Opportunity Zones for Real Estate Investors - Michael Lortz, CPA, LEED AP - NAIOP Oregon Chapter

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Opportunity Zones

for Real Estate Investors

Michael Lortz, CPA, LEED AP

(503) 221 0141

mlortz@gmco.com

March 6, 2019

Disclaimer

The purpose of this presentation is to provide

information, rather than advice or opinion. It is accurate

to the best of the presenters’ knowledge as of the date

the presentation was developed. The information,

examples, and suggestions presented in this material have

been developed from sources believed to be reliable.

Accordingly, this presentation should not be viewed as a

substitute for the guidance and recommendations of a

retained professional and should not be construed as

legal, tax, or other professional advice. We recommend

consultation with competent professional advisors before

applying this material in any particular factual situations.

2

Agenda

Background

Investors

Fund Structure & Qualified Assets

Open Issues

3Law / Guidance

Part of Tax Cuts and Jobs Act (12/22/2017)

• IRC Sec. 1400Z-1, -2

IRS Notice 2018-48 (list of designated QOZs)

• More than 8,700 QOZs, including all 50 states, D.C., and 5 U.S.

territories

• Designations valid through 12/31/2028

Proposed Reg. 115420-18 issued 10/29/2018

Rev. Rul. 2018-29 (land)

Form 8996 (QOF self-certification)

Additional guidance expected late March / early April

Oregon has proposed legislation to disconnect!

4Qualified Opportunity Zones

2010 population census tracts (1,200–8,000 inhabitants)

Low Income Community (LIC) is a census tract…

• Poverty rate ≥ 20% or median family income (MFI) ≤ 80% of

statewide MFI (modified if metro-area)

• Also, census tract contiguous to designated LIC if MFI ≤ 125% of the

contiguous LIC may be designated

Designated by CEO of each jurisdiction (e.g. Gov. Brown)

• Maximum of 25% LICs designated, only 5% of which could be non-

LIC contiguous to LIC designations

Summary: Qualified Opportunity Zone = designated LIC

https://www.cdfifund.gov/Pages/Opportunity-Zones.aspx

5Qualified Opportunity Zones in Oregon

834 census tracts → 342 low income communities →

86 qualified opportunity zones located in Oregon

• Multnomah County (17): Portland (Downtown, Gateway,

Rosewood), Gresham, Fairview

• Washington County (8): Beaverton, Forest Grove, Hillsboro,

Tigard, Tualatin

• Clackamas County (6): Clackamas, Oregon City, Wilsonville

https://www.oregon4biz.com/Opportunity-Zones/

Note: don’t forget about Vancouver, WA – waterfront!

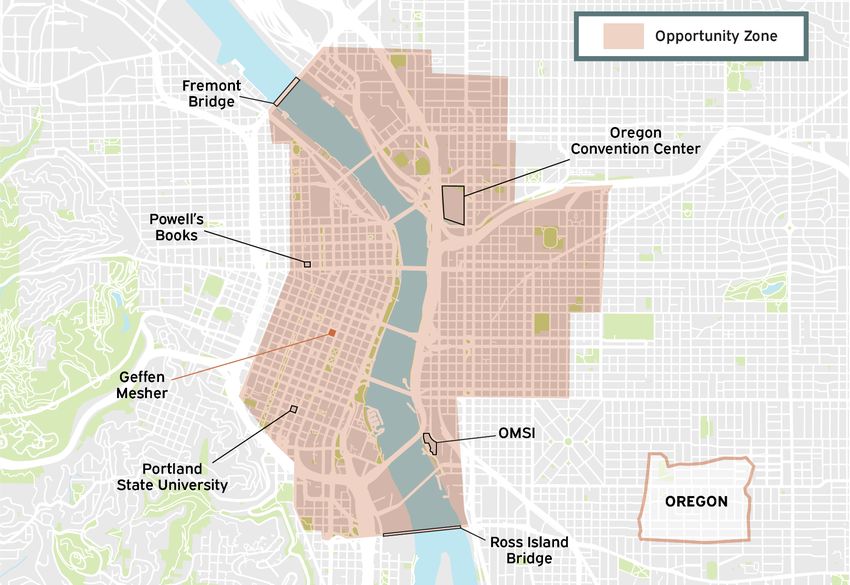

6QOZ in Downtown Portland

7Investors

Eligible investors include C-Corporations, S-

Corporations, partnerships, LLC’s, individuals, trusts,

and estates

Investor must have capital gains (long-term or short-

term) from the sale of property to an unrelated (20% or

less common ownership) person through 12/31/2026

Investor must invest capital gain (not basis) within 180

days of recognizing capital gain into Qualified

Opportunity Fund (QOF) and make election on Form

8949 when filing income tax returns

8Investor Example

Sell stock in 2018 for $500,000 realizing $300,000 gain

Within 180 days of sale, invest $300,000 into QOF

Make election in 2019 when filing 2018 tax return and

reporting stock sale

Don’t…

• Have to invest $200,000 basis

• Have to use accommodator / QI

• Have to “identify” replacement property

9Investors in PTEs

Investors receiving capital gains from pass-through

entities (PTEs) are considered to have recognized

capital gain on last day of pass-through entity fiscal

year, often 12/31

• Example: partnership with 12/31 FYE sells capital asset on

1/2/2018, giving partners 180 days from 12/31/2018 to invest

in QOF, i.e. until 6/29/2019

If PTE provides information to investors regarding sale

date, capital gain amount, and statement that PTE is

not electing to invest gains in a QOF, then investors can

individually elect to apply 180 days from PTE’s sale date

10Investors & Tax Consequences

Deferral: Investor’s initial capital gain is deferred until earlier of

12/31/2026 or disposition of investment in QOF (if disposition

proceeds are less than investment, then less gain to recognize)

• If disposition of investment in QOF, may reinvest within 180 days into

another QOF if before 12/31/2026 and continue deferral

• Deferred gain’s tax attributes remain with it until recognition, e.g. short-

term rate, 25% rate on real estate depreciation, Sec. 1256 contracts, etc.

Reduction: Investor’s initial capital gain is reduced via basis

adjustments:

• By 10% if hold QOF for 5 years (through 12/31/2026)

• By additional 5% if hold QOF for 7 years (through 12/31/2026)

Exclusion: 10-year hold allows investor to elect basis adjustment

to FMV as of date that investment in QOF is sold (through

12/31/2047)

11Investor Example cont.

Invest $300,000 capital gain into QOF on 2/1/2019 – initial

tax basis = -0-

On 2/1/2024, tax basis in QOF increases from -0- to $30,000

On 2/1/2026, tax basis in QOF increases from $30,000 to

$45,000

On 12/31/2026, investor recognizes taxable income of

$255,000 ($300,000 - $45,000), which is 85% of original gain

Sometime after 2/1/2029 but no later than 12/31/2047,

investor sells investment in QOF for $1,000,000 resulting in

a $700,000 gain –> NO FEDERAL TAX due to 10+ year hold

12Qualified Opportunity Fund

The QOF must be a U.S. entity taxable as either a

corporation or a partnership and self-certify with the IRS via

annual filing of Form 8996 with its income tax returns

Must invest ≥ 90% of assets in Qualified Opportunity Zone

Property (QOZP) acquired after 12/31/17

• Test dates are the last day of first 6-month period of QOF and on

last day of QOF’s FYE — results are averaged, e.g. if calendar-year

QOF begins 2/1, then first test dates will be 7/31 and 12/31

• Assets are valued per applicable financial statement (e.g. audit) or

cost basis if no AFS

• Penalty at underpayment rate (e.g. 6%) applies on shortfall if QOF

fails test unless “reasonable cause” – rate adjusts quarterly

13Qualified Opportunity Fund Example

1/1/2019 LLC is formed to be a QOF, has a 12/31 FYE

2/1/2019 Investor contributes gains into LLC, which

makes election to be treated as a QOF as of 2/1/2019

1st test date = 7/31/2019 (end of first 6 months)

2nd test date = 12/31/2019 (fiscal year-end)

3rd test date = 6/30/2020 (every 6 months)

4th test date = 12/31/2020 (every 6 months)

etc.

14Qualified Opportunity Fund

Per Form 8996 instructions, the QOF’s organizing

documents must contain a statement that the entity’s

purpose is to invest in QOZP as well as a description of

the QOZB(s) that QOF expects to engage in directly or

through a first-tier operating entity

Currently, no additional reporting requirements besides

Form 8996, e.g. no audited financial statement or

community impact statement required

15Qualified Opportunity Zone Property

QOZP includes:

• Qualified Opportunity Zone Business Property (QOZBP) =

tangible property used in a trade or business within a

Qualified Opportunity Zone

• Ownership interest in Qualified Opportunity Zone Business

(QOZB) organized as corporation or partnership for income tax

purposes that invests in QOZBP

• Note: preferred stock in corporations and special allocations within

partnership agreements are OK

16Qualified Opportunity Zone

Business Property

Acquired by purchase (not from related party, 20% test)

after 12/31/17

Original use of property commences with QOF / QOZB or

property is substantially improved* by QOF / QOZB

During holding period, substantially all use of property is

within Qualified Opportunity Zone

* During 30-month period after acquisition, additions to

basis must exceed adjusted basis of property at start of 30-

month period, e.g. must double the basis of an existing

building (not including the land)

17Structure Option 1 – QOF w/No QOZB

Investor A Investor B

QOF

QOZ Non-Qualified

Business Prop. Assets

Problem: It is often difficult for QOF to spend 90%+ of its cash

on qualified property before its first testing date, which could

result in a penalty, e.g. substantially improving a building or

ground-up construction typically takes more than 6 months.

18Qualified Opportunity Zone Business

Criteria:

• ≥ 70% of all tangible property, owned/leased is QOZBP

• ≥ 50% gross income derived from active conduct of its

business

• < 5% of average unadjusted basis of property attributable to

nonqualified financial property

• No portion of proceeds used for golf course, country club,

massage/hot tub/suntan facilities, racetrack/gambling

facilities, or liquor store – but it appears that you can rent to

them

19Qualified Opportunity Zone

Business Working Capital

QOZB can hold working capital as cash, cash

equivalents, or debt instruments with term ≤ 18

months

If QOZB acquires, constructs, or rehabilitates tangible

business property in OZ, then can qualify for working

capital safe harbor:

• Written plan identifying cash being held for qualifying project

• Reasonable written schedule consistent with ordinary start-up

of a business for deployment of cash within 31 months

• Working capital is spent in manner that is substantially

consistent with plan and schedule

20Structure Option 2 – QOF w/QOZB

Investor A Investor B

Partner C

QOF

Non-Qualified

QOZB

Assets

QOZ Business Property Non-Qualified Assets

• Eligible for working capital • e.g. assets purchased from related

safe harbor parties

• No restricted businesses • e.g. financial assets ≤ 5%

21Exit Strategy

Problem: 10+ year gain exclusion is only applicable on

sale of QOF ownership interest, i.e. not sale of property

Potential solutions:

• Each QOF/QOZB structure only owns 1 piece of real estate

• QOF is structured as REIT so that investors can easily sell

shares and there is no tax at REIT level when assets are sold

22Many Unanswered Questions

Is working capital qualifying for 31 month safe harbor treated as

tangible property in the interim?

Is land purchased or contributed by related parties disregarded in

tests?

How can QOF reinvest interim gains from sales of property and what is

impact on investors?

What is definition of “substantially consistent” in working capital safe

harbor?

Are there real estate leases that would not meet trade/business

definition, e.g. triple-net leased property?

What is inside basis of property owned by fund for depreciation

purposes and for Sec. 199A (new 20% deduction) purposes?

How are distributions from refinance proceeds treated?

Are multi-tiered entity structures allowed?

23Observe today. Shape tomorrow.

888 SW 5TH AVENUE, SUITE 800, PORTLAND, OR 97204

TEL 503-221-0141 | FAX 503-227-7924 | GMCO.COMYou can also read