Pan European VAT update Deloitte Global Tax Center (Europe) - 27 May 2019

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Pan European VAT update Deloitte Global Tax Center (Europe) 27 May 2019 Olivier Hody, Partner Johan Van Der Paal, Partner Bruno Roelands, Senior Director Karen Truyers, Senior Manager Sandeep Shinde, Manager

Agenda

• Introduction

• Global VAT developments

• EU VAT developments

− European Council & Commission

− CJEU

• VAT compliance 2.0

− MTD, SAF-T, real time reporting and split payment

• Pan EU VAT compliance update

− VAT rates

− Import VAT

− E-filing, upload file, XML schema, due dates

− Local reverse charge

− New obligations relating to e-commerce

− E-invoicing via government platform

• Brexit

• Conclusion

2

Global

VAT developments

3

Gulf Cooperation Council states (GCC)

VAT implementation progress timeline

June 2016

GCC VAT Agreement

signed by all six

Member States

2016

2017 2018

2019 2020 2021

Nov 2017 Jan

USA and KSA commit 2020* 2021*

to go-live by Jan 2018 Jan 2019 Qatar Kuwait

Bahrain

Jan 2018 VAT implementation

UAE & KSA

VAT implementation

*Sep 2019

Oman

* Still to be officially confirmed

4Global VAT developments

Other updates

o China

Reduction of the VAT rates on 1 April 2019:

o 16%/10% has been reduced to 13%/9%

o 6% rate remained unchanged

Angola

VAT introduction:

o Wave 1: large taxpayers, 1 July 2019

o Wave 2: remaining taxpayers, 1 January 2021

Russia and South Africa

• Change in the rules for VAT registration requirements for foreign taxpayers providing B2B

electronic services to local companies

o Russia : Since January 2019

o South Africa : Since April 2019

5EU

VAT developments

6European Council & Commission

European Commission

Study on domestic and cross border intra-EU VAT refunds

8th Directive refund claim

• Average value / claim: EUR 4.700

• Longer delays in

Greece Romania Italy

• Additional queries percentage: 9% but significantly higher in

Greece Romania Malta

• Approval rate: 94% (97% with VAT agent)

with the lowest approval rate Greece Croatia Malta

• Main reasons for rejection are:

1. Suppliers incorrectly charging VAT

2. Non-refundable VAT

Tax

3. Lack of correct supporting document authorities

43%

Taxpayers

• In case of dispute, taxpayers win in 57% of 57%

the case and tax authorities 43%

8European Commission

Study on domestic and cross border intra-EU VAT refunds

VAT reimbursements via VAT return

• Average value / claim: EUR 27.000

• Longer delays in

Greece Romania Italy

• Average delay before effective reimbursement: 16,4 weeks with Italy at 62,6

weeks

• Approval rate: 99,5%

• Main reasons for rejection are:

1. Invoice discrepancies

2. VAT incorrectly charged by the supplier

3. Lack of documentary evidence

4. Lack of business purpose of the expenditure

9European Commission

Study on domestic and cross border intra-EU VAT refunds

Recommendations:

8th Directive refund claims VAT reimbursements via VAT return

• Awareness of Member State of

refund rules and requirements

(including IT solutions)

• Increasing • Guidelines on VAT

• Verification of pro-rata adherence for reimbursement claims

calculations (including late interest frequency

guidelines) payments

• Improved additional

• Recovery of incorrectly • Improved information request procedures

charged VAT follow-up (including IT solutions)

processes

• Better targeted request within

for additional information national tax

administration

• Use of established business

languages in the VAT refund

process

10Quick fixes 2020

The Quick fixes

Call of stock Simplification

arrangements for transport

allocation in

chain supplies

Simplification

EU VAT number proof of

requirement for transport

Intracommunity

supplies

11Quick fixes

Harmonised call-off stock arrangements

Single VAT exempt IC supply

VAT taxable

IC acquisition

• Upon dispatch : record keeping

required, no tax reporting IT

• Upon sale : reporting in VAT

return and ESL

DE

• Maximum 12 month period

Supplier Customer Stock Physical flow of the goods

12Quick fixes

Harmonised call-off stock arrangements - conditions

In order to use this simplification for call-off stock arrangements, certain conditions have to

be fulfilled:

• Both the supplier and the intended acquirer are taxable persons;

• The supplier has not established his business nor does he have a fixed establishment in

the Member State to which the goods are dispatched or transported;

• The supplier records the dispatch/transport of the goods to the stock in a register held by

him;

• The supplier mentions the identity and VAT identification number of the intended acquirer

in his recapitulative statement (only that, not the value of the goods) submitted for the

period of the transport of the goods;

• The intended acquirer is identified for VAT purposes in the Member State to which goods

are transferred;

• The acquirer’s identity and VAT identification number are known by the supplier at the

time when dispatch or transport begins;

• The goods are transported from one Member State to another, excluding imports, exports

and supplies within a single Member State from the simplification;

• The goods are supplied after arrival at a later stage.

13Quick fixes

Simplification for chain transactions - situation

Chain transactions are now defined in the VAT Directive as situation where :

• Goods are supplied successively. Therefore, it is necessary that at least three persons are

involved in the chain transaction, but this can be more;

• Goods are dispatched or transported from one MS to another MS. As a result, chain

transactions involving imports and exports, or involving only supplies within the territory

of a Member State, are excluded from the provision;

• Goods are transported or dispatched directly from the first supplier to the last customer

in the chain.

Issue for VAT: what is the supply to which the transport or dispatch of the goods is to be

ascribed, that is to say, what supply is the intra-Community supply ?

14Quick fixes

Simplification for chain transactions - graphic

Logic for attribution of cross border transport to single supply within a transaction chain if

transport performed by intermediate supplier

Intra-Community IT

Intra-Community or local supply?

or local supply?

FR

DE

Supplier Customer Physical flow of the goods Invoice flow

Intermediate supplier

15Quick fixes

Simplification for chain transactions – default situation

Default: IC transport is allocated to the supply made by the intermediate operator

to his customer

IT

ICS

Local supply

FR

DE

Supplier Customer Physical flow of the goods Invoice flow

Intermediate supplier

16Quick fixes

Simplification for chain transactions - exception

IC transport is allocated to the supply made by the provider to the intermediary

operator

• The intermediary operator communicates the name of the MS of arrival to the

provider;

• The intermediary operator provides to the supplier his VAT identification umber in a

MS other than the one in which the dispatch or transport of the goods begins

IT

Local supply

ICS

FR

DE

Supplier Customer Physical flow of the goods Invoice flow

Intermediate supplier

17Quick fixes

Simplification proof of transport

Quick fix providing legal certainty on evidence requirements

Simplified proof of transport – Rebuttable

presumption

EXW

FCA

Transport or dispatch by or on Transport or dispatch by or on

behalf of the CTP supplier behalf of the CTP customer

Supplier’s possession :

2 non-contradictory • Written statement by

the acquirer

documents attesting to

• 2 non-contradictory

the transport

documents attesting

the transport

o Transport documents

o Receipt acknowledgement

o Official documents issued by public authority

o Receipt confirming storage

o Certificate by professional body

o Contract

o Correspondence

o VAT return 18Quick fixes

VAT identification number as substantive condition for

an exempt intra-Community supply

Substantive conditions New legislation includes as substantive

• Evidence of cross border transportation condition

of the goods • A valid VAT identification number

• Capacity of the buyer as a taxable of the acquirer in a MS other than

person that in which transport of the goods

• Taxed IC acquisition

begins

Tax authorities controls And also as substantive condition :

• Valid EU identification number of the • The correct filing of the European

buyer Sales Listing by the supplier

• ESL reporting of the supplies towards • Distinction will be made between

that number excusable and non-excusable errors

CJEU : If this condition is not met When a valid VAT number is not

available

• Fines or administrative sanctions can be

imposed by MS • Refusal of exemptions

• But the application of the exemption • VAT of the Member State of departure

cannot be refused of the goods should be charged

• This VAT can be recovered by

purchaser via refund procedure

19E-commerce VAT changes

Current status of 2021 changes

Current status

• VAT E-commerce main

legislation adopted in Dec

2017 – marketplace deemed

reseller provisions added in Communication on Digital Single

Council negotiations the future of VAT Market Strategy

VAT action plan

December 2011 May 2015

• Additional Directive change April 2016

adopted in March 2019 to

provide clarifications needed

to implement deemed reseller

provisions December 2017:

e-Commerce December 2016:

• Implementing Regulation proposals e-Commerce

providing precise rules on adopted proposals

marketplace obligations and

different OSS regimes adopted December 2018:

in March 2019 Implementing

Regulation &

Next steps VAT Directive

proposals

• Commission’s Explanatory

Notes– for guidance only, not 1 Jan 2021:

law – expected end of 2019 E-Commerce

March 2019: By end of

2019: entry into

• IT system changes both on further VAT

Explanatory force

customs and VAT side – EU Directive

and national level – testing in changes and IR Notes

2020 adopted

• MS and industry consultations

• Implementation on 1 January

2021 20CJEU cases

Place of supply

C-647/17 – Srf Konsulterna – 13 March 2019

Facts

“admission to event or B2B

service?

Upfront Upfront 5 days educational

registration payment course for taxpayers

(B2B)

Decision of the CJEU

• The five-day course on accountancy is taxable where the event takes place (following article 53 of the VAT Directive)

• The fact that the courses were subject to advance registration and payment is irrelevant.

22Export:

C 275/18 – Vinš - 28 March 2019

Facts

Post documents as

proof of export

CZ Authorities denied the

No export document VAT exemption for export

because there is no

export document

Decision of the CJEU

CJEU applies the substance over form principle

If it is clear that the goods actually leave the EU territory the exemption cannot be denied only because the export

document is missing.

23VAT deduction and VAT refund:

C-691/17 – PORR Építési Kft. – 11 April 2019

Facts

Invoice for construction work incorrectly with HU VAT The input VAT deduction is

rejected by the VAT

Credit note with HU VAT authorities

VWFS Customer

Decision of the CJEU

• VAT authorities can refuse the right to deduct VAT on an invoice that incorrectly applies VAT instead of reverse

charge.

• VAT authorities are not obliged to examine prior whether the supplier is able to correct the invoice and reimburse the

VAT to the recipient.

• The VAT authorities are in principle also not obliged to reimburse the VAT to the recipient of the credit note unless the

reimbursement of the VAT by the supplier is impossible or excessively difficult (f.e. suppliers’ insolvency)

(same conclusion in the Farkas case)

24VAT deduction and VAT refund:

C-133/18 – Sea Chefs Cruise Services – 02 May 2019

Facts

VAT refund claim Sea Chefs’ refund

in France claim was rejected

‘Sea Chefs’ Authorities asked additional information

(DE) ‘Sea Chefs’ failed to provide it

(within 1 month)

Decision of the CJEU

• The time limit of one month to respond to a request for additional information is not an expiry due date

• A taxable person may regularize its VAT refund application by presenting additional evidence during an appeal

procedure (pursuant to Article 23 of Directive 2008/9)

25VAT Compliance 2.O

(MTD, SAF-T, real time reporting

and split payment updates)

26Making Tax Digital (MTDfV)

Making Tax Digital (MTDfV)

Roadmap

Impact assessment and challenges in the VAT compliance process in terms of data quality, review

efficiency and control and requirement to comply with Making Tax Digital for VAT

MTD first announcement MTD Pilot launched MTD Pilot extended

Jan

2015 2018 2019

First Digital Submission period for Start of digital submission

taxpayers: M (April 2019) and Q requirement for

(Apr-June 2019 quarter) non-deferred taxpayers

July May

2019 2019 Apr

2019

Oct

2019 Apr

2020

Start of Digital submission Start of Digital Linking

requirement for deferred requirements

taxpayers

28SAF-T

SAF-T

Poland

Introduction of the extended SAF-T obligation (JPK_VDEK)

Abolition of the

traditional returns:

VAT-7, VAT-7K, VAT-27,

VAT-ZZ, VAT-ZT, VAT-ZD

ESPL return shall remain

Scope: Other considerations:

All taxpayers registered - Frequency: monthly

for VAT in Poland

- Data requirements:

definitive data fields are not

- Large taxpayers yet available

(Jan 2020) - Penalties: PLN 500 each for

- Remaining taxpayers non-compliance, errors and

(July 2020) irregularities

JPK_VDEK

SAF-T

30SAF-T

Poland

Comparison reporting data:

current JPK_VAT and VDEK SAF-T obligation

JPK_VAT JPK_VDEK

31SAF-T

Norway

January 2020 (wave 1)

Version 1: All postings, incl. G/L, customers, suppliers and VAT account;

A/R (balances, customer master data, etc.); A/P (balances, customer master

data, etc.)

TBC (Wave 2)

Version 2: Detailed invoice information and source documents, etc.

TBC (Wave 3)

Version 3: Movement during period of inventories and non-current assets, etc.

32SAF-T

Hungary

• Proposal to introduce SAF-T obligation as from January 2020

• In addition to the current real time reporting obligation

• Further details are not yet available

33Real time reporting

Real time reporting

Recent changes

Hungary

• Technical updates:

o New upload file XSD version 1.1 is applicable as from 4 June 2019

(previously: 2 May 2019)

o Version 2.0 is also expected from January 2020

35Split Payment

Split Payment

Poland

Cash-flow

• Mandatory, for all VAT registered taxpayers

impact?

(including non-established) where:

Scope o B2B transactions above PLN 15 000 and

o Transaction relates to *certain goods or

services - subject to reverse charge (as

listed in appendix 15 of the Polish VAT law)

• “Special VAT bank account” to opened with

Polish banks only

Mandatory • Taxpayers would have limited rights to this

Bank

split payment Account

bank account

• Bank charges would be reimbursed by the

1 Sep 2019* tax authorities - upon taxpayer request, on

a quarterly basis

• Invoicing requirements: should include the

In wording 'split payment mechanism’

practice • Penalties: 100% of the VAT amount in

Abolition of question/per invoice and also criminal offence

the domestic (personal liability) in certain circumstances

reverse foreseen

charge

* Still to be adopted by Parliament 37Pan EU VAT compliance

update

38VAT rate updates

VAT rates

Expected changes

Croatia

• The standard VAT rate to be decreased from 25% to 24% from 1 January 2020

(subject to further approval from the Parliament)

Greece

• Special VAT status abolishment for the remaining 5 islands (Lesbos, Chios, Samos, Kos,

and Leros) is further postponed from January 2019 to July 2019 Likely to be postponed to 2020

Italy

• The VAT rates applicable in 2018 (i.e. standard rate 22%, reduced rate 10%) continues to

apply in 2019, despite initial plans to increase the VAT rates end of 2018

• Subject to further approval from the Parliament:

o Reduced VAT rate may increase from 10% to 13% on 1 January 2020;

o Standard VAT rate: Increase from 22% to 25.2% on 1 January 2020 and to 26.5% on 1

January 2021

Lithuania

• Proposal to decrease the standard VAT rate from 21% to 18% from January 2020 has

been rejected by the government on 5 May 2019

40General VAT compliance updates

General VAT compliance updates

Import VAT

United Kingdom and Ireland

Import VAT

C79 reverse charge SAD

post-Brexit

42General VAT compliance updates

E-filing / upload files / XML schema / due dates

Estonia

Change in the mandatory e-filing process: 1 May 2019

Czech Republic

VATR: April 2019

LSPL: Sep 2019

Hungary

Real time reporting

XSD schema version 1.1: 4 June 2019

Switzerland

(Proposal) Introduction of mandatory e-filing: 1 January 2020

Finland

New VAT return form: January 2020

Belgium, Demark, Norway, Sweden, Spain

Summer extensions

43General VAT compliance updates

Local reverse charge

United Kingdom

• Introduction of the local reverse charge on supplies in the construction industry

• Go-live date: Oct 2019

Lithuania

• Introduction of local reverse charge on IT equipments (tablets, laptops, smartphones,…)

• Go-live date: August 2019

Poland

• Abolition of the local reverse charge on certain goods and services

(as listed in the Appendix 15 of the Polish VAT Act)

• Approximately 150+ goods and services in scope:

(IT equipments such as tablets, laptops, smartphones; building and construction services,

steel and metal products,…)

• Cash flow impact, as these transactions would now be subject to the mandatory split

payment regime

44General VAT compliance updates

New obligations related to e-commerce

Italy

• Scope: Online marketplaces who facilitate distance sales of goods in Italy

• Obligation : Provision of informative (non-VAT related) information

• Filing frequency : Quarterly, July 2019

• Contents of the obligation : data for each supplier:

o The name, address and email account

o The total number of units sold in Italy

o The total amount of sales prices or the average selling price of the units sold in

Italy

Bulgaria

• Scope: Certain online retailers who perform distance sales of goods in Bulgaria

• Obligation : register in a specific public database maintained by the government

• Due date: 29 June 2019

45General VAT compliance updates

E-invoicing

Link

46General VAT compliance updates E-invoicing - recent updates Sweden B2G 1 April 2019 Croatia B2G 1 July 2019 Norway B2G 1 April 2019 (at least 100 000 NOK) The Netherlands B2G (Wave 1: 1 January 2017, Wave 2: 18 April 2019) Poland B2G (Wave 1: 18 April 2019 – at least EUR 30 000, Wave 2: 1 August 2019) Ireland: B2G (Wave 1: 18 April 2019, Wave 2: 1 August 2019) Portugal: B2G (Wave 1: 18 April 2019, Wave 2: 1 August 2019) Greece: B2G (Wave 1: 18 April 2019, Wave 2: 1 August 2019) 47

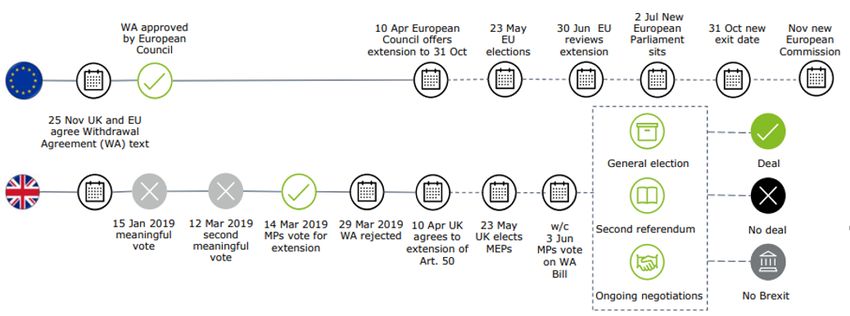

Brexit

48Brexit timeline

Latest political developments

49Conclusion

51

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and their related entities. DTTL and each of its member firms are legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not provide services to clients. Please see www.deloitte.com/about for a more detailed description of DTTL and its member firms. Deloitte provides audit, tax and legal, consulting, and financial advisory services to public and private clients spanning multiple industries. With a globally connected network of member firms in more than 150 countries, Deloitte brings world-class capabilities and high-quality service to clients, delivering the insights they need to address their most complex business challenges. Deloitte has in the region of 225,000 professionals, all committed to becoming the standard of excellence. This publication contains general information only, and none of Deloitte Touche Tohmatsu Limited, its member firms, or their related entities (collectively, the “Deloitte Network”) is, by means of this publication, rendering professional advice or services. Before making any decision or taking any action that may affect your finances or your business, you should consult a qualified professional adviser. No entity in the Deloitte Network shall be responsible for any loss whatsoever sustained by any person who relies on this publication. © 2019 Deloitte Belgium

You can also read