NTG Morning Comments www.nesvick.com - Monday, June 14, 2021 - Nesvick Trading Group

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Monday, June 14, 2021

NTG Morning Comments

www.nesvick.com

Weather

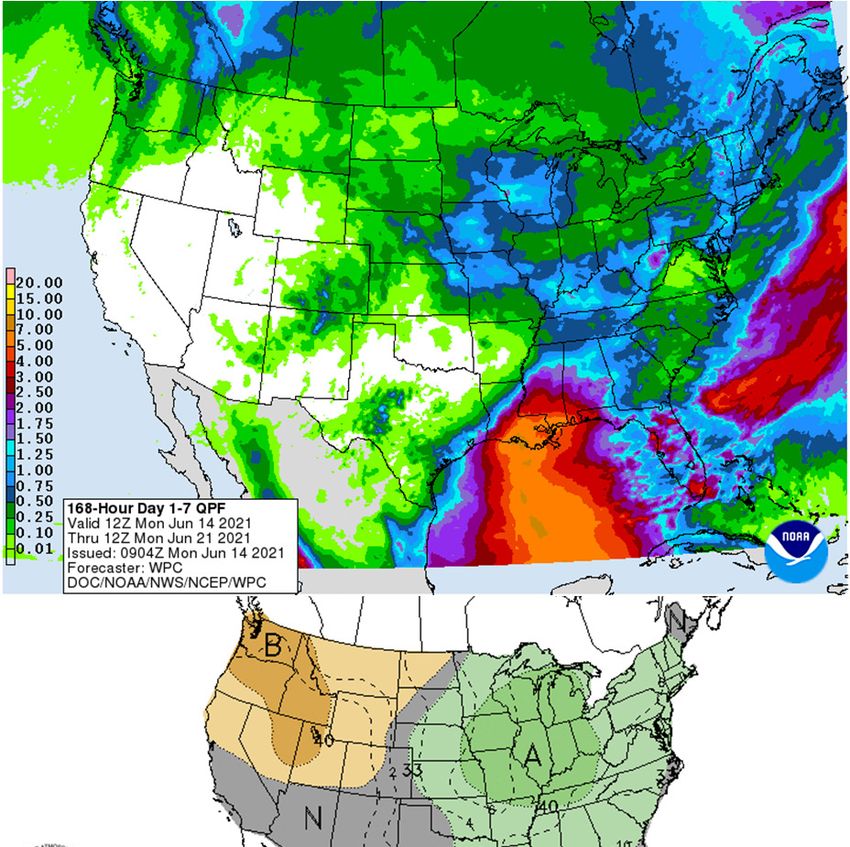

The weekend weather maps followed-through on

initial hints from late last week that the deferred

outlook was building better precipitation chances for

the Corn Belt. We should see mostly dry conditions

for another couple of days, but we should start to see

rainfall chances improve by Thursday with significant

rainfall chances developing during both the 6-10 and

11-15 day period. The 7-day QPF is shown at the right

and the vast majority of that rainfall in the Corn Belt

develops in the second half of the time frame. Odds

are that coverage of rainfall in the Corn Belt is a bit

overstated, but it is possible that actual rainfall

amounts in some areas could be understated. Note

the big rains shown along the Gulf Coast on the map.

These will come with a tropical system that will make

landfall probably sometime on Saturday with the

system moving east/northeast from there.

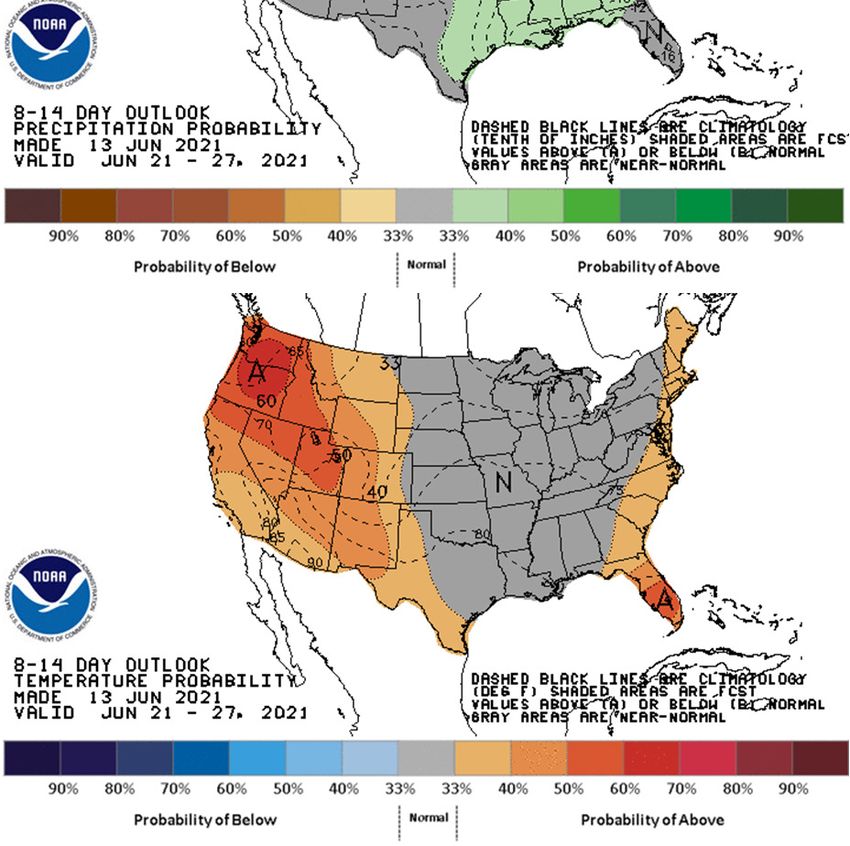

The 8-14 day map at the right that shows odds for

widespread above normal rainfall amounts through

the Corn Belt. Another big change in the forecast over

the weekend is a cooler outlook on temps. The 8-14

day map show to the right shows mostly near normal

temps for the vast majority of the growing regions.

The 6-10 day map actually features some below

normal temps possible for extreme northern portions

of the country.

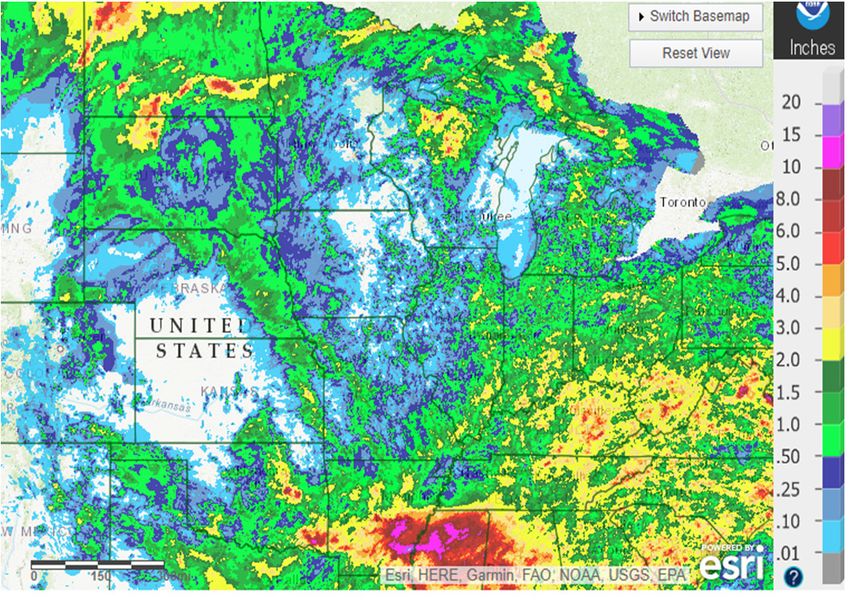

Map below shows precip over the past 7 days

1

Monday, June 14, 2021

NTG Morning Comments

www.nesvick.com

Crops

Thought we’d take a quick look at 20/21 corn export potential this morning. Last week WASDE raised their corn

export projection by 75 mb to 2,850 which was widely expected. The question is whether they have more room

to increase or not. Based on the analysis below, I’d argue there is further upside to the corn export figure.

The table is simply enough. At the top we have Sep-May Census export figures. We don’t have an official

Census projection for May this year yet, so I’ve simply plugged in my best estimate based on inspections. Below

that we have a history of outstanding export sales at the beginning of June each year, followed by total JJA

exports. I then compare JJA actual exports vs the outstanding sales level.

Monthly Census Corn Exports

10/11 11/12 12/13 13/14 14/15 15/16 16/17 17/18 18/19 19/20 20/21

Sep 174.7 121.7 92.1 80.9 159.8 132.5 245.5 138.6 208.3 80.7 149.7

Oct 135.8 125.5 68.6 130.5 144.5 93.3 142.7 107.3 222.7 90.8 145.0

Nov 141.4 159.0 60.2 138.9 103.4 75.4 159.8 102.1 199.8 97.5 150.5

Dec 159.7 172.9 54.3 138.7 117.2 103.4 155.5 140.3 170.2 99.8 181.8

Jan 112.0 139.5 53.6 118.5 128.2 106.3 182.5 151.2 183.7 98.2 228.6

Feb 131.1 131.8 55.5 135.9 158.4 130.6 199.2 148.4 142.4 154.2 248.4

Mar 171.9 134.8 68.3 206.1 154.9 171.3 267.1 255.5 187.8 181.7 372.8

Apr 172.3 137.5 60.9 222.5 190.8 201.2 211.3 303.6 215.4 199.1 334.6

May 166.0 129.0 55.7 208.9 190.2 188.4 210.9 309.8 184.6 224.4 350.0

Out. Sales 391.0 304.0 133.3 487.3 430.5 577.8 430.6 641.6 309.7 428.4 645.1

Jun 148.8 115.4 45.8 188.9 166.0 240.1 194.1 280.2 120.8 198.2

Jul 164.8 95.0 59.7 179.2 200.3 232.2 186.5 266.4 113.5 171.0

Aug 151.3 80.5 56.8 168.5 156.5 222.9 137.6 230.0 111.2 178.7

JJA Total 464.9 290.9 162.3 536.6 522.8 695.2 518.2 776.6 345.5 547.9 754.1

119% 96% 122% 110% 121% 120% 120% 121% 112% 128% 117%

MY Total 1,830 1,543 731 1,918 1,870 1,898 2,293 2,433 2,060 1,774 2,915

If we were to take an average level of shipments relative to sales, we could ballpark JJA exports this year at

around 755 mb. That would lead to a total export figure just above 2.9 billion bushels. So, it seems likely to me

that the export projection likely has some further upside. Thoughts appreciated.

Livestock

We haven’t looked at basis in a while so I thought it’d be worth a quick glance this morning. The first chart

below looks at June cattle basis. You can see basis is still weaker than normal, but it has at least moved into a

somewhat “acceptable” level recently.

2

Monday, June 14, 2021

NTG Morning Comments

www.nesvick.com

June Live Cattle Basis History

$30.00

$25.00

$20.00

$15.00

$10.00

$5.00

$0.00

($5.00)

($10.00)

($15.00)

52 47 42 37 32 27 22 17 12 7 2

Weeks Til Expiration

2015 2016 2017 2018 2019 2020 2021

August basis follows below. I suppose you could say the same thing here. It remains weaker than normal but

not a mind-blowing outlier at this point at least.

August Live Cattle Basis History

$30.00

$25.00

$20.00

$15.00

$10.00

$5.00

$0.00

($5.00)

($10.00)

($15.00)

58 56 54 52 50 48 46 44 42 40 38 36 34 32 30 28 26 24 22 20 18 16 14 12 10 8 6 4 2 0

Weeks To Expiration

2014 2015 2016 2017 2018 2019 2020 2021

3

Monday, June 14, 2021

NTG Morning Comments

www.nesvick.com

It sounds like cash cattle volume last week was pretty solid. Our friends at MP Agrilytics note it could be the

largest volume since November. Early calls for cash trade this week are for steady prices. Beef prices were soft

last week and this could be the start of the typical seasonal decline…but then again seasonal patterns have not

been very useful in the past two years.

Financials

A lot of talk about Fed tapering around, which of course makes sense. There are a lot of signals suggesting the

Fed’s massive asset purchasing program is running a bit too aggressively right now in addition to the inflation

figures. What I think is interesting about the past few weeks is the market’s perception on rate hikes appears to

have changed fairly dramatically too. The chart below looks at Fed Fund futures implied rate hikes for 2021,

2022, and 2023. Clearly the market is not looking for any change off zero for rates this year, which of course

makes sense. You can see the market is not even pricing in a “full” 25 bps rate hike for 2022 either. However,

note how rate hike expectations for 2023 have jumped in the past 2-3 weeks. For the past several months the

market was pricing in full odds for one 25 bps rate hike, but in the past few weeks it has quickly priced in

another rate hike. I would argue that this is likely the main reason for the dollar’s consolidation in the past

several weeks. It also opens up possible surprises for the market here if the Fed continues to stick with its script.

Fed Fund Futures Implied Rate Change By Year

0.65

0.60

0.55

0.50

0.45

0.40

0.35

0.30

0.25

0.20

0.15

0.10

0.05

0.00

-0.05

12/31/2020 1/31/2021 2/28/2021 3/31/2021 4/30/2021 5/31/2021

2021 2022 2023

Energy

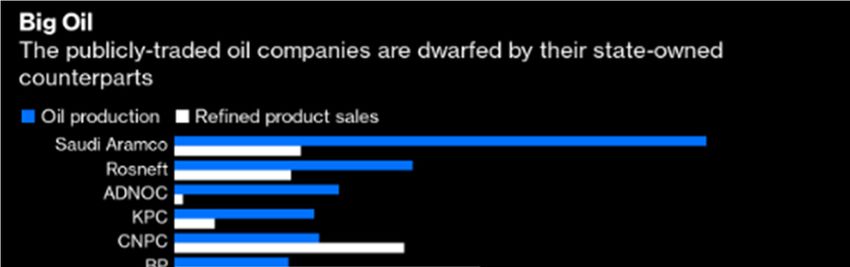

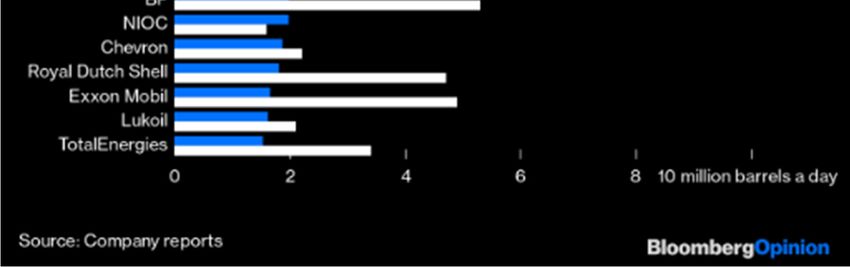

An interesting opinion piece on Bloomberg from their oil analyst Julian Lee entitled “Bashing Big Oil Won’t Save

the Planet”. He notes that the “world’s biggest oil producers aren’t susceptible to the sort of shareholder

pressure that dealt blows to the managements of Exxon Mobil Corp and Chevron Corp last month, or the Dutch

court that forced Royal Dutch Shell Plc to revise its carbon-cutting plans. They tend to be state-owned or

controlled entities in countries where climate-change activists and ESG investors have little sway”.

4

Monday, June 14, 2021

NTG Morning Comments

www.nesvick.com

He adds, “that is why we can’t tackle climate problems simply by forcing publicly-listed oil companies to pump

less of it. As long as there is demand for oil, someone will supply it.”

Further: “Until reliable and affordable electric cars, vans, and trucks are available widely, along with the

infrastructure to charge them, there will always be someone willing to provide the fuel to keep the old stock

running. Not to mention our dependence on space heating, industrial heating, shipping and a whole host of

other areas that currently depend on fossil fuels”.

It is all pretty common sense, of course, but it points out the problem that many of the “activists” are going after

the oil companies before they have any viable options to replace them. That should make the oil market very

interesting for years to come.

Today’s Calendar (all times Central)

• Export Inspections – 10:00am

• Crop Progress – 3:00pm

Thanks for reading.

David Zelinski

dzelinski@nesvick.com

901-766-4684

Trillian IM: dzelinski@nesvick.com

DISCLAIMER:

This communication is a solicitation for entering into derivatives transactions. It is for clients, affiliates, and

associates of Nesvick Trading Group, LLC only. The information contained herein has been taken from trade and

5

Monday, June 14, 2021

NTG Morning Comments

www.nesvick.com

statistical services and other sources we believe are reliable. Opinions expressed reflect judgments at this date

and are subject to change without notice. These materials represent the opinions and viewpoints of the

author and do not necessarily reflect the opinions or trading strategies of Nesvick Trading Group LLC and its

subsidiaries. Nesvick Trading Group, LLC does not guarantee that such information is accurate or complete and it

should not be relied upon as such.

Officers, employees, and affiliates of Nesvick Trading Group, LLC may or may not, from time to time, have long

or short positions in, and buy or sell, the securities and derivatives (for their own account or others), if any,

referred to in this commentary.

There is risk of loss in trading futures and options and it is not suitable for all investors. PAST RESULTS ARE NOT

NECESSARILY INDICATIVE OF FUTURE RETURNS. Nesvick Trading Group LLC is not responsible for any

redistribution of this material by third parties or any trading decision taken by persons not intended to view this

material.

6You can also read