Pan European VAT update Deloitte Global Tax Center (Europe) - 11 January 2019

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Pan European VAT update Deloitte Global Tax Center (Europe) 11 January 2019 Olivier Hody, Partner Donato Raponi, Senior Advisor EU Affairs Bruno Roelands, Senior Director Karen Truyers, Senior Manager Sandeep Shinde, Manager

Agenda

• Introduction

• Global VAT updates

• EU VAT developments

• VAT rates

• Compliance 2.0: Real-time reporting, SAF-T, split payment, e-invoicing, Making Tax Digital

• Other compliance updates

• Conclusion

2

Global VAT updates

Gulf Cooperation Council states (GCC)

VAT Implementation progress timeline

All GCC countries to

implement VAT by 2019?

GCC VAT

Agreement

signed by all

six Member

States in June

2016

2016

2017 2018

2019 2020 2021

UAE & KSA Oman: Sep 2019 (indicative)

commit to Qatar: no official announcement yet

Kuwait: 2021?

go live on 1

January

2018

1 January 2018 1 January 2019

UAE & KSA Bahrain

4

Gulf Cooperation Council states (GCC)

Bahrain – compliance highlights

Bahrain

• Go-live: 1 January 2019 • VAT regulations: English

version now available Link

• VAT rate:5%

• VAT returns frequency:

• Mandatory VAT registration

monthly or quarterly

application to be submitted

depending on the size of

by:

business

BHD > 5 000 000 : 20 Dec 18

• Late submission of the return

BHD > 500 000 : 20 June 19

or late payment: 5% to 25%

BHD > 37 500: 20 Dec 2019

of the VAT which should have

• Voluntary VAT registration: been declared or paid

BHD > 18 750

• Late VAT registration

• Non-residents VAT registration penalties: up to BHD 10 000

threshold: no minimum

amount / threshold applies

Intra-GCC transactions are still considered

as imports/exports

Deloitte Middle

East Tax Handbook

5

Gulf Cooperation Council states (GCC)

UAE and KSA – Into the second year of VAT compliance

UAE KSA

• Post-implementation VAT • Final wave of VAT

review (Link) registrations: 20 Dec 2018

• New bi-annual filing frequency

from SAR 375.000 < SAR

for certain businesses (small

1.000.000

businesses and real estate)

• Penalties for late VAT

• Regularization: VAT211 can be

registration: up to SAR 10 000

submitted in Arabic only

• VAT compliance highlights:

• Guidance on input VAT

- OTP/MFA to access the

deduction / apportionment

website

(Link)

- Official VAT compliance

• Late filing/payment penalties guidelines (Link)

enforced: AED 1000 per

• Late filing/payment penalties

offence for late filing and 2%,

enforced: 5-25% VAT due

subject to a max. 300% of the

outstanding VAT • VAT number search database

(Link)

• VAT number search database

(Link)

Intra-GCC transactions are still considered

as imports/exports

Deloitte Middle

East Tax Handbook

6

Russia

Recent updates

• VAT rate change:

o The standard VAT rate increased from 18% to 20% effective January 2019 (Link)

• New VAT registration obligation for non-residents:

o Until the end of 2018, foreign companies supplying B2B e-services to Russian

established customers could avail of the local reverse charge mechanism and

therefore there was no obligation to register for VAT in Russia

o From January 2019, foreign companies supplying B2B e-services to Russian

established customers are not able to apply the local reverse charge mechanism

anymore and therefore would be obliged to register for VAT, and account for the

VAT via the periodical VAT returns

o The VAT rate for B2C and B2B e-services also increased from 15.25% to 16.67%

(of the VAT inclusive value) effective January 2019

o Further information: Link

7EU VAT Developments

EU VAT developments

Commission and Council updates

Digital

Definitive Service

VAT Tax

E-com: Regime

New VAT

incl CTP and OSS

obligations for

Marketplaces &

payment VAT rates

providers reform

SME

simplification

rules

2019

Upgrade of

MOSS for

Generalised

TBE services 2020

R/C and VAT

VAT Split payment Quick fixes

1.Call-off stock

applied to Vouchers 2.Chain transactions 2021

e-publications Directive 3.Transport allocation

4.VAT number E-com:

OSS for

distance

E-com sales

Non-EU:

LVCR, customs

simpl and OSS 9EU VAT developments

Interesting CJEU cases

10EU VAT developments

Interesting CJEU cases

11VAT rates

VAT rates

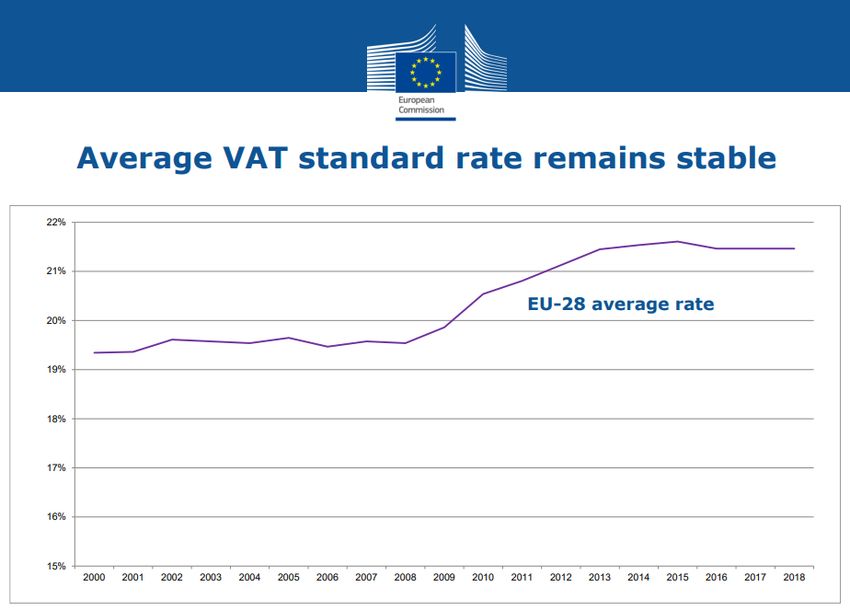

Average VAT standard rate remains stable in the EU

source: The EU Taxation Trends report 2018

• In June 2018, the EU Council has adopted 15% as the minimum standard rate (on a 13

permanent basis)VAT rates

Recent and expected changes

The Netherlands

• The reduced VAT rate increased from 6% to 9% on 1 January 2019

Canary Islands

• The general IGIC rate decreased from 7% to 6,5% on 1 January 2019

Greece

• Special VAT status abolishment for the remaining 5 islands (Lesbos, Chios, Samos, Kos,

and Leros) is further postponed from January 2019 to July 2019

Ireland

• The 9% reduced VAT rate is maintained in 2019, despite initial plans to abolish it

Croatia

• The standard VAT rate to be decreased from 25% to 24% from 1 January 2020 - subject

to further approval from the Parliament

Italy

• The VAT rates applicable in 2018 (i.e. standard rate 22%, reduced rate 10%) will also

continue to apply in 2019, despite initial plans to increase the VAT rates end of 2018

• Subject to further approval from the Parliament:

o Reduced VAT rate may increase from 10% to 13% on 1 January 2020

o Standard VAT rate: Increase from 22% to 25,2% on 1 January 2020 and to 26,5% on 1 January 2021

14VAT Compliance 2.O

Compliance 2.O

Global landscape

16Real Time VAT reporting - Spain

Suministro Inmediato de Información (SII)

Extension to Canary Islands in 2019

Extended to IGIC from

New obligations on January 2019

transactions recording

Electronic VAT Reporting System (SII) Dates of implementation

entails the electronic supply, through the

Spanish/IGIC Tax Authorities on-line Entry intro force since July 2017.

platform, of billing registries which are Mandatory for monthly taxpayer who are:

part of the VAT ledgers. (i) registered in the Monthly VAT Refund

Register, (ii) registered under VAT Grouping

Regime, or (iii) transactions performed

during last year exceeded EUR 6.010.121,04.

Extended to 8 days

for IGIC in the first semester of 2019. Key Optional for taxpayers who voluntary want to

Afterwards, reverts to 4 working days enroll the system, by submitting the

issues

corresponding census form.

Deadline to submit the information Same threshold for

Canary Islands

Issued invoices: 4 working days from its

issuance Ways of submission

Received invoices: 4 working days from its On going basis through a “web service” from

accounting. Always, before the 16th day of the Spanish/IGIC Tax Authorities on-line

the following month from the accrual date. platform.

Following returns are not be required post SII

Imports: 4 working days from the date in implementation: Taxpayers with few operations could report

which the accounting document (in which

Annual Spanish return (form 390) the information through a “web form”.

the VAT quota is indicated) was registered.

Always, before the 16th of the following Spanish ASPL return (form 347) Following returns are not be required

month from the accrual date.

Spanish VAT books for entities in REDEME (form 340) post SII implementation:

Saturdays, Sundays and national holidays

are excluded from counting. Change in the statutory date:

• IGIC Annual return (form 425)

Monthly Spanish VAT return (form 303 ) – due date • IGIC ASPL return (form 415)

extended 30th day following the end of the reporting • VAT books for entities in REDEME

period (form 340)

Change in the statutory date:

17

IGIC VAT return (form 417)Real time reporting

Hungary

•Since 1 July 2018

•All taxpayers with a VAT •Immediately ~ real time

registration in Hungary (within 24 hours requirement has been

•B2B transactions above removed)

the threshold of HUF •Without any human intervention

100000 (VAT amount)

•Upload file in XML format

•B2C transaction are out of Technical (new version released)

scope Scope

details •

•

Unique identification number – to

be maintained in the ERP system

•LSPL threshold has been reduced •Penalties up to HUF 500 000 per invoice

from HUF 1 million to HUF 100 000 Penalties & •In practice, HU tax authorities have

•Local Sales Listing return is no

longer required in certain

Impact further recently started performing

reconciliations between the LPL and real

circumstances guidance time data - raising questions on the

•Unique identification number is not mismatches and irregularities. Penalties

required to be mentioned on the have been limited so far

invoice (as previously proposed) • New technical guidelines for 2019 (Link)

•

1865M box 6 and 1865A-01-05 box 107 are not required

to be completed in the periodical VAT return

• System outage for more than 48 hours:

• Online Invoicing ystemhttps://onlineszamla.nav.gov.hu)

• Manual reporting

18SAF-T

Recent updates

Poland

• Since July 2018, all taxpayers are subject to a full on-demand SAF-T

• As of July 2019, traditional VAT returns might be abolished and replaced by an enhanced

monthly SAF-T (JPK_VDEK) file.

Proposed guidelines:

o Scope : all taxpayers registered for VAT in Poland

o Abolition of a VAT return and related annexes: VAT-7, VAT-27, VAT-ZZ, VAT-ZT, VAT-ZD

o JPK_VDEK (monthly SAF-T) would capture information currently required in the

traditional VAT return, including the carry forward, pro-rata adjustments and also VAT

ledgers

o Draft data requirements of the JPK_VDEK is expected to be published by the authorities

in February 2019

o Penalties up to PLN 500 for each irregularity/mismatch/error/incorrect/incomplete

reporting

19SAF-T

Recent updates

Norway

• What?

o The full SAF-T audit package in Norway will include:

- General ledger data level including customer and supplier breakdown, along with

relevant master data

- Standardized account numbers as per the Norwegian chart of accounts

- Standardized fixed tax codes

• When?

o 1 January 2020, on-demand

o Implementation in 3 waves (data requirements)

• Scope?

o All companies which are currently liable to maintain book-keeping information

electronically (in accordance with the Norwegian book-keeping legislation)

o Some specific exemptions apply (e.g. VoES companies)SAF-T updates

Norway

January 2020 (wave 1)

Version 1: All postings, incl. G/L, customers, suppliers and VAT account;

A/R (balances, customer master data, etc.); A/P (balances, customer master

data, etc.)

TBC (Wave 2)

Version 2: Detailed invoice information and source documents, etc.

TBC (Wave 3)

• Version 3: Movement during period of inventories and non-current assets, etc.

21Split payment

Recent updates

Romania

• EU Commission requested Romania to end VAT split payment mechanism

- Letter of Formal Notice sent in November 2018 (Link)

Poland

• Split payment is currently optional since July 2018

• Split payment could become mandatory in the course of 2019 for certain fraud-prone

industry sectors such as telecom

United Kingdom

• Public consultation (Link) (29 June 2018) and a Response document (Link) published on 7

November 2018

• Working Group (Link)has been setup to investigate the feasibility of the split payments

• Go-live date: proposed implementation date is not yet announced

• Scope:

• Non-EU businesses who are liable to account for VAT on sales to UK consumers.

• Overseas e-commerce businesses

• Further information: Link

22E-invoicing via government platform

Italy

• Established

•transas

companies

only

• The Interchange system (SDI)

• B2B and B2C XML / Fattura PA format

Transmission •

transactions Scope of e-invoices

• Effective January 2019

• Spesometro return has been abolished

and replaced by a new return from January

2019 Impact Proposed • Grace period for late e-invoicing

simplifications

• Paper invoices can be requested by foreign • Extended timing for issuance e-

established companies VAT registered in invoices

Italy

• Simplifications for accounting of

• Virtual stamp duty is applicable for all e- invoices received/issued

invoices issued after 1 January 2019 :

- quarterly

- first payment (Q1 2019) and payment is

due by 20th day following the end of the

reference quarter(20 April 2019)

- direct debit possible or via F24 form

23E-invoicing via government platform

Portugal

Go-live:

• Wave 1: 18 April 2019

(Portuguese central/state

public institutes/entities)

• Wave 2: 18 April 2020

(remaining non-central/public

entities)

(proposed)

• Established & non- • UBL2.1

•transas

established companies

Scope

Transmission • eSPap

of e-invoices ISO/IEC 19845:2015

• B2G transactions only

Further Proposed Until 17 April 2020 suppliers may still

“ESPAP” issue invoices without complying

• guidelines simplifications with the e-invoicing rules (this

(Service Shared Centre for

Portuguese Public Entities) deadline is extended to 31 December

2020 for micro and small companies)

Link

24E-invoicing via government platform

Greece and France

Greece

• Introduction of the mandatory e-invoicing (B2G):

o Proposed go-live dates:

Wave 1: 18 April 2019 (Greek central/state entities or authorities)

Wave 2: 18 April 2020 (remaining non-central public entities)

• Introduction of the mandatory e-invoicing (B2B):

o The proposed go-live date has not been announced

France

• Mandatory B2G invoicing (Chorus Pro)

o 1 January 2017 -> for large companies (more than 5000 employees) and public

entities

o 1 January 2018 -> for intermediate companies (from 250 to 5000 employees)

o 1 January 2019 -> for medium and small companies (from 10 to 250 employees)

o 1 January 2020 -> for very small companies (less than 10 employees)

25Making Tax Digital

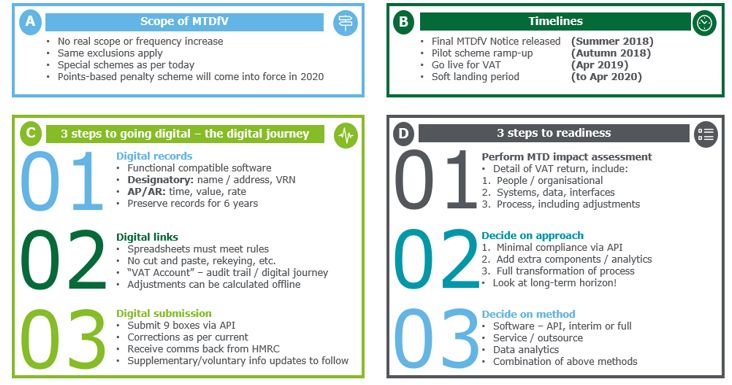

MTDfV

26Making Tax Digital

MTDfV digital submission

Pilot project ongoing

Exclusions:

• Taxpayers involved in cross border transactions

• Taxpayers who received a surcharge in the last 2 years

• Taxpayers who are recently registered and never submitted a VAT return yet

Go-live for VAT can be extended by 6 months (to Oct 2019) for:

• Trusts Prior approval/notification

letter from HMRC required!

• ‘Not for profit’ organisations that are not set up as a company

• Annual accounting scheme users

• Those public sector entities required to provide additional information on their VAT return (such as

government departments and NHS Trusts)

• Local authorities

• Public corporations

• Traders based overseas

• Those required to make payments on account

• VAT divisions and VAT groups

27Other compliance updates

Other compliance updates

Reverse charge

Croatia

• Local reverse charge applicable to non-established VAT registered taxpayers:

abolished from 1 January 2019. Therefore VAT should charged in respect of these

supplies

• VAT reverse charge scope limitation on import of machinery or equipment: reverse

charge on imports only applicable where the import value is higher than HRK 1

million and used exclusively for internal use (i.e. not as stock in trade)

• Extension of local reverse charge mechanism to supply of concrete steel, iron and

related products from 1 January 2019

United Kingdom

• Reverse charge on construction industries will be introduced

• Go-live date: Oct 2019Other compliance updates

Overview

Spain

Luxembourg

Italy

Croatia

Hungary Netherlands

EstoniaOther compliance updates

New obligations, forms, e-filing mechanism

Croatia, Italy

• New compliance obligations from January 2019:

o Croatia:

- New obligation: “Overview of incoming transactions” (Form U-RA)

- Abolished : Form INO PPO

o Italy: “Communication of cross-border transactions”

Canary Islands, Luxembourg, Netherlands

• New VAT return form January 2019

Hungary, Estonia

• New electronic submission platform:

o Hungary: Business Gate is mandatory for established taxpayers from January 2019

o Estonia: Nationality/residency card is mandatory for accessing the e-filing portal

(officially extended from January 2019 to Spring 2019)Other compliance updates

Intrastat

Belgium, Portugal, Ireland and Hungary

• Two additional fields introduced for dispatches intrastat

o Country of origin

o VAT number of the business partner

• Go-live date:

o January 2019 (Belgium and Portugal)

o January 2020 (Ireland and Hungary)

Estonia, Hungary, Austria

• Estonia: new eStat portal since January 2019

• Hungary: new e-filing portal since January 2019

• Austria: new e-filing portal from 18 February 2019

2019 commodity codes

• LinkOther compliance updates

VAT registrations

Switzerland

• (Distance) sales of low value goods

• VAT amount: CHF 5, annual threshold CHF 100 000

France

• Only one tax representative can be appointed for non-established companies from January

2019Brexit

Brexit

Guidance for no deal

Exports

• Distance selling will no longer apply to UK businesses selling goods to EU consumers.

• No requirement to complete EC sales lists or Intrastat (also applies for imports).

EU VAT refund system

• UK businesses will no longer be able to use the EU VAT refund system and will need to use

the 13th Directive mechanism

ESS

• Businesses will no longer be able to use the UK’s MOSS portal.

• UK registered businesses will need to register for the non-union MOSS scheme in another

EU Member State to continue using MOSS

• Suppliers of ESS into the UK using MOSS in another EU Member State at present will need

to register for UK VAT

35Brexit

Guidance for no deal

VAT Numbers

• UK VAT numbers will no longer be checkable on VIES. The government has committed to

developing a replacement system

Imports

• The current rules for imports from non-EU countries will also apply to imports from the EU

• Import VAT accounting via the VAT return will be introduced

• For parcels valued up to and including £135, a technology-based solution will allow VAT to

be collected from the overseas business selling the goods into the UK. Overseas businesses

will charge VAT at the point of purchase and must register with a new HMRC digital service

to account for the VAT due

• For parcels worth more than £135 VAT will continue to be collected from UK recipients in

line with current procedures

36Upcoming Webinar

Brexit

Title:

Brexit – tax readiness

When:

11 January, 1 pm (UK time)

Registration:

Link

37Conclusion

Conclusion

39Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and their related entities. DTTL and each of its member firms are legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not provide services to clients. Please see www.deloitte.com/about for a more detailed description of DTTL and its member firms. Deloitte provides audit, tax and legal, consulting, and financial advisory services to public and private clients spanning multiple industries. With a globally connected network of member firms in more than 150 countries, Deloitte brings world-class capabilities and high-quality service to clients, delivering the insights they need to address their most complex business challenges. Deloitte has in the region of 225,000 professionals, all committed to becoming the standard of excellence. This publication contains general information only, and none of Deloitte Touche Tohmatsu Limited, its member firms, or their related entities (collectively, the “Deloitte Network”) is, by means of this publication, rendering professional advice or services. Before making any decision or taking any action that may affect your finances or your business, you should consult a qualified professional adviser. No entity in the Deloitte Network shall be responsible for any loss whatsoever sustained by any person who relies on this publication. © 2019 Deloitte Belgium

You can also read