LIVING ON WITH A COVID19 HUM - Global Economic Outlook September 2020 - Euler Hermes

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

LIVING ON WITH A COVID19 HUM Allianz Research Global Economic Outlook September 2020 © Copyright Allianz

WHAT CHANGED, WHAT’S NEXT (1/2)

What was in line with What surprised What to expect next (2021 and

expectations beyond)

Covid-19 Renewed infection waves requiring Slow rise in cases in intensive care which Stop-and-go approach from governments.

sanitary tighter sanitary restrictions and could suggest that future waves could be Vaccine available in Sept 2021, but 6 months

restrictions targeted lockdowns. more contained. needed for campaign. Return to normal in 2022.

Economic Less open economies, less reliant on Stronger than expected catch-up effects for Divergence in pace of recovery due to (i) structure

activity services and benefitting from short- retail sales, residential market and exports of (manufacturing economies likely to benefit more the

term demand stimulus packages have goods. recovery); (ii) composition of stimulus packages

registered stronger acceleration (demand/supply) + speed of disbursements; (iii)

confidence effects.

Global Low consumer confidence amid rising Rapidly improving business confidence in Busy political calendar (US elections and Brexit

confidence and concerns on unemployment and contrast with still weak fundamentals. outcome in 2020, Germany and the Netherlands

political risk financial, keeping excess savings at a Political uncertainty increased in UK as in 2021, France in 2022) will shape future fiscal

high level. probability of Hard Brexit now 45%. stimuli. Expectations: last minute (partial) agreement

on Brexit. Joe Biden victory. More redistributive

policies towards households.

Investment No acceleration in investment in the Confidence in the manufacturing sector K shape recovery in investment to

cycle manufacturing sector as long as: (i) the improved strongly during summer on the prevail. Investments, notably in the manufacturing

sanitary crisis is not (close) to be back of above-expectations catch-up effects. sector, to accelerate more visibly in H2 2021 as

solved and (ii) uncertainty on demand Recovery in residential investment was confidence effects improve and stimulus packages

remains high. stronger than expected. materialize.

Global Trade, Services lagging behind goods in Stronger than expected recovery in goods No full de-globalization: some reshoring but mostly

protectionism, recovery. US-China trade tensions trade during the summer (currently 3% diversification (multi-shoring). Goods back to pre-

globalization contained, but cold "tech" war to below last August) crisis level in 2022, services in 2023.

© Copyright Allianz 2

continue.

WHAT CHANGED, WHAT’S NEXT (2/2)

What was in line with What surprised What to expect next (2021 and

expectations beyond)

Global prices Disinflationary pressures confirmed due to Record high levels in gold price during +0.3% inflation in 2020 in EZ and +1.1% in the

temp. factors (tax cuts, delayed summer summer suggest increased worries US; progressive reflation in 2021 (+0.9% and

sales), negative output gaps + falling money about stagflation. Markets are actually +1.6% respectively). Expect >2% US inflation

velocity. ambivalent about the long-term inflation from 2022. Higher inflationary pressures in EM

outlook (fixed income pricing starting end-2021. Oil prices up at 51 bbl/USD

stagflation). 2021.

Monetary Global liquidity reached record high levels Fed introduced new monetary policy Fed QE tapering in late 2022. No rate hike by

policy during summer, but transmission is not target=> comfortable with temporary Fed before Q3 2023. ECB is likely to announce

efficient given the lack of confidence of the inflation overshoot; no normalization EUR500bn in QE in Dec. 2020. BoE likely to

private sector before unemployment reaches 4 to 5% increase QE size by GBP100bn in 2021.

Fiscal policy Large phase II fiscal stimulus packages have Some countries continued to lag in Size + spending calendar of stimulus matter for

been announced, notably in Europe, along terms of size of stimulus (Spain, Italy, countries. Focusing on supply = more time

with the reduction in relief measures UK). Higher risks of a fiscal cliff in the before reaching pre-crisis levels.

US. Fiscal consolidation efforts will start in EM in

2022 as debt sustainability worries increase.

Currencies and Depreciations in EM currencies eased during Stronger than expected EUR Moderate depreciation of the USD: -2.5% in 2021

capital flows to summer. Negative real rates continues to (1.22) followed by an appreciation +3% end-2022

support risk appetite. Weaker EM (TRY, (1.18). As long as USD depreciates, positive

EM

ZAF) still on watchlist. capital flows in the EM.

Financial It can still get worse before it gets better. Technology sector driven equity market Equity and Corp. markets set to remain under

markets correction due to extreme options pressure due to extreme valuations. Gvt bond

market positioning. markets to remain anchored at low levels.

© Copyright Allianz 3

GLOBAL OUTLOOK: LIVING WITH UNCERTAINTY 01 © Copyright Allianz

COVID-19: LIVING WITH THE VIRUS AND 194 STOP-

AND-GO STRATEGIES

Daily number of new Covid-19 cases Global stringency indices Stringency index

(weighted by GDP and travel services 100 = maximum stringency/lockdowns, 0 = no distancing

100,000 Europe

imports)

Africa 80.0 • Starting from Q3 2020 and until Q4 2021, no

2.5

Middle-East sanitary “normalization” but a stop-and-go

70.0

APAC (excluding India) strategy on distancing measures, alternating

2.0 60.0 between

North America

1. Targeted lockdowns (Spain, Israel)

Latin America 50.0

50,000 1.5 or more stringent distancing

India 40.0 measures (UK, France, US...) every

time cases rise

1.0 International travel 30.0

2. Relaxed measures every time cases

restrictions (lhs)

20.0 are controlled again

0.5 Overall stringency

index (rhs) 10.0 Hiccups in economic activity due to alternation of

0 higher and lower stringencies of sanitary

0.0 0.0

01/20 03/20 05/20 07/20 restrictions

01-20 03-20 05-20 07-20

Sources: John Hopkins University, Allianz Research Sources: Oxford University, Allianz Research • Stringency indices to end 2021 between 10

and 20 in most countries, levels similar to the

Waves of reinfections to be increasingly Reinfections will push for a stop-and-go start of the sanitary crisis

more visible in countries which relaxed strategy. International travel to remain

sanitary restrictions: after Europe, Africa restricted until 2022 when we expect • Return to ~0 stringency by end of Q1 2022

after a 6-months vaccination campaign

+ Latin America should follow. APAC to the end of the sanitary crisis

starting in Q4 2021

remain

© under control.

Copyright Allianz 5

COVID-19 TWILIGHT ZONE: DIVERGING WHILE

PLATEAUING

Daily activity index (mobility, jobs and retail) 70

Manufacturing PMI

65

120

60

55

100

50

80

45

40

60

35

30

09/18

11/18

01/19

03/19

05/19

07/19

09/19

11/19

01/20

03/20

05/20

07/20

40

US China

Germany France

20 Italy Spain United States Germany Italy

UK Brazil

UK Mexico China

Mexico

0

Jan-20 Feb-20 Mar-20 Apr-20 May-20 Jun-20 Jul-20 Aug-20

France Spain Brazil

Sources: Bloomberg, Allianz Research Sources: Markit, Allianz Research

We see the recovery in daily activity rates plateauing in Activity expectations in the manufacturing sector are

most countries and even changing course in Spain, in likely to plateau at current levels post-summer catch-

line with stringency indices stabilizing and new up effects. In countries where sanitary restrictions

outbreaks

© Copyright Allianz

tightened (Spain, France), the index is back in 6

contractionary territoryCOVID19+: POLITICAL RISK IS BACK LIKE A

BOOMERANG Brexit: 55% probability for a very last minute

Key Summits

G20: November 21-22, 2020

agreement with FTA implementation by mid-

2021 Elections in Europe

45% probability for a no deal with early Sept/Oct 2021: Germany (CDU/Greens coalition expected to win with higher

elections and a comeback to the negotiating public investment for greening the economy)

table in 2021 Sep 2021: Russia Duma (United Russia expected to win). Tensions with US

on the rise

Oct 2021: Czechia (ANO expected to win without a majority)

Nov 2021: Bulgaria (GERB expected to win)

Asia-Pacific (geo)political risks to watch

Hong Kong: legislative council election postponed by one

U.S.-China tensionstensions year to September 2021. New protests are possible.

China/US Taiwan: cross-strait relations still tense, with possible

Technology cold war to intensify interventionism of the U.S.

whatever the outcome of US Japan: potential snap elections in Q4 2020.

elections Thailand: anti-government protests to be closely monitored

India: potential boomerang effect related to the Citizenship

Amendment Act.

November 03, 2020 China: long-term trend of isolation of China on the

US presidential election international stage could continue. Australia, India, Japan

Predicted outcome: and Taiwan have been putting policies in place.

60% Democrats win Other elections: New Zealand (Oct 2020), Myanmar (Nov

40% Republicans win 2020), Vietnam (May 2021)

High probability of a close race with

disputed result leading to high market’s

Elections in Africa

volatility and Supreme Court’s final say

Oct 2020: Morocco (PJD expected status-quo with

poor majority and delayed entry into office) Middle East main tension points

Oct 2020: Ivory Coast (Ouattara expected to be re- Large scale anti-government protests in Lebanon, Iraq and Iran

elected but with political instability) - Iran: impact of US withdrawal from JCPOA and new US sanctions, as

Latin America unrests Nov 2020: Burkina Faso (Kaboré expected to be re- well as potential counter measures. Parliamentary election in February

- Brazil: October 2020 local elections (challenging for elected but with period of political paralysis) as a potential source of geopolitical tension

Bolsonaro’s new party), risk of social tensions with Nov 2020: Egypt (status quo to be expected) - Lebanon: political uncertainties and potential new proxy war between

public sector reform Mali: Ghana (either incumbent Nana Akufo-Addo or Saudi and Iran

former president John Mahama to win) - Yemen: Sunni v. Shia

Other Elections : Tanzania, Liberia, Central African - Saudi vs. Iran, incl. Straits of Hormuz, revisited

Republic, Seychelles, Guinea, Somalia, Chad, lybia, - Qatar vs. Saudi Arabia, UAE, Bahrain, Egypt (blockade)

Soudan, Niger - Israel: impact of Jerusalem recognition by the US

Tunisia: new government formation may create - Turkey: Tensions with Greece

instability

© Copyright Allianz 7

Source: Euler Hermes, Allianz ResearchMONETARY POLICY: LOWER-FOR-MUCH-LONGER,

WATCH CURRENCY CONSEQUENCES

Central Banks Balance Sheets (% of GDP) Key interest rates vs 10-year yields EUR to USD

Sources: national sources, Allianz Research Sources: national sources, Allianz Research Sources: Refinitiv, Allianz Research

Global liquidity is at a record high level and should continue to We expect a start of tightening in monetary and financial

increase. The ECB is expected to announce EUR500bn conditions in 2022, as markets anticipate the Fed will

additional QE purchases in December. The Fed is likely to hike interest rates in H2 2023. We expect the USD to

continue to expand its balance sheet to USD7.7tn end of 2021, depreciate by -2.5% in 2021 (to 1.22) followed by an

before

© Copyrighta progressive tapering starting in H2 2022.

Allianz appreciation of +3.0% in 2022 (1.18) 8FISCAL POLICY: MORE THAN A QUICK FIX BUT

BEWARE OF EXECUTION RISKS

Expected impact on GDP growth from fiscal stimulus Distribution of average interest paid on debt (% of total

packages, pp countries, advanced economies)

4.5 100

4.0

3.5 80

3.0

2.5

2.0 60

1.5

1.0 40

0.5

0.0 20

France

US

Germany

UK

Italy

Spain

China

0

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 19

2020 2021 2022 0–2% 2–5% >5%

Sources: national sources, Allianz Research Sources: national sources, Allianz Research

Spending paths matter even more than size: supply side stimulus packages (e.g. France) will need more time to see positive

impact on growth (vs. Germany, UK which focused on short-term measures). China will focus on avoiding excessive private

debt while the US should push public debt into new highs post elections. Fiscal status quo in Germany post 2021 elections.

Risks to the implementation of the EU Recovery Fund by mid-2021 remain high. Debt sustainability insured by prolonged

accommodative

© Copyright Allianz monetary policies and longer average-time to maturities. 9FORECASTS: THE LAST MILE IS THE HARDEST

Real GDP, Q4 2019 = 100 Real GDP growth forecasts, %

2017 2018 2019 2020 2021

110

World GDP growth 3.3 3.1 2.5 -4.7 4.6

105 United States 2.4 2.9 2.3 -5.3 3.7

Latin America 1.0 1.0 0.1 -7.9 3.3

100 Brazil 1.3 1.3 1.1 -6.5 2.5

United Kingdom 1.8 1.3 1.5 -11.8 2.5

95 Eurozone members 2.7 1.9 1.3 -7.9 4.8

Germany 2.8 1.5 0.6 -6.0 3.5

90 United States France 2.4 1.8 1.5 -9.8 6.9

Italy 1.7 0.7 0.3 -10.1 4.2

Eurozone

Spain 2.9 2.4 2.0 -11.8 6.4

85 China

pre-Covid-19 World GDP path Russia 1.8 2.5 1.3 -5.1 2.9

Turkey 7.5 3.0 0.9 -4.7 4.0

80

Asia-Pacific 5.2 4.7 4.2 -1.5 6.2

2019-10

2019-12

2020-02

2020-04

2020-06

2020-08

2020-10

2020-12

2021-02

2021-04

2021-06

2021-08

2021-10

China 6.9 6.7 6.1 2.0 8.4

Japan 2.2 0.3 0.7 -5.5 2.5

India 7.0 6.1 4.2 -7.2 6.5

Sources: national sources, Allianz Research Middle East 1.4 0.9 0.3 -7.1 2.3

Saudi Arabia -0.7 2.4 0.3 -5.1 2.0

China should continue to lead the way in the recovery

Africa 3.1 2.7 1.9 -4.3 3.4

while the US should reach its pre-crisis GDP levels South Africa 1.4 0.8 0.3 -8.2 2.7

end-2021. Europe will remain the laggard until 2022 * Weights in glob al GDP at market price, 2019

even if divergence prevails (Germany and the NB: fiscal year for India

Netherlands

© Copyright Allianz recover faster than Spain, Italy, UK) Sources: national sources, Allianz Research 10FISCAL IMPULSE: FOR CONSUMERS OR VOTERS?

Policy interventions to protect household purchasing power (in red countries with elections in 2020-21)

AUS BEL DEU PER CHL ISR FRA GBR ITA

Expansionary monetary policy

Temporary debt relief

Targeted interventions

Expansion of existing programmes

Wage subsidies

Temporary tax relief

BRA IND PHI SWE HUN JPN S-KR NTL USA

Expansionary monetary policy

Temporary debt relief

Targeted interventions

Expansion of existing programmes

Wage subsidies

Temporary tax relief

Sources BIS, IMF Policy Tracker, Allianz Research

© Copyright Allianz 11INVESTMENT: WITHOUT CONFIDENCE, CASH AND

DEBT MAY PILE UP - FOR NOTHING

Non-financial corporations’ Credits (y/y) – Deposits (y/y) Unemployment rate, %

gross operating surplus, q/q*

15% 14.0 2019 2020 2021

30 Eurozone US 12.5

UK China 12.0

20 10%

10 5% 10.0

8.5

0 8.0

0% 6.5

5.8

-10 6.0

-5% 4.2

-20 4.0

-30 -10%

2.0

01/07

02/08

03/09

04/10

05/11

06/12

07/13

08/14

09/15

10/16

11/17

12/18

01/20

-15%

0.0

France

UK

US

Germany

China

US China UK -20%

01/04

02/05

03/06

04/07

05/08

06/09

07/10

08/11

09/12

10/13

11/14

12/15

01/17

02/18

03/19

04/20

France Germany

Sources: Macrobond, Allianz Research; *for China: industrial profits Sources: Macrobond, Allianz Research Sources: Markit, Caixin, Allianz Research

The Covid-19 profitability shock will Cash hoarding from the private sector is Deteriorating labor markets will

weigh on companies’ investment future a sign of lack of confidence and continue to weigh on consumers

intentions, notably as a majority of suggests a difficult start for a new confidence and keep precautionary

State support schemes arrive at investment cycle savings high

maturity end of 2020

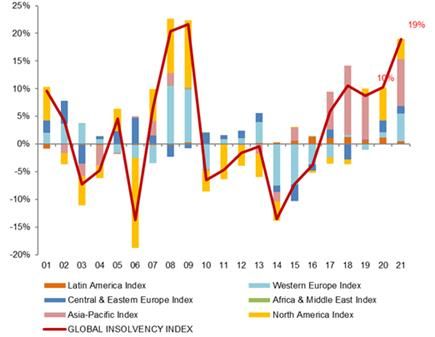

© Copyright Allianz 12INSOLVENCIES: +31% BY END-2021 AS TEMPORARY

SUPPORT SCHEMES END

Insolvency figures and forecasts EH Global Insolvency Index (yearly changes in %)

(selected countries) and contribution of regional indices

2020 Forecasts

Last point 3m y/y Ytd y/y 2020 2021 2020 y/y 2021 y/y 2021/2019

U.S. June -11% -3% 31 500 37 500 39% 19% 65%

Canada July -26% -30% 2 850 3 450 4% 21% 26%

Brazil June -26% -16% 3 450 3 800 20% 10% 32%

Germany June -9% -6% 19 350 20 850 3% 8% 11%

France August -37% -36% 46 800 62 000 -9% 32% 21%

United Kingdom June -31% -20% 22 929 30 072 4% 31% 36%

Italy 11 660 14 039 6% 20% 28%

Spain August 13% -1% 4 600 5 600 11% 22% 35%

The Netherlands August -23% -7% 4 000 5 000 5% 25% 32%

Russia June -25% -4% 13 800 14 500 18% 5% 23%

Turkey July 8% 4% 17 200 18 400 22% 7% 31%

Poland July 32% 3% 1 100 1 210 13% 10% 24%

South Africa July -7% -20% 2 280 2 450 12% 7% 20%

Morocco June -87% -38% 8 861 10 456 5% 18% 24%

China August 1% 7% 13 500 14 700 14% 9% 24%

Japan August 1% 0% 8 600 9 400 3% 9% 12%

India June -75% -25% 750 2 100 -60% 180% 11%

Australia July -51% -34% 6 150 7 150 -4% 16% 12%

South Korea August -34% -41% 400 470 -3% 18% 14%

GLOBAL INDEX 10% 19% 31%

Sources: Euler Hermes, Allianz Research Sources: Euler Hermes, Allianz Research

Our EH Global insolvency index posted a -13% y/y decline in The ending of temporary factors will lead to a trend

Q2 and -7% y/y for H1. This drop in official registrations of reversal starting end of Q3 or Q4 depending on countries

insolvencies continued in most countries during the summer, and accelerating in H1 2021. Our global insolvency index

due to (i) policy measures designed to avoid liquidity and (ii) would surge by +31% by end of 2021, with all regions

changes in insolvency frameworks designed to give time and contributing to the rise. Should the recovery switch to L-

flexibility to companies before they resort to filing for shape the rises will be +50 to +60pp higher.

© Copyright Allianz 13

bankruptcy.TRADE: RECOVERY FOR TRADE IN GOODS, BUT

REMEMBER IT’S A SERVICE CRISIS

Global merchandise trade in volume (100 = Consumption components (% total, Europe) Global trade growth, in volume terms and

Sept. 2008 and 100 = Feb. 2020) value (%, y/y)

105 15%

Volume Price 13.0%

10.2%

September 2008 / 10% 4.0%

3.3% 9.7% 5.0%

100 February 2020

5% 2.8%1.9%3.0%

2.5% 7.0%

5.6% 4.3% 1.3% 3.5%

95 0%

June 2020 -2.0%

-5% -1.6%

90

-13.0%

-10% -10.8%

85

May 2020 May 2009 -15%

-16.0%

80 -20%

1 6 11 16 21 26 31

2020 2008-2009 -25%

13 14 15 16 17 18 19e 20f 21f 22f

Sources: CPB, Kiel, Allianz Research Sources: Refinitiv, Allianz Research Sources: Bloomberg, Euler Hermes, Allianz Research

Rebound is stronger than 2009. Yet Recession victims (cyclical durables, Trade should contract -13% in 2020 (vs

transport & travel services will only clothing & footwear etc.) are joined by -15% previously). Oil + commodity price

recover in 2023 (2022 for goods).: “social expenditure” (transportation, shock = negative price effect in 2020.

Reduced US - China uncertainty, restaurants & hotels, recreation & culture 2021 = return to 51 after ~44 in 2020, +

some

© reshoring but no full de-

Copyright Allianz services) which makes up 23% of private lower USD boosting value of trade. 14

globalization. consumption.GLOBAL SECTORS: A MAJORITY OF SECTORS WILL

COME BACK TO PRE-CRISIS LEVELS POST 2021

• (Food) Retail • (Non-food) Retail

• Pharmaceuticals • Transportation (air)

• Agrifood (food)

• Electronics

• Agrifood (farming)

• Telecoms

• Transportation (rail)

• Household equipment

• Machinery

• Transportation (sea, road)

• Construction •

• Paper Textiles

• Transport equipment (ship, truck, train) • Transport equipment (aircraft)

• IT (services) • Metals • Automotive manufacturers

• Agrifood (beverages) • Automotive suppliers

• Chemicals • Energy

© Copyright AllianzGLOBALIZATION: NOT IMMUNE TO COVID19

Number of investment projects*/M&A, growth, monthly Potential trajectories for international production and

average, Q2 2020 vs. all 2019 global trade

Textiles, clothing and leather -54 -24 RE- DIVERSIFICATION REGIONALIZA REPLICAT

Pharmaceuticals -51 13 SHORING TION ION

Accommodation and food services -49 -11

IMPACT ON Shorter, less Continued fragmentation of Shorter physical Much shorter

Motor vehicles, transport equipment -41 -25

INTERNATIONAL fragmented value supply chains. supply chains, but and less

Basic materials -38 -18 chains. not less fragmented. fragmented

PRODUCTION Increased platform-based

Trade -33 -11 value chains,

Rebundling of supply chain governance Decentralized

Computer, electronic, and electrical… -40 -31

supply chain governance, Higher

-9 + concentrated VA

Primary -29 Crossborder outsourcing geographical

+ concentrated VA Increased offshoring and

Machinery and equipment -28

-26 M&A deals distribution of

Less offshoring/ outsourcing of services. More geographically

Transportation and storage -25 -18 distributed value activities, but +

outsourcing concentrated

Information and communication -29 -22 added.

-35 VA.

Food, beverages and tobacco -21

Business activities -20 -12 Greenfield + outsourcing

Construction -20-17 projects

SECTORS THAT High technology Medium-low technology Extractive industries, Global hub and

Financial and insurance activities -33 -17 WOULD BENEFIT intensity intensity (textiles and agro-based spokes

Electricity, gas, water and waste mgmt -25 2 THE MOST (automotive, apparel) (pharmaceutica

High technology

machinery and Financial services, business intensity ls)

-60 -50 -40 -30 -20 -10 0 10 20

equipment, services

Sources: UNCTAD, Allianz Research electronics) Regional processing

*With greenfield investing, a company will build its own, brand new facilities from the (food and beverage,

Wholesale and chemicals

ground up. Different from brownfield investment happens when a company purchases retail trade,

or leases an existing facility transportation and

logistics

# of announced greenfield projects and cross-border

M&As have seen a sharp decline. While some sectors

Sources: UNCTAD, Allianz Research

could benefit from “reshoring”, others could win from

© Copyright Allianz 16

diversification or regionalization.SCARRING EFFECTS: 2021 INITIAL CONDITIONS ARE

DIFFERENT

Strong state, redux Cold war, reloaded Zero interest rates, for longer

State everywhere in life of business: • Geopolitical rivalry between China Monetary policy as backstop for

• More public-private partnerships and the US has increased banana markets and excessive risk-

• Assertive and interventionist taking by debtors and investors

governments and regulators, also • Weaponizing of technology, trade,

in social security currencies, payments etc. • New wealth inequalities (access to

• Fiscal politics: threat of • EU alone in pursuit of principled property, savings opportunities)

zombification recovery (green, equitable) • Faustian fiscal-monetary bargain

Agility+ Consuming (risks) differently Work from home anyone?

Record-fast adaption to lockdowns More demand for risk cover, including Lockdowns have changed the way

unleashed new pioneering spirit tail risks but unsure about price of risk we work for good

• Change becomes much faster, • Different consumption patterns and • More flexible and innovative team

including digital leapfrogging Covid19-induced behaviors in structures

• Reset mentality v. sticky services • Risks to commercial real estate

economics • Climate risk sensitivity up and productivity

© Copyright Allianz 30-Sep-20 17CAPITAL MARKETS: IS THERE A PRICE? 02 © Copyright Allianz

CAPITAL MARKETS: NOT THE TIME TO TAKE RISKS

1. There is greater economic uncertainty than at the beginning of the year

year-end figures Latest Value Unit 2020 2021

despite the current monetary and fiscal policy mix.

2. There is more geopolitical risks than at the beginning of the year. Eurozone

Sovereign Rates

3. Valuations are tighter than at the beginning of the year.

10y yield “risk-free” sovereign (Bunds) -0.5 % -0.5 -0.3

Sovereign Rates 10y Swap Rate -0.2 % 0.0 0.3

With the short-end of most developed countries’ yield curves anchored by Italy - Germany spread (10y) 148 bps 175 (220) 160 (170)

their respective central banks, we expect a timid curve steepening towards France - Germany spread (10y) 27 bps 40 (90) 30 (40)

Spain - Germany spread (10y) 75 bps 90 (110) 80 (70)

the end of 2020 and 2021. This gradual increase in term premium will occur

Corporate Credit Spreads

on the back of higher inflation expectations and a halt in the recent decline

Investment grade credit spreads 113 bps 180 150

of real yields.

High yield credit spreads 438 bps 750 600

On the other hand, long-term emerging market sovereign spreads look Equities

overbought. The combination of this extreme bullish positioning and the MSCI EMU: total return p.a -9 % -22 10

current market fragility is a perfect combination for EM assets to become a

United States

victim of a second “risk-off” rotation in the wake of a second risky-assets

Sovereign Rates

market correction.

10y yield “risk-free” sovereign (Treasuries) 0.7 % 1.0 1.4

Corporate Credit Corporate Credit Spreads

Investment grade credit spreads 136 bps 230 180

As of today, both investment grade and high yield corporate spreads look

High yield credit spreads 514 bps 800 650

too tight. Corporate credit markets remain detached from fundamentals on

Equities

the back of the central banks’ perpetual put option. We expect corporate

MSCI USA: total return p.a. in USD 3 % -20 15

spreads to converge towards higher values on the back of higher than Emerging Markets

expected market volatility and defaults. Sovereign Rates

Hard Currency Spread (USD) 341 bps 450 370

Equities Equities

MSCI EM: total return p.a. in USD -4 % -24 20

Due to the persistent detachment from its fundamental determinants, the

recent global equity market rally is hardly justifiable. Because of that, we still * Old forecasts in parenthesis

expect EQ market to underperform in 2020 and to start a muted rally in ** We have reviewed our EUR spreads down

© Copyright Allianz as the ECB impact on peripheral spreads was larger than anticipated. 19

2021.BOND MARKETS: PRICING STAGFLATION!

US – 10y Nominal Yield Breakdown EMU – 10y Nominal Yield Breakdown

5% 10Y market inflation expectations 2%

Real 10y UST yield

4% Nominal 10Y UST yield

1%

3%

2%

0%

1%

0%

-1%

Real 10Y EUR Swap

-1%

10Y market inflation expectations

-2% Nominal 10Y EUR Swap

-2%

2015 2016 2017 2018 2019 2020 2014 2015 2016 2017 2018 2019 2020

Source: Refinitiv, Allianz Research Sources: Refinitiv, Allianz Research

Despite the recent repricing of long-term inflation expectations, As in the US, long-term inflation expectations in the EMU

nominal yields have barely bulged thanks to a fall in real yields. have been rising while real yields remain at historical lows.

To put current levels into perspective, at -1.1% real yields, are All in all, US and EUR government bond markets are

now at the lowest point in recorded history. The current bearish unwilling to believe in a rapid economic recovery scenario

growth positioning within the US government bond market and are rather positioned for a stagflation scenario.

contrasts with the recent equity market exuberance, fuelling

doubts about the short- to mid-term equity market rally

sustainability.

© Copyright Allianz 20INFLATION EXPECTATIONS: BACK TO SQUARE ONE!

US – 10y Market-based Inflation Expectations EMU – 10y Market-based Inflation Expectations

% %

3.0 3.0

2.5 2.5

2.0 2.0

1.5 1.5

1.0 1.0

10-Year US TIPS breakeven inflation rate 10-Year EUR breakeven inflation rate

In sample estimation In sample estimation

0.5 0.5

Out-of-sample forecast Out-of-sample forecast

+/- 1 std-deviation +/- 1 std-deviation

0.0 0.0

2004 2006 2008 2010 2012 2014 2016 2018 2020 2008 2010 2012 2014 2016 2018 2020

Source: Refinitiv, Allianz Research Sources: Refinitiv, Allianz Research

The recent in crease in Oil and employment has led US In contrast to the US case, EUR long-term inflation

long-term inflation expectations to follow a V-shaped expectations are nowhere near their “fair value”, as

trajectory around their March low. Since the trough, inflation monetary stimulus has not convinced market participants.

expectations are on an upward trajectory exacerbated by the According to our model, EUR inflation expectations could

recent Fed’s decision to target an average inflation rate of still move closer to 1.5% in the near future, but any

2%, (i.e. allowing some overshooting above 2%). According overshoot beyond that level would not be sustainable.

to our “fair value” estimation, inflation expectations are

unlikely to substantially overshoot the 2% upper limit.

© Copyright Allianz 21PRICES: DISINFLATION BEFORE MODERATE AND

TEMPORARY OVERSHOOT STARTING IN 2022

Inflation rates, % Correlation between US inflation rates and equity

2020 2021 2022 2023

Eurozone

Central 0.3 0.9 1.2 1.4

scenario

Protracted -0.1 -1.5 -1.2 -1.1

crisis

United States

Central 1.1 1.6 2.1 2.7

scenario

Protracted 0.5 -0.4 0/7 0.7

crisis

Sources: Allianz Research Sources: Allianz Research

In the short-term we expect disinflationary pressures to Historically, US inflation levels persistently higher

prevail as supply recovers faster than demand. A than 3% or lower than 0% tend to go in sync with a

temporary and moderate overshoot is expected in the substantial equity market correction.

US as soon as mid-2022 as the economy returns to pre-

crisis levels

© Copyright Allianz end-2021 22INVESTMENT POSITIONING: WHERE ARE THE BULLS?

US – Mutual Funds & ETF Weekly Investment Flows EMU – Mutual Funds & ETF Weekly Investment Flows

USD Bn 100 = 31.12.2019

100 = 31.12.2019

USD Bn

300 110 150 110

250 105 100

200 100

100

150 50

95

100 0 90

90

50 -50

85 80

0

80 -100

-50 70

-100 75 -150

-150 70 -200 60

Dec-19 Feb-20 Apr-20 Jun-20 Aug-20 Dec-19 Feb-20 Apr-20 Jun-20 Aug-20

Equity Bond Equity Bond

Money Market Mixed Assets Money Market Mixed Assets

Others S&P500 (RHS) Others Stoxx 600 (RHS)

Bond Index (RHS) Money Market Index (RHS) Bond Index (RHS) Money Market Index (RHS)

Source: Refinitiv, Allianz Research Sources: Refinitiv, Allianz Research

The recent US equity market frothiness is relatively hard to Differently, the Eurozone equity market does not show any

explain as both mutual fund and ETF flows show persistent signs of market exuberance (yet) as most EUR equity

transfers from Equity funds towards Fixed Income and indices have settled around -10%ytd. Nevertheless, looking

Money Market funds. This is a symptom of the current at fund flow data, one can see a small acceleration in the

market fragility as structural long-term investors seem inflows into EUR EQ funds, with Germany and France

unwilling to participate in the market, thus leaving the floor to leading the pack.

© Copyright Allianz 23

stock pickers and option traders.CORPORATE CREDIT: HARD TO KEEP A PROMISE

US – Fed Corporate Purchases US IG Issuance – Use of Proceeds

50 Commercial Paper 1400 100%

Corporate Credit 17%

45 27% 27% 24% 24%

Investment Grade Spread (RHS) 1200 30% 30%

80% 38% 42%

40 High Yield Spread (RHS)

25%

35 1000 14% 13% 22%

11% 25%

60% 17%

30 19% 7%

800

25

40%

600 49%

20 56% 56% 54% 46%

50% 48% 48%

15 40%

400 20%

10

200 5% 5% 9% 4% 7%

5 0% 3% 3% 3% 3%

2012 2023 2014 2015 2016 2017 2018 2019 2020

0 0

Dec-19 Feb-20 Apr-20 Jun-20 Aug-20 Recapitalization General Corporate Purpose

Acquisition-related Refinancing

Source: Refinitiv, Allianz Research Sources: S&P, Morgan Stanley, Allianz Research

Since April, the US Federal Reserve has bought up to ~45Bn The $1.919tn Us corporate credit issuance in the first 9

worth of corporate credit. However, since the beginning of July, months of 2020 has already surpassed the historical record

the Fed has significantly reduced its weekly purchases as credit of $1.916tn set during the 12 months of 2017. Interestingly,

markets are once again extremely tight. Yet, credit markets most of that fresh money will most likely not be invested into

spreads have not reversed back to pre-Covid19 levels and remain the issuing companies as 42% of all new issuances are

10 to 20% above pre-pandemic levels. expected to be dedicated to debt refinancing purposes.

© Copyright Allianz 24EQUITY: TECH DOMINANT CLUSTER

US EQ – Sector Weightings 30% EMU EQ – Sector Weightings

35%

25%

30%

25% 20%

20%

15%

15%

10%

10%

5% 5%

0% 0%

1975 1980 1985 1990 1995 2000 2005 2010 2015 2020 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020

Recession Technology Recession Technology

Health Care Financials Telecom Health Care

Industrials Ind. Goods & Svs Financials Insurance

Energy Consumer Staples

Source: Refinitiv, Allianz Research (Only sectors with +10% weight*) Source: Refinitiv, Allianz Research (Only sectors with +5% weight)

Historically, each financial cycle has been led by a limited group of In the case of the Eurozone, the Equity market has been

companies usually clustered around one industry group / economic permanently dominated, in terms of weight, by the financial

sector. These days, the technology sector accounts for more than sector. Nevertheless, this dominance is starting to be

25% of the US EQ market capitalization** . Additionally, the questioned by the technology and health care sector, as their

concentration risk is higher since, not only the sector accounts for respective weights within the market have increased since the

more than one fourth of the index, but the number of companies 2008 Great Financial Crisis.

within the sector itself has been reduced by 20 to 40% since the * Sudden jumps in weightings are due to sector reclassification.

© Copyright Allianz 25

Dot-com bubble. ** Weights are based on the Datastream-Refinitiv Equity sector indices.EQUITY EXUBERANCE: HIGH EXPECTATIONS!

Apple – Return expectations Market Expectations

Relevant past data

90 1,000.00 for current return

Expected annual rate of determination

80 02.09.2020 Price return (%) (in years)

70 100.00

60 Alphabet-Google 1,717.39 21.5 3.62

Amazon 3,531.45 56.0 1.66

Log scale

50 10.00

Apple 131.40 56.7 1.58

40

Bitcoin 11,398.44 46.1 1.79

30 1.00 Oil Brent 44.51 -0.8 24.21

20 Facebook 302.50 20.9 3.64

10 0.10 Gold 1,940.23 7.6 7.27

Microsoft 231.65 33.3 2.50

0

Netflix 552.84 46.7 1.86

-10 0.01 Tesla 447.37 228.2 0.60

1980 1985 1990 1995 2000 2005 2010 2015 2020

TRY to 1 USD 7.38 18.4 3.92

Apple-Perceived return at annual rate in % (L.H.S)

Zoom Video Comm. 423.56 38.7 1.97

Apple (R.H.S)

Source: Refinitiv, Allianz Research Sources: Allianz Research

The equity market is falling prey to a positive feedback loop As this expectation disproportionately depends on recent price

whereby rising equity prices increase the demand for movements (the ones observed during only the last 1.6 years), it is

equities, which in turn fosters further rises in prices. We inherently unstable. Furthermore, as the Apple stock is already trading at

estimate, for example, that the recent performance of Apple a multiple of 40, little appreciation is to be expected from further PE

leads market participants to expect a 56.7% annual return expansion; EPS growth will be the main driver of its future return, but a

from Apple. In the past, this perceived return has been 50%+ earnings growth looks ambitious and unsustainable.

higher in only 1.2% of observations (i.e. 6 days out of 500).

© Copyright Allianz 26THE U.S. PIVOT, CHINA RELOADED, AND THE ALMOST UNITED STATES OF EUROPE 03 © Copyright Allianz

US ELECTIONS: 4 SCENARIOS © Copyright Allianz 30-Sep-20 28

US ELECTIONS: SMALLER GOV. VS. BIG SPENDING

U.S. public debt, % of GDP

TRUMP BIDEN

SPENDING, $bn (-2965) SPENDING, $bn (+6435.85) 155%

1275 Infrastructure 970 Infrastructure (not 145%

elsewhere)

-125 Higher education

2000 Climate change 135%

-280 Reform welfare

programs & increase 750 Student loans

parental leave 125%

1650 Health

-1550 Discretionary, non- 115%

defense 128.2 Schools

-400 Discretionary, 23.6 Defense 105%

defense 240.5 Public-private investment 19 20 21 22 23 24 25 26 27 28 29 30

-1630 Health 640 Housing plan Biden Trump CBO

-255 Other spending cuts 33.55 Other spending

President Trump’s intentions point Both candidates have no real

REVENUE, $bn (-1085) increases

towards a supply-side oriented intention to reduce the level of

-1370 Tax decrease REVENUE, $bn (+3686) policy. Joe Biden's economic public debt. We expect them to

3746 Tax increases platform gives more weight to make public debt significantly

185 Reduce tax incentives

& raise fees higher redistribution, but won't increase above 150% of GDP by

-60 Increase tax incentives

stand as the most leftist aspects 2030, which should cause a

of his entire platform. negative impact on growth

29

© Copyright Allianz potential.AVERAGE INFLATION TARGETING: BUYING TWO

YEARS FOR THE US ECONOMY

Average performance of the Fed in terms of inflation (%) Fed's Taylor function

Sources: Wall Street Journal, Euler Hermes, Allianz Research Sources: Euler Hermes, Allianz Research

Since adoption of its 2% inflation target, the Fed has For every quarter when 4-year average inflation is

constantly failed in reaching it. In order to be credible, below 2%, we incrementally rebalance the Taylor

the Fed had no choice than rebalancing in favor of its function in favor of job market stabilization. In this

full employment mandate. case, the first hike of the Fed is expected in Q3 2023

© Copyright Allianz only. 30CHINA’S RECOVERY: UNEVEN BUT RESILIENT

GDP growth (%) and contributions (pp) Activity indicators growth, %y/y Fiscal support & infrastructure investment

Net exports 35 35

14

Gross Capital Formation 110

Government Consumption 25

Private Consumption 25

GDP %y/y 60

8.4 15

9 15

10

5

5

2.0 (5) (40)

4

-5 Infrastructure investment,

(15) ytd %y/y (90)

Real industrial production %y/y

-15 (25) Local government (140)

Nominal urban fixed assets

-1 finances*, ytd %y/y, 4-

Investment YTD, %y/y

2020E

2021E

month lead (rhs)

2011

2012

2013

2014

2015

2016

2017

2018

2019

-25 Nominal retail sales %y/y (35) (190)

07 08 09 10 11 12 13 14 15 16 17 18 19 20 12 13 14 15 16 17 18 19 20 21

Sources: National sources, Euler Hermes, Allianz Research Sources: National sources, Euler Hermes, Allianz Research Sources: National sources, Euler Hermes, Allianz Research

After the initial Covid-19 related shock The recovery has been uneven so far, The recovery is mostly policy-driven,

in Q1, the Chinese economy has being largely driven by the production with in particular infrastructure and real

surprised on the upside – in part thanks side, against consumers still showing estate investment outperforming. We

to resilient exports. We expect the low confidence and a hit to disposable estimate fiscal support at 7.1% of GDP

recovery

© Copyright Allianzto extend into 2021. income. in 2020. We expect smaller but still 31

large support in 2021 (c.5.5%).CHINA’S POLICY EASING IS PEAKING

Private non-financial sector debt service Credit impulse & manufacturing PMI FX rates

ratio (%)

25 56 Official Manufacturing PMI 25 20

7.2

55 20 15

Credit impulse, 12-month

20 lead, rhs 7 10

54 15

6.8 5

53 10 0

15 Forecast 6.6

52 5 -5

6.4

10 -10

51 0

6.2 -15

China 50 -5

5 6 -20

U.S.

Japan 49 -10 11 12 13 14 15 16 17 18 19 20

Germany Spread (bp), rhs

0 48 -15 USDCNH rate

04 06 08 10 12 14 16 18 20 09 10 11 12 13 14 15 16 17 18 19 20 21 22 23 USDCNY central parity rate

Sources: BIS, Euler Hermes, Allianz Research Sources: National sources, Euler Hermes, Allianz Research Sources: Macrobond, Euler Hermes, Allianz Research

China’s debt service ratio had increased As the economic recovery is well In a context of China leading the global

rapidly following the GFC, before underway, the PBOC’s focus could recovery, and policy easing peaking, we

stabilizing from 2016 thanks to supply gradually turn to structural issues again. expect further room for appreciation for

side reforms. The Covid-19 crisis is We thus expect the peak of monetary the CNY vs. the USD, by c.3% over the

putting

© upside pressures on the ratio

Copyright Allianz easing to be reached in coming months. coming year (USDCNY towards 6.6). 32

again.BREXIT: A LAST-MINUTE COMPROMISE

Soft Brexit with very-last minute compromise and FTA Hard Brexit on Jan 1st, 2021 with likely comeback into

implementation by mid-2021 (55%) negotiations during 2021 after early elections (45%)

2020 2021 2020 2021

GDP growth, % -11.8 +2.5 -10.9 -4.8

Consumer spending, % -13.3 5.9 -12.0 0.7

Total investment, % -26.8 -15.1 -26.8 -25.8

Exports, % -13.7 1.8 -13.7 -13.0

Inflation 0.7 1.5 0.7 4.5

Unemployment rate 7.0 8.5 7.0 10.0

GBP/EUR, annual change -2.0 -3.0 -2.0 -10.0

Business insolvencies, % 4.0 31.0 4.0 53.0

Monetary policy QE increased by 5% of GDP (around GBP100bn) and Rates cut into negative territory and QE increased by

implemented until mid-2021, rates unchanged at 0.1% GBP250-300bn, similar to the Covid-19 package

Fiscal policy 2% of GDP in 2021 (after only 1.5% in 2020) 4% of GDP in 2021 mainly focused on infrastructure spending

mainly focused on infrastructure spending and tax cuts and measures to protect consumers purchasing power. State

guaranteed loans prolonged until end-2021.

Gilt expectations and equity 10y GILT at 0.4%(eoy) 10y GILT at 0.6%(eoy) 10y GILT at -0.2%(eoy) 10y GILT at 0.1%(eoy)

strategy FTSE 100 at -22%yoy (eoy) FTSE 100 at +10%yoy(eoy) FTSE 100 at -50%yoy (eoy) FTSE 100 at -10%yoy(eoy)

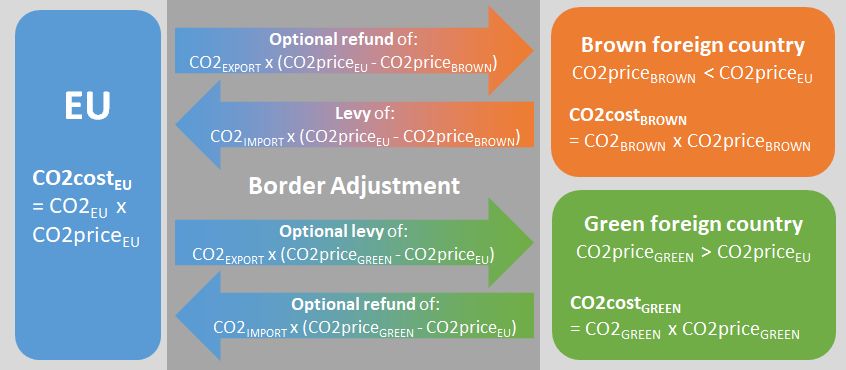

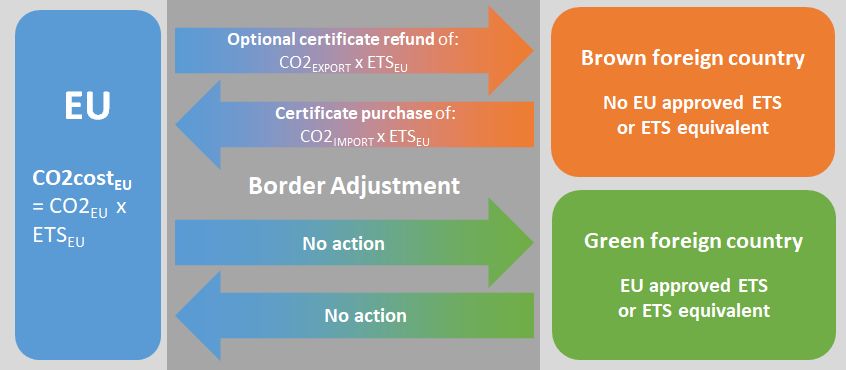

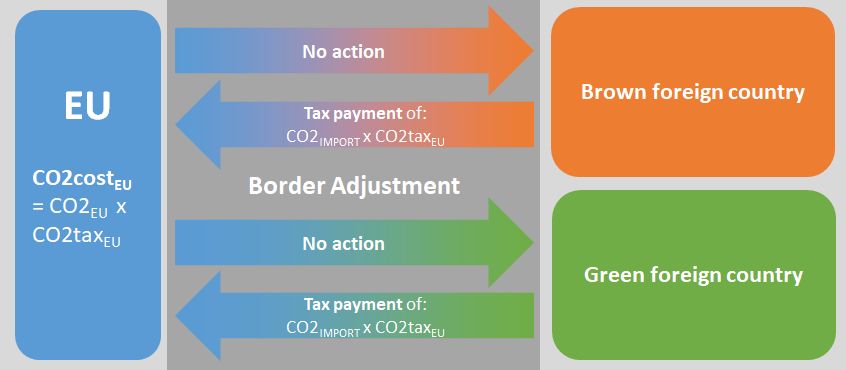

© Copyright Allianz 33EUROPE: A CARBON TAX FOR A PRINCIPLED

RECOVERY?

Option 1: Carbon tariff on imports Option 2: Extension of EU ETS to imports Option 3: Tax on product’s CO2 content

Source: Allianz Research Source: Allianz Research Source: Allianz Research

• Tariff on implicit CO2 content of traded • Purchase of certificates for implicit CO2 • Tax on implicit CO2 content of specific

intermediates and final goods content of traded intermediates and final goods

goods

• WTO conformity requires comparable • WTO conformity requires abandoning • WTO conform

pricing of domestic goods EU free allocation practice

• Possibility to “subsidize” exports to • Possibility to “subsidize” exports to • Not possibility to subsidize exports to

brown countries brown countries brown countries

• Other carbon payments can be deducted • Other carbon payments can be deducted

• Improves competitiveness of EU industry • Improves competitiveness, endorsed by • Basically just a carbon tax on some

French government output goods

© Copyright Allianz 34CHINA: DUAL CIRCULATION IS ON

High-tech exports from domestic U.S. companies’ investment plans in China China’s repackaged strategy: “dual circulation”

companies (% of total)

100 Planning to increase investment • Reroute some Chinese exports

2005 2012 2015 domestically, given the crisis

• Redirect consumers’

circulation

No investment expansion planned / Chinese

Domestic

All products 8% 12% 19% 80 Planning to decrease investment overseas spending domestically.

• Encourage firms to become less

Medical equipment 14% 34% 41% dependent on foreign supplies.

60 Further investment and supportive

Telecoms equipment 11% 26% 26% policies for strategic high-tech sectors.

37 Domestic circulation does not mean

Electronic appliances 7% 6% 16% 40 32 32

31 31

27 26 closing its doors to foreign firms. As of

International

circulation

August 2020, more measures to

Semiconductors 14% 13% 14% 16

20 support foreign companies have been

put in place than over all 2019.

Integrated circuits 2% 5% 12%

More reforms to liberalize the capital

0 account, support foreign investment

Computers 1% 1% 3% 2013 2014 2015 2016 2017 2018 2019 2020 (especially in the services sector).

Source: Kennedy, The Fat Tech Dragon (CSIS, 2017) Source: 2020 China Business Climate Survey Report Source: Euler Hermes, Allianz Research

In the long run, China still aims to climb Foreign cooperation and investment In May, China rebranded its long-term

up the global value chain. While there should help in the path of technological strategy of industrial upgrade and

have been significant improvements in upgrade. However, the loosening U.S.- self-sufficiency into the expression

the past years, there is still large room China relations could mean slowing “dual circulation”. The focus is still on

for

© catching-up

Copyright Allianz in high-tech sectors. foreign direct investment into China. domestic high-tech and foreign 35

investment.EUROZONE: LABOR MARKET FAR FROM OUT OF THE

WOODS, EU FUNDS COULD CUSHION PAIN

Number of furloughed workers, increase in unemployment EU support funds (% of 2019 national GDP)

& inactive population and zombie jobs

Sources: Eurostat, Allianz Research Sources: EU Commission, Allianz Research

In many large EU countries furlough schemes have been The great equalizer? EU funds could provide

extended until 2021. While this is good news for the short- important economic tailwind in the most impacted

term economic outlook, policymakers are not yet doing economies, but implementation risk remains a key

enough to mitigate the risk of zombie jobs (reskilling, hiring downside risk.

incentives

© Copyright Allianzetc.). 36EUROZONE: INVESTMENT, THE LAST MAN RISING IN

THE RECOVERY

NPL loss simulations (2019-2021) Eurozone: Fixed investment vs. Industrial confidence

Sources: Allianz Research. Sources: Refinitiv, Allianz Research.

Rising credit risk ( we expect NPLs to rise from 3.1% in Heightened uncertainty around the economic outlook

Q4 2019 to 4.7%-5.4% by end 2021) together with the together with depressed margins will keep a lid on

phasing out of public loan guarantees will weigh on corporate investment in the coming months. In 2022,

banks' readiness to extent credit to the private sector. investment will still be 5% below pre-crisis levels.

© Copyright Allianz 37GERMANY: MIND COMPLACENCY

Germany: Real GDP (%) & its Key fiscal support measures (EUR bn) Germany: Industrial production

components (pp) (change vs. Jan 2020, %)

Sources: Refinitiv, Allianz Research. Sources: German Ministry of Finance, Allianz Research Sources: Refinitiv, Allianz Research.

Germany's relatively resilient consumer - No quick return to the black zero: Given the The industrial rebound has been propped

in part thanks to fiscal policy's focus looming fiscal cliff in 2022 as most up by the automobile sector, but the

on stimulating demand at the expense of measures boosting consumption & uneven global recovery, the strong EUR

the supply side - will drive the partial income expire, expect the next government and high uncertainty won't allow for a full

rebound in GDP in 2021, while trade will

© Copyright Allianz to cushion the impact with fresh easing recovery before 2022. 38

3

remain muted. measures.FRANCE: GROWING CONCERNS FOR JOBS

Consumer confidence survey Outstanding bank deposits Announced Phase II stimulus (EURbn)

(index, Jan 2018=100)

Major purchases intentions, next 12 months Covid-19-adjusted

Type of measure France Germany Italy*

Unemployment, next 12 months 135 fiscal multiplier

Consumption taxes /

100 Savings intentions, next 12 months 130 US UK subsidies

0.10 0 31 1

80 125 France Germany Transfers 0.10 10 14 3

Corporate taxes &

0.50 30 13 1

60 120 competitiveness

Labor support (incl.

0.50 20 10 12

partial unemployment)

40 115

Public consumption 0.50 15 25 3

20 110

Public investment 0.85 25 50 2

0 105

TOTAL 100 143 31

-20 100 Share of GDP 4.3% 3.8% 1.5%

-40 95 Country-wide fiscal

multiplier 0.55 0.50 0.48

-60 90

01-04

01-05

01-06

01-07

01-08

01-09

01-10

01-11

01-12

01-13

01-14

01-15

01-16

01-17

01-18

01-19

01-20

Impact of stimulus

2018

2018

2018

2018

2019

2019

2019

2019

2020

2020

2020

2.4pp 2pp 0.7pp

on growth

*not all measures have been detailed, only partial categories. Totals might not add up

Sources: INSEE, Allianz Research; Latest data: August 2020 Sources: Banque de France, Allianz Research Sources: Euler Hermes, Allianz Research, IMF

The household confidence indicator The EUR110bn emergency package The French structural reforms are

(long term average =100) decreased from March 2020 helped to absorb good news for potential growth. But

in July to 94 (from 96 in June) and the Covid-19 shock but also fueled in the short-term, we see the largest

remained stable in August.

© Copyright Allianz

cash hoardings of household and deterioration in merchandise trade 393

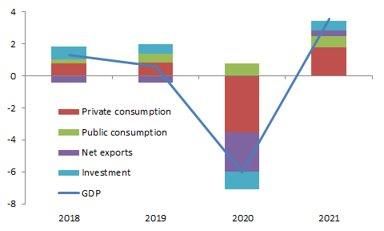

companies. deficit (-EUR12bn over 2021-22).ITALY: WORST-CASE SCENARIO AVOIDED

GDP by component, % Evolution of public finances (in EUR mn)

10.00

Households GFCF Government 80,000

5.00 Stocks Net Trade real GDP 60,000

40,000

0.00

20,000

0

-5.00

-20,000

-10.00 -40,000

01/20 02/20 03/20 04/20 05/20 06/20 07/20 08/20 09/20

-15.00 Gov. net issuance Gov. expenditures

12 13 14 15 16 17 18 19 20f 21f Gov. balance

Sources: Refinitiv, Allianz Research Sources: Refinitiv, Allianz Research

Decline in real GDP smaller than previously expected (-10.1%). Additional EUR25bn fiscal package and EU RF (~200bn in

Robust manufacturing recovery with good start into Q3. loans and grants) mostly effective in 2021. Balance

Challenges: Tourism (-70% international arrivals), reversing between maintaining short term stimulus and returning to

stocks, difficult transmission of guaranteed loans to SME due to longer term fiscal prudence as public debt will soar to

banking sector weakness. In 2021, rebound of +4.3%. 160% of GDP and primary balance remains a signal to

© Copyright Allianz markets. Risk of fiscal inaction in H2. 40SPAIN: THE COST OF INACTION

Recession & Covid-19 sensitive consumption components GDP growth forecast and potential impulse from stimulus

in % of GDP

10.0

7.4

5.0 6.4 4.5

3.5

2.5 1.5

0.0

Impulse from fiscal stimulus, if

-5.0 fully implemented

Baseline GDP growth and

-10.0 forecast

Total GDP growth, boosted by -11.8

-15.0 EU recovery fund

14 15 16 17 18 19 20 21 22 23

Sources: Refinitiv, Allianz Research Sources: National Statistics, IHS Data Insight, Allianz Research

In Spain, among worst hit, % of consumption at risk Spain could receive EUR140bn from the EU recovery

(hotels, culture…) is among the highest (25%). Bad fund in 2021. Yet continued political fragmentation

omen for recovery. Seasonality of activity means the (no 2021 budget voted) should delay the “relaunch”

disappointing summer will also weigh on recovery. stimulus. This could result in a shortfall of a

© Copyright Allianz cumulated ~5pp of GDP growth during the recovery. 41EMERGING MARKETS: EXTERNAL TAILWINDS 04 © Copyright Allianz

EMERGING MARKETS: V-SHAPED RECOVERY IN

‘CHINA WORLD’, W-SHAPED ELSEWHERE

Composite Manufacturing PMIs of ‘China-dependent’ and Net non-resident portfolio flows to EMs by region (USD bn)

‘non-China-dependent’ EMs vs. China’s PMI

55 53.1 100 Africa & Middle East Emerging Europe

80 Latin America Emerging Asia ex China

51.0 China

50 60

49.8

40

45 20

0

40 -20

China PMI

-40

'China world' EM Composite PMI

35 -60

'Non-China world' EM Composite PMI

-80

30 -100

15 16 17 18 19 20 18-01 18-07 19-01 19-07 20-01 20-07

NB: ‘China world’ includes Taiwan, Hong Kong, Singapore, Indonesia, South Sources: National statistics, IIF, Allianz Research estimates

Korea, Brazil, Russia, South Africa.

Sources: National statistics, IIF, Allianz Research estimates Negative real interest rates should support risk appetite in

the EM if no negative surprise on monetary policy or political

EMs highly dependent on exports to China follow the

risk. In addition, the USD depreciation (-2.5% end of 2021)

latter’s business cycle with a lag. Other EMs

and China’s recovery should also be positive.

experienced a deeper recession and will see a slower

© Copyright Allianz 43

recovery.EMERGING MARKETS: TOO LITTLE OR TOO MUCH

EMs pursuing government bond purchases (“’QE”) face Sustainability of fiscal stimulus depends on interest rate-

debt sustainability and inflationary risk growth spread and debt maturity structure

Emerging Asia

Low Brazil High Egypt

Emerging Europe

inflationary risk inflationary risk 25 Middle East

High debt High debt

Africa

sustainability sustainability

risk Costa Rica risk Latin America

India 20

Hungary

Debt to Average Maturity, 2020 (% of GDP)

Colombia Turkey

Croatia

Romania Croatia

Indonesia Hungary Sri Lanka

South Africa

Philippines Brazil

Poland 15

Malaysia

Thailand Czechia Morocco

Angola

Low High Belarus

Chile Ecuador

inflationary risk inflationary risk Poland

Low debt Low debt 10

sustainability sustainability Dominican R. Oman

Malaysia

risk risk Ukraine

Mexico Kuwait

India Colombia

Turkey Qatar

Romania Thailand South Africa

Sources: National statistics, IMF, IIF, Bloomberg, IHS Markit, Allianz Research Uruguay Philippines

5

Saudi Arabia

16 EMs have announced and 13 of them have actually Indonesia

Chile

Kazakhstan

Peru

Azerbaijan

embarked on ‘QE’-like monetary stimulus in the wake of Russia

Covid-19. Some of them could see rising inflation 0

-10 -8 -6 -4 -2 0 2 4 6 8 10 12

and/or difficulties to roll over peaking maturing public Projected Interest Rate–Growth Differential, 2020–21 (%)

debt

© inAllianz

Copyright 2021-2022. Paucity of policy mix is an issue. Sources: IMF, Allianz Research 44ASIA-PACIFIC: BENEFITTING FROM CHINA’S EARLY

RECOVERY CANNOT BE THE FULL STORY

Drivers of growth: domestic (horizontal External drivers: trade openness & Domestic drivers: monetary impulse and

axis) vs. external (vertical axis) exposure to reshoring policy leeway

Trade openness (% of GDP) Monetary impulse change (pt)

10

VNM 0 0.5 1 1.5 2 NPL ratio (%)

TWN HKG 0.0

8

SGP JPN

More restrictive to foreign

CHN 0.1

KOR 6

KOR TWN VNM

investment

MYS AUS JPN

0.2 4

IND THA NZL IND

MYS

THA 2

IDN 0.3

PHL IDN

0

MYS

JPN

TWN

HKG

IDN

IND

THA

AUS

NZL

PHL

VNM

CHN

SGP

KOR

PHL

0.4

Size of bubble represents Covid-19 situation and shock.

Sources: Various, Euler Hermes, Allianz Research Sources: Various, Euler Hermes, Allianz Research Sources: Various, Euler Hermes, Allianz Research

The recovery path is determined by the South Korea, Taiwan, Vietnam, HK and On top of that, their policy response has

epidemic situation, the size of the shock Singapore could benefit from China’s been comparatively more restrained.

in H1 2020, exposure to external drivers early recovery. India, Indonesia and the The policy leeway is smaller, due to

of growth, and the strength of domestic Philippines are comparatively less structural issues.

drivers.

© Copyright Allianz open, and could struggle more to attract 45

foreign investment.EMERGING EUROPE: FROM SUPPORTIVE TO

OVERHEATING?

Monetary policy accommodation M2 growth (% y/y) Public debt (% of GDP)

Rate cuts since March Rate cuts in Jan-Feb Czechia 72% 2021f

Hungary

Current policy rate (rhs) Gov. bond purchases Hungary

25% 50% 2019

(% of GDP; rhs) Poland Slovakia 56%

-900 9% Romania

-800 8% 45%

Croatia Poland 55%

-700 7% 20% Turkey (rhs) 40%

-600 6% 35% Romania 50%

-500 5%

-400 4% 15% 30%

Czechia 39%

-300 3% 25%

-200 2% 10% 20% Bulgaria 25%

-100 1%

0 0% 15%

Turkey 42%

100 -1% 5% 10%

Ukraine

Turkey

Czechia

Slovakia

Poland

Romania

Bulgaria

Russia

Croatia

Hungary

5% Russia 23%

0% 0%

18-01 19-01 20-01 0% 20% 40% 60% 80% 100%

Sources: Sources:

CEE countries do not have much room for interest rate cuts anymore. Cyclical revenue weakness along with

Poland, Croatia and Turkey need monitoring with regard to government bond fiscal stimulus will widen fiscal deficits

purchases by the CBs. M2 growth has already accelerated in these countries. and increase public debt-to-GDP ratios.

Looking ahead, this could raise inflationary pressures in 2021-2022. Yet, those ratios should remain in

InCopyright

© Hungary Allianz and Romania, QE-like stimulus has been small so far. check, except for Hungary. 46 46EMERGING EUROPE: WITH EUROPE OR AGAINST IT?

Unemployment rate (%) Russia: Isolated in the long run? Turkey: Continued BOP crisis

20 Poland Czechia Hungary Potential new / intensified Western 15% Net ext. bank borrowing

Turkey Russia Croatia sanctions, with firms linked to the Kremlin Net portfolio inv. inflows

being the most likely targets, due to: Net FDI inflows

10%

Current account balance

15 1. Alleged poisoning of Alexei Navalny

(most prominent leader of Russia’s 5%

independent opposition).

10 0%

2. Involvement in Belarus crisis – events

that resemble those that occurred in

Ukraine in 2013-2014. Like then, -5%

5

Russia will not back down on its

interests. -10%

0 -15%

2016 2017 2018 2019 2020 2021 00 02 04 06 08 10 12 14 16 18 20

Re-balancing of trade and investment

Sources:

flows to Russia away from Western

Soft FX controls already in place, but no

Diverging paths depending on virus countries towards China will continue in

excessive capital controls expected.

development and responsiveness to the next years. Such a shift was already

Europe’s recovery and policy activism. strong in the wake of the 2014 sanctions, Instead the policy interest rate should

Unemployment and inequality to rise in softened a bit from 2018, but is likely to eventually be hiked again by the end of

most vulnerable countries could cause intensify again in the next years (also 2020 to reign in the sliding TRY exchange

social unrest because of the China-U.S. tensions). rate. 47

© Copyright AllianzYou can also read