Occupational licensing - how much and what effects? - OECD Ecoscope

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Occupational licensing – how much and what effects? By Indre Bambalaite, Giuseppe Nicoletti, Christina von Rueden, OECD Economics Department Occupational licensing – the legal authorisation from a national authority or a professional association to practice a specific occupation – is one of the fastest-growing labour market institutions since World War II (Kleiner and Krueger, 2010). It is not just lawyers, architects and engineers that have to comply with minimum human capital requirements, administrative burdens or mobility restrictions, in order to demonstrate professional aptitude and protect the public from unqualified, incompetent or unscrupulous providers. Offering skincare or hair removal services as a licensed cosmetologist in Pennsylvania, for instance, takes 1250 hours of training, a state exam and a blank criminal record, and to become a baker in France one needs to take a 7 hour long state exam (Institute of Justice, 2018; Von Rueden and Bambalaite, 2020). These occupational entry regulations (OER) often reduce both business dynamism and employment, and generate higher prices for customers. However, despite their ubiquity, evidence about the intensity, scope and effects of OER has so far been confined to selected countries and/or professions, thus impeding cross-country and cross-occupational comparability on a larger scale. Also, their potential effects on productivity growth have been ignored. New cross-country measures call for a review of OER and the need for more regional integration

Using new data on OER, OECD economists (Von Rueden and Bambalaite, 2020) shed light on the scope and stringency of these regulations for a set of 18 OECD countries, India and South Africa – with Canada and the United States being covered at the province-level or state-level – in ten personal (aestheticians, bakers, butchers, driving instructors, electricians, hairdressers, painters, plumbers, taxi drivers, and nurses) and five professional services (accountants, architects, civil engineers, lawyers and real-estate agents). The results illustrate that even countries sharing the same public goals in terms of safety and consumer satisfaction, sometimes apply very different approaches in pursuing them (Figure 1). Looking at successful experiences abroad, countries can learn from each other about ways to achieve these goals with lighter occupational entry requirements. More strikingly, regulatory approaches vary a great deal even within federal countries such as the US or Canada or economic unions such as the EU (Figure 2). Despite a myriad of policy initiatives aimed at facilitating the movement of professionals across these areas, these findings suggest the need for further integration efforts at the federal and international level.

Ill-designed occupational entry regulations can curb productivity in services While there is abundant evidence on the side effects of OER on the economy – via less firm entry, lower employment and higher prices (e.g. Athanassiou et al. 2015; Blair and Chung, 2018; Cahuc and Kramarz, 2004; Larsen et al., 2019; Kleiner et al., 2016; Kleiner, 2017; Kleiner and Soltas, 2019) – evidence on the effects of occupational entry regulations on firm-level and aggregate productivity growth is scant. Yet, by creating barriers to entry, OER might also unduly protect incumbents, stifle business dynamism and prevent the most productive firms from gaining market shares, weighing down on productivity growth in economies that are increasingly driven by entrepreneurial initiative and innovation. This concern arises especially at a time when governments are fiercely seeking ways to reverse the persistent productivity slowdown in advanced economies. Looking at the effects of OER on the performance of firms that are subject to them, Bambalaite et al. (2020) highlight two channels through which productivity could be adversely affected. First, OER could lower firms’ incentives and capabilities to improve productivity by adopting best practices and hire the best professionals by curbing entry, competitive pressures and business dynamism. Estimations suggest that if those regulations were aligned on the least stringent ones, productivity could indeed increase by over 1.5 percentage points on average across occupations and firms, with the greatest gains accruing to high productive firms (Figure 3). Considering that the average productivity growth of the firms in the sample is less than half a percentage point per year, this increase would be significant. Second, OER can undermine the ability of the most productive firms to grow by limiting the supply of skilled professionals and their

ability to move across firms within occupations, across occupations and across geographic jurisdictions (Johnson and Kleiner, 2020). In this regard, Bambalaite et al. (2020) estimate that in countries like Germany or Italy (where OER are the most stringent among the EU countries surveyed) easing occupational entry requirements to meet Swedish standards (which are the most lenient) could increase by over 10 percent the contribution of labour reallocation to employment growth in the personal and professional services covered in their analysis. For policy makers, the time to act is now In light of the renewed evidence on the undesired economic consequences of ill-designed regulations, appropriate strategies for reforming occupational regulations are urgently

warranted. While preserving their public policy aims, occupational entry regulations could be usefully reviewed by (1) making means more proportionate to ends (e.g. aligning on successful experiences abroad); (2) shifting the focus from inputs to outputs when the purpose of the regulation is to ensure that the outcome (such as a building standard or the quality of meat sold) rather than the service itself is of desired quality (e.g. via ex-post evaluation); (3) extending mutual recognition of entry requirements across jurisdictions (especially within federal countries and economic unions) and (4) eliminating mobility restrictions that create unnecessary labour market rigidities. Regulators should also consider whether licensing systems could be replaced with lighter alternatives, such as certification schemes, and where information asymmetry concerns persist, alleviate those through online consumer information platforms (e.g. leveraging on reliable service quality review systems). See also: Rethinking occupational entry regulations on VoxEU References: Athanassiou, E., N. Kanellopoulos, R. Karagiannis and A. Kotsi (2015), “The Effects of Liberalization of Professional Requirements in Greece”, Centre for Planning and Economic Research (KEPE), www.ec.europa.eu/DocsRoom/documents/13363/attachments/1/transl ations/en/renditions/native. Bambalaite, I., G. Nicoletti and C. von Rueden (2020), “Occupational entry regulations and their effects on productivity in services:

Measurement and firm-level evidence”, OECD Economics Department Working Papers, No. 1605, OECD Publishing, Paris. Blair, P. Q., and B. W. Chung (2018), “How much barrier to entry is occupational licensing?”, NBER Working Paper Series, No. 25262, https://doi.org/10.3386/w25262 Cahuc, P. and F. Kramarz (2004), “De la précarité à la mobilité: vers une sécurité sociale professionnelle. La documentation française”, Ministère de l’économie, des finances et de l’industrie, Ministère de l’emploi, du travail et de la cohésion sociale. Institute of Justice (2018), “Pennsylvania Fresh Start: Law Denies Woman Right to Work Because Of Irrelevant Crime Convictions”, available at https://ij.org/report/the-continuing-burden-of-occupational-li censing-in-the-united-states/ Johnson, J. and M. M. Kleiner (2017), “Is Occupational Licensing a Barrier to Interstate Migration?”, Federal Reserve Bank of Minneapolis, Staff report No. 561, https://doi.org/10.21034/sr.561. Kleiner, M.M., A. Marier, K. W. Park, and C. Wing, (2016), “Relaxing occupational licensing requirements: Analyzing wages and prices for a

medical service”, The Journal of Law and Economics, Vol. 59(2), pp.261-291, https://doi.org/10.1086/688093. Kleiner, M. M. (2017), “The influence of occupational licensing and regulation”, IZA World of Labor, No. 392, https://doi.org/10.15185/izawol.392. Kleiner, M. M. and E. J. Soltas (2018), “A Welfare Analysis of Occupational Licensing in U.S. States”, http://dx.doi.org/10.2139/ssrn.3140912. International corporate tax reform could support global tax revenues By David Bradbury, Tibor Hanappi, Pierce O’Reilly, Ana Cinta Gonzalez (OECD Centre for Tax Policy and Administration), Asa Johansson, Stéphane Sorbe, Valentine Millot, Sébastien Turban (OECD Economics Department) Recent economic analysis suggests that a proposed solution to the tax challenges arising from the digitalisation of the economy under negotiation at the OECD would have a significant positive impact on global tax revenues.

The analysis puts the combined effect of the two-pillar solution under discussion at up to 4% of global corporate income tax (CIT) revenues, or USD 100 billion annually. The revenue gains are broadly similar across high, middle and low- income economies, as a share of corporate tax revenues. The analysis was released just weeks after the international community reaffirmed its commitment to reach a consensus-based long-term solution to the tax challenges arising from the digitalisation of the economy, and to continue working toward an agreement by the end of 2020, according to a Statement by the OECD/G20 Inclusive Framework on BEPS. The Inclusive Framework on BEPS, which brings together 137 countries and jurisdictions on an equal footing for multilateral negotiation of international tax rules, decided during its January 29-30 meeting to move ahead with a two- pillar negotiation to address the tax challenges of digitalisation. Participants agreed to pursue the negotiation of new rules on where tax should be paid (“nexus” rules) and on what portion of profits they should be taxed (“profit allocation” rules), on the basis of a “Unified Approach” under Pillar One. The aim is to ensure that multinational enterprises (MNEs) conducting sustained and significant business in places where they may not have a physical presence can be taxed in such jurisdictions. They also decided to continue discussions on Pillar Two, which aims to address remaining base erosion and profit shifting (BEPS) issues and ensure that international businesses pay a minimum level of tax. The economic analysis and impact assessment of the Pillar One

and Pillar Two proposals is being undertaken to inform key decisions on the design and parameters of the tax reform to be agreed by Inclusive Framework members as part of the negotiations underway at the OECD. The analysis covers data from more than 200 jurisdictions, including all members of the Inclusive Framework, and more than 27,000 MNE groups. Assumptions in the preliminary analysis are illustrative, and do not pre-judge decisions to be taken by the Inclusive Framework. The analysis shows that the Pillar One reform – designed to re-allocate some taxing rights to market jurisdictions, regardless of physical presence – would also bring a small tax revenue gain for most jurisdictions. Under Pillar One, low and middle-income economies are expected to gain relatively more revenue than advanced economies, with investment hubs experiencing some loss in tax revenues. More than half of the profit re-allocated would come from 100 large MNE groups. The analysis shows that Pillar Two could raise a significant amount of additional tax revenues. By reducing the tax rate differentials between jurisdictions, the reform is expected to lead to a significant reduction in profit shifting by MNEs. This will be important for developing economies as they tend to be more adversely affected by profit shifting than high- income economies. The overall direct effect on investment costs is expected to be small in most countries, as the reforms target firms with high levels of profitability and low effective tax rates. The reforms would also reduce the influence of corporate taxes on investment location decisions. In addition, failure to reach a consensus-based solution would likely lead to further unilateral measures and greater uncertainty.

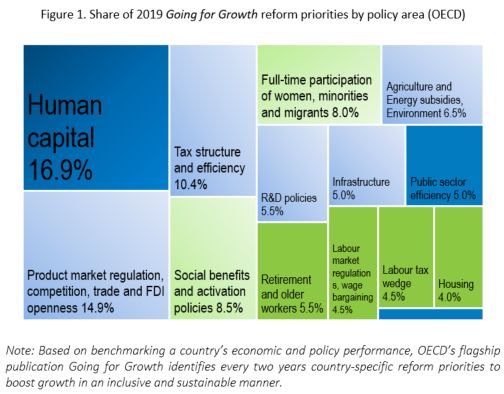

References OECD Webcast presentation of the preliminary results of the Economic analysis and impact assessment of potential reforms to address the tax challenges arising from the digitalisation of the economy (February 2020): www.oecd.org/tax/beps/webcast-economic-analysis-impact-assessm ent-february-2020.htm. OECD Secretary General Tax Report to G20 Finance Ministers and Central Bank Governors (February 2020): http://www.oecd.org/ctp/oecd-secretary-general-tax-report-g20- finance-ministers-riyadh-saudi-arabia-february-2020.pdf Statement by the OECD/G20 Inclusive Framework on BEPS on the Two-Pillar Approach to Address the Tax Challenges Arising from the Digitalisation of the Economy (January 2020): http://www.oecd.org/tax/beps/statement-by-the-oecd-g20-inclusi ve-framework-on-beps-january-2020.pdf The human capital paradox: A measurement issue? by Jarmila Botev, Balázs Égert, Zuzana Smidova, David Turner, OECD Economics Department Human capital is widely regarded as a fundamental input in the theoretical growth literature. Recommendations to boost it

feature prominently among reform priorities for a great number of countries (Figure 1). Yet, paradoxically, quantifying the macroeconomic effects of human capital has often proven frustratingly elusive. As this blogpost explains, in part this is due to the challenge of measuring human capital. A newly released OECD measure of human capital works well in productivity regressions, providing the “missing” link between growth and human capital. Human capital can be defined as the stock of knowledge, skills and other personal characteristics of people that helps them to be productive. Such knowledge is gained in formal education (e.g. early childhood care, compulsory schooling and adult training programmes) but also informally, via on-the-job learning and work experience. Health also influences one’s productivity. Nevertheless, there is no widely accepted

empirical measure that captures all these dimensions across many countries and over time. The early macroeconomic growth literature used various quantitative measures of education as a proxy for human capital, including literacy rates or enrolment rates at various levels of education. More recent studies use mean years of schooling (average number of completed years of education of a country’s entire population). However, the link of these proxies to macroeconomic outcomes has generally been poor. A meta-analysis of 60 studies published over the period of 1989-2011 found that around 20% of the reported coefficient estimates on human capital have the “wrong” (negative) sign (Benos and Zotou, 2014). In a dozen of papers by Robert J. Barro, based on similar specifications, techniques and datasets, only about a half of the coefficient estimates is positive and statistically significant. Recent OECD studies confirm the difficulty of finding a robust positive effect of human capital on income per capita or productivity levels when looking at the OECD countries (Botev et al., 2019; Guillemette et al, 2017, Fournier and Johanson 2016). And, this is the paradox, the widely accepted importance of human capital, but the difficulty of finding an empirically relevant measure of it — which our recent work addresses. The OECD’s newly released human capital measure combines an up-to- date dataset of mean years of schooling (the 2018 update of Goujon et al, 2016) with rates of return based on recent evidence on wage premia compiled mostly by the World Bank (Psacharopoulos and Patrinos, 2004; Montenegro and Patrinos, 2014). Unlike earlier studies, it applies different returns for five groups of countries and three periods. Including such measure of human capital in various macroeconomic productivity regressions yields significant and positive relationships that economists have been looking for.

Find out more: http://www.oecd.org/economy/human-capital/ Botev, J. B. Égert, Z. Smidova and D, Turner (2019), “A new macroeconomic measure of human capital with strong empirical links to productivity“, OECD Economics Department Working Paper No. 1575 References Benos, N. and S. Zotou (2014), “Education and Economic Growth: A Meta-Regression Analysis”, World Development, 64 (C), 669-689. Fournier, J. and Å. Johansson (2016), “The Effect of the Size and the Mix of Public Spending on Growth and Inequality“, OECD Economics Department Working Papers, No. 1344, OECD Publishing, Paris. Guillemette, Y., et al. (2017), “A revised approach to productivity convergence in long-term scenarios“, OECD Economics Department Working Papers, No. 1385, OECD Publishing, Paris OECD (2019), Economic Policy Reforms 2019: Going for Growth, OECD Publishing, Paris. Psacharopoulos, G. and H. Patrinos (2004), “Returns to

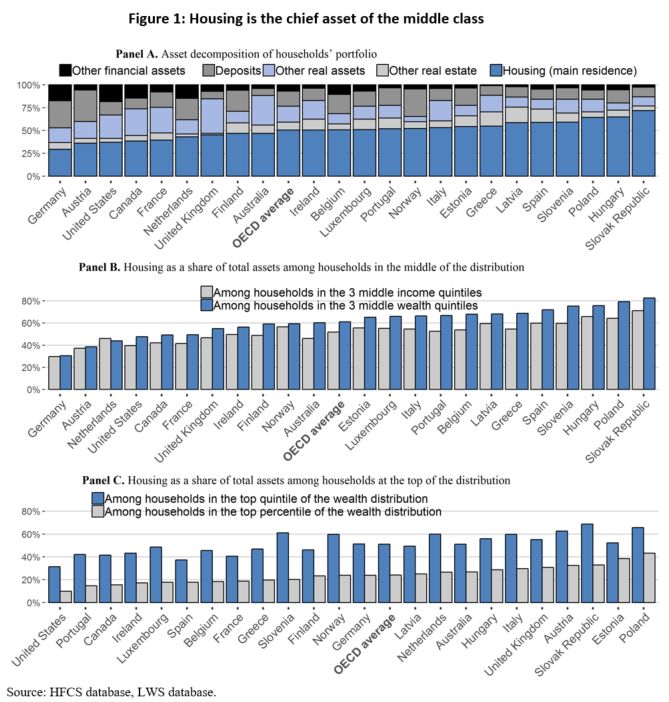

Investment in Education: A Further Update”, Education Economics, 12(2), 111-134. Psacharopoulos, G. and H. Patrinos (2018), “Returns to Investment in Education A Decennial Review of the Global Literature”, World Bank Policy Research Working Paper No. 8402. Housing, wealth accumulation and wealth distribution: risks and opportunities By Orsetta Causa and Nicolas Woloszko Is housing a vehicle for wealth accumulation for middle class and lower-income groups? Can housing mitigate wealth inequality? Assessing housing from a wealth distribution perspective is all the more important in a context where inequality has been rising, where the capital share of income has increased relative to labour and where wealth inequality is much higher than income inequality, potentially undermining equality of opportunity and social mobility. In a recent paper (Housing-wealth-accumulation-and-wealth- distribution-evidence-and-stylized-facts_) we shed light on

these questions and deliver new evidence and stylised facts on housing, wealth accumulation and wealth distribution, relying on an in-depth analysis of micro-data on household wealth across OECD countries. We assess the role of housing in shaping the wealth distribution by focusing on assets and liabilities, with particular attention to the bottom of the income and wealth distributions. We document a strong negative cross-country association between homeownership and wealth inequality. Housing tends to equalise the distribution of wealth from a static cross- country perspective because it is the most important and most widely owned asset in household balance sheets: housing is the chief asset of the middle class (Figure 1). Households in the top of the wealth distribution hold more diversified portfolios, including business and financial assets, while less wealthy households own virtually nothing.

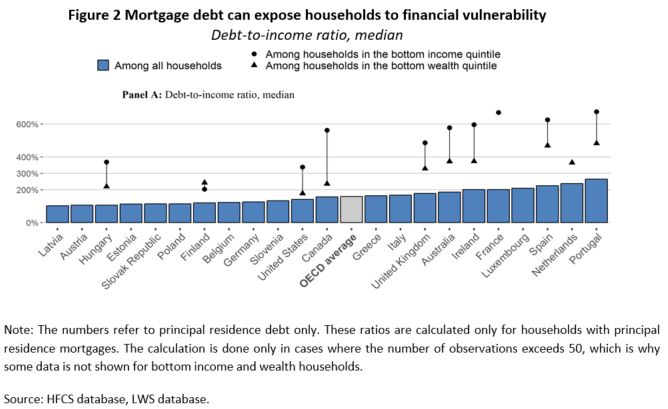

Housing is the primary asset in households’ portfolios, but is also their primary liability. This is especially true for young homeowners and homeowners at the bottom of the distribution. Yet one lesson from the financial crisis is that debt creates opportunities but also risks, particularly for vulnerable households. We deliver new cross-country evidence on the socio-economic distribution of mortgage debt and financial vulnerability. This is relevant for monitoring the sensitivity of households to income losses and declines in

house prices. Our analysis shows that the strong expansion in mortgages over the last decades, and in particular prior to the financial crisis, is very likely to have contributed to high and sometimes excessive housing-related indebtedness. Debt-to-income ratios are well above 100% in most OECD countries and exceed 200% in some of them (Figure 2). Households at the bottom of the income distribution are particularly vulnerable, with values exceeding the conventional at-risk threshold value of 300%. We compute micro-based tenure wealth gaps, that is, the net wealth ratio between homeowners and renters, in order to shed light on the role of housing as a vehicle for wealth accumulation. We find that homeowners tend to be wealthier than renters, even when housing wealth is excluded. However, we also find that this gap is significantly reduced in a quantile regression framework that controls for household drivers of wealth accumulation. These findings do not strongly

support the existence of a causal effect of homeownership on wealth accumulation. Tenure wealth gaps are likely to reflect self-selection mechanisms. Households with a higher ex-ante propensity to save and an appetite for wealth accumulation select themselves into homeownership rather than becoming homeowner making them more prone to accumulate wealth. Housing is negatively associated with wealth inequality, but also with residential mobility, as documented in our paper: this reflects cross-country differences in the housing tenure mix to the extent that homeowners tend to be less mobile than private renters. This finding is not new. Although causality cannot be easily established, a common conjecture is that mobility is lower among owner-occupiers than renters because owners face higher transaction costs of relocating and therefore spend a longer time in their residence in order to spread the costs over a longer time period. Overall, even if wealth inequality is lower where homeownership is more widespread, encouraging homeownership is probably not the appropriate policy response to make wealth more equally distributed, as this may imply trade-offs with other policy objectives such as economic resilience and labour mobility. Read the full paper: Causa, O., N. Woloszko and D. Leite (2019), “Housing, wealth accumulation and wealth distribution: Evidence and stylized facts”, OECD Economics Department Working Papers, No. 1588, OECD Publishing, Paris, https://doi.org/10.1787/86954c10-en.

Tackling the fallout from the coronavirus by Laurence Boone, OECD Chief Economist Covid-19 (coronavirus) hit China at the start of December and outbreaks have spread more widely. The virus is bringing considerable human pain. It is also resulting in significant economic disruption from quarantines, restrictions on travel, factory closures and a sharp decline in many service sector activities. The world economy is in its most precarious position since the global financial crisis. Global growth, cooling for the past two years to a subdued level, has been dealt a nasty blow by the coronavirus. High frequency indicators such as coal demand, suggest the Chinese economy slowed sharply in the first quarter of 2020. As China accounts for 17% of global GDP, 11% of world trade, 9% of global tourism and over 40% of global demand of some commodities, negative spillovers to the rest of the world are sizeable. There is mounting evidence of sharp declines in tourism, supply chain disruptions, weak commodity demand and falling consumer confidence. How far the epidemic spreads will determine economic prospects.

Even under a best-case scenario of containment to China and limited outbreaks in other countries as we see today, the OECD expects a sharp slowdown in world growth in early 2020. We have revised our projection for the year from an already low 3% in November to only 2.4%, lower than in any year since the financial crisis. In a downside-risk scenario where epidemics break out in some other countries across the globe, the slowdown will be sharper and more prolonged. Our modelling suggests that the level of world GDP would fall as low as 1.5% this year, halving the OECD’s previous 2020 projection from last November of 3%. Containment measures and fear of infection would hit production as well as spending hard and drive many of the epidemic affected countries into outright recession. Governments cannot afford to wait. Regardless of where the virus spreads, the world economy, previously weakened by persistent trade and political tensions, has already suffered a sharp setback. Households are uncertain and apprehensive. Firms in sectors such as tourism, electronics and automobiles are already reporting supply disruptions and/or a collapse in demand. The world economy is now too fragile for governments to gamble on an automatic sharp bounce-back. Containing the epidemic and limiting cases of serious illness is the policy priority. Limiting travel, quarantines and cancelling events are required to contain the epidemic. Increased government spending should be first directed to the health sector, tackling virus outbreaks and supporting research.

Complementary policy action can at least mitigate the economic and social fallout. Supporting vulnerable households and firms is essential. Containment measures and the fear of infection can cause sudden stops in economic activity. Beyond health, the priority should be on allowing short-time working schemes and providing vulnerable households temporary direct transfers to tide them over loss of income from work shutdowns and layoffs. Increasing liquidity buffers to firms in affected sectors is also needed to avoid debt default of otherwise sound enterprises. Reducing fixed charges and taxes and credit forbearance would also help to reduce the pressure on firms facing an abrupt falloff in demand. If the epidemic spreads outside China, the G20 should lead a coordinated policy response. Countries should cooperate on support to health care in countries where it is needed, as well as on containment measures. In addition, if countries announced coordinated fiscal and monetary support, confidence effects would compound the effect of policies. This would help reverse the drubbing in confidence that a more widespread outbreak would provoke. It would also be more effective than working alone. Our work presented in the Economic Outlook 2019 shows that if G20 economies implement stimulus measures collectively, rather than alone, the growth effects in the median G20 economy will be 1/3 higher after just two years. Some would say it is trite to call for international cooperation. However, in this globally connected economy and society, the coronavirus and its economic and social fallout is everyone’s problem, even if

firms decide in the wake of this virus shock to repatriate production and make it a bit less interdependent. For more information visit the latest Interim Economic Outlook, released 2 March 2020 Faire face aux répercussions de l’épidémie de coronavirus de Laurence Boone, Cheffe économiste de l’OCDE Une épidémie de coronavirus (Covid-19) vient de frapper la Chine en ce début d’année et des foyers se déclarent dans de nombreux pays. Le virus est la cause d’une souffrance humaine considérable. Il est aussi à l’origine de perturbations économiques non négligeables résultant des mesures de quarantaine, des restrictions aux déplacements, de la fermeture d’usines et de la forte contraction de l’activité dans de nombreux secteurs de services. Si l’on ne tient compte que de la situation actuelle, la flambée de l’épidémie entraînerait un recul de 0.5 point de pourcentage de la croissance du PIB mondial, qui serait ramenée à 2.4 % cette année. Cependant, l’incertitude demeure quant à l’évolution de l’épidémie : elle pourrait continuer à se propager, ce qui induirait une aggravation de ses effets sur le plan humain ainsi qu’un tassement plus marqué de la croissance mondiale. Si l’épidémie devait toucher les économies avancées de l’OCDE avec la même intensité que la Chine, la croissance mondiale

serait divisée par deux par rapport à nos prévisions du mois de novembre. L’économie mondiale se trouve dans la position la plus périlleuse qu’elle ait connue depuis la crise financière mondiale. La croissance mondiale, qui s’est essoufflée pendant les deux dernières années jusqu’à atteindre son faible niveau actuel, a subi de plein fouet l’épisode du coronavirus. Les indicateurs à haute fréquence comme la demande de charbon, qui se situe à 60 % de son niveau normal, donnent à penser que l’économie chinoise a accusé un fort ralentissement au premier trimestre 2020. Parce que la Chine représente 17 % du PIB mondial, 11 % du commerce mondial, 9 % du tourisme mondial et plus de 40 % de la demande mondiale de certains produits de base, les retombées négatives sur le reste du monde sont considérables. Des signes de plus en plus probants attestant un repli prononcé de l’activité dans le secteur du tourisme, des ruptures dans les chaînes d’approvisionnement, une atonie de la demande de produits de base et une érosion de la confiance des consommateurs, sont perceptibles. L’étendue de l’épidémie sera un paramètre déterminant des perspectives économiques. Même dans un scénario où l’épidémie serait circonscrite à la Chine et ne donnerait lieu qu’à des flambées limitées dans les autres pays, comme c’est le cas aujourd’hui, l’OCDE s’attend à un fort ralentissement de la croissance dans le monde début 2020. Nous avons ramené notre prévision pour l’année, qui était déjà basse, soit 3 %, à 2.4 % seulement, le chiffre le plus faible depuis la crise financière. Dans un scénario de

propagation de l’épidémie à certains autres pays du globe, le ralentissement serait plus prononcé et plus prolongé. Notre modélisation laisse à penser que la croissance mondiale en 2020 pourrait alors ne pas dépasser 1.5 %. Les mesures de confinement et la peur de l’infection porteraient un rude coup à la production ainsi qu’aux dépenses et entraîneraient un grand nombre de pays touchés par l’épidémie dans une véritable récession. Les pouvoirs publics ne peuvent se permettre d’attendre. Indépendamment de l’étendue de la propagation du virus, l’économie mondiale, précédemment éprouvée par la persistance de tensions commerciales et politiques, a déjà essuyé un coup de frein brutal. Les ménages sont en proie à l’incertitude et à l’appréhension. Les entreprises dans des secteurs comme le tourisme, l’électronique et l’automobile font d’ores et déjà état de ruptures d’approvisionnement et/ou d’un effondrement de la demande. L’économie mondiale est désormais trop fragile pour que les pouvoirs publics puissent se permettre de tabler sur un fort rebond automatique. La priorité des gouvernements est de contenir l’épidémie et de limiter le nombre de cas graves. La limitation des déplacements, des mesures de quarantaine et l’annulation de manifestations s’imposent pour endiguer l’épidémie. Il conviendrait d’orienter les dépenses publiques supplémentaires consenties d’abord vers le secteur de la santé afin de combattre la flambée du nombre de cas et de mettre au point un vaccin. Les actions complémentaires susceptibles d’être engagées peuvent à tout le moins viser à atténuer les répercussions économiques et sociales de l’épidémie.

Il est essentiel d’apporter un soutien aux ménages et aux entreprises les plus vulnérables. Les mesures de confinement et la peur de l’infection peuvent déclencher des interruptions soudaines de l’activité économique. Au-delà de la santé, la priorité devrait être d’autoriser la mise en place de dispositifs de chômage partiel et l’octroi aux ménages vulnérables de transferts directs pour les protéger des pertes de revenus provoquées par les fermetures d’entreprises et les licenciements. Il est également indispensable d’accroître les volants de liquidités dont disposent les entreprises dans les secteurs concernés pour éviter que des entreprises structurellement saines ne se trouvent en défaut de paiement. En plus d’une réduction des charges fixes et des impôts, une certaine indulgence de la part des créanciers aiderait également à relâcher la pression qui s’exerce sur les entreprises confrontées à un fléchissement soudain de la demande. Si l’épidémie se propageait au-delà des frontières de la Chine, il conviendrait que le G20 pilote une relance budgétaire et monétaire coordonnée. Le but serait de contribuer à inverser l’effondrement de la confiance que provoquerait une propagation plus large de la maladie. Une action collective serait en outre plus efficace que des actions isolées. Pour ce qui est du soutien à apporter aux pays qui en ont besoin en matière de santé et des mesures de confinement, les pays devraient coopérer. De plus, si des pays annonçaient un soutien budgétaire et monétaire coordonné, cette annonce aurait des effets sur la confiance qui se conjugueraient à ceux des politiques menées. Nos travaux montrent que si les économies du G20 mettaient en œuvre des mesures de relance de manière collective plutôt qu’isolément,

leurs effets sur la croissance dans l’économie du G20 médiane seraient amplifiés d’un tiers au bout de deux ans seulement. D’aucuns n’hésiteraient pas à dénoncer la banalité d’un appel à la coopération internationale. Néanmoins, dans une économie et une société connectées à l’échelle planétaire, le coronavirus et ses retombées économiques et sociales sont l’affaire de tous, même si des entreprises décident, au lendemain de cette crise, de rapatrier leur production et d’aller vers un peu moins d’interdépendance. Pour plus d’informations: Perspectives économiques de l’OCDE, Rapport intermédiaire mars 2020

You can also read