OUTLOOK 2021 INVESTMENT STRATEGY GROUP - JANNEY MONTGOMERY SCOTT LLC Published: December 14, 2020

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

INVESTMENT STRATEGY GROUP

OUTLOOK 2021

JANNEY MONTGOMERY SCOTT LLC

Published: December 14, 2020

The prospects of a post-pandemic world have brightened. We expect macroeconomic conditions to evolve positively as organic growth ensues due to the reopening of global economies augmented by fiscal and monetary initiatives as well as a therapeutic response to COVID-19, which builds a supportive and positive impulse that persists through 2021 and beyond. Certainly, we host concerns about the remaining level of underemployment, the pace of inoculations that speed the world closer to economic normality, tensions in the Middle East, and China’s drive toward hegemonic superiority. Yet, none turns aside our baseline expectation.

I N V E S T M E N T S T R AT E G Y G R O U P

OUTLOOK 2021

OVERVIEW

While we did not build a global pandemic into our forecasts last year, the outcome for the markets settled about where we

expected. Stocks posted a strong year with many global bourses, including the large cap U.S. proxy, generating returns in excess

of historical averages. Bonds benefited from the massive injection of monetary liquidity and accommodative policy setting to

deliver handsome gains as well.

Concerns that some of the recovery was artificially induced by the unprecedented level of intervention lead some to remain

skeptical the advance can continue. We are not among them. The key is the transition from liquidity to sustainable growth and

there are myriad signs of that handoff occurring.

Economy & Equity Markets...........................................................................................................................................................Page: 4

• A renewed economic expansion is underway. The nadir of the pandemic-induced contraction occurred in April, leading to a

subsequent robust and sustainable rebound.

• Rapidly rising corporate profits and the lack of alternatives for investors seeking attractive real returns is a setup for equities to

climb higher, perhaps substantially so.

• Foreign equities are attractive, but the catalyst to unlocking their value is virus mitigation and a proportional response to the

significant fiscal and monetary policies enacted.

• Central banks are highly unlikely to rescind their monetary largesse anytime soon. Indeed, many stand ready to do more as

needed to reflate their respective economies.

• A weaker dollar should boost commodities. The recovery in demand on the back of the improving growth outlook will favor oil

and precious/industrial metals.

• Geopolitical policy uncertainty will recede as the incoming Administration takes a multilateral approach to trade and other

matters, further helping to support global risk assets.

Fixed Income & Interest Rates.....................................................................................................................................................Page: 8

• It has been an exceptional year in fixed income, with returns marred by a short-lived credit crisis, but ultimately saved by plunging

interest rates and Federal Reserve action.

• We anticipate long-term interest rates will continue to rise (albeit unevenly) and credit conditions will improve as the economic

growth cycle persists.

• Cash and equivalent yields will continue to be anchored by the zero-bound policy authored by monetary officials, pressing and

holding real returns into negative territory.

• The release of unused credit reserves from the banking system could provide a surprising tailwind for credit-sensitive assets,

pulling spreads tighter.

• In general, it remains a time to take credit risk and not interest rate risk, so we favor shorter-term, lower-rated bonds for better

returns in the coming year.

• Our favorite sectors are short-term taxable municipal and BBB-rated corporates, or, for those with the appropriate risk budget,

short-term BB- and even B-rated high yield bonds.

© JANNEY MONTGOMERY SCOTT LLC • MEMBER: NYSE, FINRA, SIPC • JANNEY OUTLOOK 2021 • REF: 168315-1220 • PAGE 3 OF 10

ECONOMY & EQUITY MARKETS

Our base case is that the vaccines will allow a progressive reopening of the economy

at large, and importantly be accompanied by the sectors currently still under full or

partial lockdown.

The news that vaccines developed by Pfizer-BioNTech and Moderna are around 95%

efficacious is very encouraging. The Oxford-AstraZeneca announcement is also a source

of optimism, even if the trial results have been challenged. Moreover, other vaccines are

currently in the final testing stage, which could bring even more options to the public.

Some healthcare experts speculate that approximately 1.5 billion people globally will

MARK LUSCHINI, CMT be vaccinated by next winter if all goes well. That will lead to a further improvement in

Chief Investment Strategist

employment, consumer and business sentiment, and aggregate demand.

President and Chief

Investment Officer, Janney

Capital Management PATH TO NEW NORMAL which would defer the more positive growth

outlook we envision beginning sooner in the

Mark Luschini serves as With less fear of getting infected, consumers New Year.

Janney’s Chief Investment should return to shops, restaurants,

Strategist and leads the hotels, cruise ships, airplanes, etc. This

Investment Strategy Group, Stimulus and Growing Deficit

which sets the firm’s view on will have a beneficial impact on business

macroeconomics, as well as capital expenditures, which responds The long-term implications of aggressive

the equity and fixed income to consumption with a lag, along with policy stimulus will not likely be benign.

markets. In addition, Mark profit growth. Increased profits refuel the What form it takes may be a matter

is the President and Chief business cycle and beget hiring which of debate, but there is little doubt it will

Investment Officer of Janney

begets spending—critical as it represents have consequences.

Capital Management (JCM),

the asset management approximately 70% of the U.S. economy.

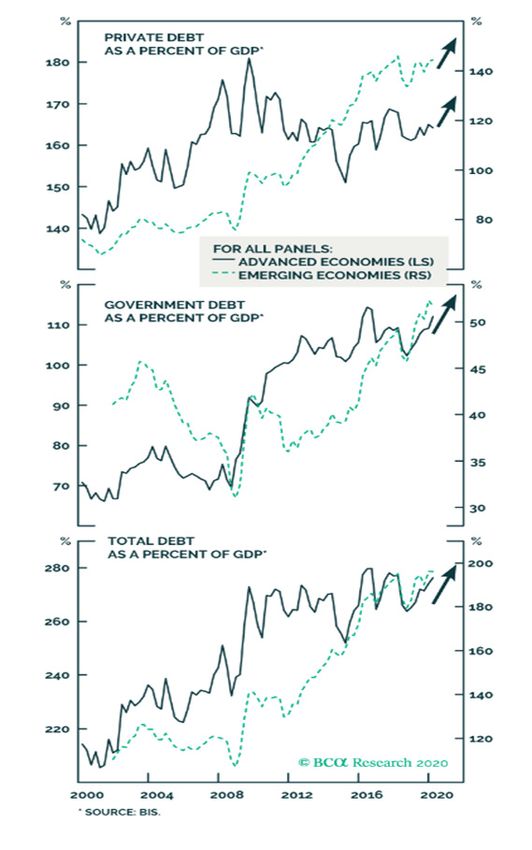

As a share of U.S. GDP, total debt has spiked

subsidiary of Janney

Montgomery Scott. Under Despite this optimistic base case, investors near a record high and, in particular, total

his leadership, JCM has must have contingencies ready. Additional nonfinancial debt has surged to new all-time

delivered competitive results waves of infections cannot be entirely ruled highs. This reflects two phenomena. First,

across its suite of investment out between now and when the vaccinations the denominator of the ratio—GDP—has

strategies and grown its are administered to large enough of the collapsed. So, while debt was already close

assets under management

general population to begin to achieve to 80% of GDP prior to the pandemic, the

to more than $3.5 billion.

herd immunity. Therefore, lockdowns might collapse in GDP in the second quarter of

Mark has spent more than 2020 grew the proportional percentage of

thirty years in the investment

continue deeper into 2021 than anyone

industry. He draws on that would hope. debt outstanding. Second, total debt also

experience to speak on topics highlights the rapid increase in government

related to macroeconomics Thus, we could still face periods of deficits due to the combination of 1) the

and the financial markets at downward pressure on activity, yields, and budget shortfall that already existed and was

seminars, client events and stocks. Indeed, even if the vaccines enjoy growing, plus 2) the deficit spending to fund

conferences. He is frequently widespread adoption, near-term threats to

quoted in publications

the stimulus programs to date.

economic activity remain. The realization

ranging from the Wall Street

that the end of the pandemic is close This problem is repeated around the world.

Journal and Barron’s to

the New York Times and may prompt a temporary period where As Chart 1 demonstrates, nonfinancial debt

USA Today. In addition, he households hunker down and behave in levels across developed and emerging-

regularly appears in various a very conservative fashion. After all, few market countries alike are rising rapidly.

media outlets including consumers will want to contract the virus Moreover, debt loads in emerging markets

CNBC, Fox Business News, are also extremely elevated. The latter is

and Bloomberg Television

just before a vaccine becomes available.

and Radio. He has an particularly worrisome since in many cases,

Moreover, the sight of the end of the that debt is dollar-denominated. The recent

undergraduate degree in

Psychology and an MBA lockdowns reduces the fiscal authorities’ weakness in the dollar, a trend we expect

in Finance from Gannon urgency to provide additional and/or to continue, will help for now. However, the

University and holds the necessary support to the underemployed absolute levels weigh on the service costs

Chartered Market Technician population, small businesses, and even

(CMT) designation from

and crowd out other necessary investment

certain levels of government. These many of these countries need to make in

the Market Technicians

Association.

dynamics could prompt a deep contraction order to evolve and grow.

in spending in the first quarter of 2021,

© JANNEY MONTGOMERY SCOTT LLC • MEMBER: NYSE, FINRA, SIPC • JANNEY OUTLOOK 2021 • REF: 168315-1220 • PAGE 4 OF 10

Chart 1: Private and Government Debt as Percentage of GDP exaggerated during the pandemic, it should. Between a

practice of yield curve control as a means of pinning interest

rates low, as is currently being practiced by the Bank of

Japan and the Reserve Bank of Australia, or the Bank of

England explicitly stepping in to buy the government’s

issuance of bonds to spend on coronavirus relief programs,

it is just around the corner if not already here.

While that likely has inflationary consequence, it is probably

more of a worry for later in the decade than 2021. Keep

in mind that inflation is not a linear process. Once it starts

to rise, it becomes very hard to control. In this regard,

the experience of the late 1960s is extremely instructive.

Through the 1960s boom, inflation was well behaved,

contained between 0.7% and 1.2%. Then it started to rise

in 1966, and quickly hit 6.1% by 1970. While the average-

inflation target the Fed recently adopted is well intentioned,

in an environment where governments are unlikely to

curtail deficits in any hurry, it could easily unleash a long-

term inflationary trend. Stay tuned.

China’s Global Influence Remains Strong

In our judgment, the biggest geopolitical risk remains

China, although any re-engagement with Iran to allow the

U.S. to pivot militarily toward China could be tricky as well.

China has expanded its global influence. In the wake of the

2008 crisis, the Communist Party was forced to change its

national strategy to better handle demographic decline,

structural economic transitioning, and rising social instability.

Slower trend growth increases long-term risks to its single-

party rule, and that caused the Chinese Communist Party

to shift the basis of its command-control from rapid income

growth to nationalism. Hence, Beijing has aggressively

sought a technological “Great Leap Forward” to improve

productivity while adopting a much more assertive foreign

policy to build a sphere of influence in Asia Pacific. Indeed,

its recent declaration of a “dual circulation” policy speaks to

(Source: Bank for International Settlements) the need to continue exporting while buying time to build its

internal consumption and self-reliance.

Going forward, either rising savings or faster nominal GDP

President Xi Jinping’s “New Era” has led to a backlash from

growth will be needed to cause the debt ratios to decline.

foreign powers, most markedly because of COVID-19, but

The first option is difficult; increasing savings is deflationary

also with the removal of Hong Kong’s autonomy, saber-

and it could worsen the debt arithmetic by keeping real

rattling in neighboring seas, and politically motivated

interest rates stubbornly high. Instead, we expect fiscal

boycotts of neighboring countries like Australia. China

and monetary policy to work in tandem to lift inflation and

is increasingly fearful of a U.S. containment policy and is

deflate the global debt load.

adopting a new five-year plan built on accelerating its quest

Modern Monetary Theory and Inflation for economic self-sufficiency and technological leadership.

The rising popularity of Modern Monetary Theory (MMT) President-elect Biden could seek to engage China to

fits within this paradigm shift. manage against a dangerous rise in tensions, while

approaching allies with a desire for multilateralism. Biden

MMT posits that as long as governments issue debt in their will start by trying to lower tensions with Beijing, which is

own currency, central bank money printing can finance the positive for global equity markets until otherwise indicated.

deficit. The only constraint on policymakers becomes the However, if China becomes convinced that Biden is not

level of inflation that society tolerates. If this sounds familiar attempting a real diplomatic reset, but is instead pursuing

given the actions of the Federal Reserve since the Great a containment policy and technological blockade, then it

Financial Crisis, and that which has only become even more may turn increasingly aggressive over rising Taiwanese pro-

© JANNEY MONTGOMERY SCOTT LLC • MEMBER: NYSE, FINRA, SIPC • JANNEY OUTLOOK 2021 • REF: 168315-1220 • PAGE 5 OF 10independence sentiment. A Taiwan Strait crisis is therefore EQUITY MARKETS

possible and that could have a significant impact on markets,

since it sources many global products and its seas are a The following comments express of our central view that

conduit for a tremendous amount of trade. This situation will the recovery will persist at an above-trend pace in 2021.

demand close monitoring in the months to come. This, in turn, should result in higher stock prices, especially

for value-oriented, cyclical stocks, as well as higher yields

Economic Growth Slows, but Not Fading and commodity prices.

Turning back to the domestic front, data has shown a loss • G

lobal Equity Markets – U.S. equities should continue

of momentum in the last several weeks, but not so much to to do well. However, it is time to stage capital into

suggest that the recovery is fading materially. those equity bourses that are levered to economic

growth, such as Europe and Japan. Also, favor emerging

Various regional Federal Reserve surveys still convey a markets as they should benefit from the increased

positive message about activity in geographies throughout demand for commodities.

the country, job growth has continued, wages are

improving, savings remain elevated, and consumer debt • Sectors – Overweight Industrials, Materials, and Energy,

levels—and the service cost associated with it—remain and look to add Financials as the yield curve steepens.

very manageable. Housing continues to elicit remarkable Sectors that are less economically sensitive, such as

strength, and residential investment—important given that Staples and Utilities should be Underweight. Also, favor

it is unmatched in terms of the multiplier effect it has on small company stocks over their larger brethren as they

economic activity—is growing smartly. will prosper while domestic conditions strengthen.

While the Senatorial runoff in Georgia, scheduled for • Commodities – A weaker dollar and the emergence

January 5th, is a wild card given it could tilt the balance of inflation should boost the prospects for this complex.

of political power from gridlock if Republicans keep one Increasing demand should help oil prices to rise while

or both seats, to one-party rule if not. Regardless, the industrial and precious metals stand to benefit from

marginal advantage the Democratic Party would hold if increased manufacturing activity, alternative energy

they win both seats probably means some compromise on adoption, and profligate fiscal policies designed to spur

party issues will be needed for significant legislative action economic growth.

to be taken. That should help to neutralize the worries of Our prognostication for the U.S. stock market’s path

market participants that higher corporate taxes and tighter forward includes three potential outcomes that emanate

regulation would impair profit margins and dim the earnings from various economic scenarios that could unfold. We

picture for corporations. assign a likelihood to each to express our confidence level

in the forecast presented. In preview, we skew decidedly

Brighter View of What is to Come bullish which is indicative of our belief in the sustainability

The swift recovery in business activity, a reduction in global of the global equity rally.

economic uncertainty, a likely fiscal package, and the

launch of a series of vaccines with high efficacy, lead us to

be quite sanguine about the macroeconomic backdrop.

The fact that governments around the world have acted

post haste in adopting similar policies to restore activity

to pre-pandemic levels only reinforces our view. While

the surroundings of the moment are still murky, even grim

in some cases, there are very positive developments

occurring. Moreover, a means to thwart the coronavirus

from inducing further human suffering and economic

damage, which was once thought to be a distant hope, is

now approaching rapidly. The new normal, may include a

different way to do business, dine, shop, and live, but at

least it will be a safer path forward, and that pays dividends.

© JANNEY MONTGOMERY SCOTT LLC • MEMBER: NYSE, FINRA, SIPC • JANNEY OUTLOOK 2021 • REF: 168315-1220 • PAGE 6 OF 10VARIOUS ECONOMIC SCENARIOS AND PROBABLE OUTCOMES

S&P 500 is 3,667 at the time of this writing.

Scenario 1: Mini Boom Scenario 2: Sturdy if Unspectacular Growth

The economy experiences a slight downshift in growth early Growth in the economy stalls. However, Congress is able to

in the year due to coronavirus mitigation efforts and the fiscal settle on a modest relief package, albeit one that leaves many

cliff, which hits for more than 10 million workers that saw their without income near previous employment. The adoption of

pandemic relief assistance programs expire in late December. the vaccinations is slower than hoped, leading to an extension

of social safety measures longer than anticipated.

However, the economy’s momentum carried over from

2020 is sufficient for employment to continue to improve. In turn, delays in reopening industries such as travel, leisure,

Ultimately, a new fiscal package is delivered to extend relief and entertainment, which represent 10% of the economy but

to those displaced workers until they can be reabsorbed 25% of employment, dampens consumer confidence.

into jobs that are opening quickly as mitigation protocols

Still, a supportive Federal Reserve and low yields on

begin to loosen.

interest-bearing instruments leads investors to buy stocks.

Commercial distribution of vaccines for the coronavirus reach With the output gap remaining high, inflation stays at non-

enough mass around mid-year to restore activity closer to threatening levels, therefore interest-rate sensitive sectors

pre-pandemic levels. The combination ignites a spurt of perform well.

growth at an elevated rate.

Growth stocks continue their leadership, with Technology

Risk assets rally as it occurs concurrent with similar and tech-related, Health Care, Utilities, and Consumer

sequencing around the world. While U.S. equities rise, led by Staples, doing well. While the Biden Administration turns

pro-growth sectors such as Industrials, Materials, Energy, and the heat down on foreign policy matters in general, the

Financials, better returns are generated in overseas markets bipartisan support for a tough-on-China stance keeps trade

where the gearing is more heavily tilted toward cyclicals. tensions elevated and Sino-American relations iced.

Still, rising corporate profits and estimates for double-digit The defensive nature of the S&P 500 keeps it among the

gains through 2022, coupled with multiple expansion, lead performance leaders once again and global investors bid

the S&P 500 to 4,500. the market higher by about 6% to 3,900.

Probability: 65% Probability: 30%

Scenario 3: Structural Issues Linger BOTTOM LINE: ENSEMBLE FORECAST

While the economic recovery has been remarkably strong The economy is mending. The pace of growth could

to date, the policies unleashed to spur its growth have been accelerate if three things conspire:

unprecedented. The level of global indebtedness is spiking, 1) Organic growth from the natural release of pent-up

some dollar-denominated debt loads in countries like Turkey,

demand as reopening continues,

Chile, and South Africa are nearly untenable, and in some

cases monetary policy has spilled into an extension of fiscal 2) another fiscal relief stimulus is provided to supplement the

policy thereby blurring the lines between institutions that void in incomes caused by the involuntary job losses, and

heretofore operated with at least feigned independence.

3) the swift and wide adoption of available vaccines leads

The new Administration will engender enough bipartisanship

to herd immunity and socioeconomic normalcy perhaps by

to pass some tax increases and tighten regulations. Other

the middle of the year.

fiscal accords are viewed suspiciously by market participants

and while the economy grows, the stock market’s valuation There are domestic concerns to overcome, but more

compresses as the risk premium expands. Concerns so, it is exogenous risks that stand as a greater threat

about subdued growth due to structurally higher levels to undermining our sanguine views. Accounting for the

of unemployment and softening demand incite whispers

probabilities assigned to the scenarios presented, our

of deflation. Efforts to bring back production of goods of

ensemble price target for the S&P 500 Index is up more

national interest and other industry is disruptive to supply

than 15% to roundly 4,250.

chains and the cost of goods rises, inviting an alternative

theory of stagflation into consideration.

Bonds rally or fall depending on the scenario that unfolds,

but in either case, stocks decline on lower profit expectations

and S&P 500 index falls to 2,950.

Probability: 5%

© JANNEY MONTGOMERY SCOTT LLC • MEMBER: NYSE, FINRA, SIPC • JANNEY OUTLOOK 2021 • REF: 168315-1220 • PAGE 7 OF 10FIXED INCOME & INTEREST RATES

For the fixed income markets, and indeed many of our personal experiences, 2020 has

been a play in three acts. There was the benign introduction, then a seemingly impossible

conflict, and finally a long resolution—which continues.

At risk of sounding self-congratulatory, we Chart 2: While the Fed Will Likely Pin Short-Term

identified market plumbing in last year’s Yields, Longer-Term Bond Yields Should Rise

Moderately (Dotted Lines Represent Forecasts)

Outlook 2020 report as the source of the

financial conflict that emerged and Fed 2.50%

rate cuts as the cure. Both came to pass,

2yr Treasury 10yr Treasury 30yrTreasury

2.15%

GUY LEBAS, CFA® although the catalyst was unexpected and 2.00%

Chief Fixed Income Strategist tragic. Similarly, we identified the rebound 1.50%

Director of Custom Fixed in credit in our Mid-Year 2020 Outlook, and 1.35%

Income Solutions, Janney credit has indeed rebounded impressively. 1.00%

Capital Management 0.50%

Guy LeBas is responsible SUPPORT FOR GROWTH 0.28%

0.00%

for providing direction to THROUGH 2021

the firm’s clients on the

macroeconomic, interest With about two weeks left in the year, (Source: Janney Investment Strategy Group; Bloomberg)

rate, and bond market benchmark 10-year Treasury yields declined

investing climate. in 2020 to 0.93% from 1.92% after having

Guy authors bond reached all-time lows over the summer. Recent qualitative comments in Institute

market periodicals which Investment-grade corporate bond spreads for Supply Management (ISM) survey data

provide relative value

look to end the year roughly unchanged after have indicated large firms are looking to

recommendations across push higher costs onto consumers, usually

the fixed income spectrum. having violently widened in March/April and

subsequently rebounded. This sharp decline an early indication of inflation risks. Given

Bloomberg named him the

most-accurate forecaster of in interest rates combined with ultimately the last decade, it is important to remain

the Treasuries market in 2015 unchanged spreads helped power most fixed skeptical about our economy’s probability

and previously recognized income markets to strong returns in 2020, of returning to the Fed’s 2% inflation target,

him as a “Bloomberg Best” but rarely have so many forces lined up

for his work in bond market

despite a host of very prominent risks.

on the inflationary side of the fence. The

forecasting.

Table 1: 2020 Returns by Sector net impact of these economic growth and

Prior to joining Janney in inflationary forces is that longer-term (10-to-

2006, Guy served as Interest

Rate Risk Manager for U.S.

30-year) interest rates are likely to rise in

Trust’s bank asset and liability 2021. Specifically, we are looking for 10-year

portfolios, a role in which he Treasury yields to end next year in the 1.25%-

oversaw risk and return on 1.45% range.

an $11 billion balance sheet.

He received his education

from Swarthmore College Chart 3: Banks Appear to Be Holding Excess Credit

and is a CFA Charterholder. Reserves; Releasing These Reserves Should Support

Credit Markets in 2021

(Source: Bloomberg/Barclays Indices)

$70bln

17.50%

$60bln

In the coming year, we anticipate further

15.50%

normalization in economic growth as the 13.50%

Loan Loss Provision at

$50bln

labor market heals from the 2020 downturn, 11.50% US Banks (Right Axis)

$40bln

HY Yield Credit Spreads

and knock-on effects from housing strength 9.50% (Qrtly Avg; Left Axis)

$30bln

support many other areas of growth as well. 7.50%

$20bln

5.50%

When it comes to inflation, the jury is still 3.50% $10bln

out. Both Fed and fiscal policy are broadly

1.50% $0bln

inflationary. Although the violent demand

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

shock this past year dampened inflation in

the short term, many economic changes are, (Source: Janney Investment Strategy Group; FDIC; Bloomberg/Barclays)

similar to policy, broadly inflationary.

© JANNEY MONTGOMERY SCOTT LLC • MEMBER: NYSE, FINRA, SIPC • JANNEY OUTLOOK 2021 • REF: 168315-1220 • PAGE 8 OF 10CREDIT MARKETS Meanwhile, trends for stressed issuers—a handful of

states come easily to mind—have accelerated through

When it comes to credit conditions, economic growth the economic downturn. On the other side of the coin,

should help. However, there is an additional factor: bank municipal buyers have been very active, partially as

reserves. The banking sector added credit reserves into rebalancing dollars come out of equities and go into fixed

the March downturn that, on average, have exceeded income. The net effect is, in our view, that high-grade muni

actual losses. markets will largely track Treasury yields, at least in the

In 2021, it is likely the banking sector will be able to release beginning part of 2021, with muni/Treasury ratios stable.

these reserves, add to capital (especially if regulators Still, given the risk of accelerating deterioration in riskier

prevent them from returning capital to owners), and state and local government credits, we recommend an

increase lending activity. With positive lending forces in up-in-quality (AA- and higher) bias for the coming year.

the banking sector, the credit markets are likely to respond The opposite goes for diversified health care and higher

with tightening spreads, which would allow corporate and education, in which incremental spread for 2- to 7-year

taxable muni credit, especially lower-investment-grade bonds in the A-ratings range is generally worth the risk,

and high yield sectors, to perform well. In that sense depending on the credit.

(and thanks in large part to banking reserves), the post- While the strongest returns for fixed income are likely

coronavirus financial landscape is likely to proceed much behind us—it’s hard to see high single-digit results

as the post-Global Financial Crisis landscape did a decade repeating themselves given the low level of interest

ago. The primary difference is that everything in 2020 is rates—there are still opportunities to generate reasonable

unfolding at two to four times the speed it did in 2009. performance. The key, we believe, lies in taking credit risk

more so than interest rate risk in 2021 and, depending on

MUNICIPAL MARKETS how the credit cycle evolves, perhaps beyond.

Finally, we’ll touch on the municipal markets.

Chart 4: Current 10yr Muni/Treasury Ratio Well Below Median,

but Supported by Strong Demand

(Source: Janney Investment Strategy Group; Bloomberg)

Despite pervasive fears of tax shortfalls and revenue

declines across sector, the fiscal impact of the coronavirus

has proven manageable for the vast majority of issuers. A

first round of fiscal transfers from the CARES Act to state

and local governments and the prospects of a second

round went a long way to filling budget holes.

Sectors most affected (health care, transportation,

education) have, with a few notable exceptions, pulled

through the worst of the downturn with only moderately

impaired credit profiles. Perhaps the biggest boon,

however, is not fiscal transfers, but rather record-low

borrowing costs, which have made it easy for all but the

most stressed issuers to borrow through temporary gaps.

© JANNEY MONTGOMERY SCOTT LLC • MEMBER: NYSE, FINRA, SIPC • JANNEY OUTLOOK 2021 • REF: 168315-1220 • PAGE 9 OF 10Disclosures Definition of Ratings

This is for informative purposes only and in no event should be construed as a Overweight: Janney ISG expects the target asset class or sector to outperform the

recommendation by us or as an offer to sell, or solicitation of an offer to buy, any comparable benchmark (below) in its asset class in terms of total return.

securities. The information given herein is taken from sources that we believe to be

Marketweight: Janney ISG expects the target asset class or sector to perform in line with

reliable, but is not guaranteed by us as to accuracy or completeness. Opinions expressed

the comparable benchmark (below) in its asset class in terms of total return.

are subject to change without notice and do not take into account the particular

investment objectives, financial situation, or needs of individual investors. Employees Underweight: Janney ISG expects the target asset class or sector to underperform the

of Janney Montgomery Scott LLC or its affiliates may, at times, release written or oral comparable benchmark (below) in its asset class in terms of total return.

commentary, technical analysis, or trading strategies that differ from the opinions

expressed here.

Benchmarks

Returns reflect results of various indices based on target allocation weightings.

Weightings are subject to change. Index returns are for illustrative purposes only and Asset Classes: Janney ISG ratings for domestic fixed income asset classes including

do not represent the performance of any investment. Index performance returns do not Treasuries, Agencies, Mortgages, Investment Grade Credit, High Yield Credit, and

reflect any management fees, transaction costs, or expenses. Indexes are unmanaged, Municipals employ the “Barclays U.S. Aggregate Bond Market Index” as a benchmark.

and you cannot invest directly in an index. Treasuries: Janney ISG ratings employ the “Barclays U.S. Treasury Index” as a benchmark.

Performance data quoted represents past performance and is no guarantee of future Agencies: Janney ISG ratings employ the “Barclays U.S. Agency Index” as a benchmark.

results. Current returns may be either higher or lower than those shown.

Mortgages: Janney ISG ratings employ the “Barclays U.S. MBS Index” as a benchmark.

This report is the intellectual property of Janney Montgomery Scott LLC (Janney) and

may not be reproduced, distributed, or published by any person for any purpose without Investment Grade Credit: Janney ISG ratings employ the “Barclays U.S. Credit Index”

Janney’s prior written consent. as a benchmark.

This presentation has been prepared by Janney Investment Strategy Group (ISG) and High Yield Credit: Janney ISG ratings employ the “Barclays U.S. Corporate High Yield

is to be used for informational purposes only. In no event should it be construed as Index” as a benchmark.

a solicitation or offer to purchase or sell a security. The information presented herein Municipals: Janney ISG ratings employ the “Barclays Municipal Bond Index” as a benchmark.

is taken from sources believed to be reliable, but is not guaranteed by Janney as to

accuracy or completeness. Any issue named or rates mentioned are used for illustrative

purposes only and may not represent the specific features or securities available at a Analyst Certification

given time. Preliminary Official Statements, Final Official Statements, or Prospectuses for

any new issues mentioned herein are available upon request. The value of and income We, Mark Luschini and Guy LeBas, the Primarily Responsible Analysts for this report,

from investments may vary because of changes in interest rates, foreign exchange hereby certify that all views expressed in this report accurately reflect our personal

rates, securities prices, and market indices, as well as operational or financial conditions views about any and all of the subject sectors, industries, securities, and issuers. No

of issuers or other factors. Past performance is not necessarily a guide to future part of our compensation was, is, or will be, directly or indirectly, related to the specific

performance. Estimates of future performance are based on assumptions that may not recommendations or views expressed in this research report.

be realized. We have no obligation to tell you when opinions or information contained in

Janney ISG presentations or publications change.

© JANNEY MONTGOMERY SCOTT LLC • MEMBER: NYSE, FINRA, SIPC • JANNEY OUTLOOK 2021 • REF: 168315-1220 • PAGE 10 OF 10You can also read