Manawatū District Quarterly Economic Update - September 2020 17 December 2020

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Manawatū District Quarterly Economic Update – September 2020 17 December 2020

Key messages • Economic performance is stronger than expected and the outlook for the local economy is positive; • High earnings growth, relatively strong GDP performance, and increased spending by households and businesses reflects the resilience of the local economy; • Trade and investment conditions have added substantial support to economic performance; • Labour force indicators are positive relative to expectation, but there has been impacts;

Key messages • The housing market continues to drive wealth while causing concern as house prices and weekly rents continue to rise; • Supportive monetary and financial policy is needed to support levels of investment in new residential properties (despite the hype). Central and local government policy also have an important role to play; • Rebounding expenditure on vehicles by firms and households reflects confidence in the local economy; • Trade conditions exceed expectation in 2020. Performance in 2021 will depend in‐ part on the recovery of global economic activity, and; • Housing our growing population and central government legislation will present challenges and opportunities in 2021.

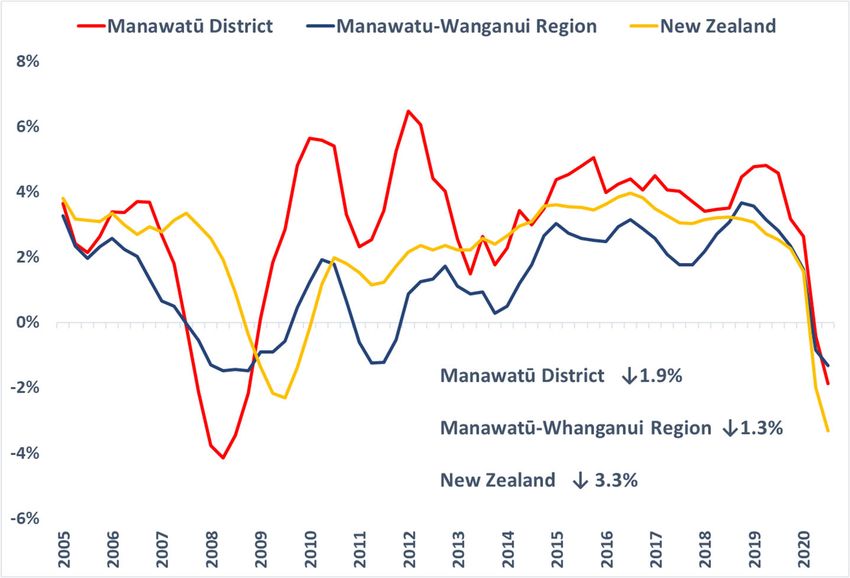

Annual GDP contracts as expected

Worst affected Annual GDP

change

Queenstown‐ ↓ 7.7%

Lakes District

Westland District ↓ 5.4%

Auckland ↓ 4.9%

Rotorua District ↓4.9%

Christchurch City ↓ 4.2%

Hamilton City ↓ 3.5%

Waitomo District ↓ 3.5%

Grey District ↓ 3.5%

Wellington City ↓ 3.3%

Kaikoura District ↓ 3.2%

Quarterly GDP bounces back as expected

2020 quarter vs

same quarter

Quarterly GDP change the previous

% year

Ruapehu District +20.5% +2.9%

Whanganui District +10.2% ‐+2.0%

Rangitikei District +9.4% ‐1.3%

Manawatū District +10.1% ‐2.3%

Palmerston North

City +9.1% ‐1.2%

Tararua District +10.8% 2.4%

Horowhenua District +20.2% 1.7%

Manawatū‐

Whanganui Region +11.3% ‐0.1%

New Zealand +12.3% ‐3.2%

Queenstown‐Lakes

District +35.6% ‐9.3%

Auckland +9.0% ‐7.1%

Earnings ↑ 9.4% in Q3 2020 vs Q3 2019

• Council Change in annual

earnings %

Horowhenua ↑ 10.7%

Manawatū ↑ 9.4%

Whanganui ↑ 9.2%

Tararua ↑ 8.5%

Rangitikei ↑ 8.4%

Manawatū‐ ↑ 8.0%

Whanganui Region

Palmerston North ↑ 6.1%

Ruapehu ↑ 4.9%

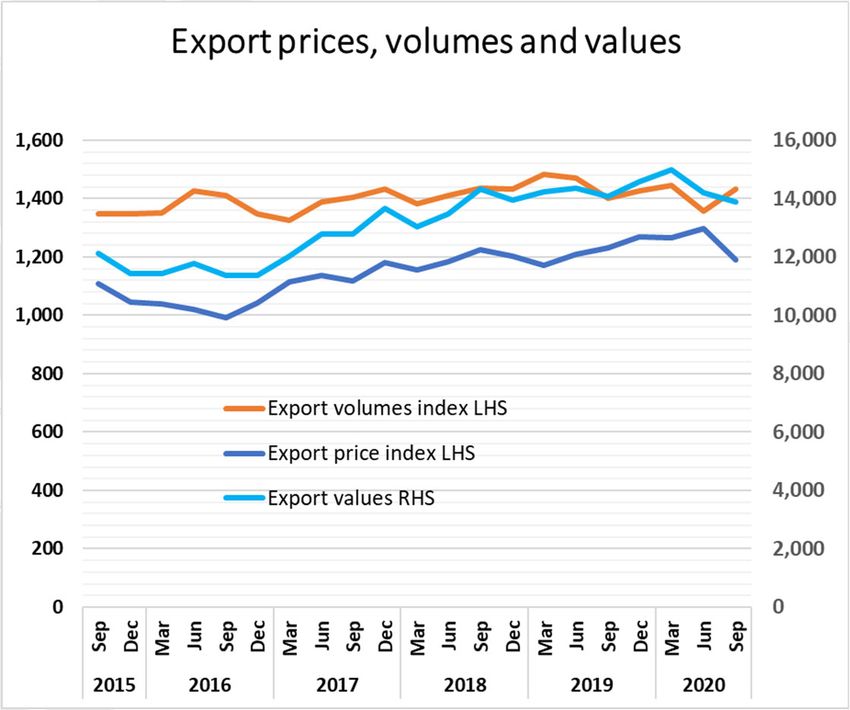

Trade continues to support economic performance

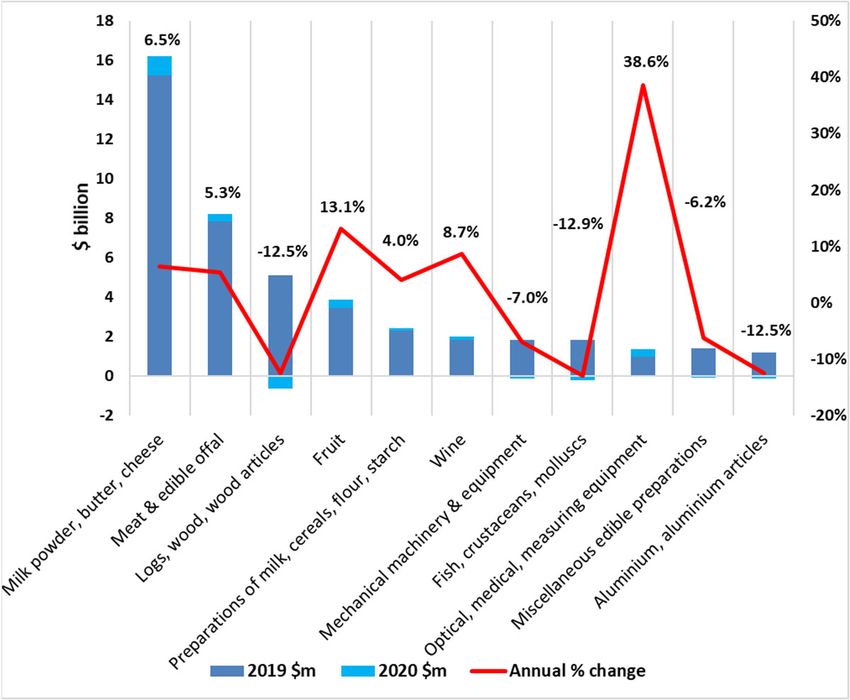

Annual export values continue to grow despite challenges

• The value of exports to the year ended October

↑ 1.2% to a total of $60.1b;

• The annual value of dairy and red meat exports

increased by 6.5% and 5.3% respectively. The

value of fruit exports ↑ 13.1%.

• Indicating a change in fortunes, the value of

forestry sector exports ↑ 9.8% over the quarter,

and ↑ 22.1% for the October month.

• The value of exports to China and the USA

increased by 2.7% and 15.2% respectively over

the year. Exports to Taiwan also posted strong

growth ↑ 9.8% YOY.

• The value of exports to Australia ↓ 6.4% over the

year while exports to India ↓ 28.5%.

$4b + of investment support the regional economy

Development $ million Timing

Manawatū Gorge 650 start January 2020

Linton and Ohakea regeneration plan 660 2019 - 2035

Mercury Energy - Turitea 450 2019 - 2021

Massey University capital plan 230 2020 - 2030

Powerco growth and security projects 245 2017 - 2024

Hokowhitu campus redevelopment 90 - 135 started late 2019

NZTA PN regional road & Napier Road cost and timing to be confirmed

NZTA Otaki to North of Levin 817 2024 - 2029

BUPA retirement village 40 started 2017

KiwiRail regional freight hub cost and timing to be confirmed

MidCentral DHB acute services block 370 timing uncertain

MidCentral surgical and mental health 57 early 2021

Countdown distribution centre 66 2020 - 2021

Countdown supermarket 20 start 2021

Palmerston North new schools 60 2021 - 2030

Labour force indicators reflect the moderate impact of COVID‐19

• The District unemployment rate remains beneath the

Manawatū‐Whanganui Region

and NZ unemployment rate (2.8% vs 5.1%)

Change in the Labour Force – Sep 2020 vs Mar 2020

• The number of people of working age increased by

1,000 between March and September while 300 less

Working age population = 202,900 (↑ 1,000)

people were either working or available for work

• The underutilisation rate declined from 15.0% in the Workforce = 138,900 LFPR = Not in

Workforce =

June quarter to 12.8% in the Sept quarter (↓300) 68.4%

64,000 (↑

(↓0.5%) 1,300)

• There was 1,100 less people employed in the region in

the September quarter vs the March quarter

Employment Unemployment

• In contrast, there were 6,000 more people employed rate = 65.2% rate = 4.7% (↑

0.7%)

(↓ 1.0%)

in the September 2020 quarter vs September 2019

• Labour force changes are an important indicator and

Underutilisation

will continue to be monitored in detail. rate = 12.8% (↑

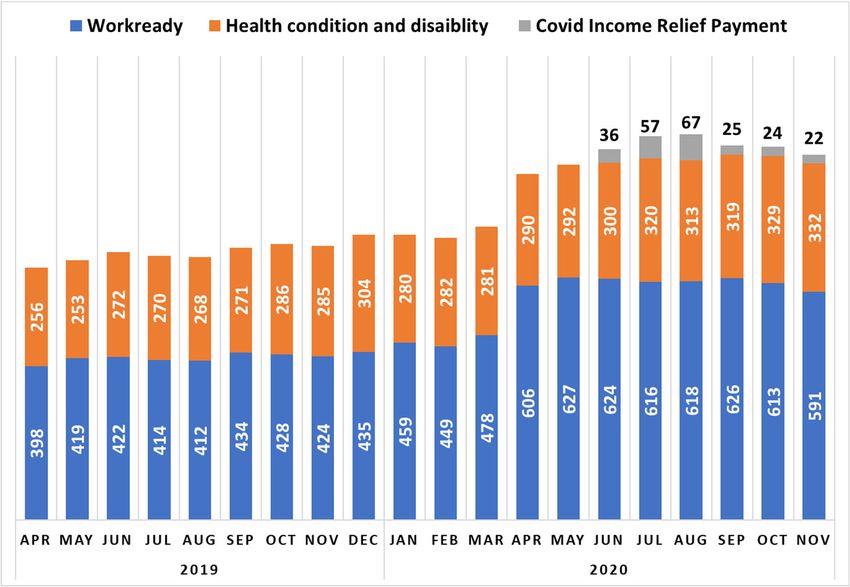

2.2%)Jobseekers decline while employment intentions remain strong • Total jobseekers and recipients of COVID Income Relief Payment ↓ 25 (from Sept) to 945 in November 2020; • Workready jobseekers ↓ 35, Jobseekers (health condi on) ↑ 13 and CIRP recipients ↓ 3; • To YE Nov, combined income payments increased by 236. This is ↑33.3% on Nov 2019 compared with ↑ 48.2% in NZ. • Job ads indicate strong local recruitment inten ons ↑31.5% on Feb 2020 vs NZ ↓ 6.9%.

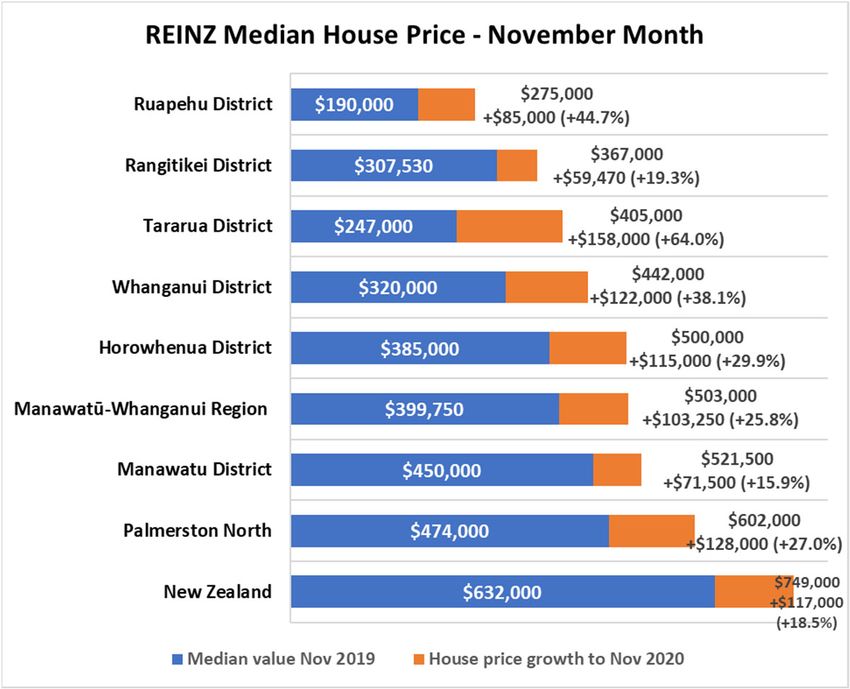

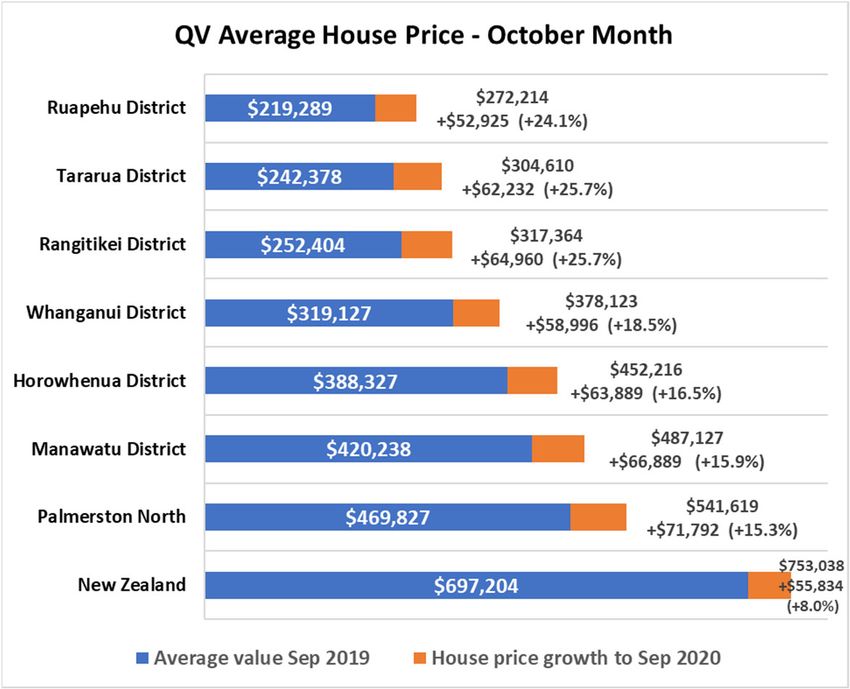

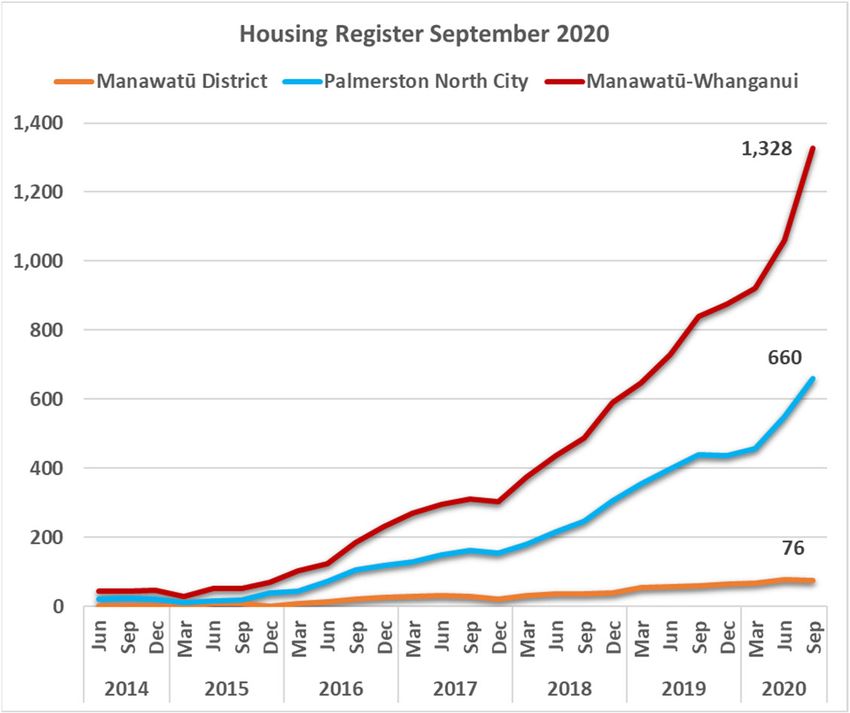

No slowing down in house price growth

New dwellings and construction investment holds up relatively well

Rental prices continue to grow while social housing demand plateaus

Annual retail spending ↑ 3.3% vs a ↓ 3.2% in na onal spending

Things to watch

• Trade conditions

• The impact of global economic restrictions on demand for NZ beef and lamb

• We will be watching this closely!

• Housing market

• Availability and affordability of housing

• Not as simple as hiking interest rates or imposing LVRs

• Legislative risk

• Climate Change Response (Zero Carbon) Amendment Bill and RMA reform

• NPS – Freshwater Management, Urban Development, Highly Productive Land

• Holidays (Increasing sick leave) Amendment Bill and Minimum wage increasesLocal industry strengths are driving economic performance • Food production, government employment, high levels of inward investment and limited exposure to international tourism have driven our strong economic performance; • Continued demand for our exports is crucial to local economic performance. Data will be watched closely; • Labour market data shows we have not escaped the impacts of COVID‐19, however, impacts have been substantially less than expected. Levels of jobs growth and strong employment intentions are positive; • Consumption indicators are strong and reflect the confidence of local businesses and households. This is particularly positive for the District and will support jobs and incomes in the services sector; • Cost pressures in the housing market and increasing rental prices continue to place pressure on vulnerable families. A comprehensive and well‐informed response is needed; and, • Central Government legislation is likely to impose additional costs and resource needs on local government and private businesses. The impacts and opportunities will also be watched closely!

You can also read