Job Search with Financial Information: Theory and Evidence - GSB Faculty ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Job Search with Financial Information:

Theory and Evidence

Bong-Geun Choi, Jung Ho Choi, and Sara Malik∗

November 30, 2020

Abstract

This paper examines whether, when, and why job seekers use firms’ financial in-

formation in the job search process. We find first evidence of financial information’s

relevance to job seekers by documenting a substantial increase in job search activity

around earnings announcements in the spirit of Beaver (1968). We also find that fi-

nancial information acquisition by job seekers is positively related to both job postings

and interviews at the firm-county-month level. Spurred by this finding, we develop

a theoretical model of job search paired with firms’ heterogeneous earnings to better

understand job seeker’s information acquisition behavior. Our model predicts that job

seekers trade off the probability of an offer with the value of the employment con-

tract and intensify information acquisition as the number of available positions shrinks

relative to the pool of job seekers. Consistent with these predictions, we find that

firm performance is positively correlated with both job seekers’ search activities and

employers’ posted wages. We also find that the positive association between finan-

cial information acquisition and interviews is stronger when the job market is more

competitive. Overall, these results indicate that, like capital market participants, job

seekers value and use financial reporting.

Keywords: Job Search and Match, Financial Accounting, Firm Heterogeneity.

JEL Classification Numbers: D83, J62, J64, M41, M51.

∗

We thank Maureen McNichols, Kathryn Shaw, and Sorabh Tomar, who helped us with early project

development. We thank Tarik Umar for sharing the geocoding data with us. We thank Judson Caskey, Nick

Bloom, Ron Kasznik, Gwen Yu (discussant), and participants at UCLA, Stanford University Economics

Department Reading Group, and Stanford Accounting Summer Camp. We thank Teamblind for sharing

proprietary job search data with us. We thank Andrew Chamberlain at Glassdoor for supporting our research.

We thank Rishabh Aggarwal, Austin Pennington, and Mohammadhossein Shafinia for their superb research

assistance. Sal Mancuso and the Stanford GSB Data, Analytics, and Research Computing (DARC) team

provided superb hands-on support. Wonhee Lee helped us collect the Glassdoor data. Jung Ho Choi and

Sara Malik thank Stanford Graduate School of Business for research support. Bong-Geun Choi is affiliated

with Fount Inc. Please direct all correspondence to jungho@stanford.edu.

1 Introduction

The importance of financial information to capital providers has been studied extensively in

the academic literature. However, evidence of its importance to job seekers is comparatively

absent. This is especially surprising given the increasingly important role of labor as an

input to production (Zingales, 2000; Benson et al., 2020). Job seekers often have imperfect

information about job vacancies and prospective employers’ characteristics (Autor, 2001). A

natural question is whether job seekers turn to financial information to resolve the imper-

fection. Stated more explicitly, do job seekers use a firm’s financial information in the job

search process?1 If so, when does financial information matter most? What are the primary

economic drivers for why financial information matters to job seekers? Our belief is that the

gap in the literature around these topics is attributable to limited data and an insufficiently

developed theoretical foundation about job seekers’ search behaviors. In this paper, we first

examine job seekers’ search behavior at earnings announcements and during the job search

process. Then, we propose a search theoretic model of the job market with firms’ financial

information. Finally, we test the model’s implications by constructing and exploiting a novel

database that matches job search, job posting, and interview data with financial information

search data.

Anecdotal evidence suggests that financial information is valuable in both the job appli-

cation and interview processes.2 Job seekers are known to care about a wide range of job

characteristics, including wage, monetary compensations, fringe benefits, and work arrange-

ments (Mas and Pallais, 2017). Job postings often do not provide sufficient information

about these factors. For example, wages may not be listed in a job posting and are instead

negotiated after a match is made. Moreover, job seekers also care about firm characteristics

1

Financial information is defined by information provided by financial reporting (e.g., information con-

tained in 10-K or 10-Q).

2

“This research comes in handy at three pivotal times during a job search: first when you’re deciding

what kind of employers you’d like to work for, then when you are ready to apply, and finally when you’re

interviewing and your knowledge of the company is put to the test.” - https://www.indeed.com/career-

advice/finding-a-job/the-complete-guide-to-researching-a-company.

1

that cannot be captured in an employment contract (e.g., career growth and job security)

3

. In these cases, financial information provides rich, germane evidence. Reading financial

reports helps job seekers predict prospective match quality between themselves, jobs, and

employers. It also helps in preparation for interviews and thus improves the likelihood of

being hired.4

Our first analysis is a litmus test for the relevance of financial information to job seekers.

Beaver (1968) examined whether capital market participants took action based on earnings’

perceived information content by measuring abnormal trading volume around earnings an-

nouncements. In the same spirit, we measure abnormal job search volume around earnings

announcements on a popular, online professional network for job seekers. Job search vol-

ume is a proxy for job seekers’ interest in a company. In Figure 1, we find that abnormal

job search volume consistently spikes at earnings announcements. We also find that the

magnitude of job search volume at earnings announcement is increasing in earnings growth

measured year on year. This analysis suggests that, like capital market participants, job

seekers believe earnings announcements contain pertinent information and act accordingly.

We then examine when job seekers engage in financial information search by testing for

search activity in response to both job postings and interviews. We measure job seekers’

financial information search using Internet Protocol (IP) log data from SEC Edgar. We

access large scale job posting data from Burning Glass Technologies (BGT), which collects

job postings from over 40,000 websites. We measure the interview intensity by counting the

number of interviews voluntarily reported by interviewees on the job and recruiting website,

Glassdoor. Our identification strategy exploits the geographical and time variation in job

postings, interviews, and information searches. We measure our variables at the firm-county-

month level. In other words, if, within a county, a company issues a job posting or initiates

3

See Glassdoor Job Seeker Preferences Study (2018).

4

“Researching potential employers is vital to an effective job search. ... For public companies, you can

get this information from the company as well as access certain financial information, office locations, and

learn how the company is structured. Public companies typically post annual reports and other public

financial documents online.” - https://www.indeed.com/career-advice/finding-a-job/the-complete-guide-to-

researching-a-company.

2an interview, we examine whether Edgar searches for the company’s filings increase in that

region relative to others.

We find that the number of job postings and interviews is positively correlated with

Edgar searches at the firm-county-month level, indicating that job seekers search for financial

information during both the application and interview processes. In a multivariate analysis

on job postings, the elasticity is 0.5475, meaning that a 100% increase in job postings leads

to a 54.75% increase in Edgar searches. The median of annual Edgar searches is 36, meaning

that doubling job postings leads to 19.8 additional Edgar downloads each year. As we control

for county and time variation, the magnitude halves. Our results are effectively unchanged

even after controlling for the influence of firm performance with firm fixed effects. When we

control for home bias, our estimate is 0.0156, indicating that firm-county pair might capture

regional concentration of Edgar searches attributable to both employees and investors. Using

the number of job interviews, we find the same relations qualitatively. When we control for

home bias, our estimate of the elasticity of Edgar searchers to job interviews is 0.0254. These

conservative magnitudes of the elasticity suggest that doubling job postings and interviews

are translated into 0.56 and 0.91 additional downloads per year, respectively. These numbers

are economically significant, especially given that Edgar is only one of many possible means

to acquire financial information. Our robust findings support the argument that job seekers

acquire financial information in the job search process.

To better understand why job seekers use financial information, we present a model of

labor market search. While the relation between financial information acquisition and job

search may appear intuitive upon first glance, it is predicated on complex labor market

frictions. If a worker were always compensated based on his or her marginal productivity,

employers’ financial information would not matter. Likewise, if job seekers could effortlessly

identify all vacancies and submit applications, then job seekers would apply to every job

vacancy (Stigler, 1962). Instead, these search frictions are pervasive and large. Our model is

a hybrid of the two competing approaches to theoretic models with search frictions: directed

3search and random search. The model features firm heterogeneity, i.e., different types of

firms as measured by firm performance. We allow job seekers to choose their optimal search

efforts to secure an offer. Job seekers first direct their search to a group of firms of the

same type and exert their optimal search efforts over that set. Wages are realized afterwards

when the job offers are made, which is the random search component. Compared with the

standard directed search model, in our model, job seekers direct their search to the firm types

rather than to the contracts, which is consistent with the data. Different types of firms have

different distributions for the employment value. Within the same type, the employment

value distribution is matched one to one with the wage distribution. To generate a wage

distribution within the same type firms, we allow on-the-job search within and between

types, which is also realistic.

Our model proposes two major aspects of financial information’s role in the equilibrium

match and the search effort allocation. The first key feature is that job seekers trade off the

probability of receiving a job offer with the value of that offer. In other words, job seekers

understand that if they apply to high performing firms, they are less likely to be hired

by those firms due to a high volume of applications, but conditional on being hired, their

offers are preferred.5 The second feature is that job seeker effort is increasing in competition

in the job market. In other words, if others exert more efforts, a worker should do the

same to maintain the same level of the visibility to employers. Search efforts are costly,

but they can increase the match probability by improving application quality (e.g., a well-

researched cover letter or strong interview performance). Therefore, the model predicts that

intense competition in the job market motivates the job seekers to conduct more financial

information acquisition.

We test the first proposition of the model by evaluating how and why job seekers use

this financial information in their job search process. First, we test whether a firm’s finan-

5

A job seeker applies to firms with better performance with the intention of securing a higher valued job

offer. In the equilibrium, however, a job seeker knows that other job seekers are also likely to apply to those

same firms and competition for the limited number of vacancies will be high. Therefore, the model suggests

a positive correlation between a firm’s performance and the job applications for the firm.

4cial performance is positively correlated with the job search intensity for the firm. Using

proprietary job seeker interest data from Indeed, we find that ROA and Market to Book are

positively correlated with job search intensity. We construct a summary score of each firm’s

financial performance using ROA, Sales Growth, and Market to Book under the assump-

tion that job seekers assess firm financial health use multiple pieces of information (Brown

and Matsa, 2016). We find a positive association between a firm’s summary score and job

search intensity. The coefficient of 0.0255 indicates that an increase in the score by 3 points

increases the number of job application by 7.65 percents. Using the subsample of the BGT

job postings that include posted wages, we find evidence of a positive correlation between a

firm’s financial performance and the posted wage. This result supports the argument that

one reason job seekers apply to high performing firms is the high expected compensation.

We also test the second proposition of the model: job seekers search more intensively

for financial information when the job market is more competitive. We measure job market

competitiveness with the Herfindahl–Hirschman Index where a firm’s market share is defined

by its share of the job postings in the county-month. We segment counties by labor market

concentration. Labor market concentration increases the market power of employers and

decreases the choice set of job seekers, making the job market more competitive assuming the

number of applicants is constant (Azar et al., 2018). We find that labor market concentration

increases the relation between job interviews and Edgar searches. This result supports the

argument that financial information acquisition is increasing in job market competition.

We conduct multiple cross-sectional and robustness tests to ensure that our results sup-

port our hypotheses. We examine which job seeker groups utilize financial information

in the job search process. We find that strengthening the enforcement of non-compete

clauses reduces the relation between job postings and financial information search because the

non-compete clauses limit labor mobility. Financial reports are complex and management-

focused, which implies that the information is likely more accessible and valuable to well-

educated job seekers, job seekers with experience, and job seekers with accounting or finance

5backgrounds. We find that job postings with high education requirements, longer experience

requirements, and in accounting, finance, and manager positions are more strongly corre-

lated with financial information acquisition. Our results are robust to alternative measures

of financial information acquisition: Edgar searches only from residential IPs and Google

searches.6 Finally, we find that the relation between the financial performance variables and

job search intensity is stronger for firms characterized by more Edgar searches, i.e., more fi-

nancial information acquisition. This finding is consistent with job seekers who use financial

information reacting more intensely to financial performance than job seekers who do not

use financial information.

Our paper makes three contributions. First, we provide robust evidence that job seek-

ers, like capital market participants, use financial information. A relatively small number of

papers in the accounting literature study the role of financial information to rank-and-file em-

ployees (Chakravarthy et al., 2014; Dou et al., 2016). For example, Liberty and Zimmerman

(1986) study how wage negotiations with labor unions influence earnings management.7 De-

Haan et al. (2020) study current employees using financial statements for voluntary turnover

decisions (Lester et al., 2020).8 Our paper complements these studies by demonstrating

whether, when, and why prospective employees use financial information in the job search

process. In the spirit of Ball and Brown (1968) and Beaver (1968), we emphasize the per-

6

One important identification challenge is that job postings may induce not only job seekers’ interest but

also other stakeholders’ interest in financial information. We investigate the heterogeneity of job seekers’

financial information search activities mainly to mitigate a concern that the relation between job postings

and Edgar searches captures investors’ search behaviors. Investors extensively use SEC Edgar system to

understand firms’ financial performance especially during earnings announcement periods (Drake et al.,

2015). Furthermore, high income individuals are more likely to invest in the stock market. We find that our

results are strong even during non-earnings announcement periods and in low income areas, supporting our

conjecture that job seekers download firms’ financial reporting information during their job searches.

7

For example, Kedia and Philippon (2009) document the impact of financial misreporting on employee

turnover. Hann et al. (2020) demonstrates the usefulness of aggregate earnings for explaining the labor mar-

ket. Choi et al. (2019) demonstrates that low financial reporting quality increases rank-and-file employees’

wage premiums for high turnover risk, suggesting the usage of financial information in wage determination

(Baik et al., 2019; Bai et al., 2019).

8

While employees are also an important stakeholder of financial information, they are a distinct group

from job seekers. The same financial information may not be equally relevant for both groups. For example,

job seekers may care more about growth whereas current employees are more concerned about pension

obligations.

6ceived information content of financial information that informs job seeker’s behavior.

Zingales (2000) encourages researchers to study the relation between corporate finance

decisions and human capital. Following the call, Berk et al. (2010) establishes the theoretical

foundation of how capital structure decisions influence wage determination via bankruptcy

risk. Agrawal and Matsa (2013) demonstrates that high labor unemployment risk decreases

corporate leverage due to labor market frictions, emphasizing the undiversifiable nature of

human capital. With one notable exception, however, the literature has not explored the

role of financial information in job search. Brown and Matsa (2016) find that, during fi-

nancial crisis, financial professionals apply less often to financial companies that are more

likely to file for bankruptcy due to the separation risk. In addition, those financial com-

panies tend to offer higher wages. Extending Brown and Matsa (2016), we highlight the

importance of positive financial performance for job seekers during earnings announcements

and throughout job search including both the application and the interview processes. Our

model provides a prediction about financial performance (as a signal for the employment

value) and (information) search efforts.

Finally, our model highlights information frictions around firm performance and more

fully represents the realities of the labor market. An information friction about firm char-

acteristics has been overlooked frequently in the literature (Benson et al., 2020). Although

simple directed search is a powerful framework in labor economics, it is predicated on publicly

posted wages, which are rarely available. Mixed results about the relation between posted

wage offers and job applications are puzzling (Marinescu and Wolthoff, 2020). We propose

that financial information may be another allocative mechanism. Likewise, we incorporate

a random component to model job search intensity (an important choice variable for job

seekers) and allow for on-the-job search within and between types.

Section 2 describes the institutional details about job search and financial information

acquisition. We review the literature in the section. Section 3 describes data. Sections 4

and 5 discuss job search around earnings announcements and financial information search in

7the job search process, respectively. Section 6 discusses a theoretical foundation for why job

seekers look for financial information. Sections 7 and 8 test the propositions of the model.

Section 9 concludes.

2 Institutional Setting and Literature Review

2.1 Job Search

In this section, we discuss the information frictions job seekers face during search and match

process in the labor market.9 Identifying these frictions is important to understanding why

job seekers may engage in financial information.

The search and match process starts when employers advertise a job vacancy. Job seekers

face twin information problems: identifying job vacancies and evaluating the prospective jobs

and employers. Workers could hypothetically spend infinite time and energy applying for

jobs but in reality only apply to the subset of prospective jobs and employers they find

most appealing. Job postings typically do not contain sufficient information to make that

determination, so job seekers must engage in information acquisition.10

Historically, job seekers would read help-wanted advertisements in newspapers to identify

vacancies. The development of the internet in the 1990s and 2000s changed the dynamics

of job search substantially. Now, millions of vacancies are summarized in centralized online

job boards. For example, as the leading job board in early 2000s, Monster.Com offered 3.9

million resumes and 430,000 jobs in August 2000 (Autor, 2001). These online job boards are

heavily utilized by job seekers. Current Population Survey (CPS) estimates suggest that by

2011 approximately 75% of job seekers used online job search compared to approximately

25% in 2000. Likewise, the internet made information about employers more accessible

(Gao and Huang, 2020). Firm financial reports are now readily available through company

9

Firms also have their own information frictions when trying to evaluate prospective employees’ produc-

tivity. We omit those for brevity.

10

In fact, most job postings do not include details about compensation.

8websites and the SEC’s Edgar system.

The development of these platforms has not eliminated the information frictions faced

by job seekers. In fact, in some cases they have exacerbated them. Instead of reading a few

newspaper broadsheets’ worth of vacancies, job seekers have access to millions of vacancies.

This has increased the challenge of identifying the subset to which job seekers want to apply.

More importantly, the platforms provide an opportunity to trace previously unobservable

jobseeker behavior during the job search process.11

After applying to vacancies advertised by employees, job seekers may be contacted by

firms for an interview. Firms use interviews to acquire more information about prospective

employees and for screening (Barach and Horton, 2021). Job seekers can use interviews to

highlight their fit for the vacancy and evaluate the company (Judge et al., 2000). Many job

seekers spend time preparing for their interviews by researching the prospective employer

and networking with current employees. They may also engage in financial information

acquisition. If the company decides the job seeker is a good match, it will extend an offer

to the job seeker. Wage negotiation may follow. Once the offer is accepted, the job search

process is complete.

2.2 Literature Review

A recent literature uses the development of technologies and intermediaries to expand our

understanding of the labor market. Kuhn and Mansour (2014) document that unemployed

workers who use the internet during their job search have shorter joblessness durations.

Baker and Fradkin (2017) find that an increase in unemployment benefits is associated

with a decrease in job search activity in the Google search box, likely because it reduces

the incentive to find a new job. A few recent papers study the importance of employers’

11

Internet platforms have also firms’ information acquisition costs about prospective employees. Informa-

tion about workers’ characteristics can be divided into two categories: low and high ”bandwidth” variables

(Autor, 2001). Low bandwidth data are objectively verifiable information such as education and experience.

In recent years, multiple intermediaries including LinkedIn provide this verifiable information about potential

workers at a lower cost by publicly posting resumes of its members.

9reliance on new institutions. Benson et al. (2020) finds that firms’ reputation about payment

history has an impact on freelancers’ application behaviors in the gig economy. Using a field

experiment and the crash of the review board as a research setting, the authors find that

firms’ reliable payment history allows them to get more applications at a lower wage on

Amazon Mechanical Turk.

The implementation of the Edgar system also provides a new opportunity to study fi-

nancial information acquisition (Drake et al., 2015). For example, Bernard et al. (2020)

demonstrate that competing companies search for other companies’ financial reports. This

bilateral search behavior is associated with the similarity in investment decisions. Drake et al.

(2017) find that Edgar searches vary across counties. High search volumes are associated

with income and education levels.

3 Data

In this section, we describe the data sets used in our analysis: job posting data, job in-

terview data, financial information acquisition data, and job search intensity data. These

data sets have many strengths, chiefly among them is broad and deep coverage. This is a

significant departure from prior literature’s reliance on surveys. In addition to these data

sets, we also use the well-known merged quarterly Compustat-CRSP data set to evaluate

firm performance.12

3.1 Job Posting Data and Job Interview Data

We use large scale data from Burning Glass Technologies (“BGT”), an analytics software

company, to identify job vacancies. Every day, BGT scans more than 40,000 sources, in-

cluding job boards and corporate websites, to create a catalogue of new job postings. The

company then uses its natural-language processing software to identify the job title, occu-

12

We winsorize the Compustat-CRSP variables at the 1st and 99th percentile of all Compustat-CRSP

firms to minimize the influence of outliers.

10pation, employer, and skills for each vacancy. Each observation in the BGT data represents

a job posting. In total, BGT provides 52 standardized fields for each observation. These

standardized fields allow for improved comparability of job postings across region and time.

The BGT data set spans 2007 and 2010 to present and covers all 50 states. As part of our

data processing, we aggregate the data to the firm-county-month level and count the number

of job postings. BGT classifies job listings into 24 occupation family codes. For each firm-

county-month tuple, we also count the number of job postings in each distinct occupation

code. Our Appendix indicates that our sample firms post vacancies across various occupation

families, including sales, management, and health care.13

We use proprietary data from Glassdoor, an online job and recruiting website, to collect

a record of job interviews. Each record is interviewee-specific and includes the interview

date, firm name, interview location (city and state), an indicator for whether the interviewee

received an offer, and an indicator whether the interviewee accepted or declined an offer.

These records are self-reported by the interviewees and are not corroborated by the individual

firms.

3.2 Financial Information Search Data

We use the SEC’s publicly available server log files to identify financial information acqui-

sition. The server log files measure traffic for Edgar filings through SEC.gov. Each record

contains the accessor’s semi-anonymized IP address, the date of access, the firm CIK num-

ber, and the searched document. We geo-locate each user by using the MaxMind data and

are therefore able to include each accessors’ city and state for each record. The data are

aggregated to firm-county-month level, summing the number of searches. We exclude CIK-

IP-date tuples with a large number of searches to eliminate records conducted by bots and

crawlers (Ryans, 2018).

13

Prior literature in economics has compared the BGT data to other commonly used data sources on job

vacancies (Hershbein and Kahn, 2018). Relative to the survey data collected by the U.S. government, the

BGT data represent the near universe of job postings. The data set generally over-represents technical fields,

which are more likely to be posted on websites, but the over-representation does not change over time.

11We acknowledge that job seekers may access firms’ financial information through different

conduits, including companies’ homepages, search engines, and Yahoo finance. We find that

some firms link to the SEC Edgar filings on their websites. Thus, job seekers are likely to

acquire firms’ financial information from the Edgar system without explicitly noticing it.

One salient example is Alphabet, Inc.’s investor page. When one clicks on the link to a

10-K, it directs the viewer to the filing hosted on the SEC’s website. Additionally, when

users search for firms’ annual reports on Google, financial reports in the Edgar system are

frequently ranked in the top five to ten Google search results.

To directly tackle this alternative source of financial information, we supplement the

SEC’s publicly available server log files with Google Trends data. Google Trends data

measure the number of searches in the Google search bar across different regions and across

time.14 We collect Google Trends data from 2011 to 2016 for firms in the S&P500 as of 2019.

Google search is a popular way to look for companies’ financial information, but the Trends

data may also represent search for purposes other than employment.

3.3 Job Search Intensity Data

We collect proprietary data from Indeed, an online job and recruiting website, to measure job

search intensity. For a large subset of the firms on its website, Indeed creates two separate

daily indices: one for job postings intensity and one for job search intensity. The job search

intensity from Indeed is measured in the same way as Google Trends data. Indeed tracts

users search activities on the search bar on its website. For example, if more users search

for Amazon within Indeed, Indeed data indicate higher job search intensity for Amazon.

Consequently, these indices are relative measures. We aggregate the data to the firm-quarter

level and take the average of the indices. One advantage of this data set is that it tracks

behaviors of individuals who are very likely to be job seekers.

14

Google Trends data are randomly sampled statistics. The measure is noisy, which may lead to slightly

different search volumes when downloading the same series. We believe this noise is uncorrelated with our

test and will not introduce bias. It may, however, reduce our statistical power.

12We also obtain proprietary data from Teamblind, an online professional social network

with job boards and anonymous forums, as a second measure job search intensity. The data

covers a smaller number of firms but is high-frequency and captures anonymized individuals’

job search queries. The sample period is from September 2019 to September 2020. For

each company-day, we count the number of unique (anonymized) users who search for the

company’s name.

4 Job Search and Earnings Announcements

4.1 Research Design

To provide initial evidence of firm financial information’s relevance to job seekers, we measure

firm-specific abnormal job search volume at quarterly earnings announcements. This analysis

is in the spirit of Beaver (1968) and Landsman and Maydew (2002). We use earnings

announcement dates from IBES and daily search volume from Teamblind. Abnormal job

search volume is measured using a z-statistic; we compute firm-specific means and standard

deviations of search volume over all days exclusive of the +/- 10 day range around each

earnings announcement.

4.2 Empirical Results

In Figure 1, we plot abnormal job search volume from -20 days to 20 days around earn-

ings announcement dates.15 We find that abnormal job search volume spikes at earnings

announcements. The daily fluctuations around earnings announcements are minimal. This

figure is consistent with job seekers using earnings announcements to learn about potential

employer’s financial performance and then directing their search activity to said employ-

ers. The magnitude of the job market reaction in Figure 1, 0.4, is strikingly similar to the

15

The number of unique companies in Figure 1 is about 50. Due to confidentiality issues, we cannot

provide the exact number.

13magnitude of the capital market reaction (also 0.4), in Figure 1 in Landsman and Maydew

(2002).

One alternative explanation for our figure is that job seeker interest increases at earnings

announcements because firms are featured in the news. To clarify the relative strengths of

these explanations, we compute year-on-year earnings growth and group earnings announce-

ments into above median earnings growth and below median earnings growth announcements.

Our contention is that both high earnings growth and low earnings growth firms are likely

be to be featured in the news. We then reproduce our plot separately for each group in

Figure 1 Panels B and C. We make two observations. First, the spike in abnormal job search

volume at earnings is larger in the above median earnings growth group compared to the

below median group. This result is comparable to Beaver et al. (2018)’s finding that the

capital market reaction to profitable firms is substantially larger than that for loss firms.

This analysis is distinct from Brown and Matsa (2016) because our study focuses on the in-

formation content of financial reports and the importance of positive financial performance.

Second, search volume is generally higher after earnings announcements in the above median

earnings group compared to the below median group. This suggests job seekers react to earn-

ings announcements’ information content even after earnings announcements. Collectively,

our results indicate that, like capital market participants, job seekers act on the perceived

information content of earnings announcements.

5 Job Postings, Interviews, and Financial Information

5.1 Research Design

We estimate the relation between job postings (interviews) and financial information acqui-

sition using the data set created by merging Edgar log data with BGT job postings and

14Glassdoor job interviews data. The specification is:

EdgarSearchesjst = β · JobP ostings(Interviews)jst + γ · Xjst + αj + µs + τt + jst (1)

where j indexes company, s indexes county, and t indexes month. Our first variable of interest

is JobP ostingsjst , which is the log of one plus the number of job postings in a firm-county-

month tuple. Our second variable of interest is Interviewsjst , which is the log of one plus

the number of job interviews in a firm-county-month tuple. We measure EdgarSearchesjst

as the log of one plus the number of Edgar Searches, also in a firm-county-month tuple.

Note that in order to avoid dropping observations without Edgar searches, job postings, or

interviews, we add one to the raw value before taking the log. Our control variables include

ROA, the sum of the last four quarters of operating income after depreciation divided by

total assets lagged five quarters; Sales Growth, the previous quarter’s sales minus sales lagged

five quarters, divided by sales lagged five quarters; Market to Book, the previous quarter’s

market cap divided by previous quarter’s common equity; Size, the log of the previous

quarter’s total assets; Leverage, the previous quarter’s current and long term debt divided

by previous quarter’s total assets; and Labor Productivity, the sum of the previous four

quarters’ sales divided by the most recent employee count, subsequently logged. In addition

to the fixed effects indicated in Equation 1, we also run this specification with varied, more

dense fixed effects. Standard errors are clustered at the firm level.

5.2 Job Postings and Financial Information

Table 1 Panel A summarizes descriptive statistics. The number of firm-county-month obser-

vations is 0.4 million. After matching firms in the BGT job posting data set with firms in

the Edgar financial information download data set, we identify approximately 2,400 unique

common firms. The median number of non-logged Edgar searches at the firm-county-month

level is 3. The 75th percentile is 14. The median number of non-logged job postings at

15the firm-county-month level is 2 because we exclude a firm-county-month pair without job

postings.16 We focus on three performance measures in the paper: ROA, Sales Growth, and

Market to Book. The median of ROA is 9.8%. The median of total assets is $8,752M.

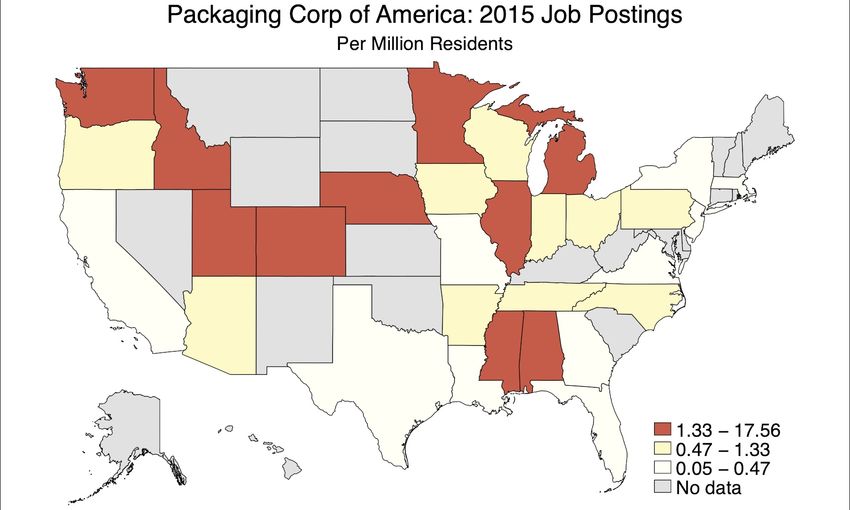

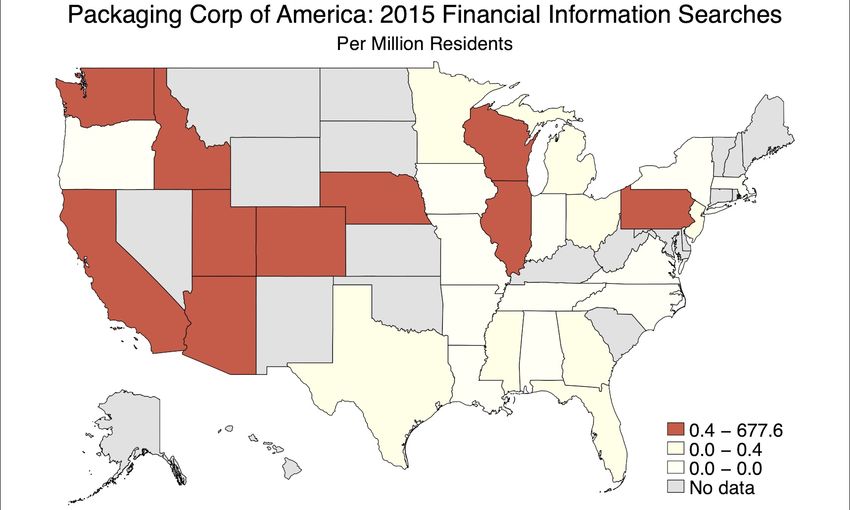

Figure 2 is a set of heat maps of job postings, interviews, and Edgar searches for the

firm Packaging Corporation of America (“PCA”). PCA is one of the largest producers of

containerboard and packaging material in the U.S. It is headquartered in Illinois and has

establishments across the country, including in California, Texas, and Maryland. The figure

shows that PCA issues job postings in the states in which its plant, mills, and customer

service centers are located and those states are characterized by more Edgar searches for

PCA’s financial information. PCA also conducts interviews in the states where it has a

presence, including Illinois and Texas. Figure 3 illustrates the time-series variation in job

postings and Edgar searches for PCA. The figure indicates that the number of job postings

changes over time. We exploit both cross-sectional and time-series variation in job postings

and interviews to study the relation between job postings and Edgar searches.

In Table 1 Panel B, we find that Edgar searches are positively correlated with job post-

ings. The correlation is 0.2896, which is the highest relative to the other financial variables

in our table. Job postings are also positively and highly correlated with size and profitabil-

ity (ROA). Overall, a univariate analysis supports our hypothesis that job seekers gather

financial information about potential employers.

Table 2 Panel A echoes our univariate analysis. We start with controls but without fixed

effects to ensure that both across and within firm and across and within county variation

support our arguments. The elasticity is 0.5475, meaning that a 100% increase in job post-

ings leads to a 54.75% increase in Edgar searches. To mitigate concerns over macroeconomic

and geographic factors, we use time and county fixed effects. For example, economic recov-

ery might increase both Edgar searches and job postings. In addition, counties may have

16

In Online Appendix Table A.2, we re-estimate this equation on a data set that includes firm-county-

month pair without job postings if the firm-county pair has at least one job posting over the entire sample

period.

16a large number of both investors and employees. We also use firm fixed effects because

large firms have more investors and employees. These fixed effects reduce the coefficient on

JobP ostingsjst but the coefficient is still statistically and economically significant. Finally,

excluding observations in a firm’s headquarters county does not change the main implication

of our paper. It is worth mentioning that the role of the financial performance variables in

Table 2 is to serve as controls. Prior papers indicate that financial performance is associ-

ated with investors’ attention. Later, we use firms’ financial performance as an independent

variable to study the relation between job search intensity and financial performance.

Table 2 Panel B shows that our results are robust to alternative fixed effects. To address

alternative explanations, we introduce the interacted fixed effects. We first use firm-month

fixed effects. Firms with high sales growth might drive job postings and investors attentions

at the same time. In this specification, we capture the association between Edgar searches

and job postings within a firm-month pair but across different counties to mitigate concern

that firm performance is driving our results. We then use county-firm and county-month

fixed effects additionally. Investors are more likely to invest in firms near them. Firms are

also more likely to hire local job seekers. The county-firm interacted fixed effect captures

this home bias. In Column (3), the coefficient of JobP ostings is 0.0156, indicating that

firm-county pair might capture regional concentration of Edgar searches due to employees

as well as investors. Across the different specifications, we continually find the positive and

significant relation between job postings and Edgar searches, supporting the argument that

job seekers acquire financial information during job applications.

5.3 Job Interviews and Financial Information

Table 3 Panel A echoes our findings with job postings. We start with controls but without

fixed effects to ensure that both across and within firm and across and within county variation

support our arguments. The elasticity is 1.7935, meaning that a 100% increase in job postings

leads to a 179.35% increase in Edgar searches. As the same in Table 2, we use time and county

17fixed effects and exclude observations in a firm’s headquarters county. These specifications

reduce the coefficient but the coefficient is still statistically and economically significant.

Table 3 Panel B shows that our results are robust to alternative fixed effects. Especially, in

Column (3), the coefficient of Interviews is 0.0254 even after controlling for both firm-month

and county-firm fixed effects.

The economic magnitude of the coefficients in Column (3) of Table 2 and 3 is still mean-

ingful. The median of the number of non-logged Edgar searches is 3. The number is not large

because we measure Edgar searches at the firm-county-month level and we exclude Edgar

searches by bots and crawlers. Doubling job postings and interviews translate into additional

0.0468 and 0.0762 Edgar searches.17 Annually, doubling job postings and interviews within

a firm-county increases Edgar searches from 36 to 36.56 and from 36 to 36.91, respectively.

Acknowledging that job seekers are one of multiple user groups of Edgar searches and Edgar

search is only one of multiple methods to search for financial information by job seekers, one

additional Edgar search is economically significant. In addition, we separately measure job

seekers’ financial information search in the application process and the interview process.

Finally, the coefficient captures the average effect. We study the heterogeneous effect of job

postings on financial information searches in Table 8.

6 Theoretical Foundation

We present a model of labor market search where unemployed workers can direct their search

on a firm type (e.g., productivity or performance) but not on a specific wage contract. Wage

offers are randomly drawn from the firm type specific wage distribution. Moreover, we allow

on the job search at exogenous match rates as in Burdett and Mortensen (1998). This

feature allows us to have non-degenerate wage distributions between homogeneous workers

and homogeneous firms. Also, motivated by our empirical results on job seekers’ financial

17

Doubling job postings and interviews is consistent with the standard deviation of EdgarSearches in

Table 1 and twice the standard deviation of Interviews only with the sample with non-zero interviews.

18information acquisition, we model optimal choice of search efforts in each submarket. Search

efforts are costly, but they can increase the effectiveness of search, thus increasing the match

probability.

In the steady state, our model suggests that more productive firms tend to offer higher

value contracts and attract more job applications. Consequently, more productive firms are

more competitive to match. From the perspectives of a job seeker, the merit of a higher value

contract is offset by a lower chance of receiving an offer. Moreover, more intense competition

to match with a productive firm leads to more intense job search efforts (including financial

information acquisition).

The model implies a positive relation between the firm’s productivity type (or perfor-

mance) and the value of employment, a positive relation between the firm’s productivity

type and the job search efforts, and a positive relation between the firm’s productivity type

and the number of job applications.

6.1 Model Environment

We study the steady state implications of a continuous time economy. There exits a unit

measure of continuum of workers. Workers are identical and are infinitely lived. The economy

is populated with firms, potentially of a larger mass than one. However, each firm can hire

only one worker, and the measure of participating firms in the labor market is endogenously

determined by the free entry condition. We assume that firms and workers are risk neutral,

and they discount the value of future time at an instantaneous rate r > 0.

Firms are heterogeneous in terms of their own performance yi ∈ {yH , yL } where i ∈

{H, L} is the productivity index of a firm so that yH ≥ yL . We denote the measure of

type i firms recruiting in the labor market (i.e., vacant for a job) as mi and the measure of

workers employed by a type i firm as ni . Once a type i firm is filled for a job with a worker,

the firm-worker pair produces output yi . Each pair faces an exogenous separation at rate

δi ∈ {δH , δL }, with δH ≥ δL . We denote the measure of unemployed workers seeking a job at

19a type i firm as ui . Employed workers receive different wages w, and unemployed workers

receive unemployment benefits b, with 0 ≤ b < yL ≤ yH , while firms with a vacancy should

bear job posting cost k to recruit. All unemployed workers participate in the labor market

(i.e., either employed or unemployed), so nH + nL + uH + uL = 1.

We make a few key assumptions on the search and match process as follows. First, the

market is segmented due to directed search as in Moen (1997) and Acemoglu and Shimer

(1999). However, in our model, the segmentation and the directed search are based on a

firm’s type instead of a contract. Knowing the equilibrium wage offer value distribution, the

job separation rate, the future on the job search prospects, and the competitiveness of the

job market involved with each type of the firms, workers direct their search over the firm

type. Therefore, the submarket for the segmentation is defined by the type of the firms.

Once workers choose which type of the firms to direct in their search, they should compete

with other workers pursuing a job in the same submarket.

Second, we allow on the job search as in Burdett and Mortensen (1998) and Hoffmann

and Shi (2016). Knowing the matching chance and the offer value distribution in each

submarket, firms with job vacancies offer optimal wages to maximize their profits. A higher

valued offer is more likely to be accepted and more likely to retain a worker. The optimal

value offer decisions made by the firms form a nondegenerate wage offer distribution, which

can be also interpreted as a mixed strategy. If a firm of type i posts a vacancy, then it

should compete with the same type vacant firms to attract job applications by offering a

different wage. In each submarket, unemployed workers have a queue to be matched with a

firm. The key departure from Burdett and Mortensen (1998) or Hoffmann and Shi (2016) is

that an unemployed worker who directs his search to type i firms receives a wage offer at an

endogenously determined arrival rate which will be explained later. Moreover, an employed

worker at an i type firm receives an offer at an exogenous arrival rate λ from the same type

firms as the current employer and at an exogenous arrival rate σ from the other type of the

firms.

20Third, we consider costly search efforts by the workers as in Decreuse and Zylberberg

(2011). However, in our model, directed search and the search effort allocation are about the

firm’s type and conducted before the workers receive a wage offer. Moreover, once the workers

direct their search to a type of the firms, they cannot further direct their searches on a specific

contract. We denote the function that maps each submarket to search effort by s : {H, L} →

R+ , where si ∈ {sH , sL } is the search efforts level exerted by other unemployed workers in

each submarket i. In a symmetric equilibrium, job search efforts s = si are involved with

the search cost function c (·) as well as the search effectiveness function x (·). Both of them

are increasing functions of s. Marginal cost of search increases in the search efforts, and

marginal effectiveness of search decreases in s. We assume that the matching technology of

the economy M (·, ·) is an increasing CRS function of its arguments. Then the effectiveness

of search of an unemployed worker with search intensity s at submarket i is expressed by

M [x(s)ui ,mi ]

an endogenous rate of αi (s; si ) := x(si )ui

, given the measures of the vacancies and

unemployed job seekers as well as other job seekers’ search intensity at submarket i , si .

Assumption 1.

• The search effort cost function c : [0, +∞) → [0, +∞) is strictly increasing, strictly

convex, and twice differentiable.

• The search effort cost function satisfies c (0) = 0, and c0 (+∞) = +∞.

• The search effort effectiveness function x : [0, +∞) → [0, +∞) is strictly increas-

ing, strictly concave, and twice differentiable.

• The search effort effectiveness function satisfies x (0) = 0 and x0 (0) = +∞, and

x0 (+∞) = 0.

• An unemployed worker pursuing a job at a type i firm may meet a type i vacancy

at an endogenous arrival rate αi (s; si ), which increases in the worker’s own search

efforts s given si , ui and mi .

21• An employed worker at a type i firm may meet the same type firms with a vacancy

at an exogenous arrival rate λi .

• An employed worker at a type i firm may meet the other type firms with a vacancy

at an exogenous arrival rate σi .

From Assumption 1, we know that a type i firm with a vacancy may meet an unemployed

M [x(si )ui ,mi ]

worker pursuing a job at a type i firm at an endogenous arrival rate mi

. An employed

worker receives an offer from a same type employer at an exogenous arrival rate λi , and an

employed worker at the other type of a firm at an exogenous arrival rate σi . A type i firm

with a filled job may separate from the worker with an exogenous probability δi , in which

case the workers become unemployed and the firms lose their workers for an unmodeled

reason. In addition, a type i firm with a filled job may lose its worker when the employee

was matched by a vacant firm offering a higher value with a higher wage.

6.2 Worker

Wage w is the source of utility value for the workers. We denote the life time utility value

of being an unemployed worker by Vu and the utility value of unemployment seeking a job

at a type i firm by Vu,i , respectively. Workers may receive only one offer at a time. The

utility value of employment at a type i firm with wage w by Ve,i (w), respectively. We denote

the support of the life time utility value distribution for employed workers at type i firms as

Fi as suppi ≡ V i , V i . We also denote the supports of wage that corresponds to suppi as

b

[wi , wi ]. Then we know that V i ≥ Vu and Vu ≥ r

because any wage should provide better

utility value than unemployment, and employed workers hope to receive wage offers better

than the unemployment benefit.

Assumption 2.

• A type i firm which has been idling with a vacancy strategically offer a wage of

value V ∼ Fi (V ) to attract a worker to match where Fi (V ) is an endogenous

22mixed strategy equilibrium value of the offer by a type i firm.

• Employment value for type i firms with a filled job form a cumulative distribution

function Gi (V ).

• Fi and Gi are differentiable in the interior of their supports.

• V H ≥ V L but no restriction on the comparison between V H and V L .

The value function for unemployed workers is rVu = max {rVu,H , rVu,L } so that

b + max αH (s˜H ; sH ) 0∞ max {0, z − Vu,H } dFH (z) − c (s˜H ) ,

R

s˜H

rVu = max , (T 1)

b + max αL (s˜L ; sL ) ∞ max {0, z − Vu,L } dFL (z) − c (s˜L )

R

s˜L 0

for given {sH , sL }. The value function for employed workers at type i ∈ {h, l} firm with

wage w ∈ R+ is

w + δi [Vu − Ve,i (w)]

R∞

rVe,i (w) = +λi max {0, z − Ve,i (w)} dFi (z) . (T 2)

0

R∞

+σi

0

max {0, z − Ve,i (w)} dF−i (z)

6.3 Firm

A firm with a vacancy seeking a worker should pay instantaneous vacancy cost k ≥ 0.

Acknowledging the distribution of offer value V from type and the employment value dis-

tribution of employed workers, Gi , on suppi ≡ V i , V i , firms can form a rational expec-

tation about the offer acceptance rate for an offer of value V ∈ suppi from a type i firm:

hi (V ) ≡ αi xi ui + λi ni Gi (V ) + σ−i n−i G−i (V ) for any V ≥ Vu . For a type i firm offering

hi (V )

V ∈ suppi , the vacancy filling rate is mi

: αimxiiui from an unemployed worker, λi ni

mi

Gi (V )

σ−i n−i

from an employed worker at a same type firm, mi

G−i (V ): from an employed worker at

a different type firm. Then it must be that h0i (V ) > 0 for all V ∈ suppi . The instantaneous

profit of a type i operating firm offering wage wi (V ) of value V is yi − wi (V ), the effective

23discount rate of a type i operating firm offering value V is r + qi (V ) where qi (V ) is the

effective separation rate from a job from type i firm with value V . Then the present value

yi −wi (V )

of the profit stream for a type i operating firm offering V to its employee is r+qi (V )

. Using

this, the expected flow profit of job posting for a type i vacant firm offering V and paying

posting cost k is,

yi − wi (V ) hi (V )

π̂i (V ) = −k (T 3)

r + qi (V ) mi

where for V ∈ V H , V H ,

λH [1 − FH (V )] + σH [1 − FL (V )] + δH

if V ∈ V H , V L

qH (V ) =

λH [1 − FH (V )] + δH

if V ∈ V L , V H

and for V ∈ V L , V L ,

λL [1 − FL (V )] + σL [2 − FH (V )] + δL

if V ∈ [V L , V H )

qL (V ) = .

λL [1 − FL (V )] + σL [1 − FH (V )] + δL

if V ∈ V H , V L

We denote the maximized expected profit of job posting for a type i vacant firm offer-

ing any V ∈ suppi as πi , i.e., π̂i (V ) = πi for i ∈ {H, L} and V ∈ suppi . Note that the free

entry condition by offering V requires that πi = 0 for i ∈ {H, L}.

6.4 Symmetric Steady State Equilibrium

Steady state requires outf low = inf low for each V = Vi (w) ∈ V L , V H in the CDF’s, Fi

18

and Gi , for i ∈ {H, L}. We define the symmetric steady state equilibrium as follows .

Definition 1. {ui , si , ni , Gi (V ) , mi , Fi (V ) , πi , Vu,i , Wi (V )}i∈{H,L},V ∈[V ]

i ,V i

18

The derivation of the symmetric steady state equilibrium condition is shown in the Online Appendix.

241. Value function of unemployed workers

rVu = max {rVu,H , rVu,L }

where

" #

Z VH

rVu,H = b + αH (sH ; sH ) V H − Vu,H + {1 − FH (x)} dx − c (SH )

VH

Z VL

rVu,L = b + αL (sL ; sL ) {1 − FL (x)} dx − c (sL )

VL

µ(xi (s)ui ,mi )

with αi (s; si ) = xi (si )ui

and the assumptions

(a) Given other unemployed workers’ search efforts si for i ∈ {H, L}, the optimal

search intensity of an unemployed worker is si for i ∈ {H, L}

(b) V L = Vu and V H ≥ V L .

2. Workers are indifferent to submarkets:

Vu,H = Vu,L = Vu .

3. Value function of employed workers at H type firm offering wage w ∈ [wH , wH ]

(a) If VH (w) ∈ V H , V L :

Z VH

rVH (w) = w + λH {1 − FH (x)} dx

VH (w)

Z VL

+ σH {1 − FL (x)} dx + δH (Vu − VH (w))

VH (w)

25

(b) If VH (w) ∈ V L , V H :

Z VH

rVH (w) = w + λH {1 − FH (x)} dx + δH (Vu − VH (w))

VH (w)

4. Value function of employed workers atL type firm offering wage w ∈ [wL , wL ]

(a) If VL (w) ∈ [V L , V H ):

Z VL

rVL (w) = w + λL {1 − FL (x)} dx

VL (w)

" #

Z VH

+ σL V H − VL (w) + {1 − FH (x)} dx + δL (Vu − VL (w))

VL (w)

(b) If VL (w) ∈ V H , V L :

Z VL

rVL (w) = w + λL {1 − FL (x)} dx

VL (w)

Z VH

+ σL {1 − FH (x)} dx + δL (Vu − VL (w))

VL (w)

5. Equal profit condition within each type19 :

yi − wi (V ) hi (V )

π̂i (V ) = − k = πi

r + qi (V ) mi

for i ∈ {H, L} and V ∈ suppi

6. Free entry for each type of firms: equal profit condition between firm types20 :

πi = 0

for i ∈ {H, L}.

19

This condition is used to find the offer and employed workers’ value distributions, for any given (mH , mL ).

20

This condition is used to solve mH and mL .

26You can also read