Pan European VAT update Deloitte Global Tax Center (Europe) - 24 September 2018

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Pan European VAT update Deloitte Global Tax Center (Europe) 24 September 2018 Olivier Hody, Partner Bruno Roelands, Senior Director David Elliot, Associate Director Deloitte UK Karen Truyers, Senior Manager Sandeep Shinde, Manager

Agenda

• Introduction

• Global and EU VAT developments

• VAT Compliance 2.O: MTD, SAF-T, real time reporting and split payment updates

• Pan EU VAT compliance update

• Conclusion

2

Global and EU

VAT developments

3

GCC

Gulf Cooperation Council states (GCC)

VAT Implementation progress timeline

All GCC countries to

implement VAT by 2019?

GCC VAT

Bahrain, Oman and Qatar

Agreement Domestic are still considering VAT

signed by all legislation implementation end 2018/

six Member in KSA & January 2019. No official

States in June UAE announcements yet

2016 released

2016

2017 2018 ‘18 2019

UAE & KSA Kuwait is rumored to

commit to further postpone the

go live on 1 implementation to 2021

January

2018

1 January 2018

VAT went live in the UAE & KSA

5

Gulf Cooperation Council states (GCC)

UAE and KSA – compliance highlights

UAE KSA

• Voluntary disclosure to be • Stricter approach:

submitted within 20 business high number of VAT

days of discovering an error inspections already taken

(VAT 211) place and penalties for non-

compliance

• Using daily exchange rates

from the Central Bank’s • Extensive guidance published

published list only on Record keeping and VAT

invoicing requirements

• Bank account validation letter

must be submitted when

requesting a VAT refund

Intra-GCC transactions are still considered

as imports/exports

Deloitte Middle

East Tax Handbook

6

European Council & Commission

European Council & Commission

Progress towards e-commerce and definitive VAT

regimes

Communication on the future

of VAT Digital Single Market Strategy VAT action plan

December 2011 May 2015 April 2016

Definitive VAT regime proposals

October 2017

E-commerce proposals

Directive amending the VAT December 2016

Directive:

• Concept of certified taxable

person (CTP)

• ‘Quick fixes’

• Cornerstones of the

definitive VAT system Digital

Entry into Services Tax ?

Amending of the Adoption of VAT e-Com force of MOSS January 2020

Implementing package improvements

Regulation (EU) No December 2017 January 2019

282/2011:

Entry into

4th “quick fix”

force

Amending of the VAT of new VAT

Regulation on SME and Digital Definitive VAT

rules for

Administrative VAT rate Taxation regime proposal

online sales of

Cooperation IT tool proposals proposal (CTP/limited

goods January

January March 2018 ambition)

2021

2018 May 2018

2022: Definitive VAT

regime? 8

Full taxation of

destination principle

European Council & Commission

Progress towards e-commerce and definitive VAT

regimes

Definitive VAT regime E-COM Package

Quick Fixes Current OSS for TBE services

Legal issue with a 5th quick fix -> 1 Improvements (invoicing rules, EUR 10k

year delay expected (entry into force threshold, opening for VAT registered

in 2020 rather than 2019) non-EU businesses) are still expected

for 2019

Destination principle and taxable Extension of OSS to distance sales

intra-EU supply Proposals of Implementing Regulations

Austrian presidency in favour of are drafted and expected to be issued

generalised reverse charge by the Commission still in 2018

CTP Concept Simplified customs arrangements

Many Member States still to be Union Customs Code (and UCC IA – DA)

convinced -> Back to Commission for will be adapted

“rework”

Detailed Proposals for Definitive Supplies facilitated by electronic

VAT regime interfaces

It will not be discussed in the Council Implementing provisions are drafted

before 2019 and discussions are progressing (e.g.

VEG on September 24)

9CJEU cases

European Court of Justice

Interesting CJEU cases

Case Facts

2008-2010 2011 3

Biosafe, Biosafe

C-8/17, 12 incorrectly Correction Expired right to

April 2018 charged the (debit notes) deduct

reduced rate

The substantive and formal conditions giving rise to a right to deduct VAT were met only after

Comment Decision

the adjustment since beforehand it was objectively impossible to exercise the right to deduct

No corrective document

No knowledge about the additional VAT due

Substance

Right to deduct cannot be denied on the ground that the period for the

over form

exercise of that right started to run from the date of issue of the initial

invoices and had expired.

Direct effect

11European Court of Justice

Interesting CJEU cases

Case

Facts

• Gamesa was declared an ‘inactive taxpayer’

on the ground that, for half a calendar year, it had not filed any of its

Siemens returns

• VAT on the purchases was recovered via later VAT returns when the

Gamesa,

VAT number was re-activated

C-69/17, 12

September

2018 Tax audit

Rejection of its right of deduction + penalties

on the ground that the acquisitions were made in the period during

which it had been declared inactive

Comment Decision

A taxable person is entitled to assert its right of deduction

by means of VAT returns filed or invoices issued after the reactivation of its VAT identification number

Substance over even though the acquisitions were made during the period in which its VAT identification number was

form principle revoked

in so far as

the substantive requirements conferring a right to deduct input VAT have been satisfied

and that right of deduction is not being invoked fraudulently or abusively

12European Court of Justice

Interesting CJEU cases

Case

Facts

Immovable let

Marle, Question referred:

C-320/17, 5

Acquisition of shares Does the (intended) letting of an immovable property to

July 2018 a subsidiary constitutes direct or indirect involvement in

the management of that subsidiary.

Holding

MARLE GROUP

Comment Decision

a consideration Letting of a building by a holding company to its subsidiary

(ECJ Larentia) ‘involvement in the management’ of that subsidiary

economic activity

right to deduct the VAT on the expenditure incurred for the purpose of acquiring shares in

that subsidiary

AG opinion

Expenditure connected with the acquisition of shareholdings

Ryanair

belonging to its general expenditure + fully VAT deductible if the holding involves itself in

the management of all its subsidiaries

only partially belonging to its general expenditure + proportionally VAT deductible if the

holding involves itself in the management of only some of those subsidiaries

13VAT Compliance 2.O

(MTD, SAF-T, real time reporting

and split payment updates)

14Making Tax Digital (MTD)

Making Tax Digital

16Making Tax Digital

17SAF-T

SAF-T updates

Poland

• Since July 2018 all taxpayers are subject to a full on-demand SAF-T

• Discussions are taking place to abolish the VAT return in 2019

19Real time reporting

Real time reporting

Hungary

•Since 1 July 2018 •Immediately ~ real time

•All taxpayers with a VAT (within 24 hours requirement has been

registration in Hungary removed)

•B2B transactions above •Without any human intervention

the threshold of HUF

Technical •Upload file in XML format

100000 (VAT amount)

Scope (new version released)

•B2C transaction are out

of scope details •Unique identification number – to be

maintained in the ERP system

•LSPL threshold has been reduced

from HUF 1 million to HUF 100 000 Penalties & •Penalties up to HUF

500 000 per invoice

•Local Sales Listing return is no

longer required in certain Impact further •Official guidance &

circumstances guidance FAQ in English : Link

•Unique identification number is not

required to be mentioned on the

invoice (as previously proposed)

• 1865M box 6 and 1865A-01-05 box 107 are

not required to be completed in the periodical

VAT return

• System outage for more than 48 hours:

o Online Invoicing System

(https://onlineszamla.nav.gov.hu)

o Manual reporting

21Real time reporting

Canary Islands (IGIC)

Due dates

Dates of implementation

Issued invoices: 4 days from its issuance.

However, always before the 16th day of the

Entry intro force from 1 January 2019

following month from the accrual date.

Received invoices: 4 days from its accounting. Mandatory for monthly taxpayer who are:

However always, before the 16th

day of the (i) registered in the Monthly VAT Refund

following month from the accrual date. Register, (ii) registered under VAT Grouping

Regime, or (iii) transactions performed

during last year exceeded EUR 6.010.121,04.

Optional for taxpayers who voluntary want to

enroll the system, by submitting the

corresponding census form.

Submission/due date change for

other Canary Islands returns

Following returns will not be required upon SII

implementation:

Annual IGIC return (form 425)

Local sales and purchase listing (form 415)

Ways of submission

Monthly (form 340) Tax Authorities on-line platform

Change in the statutory date:

Monthly IGIC return (form 420): due date extended to

the last day of the month, following the end of

reporting period

New VAT return form:

A new VAT return form will be introduced applicable

from 1 January 2019

22Split Payment

Split payment

Key updates

Romania

• In force since 1 March 2018

• Mandatory, in case of unreliable taxpayer

• Special VAT Bank Account Register

• Register of ‘Reliable’ taxable persons

• Customer to split the taxable base and VAT payment

Poland

• In force since 1 July 2018

• Optional regime (however it might become mandatory for certain fraud-

prone industry sectors such as telecom)

• A single payment into supplier’s Polish bank account. The supplier’s bank

then segregates the taxable base and VAT amount. VAT then flows into a

special account (“VAT account”)

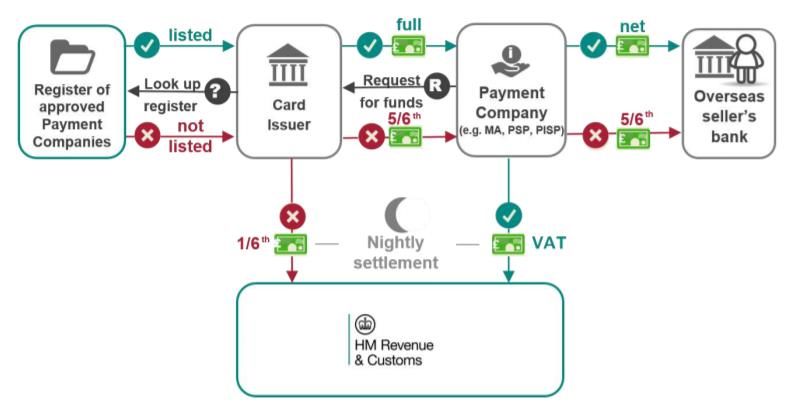

United Kingdom

• Public consultation closed on 29 June 2018

• A technology-based split-payment mechanism, which extracts VAT in real time

and deposits it with HMRC

24E-invoicing via government platform

E-invoicing via government platform

Italy

Scope:

Established

companies only

Foreign companies

with a direct VAT

registration are no

longer in the scope

Start Date:

1 January 2019 Transmission of e-

invoices:

- The Interchange

(Also e-invoicing Mandatory system (SDI)

applicable to supplies E-Invoicing

of fuel has been - XML / Fattura PA

postponed from 1 format

July 2018 to 1

January 2019)

Spesometro return is set to be abolished from 1

January 2019*. (A new return is expected to replace Spesometro)

Paper invoices can be requested by foreign

established companies VAT registered in Italy.

.

26E-invoicing via government platform

Portugal and Greece

Portugal

• Mandatory e-invoicing will be introduced for B2G transactions from 1 January 2019,

• Taxpayers are expected to use a designated via the government platform (further details

are expected in October)

Greece

• Greece is also considering introduction of a mandatory e-invoicing for B2G transactions

from 1 January 2019; and

• Other transactions as from 1 January 2020

27Pan EU VAT compliance

update

28VAT rate updates

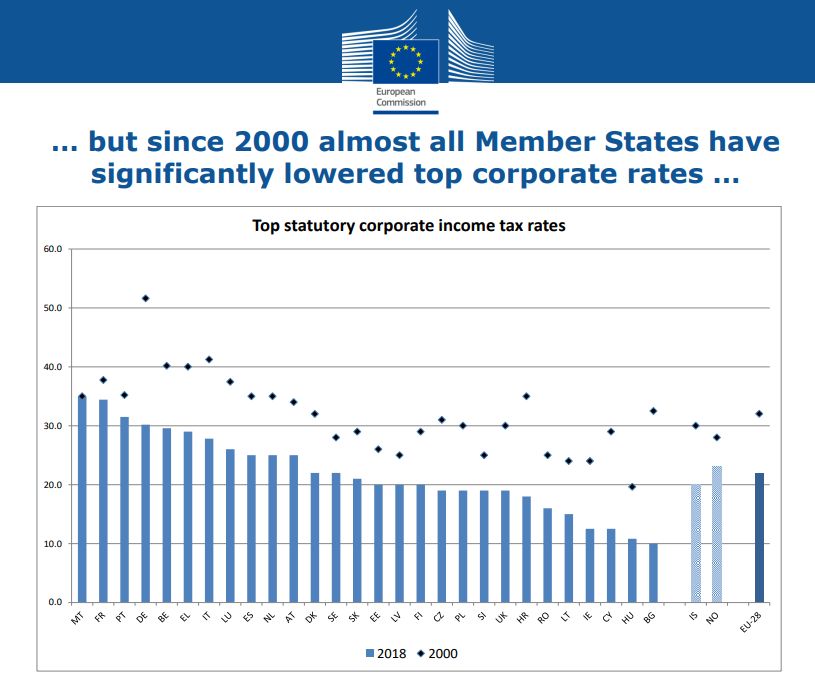

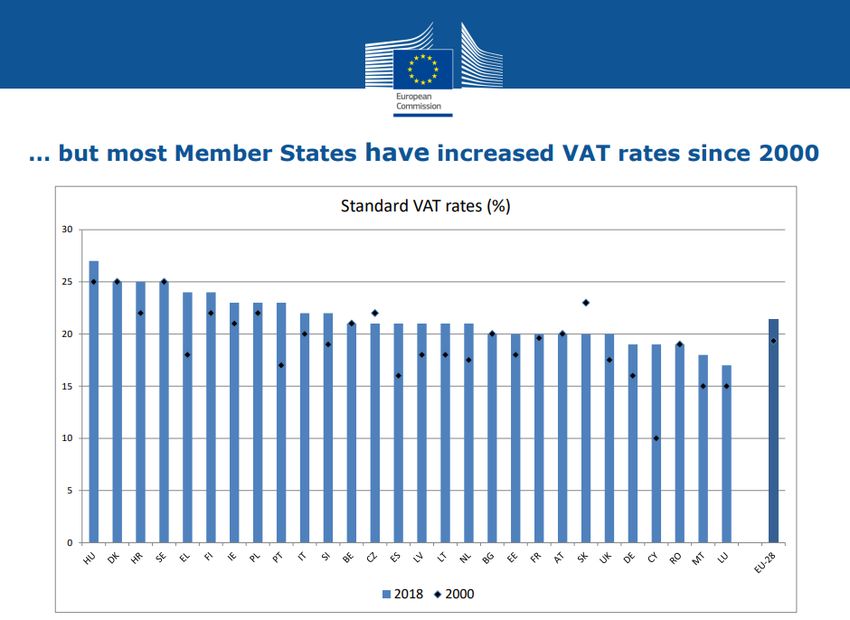

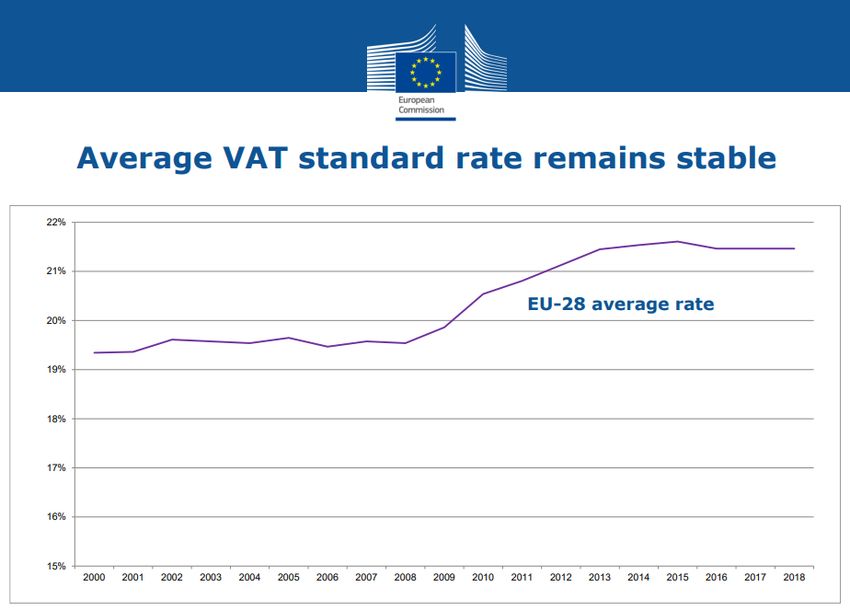

VAT rates

Average VAT standard rate remains stable in the EU

source: The EU Taxation Trends report 2018

• In June 2018, the EU Council has adopted 15% as the minimum standard rate (on a 30

permanent basis)VAT rates

Recent updates

Greece

• Special VAT status will be abolished for the remaining 5 islands from 1 January 2019

(Lesbos, Chios, Samos, Kos, and Leros)

The Netherlands

• The reduced VAT rate will increase from 6% to 9% from 1 January 2019

Croatia

• The standard VAT rate may decrease from 25% to 24% from 1 January 2019 - subject to

further approval from the Parliament.

31General VAT compliance updates

General VAT compliance updates

Input VAT recovery

Italy

• Purchase of fuel, oil and other transport related services from 1 July 2018

provided the payment is performed using one of the following means of payment

methods:

o Cheque or electronic bank transfer, any other e-payment method

o Direct debit

o Credit card, debit card, prepaid card

Greece and Hungary

• VAT incurred prior to VAT registration can now be recovered in certain circumstances

Portugal

• In a recent domestic case, the Administrative Court has concluded that the right to

deduct VAT incurred with a ceased supplier is not restricted; and therefore the

customer is entitled to a VAT deduction in respect of such transaction

• The tax authorities have also published recent binding rulings on bad debts

concerning:

o Sale of receivables and

o Due date by which the invoice is considered as due

33General VAT compliance update

E-filing/ Software/ E-communication

Estonia

• Change of VAT e-filing login system:

o An Estonian nationality ID card is required for e-filing purposes

o In force from 1 January 2019

Norway

• A valid email address is required for primary / authorized contact person to receive

communication electronically from the tax authorities

• Paper correspondence is also abolished in certain cases (such as: notifications concerning

late submissions, change in a VAT registration details). The e-messages will appear on

Altinn (official web platform of the tax authorities)

United Kingdom

• Two-step verification has become mandatory for all taxpayersGeneral VAT compliance updates

Penalty regime

Belgium

• New policy on VAT administrative penalties

o Applicable retrospectively for all penalties issued since 1 January 2018

o Based on the assumption that a taxpayer is in good faith

o Under the new policy, the imposed penalty will be fully waived at the taxpayer’s

request if the following conditions are (cumulatively) met: -

- It is a first offense of its nature (in a reference period of four years)

- The offense was committed in good faith

- The offense has no impact on the amount of VAT due

Latvia

• Proposed changes in the penalty legislation from January 2019

Czech Republic

• Czech tax authorities have started freezing bank accounts of the taxpayers having

recurring outstanding VAT liabilities (i.e. unreliable taxpayers)

35General VAT compliance updates

New bank account of the tax authorities

Germany

• Some local tax offices in Germany have recently changed their bank accounts used for

receiving VAT payments from the taxpayers

• A full list of valid bank account details of the German tax authorities can be found using

the tax authorities website

Romania

• Non-established companies should use the new IBAN account of the tax authorities when

performing a payment of VAT liability in Romania

Bulgaria

• Since 1 August 2018, the bank account is changed for all companies registered with NRA

Sofia, Office Center

36General VAT compliance updates

Import VAT

United Kingdom

• A new Customs Declaration Service (CDS) has been implemented in the UK from 1

August 2018 and will replace the existing Customs Handling of Import and Export

Freight (CHIEF) system over three waves:

o Wave 1: August 2018 - HMRC invited certain companies to test/implement the

system

o Wave 2: November 2019 – CDS will be officially launched for all importers

o Wave 3: Date TBC – CDS will also become available for all exporters

• The new system is intended to meet the requirements Union Customs Code (UCC)

concerning the additional data requirements

• A CDS compatible software is a requirement

Portugal

• In case of imports, exchange rate published via monthly circular should be used to

determine the Euro equivalent of customs value

37General VAT compliance updates

Other

Hungary

• LSPL return: HUF 100 000 (VAT amount) per invoice, from 1 July 2018

Poland and Canary Islands

• New VAT return form is applicable from 1 July 2018 and 1 January 2019 respectively

Malta and Luxembourg

• VAT grouping is introduced from 1 June 2018 and 31 July 2018 respectively

Sweden

• PAYE report needs to be submitted per employee from 1 January 2019

Switzerland

• Radio and Television corporate fee (RTV) will be introduced from 1 January 2019

• Applicable only the Swiss established companies

• Foreign companies are out of scope

38Conclusion

Upcoming Webinar

Brexit

Title:

Brexit - What Would a No-Deal Mean for VAT Compliance?

When:

26 September, 11 am CET

Registration:

Link

40Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and their related entities. DTTL and each of its member firms are legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not provide services to clients. Please see www.deloitte.com/about for a more detailed description of DTTL and its member firms. Deloitte provides audit, tax and legal, consulting, and financial advisory services to public and private clients spanning multiple industries. With a globally connected network of member firms in more than 150 countries, Deloitte brings world-class capabilities and high-quality service to clients, delivering the insights they need to address their most complex business challenges. Deloitte has in the region of 225,000 professionals, all committed to becoming the standard of excellence. This publication contains general information only, and none of Deloitte Touche Tohmatsu Limited, its member firms, or their related entities (collectively, the “Deloitte Network”) is, by means of this publication, rendering professional advice or services. Before making any decision or taking any action that may affect your finances or your business, you should consult a qualified professional adviser. No entity in the Deloitte Network shall be responsible for any loss whatsoever sustained by any person who relies on this publication. © 2018 Deloitte Belgium

You can also read