NORWEP Global Offshore Wind Report 2021 & Norwegian industry expectations - In collaboration with: Research by

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

NORWEP

In collaboration with:

Global Offshore Wind

Report 2021

&

Nor wegian industry

expectations

Research by:

Agenda

• Welcome - Jon Dugstad, Director Wind and Solar, Norwegian Energy

Partners

• Launch of NORWEP's Global Annual Offshore Wind Market Report with

new targets for the industry - Jon Dugstad, Director Wind and Solar,

Norwegian Energy Partners

• Key figures, opportunities and challenges in key global offshore wind

markets – Ronnie Quinn, Advisor Renewable Markets UK and Ireland,

Norwegian Energy Partners

• Tony Christian Tiller, State Secretary, Ministry of Petroleum and Energy

• Norwegian industrial growth opportunities in the European offshore

wind industry - Giles Dickson, Chief Executive Officer, WindEurope

• Discussion: How should the Norwegian supply industry engage in these

exciting opportunities? How can NORWEP and the wider Norwegian

support community help the Norwegian industry to become a leading

offshore wind contender on a global scale?

Norwegian Energy Partners Founders

Organisations

- Energy Norway

- Federation of Norwegian Industries

- Norwegian Oil and Gas Association

is an independent non-profit foundation established to strengthen the

- Norwegian Shipowners’ Association

long-term basis for value creation and employment in the Norwegian

- The Norwegian Confederation of

energy industry through facilitation of the industry’s international

Trade Unions

business activities.

Norwegian Government

- Ministry of Petroleum and Energy

We have 300 partners/company members from the Norwegian - Ministry of Trade and Industry

offshore, energy and maritime industries! - Ministry of Foreign Affairs

Industry

- Equinor

- Statkraft

| 3

NORWEP - what we do

Provide market and project information to

NORWEP partners and Norwegian industry at

large

Identify Norwegian competence and technology

that fit the needs of the global energy industry

Create relevant dialogues between the

Norwegian industry and international partners

and clients

Equinor Peregrino B

Ole Jørgen Bratland

Market Report and Offshore Wind Tool

Capacity of announced projects almost doubled in

2020

# Country Operational Secured Development* Total

1 Vietnam 99 783 64,919 65,801

2 China 8,524 24,824 30,237 63,586

3 United Kingdom 10,424 9,927 28,978 49,329

4 Brazil 42,537 42,537

5 Taiwan 128 5,167 36,229 41,524

6 USA 42 11,586 27,538 39,166

7 Sweden 191 36,766 36,957

8 Japan 61 146 36,162 36,369

9 Germany 7,653 3,125 10,552 21,330

10 South Korea 95 95 21,121 21,311

11 Ireland 25 21,023 21,048

12 Poland 5,933 12,804 18,737

13 Australia 15,887 15,887

The

14 2,620 2,682 6,100 11,402

Netherlands

33.9 GW 68.9 GW 430.4 GW 533.2 GW 15 Denmark 1,701 949 7,768 10,418

Operational Secured In development* Total 16 France 2 3,513 3,384 6,899

No change from Q1 ▲ 6.6% from Q1 ▲ 7.7% from Q1 ▲ 7.0% from Q1

*includes capacity without owners that is scheduled for

auction

Ranking based on total size of portfolio

6

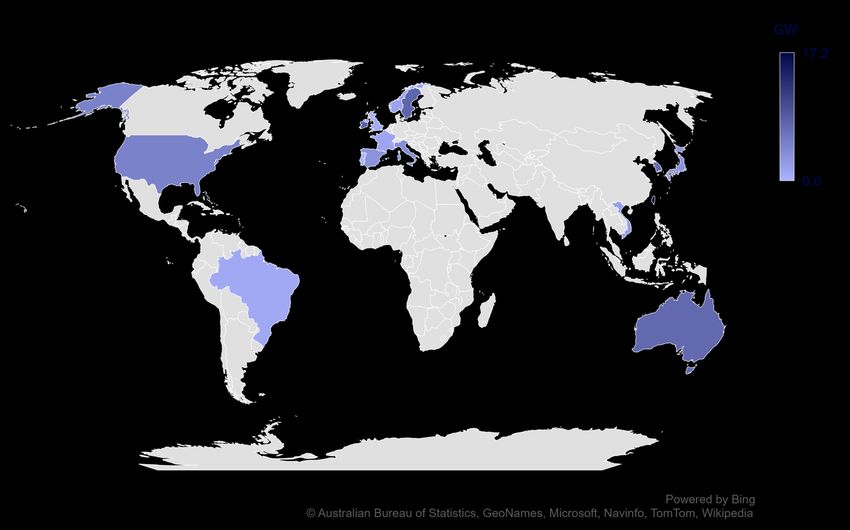

Utility scale floating wind emerge

Taiwan 17.2

Ireland 8.4

Sweden 7.8

Australia 7.4

South Korea 7.2

Key markets

USA 4.9

Italy 3.7

Other 13.3

0 5 10 15 20

GW

Operational Route to market secured Development*

InfraVest 7.4

Oceanex Energy 7.4

CIP 5.8

Aker ASA 4.4

Hexicon 4.0

Key developers

0.07 GW 0.15 GW 69.7 GW 70 GW Stonepeak 2.9

Operational Secured In development* Total Renexia 2.8

No change from Q1 No change from Q1 ▲ 34.4% from Q1 ▲ 34.2% from Q1

Other 25.6

0 5 10 15 20 25 30

GW

Operational Route to market secured Development**

7

Upcoming lease auctions*

Netherlands – 2021 Norway – 2021

*Does not include projects established by developers with a

The Hollandse Kust West auction will take The Norwegian government is currently

view to be tendered to new owners at a later date.

place in Summer 2021, with further formulating a competitive process to allocate Denmark – 2021

auctions to follow sites in the UN and SN2 zones, with a view to The Danish government will offer a reverse auction CfD

offer projects by the end of 2021. tender for the Thor and Hesselø wind farms in 2021.

Ireland – 2021

Prequalified bidders for Thor were announced in February

Ireland has scheduled an offshore wind

’21.

specific RESS auction for 2021. There is

speculation over whether it will be

launched by the end of the year. Lithuania – 2023

The Lithuanian government is preparing to

tender a 700 MW project with a provisional

auction date of February 2023.

New York – 2021 / 22

In 2021 BOEM specified call areas for

lease in the New York Bight and

announced an auction would be

launched in late 2021 or early 2022. Germany – 2021

Three sites with a combined capacity of 958

California - 2022 MW will be tendered in September 2021

After multiple delays to an auction

originally planned for 2019, BOEM

announced in 2021 it would ramp up

activity to lease areas off California in

Japan - 2021

2022.

Japan is expected to announce the

winners of ongoing tenders for both

North Carolina - 2022 fixed and floating areas in 2021 and

BOEM announced in 2021 that it would 2022. Further auctions are also

seek to launch a lease auction for WEAs planned.

offshore North Carolina in 2022, prior to

the implementation off a moratorium on

new leasing off the coast of the state from

Taiwan – 2022

2023.

The draft zonal development plan

for offshore wind in Taiwan

Confirmed lease France – 2021 / 2022 outlines auctions for 3 GW of

auctions Competitive lease auctions are currently capacity each year from 2022 to

underway at various stages for the 1 GW Belgium – 2023 India - 2022 2024.

Speculated lease Normandy fixed foundation project and The Belgian government has identified 1 GW lease had been

auctions the 270 MW Brittany I floating site. Both a second Marine Development Area for scheduled for 2019 but has

auctions will be completed in 2022. offshore wind leasing and is expected been delayed to 2022 awaiting

to auction three sites in the area in site inspections from LiDAR

2023. devices

8 8

10

11

Key developers • As early movers in the

offshore wind sector,

European utilities lead the

global portfolio ranking.

Iberdrola 29.2

Ørsted 28.7 • Increased competition from

oil majors and regional

Ocean Winds 20.8

developers.

CIP 19.4

RWE 14.0 • EPCI and institutional

wpd 12.8 investors are investing in early

Equinor 12.3

stage projects in line with

inherent developers.

Other 317.9

0 50 100 150 200 250 300 350 • Alliances are evolving – across

GW the world.

Operational Route to market secured Development**

12Technologies

• Fixed-foundation project development

33.9 continues to be the industry focus.

Fixed 68.7

• The first tenders to allocate a route to

360.7 market for utility-scale floating

foundation projects are due to take

0.1 place from 2021.

Floating 0.2

• Consistent deployment of floating-

69.7 foundation projects from 2025 is

expected to encourage further

0 50 100 150 200 250 300 350 400

development.

GW

Operational Route to market secured Development*Projects and turbines are getting bigger

Average project size by region and year Average wind turbine generator size by year

1.6 20 300

1.4 18

250

1.3 16

1.2

14

200

1.0 1.0

0.9 12

metres

0.9

MW

GW

0.8 0.8 0.8

0.8 10 18.5

150

17.0

0.6 0.6 8 14.5

15.4 16.0

0.5 0.5 0.5 100

0.4

0.5 0.5 6 11.6 11.6

0.4 0.4 0.4 0.4 0.4 0.4 9.5

0.3 0.3 4 7.7 7.8 7.7

0.3 0.3 0.3 6.2

7.4

50

0.2 0.2 0.2 5.5

0.2 0.2 0.2

2 4.1 4.3 4.1 4.3

0.1 0.1 3.0 3.2 3.1

0.1

0.0 0 0

Operational year Operational year

EMEA APAC (excl. China) Americas Avg. WTG rating (MW) Avg. rotor diameter (m) Avg. hub height (m)Boom!

• Capacity commissioned to close in on

230 GW i 2030

• A consistent stream of tenders and

capacity auctions will ensure more

35 250 projects secure a route to market

30.7 29.8 through to 2030 in the EMEA

30

200 • APAC commissioning expected to grow

23.9

25

Cumulative GW

22.2

GW per annum

rapidly with identified routes-to-

19.4 19.1 markets

20 150

15.0

15

13.7 • China project commissioning at

11.1 100 unprecedented rates as central support

8.5 8.1

10 6.1

is due to expire in 2022

3.5 4.2 50

5 1.5

• In the Americas a strong route to

market pipeline has been secured by

0 0 state-level authorities in the US

• Ambitious government targets will be

Year missed due to supply chain constraints

Cumulative EMEA China APAC (excl. China) Americas and administrative delays

15O ve ra l l ex p e n d i t u re i s s et t o r i s e

• An average global annual market

of 50 bn EUR in the early 2020s

will be worth 80-90 bn EUR

100 90.7 900

86.2 86.3 annually towards 2030.

90 800

75.8

80 72.8 700 • TotEx is forecast to fall in China

Cumulative EURbn

EURbn per annum

67.1

70 600 based on the current project

60 53.7

51.2

47.0 49.8 47.9 500 pipeline. The expected increase in

50 41.6 new development activity

400

40 following adjustment to updated

28.4

300

30 19.1 21.4 route to market mechanisms from

20 200 2022 is however likely to increase

10 100 expenditure in line with trends in

0 0 other regions.

• Supply chain bottlenecks and

Year

localisation requirements may

Cumulative China United Kingdom USA Germany Taiwan Japan Vietnam Other limit cost reductions.Europe maintains its pole position

Top 16 (Q2 2021)

# Country Operational Secured Development* Total

1 United Kingdom 10,424 9,927 28,978 49,329

2 Sweden 191 36,766 36,957

3 Germany 7,653 3,125 10,552 21,330

4 Ireland 25 21,023 21,048

5 Poland 5,933 12,804 18,737

6 The Netherlands 2,620 2,682 6,100 11,402

7 Denmark 1,701 949 7,768 10,418

8 France 2 3,513 3,384 6,899

9 Estonia 6,264 6,264

10 Italy 30 5,097 5,127

11 Norway 2 92 4,519 4,613

12 Belgium 2,261 2,040 4,301

13 Spain 5 2 3,197 3,204

14 Finland 68 740 808

15 Greece 714 714

25.0 GW 26.3 GW 151.4 GW 202.6 GW

Operational Secured In development* Total 16 Lithuania 700 700

No change from Q1 ▲ 6.6% from Q1 ▲ 8.0% from Q1 ▲ 6.7% from Q1

Ranking based on total size of portfolio

*includes capacity without owners that is scheduled for auction

17A short journey from Nor way

North Sea 80.4

Baltic Sea 52.2

Irish Sea 18.7

Gulf of Bothnia 10.6

Atlantic Ocean 9.8

Kattegat 9.3

Celtic Sea 5.7

Other 15.9

0 10 20 30 40 50 60 70 80 90

GW

Operational Route to market secured Development*

18Americas

• US market remained focused on

offtake solicitations and

permitting for late-stage

development projects.

• Brazilian early stage

development portfolio expanded

rapidly in 2020.

0.04 GW 11.6 GW 70.7 GW 82.3 GW • First offshore wind farm in

Operational Secured In development* Total Colombia was unveiled.

No change from Q1 ▲ 29.8% from Q1 ▲ 6.5% from Q1 ▲ 9.3% from Q1

*includes capacity without owners that is scheduled for auction

19# Country Operational Secured Development* Total

APAC ex. China 1

2

Vietnam

Taiwan

99

128

783

5,167

64,919

36,229

65,801

41,524

3 Japan 61 146 36,162 36,369

4 South Korea 95 95 21,121 21,311

5 Australia 15,887 15,887

6 Philippines 2,450 2,450

7 India 1,400 1,400

0.38 GW 6.2 GW 178.2 GW 184.7 GW

Operational Secured In development* Total

No change from Q1 No change from Q1 ▲ 9.3% from Q1 ▲ 9.0% from Q1

• *includes capacity without owners that is scheduled for auction or where owner

info is absent

20The Chinese dragon

# Country Operational Secured Development Total

1 Guangdong 1,022 9,934 21,333 32,289

2 Jiangsu 5,777 6,771 1,901 14,449

3 Fujian 129 3,619 1,855 5,603

4 Zhejiang 486 2,389 900 3,775

5 Shandong 1,205 1,803 3,007

6 Liaoning 303 400 1,199 1,902

7 Hebei 300 300 497 1,097

8 Shanghai 417 206 200 823

9 Tianjin 90 350 440

10 Hong Kong 200 200

8.52 GW 24.8 GW 30.2 GW 63.6 GW

Operational Secured In development Total

No change from Q1 No change from Q1 No change from Q1 No change from Q1

21An emerging Nor wegian offshore wind industr y Source: Multiconsult: Statusrapport Norges energinæringer (2020)

An annual 80-100 bn NOK worth of Nor wegian

offshore wind solutions

90 000 14.0 %

80 000

12.0 %

70 000

10.0 %

60 000

50 000 8.0 %

40 000 6.0 %

30 000

4.0 %

20 000

2.0 %

10 000

- 0.0 %

2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

Annual international turnover Norwegian supply industry market share

..with a 10% market share and more than 500 bn NOK deliveries in the period to 2030. 23What does it take?

• A number of large Norwegian suppliers engage successfully in offshore wind globally

• Norwegian based companies

• develop market and industry acumen and risk understanding

• increase offshore wind ambitions and deploy the necessary resources

• develop volume manufacturing skills

• establish scale in international markets in competition with established global supply chain

• Norwegian developers are active on the Norwegian and international shelf

• Norwegian developers and international partners on the NS adopts more Norwegian

solutions in projects globally

24Would you like to know more? www.norwep.com/wind

You can also read