Monthly Market Commentary - Unique Wealth

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Monthly Market Commentary

August 2021

Where We Are

Because it was the time of several of his great military triumphs, including the conquest of Egypt, the month

originally called Sextilis (in Latin) was renamed in 8 BC in honor of the first Roman Emperor, Augustus (63

BC-14 AD). Originally named Gaius Octavius, he was officially renamed Augustus (meaning “revered,“

“venerable,” “consecrated by augury,” or even “favored by the gods“) by the Roman Senate in 27 BC,

reflecting the unrelenting patience, skill, and efficiency with which Augustus overhauled virtually every

aspect of Roman life and brought durable peace and prosperity to the Greco-Roman world.

Given the “august” +17.0% year-to-date gain in the S&P 500 index through the end of July — as shown in

the chart on the following page, when the index advanced +2.3%, its sixth consecutive monthly advance —

investors may do well to keep in mind that despite August’s +7.2% total return in 2020, over the past 30

years, August has turned out to be the second worst performing month, declining an average -0.2% in total

return over the 1991-2020 time frame. As shown in the chart below, over the three decades from 1990

through 2019, August and September on average (not always) have generally produced lackluster returns

for the S&P 500 index.

Also worth noting in the accompanying table on the following page is the past five months’ sluggish

performance of the Russell 2000 index of small and mid-capitalization companies. After significantly

outperforming the S&P 500 index in January and February, the Russell 2000 index has not matched the S&P

500 index in any month since, and actually retreated -3.6% in July.

Past and projected performance

1

does not guarantee future results.

MARKET COMMENTARY - AUGUST 2021

Monthly and Year-to-Date Price Performance

YTD

Index/Commodity Jan. Feb. Mar. Apr. May Jun. Jul. (through 7/30)

S&P 500 -1.1% +2.6% +4.2% +5.2% +0.5% +2.2% +2.3% +14.4%

Nasdaq Composite +1.4% +0.9% +0.4% +5.3% -1.5% +5.5% +1.2% +12.5%

Russell 2000 +5.0% +6.1% +0.9% +2.1% +0.1% +1.8% -3.6% +17.0%

Gold -2.6% -5.9% -1.6% +3.6% +7.9% -7.3% +2.6% -6.5%

West Texas Int. Oil +7.5% +18.0% -3.8% +7.3% +4.4% +10.8% +0.6% +51.4%

Source: The Wall Street Journal, and Yahoo Finance.

The multi-month lackluster performance of the Russell 2000 index may be ascribed to a puzzling, often

internally contradictory gallimaufry of factors, including, among them: (i) an increased concentration of

mainstream institutional and individual investors’ interest in the heavyweight big five “Atlas” or “Hercules”

stocks (Apple, Microsoft, Amazon, Facebook, and Alphabet/Google); (ii) continued focus by social media-

and discussion forum-based millennials on meme stocks and short-dated call options buying; (iii)

expectations of profit margin pressures owing to the fact that higher input and labor costs may not be able

to be easily passed on by Russell 2000-type firms in the form of price increases; (iv) assumptions that rising

interest rates, if they occur, would chiefly hurt small and mid-cap companies who borrow money since they

tend not to be as flush with cash and liquidity as the much larger enterprises; and (v) — especially when

viewed in conjunction with the meaningful declines in 10- and 30-year U.S. Treasury yields — perhaps a

message is being sent about the possibility of a larger-than-generally-anticipated deceleration in economic

activity in 2022.

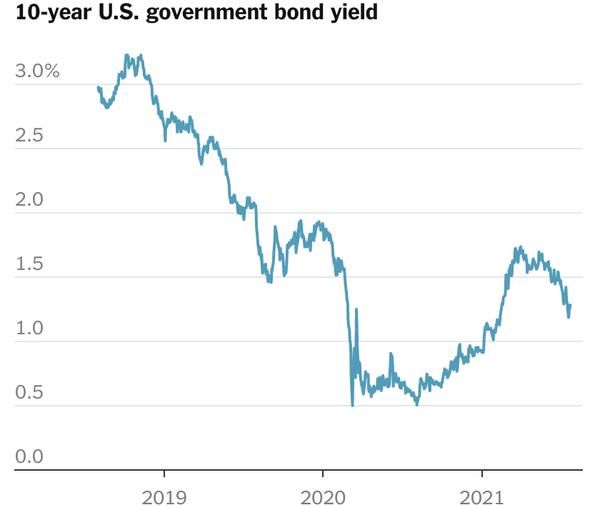

Speaking of mystifying, it would not be unduly exaggerating to observe that the course of intermediate- and

long-term U.S. Treasury yields over the past two months has wrong-footed a significant number of investors

and market commentators. After rising 11 basis points (0.11%) in June to finish the month at 0.25%, two-

year U.S. Treasury yields declined six basis points (0.06%) to close at 0.19% on July 30 th. More surprisingly to

many market participants, after declining 13 basis points (0.13%) in June to end the month at 1.45%, 10-

year U.S. Treasury yields (as shown in the accompanying chart) declined another 21 basis points (0.21%) to

close at 1.24% on July 30th. And equally baffling, after declining 20 basis points (0.20%) in June to wind up

the month at 2.06%, 30-year U.S. Treasury yields declined a further 17 basis points (0.17%) to close at

1.89% on July 30th.

Source: FactSet • By The New York Times

Past and projected performance

2

does not guarantee future results.

MARKET COMMENTARY - AUGUST 2021During July, following the course of declining U.S. Treasury yields, the U.S. dollar retreated -0.4% versus the

DXY index comprised of six major currencies (Euro, Japanese yen, British pound, Canadian dollar, Swiss

franc, and Swedish krona). On June 30, the DXY index was 92.44 and on July 30 th, the index closed at 92.09.

Over the course of the month, West Texas Intermediate crude oil prices rose +0.7%, from $73.47 per barrel

on June 30th to $73.95 per barrel on July 30th. With the global economy and global oil demand continuing to

gradually recover from the effects of the coronavirus pandemic, on the supply side: (i) facing pressure from

investors to moderate growth and address their emissions amid concerns about increasing regulations and

climate change, large U.S. and European oil companies continue to spend sparingly to boost production

despite higher prices; (ii) consolidating U.S. shale producers have exercised financial probity and exerted

capital spending discipline; and (iii) following the 19th OPEC and non-OPEC ministerial meeting in mid-July

(and a post-meeting ratification of new output quotas for selected countries), the group (which includes

Saudi Arabia, Russia, the United Arab Emirates, Kuwait, Iraq, and other countries) agreed to increase output

by a further 0.4 million barrels per day per month from August until December 2021, aiming to fully phase

out production cuts by September 2022.

Worrisome Developments

Possible Earlier-than-Expected Moves Toward Monetary Policy Tightening: As shown in the accompanying

chart, respondents to a Bank of America global fund manager survey expect the Federal Reserve to begin

hiking interest rates in the second half of 2022 or the first half of 2023. In addition, numerous major global

central banks besides the Fed appear committed to reducing stimulus — the European Central Bank, the

Bank of England, the Bank of Japan, the Bank of Canada, and the Reserve Bank of Australia. In late-July and

early-August media interviews, St. Louis Federal Reserve President James Bullard, Fed governor Christopher

Waller, and Fed Vice Chair Richard Clarida, among several other senior Fed officials, have begun to outline in

greater detail their thinking about a path toward more timely withdrawal of monetary policy support,

including: (i) the commencement of trimming the Fed’s $120 billion in monthly Quantitative Easing (money

printing to purchase U.S. Treasury and mortgage-backed securities); (ii) reducing this Quantitative Easing

rate to zero sometime in early 2022; and (iii) expressions of additional readiness to raise interest rates

earlier than anticipated if inflation threatens to remain too high for too long.

Past and projected performance

3

does not guarantee future results.

MARKET COMMENTARY - AUGUST 2021The Delta Variant of COVID-19: As shown in the accompanying chart, the share of all residents in each of

the 50 states who have been fully vaccinated against COVID-19 as of July 4th ranges from 29.89% (in

Mississippi) to 65.98% (in Vermont). In recent weeks, the Delta variant of COVID-19 has gained momentum,

with the most rapid rates of increase among the unvaccinated. The Delta variant is twice as transmissible as

the Alpha variant first recorded in England, which itself was 40% more infectious than earlier forms of the

virus first detected in China. While the Delta mutant of COVID-19 remains reason for caution, its likely

impact on economic reopening and recovery needs to take into account the low numbers of

hospitalizations and fatalities compared with infections. For the week ended July 30th, the Centers for

Disease Control and Prevention reported that the 7-day moving average for new cases reached 66,606,

more than quadruple the June 19th weekly figure and up +64.1% versus the prior week. According to the

World Health Organization, global infections have surged to an average of 540,000 a day, and an average of

almost 70,000 weekly deaths. Although highly unlikely to lead to anything approximating the severity of

closures and lockdowns experienced during the height of the pandemic in 2020, the Delta variant (and

possible additional variants, as the coronavirus third wave may create fertile breeding grounds for more

infectious and potentially vaccine-resistant new variants) has affected consumer, worker, teacher, student,

and parental psychology and behavior, thereby leading to a resurgence in hesitancy to engage in activities

considered to be high-risk (such as dining out, visiting shopping malls, working out in gyms, and attending

entertainment and sporting events), thereby slowing the trajectory of recovery and economic restoration. It

is worth keeping in mind that nearly 80% of Americans over the age of 65 — those at highest risk — and

60% of all adults are fully vaccinated. In fact, a silver lining of the summer 2021 Covid-19 surge may be an

intensified impetus toward even higher levels of vaccination, which would hasten the country’s progress

toward a more complete economic recovery.

Past and projected performance

4

does not guarantee future results.

MARKET COMMENTARY - AUGUST 2021Uncertain Course of Inflation: In June, the core — excluding food and energy prices —Personal

Consumption Expenditures price index (the Fed’s preferred measure of inflation) rose +0.7% month-over-

month and +3.5% year-over-year; the core Consumer Price Index rose +0.9% month-over-month and +4.5%

year-over-year (the highest rate of growth in 13 years); and the core Producer Price index rose +1.0%

month-over-month and +5.6% year-over-year (with the headline Producer Price Index up +1.0% month-

over-month and +7.3% year-over-year, its fastest rise since November 2010). Partly due to ongoing supply

chain disruptions, logistics cost pressures, and shortages of labor in certain sectors, inflation for the time

being appears to be somewhat more enduring than previously anticipated. In our opinion, inflation in fact

may not turn out to be so transitory, and while the U.S. economy is unlikely to return to the very high

inflation rates of the late 1970s, at the same time, to us it appears unlikely that consumer prices will return

to the 2%-and-below rates of price change prevailing in the years immediately preceding the coronavirus

pandemic.

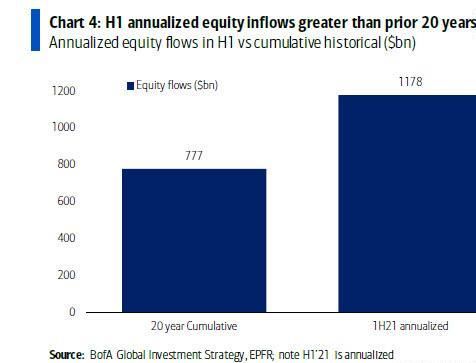

Broadening Evidence of Elevated Investor Bullishness: As shown in the accompanying chart, during the

first half of 2021, annualized equity inflows were greater than the cumulative amount of equity inflows in

the entire preceding 20 years. Data stretching back to 1951 from Ned Davis Research show that American

households had nearly 60% of their portfolios allocated to equities at the end of March 2021, a figure just

below the all-time high of 61.7% reached during the dotcom bubble of the late 1990s. According to Charles

Schwab Corporation, when households’ equity allocations have risen to 54.6% or higher, the average

annualized return for the S&P 500 over the next 10 years has been only +4.1%, as compared to the +10.3%

return the S&P 500 has averaged since 1965.

Past and projected performance

5

does not guarantee future results.

MARKET COMMENTARY - AUGUST 2021Taxes’ Potential Impact on Economic and Financial Activity: Although the final details of any additional

Corporate, Personal, Estate, and Capital Gains tax changes (to pay for some portion of the various

infrastructure initiatives) are not yet specified, when they do become clearer they are likely to influence

securities prices and financial market conditions. As shown in the accompanying chart, which depicts the

price return of the S&P 500 index six months before and six months after capital gains taxes were

increased, by far, the six months before capital gains are increased represent the periods of most risk to

equity prices. Taking an average of the 1975-1976, 1986–1987, and 2012-2013 equity market reactions to

episodes of capital gains tax increases, the S&P 500 index declined -1.3% in the six months before capital

gains taxes were increased and gained +17.9% in the six months after capital gains taxes were increased.

China’s Authorities Exercising Increased Control: Since November 2020, Chinese regulators have taken

more than 50 actual or reported actions in sectors including ride-hailing, food delivery, for-profit tutoring,

streaming, and online gaming aimed at realigning the relationship between private business and the

state. From a peak in February 2021 through August 5th, more than $1 trillion in aggregate market value

declines have occurred in the six largest Chinese technology companies due to regulatory edicts — relating

to issues including Variable Interest Entities (the precarious legal structure underpinning many of China’s

largest equity listings in the U.S.), monopolistic behavior, financial stability, and data security. Such

intensified regulatory assertiveness has increased equity market volatility and heightened risk awareness in

China and globally.

Reduced Affordability of Shelter: Against a backdrop of historically low mortgage interest rates, reduced

housing inventory levels, and the broadest global housing price boom in 20 years, the rising price of housing

for homeowners and renters has raised U.S. policymakers’ concerns about affordability: According to July

data from the S&P CoreLogic Case-Shiller index, national house prices in May were +16.6% year-over-year,

up from +14.8% in April, the largest rate of gain in more than three decades.

Past and projected performance

6

does not guarantee future results.

MARKET COMMENTARY - AUGUST 2021Constructive Developments

Currently Reasonable Expectations of Near-Term Monetary Policy: The Federal Open Market Committee

(FOMC) statement and Fed Chair Jerome Powell’s press conference following the FOMC meeting on July 27-

28th have for the moment confirmed financial market participants’ generally expected tapering timeline of:

(i) announcement in August or September of the tapering schedule; (ii) commencement of tapering

beginning in December 2021 or January 2022; and (iii) initial tapering likely projected at $10 billion per

month in U.S. Treasury securities and $5 billion per month in mortgage-backed securities. Fed Chair Powell’s

acknowledgment of higher inflation and admission that inflation may very well persist longer than initially

expected implies that, at least for now, the Federal Reserve continues to allow inflation to run above target

and actively seeks to escape a Japanese-style deflationary mire by promoting longer-term inflation.

Positive Corporate Profit Results and Sanguine Forward Guidance: During the 2021 second calendar

quarter earnings reporting season — even as Apple’s profits guidance was deemed somewhat disappointing

by investors — mega-cap tech companies Microsoft and Alphabet/Google reported very positive earnings;

equally significant has been the broadly positive revenue and earnings commentary and forward outlook

from reopening sectors including airlines, credit card companies, restaurants, and numerous other industry

groups leveraged to the economic recovery and reopening. As of August 6th, according to FactSet, securities

analysts were carrying the following forecasts for S&P 500 revenues and earnings, respectively: 1Q2021,

+10.9% and +52.5%; 2Q2021, +24.7% and +88.8%; 3Q2021, +14.4% and +28.0%; 4Q2021, +11.0% and

+21.4%; for the full 2021 calendar year, +14.3% and +41.6%, and for the full 2022 calendar year, +6.5% and

+9.5%.

Quickening Pace of Labor Market Gains: Following net employment gains of +614,000 jobs in May and

+930,000 jobs in June, the US economy added +943,000 jobs in July, with the unemployment rate declining

-0.5 percentage points to 5.4%. The July U-6 unemployment rate (a measure of all unemployed, marginally

attached, and part-time for economic reasons individuals as a percent of the civilian labor force plus all

marginally attached workers) reached 9.2% in July, down 0.9 percentage points from 10.1% in June, and

average hourly earnings increased +0.4% month-over-month in July and +4.0% year-over-year. The

Aggregate Payrolls Index (comprised of the average workweek, changes in employment, and wage growth)

gained +1.0% in June, +0.9% in July, and on a year-to-date basis, is rising at a +9.6% annualized rate. Even

though the U.S. economy remains a total of 5.7 million jobs below the pre-pandemic levels of February

2020, employment rolls have added +16.7 million jobs since the employment low point reached in April of

last year.

Healthy U.S. Economic Growth: Even though some mild hints of a reduction of economic momentum have

surfaced in some quarters of the economy, our view remains that the strong economic activity continues to

be supportive of risk assets including equities, commodities, private equity, and real estate. The July ISM

Services index reached an all-time record high of 64.1 versus 60.1 in June, and the July ISM Manufacturing

index registered a still quite strong 59.5 versus 60.6 in July. In its June 16 Summary of Economic Projections

report, the Federal Reserve was carrying the following median economic projections for U.S real GDP: 2020

actual: -3.5%; 2021 est.: +7.0%; 2022 est.: +3.3%; 2023 est.: +2.4%; Longer Run: +1.8%. And

following 1Q21 GDP growth of +6.3% annualized, the 2Q21 advance report of GDP (issued on Thursday, July

29th, with a revised report to be released on Thursday, August 26th, and the final report released on

Thursday, September 30th) came in at +6.5%, with the Atlanta Fed GDPNow estimate (as of August 6th) of

3Q21 GDP growth at +6.0%. It is at the same time worth keeping in mind that the global economy is likely

to experience GDP deceleration of varying magnitude in 2022 and beyond as economic growth slows down

Past and projected performance

7

does not guarantee future results.

MARKET COMMENTARY - AUGUST 2021from its recovery velocity to a steadier state.

Significant Excess Savings: As shown in the accompanying chart, the excess dollars saved above the average

monthly savings from January 2017 through February 2020 has reached $2.6 trillion as of the end of May

2021, representing significant liquidity available to be deployed into spending and investing — in the

present era of ultra-low and even negative interest rates (please see the Fixed Income Securities comments

in the Portfolio Positioning Section at the end of this Commentary).

Past and projected performance

8

does not guarantee future results.

MARKET COMMENTARY - AUGUST 2021PORTFOLIO POSITIONING

Portfolio Positioning Strategies:

In the current moderately slowing yet still robust economic expansion and softer yields environment, we

believe that careful thought, planning, and attention needs to be devoted to the investor’s most

appropriate forms and vehicles for implementing the fundamental elements of Asset Allocation and

Investment Strategy, which include:

i. Diversification: while it doesn’t guarantee a profit or ensure against a loss, diversification means

having sustainably low- and negatively-correlated investment exposures that truly counterbalance price

movements in other assets, particularly during times of great financial stress and/or market volatility;

ii. Rebalancing: which encompasses using concepts of reversion to the mean to trim exposures to assets

that have grown to represent too large a portion of the overall portfolio, while at the same time,

adding exposure to high-quality assets that have fallen out of investor favor and suffered significant,

though deemed not permanent, price declines vs. intrinsic value;

iii. Risk Management: which involves recognizing when markets have become consumed by meme

securities, momentum plays, “story stocks,” and information overload — a situation that has pertained

in recent months to more than a few companies in the technology space — and understanding the

degree of liquidity, the true pricing realism, and the appropriate roles of short-term liquid securities,

real assets, financial assets, and alternative assets in decades-long (or longer) regimes of inflation,

stagflation, deflation, monetary disruptions, and currency resets;

iv. Reinvestment: which encompasses knowing when to emphasize and trade off income versus capital

growth, all the while keeping in mind the critical importance of discipline, equanimity, patience, tax

awareness, and longevity in capturing and compounding dividend, coupon, rental, and other income

flows; and

v. Asset Protection and Husbandry: which encompass considerations of income and capital gains

taxation at the state, local, federal, and possibly international level; estate planning; relevant insurance

design and structuring; cybersecurity shielding; portfolio monitoring and reporting; administrative

costs; forms, frequency, and means of access; and custody.

Portfolio Positioning Principles:

We continue to allocate to a considered and considerable exposure to equities, with judicious shifts

between styles, sectors, geographies, and — where appropriate from a cost, timing, tax, liquidity, and size

standpoint — public versus private markets. Expressed below are a number of themes that we believe

should be taken into consideration over the next few years in selecting asset categories, asset classes, asset

managers, sectors, companies, and security types:

i. Paying Attention to the Value of Money: Taking advantage of (rather than being taken advantage of

by) the likelihood of money printing, internal and external currency debasement, government debt

monetization, and the ‘Modern Monetary Theory’ approach that to some degree in the pandemic-

response era has been pursued by the Authorities — within shifting money and credit cycles — to

service America’s massive explicit government and corporate indebtedness and the enormous implicit

obligations of pension and healthcare promises;

Past and projected performance

9

does not guarantee future results.

MARKET COMMENTARY - AUGUST 2021PORTFOLIO POSITIONING

ii. Concentrating on “All-Weather” Sectors and Companies: Seeking investments with balance and

flexibility, that are able to thrive regardless of: which political persuasion informs the thinking and

policies of the White House, Congress, and the regulatory authorities; evolving Environmental, Social,

and Governance (ESG) priorities and values; wealth distribution initiatives and public health conditions;

and wider socioeconomic trends;

iii. Distinguishing Between Temporary and Permanent Change: Focusing on the commercial and financial

implications of new social and political power structures, alliances, and geopolitical relationships; new

energy sources and resources; new trade patterns; new on- and offshoring channels; new “WFH” and

“WFA” (Work From Home and Work From Anywhere) employment modalities; and new business

models, pathways, digitalizations, and forms of person-to-person and business-to-business work,

leisure, learning, and wellness activity;

iv. Taking Advantage of Demographic Tailwinds: Through U.S. and select non-U.S. companies, gaining

exposure to, and meeting the rising needs, aspirations, and spending power of, the rapidly expanding

global middle class, especially in Asia;

v. Comprehending and Verifying Past Success: Emphasizing companies and sectors that have

demonstrated successful track records and past experience in: capital allocation; balance sheet

strength; risk management; sustainably defendable business models; and the ability to generate and

sustain high multiyear returns on equity (derived from revenue growth and favorable margin

preservation, rather than through overly high levels of leverage) meaningfully above the companies’

and sectors’ weighted average cost of capital; and

vi. Identifying Innovative and Disruptive Technology Hegemons: Focusing on technology enablers,

disrupters, and dominators in biotechnology, diagnostics and therapeutics based on CRISPR (Clustered

Regularly Interspaced Short Palindromic Repeats), weight management and wellbeing, public health,

medical nutrition, regenerative medicine, artificial intelligence, data analytics, machine learning, 5G

cellular network technology, the Internet of Things, infrastructure, robotics, retraining, quantum

computing, battery inventions, alternative energy, electric vehicles, and cybersecurity, while not least,

also taking account of the Environmental, Social, and Governance (ESG) characteristics of companies in

these and other fields.

Past and projected performance

10

does not guarantee future results.

MARKET COMMENTARY - AUGUST 2021Important Disclaimers and Disclosures

Unique Wealth (“Unique”) is a registered investment adviser with the Securities and Exchange

Commission. Any reference to the terms “registered investment adviser” or “registered” does not imply

that Unique or any person associated with Unique has achieved a certain level of skill or training. A copy of

Unique Wealth’s current written disclosure statements discussing our advisory services and fees is

available for your review upon request.

This message is intended for the exclusive use of clients or prospective clients of Unique Wealth. It should

not be construed as an attempt to sell or solicit any products or services of Unique or any investment

strategy, nor should it be construed as legal, accounting, tax or other professional advice. Different types

of investments involve varying degrees of risk, and there can be no assurance that any specific investment

will either be suitable or profitable for a client or prospective client’s investment portfolio.

This material is proprietary and may not be reproduced, transferred, modified or distributed in any form

without prior written permission from Unique. Unique reserves the right, at any time and without notice,

to amend, or cease publication of the information contained herein. Certain of the information contained

herein has been obtained from third-party sources and has not been independently verified. It is made

available on an "as is" basis without warranty. The content of this communication is provided solely for

your personal use and shall not be deemed to provide access to any particular transaction or investment

opportunity. Unique does not intend the information in this Presentation to be investment advice, and the

information presented in this communication should not be relied upon to make an investment decision.

The views expressed in the referenced materials are subject to change based on market and other

conditions. This document contains certain statements that may be deemed forward‐looking statements.

Please note that any such statements are not guarantees of any future performance; actual results or

developments may differ materially from those projected. Any projections, market outlooks, or estimates

are based upon certain assumptions and should not be construed as indicative of actual events that will

occur.

Historical performance results for investment indices and/or product benchmarks have been provided for

general comparison purposes only, and do not include the charges that might be incurred in an actual

portfolio, such as transaction and/or custodial charges, investment management fees, or the impact of

taxes, the incurrence of which would have the effect of decreasing historical performance results.

Past and projected performance

11

does not guarantee future results.

MARKET COMMENTARY - AUGUST 2021You can also read