reporting period at fair value through net income, with key exception: those without

readily determinable fair value only marked to observable price changes

• No more other-than-trading equity securities

57 Financial Liabilities

• Fair value change resulting from own credit for financial liabilities measured under fair

value option will be recognized through other comprehensive income (OCI)*

Disclosures

• Entities other than public business entities (includes all NFPs) no longer required

to disclose fair value of financial instruments not recognized at fair value on

balance sheet*

*Entities can early adopt these provisionsASU No. 2016-13, Financial Instruments—Credit Losses (Topic

326): Measurement of Credit Losses on Financial Instruments

Effective for CY 2021 (FY 2021-22); one year earlier for PBEs

HFMA 2018 Spring Conference

Trade receivables and student

Contributions (pledges)

loans (and other programmatic

receivable are excluded

loans) receivable are included

58

CECL model not expected to result in significant impact on most entities

that aren’t financial institutions

• Likely already taking CECL considerations into account for their trade and loan receivables

More noteworthy is the change for Available-for-Sale Debt Securities: now

an allowance approachASU No. 2017-12, Hedge Accounting – Key Simplifications

Effective for CY 2020 (FY 2020-21); one year earlier for PBEs; early adoption allowed

HFMA 2018 Spring Conference

The concept of separately recording “ineffectiveness” will be eliminated

SIFMA rate will now be among the indexes eligible to be designated in

59

a hedge of interest rate risk

Hedge Documentation – Initial quantitative effectiveness test can now

be performed anytime before issuance of next financial statements

(instead of immediately after entering the hedge).*

*Public Healthcare NFPs (those that have issued, or are a conduit bond obligor for, securities that are traded, listed or

quoted on an exchange or an over-the-counter market) have 3 months to document hedging relationships.ASU No. 2017-12, Hedge Accounting – Key Simplifications

HFMA 2018 Spring Conference

Shortcut Method – Long-haul method may be used if use of the shortcut

method was not or no longer is appropriate.

Critical Terms Match – When hedging a group of forecasted transactions,

the timing of the derivative and transactions can be considered to “match,”

60 if the transactions occur and derivative matures within a 31-day period.

Qualitative Testing – Allowed after an initial quantitative test at hedge

inception if certain conditions are met.AFI – Hedge Documentation – Private Company Alternative

HFMA 2018 Spring Conference

Statement of intent to hedge at inception

• Hedging instrument

• Hedge item or transaction

• Nature of risk being hedged

61

Following will need to be finalized once FS are

made available for issuance

• Method of hedge effectiveness

• Qualitative or quantitative hedge effectiveness testingOther Recent ASUs 1. Restricted Cash (ASU 2016-18) 2. Net Periodic Benefit Cost Presentation (ASU 2017-07) 3. Definition of a Business and Goodwill Impairment (ASU 2017-01 and ASU 2017-04)

ASU No. 2016-18, Restricted Cash

Effective for CY 2019 (FY 2019-2020); early adoption permitted

HFMA 2018 Spring Conference

Requires the statement of cash flows to

explain the change during the period in

Does not provide a definition of restricted

the total of cash, cash equivalents,

cash or restricted cash equivalents

restricted cash, and restricted cash

equivalents

63

Requires entities to disclose the line items

and amounts of cash, cash equivalents,

Includes restricted cash and restricted

and amounts generally described as

cash equivalents in the beginning and

restricted cash or restricted cash

ending totals of the cash flow statement

equivalents reported within the statement

of financial positionASU No. 2017-07, Improving the Presentation of Net Periodic

Pension Cost and Net Periodic Postretirement Benefit Cost

Effective for CY 2019 (FY 2019-2020); early adoption permitted

HFMA 2018 Spring Conference

• Net benefit cost contains several components with different nature

• No GAAP guidance on presentation

Background • Reduced predictive value and usefulness of information to users

• Board added project

64

Presentation of net

benefit cost in the • Service cost in the same line item or items as other current

employee compensation costs

income statement • Remaining components in a separate line item or items outside

(retrospective operating items, if applicable

application)

Capitalization of only service cost in assets (prospective application)Other Recent ASUs

HFMA Spring Conference 2018

ASU No. • Provides a more robust framework to

2017-01, determine when a set of assets and Effective for CY 2019

activities is a business and more

Clarifying the consistency in applying the guidance,

(FY 2019-2020); early

adoption permitted, with

Definition of reducing application costs, and limitations

increasing operability in practice

a Business

65

ASU No. • Changes the test for goodwill

2017-04, impairment to a one-step quantitative Effective for CY 2022

impairment test whereby a goodwill (FY 2022-2023); early

Accounting impairment loss is measured as the adoption permitted

for Goodwill excess of a reporting unit’s carrying

amount over its fair value

ImpairmentRecently Issued Standards (ASU)/FASB

- ASU 2015-14 | Revenue

HFMA 2018 Spring Conference

- ASU 2015‐07 | Fair Value Hierarchy Levels for Certain Investments Measured at Net Asset Value

(Topic 820)

- ASU 2015-16 | Simplifying the Accounting for Measurement – Period Adjustments

- ASU 2015‐17 | Income Taxes (Topic 740)

66

- ASU 2016‐01 | Financial Instruments (Subtopic 825-10)

- ASU 2016-13 | Measurement of Credit Losses on Financial Instruments

- ASU 2016‐02 | Financial Leases

- ASU 2016‐14 | Not-for-Profit Entities (Topic 958)Recently Issued Standards (ASU)/FASB (Continued)

- ASU 2016-07 |Equity Method of Accounting

HFMA 2018 Spring Conference

- ASU 2016‐15 & 18 | Statement of Cash Flows (Topic 320) Classification of Certain Cash Receipts and

Cash Payments

- ASU 2017-02 |Not-for-Profit Entities Consolidation

67

- ASU 2017-04 |Goodwill Impairment

- ASU 2017-07 |Net Periodic Benefit Costs

- ASU 2017-12| Targeted Improvements to Accounting for Hedging Activities

- Proposed Grant vs. Contribution Guidance68

HFMA 2018 Spring Conference

Questions?HFMA 2018 Spring Conference

The material appearing in this presentation is for informational purposes only and should not be construed

as advice of any kind, including, without limitation, legal, accounting, or investment advice. This information

is not intended to create, and receipt does not constitute, a legal relationship, including, but nor limited to,

an accountant-client relationship. Although this information may have been prepared by professionals, it

should not be used as a substitute for professional services. If legal, accounting, investment, or other

professional advice is required, the services of a professional should be sought.

69 Assurance, tax, and consulting offered through Moss Adams LLP. Investment advisory services offered

through Moss Adams Wealth Advisors LLC. Investment banking offered through Moss Adams Capital LLC.You can also read