LIBOR TRANSITION: THE STATE OF PLAY - April 14, 2020 Noon, US Eastern Daylight time - Oliver Wyman

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

LIBOR TRANSITION: THE STATE OF PLAY April 14, 2020 Noon, US Eastern Daylight time

DAN

ROSENBAUM

Partner, Retail and

Business Banking

OPENING

Dan.Rosenbaum@oliverwyman.com

REMARKS

LIBOR TRANSITION – THE STATE OF PLAY

AGENDA

Opening Remarks Dan Rosenbaum

1 State of the Transition with Guest Speakers Tom Wipf

and David Bowman

Tom Wipf

David Bowman

2 Regulatory Imperative and Transition Timeline Douglas Elliott

3 Lending with SOFR Esther Bruegger

4 Getting to Green through the Crisis Adam Schneider

5 Closing Remarks Dan Rosenbaum

Copyright © Oliver Wyman 3

OUR HOSTS

Dan Rosenbaum Madeline Kreher

Partner, Retail and Engagement Manager, LIBOR

Business Banking Platform

Dan.Rosenbaum@oliverwyman.com Madeline.Kreher@oliverwyman.com

OUR PANELISTS

Tom Wipf

Esther Bruegger

Vice Chairman of Morgan Stanley

Principal, Finance & Risk

and Chair of the ARRC Esther.Bruegger@oliverwyman.com

Thomas.Wipf@morganstanley.com

David Bowman

Senior Associate Director at the

Adam Schneider

Board of Governors of the

Partner, Lead LIBOR Platform

Federal Reserve Adam.Schneider@oliverwyman.com

David.H.Bowman@frb.gov

Doug Elliott Pin Su

Partner, Risk & Public Policy Engagement Manager, LIBOR

Douglas.Elliott@oliverwyman.com Platform

Pin.Su@oliverwyman.com

Copyright © Oliver Wyman 4

1 TOM WIPF

Vice Chairman of Morgan

Stanley and Chair of

the Alternative Reference

Rates Committee

STATE

OF THE

DAVID BOWMAN

Senior Associate Director at

TRANSITION

the Board of Governors of

the Federal Reserve

Alternative Reference Rates Committee

Update

Tom Wipf, Vice Chairman of institutional securities at Morgan Stanley and Chair of the

Alternative Reference Rates Committee

David Bowman, Senior Associate Director, Board of Governors of the Federal Reserve

Copyright © Oliver Wyman 6

ALTERNATIVE REFERENCE RATES COMMITTEE

The Federal Reserve convened the ARRC in 2014 to identify

a robust alternative to U.S. dollar LIBOR that met best

practices and to promote the use of that rate and robust ARRC Members

fallback language on a voluntary basis. American Bankers Association International Swaps and Derivatives Association

Association for Financial Professionals JPMorgan Chase

AXA KKR

Bank of America LCH

Following the remarks by Andrew Bailey at the UK’s BlackRock MetLife

Financial Conduct Authority (FCA) indicating that the Citigroup Morgan Stanley

CME Group National Association of Corporate Treasurers

continued production of LIBOR is not guaranteed beyond Comerica Pacific Investment Management Company

2021, the ARRC (2.0) was reconstituted in 2018 with an CRE Finance Council PNC

expanded membership to help to: Deutsche Bank Prudential Financial

Fannie Mae Structured Finance Association

Ford Motor Company TD Bank

Freddie Mac The Federal Home Loan Banks

1. Ensure the successful implementation of the Paced GE Capital The Independent Community Bankers of America

Transition Plan, Goldman Sachs The Loan Syndications and Trading Association

Government Finance Officers Association The Securities Industry and Financial Markets Association

2. Address the increased risk that LIBOR may not exist HSBC Wells Fargo

beyond 2021, and Huntington World Bank Group

Intercontinental Exchange

3. Serve as a forum to coordinate and track planning

across cash and derivatives products and market.

Ex Officio Members

Commodity Futures Trading Commission New York Department of Financial Services

In order to fulfill this mandate, the ARRC continues to Consumer Financial Protection Bureau Office of Financial Research

Federal Deposit Insurance Corporation Office of the Comptroller of the Currency

conduct the widest possible outreach, seeking input and Federal Housing Finance Agency U.S. Department of Housing and Urban Development

comments from all parties that may be affected by the Federal Reserve Bank of New York U.S. Securities and Exchange Commission

possible cessation of LIBOR after 2021. Federal Reserve Board U.S. Treasury

National Association of Insurance Commissioners

Copyright © Oliver Wyman 7

LIBOR TRANSITION TIMELINES AND COVID Statement by the UK Financial Conduct Authority (March 25) “The central assumption that firms cannot rely on LIBOR being published after the end of 2021 has not changed and should remain the target date for all firms to meet. The transition from LIBOR remains an essential task that will strengthen the global financial system. Many preparations for transition will be able to continue. There has, however, been an impact on the timing of some aspects of the transition programmes of many firms. “ https://www.fca.org.uk/news/statements/impact-coronavirus-firms-libor-transition-plans Statement by the Financial Stability Board (April 2) Benchmark transition. The transition from LIBOR remains a priority as firms cannot rely on LIBOR being produced after end 2021. Benchmark transition will help to strengthen the global financial system. https://www.fsb.org/work-of-the-fsb/addressing-financial-stability-risks-of-covid-19/ The ARRC is taking the timelines provided by the official sector as given and continuing its work, recognizing that although some near-term goals may be delayed, other efforts can continue Copyright © Oliver Wyman 8

ALTERNATIVE REFERENCE RATES COMMITTEE – TIMELINE

The ARRC was originally convened in November 2014. Significant progress has been made to

date.

May – CME launched SOFR futures

Jul. – LCH cleared SOFR Nov./Dec – U.S. Authorities

OIS and basis swaps issue accounting, tax, and

Apr. – FRBNY/OFR began margin relief proposals Create a SOFR term

Fannie Mae issued first

publishing SOFR reference rate

SOFR-based FRN Q3 – ISDA Protocol

Oct. – ARRC Paced Transition

Plan adopted Apr/May – ARRC issues FRB, Oct –LCH/CME

Loan, and Secruitization Mar. – FRBNY move to SOFR

fallback recommendations began publishing PAI/diiscounting

and Users Guide to SOFR SOFR averages

2016 2017 2018 2019 2020 2021

Mar. – ARRC’s Second report Jul. – ARRC’s issues Apr - ARRC’

May – ARRC published SOFR ARM Whitepaper recommended

Interim Report and Spread Adjustment Q4. – GSEs to stop

Consultation ARRC 2.0 reconstituted with Oct. – CME begins clearing announced LIBOR ARMs and

expanded membership Sep – ARRC issues start SOFR ARMS

Jun. – SOFR selected as SOFR swaps using SOFR

Implementation

recommended PAI/discounting and FASB

Checklist

alternative to USD LIBOR adds SOFR to its hedge

accounting list Nov. – ARRC’s issues ARM

Jul. – FCA Bailey: Official sector fallback recommendations

can no longer guarantee and agrees to pursue NY

LIBOR’s stability past 2021 legislative relief

Copyright © Oliver Wyman 9

ARRC WORKSTREAMS • Best Practices: date-based best practices for use of hardwired fallback language, vendor readiness, setting out successor rates for contracts that allow discretion, and ending use of LIBOR, • Conventions: final recommended conventions for SOFR-based floating rate notes, business loans, securitizations, and student loans • Fallback Language: revisions to the ARRC’s hardwired business loans fallback language (including a more permissive early opt-in trigger) and finalize recommended fallback language for new student loans referencing LIBOR • Legislative Relief: pursue potential legislative relief for legacy contracts that may be otherwise difficult to amend and that do not have economically appropriate fallbacks • Operations/Infrastructure: internal systems, work with external vendors • Reference materials: materials laying out actions that market participants could take in order to create clear and effective programs for consumer education and outreach as well as materials to educate market participants on tax/accounting relief. • Single Step: Move to SOFR PAI and discounting for cleared derivatives (October 2020). • Spread Adjustments: finalizing technical details and establishing an RFP process for selection of an administrator to publish the ARRC’s recommended spread adjustments and spread-adjusted rates. • Tax/Regulation/Accounting: continuing work with tax, regulatory, and self-regulatory organizations as they finalize proposals for transition relief • Term Rate: Establishing RFP process to select an administrator of an ARRC-recommended forward-looking term SOFR rate to be published in 2021 if liquidity in SOFR derivatives markets has developed sufficiently, and establish recommended scopes of use for the rate Copyright © Oliver Wyman 10

SOFR MARKETS • SOFR Futures trading has started at a faster pace than either Eurodollar Futures or Fed Funds Futures. Average daily volume is over $100 billion notional, with open interest surpassing $2 trillion • SOFR swaps trading FR in cash markets. SOFR OIS and basis swap trading has begun to pick up, but averages in the range of $30 billion per month. SOFR basis trades had a record month in March at CME. We have also seen recent SOFR cross- currency swap and options trading. • The floating rate debt market has been the first to take up SOFR, with over $500 billion in SOFR debt having been issued, with a record $150 billion issued in March • Fannie and Freddie are now developing the capability to accept SOFR ARMs based on this work and will stop accepting LIBOR ARMs. • We’ve seen several recent SOFR loans, and Ginnie Mae and Freddie Mac have issued securitization with payments based on SOFR. Copyright © Oliver Wyman 11

MOVEMENTS IN SOFR

Averages of Treasury repo rates move quite closely with the fed funds effective rate and the Fed’s

monetary policy targets and are relatively unaffected by any volatility in daily SOFR rates.

SOFR has moved down with the reduction in monetary policy targets to the zero lower bound, and

is currently about 1 basis point, a few basis points lower than EFFR. Market expectations are for

SOFR rates to move up to EFFR rates.

Repo Rates Like SOFR Move Closely with Other Risk-Free Rates

7%

6%

5% Quarterly Compound SOFR/PD Survey

4% Quarterly Compound EFFR

3%

2%

1%

0%

1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Copyright © Oliver Wyman 12MOVEMENTS IN RISK-FREE RATES VS LIBOR

There are differences between LIBOR and risk-free rates like EFFR and SOFR, but it is important to

keep in mind that over the long run, LIBOR has actually moved up and down with monetary policy,

as do risk-free rates. These changes in monetary policy expectations account for 99% in the

movements in LIBOR over the last 30 years. And, from a borrower perspective, the times that

LIBOR has risen relative to risk-free rates may not actually be an attractive feature.

Over the Long Run, LIBOR and Risk-Free Rates Move 3-Month LIBOR-OIS Spread

Percent Basis Points

Closely Together 400

12 350

10 3-Month EFFR term 300

OIS rate 250

8 3-Month Libor

200

6 150

4 100

50

2

0

0 -50

1988 1992 1996 2000 2004 2008 2012 2016 2020 1988 1992 1996 2000 2004 2008 2012 2016 2020

Copyright © Oliver Wyman 13SOFR AND BANK FUNDING COSTS

Because banks are now far less dependent on wholesale unsecured funding, their holdings of

Treasuries and repo funding is now a larger proportion of their liabilities. Compound Averages of

Treasury repo rates were more correlated with bank funding costs than LIBOR, even over the

period covering the 2007-09 financial crisis.

Recently, wholesale unsecured funding volumes have dropped (the Federal Reserve has not

published its financial CP series since March 27, while low-cost core deposits and funding from

Federal Reserve facilities have increased notably, helping to lower overall funding cost even as

LIBOR has been rising.

Share of LIBOR Funding in Bank Correlations with Bank Funding Costs, 2006Q3-2011Q2

Correlation with Compound SOFR in

1

Liabilities

0.9

12.00%

0.8

10.00% 0.7

Advance

8.00% 0.6

6.00% 0.5

0.4

4.00%

0.3

2.00%

0.2

0.00% 0.1

0

-0.2 0 0.2 0.4 0.6 0.8 1

gsib_libor_share nongsib_libor_share Correlation with LIBOR

Copyright © Oliver Wyman 14

14Legacy Products and Fallback Language Copyright © Oliver Wyman 15

CASH PRODUCTS

The largest exposures to USD LIBOR (95 percent) are through derivatives, which are used to dealing

with overnight rates.

However, cash products have $8.4 trillion in exposure and large banks will have myriad connections

to these products and in many ways they will be more problematic since they do not tend to have

uniform documentation and do not have access to a protocol process to amend legacy instruments

as derivatives do.

Securitizations,

Exchange-Traded $1.8 trillion

Derivatives, $45 trillion

Syndicated Loans,

$1.5 trillion

Cash Products, Floating Rate Notes,

$8.4 trillion $1.8 trillion

Nonsyndicated CRE Loans,

Over-the-Counter Derivatives, $1.1 trillion

$146 trillion Nonsyndicated Business Loans,

$810 billion

Retail mortgages,

$1.2 trillion

Other Consumer loans,$63 billion

Copyright © Oliver Wyman 16ISDA PROTOCOL: CONVERTING LEGACY DERIVATIVES CONTRACTS

ISDA will amend its 2016 definitions to incorporate more robust IBOR fallbacks by the end of this year. It will offer

a protocol allowing legacy contracts to incorporate the new definitions at the same time.

ISDA concluded its first market consultation (of ISDA members and non-members) in October, 2018.

o This initial consultation was for Sterling, Swiss Franc, Yen LIBOR and Yen TIBOR and the BBSW rate.

ISDA concluded a supplemental consultation on USD LIBOR, CDOR, HIBOR and SOR in July 2019.

o Responses to the supplemental consultation were consistent with the first

ISDA has now finished consulting on final parameterizations. Responses to the two consultations showed a

cleared preference for:

Fallback Rate: Spread Methodology

Compounding Setting in Arrears Rate – the RFR Historical Mean/ Median Approach –

observed over the relevant IBOR tenor and Spreads would revert to a 5-year median of

compounded daily during that period the spread between the relevant IBOR and

RFR

Pre-Cessation Trigger: The OSSG has encouraged ISDA to include a trigger in the event that LIBOR has been

found to be non-representative

by the UK Financial Conduct Authority (the regulator of IBA LIBOR). CME and LCH have indicated that they will

trigger in these circumstances. ISDA has consulted on this issue but has not made any decision.

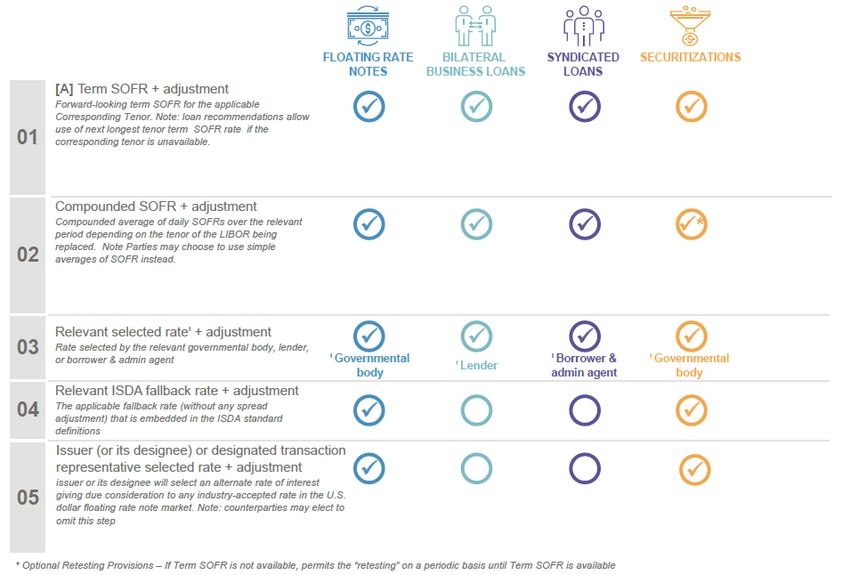

Copyright © Oliver Wyman 17ARRC HARDWIRED FALLBACK RECOMMENDED RATES WATERFALLS Copyright © Oliver Wyman 18

THE ARRC’S RECOMMENDED SPREAD ADJUSTMENT

The ARRC has recommended a spread adjustment based on a static, 5-yearar median of the

historical spread between LIBOR and SOFR, the same as ISDA’s choice for derivatives, with the

addition of a 1-year transition period for consumer products. A static spread adjustment appears

to work well, even in comparison to potential “dynamic” spread adjustments.

Table 1: Historical Errors Between Returns on a LIBOR Loan and Spread-Adjusted Rates Percent Illustration of a Transition Period to a Long-Run

1.10

Median

Mean Absolute

Loan with 1-year remaining maturity Error

Static Spread Based on 5-Year Median Spread to SOFR In 1-Year

Advance 0.10

0.80 LIBOR -…

Dynamic Spread Using 1-Month Financial CP Series 0.11

Mean Absolute

Loan with 5-years remaining maturity Error

0.50

Static Spread Based on 5-Year Median Spread to SOFR In

Long-Run Median

Advance 0.08

Dynamic Spread Using 1-Month Financial CP Series 0.11 Transition Period

Data sources: FRBNY, Federal Reserve Board, Refinitiv, and Federal Reserve Board staff calculations. 0.20

Annualized differences in returns (in percentage points) in a loan based on 1-month LIBOR and a loan

2014 2015 2016 2017 2018 2019

based on a spread-adjusted rate. Mean Absolute Errors calculated over 1999-2019 and reported in

Source: Ice Benchmarks Administration, Refinitv, and Federal Reserve Board staff calcu

percentage points.

Copyright © Oliver Wyman 19ARRC PROPOSED NEW YORK STATE LEGISLATION FOR LEGACY

CONTRACTS

Key Components Possible Legislation Structure

• Mandatory: If the legacy contract is silent as to fallbacks.

“Mandatory” v. “Permissive” • Mandatory: If the legacy language falls back to a Libor-based rate (such as last-quoted Libor).

Application of the Statute • Permissive: If the legacy language gives a party the right to exercise discretion or judgment regarding the fallback, that

party can decide whether to avail itself of the statutory safe-harbor.

• Override: Where the legacy language falls back to a Libor-based rate (such as last quoted Libor).

• Override: If the legacy language includes a fallback to polling for Libor or other interbank funding rate, the statute would

mandate that the polling not occur.

Degree of Override of Legacy

• No Override: Where the legacy language is silent as to fallbacks or gives a party the right to exercise judgment or

Contract Fallback Provisions

discretion regarding the fallback. In these instances, there is nothing to override.

• No Override: The statute would not override legacy language that falls back to an express non-Libor based rate (such as

Prime).

• Parties would be permitted to mutually opt-out of the application of the statute, in writing, at any time before or after the

Mutual “Opt-Out”

occurrence of the Trigger Event.

• The statute would become applicable or available (as described in “Mandatory” v. “Permissive” above) upon the

occurrence of statutory trigger events

Trigger Events • Cash Products: The statutory trigger events for cash products would be based on the ARRC permanent cessation

and pre-cessation trigger events

• Derivatives: The statutory trigger events for derivatives would be based on what ISDA does

“All Products” • No Exclusions: No product would be categorically excluded from the statute. Parties can opt-out as described above.

• The statute would be drafted to provide safe-harbor protection for parties who add conforming changes to their

Conforming Changes

documents to accommodate administrative/operational adjustments for the statutory endorsed benchmark rate.

Copyright © Oliver Wyman 20ARRC – STAY INFORMED • https://www.newyorkfed.org/arrc • Sign up for email updates • Office Hours Dial-In Information: –Fridays at 2:00 PM EST –1-855-377-2663 (U.S. callers) –+1 972-885-3168 (International callers) –Code: 09823427 Copyright © Oliver Wyman 21

ARRC – GET INVOLVED

ARRC 2.0

Derivatives Cash Products Support

Market

Floating Rate Consumer Infrastructure/ Tax and Regulatory

Structure/Pace Term Rate Business Loans Securitizations Legal

Notes Products Operations Accounting Issues

d Transition

SIFMA/ISDA

Official Sector

CCPS and SEFs

Copyright © Oliver Wyman 222

REGULATORY

Doug Elliott

IMPERATIVE Partner, Risk & Public Policy

Douglas.Elliott@oliverwyman.com

AND

TRANSITION

TIMELINE1 Why are the authorities forcing a change? 2 Who are the key authorities? 3 Will LIBOR really go away? 4 Will it happen on the original schedule? 5 What key decisions are still to be made by authorities? 6 How is the transition coordinated globally?

3

ESTHER

BRUEGGER

Principal

Esther.Bruegger@oliverwyman.com

LENDING

WITH SOFR1 What is the background on lending with SOFR?

2 What are the regulatory concerns with respect to loans?

3 What are the considerations in repricing loans “fairly”?

What are the concerns for new SOFR-based products? How will

4 clients react?

Do we really need to analyze this, or just let “the market”

5 decide?

6 The Fed’s Main Street Lending is using SOFR?LENDING WITH SOFR

LIBOR and SOFR in crisis scenarios

Repricing existing LIBOR products

Designing new products referencing SOFR

• Clients’ needs and SOFR product design

• Pricing of SOFR products

Copyright © Oliver Wyman 27LENDING WITH SOFR

LIBOR and SOFR in crisis scenarios

Repricing existing LIBOR positions to SOFR

Designing new products referencing SOFR

• Clients’ needs and SOFR product design

• Pricing of SOFR products

Copyright © Oliver Wyman 28LIBOR AND SOFR PRODUCTS ARE EXPECTED TO PERFORM

DIFFERENTLY THROUGH ECONOMIC CYCLES

Interest rates 1M LIBOR – 1M Compounded SOFR Spreads

January 1, 2019 – April 1, 2020 April 1, 2018 – April 1, 2020

3% 1.00%

0.75%

2%

0.50%

1%

0.25%

0% 0.00%

Jan 2020 Feb 2020 Mar 2020 Apr 2020

Apr-18

Jan-19

Apr-19

Jan-20

Apr-20

Jul-18

Jul-19

Oct-18

Oct-19

1M USD LIBOR 1M comp. SOFR in arrears

-0.25%

SOFR AMERIBOR

Note: 1M compounded SOFR in arrears are filled in using forward rates starting March 1, 2020.

Source: Bloomberg, Inc.

Copyright © Oliver Wyman 29IN A CRISIS SCENARIO (SUCH AS 2020), THE HISTORICAL SPREAD

IS NOT ADEQUATE FOR LOANS TO BE VALUE NEUTRAL

SOFR portfolio likely to yield less revenue in crisis over a year

Margin over LIBOR

Bps 0 50 100 200 500

Additional margin, i.e., spread

adjustment, for SOFR loans

0 -43% -25% -18% -11% -5%

5-yr historical

10 -29% -17% -12% -8% -4% 1M LIBOR to

1M comp.

25 -8% -4% -3% -2% -1% SOFR spread

50 28% 16% 11% 7% 3%

Notes:

Interest revenue percentage differences calculated for a loan portfolio referencing 1M LIBOR and a loan portfolio referencing 1M

compounded SOFR in arrears. Loan resets are equally distributed across business days of a month. Historical rates used up to April 1,

2020, forward rates used thereafter. Data from Bloomberg, Inc.

Copyright © Oliver Wyman 30LENDING WITH SOFR

LIBOR and SOFR in crisis scenarios

Repricing existing LIBOR products to SOFR

Designing new products referencing SOFR

• Clients needs and SOFR product design

• Pricing of SOFR products

Copyright © Oliver Wyman 31REGULATORY CONCERNS FOR TRANSITION FOCUS ON “FAIRNESS”

CREATING A NEED TO ANALYZE IMPACT ON CLIENTS

Regulatory concerns How would you reprice this “reasonably”?

• 3M LIBOR +125 bps loan

– Issued in 2019, matures in June 2022

An overarching concern …

• Different scenarios have different value neutral margins

will be whether firms have

• Adjustment to margin for SOFR as the replacement rate

taken reasonable steps to treat

customers fairly. Market Crisis with Strong recovery

implied rates delayed recovery in 2021

LIBOR discontinuation should

not be used to move customers

with continuing contracts to

replacement rates that are

expected to be higher than +30 bps +45 bps +38 bps

what LIBOR would have been, • ARRC recommended cash product spread will likely

or … introduce inferior terms. differ from value neutral spread (today 25 bps)

FCA, Conduct risk during LIBOR • Clients will compare to what is offered “on the run,”

transition, November 19, 2019 regardless of historically-based adjustments

• Which will you use?

Copyright © Oliver Wyman Calculated using LIBORITHMICS™, Oliver Wyman’s analytics tool, 4/7/2020. 32LENDING WITH SOFR

LIBOR and SOFR in crisis scenarios

Repricing existing LIBOR products

Designing new products referencing SOFR

• Clients’ needs and SOFR product design

• Pricing of SOFR products

Copyright © Oliver Wyman 33DESIGNING NEW SOFR PRODUCTS REQUIRES BALANCING A BANK’S

OBJECTIVES WITH CONSTRAINTS AND CUSTOMER PREFERENCES

Bank objectives Client preferences

• Maintain client trust • Product to work with operational

• Address client needs effectively constraints

• Transparent product features

• Achieve business targets

and behavior

• Manage risks of new products

• Product compatible with hedges

prudently

as needed

• Offer competitive pricing

• Fair and competitive pricing

and services

Copyright © Oliver Wyman 34SOFR POSES NEW CHALLENGES IN HOW IT IS USED AS A REFERENCE

RATE AND HOW SOFR PRODUCTS CAN MEET CLIENT PREFERENCES

Loan pricing features

Example customization to client preferences

Client needs and preferences

Product Fixed Floating

Precise Cash flow

cash flow uncertainty Reference

Select other rates SOFR

certainty acceptable rate

Simple

Complexity Term Comp. in Comp. in

Low Use of rate average in

SOFR advance arrears

complexity acceptable advance

New FTP and In reference

Based on

Spread historical data

bottom-up to existing

calculation LIBOR product

Rate stability Hedge

relevant compatibility

important Option None Floors Caps Other

features

Copyright © Oliver Wyman 35CLIENT ACCEPTANCE COULD BE LOW EVEN FOR SPREADS SIMILAR

TO THOSE IMPLIED BY INDUSTRY CONSULTATIONS

Market implied rates Crisis with delayed recovery Strong recovery in 2021

3% 3% 3%

2% 2% 2%

1% 1% 1%

0% 0% 0%

Oct 2020

Oct 2021

Apr 2020

Jul 2020

Jan 2021

Apr 2021

Jul 2021

Oct 2020

Oct 2021

Oct 2020

Oct 2021

Apr 2020

Jul 2020

Jan 2021

Apr 2021

Jul 2021

Apr 2020

Jul 2020

Jan 2021

Apr 2021

Jul 2021

5-year historical 5-year historical 5-year historical

median spread

27 bps median spread

32 bps median spread

30 bps

Spot spread Spot spread Spot spread

during transition

~19 bps during transition

~13 bps during transition

~35 bps

Client acceptance ? Client acceptance ??? Client acceptance Yes

3M USD LIBOR 3M Comp. SOFR in arrears

Copyright © Oliver Wyman 36BROADENING PRODUCT FEATURES CAN PROVIDE AN EDGE IN

CHALLENGING CLIENT OR COMPETITIVE ENVIRONMENTS

LIBOR Interest rate Cash flow and

transition scenario discounting

capabilities capabilities

analytics

Contract 1 Contract 2 Contract 3 Contract 4

Contract

features Loan $10 MM Loan $10 MM Loan $10 MM Loan $10 MM

Maturity 4/14/25 Maturity 4/14/25 Maturity 4/14/25 Maturity 4/14/25

that are

Base rate 3M LIBOR Base rate 90D SOFR IA Base rate 90D SOFR IA Base rate 90D SOFR IA

value Margin 125 bps Margin 162 bps Margin 153 bps Margin 125 bps

equivalent Floor No floor Floor No floor Floor 2.50 % Floor 2.95 %

Contract example analyzed using LIBORITHMICS™, Oliver Wyman’s LIBOR transition analytics tool,

interest rate simulations in collaboration with ARPM

Copyright © Oliver Wyman 37KEY TAKEAWAYS FOR SOFR PRODUCT DESIGN AND PRICING

1 Banks will develop numerous new products

referencing SOFR and other rates to address

client needs across segments

ARRC recommended spread adjustment may

2 not be perceived acceptable by clients for

cash products

Analytics are needed to study scenarios and

3 get product pricing right

Copyright © Oliver Wyman 38GET READY: THE FED’S MAIN STREET LENDING PROGRAM

MANDATES SOFR (DID YOU EXPECT LIBOR?)

• Overview (as of April 13; program details are not final)

–The Fed is setting up 2 lending facilities for small/mid-size businesses: Expanded Loan

Facility & New Loan Facility

–The loans are carried on bank books

–The Fed’s Special Purpose Vehicle (SPV) will purchase 95% participation when eligible

–The SPV will be operational ASAP and cease by 9/30/2020. Maximum size $600 Billion

• Loan term extract:

–4 year maturity

–Deferred amortization of principal and interest for 1 year

–SOFR + 250-400 bps (“which” SOFR not specified)

Is this good for your balance sheet – or not?

Can you use SOFR in your systems and analytics?

Do you know how to compare this to a similar set of LIBOR loans?

Copyright © Oliver Wyman 394

GETTING ADAM

TO GREEN SCHNEIDER

Partner, LIBOR Co-Lead

THROUGH

Adam.Schneider@oliverwyman.com

THE CRISISTHE ROUTE TO GETTING TO GREEN

LIBOR TRANSITION

The route to green requires a careful coordination of activities across:

• Lines of businesses, corporate functions and geographies, Initiate Models & Risk Management

• Infrastructure and operations, Clients & Contracts Infrastructure & Operations

• Legal, risk and finance, Products Manage Financial Implications

• and importantly: Clients and relationship management Path to Green

Top of house

financial Funding and

assessment hedging strategy Update FTP

Product New Product Selling non-LIBOR Stop selling LIBOR

Inventory Design products products

Selling Executive

Successful

LIBOR empowerment Approaching

Transition

products and budget GREEN

GREEN

Exposure Assessment Revised models

Mobilize Work- Contract Legal Fallback Legal Client Fallback

program planning Inventory Review Readiness Review Communications Processing

Client General Renegotiation Revised Vendor & Internal

Inventory Communications Terms Remediation

Technology Inventory Define Technology Engage Potential Stopgaps

requirements Remediation Plan vendors

Since LIBOR was “everywhere” and usage usually not managed, enormous work is needed to

remove it from the financial system.

Copyright © Oliver Wyman 41WHERE ARE YOU NOW?

What does “green” look like as of April 2020?

1

Exposure assessment complete – scope of LIBOR in the firm is known

Assess exposure

Exposures are produced regularly (quarterly? monthly?)

2

LIBOR Transition Office (LTO) fully organized and resourced

Program and

…Although reasonable if resources are re-deployed for COVID for time being

governance

Business and function workstreams mobilized – who is on point well defined

Fallback inventory well underway or complete

Transitioning

Strategies developed for fallback treatment

3

back book

Plans for communications to clients being developed for 2021 implementation

New exposures use robust fallback language

Developing

LIBOR product issuance has an “end” e.g. we will stop by xx/xx/xx

new products

New ARR products and pricing under development

4

Completed risk assessment and identified impacted models

Risk & models

Redevelopment schedule exists, timeline to complete mid-2021 (CCAR 12/31/20)

5

Comprehensive view of impacted tech & ops and required capabilities

Systems

Complete plan developed; updates underway; begun implementing priority systems

6 Manage financial Scenarios defined, detailed top of house financial assessment underway

implications

Copyright © Oliver Wyman

Evaluating implications on funding, hedging, FTP

42APRIL 2020: RECOMMENDATIONS FOR GETTING TO GREEN

Firms that are behind should be strategic in where and how they focus efforts

• Industry is defining key outcomes across products, with 2020 dates

G2G – 1 unlikely to move

Ensure workplans link to

• LTO must integrate industry deadlines to specifics of firm exposures and

industry timelines

then do business work plans so as to keep progressing

• LIBOR cessation date still in force; underlying submissions very low

G2G – 2

• Shift in focus near-term is reasonable; but do not let the urgent

Maintain focus despite overwhelm the important

real-world urgencies

• Continue engagement with committees/execs

• LTO as the nerve center via “Smart PMO” practices

G2G – 3

• Ensure clear ownership of activities across the firm

LTO continues to orchestrate

• LTO empowered to monitor timelines and “jawbone” progress

G2G – 4 • Maintain progress in areas with long lead-times

Be prepared for a Fall 2020

• Ensure program can “surge”; define areas and resources required

“surge”

Copyright © Oliver Wyman 43G2G 1: ENSURE WORKPLANS LINK TO INDUSTRY TIMELINES

2019 2020 2021

Capability Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

Fannie Mae and Freddie Mac

NY FED publishes ARRC recommended spread SOFR swaptions LIBOR

Key industry assumptions €STR published

SOFR averages for cash products

ceased purchasing long-dated

LIBOR-based ARMs

actively traded discontinued

CCP SOFR discounting

Discontinuation of

Tax, regulatory, and FHLBanks cease to enter long-dated

LIBOR-lending in Pick-up in SOFR FRNs Create a SOFR term reference rate

accounting rule relief LIBOR-based instrument

SONIA averages Sterling markets

ARRC publishes proposal for

Effectiveness of the amendments to the Pick-up in SOFR ARM and

NY State legislation to reduce the

2006 ISDA definitions and protocol bilateral commercial loan origination

legal uncertainty of the transition

Operational Contingency time

1. Assess Exposure Assess LIBOR Exposure readiness, testing and

remediation

2. Mobilize the LTO Mobilize workstream

3a. Identify fallbacks and determine Extract fallbacks Insert new fallback language in LIBOR contracts

transition approach Determine transition approach

3b. Develop new ARR products Design ARR products & pricing Launch ARR products

3c. Manage client communications Define bank-wide comm. strategy Continuous update Fallbacks updated/negotiated/processed

4. Assess risk and update models Update and validate models referencing LIBOR1

Assess risks Create mitigating actions Monitor risk

5. Update systems Prioritize and fund Implement capabilities to process ARR products1

technology and

vendor needs Collect fallback data and build processing capabilities1

6. Manage the financial implications Determine scenarios and top of house financial impact New product pricing and analytics

Develop funding and hedging strategy Update FTP

1. Non-discrete, varies by product/LoB

Today Industry-driven events Potential Industry driven events

External-facing milestones (clients, Internal-facing milestones

Copyright © Oliver Wyman regulators) 44G2G 2: MAINTAIN FOCUS DESPITE REAL-WORLD URGENCIES

Illustrative portfolio composition

• Follow industry deadlines (ex: CCP) with active fallback management

• Maintain focus on systems upgrades Percentage by reference rate

and vendors 100%

• Categorize fallbacks and build out

what you need for transition 80%

• Push on new product development

60%

1 LIBOR: Legacy fallbacks 40%

2 LIBOR: New, robust fallbacks

20%

3 New ARR products

0%

Q1 2020 Q3 2020 Q1 2021 Q3 2021 Q1 2022

Copyright © Oliver Wyman 45G2G 3: LTO CONTINUES TO ORCHESTRATE

Adopt “Smart PMO” practices in the LTO to act as the transition nerve center

Key roles and responsibilities

01 Inject structure and discipline 02 Ensure innovative and

across workstreams best-in-class solutioning

01 02

• Drive program management activities • Challenge workstreams to think

centrally and within workstreams creatively

• Provide tools and set standards • Identify dependencies and ensure

for workstreams cross-functional collaboration

• Manage investment budgets Imperative • Assure adherence to design

and implementation planning of the LTO principles during rollout; review

05 03 design issues

05 Provide content support 03 Accelerate delivery

• Provide advisory support for • Introduce approaches to accelerate

workstream leads 04 workstream completion

• Drive decision-oriented, content- • Build momentum through

driven discussions among quick wins

stakeholders 04 Build out transition advocates

• Establish a strong set of senior change

leaders

• Build a cohort of transition advocates

across the firm

Copyright © Oliver Wyman 46G2G 4: BE PREPARED FOR A FALL 2020 “SURGE”

Build Out Technology Get Fallbacks in Order Keep Communicating

• Understand new • Source and digitize • Communicate to keep

system requirements contracts to identify employees and clients

LIBOR exposure informed about LIBOR

• Collaborate with

developments

internal IT team and • Review contract

engage vendors language and define • Keep communicating to

remediation treatment management about

• Prioritize systems likely

buckets nature of work to

to be impacted first

happen under tight

• Implement improved

timelines

fallback language

Aggressively rework and challenge plans, forward-identify resource needs,

prepare to obtain in-house or external resources, build training.

Copyright © Oliver Wyman 47BUT WAIT – WHAT IF THE DEADLINE REALLY DOES MOVE?

Naturally COVID-19 is impacting many bank programs, including LIBOR. While

authorities continue to press for LIBOR ending after 2021, how should you

respond IF transition is delayed…

Market: Continue Alternative Reference Rate (ARR) market development

Additional ARR liquidity is sorely needed. Focus on issuance of existing products,

continuing current programs (e.g. ending LIBOR mortgages) and CCP discounting.

Progress on new fallbacks

Implement good fallbacks for new issuances and the ISDA protocol for derivatives;

save yourself conversion time later.

Finalize SOFR for lending — or not – “fish or cut bait”

Understand the need for another rate, validate against recent market experience,

finalize thinking.

Use the extension wisely

There are two standout activities: Upgrade systems to support the new rates and

manage LIBOR fallbacks. Continue both.

If the program pauses: Inventory and organize to simplify restarting

Most firms’ LIBOR transition programs already have substantial work underway –

invaluable to have this organized and archived so as to support a quick restart.

Copyright © Oliver Wyman 485

DAN

ROSENBAUM

Partner, Financial Services

CLOSING

Dan.Rosenbaum@oliverwyman.com

REMARKSOW IS DEDICATED TO SUPPORTING OUR CLIENTS THROUGH THE TRANSITION Deep understanding of the issues and solutions • We are helping shape the transition as active members of both the U.S.’s ARRC and the U.K.’s Sterling Working Group • We have published many POVs on how firms can best prepare for the transition Pulse on industry priorities and developments • We are in regular dialogue with over 100 institutions (including banks, asset managers, infrastructure providers, insurers, and corporates) and have direct access to key regulatory authorities Real-world transition expertise • We have a coordinated global team working together seamlessly to support clients • Our LIBOR toolkit allows firms to accelerate mobilization and transition LINK to OW LIBOR Transition HUB: https://www.oliverwyman.com/our-expertise/hubs/libor.html Copyright © Oliver Wyman 50

You can also read