Markets: Bitcoin - the way of the future or another bubble?

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

May 2021

The Monthly Bulletin by

Markets: Bitcoin – the way of the future or another bubble?

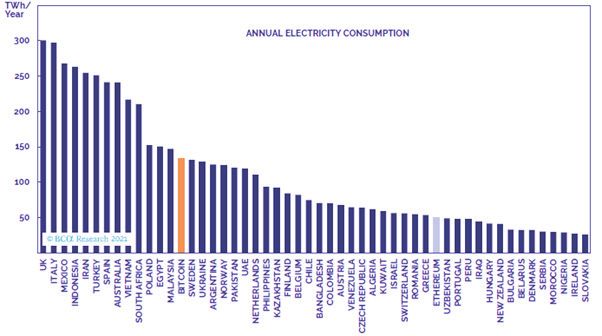

Tesla founder Elon Musk sent bitcoin tumbling after suspending all future bitcoin purchases

of Tesla vehicles. Musk described the cryptocurrency’s energy consumption trend as “insane”

and raised concerns about the “rapidly increasing use of fossil fuels for bitcoin mining and

transactions”. The People’s Bank of China (PBOC) reiterated that their institutions may not

use the virtual currency to price products or services – the growing Chinese crackdown is

intended to maintain financial stability but may also be intended to boost China’s state-

backed digital yuan. The US Treasury Department further announced that it will require any

cryptotransfer worth $10 000 or more to be reported to the IRS, noting that cryptocurrency

poses a significant problem by facilitating illegal activity. Both Musk and China are at the

forefront of caution on the back of concerns over a growth trend pointing to a potential

bubble, with the value of bitcoin having risen 300% in the last 12 months.

Following Musk’s comments and the US and PBOC crackdown, however, bitcoin fell to half of its April peak

of $64 869, touching $30 016. Tech shares, including Naspers, followed Bitcoin in its downward spiral. Prosus

announced that it intends to acquire 45.4% of Naspers shares by offering Naspers shareholders the option

to exchange their shares for 2.27443 newly issued Prosus shares. Based on estimates, Naspers’ SWIX weight

could halve to 12%, while Prosus’ SWIX weight could triple to 6%. Overall, the index would hold less exposure

to the Tencent Group, with the combined holding falling from 24% to 16%, leaving SA investors with less

exposure to China’s quickest-growing sector.

Chart 1: Bitcoin’s annual electricity consumption is “insane”.

Source: BCA

Sygnia Sygnals: May 2021 • Page 1

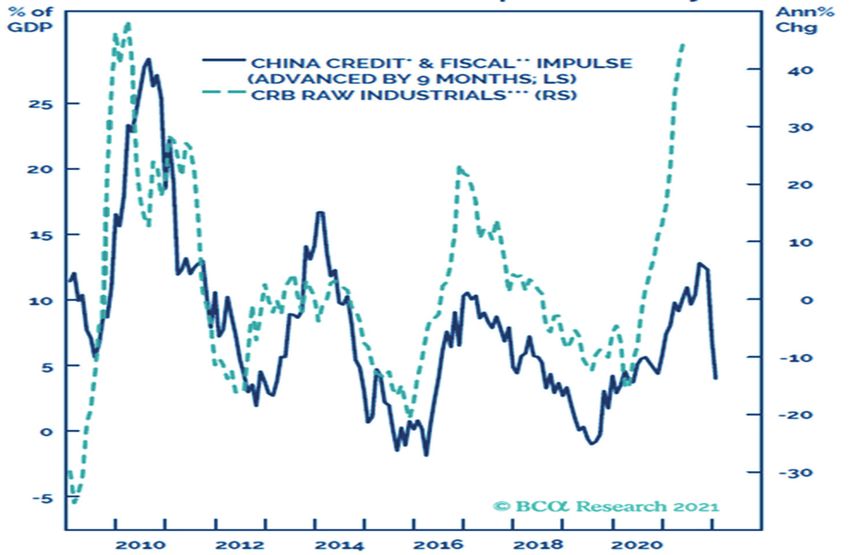

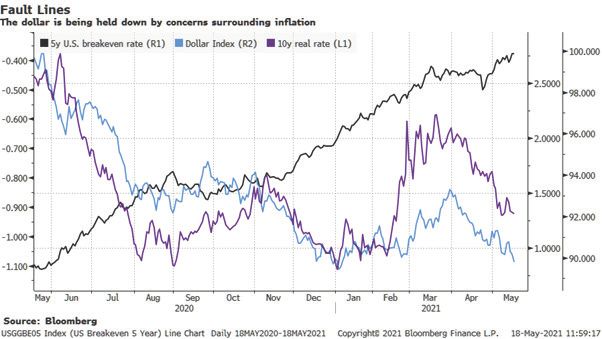

US – Are we facing a 70s revival in inflation? US inflation peaked at 14.7% in April 1980, with the economy experiencing “stagflation”, a nightmare scenario of weak growth and rising prices. US core inflation has now seen its biggest jump since 1982, resulting in US bond yields rising higher, along with the dollar, as investors push forward on expectations that the Fed will raise rates. Inflation, while much higher than expected, still looks transitory and has largely been concentrated in sectors that are re-opening and/or facing intense supply shortages. The normally cyclically sensitive components of CPI (rent and healthcare) continue to rise at a modest pace and wage growth remains stable. We are not facing a 70s revival in inflation, as the current backdrop differs from that of the 1970s and 1980s in many ways: the growth rate is much higher as economies reopen and stimulus takes effect; inflation is much lower due to improved central bank credibility; and there is no supply stress from spiking oil prices. With the employment rate still over eight million short of pre-pandemic levels, we expect the Fed to maintain its dovish line, even as inflation continues to rise over the rest of the year. The Fed will not lift rates until the labour market reaches full employment, which means that interest rates are unlikely to rise until 2023. However, treasury yields will continue to rise as inflation continues to flow through in the short term. Risks to the inflation outlook are multiple, and we will be monitoring those risks closely to confirm the transitory nature of the inflation. Chart 2: US dollar weaker on lower real yields. Source: Bloomberg China – Growth expected to slow, commodities at risk Chinese regulators warned steel mills that steel prices were too high and threatened punitive action if they engaged in pricing activities. Several Chinese exchanges have already raised transaction fees to curb speculative activity, reflecting the PBOC’s desire to reduce financial risks rather than stimulate the economy. China’s credit data surprised to the downside in April, continuing to indicate a reduction of stimulus and a slowing of the economy. Aggregate financing declined to CNY1.85 trillion from CNY3.34 trillion. The firming global growth backdrop will allow Chinese policymakers to reduce support as part of China’s ongoing change of its economic model from reliance on foreign trade to reliance on domestic demand. China’s old economy is likely to start slowing in the third quarter, with commodities particularly at risk of a correction as a result of China’s policy tightening. Sygnia Sygnals: May 2021 • Page 2

Chart 3: China’s leading indicator suggests commodity demand will drops Source: BCA South Africa – Energy continues to constrain growth Eskom announced stage two load-shedding as a result of more plant breakdowns, just as the Pretoria High Court of South Africa awarded the National Prosecuting Authority’s investigating directorate a restraint order valued at R1.4 billion against former Eskom executives and contractors. In addition, allegations of corruption around the use of floating power plants and the R255 billion contract scored by the Turkish company that owns them continue unabated. Despite the focus on Eskom since the introduction of load-shedding more than 13 years ago, the energy availability factor has continued on a downward trend. Chart 4: Eskom’s energy availability factor (EAF) has plunged over the last decade. Source: Eskom medium-term systems adequacy outlook 2020 SA – Vaccine rollout halted The rollout of the second phase of South Africa’s Covid-19 vaccination programme started on Monday, 17 May 2021, but the country moved to an adjusted level two lockdown on Monday, 31 May due to rising infections, with the Free State, Northern Cape, North West and Gauteng already experiencing a third wave. SA currently only has 1.3 million doses in the country ready to be administered, despite having agreements in place for 50 million doses. As at Monday, 31 May, just under 1 million vaccines (963 876) had been administered. Sygnia Sygnals: May 2021 • Page 3

In other news, ANC Secretary-General Ace Magashule is taking the ANC to court following his suspension in

early May, with ANC Deputy Secretary-General Jessie Duarte scathing in her dismissal of Magashule’s attempts

to retain his position, describing his legal argument as “absurd and incoherent”. Speaking decisively in May after

Magashule’s suspension, President Cyril Ramaphosa summed up the situation in a nutshell: “For as long as we

are divided as leadership, for as long as we fail to act against corruption, and unless we put the needs of our

people first, we will struggle to restore the credibility of the ANC.”

Former president Jacob Zuma had his own appeal shot down in the last week of May, when the Constitutional

Court dismissed his appeal against an estimated R10 million costs order. The R10 million legal bill is related to

Zuma’s efforts to challenge the constitutionality of the State Capture Inquiry. The matter was struck off the roll

and dismissed with costs, adding to his financial woes.

Key take-aways

After initial indications of a quick recovery post-2020, markets seem to be slowing somewhat. A slowing

economy in China, a drop in tech and an apparent bubble in cryptocurrency all point to a wait-and-see

approach for investors.

Locally, the South African Reserve Bank has cautioned that the slow vaccine rollouts and an imminent third

wave could see the pandemic last well into 2022 in South Africa. We’re not out of the woods yet – not by a

long shot.

Key indicators

1 mo. 3 mos. 6 mos. 1 yr. 2 yrs. 3 yrs. 5 yrs. 10 yrs.

J203T FTSE/JSE All Share Index 1.6% 4.2% 20.9% 38.1% 14.0% 10.0% 8.0% 11.0%

J200T FTSE/JSE Top 40 Index 1.1% 3.1% 19.8% 36.1% 15.0% 10.8% 8.3% 11.0%

J210T FTSE/JSE Resources 10 Index -1.4% 2.9% 31.7% 49.3% 30.1% 24.6% 21.1% 5.7%

J211T FTSE/JSE Industrials 25 index 0.9% 1.1% 10.6% 26.2% 14.2% 8.3% 5.2% 14.4%

J212T FTSE/JSE Financials 15 Index 9.2% 12.3% 23.1% 41.3% -6.4% -2.4% 2.2% 9.5%

J403T FTSE/JSE SWIX Index 1.3% 4.2% 18.9% 35.4% 10.2% 7.0% 5.7% 10.5%

J433T FTSE/JSE Capped SWIX Index 2.9% 7.6% 23.2% 40.8% 9.9% 6.1% 4.7% -

J303T FTSE/JSE CAPI Index 2.6% 6.4% 23.4% 41.2% 14.2% 9.8% 7.8% 11.0%

J253T FTSE/JSE SA Listed Property Index -2.9% 9.8% 31.2% 37.3% -13.8% -10.9% -7.3% 4.9%

ALBI JSE All Bond Composite Index 3.7% 3.0% 6.4% 11.1% 8.8% 8.4% 9.8% 8.4%

STeFI STeFI Index 0.3% 0.9% 1.8% 4.1% 5.5% 6.1% 6.7% 6.3%

MSCI World Index in SA Rands -4.1% -0.6% 2.9% 9.4% 18.7% 17.4% 11.2% 18.3%

Rand/US Dollar Exchange Rate -5.4% -9.4% -11.3% -22.2% -3.1% 2.6% -2.7% 7.3%

Rand/Euro Exchange Rate -3.9% -8.8% -9.4% -14.5% 1.4% 4.1% -0.8% 5.5%

Rand/Pound Exchange Rate -2.9% -7.9% -5.6% -10.5% 2.8% 4.9% -3.0% 5.7%

Headline CPI 0.7% 2.0% 2.6% 4.4% 3.7% 3.9% 4.3% 5.0%

PPI 1.3% 2.8% 3.4% 5.2% 4.3% 4.9% 4.7% 5.5%

Sygnia Sygnals: May 2021 • Page 4You can also read