HSBC Kapitalmärkte Kompakt Performance trotz(t) Unsicherheit - HSBC Global Asset ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

HSBC Kapitalmärkte Kompakt

Performance trotz(t) Unsicherheit

17. Januar 2020

Dieses Dokument inkl. aller enthaltenen

Informationen ist nicht für Kleinanleger (Privatkunden)

i. S. d. Artikels 4 Abs. 1 (11) der Richtlinie

2014/65/EU bestimmt und darf weder ganz noch in

Teilen an diese weitergegeben werden.

Performance trotz(t) Unsicherheit

Dr. Axel Cron

Chief Investment Officer

Dieses Webinar liefert einen Überblick über das wirtschaftliche Umfeld und dient ausschließlich Marketingzwecken. Die Angaben stellen in keiner Weise eine

Finanzanalyse, Anlageberatung bzw. eine Kauf- oder Verkaufsempfehlung dar. Die Angaben wurden nicht in Einklang mit den Rechtsvorschriften zur

Förderung der Unabhängigkeit von Finanzanalysen erstellt und unterliegen auch keinem Verbot des Handels im Anschluss an die Verbreitung von

Finanzanalysen.

Das Zeitalter der Unsicherheit

Signifikanter Anstieg der Verunsicherung

Index level

Global Economic Policy Uncertainty Index (3m avg)

350

300

US presidential

election

250 Sovereign debt crisis

in Europe and US

fiscal cliff

9/11 Lehman brothers

200 terrorist Iraq war and global Brexit referendum

attack and markets turmoil

outbreak

Asia of SARS

150 crisis

Financial

credit

crunch

100

US-China Trade

50 tensions

-

1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017 2019

Source: Bloomberg, HSBC Global Asset Management, November 2019

3

2019 – Ein Ausnahmejahr

Performance 2019 und seit 2010

USD Total Returns

40%

30% Since 2010 (annualised) 2019

20%

10%

0%

-10%

-20%

Government Bonds Corporate Bonds EM Debt Equity Other Asset Classes

-30%

US Cash US Treasuries Global Bonds Global ILBs (H) Global IG Credit Global HY USD EM Debt Local EM Debt US Equities Global Equities EM Equities WTI Oil Gold US Dollar

(H) (H) Credit (H)

Source: Bloomberg, HSBC Global Asset Management, 30 December 2019. Any performance information shown refers to the past and should not be seen as an indication of future returns.

4

Performance trotz(t) Unsicherheit

Mögliche Erklärungsversuche (I)

Source: Bloomberg, Macrobond, HSBC Global Asset Management, 31 October 2019. Any views expressed were held at the time of preparation and are subject to change without notice. Any forecast, projection or target where provided is

indicative only and is not guaranteed in any way.

5

Performance trotz(t) Unsicherheit

Mögliche Erklärungsversuche (II)

Quarterly

change Global HY spread DM equities earnings yield EM equities earnings yield

2,0%

1,5%

1,0%

0,5%

0,0%

-0,5%

2018 Q1 2018 Q2 2018 Q3 2018 Q4

Source: Bloomberg, Macrobond, HSBC Global Asset Management, 31 October 2019. Any views expressed were held at the time of preparation and are subject to change without notice. Any forecast, projection or target where provided is

indicative only and is not guaranteed in any way.

6

Performance trotz(t) Unsicherheit Mögliche Erklärungsversuche (III) Source: HSBC Global Asset Management, November 2019 7

Performance trotz(t) Unsicherheit

Mögliche Erklärungsversuche (IV)

Near 40-year low

Source: HSBC Global Asset Management, November 2019 82020 – Perspektiven

9Was “diskontiert” der Markt?

Pessimismus im Hinblick auf Wachstum und Inflation

Index Index

Market-implied

AMG Growth

Market-implied Growth Market-implied

AMG Inflation

Market-implied Inflation

106 100

Phantom Goldilocks Back to Age of

104 uncertainty - 99

recession reality

Recession

worries

102 98

100 97

98 96

96 95

94 94

92 93

90 92

2015 2016 2017 2018 2019 2015 2016 2017 2018 2019

*These indicators are the market performance of an equal volatility long-short portfolio of (1) growth asset

classes against defensive asset classes (implied growth index), and (2) inflation-hedged asset classes

against inflation-vulnerable asset classes (implied inflation index)

10

Source: HSBC Global Asset Management, November 2019.Rezessionsgefahr?

… obwohl…

Excess return (relative to duration matched US Treasuries),

10 CCC Excess Return B Excess Return BB Excess Return

8

6

4 What’s going on?

2

0

-2

ppts

-4

Jan 19 Mrz 19 Mai 19 Jul 19 Sep 19 Nov 19

Source: HSBC Global Asset Management, November 2019 11Globales Wachstum – Langsam, aber sicher

Rezession ebenso unwahrscheinlich wie starker Aufschwung

Nowcast (%)

12,00

10,00

8,00

6,00

4,00

2,00

0,00

-2,00

Global US Euro Area Japan UK Canada EM (ex. Asia ex China India Turkey Latin Brazil Mexico

China) Japan America

Dezember 2017 November 2019

Source: HSBC Global Asset Management, December 2019.

Any views expressed were held at the time of preparation and are subject to change without notice. While any forecast, projection or target where provided is indicative only and not guaranteed in any way. HSBC Global Asset Management

accepts no liability for any failure to meet such forecast, projection or target. 12Die Legende von der Rezession

Die Natur der Zyklen hat sich verändert

Growth

Australia 1992-today 107

Australia 1962-1982 83

UK 1956-1974 71 Old cycle New cycle

Expansion

France 1975-1993 70

US 1991-2008 67

.

UK 1992-2008

. 64

.

Recession

US 2010-today 41

0 20 40 60 80 100 120

Expansion = no. of consecutive quarters of positive yoy real GDP

growth

Quelle: Bloomberg, HSBC Global Asset Management, Dezember 2019.

13Globale Inflation

Unter Ziel

1,0 pp deviation in y/y inflation from target

2% target 2.5% target

0,5

0,0

-0,5

-1,0

-1,5

Latest core inflation

-2,0

3% to 4.5% target

-2,5

US Can UK EZ Kor Jpn Aus Tha Mex ZAF Bra Chn

Source: HSBC Global Asset Management, November 2019 14Geldpolitik (II)

„Repo-Calypse Now“

28,00 120,00

3

26,00

100,00

Central Banks - Balance Sheets as % of GDP

2,5

24,00

22,00 80,00

US Excess Reserves

2

20,00

60,00

18,00 1,5

16,00 40,00

1

14,00

20,00

12,00 0,5

10,00 0,00

0

Federal Reserve Balance Sheet

European Central Bank Balance (rhs)

Bank of Japan Balance Sheet as (rhs) Required Reserves (trn USD)

Quelle: Bloomberg, HSBC Global Asset Management, Dezember 2019.

Reserves including Vault Cash (trn USD)

15Globale Fiskalpolitik

Zunehmend unterstützend

Source: HSBC Global Asset Management, November 2019.

Any views expressed were held at the time of preparation and are subject to change without notice. While any forecast, projection or target where provided is indicative only and not guaranteed in any way. HSBC Global

16

Asset Management accepts no liability for any failure to meet such forecast, projection or target.Unternehmen – Gewinne

Einstelliges Wachstum in Sicht

% World ex US consensus EPS growth forecast

30

US consensus EPS growth forecast

25

20

2018

15 2017

10

2020

5 2014

2012 2013

0

2019

2015

-5 2016

-10

2012 2013 2014 2015 2016 2017 2018 2019

Source: HSBC Global Asset Management, November 2019.

This chart tracks the live calendar year earnings growth expectations and shows the growth rate between the latest calendar year-end EPS estimate and the previous year-end trailing EPS.

Note: for 2020 growth rates we proxy year-end 2019 trailing earnings growth with the latest 2019 expectations

17Unternehmen – Gewinne

Talsohle durchschritten?

Trailing earnings growth (qoq, local terms) vs 3m ago

Source: HSBC Global Asset Management, Nov. 2019.

18Langfristige Rendite- / Risikoprofile

10%

Aktien

9%

Anleihen (Industrieländer)

Anleihen (Emerging Markets) Frontier Equity (8,2%) Private Equity (8,4%)

Anleihen (Unternehmen) EM Equity (8,1%)

8%

Alternative Anlageklassen Asia ex Japan Equity (7,6%)

7%

Local EMD (6,6%) Japan Equity (6,4%)

6% US Equity (5,6%)

Eurozone Equity (5,9%)

Asia Local Bonds (5,3%)

5% DM Equity (5,7%)

Erwartete Rendite

Commodities (4,4%)

4% Asia HY (4,3%)

Hedge Funds (3,5%)

3%

US HY (2,1%)

2% EMD Hard Currency (1,7%)

Lev Loans (1,4%)

EUR HY (1,6%)

1% EUR IG (0,6%) Asia IG (1,4%)

US IG (0,6%)

0% US 2y Treasuries (0,4%)

US 10y Treasuries (-0,3%) Japanese JGBs (-0,6%)

-1%

German Bunds (-1,1%)

-2%

-3%

0% 5% 10% 15% 20% 25% 30%

Erwartete Volatilität

Prognosen und Zielvorgaben sind rein indikativ und in keiner Weise garantiert. Quelle: HSBC Global Asset Management. In EUR. ASIA HY, ASIA IG, EMD Hard Currency, Japanese JGBs, US HY, US IG, 2y US Treasuries, 10y

US Treasuries und Lev Loans in EUR hedged. Alle anderen Assetklassen unhedged. Stand Januar 2020.

19Zusammenfassung

Valuation signals Business cycle signals Macro regime Market signals

Leading

Nowcast Nowcast Inflation Time Series Market narratives &

vs 3m ago vs 12m ago vs 3m nowcast (3m Monetary bias Fiscal bias

(3m avg) momentum model Momentum sentiment

ahead)

Global Bonds p q pp

Global Credit IG p q pp "Top of mind" themes:

World

Global Credit HY

2.3 pp

Trade truce, Fed policy

and macro data

Global Equities pp

US 10y Treasuries p q pp Sentiment has improves

Muted inflation pressures and

US IG Credit p q 2.0 downside risks to growth 2018/19 fiscal boost fading. pp since August

US

2.6 "Fed on hold" and "repo"

US HY Credit rising make "insurance" rate cuts No meaningful plans for 2020

pp narratives dominate

likely

US Equity pp news, but less central

Germany 10y Gov't Bond p The ECB delivered a pp

substantial easing package. It Increased focus on ECB

Eurozone

Eurozone IG Corporate Bonds p 1.2 also now expects to maintain pp policy actions. "Italy" is a

0.0 stable rates at current or lower levels

Modest easing

pp highly negative narrative,

EUR HY

until core inflation trend but not central

Eurozone Equities improves pp

UK 10y Gov't Bond p BoE has acknowledged pp Sentiment is being pulled

increased downside risks to

p pp

UK

UK IG Corporate Bonds -0.9 2.0 Bias to ease down by Brexit

growth. Policy path

uncertainties

UK Equities stable dependent on Brexit pp

q pp

Japan

Japan 10y Gov't Bond 0.7 VAT hike to be offset by other

-0.4 declining

Unchanged/easing

measures

pp

Japan Equity

pp

Emerging

Local EM Debt

Markets

EM sentiment has

Lower US rates allows EM Loosening across a range of

USD EM Sovereign Bond 1.7 policy easing economies pp improved following news

of a "trade truce"

EM Equity p

Asia Local Bonds p pp

p q Lower US rates and bias to pp

Asia

Asia IG Loosening across a range of

p

4.8 ease in China allows looser

economies

pp

Asia HY EM policy

Asia ex Japan Equity p

As of December 2019. Source: HSBC Global Asset Management. Note: Nowcast vs 3m arrows signal when there is a change in the 3m average Nowcast number that is greater than 0.15% versus 3m ago;

Nowcast momentum is looking at momentum over a 6, 9 and 12m period and giving an overall positive or negative score;

20Frontier Markets

Martin Bechtloff

Sales Manager

Wholesale Business / Insurance & IFA/IAMFrontier Märkte

schnelle Wachstumsraten und niedrige Einkommen

BIP pro Kopf BIP-Wachstum pro Kopf

(USD, Tsd.) (2002-2017, annualisiert)

0% 5% 10% 15%

China

35 Vietnam

Kazakhstan

Romania

Argentina

30 Russia

Indonesia

Sri Lanka

India

25 Bangladesh

Kenya

Brazil

Chile

20 Peru

Jordan

Thailand

Philippines

Turkey

15 Nigeria

Egypt

Pakistan

Colombia

10 Serbia

Poland

South Africa

Mauritius

5 Malaysia

Morocco

Lebanon

Oman

0 Croatia

Hungary

Slowenien

Oman

Ungarn

Rumänien

Brasilien

Jordanien

Kuwait

Griechenland

VAE

Litauen

Chile

Südafrika

Serbien

Marokko

Ägypten

Kolumbien

Sri Lanka

Thailand

Peru

Bahrain

Tschechien

Mauritius

Korea

Tunesien

Mexiko

Malaysia

Russland

Vietnam

China

Indonesien

Katar

Kroatien

Libanon

Estland

Argentinien

Polen

Nigeria

Philippinen

Kenia

Türkei

Kasachstan

Bangladesch

Qatar

Bahrain

Kuwait

Tunisia

Mexico

UAE

Schwellenmärkte 2000 Frontier Märkte 2017 Frontier markets Emerging markets

Quelle: HSBC Global Asset Management, International Monetary Fund, World Economic Outlook Database Schätzungen, Oktober 2017

Nur zu illustrativen Zwecken geeignet.

22Umfassendes Anlageuniversum

Global diversifiziertes Engagement in rund 30 Frontier Markets¹

Litauen Estland

Kroatien

Slowenien

Kasachstan

Rumänien

Serbien

Libanon

Tunesien

Kuwait Pakistan

Marokko

Vietnam

Ägypten

Jordanien

Oman

Senegal Philippinen

Guinea Bissau

Kolumbien Mali VAE

Elfenbeinküste Qatar

Burkina Faso Bahrain

Togo Kenia Bangladesch

Peru

Benin Sri Lanka

Sub-Saharan Africa (11) Mauritius

Nigeria

Latin America (3)

Niger

Asia-Pacific (5) Argentinien

Europe (7)

MENA (10)

Potential ‘off-benchmark’ (numerous)

1. Unser hauseigener Referenzindex beinhaltet 36 Länder, wie in dieser Grafik abgebildet. Als aktive Strategie können jedoch Abweichungen in Bezug auf die gehaltenen Länder bestehen sowie nicht in der Benchmark enthaltene Frontier-

Märkte im Portfolio vertreten sein. Sie werden in der Abbildung nicht gezeigt (darunter Kambodscha, Georgien).

Quelle: HSBC Global Asset Management, Dezember 2019. Nur zu illustrativen Zwecken.

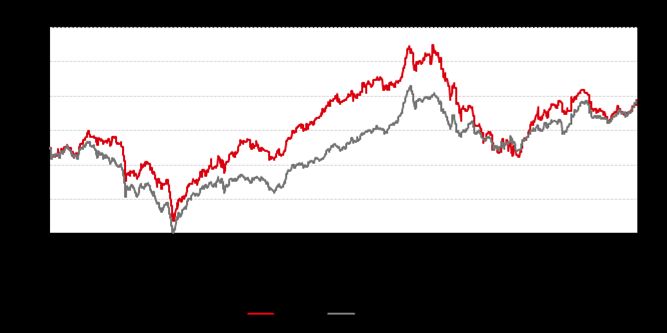

23Vorteile der Diversifikation

Volatilität der Assetklassen Renditen der Assetklassen

(Monatliche Basis, 10 Jahre bis Oktober 2019) (Annualisiert, 10 Jahre bis Oktober 2019)

Schwellenmärkte 17,09% Schwellenmärkte 3,78%

Frontier Märkte 12,30% Frontier Märkte 4,00%

0% 2% 4% 6% 8% 10% 12% 14% 16% 18% 0% 2% 4% 6% 8% 10%

Volatilität Korrelation

(1 Jahr, wöchentliche Renditen) (6 Jahre, wöchentliche Renditen)

50%

40%

30%

20%

10%

0%

Jan 08

Mai 09

Jan 10

Mai 11

Jan 12

Mai 13

Jan 14

Mai 15

Jan 16

Mai 17

Jan 18

Mai 19

Sep 08

Sep 10

Sep 12

Sep 14

Sep 16

Sep 18

Frontier Märkte Schwellenmärkte Entwickelte Märkte

Die hier gezeigten Informationen beziehen sich auf Performance in der Vergangenheit und sollten nicht als Indikator für zukünfitge Renditen angesehen warden.

Quelle: HSBC Global Asset Management, Bloomberg zu Oktober 2019. Monatliche Daten von Oktober 2009 bis Oktober 2019. Frontier Märkte: MSCI Frontier Markets Daily TR Net USD; Schwellenmärkte: MSCI Emerging Markets Daily TR

Net USD. Die gezeigten Daten dienen nur der Veranschaulichung und nicht der Indikation zukünftiger Performance.

24HSBC GIF Frontier Markets

Fondsüberblick

Fondsdetails

Fondsmanager Ramzi Sidaní Benchmark MSCI Select Frontier & Emerging

Lead/Co-Portfoliomanager Markets Capped Net

10 Jahre Branchenerfahrung

Morningstar-Kategorie Aktien Global Frontier Markt

Seit 2016 bei HSBC

-Titelanzahl 50-70 Aktien

Auflegungsdatum Februar 2008

Aktiengewichtung maximal 10% pro Aktie

Basiswährung USD Ländergewichtung maximal 15% pro Land

Geschäftsjahres-ende 31. März Off-Benchmark- Positionen keine Einschränkungen

Fondsvolumen 277 Mio. USD Kasse 0-5%

Investmentgründe

Bietet Zugang zu aufstrebenden Frontier- Markets-Märkten

Outperformance der Benchmark

Niedrige Korrelation der Frontier Markets im Vergleich zu anderen Märkten nutzen

HSBCs Reputation und langjährige Erfahrung in aufstrebenden Märkten

Bei Morningstar über 1 Monat, YTD und über 1 Jahr im ersten Quartil. Im zweiten Quartil über 3 und 5 Jahre1

Quelle: HSBC Global Asset Management. Stand: 31.12.2019. 1Bezieht sich auf die I-Anteilklasse, Quelle: Morningstar.

Zielvorgaben sind rein indikativ und in keiner Weise garantiert.

25HSBC GIF Frontier Markets

Performance und Kosten

Nettowertentwicklung der IC-Anteilklasse in USD (%)

Risiko- und Ertragsprofil1

Geringeres Risiko Höheres Risiko

Typischerweise geringere Typischerweise höhere

Rendite Rendite

1 2 3 4 5 6 7

Anteil- ISIN Ausgabe- Laufende

klasse aufschlag Kosten

AC LU0666199749 Max. 5,00% 2,25% p. a.

ACEUR LU0708055370 Max. 5,00% 2,25% p. a.

AD LU0666200265 Max. 5,00% 2,25% p. a.

ADEUR LU0717916968 Max. 5,00% 2,25% p. a.

IC LU0666200349 Max. 5,00% 1,65% p. a.

ICEUR LU0708055537 Max. 5,00% 1,65% p. a.

ID LU0666200695 Max. 5,00% 1,65% p. a.

IDEUR LU0717918238 Max. 5,00% 1,65% p. a.

XC LU0666200935 Max. 5,00% 1,30% p. a.

XD LU0666201156 Max. 5,00% 1,30% p. a.

Eine Aufstellung der Risiken finden Sie im

Quelle: HSBC Global Asset Management. Nettoperformance in USD per 31.12.2019. Kapitel Weiterführende Informationen.

Die Wertentwicklung in der Vergangenheit ist kein verlässlicher Indikator für die zukünftige Wertentwicklung. Die dargestellte Wertentwicklung basiert auf Netto-

Inventarwerten, weitere Gebühren (soweit diese anfallen) sind in der Darstellung nicht berücksichtigt und wirken sich negativ auf die Wertentwicklung der Anlage aus. 1SRRI (Synthetischer Risiko- und Ertragsindikator) Dieser Indikator beruht

auf historischen Daten; eine Vorhersage künftiger Entwicklungen ist damit nicht möglich. Die Einstufung des Fonds kann sich künftig ändern und stellt keine Garantie dar. Auch ein Fonds, der in Kategorie 1 eingestuft wird, stellt keine völlig

risikolose Anlage dar.

26HSBC GIF Frontier Markets

Länder- und Sektorenallokation – Dezember 2019

Ländergewichtungen (%) Sektorengewichtungen (%)

Kuwait 14,4

Finanzsektor 52,2

Egypt 12,6

United Arab Emirates 10,2 Industriesektor 10,6

Philippines 10,1

Bahrain 7,5 Basiskonsumgüter 9,9

Kenya 6,2

Vietnam 5,8 Zyklische Konsumgüter 8,5

Kazakhstan 5,1

Immobilien 8,2

Romania 4,6

Colombia 3,8

Kommunikation 3,9

Qatar 3,5

Georgia 3,4

Werkstoffe 2,6

Peru 3,0

Mauritius 2,1 Gesundheitssektor 1,8

Nigeria 1,9

Morocco 1,8 Energiesektor 0,5

[Cash] 1,4

Bangladesh 1,0 IT 0,4

Argentina 0,9

Versorger 0,0

Slovenia 0,6

0 2 4 6 8 10 12 14 16 0 10 20 30 40 50 60

Quelle: HSBC Global Asset Management, MSCI zum 31. Dezember 2019.

Als Referenzindex dient der MSCI Select Frontier & Emerging Markets Capped Index. Diese Benchmark dient lediglich der Orientierung und ist in keener Weise garantiert. HSBC Global Asset Management (UK) übernimmt

keine Verantwortung für den Fall, dass die Benchmark nicht outperformt wird.

.

27Zusammenfassung

Umfassendes Wandel Verbraucher Rohstoffreichtum Korrelationen Barrenditen Überzeugende

Anlageuniversum Bewertungen

1 2 3 4 5 6 7

Quelle: HSBC Global Asset Management.

Nur zu illustrativen Zwecken.

28Treffen Sie unseren Fondsmanager persönlich

auf dem Mannheimer Fondskongress 2020

“Frontier Markets – ein Markt für sich?”

Wann: Mittwoch, 29.01.2020

um 14.15 UHR

Wo: Saal 8

Ramzi Sidani

Fondsmanager

HSBC GIF Frontier MarketsPräsentation

E-Mail an fonds@hsbc.de

www.assetmanagement.hsbc.de/de

Unser nächstes

Kapitalmarkt-Webinar:

14. Februar 2020

30Anhang

HSBC GIF Frontier Markets

Fondsüberblick

Anlageziel Anlagestrategie Fondsdetails

Erzielung einer Outperformance Ausnutzung der Ineffizienzen der Frontier Fondsmanager Ramzi Sidaní

gegenüber dem MSCI Select Frontier & Markets durch Konstruktion eines Lead/Co-

Emerging Markets Capped Index diversifizierten Portfolios von attraktiven Portfoliomanager

Exposure zu Ländern, die durch globale Investmentideen 10 Jahre

Emerging-Markets-Equity-Strategien Fundamentales Research als Basis für Branchenerfahrung

nicht abgedeckt werden die Investitionsentscheidung Seit 2016 bei HSBC

Erzielung langfristiger Erträge durch Auflegungsdatum Februar 2008

Aktien mit guten Cash Flows

Basiswährung USD

Geschäftsjahres- 31. März

ende

Fondsvolumen 277 Mio. USD

Investmentteam Investmentgründe

Benchmark MSCI Select Frontier &

Team aus zwei erfahrenen Frontier- Bietet Zugang zu aufstrebenden Frontier- Emerging Markets

Markets-Portfoliomanagern mit Markets-Märkten Capped Net

durchschnittlich 14 Jahren Outperformance der Benchmark

Branchenerfahrung Morningstar- Aktien Global Frontier

Niedrige Korrelation der Frontier Markets

Unterstützt durch das Emerging- Kategorie Markt

im Vergleich zu anderen Märkten nutzen

Markets-Team der HSBC HSBCs Reputation und langjährige Titelanzahl 50-70 Aktien

Erfahrung in aufstrebenden Märkten

Bei Morningstar über 1 Monat, YTD und Aktiengewichtung maximal 10% pro Aktie

über 1 Jahr im ersten Quartil. Im zweiten Ländergewichtung maximal 15% pro Land

Quartil über 3 und 5 Jahre1

Off-Benchmark- keine Einschränkungen

Positionen

Quelle: HSBC Global Asset Management. Stand: 31.12.2019. 1Bezieht sich auf die I-Anteilklasse, Quelle: Morningstar. Kasse 0-5%

Zielvorgaben sind rein indikativ und in keiner Weise garantiert.

32Risiken

Diese Fonds sind nicht für jeden Anleger geeignet. Es ist möglich, dass der Anleger bei Investment in diese Fonds einen

Verlust, auch bis zur Höhe seines gesamten Investments, erleidet.

Für den Fonds/die Strategie werden Anlagen in Schwellenländern getätigt. Diese sind risikoreich, weil sie eine volatile Wertentwicklung

aufweisen und über eine geringe Liquidität verfügen können. Bei Investitionen in Schwellenländer können zudem politische,

Glattstellungs-, Liquiditäts-, Devisen- und Verwahrungsrisiken sowie Risiken in Bezug auf die Rechnungslegungsstandards bestehen.

Aufgrund der Konzentration auf wenige Märkte/Wertpapiere hat der Fonds/die Strategie einen geringeren Diversifikationsgrad und damit

ein höheres Risiko. Der Anteilwert von Aktienfonds/Aktienstrategien kann relativ stark schwanken, auch Kursverluste sind möglich. Der

Fonds/die Strategie tätigt auch Anlagen in kleine Unternehmen. Diese können weniger liquide sein als Anlagen in große Unternehmen

und eine erhöhte Volatilität aufweisen. Daher weisen solche Anlagen ein höheres Risiko auf. Der Fonds/die Strategie kann unter anderem

zu Zwecken der Ertragssteigerung in derivative Finanzinstrumente investieren. Derivate können zu einer wesentlich höheren

Schwankung des Anteilpreises führen als der unmittelbare Erwerb der Basiswerte. Der Fonds/die Strategie investiert auch in Instrumente,

die in anderen Währungen denominiert sind. Hieraus folgt ein Wechselkursrisiko. Ist die Heimatwährung des Anlegers nicht USD, kann

für ihn hieraus ein zusätzliches Wechselkursrisiko resultieren.

Die ausführlichen Risiken können dem Verkaufsprospekt und den wesentlichen Anlegerinformationen (KIID) entnommen

werden.

33Reduced institutional voids can give rise to productivity gains

High

Low productivity in frontier markets may High institutional voids in frontier

be due to underdeveloped: markets can exist in:

Policy and institutional structure Developed Capital markets

Markets

Economic infrastructure Labour markets

Social infrastructure Product markets

Economic institutions Regulation

Contract enforcement

PRODUCTIVITY

Improvements in these factors may drive Emerging Reduced institutional voids may result in

productivity growth, resulting in: Markets productivity growth through:

Increased profits and dividends to Small reductions in Development of effective institutional

institutional voids

shareholders can lead to mechanisms

productivity gains

Better wages and conditions to the = return

Improved regulation

workforce opportunity

Reduced bureaucracy

for equity

Lower prices to consumers investors Improvements in communication and

Increased tax payments to infrastructure

governments Frontier

Markets

Low

Low INSTITUTIONAL VOIDS High

Source: HSBC Global Asset Management.

For illustrative purposes only.

34HSBC GIF Frontier Markets

Country positioning – December 2019

Supplemental information

Country Weightings (%) Top & Bottom 5 Country Active Weights1 (%)

Kuwait 14,4

16

Egypt 12,6

United Arab Emirates 10,2

12 11,2

Philippines 10,1

Bahrain 7,5

Kenya 6,2 8

Vietnam 5,8

Kazakhstan 5,1 4,0 3,7 3,6 3,4

4

Romania 4,6

Colombia 3,8

Qatar 3,5 0

Georgia 3,4

-1,4 -1,6

Peru 3,0

(4)

Mauritius 2,1 -4,3

Nigeria 1,9 -6,0

Morocco 1,8 (8) -7,3

[Cash] 1,4

Bangladesh 1,0 (12)

UAE

Qatar

Kuwait

Croatia

Vietnam

Georgia

Nigeria

Morocco

Egypt

Kazakhstan

Argentina 0,9

Slovenia 0,6

0 2 4 6 8 10 12 14 16

Source: HSBC Global Asset Management, MSCI as at 31 December 2019.

Reference index is the MSCI Select Frontier & Emerging Markets Capped Index. This reference index is indicative only and is not guaranteed in any way. HSBC Global Asset Management (UK) Limited accepts no liability for

any failure to outperform this reference index.

Information is given for illustrative purposes. Data is supplemental to the GIPS© compliance performance details at the end of this presentation. Characteristics and weightings are for illustrative purposes only, as at the date indicated, and

subject to change without prior notice.

35HSBC GIF Frontier Markets

Sector positioning – December 2019

Supplemental information

Sector Weightings (%) Active Sector Weight1 (%)

Financials 52,2

10

8,18

Industrials 10,6

5 4,28

Consumer Staples 9,9 3,46 3,15

Consumer Discretionary 8,5

0

-0,18

-0,94

Real Estate 8,2 -1,86 -2,15 -2,55

(5) -4,25

Communication Services 3,9

(10) -8,54

Materials 2,6

Real Estate

Materials

Consumer Discretionary

Consumer Staples

Communication Services

Information Technology

Industrials

Financials

Health Care

Energy

Utilities

Health Care 1,8

Energy 0,5

Information Technology 0,4

0 10 20 30 40 50 60

Source: HSBC Global Asset Management, MSCI as at 31 December 2019.

Reference index is the MSCI Select Frontier & Emerging Markets Capped Index. This reference index is indicative only and is not guaranteed in any way. HSBC Global Asset Management (UK) Limited accepts no liability for

any failure to outperform this reference index. Data is supplemental to the GIPS© compliance performance details at the end of this presentation. Characteristics and weightings are for illustrative purposes only, as at the date

indicated, and subject to change without prior notice.

36Comprehensive universe

Sensibly diversified by region and country

HSBC has devised a customised and proprietary ‘capped’ reference index in tandem with MSCI that reflects our sensibly diversified

approach to investing in frontier markets globally

Publicly available Exclusive to HSBC

MSCI Frontier Markets MSCI Frontier Emerging Markets MSCI Select Frontier & Emerging Markets

Capped¹

Introduced: 30 November 2007 Introduced: 30 September 2008 Introduced: 30 May 2014

Back history: from 31 May 2002 Back history: from 29 November 2002 Back history: from 27 February 2009

Number of Countries: 28 Number of Countries: 34 Number of Countries: 36

Number of Stocks: 95 Number of Stocks: 144 Number of Stocks: 164

Africa = 15%

Africa = 23% Africa = 21%

Europe = 6%

Europe = 11% Europe = 8%

Asia = 34%

Asia = 19% Asia = 23%

Middle East = 23%

Middle East = 34%

Middle East = 47%

Latin America = 22%

Latin America = 14%

Index is heavily concentrated to the Middle Index is heavily concentrated to Asia (34%) Our custom index ensures a broad,

East, particularly Kuwait (38%) and Latin America (22%)

well-diversified universe.

Source: MSCI, pro-forma weights as of 31 December 2019.

Notes: Africa: Egypt, Ivory Coast, Kenya, Mauritius, Morocco, Nigeria, Senegal, Tunisia; Europe: Bulgaria, Croatia, Estonia, Kazakhstan, Lithuania, Romania, Serbia, Slovenia, Ukraine; Asia: Bangladesh, Pakistan, Philippines, Sri Lanka,

Vietnam; Middle East: Bahrain, Jordan, Kuwait, Lebanon, Oman, Qatar, UAE; Latin America: Argentina, Colombia, Peru.

1. This index supersedes the previous index (MSCI Frontier Emerging Markets Capped index) which was introduced on 31 May 2009 and with a back history from 29 November 2002.

There is an initial cap of 10% for any country. This gets reset back to 10% every time it breaches 12%. There is also an initial cap of 30% for the combined weight of the 8 crossover countries*. This gets reset back to 40% if it breaches 45%.

The MSCI Select Frontier & Emerging Markets Capped index is maintained and calculated by MSCI. For illustrative purposes only.

37HSBC GIF Frontier Markets

Stock positioning – December 2019 – Supplemental information

Top 10 Portfolio Holdings

8

7,54

7

6

5,02

5

3,93 3,84

4 3,81 3,78 3,76

3,20 3,20

3 2,77

2

1

0

AHLI UNITED BANK NATIONAL BANK SAFARICOM AGILITY HUMANSOFT BANCO HALYK SAVINGS BANCA DP WORLD COMMERCIAL

OF KUWAIT HOLDING DAVIVIENDA BANK TRANSILVANIA BANK

Source: HSBC Global Asset Management, MSCI as at 31 December 2019. For illustrative purposes only and does not constitute any investment recommendation in the above mentioned companies.

Data is supplemental to the GIPS© compliance performance details at the end of this presentation. Characteristics and weightings are for illustrative purposes only, as at the date indicated, and subject to change without prior notice.

38Frontier markets outlook

Regional market outlook

Middle East and North Africa

The GCC (Gulf Cooperation Council) economies continue undergoing structural change to reduce their reliance on oil and diversify their revenue sources. Indeed, a number of countries

have already started implementing VAT. Subsidies are slowly being removed and there is a focus on job creation. Fiscal consolidation is leading governments to focus on projects

strategic to economic growth. The magnitude of future GDP growth will depend on how fast economies are adjusting to this new reality. Most GCC countries still boast high financial

reserves and we expect the non-energy sector to continue showing positive growth rates.

The fund continues to have exposure to select countries in the GCC region, mainly due to attractive valuations and sustainable returns but with the added benefit of the markets' US

dollar pegs and high yields. We currently do not see any risk to the dollar peg in the countries we are invested in and in an environment of global currency concerns, we feel that this link

to the US currency offers higher earnings visibility.

The UAE is one of the top five countries in our portfolio in relative weight. Dubai continues to invest in its infrastructure and key projects and the economy’s direct reliance on oil is much

lower than that of neighbouring countries. Even though the real estate sector is experiencing a slowdown, we find valuations to be very attractive and not reflecting the robustness of the

companies we are invested in.

In Qatar, the fund remains underweight on valuation considerations. Even though our underweight position hurt us in 2018, passive flows and not earnings growth were the main reason

behind the rerating that took place. We find valuations to be in disconnect with the impact the blockade is bringing on to the economy. We currently do not have any exposure to the off-

index market of Saudi Arabia. The Kingdom will become in 2019 part of the MSCI EM Benchmark. Until then flows will be in the driving scene and fundamentals will become secondary.

We increased our exposure to Kuwait in 2018 by adding to the companies that we already own and deem to be very attractive. Kuwait has very high financial reserves and the lowest

fiscal budget breakeven oil price in the GCC at less than USD 60/barrel. We are very encouraged by the increased liquidity in the stock market that we saw in 2018 and we believe the

government will continue to implement its infrastructure plans. Kuwait is a market that could potentially be upgraded to EM, however, our allocation do not factor this into account. We

have exited Oman as the fiscal picture is deteriorating. In 2019, we have initiated a position in Bahrain that has operation in GCC and Egypt.

In North Africa, Egypt is our largest overweight position in the portfolio. We find the currency to be attractively valued and believe that government had taken the difficult but positive

steps on fiscal reforms. This includes removing subsidies, modifying VAT, and making the investment climate more investor friendly. We believe this is very positive for long-term growth

in the country. We see valuations to be attractive and our investments in the country represent a very diversified set of sectors. We see inflation reducing in 2019 and the country should

start reaping the benefits of lower interest rates and higher local gas production.

In Morocco, we continue to be underweight due to unattractive valuations. However, market liquidity has improved over the past few quarters, presenting us with possible new

investment opportunities, once valuations move to a more compelling level.

We continue to have no exposure to Tunisia, Jordan and Lebanon due to high valuations or low liquidity and political worries.

Any forecast, projection or target when provided is indicative only and is not guaranteed in any way.

The views expressed above were held at the time of preparation and are subject to change without notice.

39Frontier markets outlook

Regional market outlook

Asia

We currently do not hold any companies in Pakistan. We have reduced our exposure to Pakistan in the run-up to the MSCI reclassification in May 2017 as its valuation reached our

level of fair value. Pakistan has approached the IMF in Q3 2018 and we await to see green shoots in the economy before investing. We would also like to see reforms being enacted to

reduce circular debt levels, subsidies and enhance the tax base. We continue to believe that there are many well-run companies with excellent disclosure and a reasonable valuation

however, the macro challenges weigh on our investment decision. The China Pakistan Economic Corridor (CPEC), an investment program of USD46 billion, will transform the country’s

infrastructure and alleviate the power shortage.

The Philippines economy continues to perform well and inflation after peaking in 2018 has been declining in 2019 opening the door for a possible rate cut. Lower oil prices should act as

a boon to inflation and will alleviate the mounting pressure on the Peso. The country continues to benefit from strong remittances and BPO earnings. We expect infrastructure spending

to continue growing in 2019 and expect the private sector to play a more important role in funding these projects. The fund’s largest relative weight is to a supermarket chain that should

continue to benefit from positive consumption trends, and also to the largest port operator in the country. We have been increasing our investments in the Philippines and believe the

economy in 2020 should be stronger.

The fund has exposure to select holdings in Vietnam. Access remains restricted by foreign ownership limits (FOL) and low levels of liquidity. We struggle to find attractively valued

companies that have FOL availability. We expect FOL is to continue to rise and new investment opportunities to arise as more Vietnamese companies IPO. We are constructive on

Vietnam from a top-down standpoint as more manufacturing jobs move from China to Vietnam.

We increased our exposure to Bangladesh in 2017 after identifying a couple of fundamentally strong companies that were trading at attractive levels. The country continues to witness

one of the highest GDP growth rates in Asia. In 2018, as our holdings approached their fair value, we started taking profits. We are more cautious on the currency given it is

approaching pricey levels. We continue to stick to our disciplined investment process and are actively looking at new opportunities in the country.

Any forecast, projection or target when provided is indicative only and is not guaranteed in any way.

The views expressed above were held at the time of preparation and are subject to change without notice.

40Frontier markets outlook

Regional market outlook

Latin America

After two years of anaemic economic growth in Colombia, we are seeing corporate profitability improving in 2019 with a continuation in 2020. Corporates have adjusted well to the peso

depreciation triggered by the fall in the oil price in the period 2015-2016 and growth is picking-up in 2019-2020, driven by investments in infrastructure and improved confidence.

We are underweight Peru relative to the reference index. The macro story remains supportive, however we would like to see lower political uncertainty before considering increasing our

exposure. Rising metals output (particularly copper) is providing a boost to economic activity.

We are underweight Argentina due to very low visibility on the new administration’s economic plan. Unfortunately we see 2020 to be another tough year for the country with GDP

shrinking for the 3rd consecutive year. Our current holdings in Argentina either derive very little revenue from the domestic country or are developing the oil resources of the country and

thus will be eventually an exporter. We would like to see inflation on a downward trend, interest rates normalizing and the currency stabilizing for a prolonged period before we turn

positive on the country.

Eastern Europe

The fund’s exposure to Eastern Europe remains relatively high. We are neutral on Romania. We fear that the government will penalize the corporate sector in order to fund its higher

fiscal deficit. Even though the economy delivered strong GDP growth 2018, we see 2019 & 2020 delivering a slower growth with higher taxes as the main talking point.

Kazakhstan has seen currency stability after a series of devaluations. We have exposure to Halyk Bank, the country’s largest bank, which has maintained its strong capital position and

profitability. The bank has acquired one of its largest rivals and improved its leading position in the markets. We also own a copper mine operator.

Any forecast, projection or target when provided is indicative only and is not guaranteed in any way.

The views expressed above were held at the time of preparation and are subject to change without notice.

41Frontier markets outlook

Regional market outlook

Sub-Saharan Africa (SSA)

In Nigeria, the economy has moved out of recession, driven by much better availability of foreign currency and higher oil production. However, a lack of government reforms and a

struggling consumer are holding back a stronger recovery. We are watching the recovery to see any signs of pick-up in investment before increasing our allocation to the market. The

outcome of the presidential elections in Q1 2019 was in line with our expectations and thus we don’t expect sweeping reforms from the current administration.

We have increased our allocation to Kenya in 2019 after seeing green shoots in the economy and some positive changes on the interest rate cap. Indeed, we have increased our

banking exposure after valuations reached very compelling levels.

Any forecast, projection or target when provided is indicative only and is not guaranteed in any way.

The views expressed above were held at the time of preparation and are subject to change without notice.

42Wichtige Informationen

Beispielhafter Ex-ante-Kostenausweis nach MiFID II auf Basis einer fiktiven Transaktion

Rentenfonds und Mischfonds, institutionelle Anteilklasse

Produkttyp: Gesamtaufstellung der Dienstleistungskosten: Summe der Kosten, berechnet für die unterstellte Dauer der Kumulative Auswirkung der Dienstleistungs-

Rentenfonds und Dienstleistung: und Produktkosten auf die Rendite:

Mischfonds,

institutionelle 0 % des Anlagebetrages.

Anteilklasse Dies entspricht EUR 0,00. Ohne Einstiegs- und laufende Kosten wäre

In % In EUR die Rendite in den jeweiligen Jahren um

Anlagebetrag:

2.450,00 EUR bis 15.050,00 EUR höher.

1.000.000 EUR Zuwendungen an HSBC Global Asset Dienstleistungskosten 0,000 0,00

Management (Deutschland) GmbH:

Kauf

Haltedauer: Kosten von Dritten 0,000 0,00

0 % des Anlagebetrages.

1 Jahre

Dies entspricht EUR 0,00.

Produktkosten 0,245 – 1,505 2.450,00 – 15.050,00

Produktkosten wiederkehrend: Gesamtkosten 0,245 – 1,505 2.450,00 – 15.050,00

0,245 – 1,505 % p. a. des Anlagebetrages.

Dies entspricht jährlich 2.450,00 – 15.050,00

EUR.

Für die Ermittlung der Dienstleistungskosten wird unterstellt, dass der Wert des Anlagebetrags über die gesamte Haltedauer unverändert bleibt.

Die genannten Produktkosten für die institutionelle Anteilklasse eines Rentenfonds und Mischfonds entsprechen einer Bandbreite. Die tatsächlichen Kosten hängen vom jeweiligen Fonds ab und können höher

oder niedriger als die hier gezeigten Kosten ausfallen.

Die angegebenen Beträge beruhen teilweise auf einer Schätzung. In jedem Fall können sich die Angaben nach Erstellung der Beispielkostenausweise ändern.

Die angegebenen Werte können Rundungsdifferenzen enthalten.

Der Anlagebetrag entspricht bei Wertpapieren dem Kurswert, bei Optionen der Optionsprämie, bei Futures dem Nominal.

Zusätzlich entstehen Ihnen regelmäßig weitere Dienstleistungskosten, z.B. für die Annahme, Weiterleitung und Durchführung einer Wertpapierorder und für die Verwahrung der Wertpapiere. Diese weiteren

Kosten werden Ihnen durch das diese Dienstleistungen erbringende Wertpapierdienstleistungsunternehmen in Rechnung gestellt und nicht im oben gezeigten Beispiel berücksichtigt. Sie senken die Rendite

zusätzlich.

Quelle: HSBC Global Asset Management. Stand: 23.11.2017

44Übersicht der Fonds für institutionelle Kunden (1)

Anteils- Manage- davon Outper- Depot-

Ausschüttend Thesaurierend KVG- Admin-

Name klassen- ment- Production- formance- bank-

ISIN ISIN 1 Gebühr8 gebühr³

Währung gebühr Fee² gebühr4 gebühr

Aktien Europa

HSBC GIF - Euroland Equity I EUR LU0165075127 LU0165074823 0,750% 0,3750% - 0,25% - -

HSBC GIF - Euroland Equity Smaller Companies I EUR LU0165074401 LU0165074070 0,750% 0,3750% - 0,25% - -

HSBC GIF - Euroland Growth I EUR - LU0362711326 0,750% 0,3750% - 0,25% - -

HSBC GIF - European Equity I EUR LU0149719980 LU0164907411 0,750% 0,3750% - 0,25% - -

HSBC GIF - UK Equity I GBP LU0156333956 - 0,750% 0,3750% - 0,25% - -

7

HSBC German Equity EUR - DE0008489808 1,250% - 0,05% - - 0,07%7

HSBC Sector Rotation EUR - DE0009756825 1,250%7 - 0,05% - - 0,07%7

Aktien Global

HSBC GIF - Economic Scale Global Equity I USD - LU0164942087 0,300% 0,1500% - 0,25% - -

HSBC GIF - Global Equity Climate Change I USD - LU0323240613 0,750% 0,3750% - 0,25% - -

HSBC GIF - Global Equity Volatility Focused I USD - LU1103712250 0,750% 0,3750% - 0,25% - -

HSBC GIF - Global Real Estate Equity I USD LU1163227736 - 0,750% 0,3750% - 0,25% - -

Aktien Emerging Markets

HSBC GIF - Brazil Equity I USD LU0196698236 LU0196697857 0,875% 0,4375% - 0,30% - -

HSBC GIF - BRIC Equity I USD LU0449510295 LU0449509958 0,750% 0,3750% - 0,25% - -

HSBC GIF - BRIC Equity I EUR - LU0551368318 0,750% 0,3750% - 0,25% - -

6

HSBC GIF - BRIC Equity L1 USD - LU0342152195 0,500% 0,2500% - 0,25% - -

HSBC GIF - BRIC Markets Equity I USD - LU0254983488 0,750% 0,3750% - 0,25% - -

HSBC GIF - Economic Scale GEM Equity I USD LU0819121145 LU0819121061 0,300% 0,1500% - 0,30% - -

HSBC GIF - Frontier Markets I USD LU0666200695 LU0666200349 1,250% 0,6250% - 0,40% - -

HSBC GIF - Frontier Markets I EUR LU0717918238 LU0708055537 1,250% 0,6250% - 0,40% - -

6 7

HSBC GIF - Frontier Markets X USD LU0666201156 LU0666200935 1,000% 0,500% - 0,30% - -

HSBC GIF - GEM Equity Volatility Focused I USD - LU1236621055 0,750% 0,375% - 0,30% - -

HSBC GIF - Global Emerging Markets Equity I USD - LU0164872797 0,750% 0,375% - 0,30% - -

HSBC GIF - Mexico Equity I USD - LU0926764712 0,875% 0,438% - 0,30% - -

HSBC GIF - Russia Equity I USD - LU0329931413 0,875% 0,438% - 0,30% - -

HSBC GIF - Turkey Equity I EUR - LU0213961922 0,875% 0,438% - 0,30% - -

45Übersicht der Fonds für institutionelle Kunden (2)

Anteils- Manage- davon Outper- Depot-

Ausschüttend Thesaurierend KVG- Admin-

Name klassen- ment- Production- formance- bank-

ISIN ISIN 1 Gebühr8 gebühr³

Währung gebühr Fee² gebühr4 gebühr

Aktien Asien

HSBC GIF - Asia ex Japan Equity I USD LU0149712548 LU0165193169 0,750% 0,375% - 0,25% - -

HSBC GIF - Asia ex Japan Equity X6 USD - LU0404495664 0,700% 0,350% - 0,20% - -

HSBC GIF - Asia ex Japan Equity Smaller Companies I USD LU0149726845 LU0164939885 0,750% 0,375% - 0,25% - -

HSBC GIF - Asia ex Japan Equity Smaller Companies X6 USD LU0404496555 LU0404496472 0,700% 0,350% - 0,20%7

HSBC GIF - Asia Pacific ex Japan Equity High Dividend I USD - LU0197774135 0,750% 0,375% - 0,25% - -

HSBC GIF - Asia Pacific ex Japan Equity High Dividend I EUR - LU0622165578 0,750% 0,375% - 0,25% - -

6

HSBC GIF - Asia Pacific ex Japan Equity High Dividend X EUR - LU0404495821 0,700% 0,350% - 0,20% - -

HSBC GIF - China A-Shares Equity X USD LU2047620070 LU2038982745 0,700% 0,350% - 0,20%7 - -

HSBC GIF - Chinese Equity I USD LU0149719717 LU0164867441 0,750% 0,375% - 0,30% - -

HSBC GIF - Chinese Equity X6 USD LU1796207071 LU0404497447 0,700% 0,350% - 0,20%7 - -

HSBC GIF - China Consumer Opportunities I USD - LU0792368614 0,750% 0,375% - 0,30% - -

HSBC GIF - Economic Scale Japan Equity I JPY - LU0164882242 0,300% 0,150% - 0,25% - -

HSBC GIF - China Consumer Opportunities I EUR - LU0708055297 0,750% 0,375% - 0,30% - -

HSBC GIF - Hong Kong Equity I USD - LU0164880626 0,750% 0,375% - 0,25% - -

HSBC GIF - Indian Equity I USD LU0149722851 LU0164881350 0,750% 0,375% - 0,30% - -

HSBC GIF - Indian Equity I EUR - LU0551366700 0,750% 0,375% - 0,30% - -

HSBC GIF - Indian Equity X6 USD LU0404507260 - 0,700% 0,350% - 0,20%7 - -

HSBC GIF - Thai Equity I USD - LU0210638432 0,750% 0,375% - 0,25% - -

Aktien USA

HSBC GIF - Economic Scale US Equity I USD LU0149725441 LU0164902883 0,300% 0,1500% - 0,25% - -

Strukturierte Fonds

HSBC Aktienstrukturen Europa EUR - LU0154656895 1,25%7 - 0,25% - - 0,15%7

HSBC Discountstrukturen I EUR - DE000A0NA4K9 0,750%7 - 0,05% - - 0,09%7

7

HSBC Rendite Substanz I EUR - DE000A0NA4J1 0,600% - 0,05% - - 0,09%7

HSBC GIF Euro Convertible Bond I EUR LU1460729848 - 0,600% 0,3000% - 0,20% - -

46Übersicht der Fonds für institutionelle Kunden (3)

Anteils- Manage- davon Outper- Depot-

Ausschüttend Thesaurierend KVG- Admin-

Name klassen- ment- Production- formance- bank-

ISIN ISIN 1 Gebühr8 gebühr³

Währung gebühr Fee² gebühr4 gebühr

Renten Staatsanleihen Europa

HSBC Euro Gvt Bond Fund H EUR - FR0000971293 0,42%7 0,3100%7 - - - -

HSBC GIF - Euro Bond I EUR LU0165129825 LU0165130088 0,375% 0,1875% - 0,15% - -

Renten Staatsanleihen Global

HSBC GIF - Global Bond I USD LU0149731258 LU0165191460 0,375% 0,1875% - 0,15% - -

HSBC GIF - Global Bond Total Return I USD - LU1560770387 0,450% 0,2750% - 0,20% - -

HSBC GIF - Global Inflation Linked Bond I USD - LU0518436737 0,350% 0,1750% - 0,20% - -

HSBC GIF - Global Inflation Linked Bond I H EUR - LU0522826592 0,350% 0,1750% - 0,20% - 0,025%5

HSBC GIF - US Dollar Bond I USD LU0149734195 LU0165076109 0,375% 0,1875% - 0,15% - -

Renten Unternehmensanleihen

HSBC Euro Credit Non-Financial Bond I EUR DE000A0Q7S32 - 0,700%7 - 0,05% - - 0,07%7

HSBC Euro Credit Subordinated Bond I EUR DE000A0H0RA1 - 0,700%7 - 0,05% - - 0,07%7

HSBC GIF - Euro Credit Bond I EUR LU0165125914 LU0165125831 0,425% 0,2125% - 0,20% - -

HSBC GIF - Euro Credit Bond X6 EUR LU0374601176 LU0374601093 0,350% 0,1750% - 0,15%7 - -

HSBC GIF - Euro Credit Bond Total Return I EUR LU0988493788 LU0988493606 0,450% 0,2250% - 0,20% - -

HSBC GIF - Euro Credit Bond Total Return X6 EUR - LU0988494596 0,400% 0,2000% - 0,15%7 - -

HSBC GIF - Global High Income Bond I USD LU0524292009 LU0524292264 0,625% 0,3125% - 0,20% - -

HSBC GIF - Global High Income Bond I H EUR - LU0807188452 0,625% 0,3125% - 0,20% 0,025%5

Renten Emerging Markets Debt

GEM Debt Hard Currency Investment Grade X H6 EUR DE000A117YQ8 - 0,490%7 - 0,07% - - 0,05%7

HSBC GIF - Asia Bond I H EUR LU1436996257 - 0,550% 0,2750% - 0,25% - -

HSBC GIF - Asia Bond I USD - LU1436995523 0,550% 0,2750% - 0,25% - -

HSBC GIF - Asia Bond X USD - LU1437003137 0,500% 0,2500% - 0,20%7 - -

HSBC GIF - Asia Bond X H6 EUR LU1770381645 - 0,500% 0,2500% - 0,20%7 - -

HSBC GIF - Asian Currencies Bond I USD LU0210635842 LU0210635685 0,625% 0,3125% - 0,25% - -

HSBC GIF - Asian Currencies Bond I EUR LU0643830515 - 0,625% 0,3125% - 0,25% - -

HSBC GIF - Brazil Bond I USD - LU0254980898 0,500% 0,2500% - 0,25% - -

HSBC GIF - GEM Debt Total Return L1 H6 EUR LU0432931250 LU0570051812 0,500% 0,2500% - 0,25% 20% 0,025%5

HSBC GIF - GEM Debt Total Return L16 USD LU0310511695 LU0310511422 0,500% 0,2500% - 0,25% 20% -

HSBC GIF - GEM Debt Total Return L16 EUR - LU0551372344 0,500% 0,2500% - 0,25% 20% -

HSBC GIF - GEM Debt Total Return X H6 EUR LU1455023900 - 0,750% 0,3750% - 0,25%7 - 0,025%5

47Übersicht der Fonds für institutionelle Kunden (4)

Anteils- Manage- davon Outper- Depot-

Ausschüttend Thesaurierend KVG- Admin-

Name klassen- ment- Production- formance- bank-

ISIN ISIN 1 Gebühr8 gebühr³

Währung gebühr Fee² gebühr4 gebühr

HSBC GIF - GEM Inflation Linked Bond I USD - LU0630379070 0,500% 0,2500% - 0,25% - -

HSBC GIF - GEM Inflation Linked Bond I EUR - LU0630380169 0,500% 0,2500% - 0,25% - -

HSBC GIF - Global Emerging Markets Bond I USD LU0149732736 LU0164944026 0,500% 0,2500% - 0,25% - -

HSBC GIF - Global Emerging Markets Bond I EUR LU0551370561 LU0551370306 0,500% 0,2500% - 0,25% - -

HSBC GIF - Global Emerging Markets Bond I H EUR LU0431287282 LU0747734787 0,500% 0,2500% - 0,25% - 0,025%5

HSBC GIF - Global Emerging Markets Bond X6 USD LU0404503277 LU0404503194 0,500% 0,2500% - 0,20%7 - -

HSBC GIF - Global Emerging Markets Bond X H6 EUR LU0473929775 LU0473929692 0,500% 0,2500% - 0,20%7 - 0,025%5

HSBC GIF - Global Emerging Markets Local Currency Rates I USD - LU0992595826 0,625% 0,3125% - 0,25% - -

HSBC GIF - Global Emerging Markets Local Currency Rates I EUR - LU0992597285 0,625% 0,3125% - 0,25% - -

HSBC GIF - Global Emerging Markets Local Currency Rates I O EUR - LU0992598929 0,625% 0,3125% - 0,25% - 0,025%5

HSBC GIF - Global Emerging Markets Local Currency Rates X6 USD LU0996084553 LU0996084397 0,600% 0,3000% - 0,20%7 - -

HSBC GIF - Global Emerging Markets Local Debt I USD LU0234594348 LU0234594009 0,625% 0,3125% - 0,25% - -

HSBC GIF - Global Emerging Markets Local Debt I EUR LU0551371965 LU0551371700 0,625% 0,3125% - 0,25% - -

HSBC GIF - Global Emerging Markets Local Debt X6 USD LU0404505058 LU0404504911 0,600% 0,3000% - 0,20%7 - -

HSBC GIF - India Fixed Income I USD LU0780248364 LU0780248281 0,550% 0,2750% - 0,25% - -

HSBC GIF - India Fixed Income I EUR LU0780249255 LU0780249172 0,550% 0,2750% - 0,25% - -

6 7

HSBC GIF - India Fixed Income X USD LU0780248521 LU0780248448 0,500% 0,2500% - 0,20% - -

HSBC GIF - RMB Fixed Income I USD LU0692310633 LU0692310807 0,375% 0,1875% - 0,20% - -

HSBC GIF - RMB Fixed Income I EUR - LU0708054647 0,375% 0,1875% - 0,20% - -

HSBC GIF - RMB Fixed Income I O EUR - LU0782296759 0,375% 0,1875% - 0,20% - 0,025%5

Renten High Yield

HSBC GIF - Asia High Yield Bond XD USD - LU2067029749 0,600% 0,3000% - 0,20% - -

HSBC GIF - Asia High Yield Bond XD H EUR - LU2067029822 0,600% 0,3000% - 0,20% - 0,025%5

HSBC GIF - Euro High Yield Bond I EUR LU0165129155 LU0165129072 0,550% 0,2750% - 0,20% - -

6 7

HSBC GIF - Euro High Yield Bond X EUR - LU0404498767 0,500% 0,2500% - 0,15% - -

HSBC GIF - Global High Yield Bond I USD LU0780246400 LU0780246319 0,550% 0,2750% - 0,20% -

HSBC GIF - Global High Yield Bond I H EUR - LU0850060707 0,550% 0,2750% - 0,20% - 0,025%5

HSBC GIF - US High Yield Bond I USD - LU1890106484 0,550% 0,2750% 0,15% - -

48Übersicht der Fonds für institutionelle Kunden (5)

Anteils- Manage- davon Outper- Depot-

Ausschüttend Thesaurierend KVG- Admin-

Name klassen- ment- Production- formance- bank-

ISIN ISIN 1 Gebühr8 gebühr³

Währung gebühr Fee² gebühr4 gebühr

Renten Short Duration

HSBC Euro Short Term Bond I EUR FR0010495051 FR0010495044 0,300%7 0,2500%7 - - - -

HSBC GIF - Global Short Duration Bond X6 USD - LU1163226506 0,200% 0,1000% - 0,11%7 - -

HSBC GIF - Global Short Duration High Yield Bond I USD - LU0922810196 0,450% 0,2250% - 0,20% - -

HSBC GIF - Global Short Duration High Yield Bond I H EUR - LU0922810600 0,450% 0,2750% - 0,20% - 0,025%5

Nachhaltigkeit

HSBC RIF SRI Euro Bond I EUR - FR0010489567 0,400% 0,2000% - - - -

HSBC RIF SRI Euroland Equity I EUR - FR0010250316 0,750%7 0,375%7 - - - -

HSBC GIF Global Lower Carbon Equity I USD LU1689525381 - 0,400% 0,2000% - 0,25%7 - -

HSBC GIF Global Lower Carbon Equity X6 USD - LU1674673774 0,350% 0,1750% - 0,20%7 - -

HSBC GIF Global Lower Carbon Bond X6 USD - LU1674673006 0,350% 0,1750% - 0,15%7 - -

HSBC MSCI Europe Select SRI Index A EUR DE000A2DXMD9 - 0,225%7 - 0,225%7 - - 0,06%7

HSBC MSCI World Select SRI Index A EUR DE000A2H5YR8 - 0,225%7 - 0,225%7 - - 0,06%7

Liquidity Funds

HSBC Canadian Dollar Liquidity Fund A CAD IE00B233G129 IE00B233G343 0,170% 0,0200% - 0,03% - -

HSBC Euro Liquidity Fund A EUR IE0030028439 IE0030819498 0,170% 0,0200% - 0,03% - -

HSBC Sterling Liquidity Fund A GBP IE0007966447 IE0030819050 0,170% 0,0200% - 0,03% - -

HSBC US Dollar Liquidity Fund A USD IE0009489620 IE0030819274 0,170% 0,0200% - 0,03% - -

Multi Asset / Mischfonds

HSBC Horizont 1+ I EUR - DE000A2N67U6 0,720% - 0,07%8 - - 0,07%7

HSBC Horizont 2+ I EUR - DE000A2N67V4 0,770% - 0,07%8 - - 0,07%7

HSBC Horizont 4+ I EUR - DE000A2PBFJ0 0,810% - 0,07%8 - - 0,07%7

HSBC Horizont 7+ I EUR - DE000A2PBFK8 0,840% - 0,07%8 - - 0,07%7

HSBC Horizont 11+ I EUR - DE000A2PBFL6 0,870% - 0,07%8 - - 0,07%7

HSBC Horizont 16+ I EUR - DE000A2PBFM4 0,900% - 0,07%8 - - 0,07%7

HSBC GIF Global Emerging Markets Multi-Asset Income I USD - LU1711226511 0,675% 0,3375% - 0,25% - -

HSBC GIF Multi-Asset Style Factors I EUR LU1529682137 LU1460782227 0,700% 0,3500% - 0,20% - -

HSBC GIF Multi-Asset Style Factors X6 EUR LU1529682210 LU1460782573 0,550% 0,2750% - 0,15%7 - -

HSBC Multi Markets Select MD EUR DE000A0RAD67 - 1,500%7 - 0,05% - 20% 0,12%7

HSBC Multi Markets Select LD EUR DE000A2PL118 - 1,500%7 - 0,05% - 20% 0,12%7

HSBC GIF China Multi Asset Income I O EUR - LU1903293055 0,675% 0,3375% - 0,25% - 0,025%5

HSBC Portfolios - World Selection 1 B H EUR - LU0931136328 0,500% - - 0,25% - 0,06%5

HSBC Portfolios - World Selection 2 B H EUR - LU0931136757 0,500% - - 0,25% - 0,06%5

HSBC Portfolios - World Selection 3 B H EUR - LU0931136914 0,600% - - 0,25% - 0,06%5

HSBC Portfolios - World Selection 4 B H EUR - LU0931137219 0,600% - - 0,25% - 0,06%5

HSBC Portfolios - World Selection 5 B H EUR - 49 LU0931137565 0,650% - - 0,25% - 0,06%5Übersicht der Fonds für institutionelle Kunden (6)

Anteils- Manage- davon Outper- Depot-

Ausschüttend Thesaurierend KVG- Admin-

Name klassen- ment- Production- formance- bank-

ISIN ISIN 1 Gebühr8 gebühr³

Währung gebühr Fee² gebühr4 gebühr

Asset Backed Fonds

HSBC GIF - Global Securitised Credit Bond Bond I USD - LU1823213381 0,650% 0,3250% - 0,20% - -

HSBC GIF - Global Securitised Credit Bond Bond X 6 USD LU2080989697 LU1717580259 0,600% 0,3000% - 0,15% - -

HSBC GIF - Global High Yield Securitised Credit Bond X6 USD - LU1194162217 0,700% 0,3500% - 0,15% - -

HSBC GIF - Global Investment Grade Securitised Credit Bond

USD - LU1194161839 0,450% 0,2250% - 0,15% - -

X6

HSBC GIF - Global Investment Grade Securitised Credit Bond

EUR - LU1808483801 0,450% 0,2250% - 0,15% - 0,025%5

H6

50Berechnungsmethodik der Vergütung

HSBC Deutschland/HSBC Global Asset Management (Deutschland)

Eigene Berechnung Berechnungsbeispiele

Name des Fonds HSBC GIF – Global Emerging Markets Debt Total Return (EUR Hedged)

Managementgebühr % Managementgebühr 0,50 %

./. Production-Fee % ./. Production-Fee -0,25 %

./. KVG-Gebühr -

./. KVG-Gebühr %

./. Rabatt der Lagerstelle1 -

./. Rabatt der Lagerstelle1 %

= bei HSBC Deutschland / HSBC Global Asset Management

= bei HSBC Deutschland / HSBC Global Asset Management 0,25 %

% verbleibende Vertriebsgebühr

verbleibende Vertriebsgebühr

Zuzüglich ggf. anfallender, anteiliger Outperformance-Gebühr

1 Ggf. mit der Lagerstelle individuell zu verhandeln

HSBC Multi Markets Select

Managementgebühr 1,00 %

Name des Kunden

./. Production-Fee -

Entgelte und Erlöse, die bei arbeitsteiliger Leistungserbringung im HSBC-Konzernverbund

anfallen, werden in der Regel zwischen den an der jeweiligen Leistung beteiligten HSBC- ./. KVG-Gebühr -0,05 %

Einheiten aufgeteilt.

./. Rabatt der Lagerstelle1 -

= bei HSBC Global Asset Management verbleibende

0,95 %

Vertriebsgebühr

Zuzüglich ggf. anfallender, anteiliger Outperformance-Gebühr

1 Ggf. mit der Lagerstelle individuell zu verhandeln

1. Die Managementgebühr deckt die Gebühren für die Anlageverwaltungs-, Anlageberatungs- und Vertriebsdienstleistungen, die dem jeweiligen Teilfonds der Gesellschaft von der Verwaltungsgesellschaft, von den Anlageberatern und den

Vertriebsstellen erbracht werden. Bei HSBC Global Investment Funds (GIF) besteht die Managementgebühr jeweils zur Hälfte aus der Beratungsgebühr und der Vertriebsgebühr.

2. Die Production-Fee steht bei HSBC Global Investment Funds (GIF) und Französischen FCP Fonds dem Portfolio Manager zu. Bei HSBC Global Liquidity Funds enthält die Production-Fee auch die KVG Gebühr sowie die laufenden Kosten

der Fonds.

3. Die Admingebühr fällt gemäß Prospekt zur Deckung der Betriebskosten, Verwaltungs- und Kontoführungsgebühren von HSBC GIF Fonds an. Über-/Unterdeckungen gleicht die Managementgesellschaft unter Beteiligung der

Vertriebsstellen aus.

4. Bei diesen Fonds erhält die KVG einen Teil der/die gesamte Performancegebühr, soweit diese gemäß Verkaufsprospekt anfällt. X% (s.o.) jährlich von der vom Fonds erwirtschafteten Rendite über einem festgeschriebenen Schwellenwert.

Der Schwellenwert ist den wesentlichen Anlegerinformationen (KIID) des Fonds zu entnehmen.

5. Für die Währungsabsicherung erhebt die Depotbank/Verwaltungsstelle eine Gebühr von max. 2,5 Basispunkten p. a.

6. Anteile der Klassen X & L sind für institutionelle Anleger im Sinne von Artikel 174 des Luxemburgischen Gesetzes vom 17. Dezember 2010 über Organismen für gemeinsame Anlagen zur Umsetzung der OGAW IV-Richtlinie 2009/65/EG

in luxemburgisches Recht erhältlich. Für den Erwerb der Klasse X gilt außerdem, dass der Anleger in eine der folgenden Kategorien fallen muss: Unternehmen oder Pensionsfonds von Unternehmen, Versicherungsgesellschaften,

eingetragene wohltätige Organisationen oder von Körperschaften der HSBC-Gruppe verwaltete oder beratene Fonds und andere vom Verwaltungsrat genehmigte institutionelle Anleger. Anteile der Klasse L für den HSBC GIF - BRIC

Equity können seit dem 01.04.2010 nur noch von Anteilsinhabern gezeichnet werden, die einen regelmäßigen Sparplan haben.

51

7. Bei diesem Prozentsatz handelt es sich um ein Maximum. Der gezahlte Betrag wird in den Halbjahres- und Jahresberichten der Gesellschaft bekannt gegeben.

8. Die KVG-Gebühr ist bereits in der Managementgebühr enthalten.You can also read