SONAR Monthly Market Update - A deep dive into the freight markets with unprecedented - FreightWaves

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

SONAR Monthly Market Update

A deep dive into the freight markets with unprecedented

charts, analysis and market commentary.

February 2019 Edition

For distribution and use by FreightWaves SONAR seat licensed users only.

sonar.freightwaves.com

1

Table of Contents

1. Economic Outlook…….…………………………….……………………………….……………………………….………………...Page 3-4

2. Manufacturing……………………………..……………………..….……………………………….………………………………….Pages 5-6

3. Retail and Inventories…..………………..…………..……...……………………………….……………...…………..……….Pages 7-8

4. Labor Markets………………………...……………...……………………..….………….…………………….……………..……...Pages 9-10

5. Housing and Construction………..…………………………….…………………….……………….……………..…..…Pages 11-12

6. International Trade………...……………………………..……………………………………...……………..…………...…Pages 13-14

7. Pricing and Inflation…………………………………….………………………….…….……………..……….………..…….……...Page 15

8. Policy & Risks………………………………….………………………….………………………………...…………………….….….Pages 16-17

9. Freight Market Overview…………………….…………………….……………….………...…….…………….………Pages 18-25

sonar.freightwaves.com

2

Economic Outlook

Source: Survey of Professional Forecasters, FreightWaves Economics

Current Environment: Government shutdown clouds economic performance

Signs continue to point towards a slowdown in growth over the next couple of months, and

the recent government shutdown has added some additional uncertainty into the mix at the

start of 2019. The U.S. economy likely slowed during the 4th quarter of 2018 after impressive

growth in the middle of the year. Consumer spending is estimated to have continued to

drive growth during the quarter, but a smaller contribution from inventories likely caused

growth to moderate to round out the year.

In total though, 2018 impressed with full-year GDP growth estimated at 2.9%, matching 2015

as the strongest year of growth since the recession ended. More importantly, many of the

areas of the economy that drive freight demand did particularly well. Growth in industrial

output, retail sales, and trade all hit multi-year highs during the course of the year,

contributing to one of the strongest years for freight movements in recent memory

sonar.freightwaves.com

3

However, signs are already beginning to mount that suggest that economy is slowing down

at the start of 2019. Concerns over tariffs, global growth, and the strength of the U.S. Dollar

have darkened the outlook for export growth in 2019. Business investment demand appears

to have slowed significantly after strong growth, and will likely contribute little to growth

during the 1st quarter. Some of this is also likely connected to concerns over tariff policy, and

the recent plunge in oil prices should make matters worse for investment in the energy

sector.

Consumer spending remains the primary engine of demand in the economy, but even that is

showing some signs of slowing. After three straight quarters where real consumer spending

grew above 3.5%, household purchases are expected to take a hit during the 1st quarter. The

plunge in the stock market in December has taken some of the wind out of the sails of U.S.

households. Consumer confidence is starting to show some signs of concerns, and as a

result, consumers should spend at a more modest pace to start the year.

The recent government shutdown further complicates things during the 1st quarter. For one,

there is a direct impact on economic activity stemming from lost wages and productivity

from affected government workers. With the government reopened, some of this activity will

be made up in upcoming months as the government issues back pay. However, we still

expect that the shutdown cost the economy approximately 0.2% of GDP growth during the

quarter.

In addition, some of the government’s most important statistical agencies were forced to

stop releasing data during the shutdown. While many agencies, such as the Federal Reserve

and Bureau of Labor Statistics, secured their funding for the year before the shutdown took

effect, releases from both the Census Bureau and the Bureau of Economic Analysis were put

on hiatus. This affects several key indicators related to freight demand, including retail sales,

inventories, trade, and factory orders.

As a result, policymakers and market analysts have been forced to operate with an

incomplete view of the economy. This is a particularly challenging time to be without data,

with the economy shifting from the high pace of growth in 2018. Policymakers are currently

trying to assess the impact that tariffs are having on the economy and determine the

appropriate level of fiscal and monetary policy, and the lack of available data has complicated

the outlook. With the shutdown temporarily resolved, these agencies will begin releasing

data updates, but will likely be delayed in the near future as they deal with a backlog of work.

sonar.freightwaves.com

4

Manufacturing

In the industrial sector, i ndustrial production (IPROG.USA) growth again beat expectations

in December by advancing 0.3% from November’s levels. Year-over-year growth improved to

4.0%, down from the rapid pace of growth in the 3rd quarter but up slightly from November’s

results. Perhaps even more

impressive is that this gain came

despite a sizeable decline in

utilities production during the

month. Temperatures were

abnormally cold in November,

leading to a surge in heating

utilities during the month.

December’s decline is largely just

a normalization as the weather

returned to more regular

seasonal patterns.

Manufacturing industrial production, which excludes utility and mining production from

the total, surged in December. up 1.1% from November’s levels. This marks the largest

monthly gain in the manufacturing sector since February of 2018, and provides some relief

for a sector that looked to be stalling in the early parts of the 4th quarter. Year-over-year

growth in manufacturing production (IPROG.MFTG) jumped up to 3.2% in December, after

tumbling to 2% in the previous month.

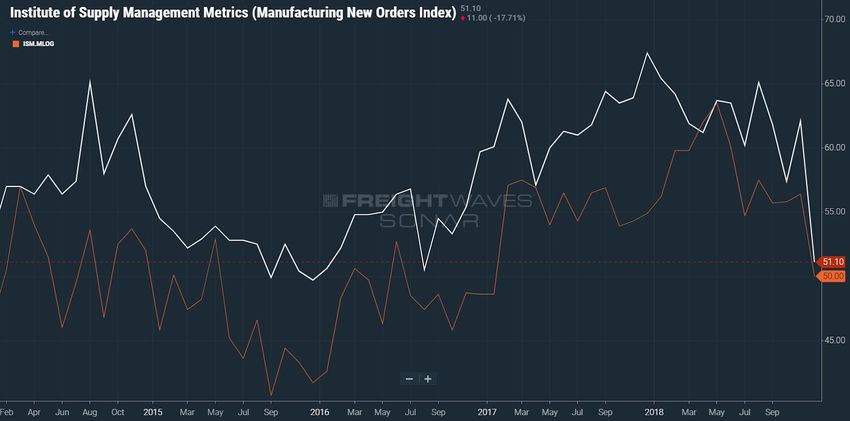

It is not quite all clear for the manufacturing sector, however. Survey data from the Institute

of Supply Management’ (ISM)

purchasing managers’ index

(ISM.PMI) from the

manufacturing sector

declined sharply in December,

falling 5.2 points to 54.1 during

the month. This marks the

lowest reading in the ISM

headline index since

December of 2016, and the

largest monthly decline since

October of 2008 when the

economy was in the throes of

the financial crisis.

sonar.freightwaves.com

5

Manufacturing (cont.)

Results from PMI data represent the percentage of survey respondents that report that

business activity is expanding, so numbers above 50 signal expansion in the manufacturing

sector. PMI data historically has a tight correlation with year-over-year growth in

manufacturing production, with readings above 55 signaling above average growth.

December’s results suggest that activity is still expanding in manufacturing overall, but the

sector has lost considerable momentum as we head into 2019.

A look at the details in the ISM

data gives some insight into

where this loss in momentum is

coming from. The biggest

decline in December came from

the N ew Orders c omponent of

the index (ISM.MNEW), which

dropped 11.1 points during the

month. This would suggest that

upcoming demand for

manufacturing production is

going to be growing, but at a

below-average pace. Backlogs of Orders (ISM.MLOG) also saw a significant drop during the

month, falling to the break-even reading of 50.0.

Putting together the pieces, this would suggest that much of the current production that

occurred in December was devoted to fulfilling previous orders and reducing the amount of

backlogs faced by U.S. manufacturers. The sharp decline in new orders points to slowing

demand growth in upcoming months.

It is worth reiterating that none of these readings point to a contraction. The manufacturing

sector still faces a number of headwinds for 2019, with slowing global growth, continued

policy uncertainty, and softening business investment demand, but general strength

throughout the year from consumer demand should keep growth positive in 2019. Moreover,

if the trade dispute with China is resolved favorably and in a timely fashion, there could be

some upside risk to the outlook.

sonar.freightwaves.com

6

Retail and Inventories

Updates on the retail and inventory environment were sparse throughout the month, as the

government shutdown led to delays in the release of retail sales and retail, wholesale, and

manufacturing inventories. This is particularly disappointing for retail performance, because

January’s scheduled release would have covered December activity, which is the busiest

month of the year for retail.

In the absence of hard data

on holiday season

performance, the longer term

outlook for the retail sector

remains largely the same.

year-over-year growth in

retail sales (RESLG.USA) has

come down from the

multi-year highs seen in

mid-2018, but remains

generally solid at 4.2%.

Most of the fundamentals for consumer spending remain generally strong at the start of

2019. Job growth surged in December of 2018, and weekly results from jobless claims

suggest that the labor market remains tight in January. Wage growth has also been

impressive in recent months, and should accelerate further as businesses look for workers in

a sparse worker pool. This combination of solid job growth and healthy wage gains has driven

retail performance throughout the past year, and should continue to underpin consumer

spending going forward.

There are a few reasons to be concerned about retail activity however, particularly in the

short-term. The recent collapse in equity markets in December has negatively affected

household wealth, and may lead to weaker consumer spending at the start of the year

There are also signs that suggest that this recent drop in the stock market is starting to affect

consumer confidence. The Conference Board’s consumer confidence index experienced the

largest monthly drop in over three years in December, and pushed down further in January.

The recent government shutdown likely played a role in pushing consumer confidence even

lower in January, as households are beginning to get concerned about the future state of

policy under a divided Congress.

There are also some longer-term headwinds that consumers will face in 2019. The Federal

Reserve has paused on interest hikes at the start of the year, but consumers will likely be

affected by all of the 2018 rate hikes this year. This is particularly true for larger purchases in

sonar.freightwaves.com

7

Retail and Inventories (cont.)

retail, such as automobiles and appliances, which are more sensitive to interest rate

movements.

In addition, the tariff situation with China is still unclear. Right now, much of the cost of

existing tariffs is absorbed by producers, but there remains the threat that the range of

targeted goods could broaden to include more consumer goods. The margins on these types

of goods are normally smally, and consumers would likely bear the brunt of these tariffs

should they go into place.

As a result of these factors, we still expect retail spending to be fairly strong in 2019, but will

likely not reach the pace seen in 2018. Consumers got a big boost in 2018 from favorable

conditions and a cut in taxes, but growth should return to a more normal pace in 2019.

On the inventory side, levels

have climbed steadily over the

past couple of months after

falling in the 2nd quarter of

the year. Due to tariff concerns

much of this inventory build

has been driven by US

businesses importing more

goods than they traditionally

would. This has caused

inventory/sales ratios to creep

up from the lows seen earlier

in the year. The total business

inventory-sales ratio

(TBIS.USA) reached 1.35 in October after hitting a multi-year low of 1.33 in the middle of the

year.

With the tariff situation still unresolved, companies are likely to be cautious about drawing

down at the start of the year. Once tariffs hit there should be a shift away from port volumes

and a rise in shipments from warehouses to retailers or manufacturers. When this happens,

inventory/sales ratios should continue to drift downward, resuming the trend seen in the first

half of 2018.

sonar.freightwaves.com

8

Labor Markets

As mentioned earlier, the primary support for consumer spending comes from strength in

the labor market. Healthy job growth fuels income gains in the economy, which in turn gives

households a foundation for spending.

The economy added an impressive 312,000 workers to payrolls in December, up from 179,000

in the previous month. This far exceeded consensus estimates of a gain of 184,000 and is the

strongest monthly gain since the 324,000 jobs added in February of this year. In addition,

data from both November and October were revised upward by a combined 95,000 jobs,

bringing up the average job growth for the fourth quarter to 254,000 jobs per month. During

2018, over 2.6 million workers were added to payrolls in the U.S. economy. That is up from the

nearly 2.2 million jobs added in

2017, and marks the best year of

job growth since 2015.

The results from 2018 are even

more impressive when you

consider that the labor market

was already fairly tight headed

into the year. The

unemployment rate has been at

or below 4% throughout most of

the past year, and well below

what most economist would consider the “natural” rate of employment in the economy.

Normally, as the labor market gets tight, employment growth tends to slow down as wages

rise. However, total employment (EMPS.NFRM) has risen at a fairly steady place over the last

several years, and has showed no signs of slowing down.

Much of this has been accomplished by drawing previously marginalized workers back into

the workforce. During the recession and early recovery years, many workers effectively

dropped out the workforce because they were so discouraged by job prospects. As wage

growth improved, these marginalized workers have rejoined the labor force and found

employment.

Going forward, the economy is going to transition from a high job growth, modest wage

growth environment to one with more modest job gains but better wage growth. As long as

economic growth in the economy remains at or above trend, labor market conditions will

remain tight and this shift should continue in upcoming quarters.

sonar.freightwaves.com

9

Labor Markets (cont.)

It is worth noting, however, that employment is typically a lagging indicator of economic

activity. With trouble in some of the other areas of the economy and policy uncertainty still

quite high, the economy is expected to cool and could bring the pace of hiring down with it.

Despite the general strength in hiring in the economy, job growth in the transportation and

logistics sector stumbled in December, as employment grew by just 2,200 during the month.

The main culprit was a 5,200 job decline among couriers and messenger services, which is

mostly parcel companies such as UPS and FedEx. However, several transportation industries

struggled during the month, with most registering job growth below 1,000 in December.

Within the transportation sector,

the trucking industry performed

relatively well by adding 2,900

workers to payrolls during the

month. This marks the eighth

consecutive month with positive

job growth and puts trucking

employment (EMPS.TRUK) 2.5%

higher than at this point last year.

For the year, the trucking

industry added 36,600 jobs in

2018, up from 9,400 added in 2017

and is the best year for hiring within trucking since the 50,400 jobs added in 2014.

The pace of hiring in the trucking industry has outpaced the rest of the economy for several

months now, which has helped to ease the capacity crunch from where it was earlier in the

year. In fact, with the economy expected to slow, the concern i s that the industry may be

adding capacity for demand growth that may not be there much longer.

The drop in hiring by parcel companies probably does not mean much in the grand scheme

of things. The decline comes on the heels of strong hiring in the previous couple of months,

which would suggest that parcel companies simply ramped up their hiring for the holidays

earlier than they normally would. Parcel companies did well with on-time delivery during the

holiday surge, and an earlier holiday ramp up in hiring would have helped achieve that.

Courier and messenger employment is still over 9% higher than it was at this point last year

and is one of the fastest growing industries in the entire economy.

sonar.freightwaves.com

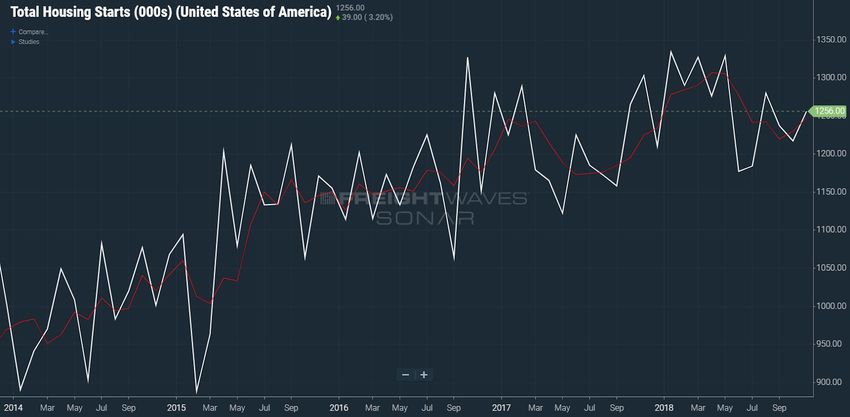

10Housing and Construction

Housing and construction data has been another area that has been impacted by the

government shutdown, as updates on the value of construction put into place, housing

starts, and new home sales were all delayed in January. The little data that has been available

has not been positive, leaving little reason for optimism about the housing sector in 2019

On the construction side, h

ousing starts (HOUS.USA) have been significantly affected by

weather related disruptions

over the past few months.

Hurricane season followed by

wildfires in California have

caused some significant

swings from month-to-month,

making it difficult to discern

the underlying trends in

construction. For the

short-term future, we expect

that there is still some

significant pent up

construction that will be

taking place over the next couple of months, as weather-affected areas continue to rebuild.

However, home building activity still faces some significant structural challenges that will

constrain activity going forward. Potential builders still face constraints from a lack of skilled

workers and a shortage of developed lots to build on. Once the weather-related fluctuations

settle, these longer term constraints will continue to affect the pace of home building. We

expect that the pace of housing starts will gradually improve in 2019, but should remain

relatively subdued.

On the demand side, sales have also been generally disappointing over the past year. Sales of

new home sales from December are not yet available, but existing home sales plummeted

to end the year, raising some real concerns about the state of home buying going forward.

Sales of previously-owned homes fell 6.4% in December from November’s levels to a 4.99

million annualized pace. This marks the first time that the pace has fallen below 5 million

units in over three years and is a whopping 10.3% from December 2017.

The lack of available inventory for purchase remains a key issue for existing home sales.

Home building activity has been weak, so potential buyers are having a hard time finding

homes for

sonar.freightwaves.com

11Housing and Construction (cont.)

purchase. This, in turn, has pushed up prices in the economy throughout the course of the

year and further affected demand. Rising mortgage rates may also be curbing activity. The

pace of home price appreciation has eased in recent months but the 30-year mortgage rate

has increased by 60 basis points throughout the course of the year. This has further affected

the ability of potential consumers to purchase a home.

Lastly, the recent change in the tax code contained some provisions that were unfavorable to

homeowners. Specifically, the limits placed on the amount of property taxes that can be

deducted from taxable income have removed some of the incentives for purchasing

higher-end homes, particularly in high property tax states in the Northeast.

This combination of rising home prices, higher mortgage rates, and unfavorable changes to

the tax code have created a difficult environment for home buying activity. As with

construction, these issues are not disappearing any time soon, so expect home purchasing

behavior to advance at a slow pace in upcoming quarters. The H ome Purchase Sentiment

Index (HPSI) collected by Fannie Mae has trended steadily downward since early-2018, falling

to the lowest level since the start of 2017 in December. This would suggest that the problems

facing the housing industry

The softness in home buying has begun to affect some of the connected industries in retail.

Home buying typically drives remodeling and renovation spending, as well as additional

spending on home furniture and household appliances. Retail spending on building

materials and appliances have seen growth in 2018, but have lagged behind overall retail

spending in the economy. It is through these channel that home sales affects freight

demand in the trucking industry, and weakness on the home sales front combined with

softness in home building has negative implications going forward.

sonar.freightwaves.com

12International Trade

Like housing, much of the data updates on the state of trade have been delayed by the

government shutdown. Monthly trade figures are captured by the Census Bureau, while the

Bureau of Economic Analysis reports quarterly results on real exports and imports as part of

the GDP release. The shutdown began just days before a scheduled release of November’s

trade results, so for now, the official trade data runs only through October.

This is an unfortunate development for the trade sector, because the lack of data comes just

as analysts are looking for signs of tariff-induced swings in global trade patterns. Data from

on both goods imports growth (GOIMG.USA) and goods exports growth (GOEXG.USA) has

been volatile over the past several months, as buyers and shippers in the international trade

arena have shifted away from normal season in an attempt to minimize the impact of tariffs.

Despite these abnormal

fluctuations, growth in trade has

remained generally strong

throughout the past year, with

both import and export growth

remaining elevated after

moderating from multi-year

highs earlier in 2018

Signs are emerging that suggest

that the pace of trade growth is

slowing at the start of the year,

however. Data from both China

and Europe point to a slowdown in economic growth in those two regions, particularly within

the manufacturing sectors. As a result the International Monetary Fund (IMF) r ecently

lowered projections for global growth for 2019. A global slowdown in economic activity is bad

news for U.S. exports, as this would translate into softer demand for U.S.-made products. In

addition, the general strength of the U.S. dollar has hampered export demand by making U.S.

products relatively more expensive for potential foreign buyers.

Survey data backs up this notion of slowing trade growth going forward. Within the ISM

manufacturing index, data on N ew Export Orders improved slightly in December, but

remains far below the levels seen early in 2018. This subcomponent in the ISM data has been

hovering around 52 over the past few months, signaling positive, but subdued growth.

sonar.freightwaves.com

13International Trade (cont.)

Historically, the New Export Orders component of the ISM (ISM.MEXP) index has a fairly tight

correlation with year-over-year growth in goods exports, and leads export performance by 1-2

months. The surge in export

growth in the middle of the

year was preceded by a similar

surge in export orders a

couple months earlier.

What this means is that there

may be a moderation in

export activity once

government data releases

resume in the trade sector.

Growth will likely remain

positive barring some sort of global growth meltdown, but the pace of growth should be

slower in 2019.

On the import side, import growth should be slightly stronger than exports, as the U.S.

economy is performing better than much of the rest of the developed world, and the strong

U.S. encourages imports into the country. Like exports, import volume has been subject to

considerable volatility, but given the fact that the U.S. economy itself is expected to moderate

throughout the course of the year, import activity should also be weaker in 2019 than it was in

2018.

For freight markets, this suggests weaker demand growth overall from the trade sector. Like

many other aspects of freight demand, 2018 was an overall impressive year for trade activity,

and as growth in the U.S. and the rest of the world slows and potentially protectionist policies

take hold, there should be less movement of goods between economies in 2018

sonar.freightwaves.com

14Prices and Inflation

Overall, signs from nearly every areas of freight demand point to softening growth headed

into next year. In addition, hiring trends within the industry suggest that trucking has been

adding capacity at a decent clip. As a result, trucking will likely feel less capacity-constrained

in 2019 than it did in 2018.

As a result, rate increases should calm somewhat within trucking. Year-over-year rate

inflation in the trucking industry is facing increasingly tough comparisons to last year, which

is going to put downward pressure on yearly gains going forward. Freight rates began their

surge last in August in the aftermath of Hurricane Harvey, and continued through the

impressive holiday season of 2017 and the ELD mandate. As a result, the tough comparisons

should lead moderating yearly

rate growth even if rates

continue to climb.

Despite this, data from the

Producer Price Index (PPI)

suggests that rate gains

continue in the trucking

industry. Producer prices for

General Freight Trucking

(PPIG.GFTK) rose 0.6 percent

in December on the heels of

another 1.3 percent gain in the

previous month. This pace has been enough to keep year-over-year rate inflation at or above

8.0 percent in recent months, registering 8.0 percent in December despite increasingly

tough comparisons to last year.

Gains during the month were almost entirely driven by long-distance truckload services,

which posted a third consecutive monthly gain above 1 percent with a 1.3 percent gain in

December. Long-distance less-than-truckload (LTL) and local trucking rates both

experienced declines during the month, though year-over-year growth held relatively stable

relative to recent performance at 9.8 percent and 4.7 percent, respectively.

This would suggest that carriers still retain some pricing power in this environment of

moderating demand,and have been able to extract higher rates across many different types

of freight. Year-over-year rate inflation probably will not reach the highs seen in the middle of

last year for quite some time, but the pace of rate increases is still well above average as we

head into next year. Longer-term, we expect that rate increases will settle in around 5%

year-over-year through 2019, though much of this depends on if the economy is able to

sustain a slightly above average pace of growth throughout the year

sonar.freightwaves.com

15Policy and Risks

Much of this outlook for above-average but moderating growth going forward hinges on the

policy environment in 2019, which at this point remains largely unsettled. Fiscal, monetary,

and trade policy have all entered into a period of uncertainty over the past view months, and

the path that policymakers choose will go a long way to determining growth during the year.

The p

artial shutdown of government operations thrust fiscal policy into the forefront early in

2019. The shutdown started in late-December and lasted a record 35 days before President

Trump signed a temporary funding agreement. This temporary agreement allows the

government to function as normal until February 15th, at which point either a more

permanent solution will be reached or the government will shut back down

As it stands, the shutdown in January already disrupted economic activity during the month.

Affected worked were either furloughed or forced to work without pay for the duration of the

shutdown. These federal workers will be receiving back pay now that the government has

reopened, but there are hundreds of thousands of contractors and businesses that interact

with the government that must simply deal with the lost business and wages during the

shutdown. In addition, the economy suffers from the lost productivity for workers that are

furloughed. The combination of lost productivity from federal workers and lost wages from

entities that interact with the government likely subtracted approximately 0.2% from 1st

quarter growth.

It is also worth noting that there was not much compromise involved in this temporary

agreement. President Trump agreed to reopen the government shortly after LaGuardia

airport was forced to shut down because federal air traffic controllers did not show for work.

However, the President seemly remains committed to his stance of requiring border wall

funding for any permanent funding agreement. As a result, we may soon find ourselves with

the same problems we had at the end of December when the shutdown first began.

Because of the drama surrounding the government shutdown, tariff policy took a bit of a

backseat in January. The U.S. and China entered into a temporary moratorium on escalating

their t rade conflict at the end of December. Negotiations have continued throughout the

month of January, but the two nations still apparently remain far from an agreement.

Chinese officials unofficially made an offer to eliminate their trade surplus with the U.S. by

ramping up purchases of U.S.-made goods, but concerns over intellectual property

protection and other non-tariff barriers have kept the two sides relatively far apart on a more

comprehensive agreement.

Unfortunately, the lack of a trade deal only serves to keep policy uncertainty high in 2019.

Survey data suggests that manufacturers and business owners are beginning to alter their

sonar.freightwaves.com

16Policy and Risks (cont.)

hiring and investment plans due to the lack of clarity on the trade front. The longer this drags

on without a resolution, to bigger the effect it will have on economic activity.

Oddly enough, the recent slowdown in activity in both China and the U.S. should help

negotiations going forward. As mentioned throughout, there are a number of different

factors that suggest that the U.S. economy is slowing down from the rapid pace seen in 2018.

By the end of 2019, the economy will likely be growing at a trend-like pace a will be less

capable of absorbing negative shocks from trade policy.

Conditions in China are far worse, as the Chinese economy slowed throughout 2018. For the

year, 2018’s growth of 6.6% was the worst performance in 28 years. China faces significant

structural challenges after years of debt-fueled overinvestment in their industrial capacity.

Manufacturing appears to be contracting already in the world’s second largest economy, and

export performance turned sharply negative at the end of the year. Against this backdrop,

China can ill afford additional complications connected to a trade dispute with the U.S.

Because of these concerns about fiscal and trade policy, the F ederal Reserve held interest

rates steady in the first meeting of 2019 for the Federal Open Market Committee (FOMC).

With inflation low, unemployment near historical lows, and signs emerging that growth is

slowing, the Fed may decide to hold off on rate increases entirely in 2019. For now, we still

estimate 1-2 rate hikes throughout the course of 2019 after four rate increases in 2018.

It is worth noting that there is a considerable lag between when monetary policy is enacted

and when it actually takes hold on economic activity in the economy. What this means is that

the economy next year will be affected by the rate increases that were put into place

throughout 2018, particularly for the housing and automotive sectors. Even if there are not

further increases from this point, much of the impact on 2019 growth have already been put

into place. Still, if the Federal Reserve decides to hold off on rate increases altogether, it

would give a slight boost to the economic outlook towards the end of 2019 into 2020.

sonar.freightwaves.com

17Freight Market Update

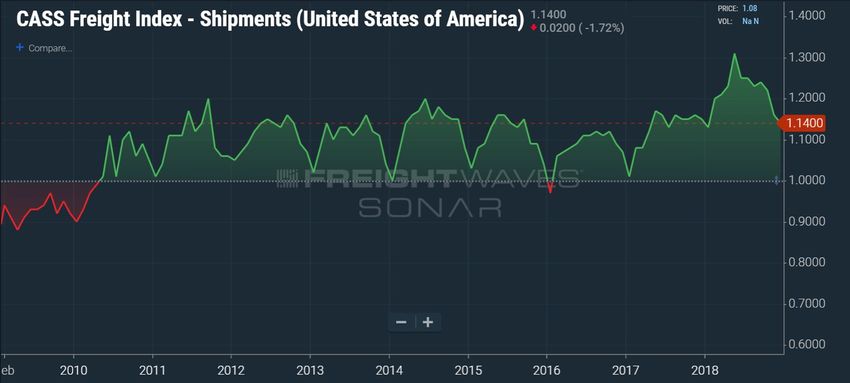

2018 may have started with a bang, but it ended with a fizzle as freight volume slid from the

beginning of December to the end. The Cass Freight Index for shipments was down

year-over-year for the first time since September of 2016 – December 2017 was 1.15 vs

December 2018 at 1.142. Though it was not a dramatic drop, it ended the longest streak of

consecutive monthly YoY increases this millennium of 26 months. It was the first 20-month

expansion since 2010-11 as the economy recovered from the recession. Prior to that there was

a 25-month streak from 2003-5. It should also be noted that the 1.142 value was the second

highest for the month of December in the last decade. December of 2017 being the highest.

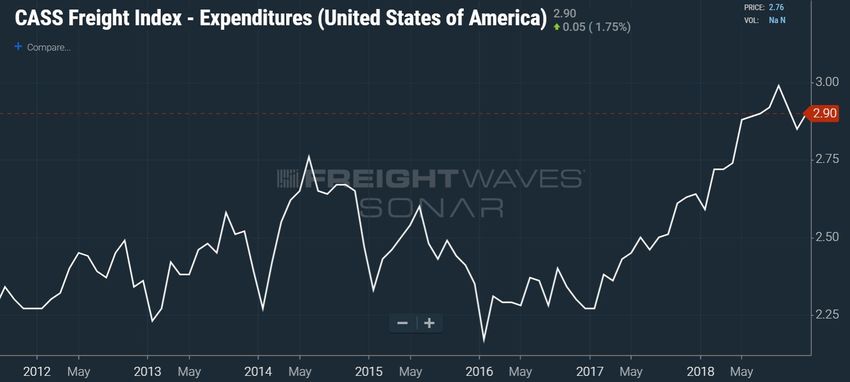

Even though volumes fell freight costs increased sequentially over November. The CASS

Freight Expenditure Index that measures the average total cost of freight including things

like fuel and other accessorial charges increased to $2.90 from $2.85. The index also measures

rail cost. It was the first monthly increase in the index since September. Holiday surges and

increased import volume due to tariff concerns and holiday inventory replenishments

certainly had an impact. The movement is a bit unusual, as it marks the second time in the

past six years for December to be higher than November. Last year being the other

occurrence as the market was heating.

sonar.freightwaves.com

18The National Tender Volume Index (OTVI.USA) fell over 11% from December 1st to the 23rd.

Characterized by a relatively smooth trendline, the OTVI did not take an erratic path to the

bottom. Volumes fell gradually and did not spike or drop significantly in a short time. With no

major occurrences in the market there was little disruption.

December freight volume is traditionally driven by retail demand and keeping store shelves

and distribution centers full. December of 2017 was characterized by unusually high freight

volume due to a busier than expected retail season and parcel carriers like UPS being caught

off-guard as capacity was already thin due to hurricanes and strong economic growth. On

sonar.freightwaves.com

19this note, seeing some contraction on a year-over-year basis was inevitable, but market

participants were far more prepared in 2018 as the general economy was also not quite as

bullish as it was a year ago.

With volume sliding, capacity was readily available outside of the week and a half leading up

to Christmas as drivers positioned themselves closer to home. The National Tender Rejection

Index dropped to 12.31% -- the second lowest value of the year at this point next to October

27th -- by the second week of December, and gradually increased to 13.25% over the next

seven days before shooting up to peak above 16.2% on Christmas. It is important to note that

the rejection rates climbed on lower volume, meaning that capacity would have been doubly

constrained had there been any late month surges.

Weather did not have a significant long-term impact in the U.S. freight market in December

with it being relatively warm in the eastern half of the country. This meant less snow cover for

trucks to deal with and less volatility in the market. Most of the disruption originated from

holiday availability as drivers were positioned closer to home for Christmas which drove

tender rejection rates higher around Christmas even though volume was declining.

sonar.freightwaves.com

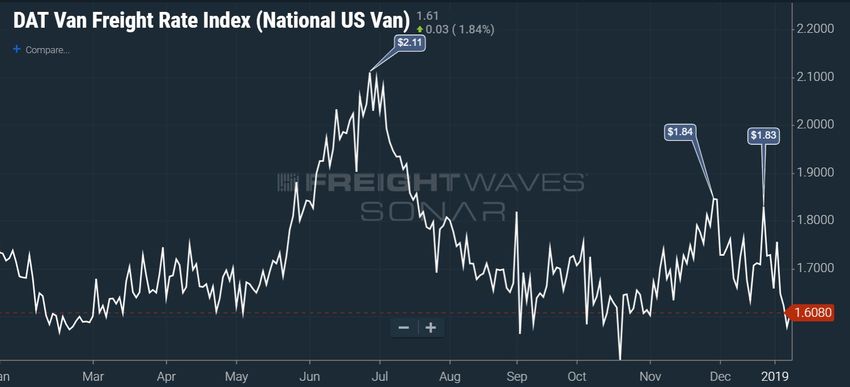

20Spot market rates were lower than a year ago as the DAT Van Freight Rate Index showed an

average rate for dry van truckload moves peaking around Christmas at $1.83 versus $1.941 in

2017. Another difference from a year ago is the fact the index shows us that spot rates

remained elevated for several weeks after Christmas whereas this year rates fell back

immediately following the holiday, another indication the freight market is much more

stable than a year ago.

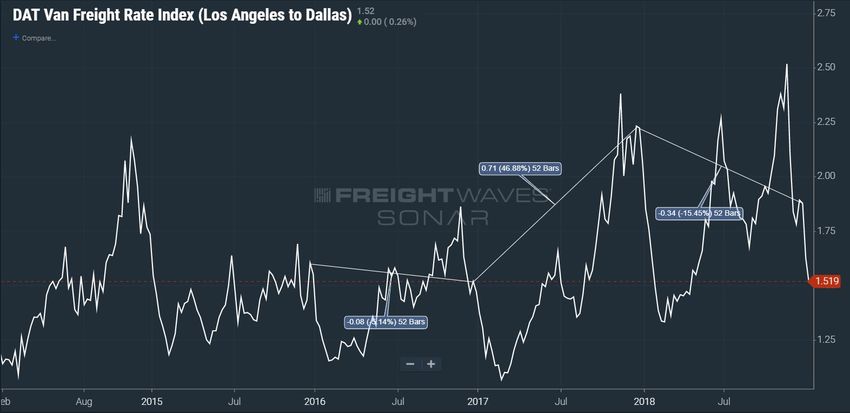

The Los Angeles to Dallas spot rate, which has been extremely volatile over the past 18

months, had a muted December peak value of $1.89 – 18% lower than 2017 at $2.23 per mile.

L.A. had been the hot market this fall as volumes surged from the overwhelming amount of

inbound container volume being pulled into the country in front of the tariff deadline that

was January 1st before being extended to March. While most of the country had been seeing

volume decline L.A. was still very active. December was the first month to have sequential

contraction in volumes since the June to July. Volume dropped roughly 12% from November

to December on average.

sonar.freightwaves.com

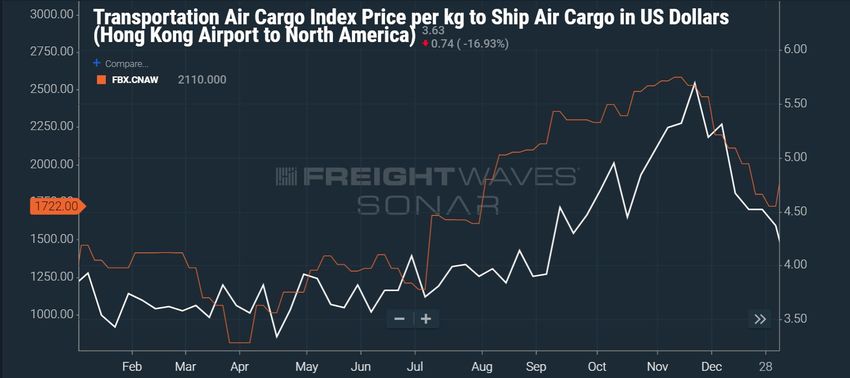

21The spot market for container rates which had been heated into mid-November also cooled

throughout December. The average rate for a 40-foot container from China to the North

American West Coast dropped 21% in December. The drop is not terribly unusual late in the

year, but it normally occurs earlier in the season with holiday inventories having already been

brought into the country in early November.

Pairing with the container flows, air cargo rates followed a similar pattern dropping about

18% in the Hong Kong to North America lane (AIRUSD.HKGNOA). Air cargo is a much more

expensive mode of transport than maritime shipping, so the freight tends to be more

sonar.freightwaves.com

22expensive so that it can absorb the cost. Items such as electronics and pharmaceuticals tend

to be correlated in this lane. The maritime lane got going earlier than air cargo which

traditionally peaks in November. This year the peak price was roughly 2.3% higher than in

2017.

With L.A. settling in December the Northwest corner of the country picked up the slack in

terms of volatility. Tender rejection rates in the region (OTRI.URNW) were extremely volatile

as the bulk of their produce season occurs in late fall. Christmas trees also move in earnest

around this time. One of the biggest factors leading to this was the fact L.A. had been the

place for carriers to go to find freight, pulling a lot of capacity south as reflected by the

steadily declining rejection rate in the West region (OTRI.URWT). West Coast rejection rates

had the smoothest decline in the country in December.

The Midwest was the other region of the country experiencing elevated tender rejection

rates, hitting above 20% most of the month, while the rest of the U.S. averaged 14-15%.

Volumes slid in the Columbus and Indianapolis markets, falling roughly 8% and 3 %

respectively. but the Chicago and Joliet markets fell much more severely throughout the

month, declining 22 and 14% respectively. Drivers being positioned for home-time were a big

factor in keeping tender rejections high on lower volume.

sonar.freightwaves.com

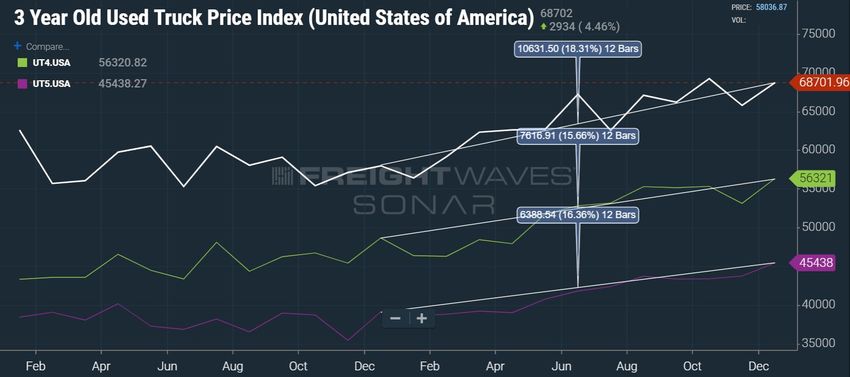

23Used Truck prices for 3 (UT3.USA) 4 (UT4.USA) and 5 (UT5.USA) year old models all increased

sequentially in December after 3 and 4-year models fell in November. This caps off a year

where all 3 values increased by 15-19% as demand for equipment went higher due to tax

break benefits and increased demand for capacity. Most large carriers reported very

profitable years, some even hitting record low operating ratios. This additional cash

combined with tax cuts increased demand for trucks that have lower maintenance expense.

Prices are expected to come back down as the market cools and tax breaks expire.

sonar.freightwaves.com

24Looking into early 2019, January has been a much quieter month than it was in 2018. Tender

rejection rates have fallen throughout the month even though volume was strong early.

There has been no indication of any significant additional inbound volume in front of the

tariff implementation to this point. Chinese New Year is just around the corner and

international shippers are running out of time, but they may have already made their move.

sonar.freightwaves.com

25You can also read