Revised Fiscal Plan of February 2020 - Estudios Técnicos

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Perspectivas Año

Núm. 3

marzo 2020

27

“Este número de Perspectivas se publica en un momento de mucha incertidumbre por la epidemia de COVID19. El Plan Fiscal, que se resume,

seguramente sufrirá cambios por la necesidad de abordar el impacto económico por parte del gobierno. En ETI se está trabajando en el

tema del impacto, difícil de establecer con precision, precisamente por el desconocimiento sobre la evolución de la epidemia. Entendemos

que es esencial no solo tener una cifra global, sino también como impacta a distintos componentes de la economía y de la sociedad. De

esta manera se podrán enfocar de una manera más efectiva las acciones para mitigar el impacto. Incluimos un artículo de David Jessop del

Caribbean Council en Londres sobre el impacto de la epidemia en el Caribe, pues es bueno saber lo que ocurre con nuestros vecinos.”

Los Editores

Revised Fiscal Plan of February 2020

Por Estudios Técnicos, Inc.

T

he 2020 Fiscal Plan maintains the following structural goods, registering property, and obtaining permits. These

reforms that are expected to improve the economy and reforms are projected to drive a 0.4% increase in overall

drive long-term GNP growth by a cumulative 0.85% (Figure 1): growth by FISCAL YEAR 2025, with annual increases of 0.2%

in FISCAL YEAR 2022 and FISCAL YEAR 2023.

• Human capital and welfare reform: to promote participation

in the formal labor force by creating incentives to work

Continúa en la página 2

through EITC benefits and welfare reform, and providing

comprehensive workforce development opportunities. These Contenido

measures are projected to increase economic growth by 0.15%

by FISCAL YEAR 2025.

• Ease of doing business reform: promoting economic activity Revised Fiscal Plan of February 2020.......................................................................................................1

and reducing the obstacles to starting and sustaining a Repensando los municipios................................................................................................................................. 6

Falling oil prices and COVID-19 will damage Caribbean growth...............................7

business in Puerto Rico through comprehensive reform to

improve ease of paying taxes, importing and transporting

Estudios Técnicos, Inc. no necesariamente suscribe los puntos de vista de los artículos incorporados en la revista, uno de cuyos objetivos

es, precisamente, presentar diversos acercamientos a temas de política pública.

Perspectivas es una publicación de Estudios Técnicos, Inc. Se prohibe la reproducción total o parcial del contenido sin el consentimiento

de los editores. Si le interesa recibir Perspectivas en formato electrónico comuníquese a través de olandino@estudiostecnicos.com

o a través del 787-751-1675. © 2020. Domenech 113 Hato Rey, Puerto Rico 00918-3501 • estudiostecnicos@estudiostecnicos.com.

Perspectivas marzo 2020

Viene de la portada

Figure 1: Impact of Structural Reforms in the May 9, 2019 Certified Fiscal Plan to an assumed 55%

$M flat FMAP.

• Payroll, Operating Expenses and Associated Measures:

General fund payroll and operating expenses have been

updated to reflect the FISCAL YEAR 2020 budget. As such,

measures are included in the baseline forecast in FISCAL

YEAR 2020. FISCAL YEAR 2021 general fund payroll and

operating expenses align with Office of Management and

Budget (OMB)’s recommended FISCAL YEAR 2021 budget.

• Power sector reform: providing low-cost and reliable energy This includes a reinvestment in agency budgets to ensure

through the transformation of PREPA and establishment of an proper delivery of services that have been affected due

independent, expert, and well-funded energy regulator. This is to aggressive expense measures imposed by the FOMB.

projected to increase growth by 0.3% by FISCAL YEA R2025 Additional measures are assumed beginning in FISCAL YEAR

with incremental annual upticks of 0.10% from FISCAL YEAR 2022.

2022 to FISCAL YEAR 2024. The Government has advanced

the process of selecting a proponent for the O&M agreement • Independently Forecasted Components Units (IFCU): IFCU

that will be responsible for the operation of the transmission forecasts have been updated to reflect the FISCAL YEAR 2020

and distribution operation. Selection will be announced by the budget and the FISCAL YEAR 2021 targets, which have been

end of first calendar quarter with a transition period following. re-aligned with management forecasts. Additionally, two IFCU’s

(PRIDCO and Ports Authority) which have outstanding debt

• Infrastructure reform: prioritizing economically transformative and cash flows that will need to be used to fund restructured

capital investments with Federal funds and launching debt service have been removed from the 2020 Fiscal Plan.

maintenance and infrastructure investment policies including

utilizing the P3A to deliver projects efficiently and effectively. • Pensions: The Pay as You Go forecast included in the 2020

Fiscal Plan exclude System 2000 benefits, as the Government

Forecast Update opposes the additional pension reduction measures of the

Incorporates the following relative to the May 2019 Fiscal Plan FOMB.

(Pp. 19-21).

• Impacts of fiscal measures and structural reforms:

• Forecast Period: The forecast period was revised to align

– Before the measures and structural reforms (“baseline

with the new PSA that modifies the September 2019 Plan of

forecast”), there is a pre-contractual debt service surplus

Adjustment. The 2020 Fiscal Plan forecasts revenues and

through FISCAL YEAR 2025. The positive surplus is

expenditures over a 20-year period, from fiscal year 2020

due, in part, to revenues from an expected positive

through fiscal year 2039, to coincide with the maturity of the

macroeconomic trajectory resulting from the disaster relief

new bonds contemplated in the new PSA.

funding stimulus and the incremental Medicaid funding.

• General Fund Revenues: Revenues have been updated for

fiscal year 2020 based on data for the six-months of July 2019

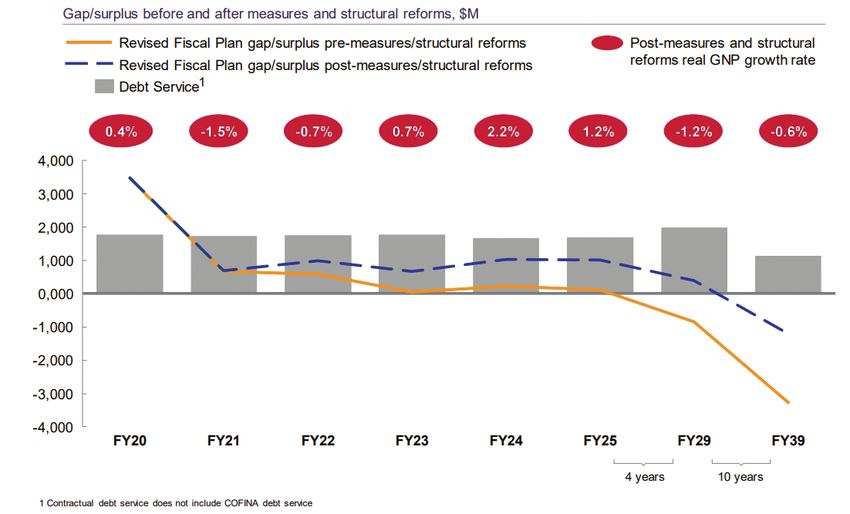

Figure 2: Fiscal Plan Projected Surplus Before and After Measures and

through December 2019. The prior forecast was adjusted in Structural Reforms Macroeconomic and Demographic Trajectory

the short term for outperformance in Personal Income Taxes Post-Maria

(PIT), Corporate Income Taxes (CIT), and Motor Vehicles, which

were 9%, 7% and 39% ahead of plan, respectively. The forecast

outperformance was then phased out over a five-year period

to reflect a realignment of the revenue data as a percentage

of GNP consistent with historical averages and consistent with

the May 9, 2019 Certified Fiscal Plan.

• Medicaid: The Medicaid federal funding forecast has been

updated to reflect the enactment of the “Further Consolidated

Appropriations Act, 2020” which granted the Government of

Puerto Rico $5.3 billion of Medicaid funding in federal FISCAL

YEAR 2020 through FISCAL YEAR 2021 at a 76% Federal

Medical Assistance Percentage (FMAP). Subsequent years

have been updated from a capped approach that was used

2

Perspectivas marzo 2020

– Over the long term, the baseline forecast surplus decreases Revised estimates of federal funds disbursements

as Federal disaster relief funding slows down, Act 154 (Pp. 29-30)

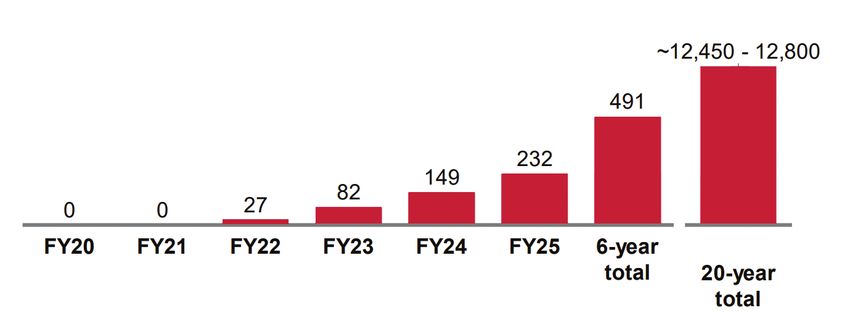

and Non-Resident Withholding (NRW) revenues decline, The 2020 Fiscal Plan projects that $81 billions of disaster relief

and pensions and healthcare expenditures rise. Fiscal funding, including federal and private sources, will be disbursed

measures and structural reforms contained in the 2020 in the reconstruction effort. Of that $47 billions are estimated to

Fiscal Plan would mitigate this downward trend. come from FEMA’s Disaster Relief Fund (DRF). An estimated $8.4

billions will come from private and business insurance payouts,

– Even after the fiscal measures and structural reforms, the

and $6 billions is related to other federal funding. The 2020 Fiscal

annual pre-contractual debt service surplus decreases

Plan includes $20 billion from the CDBG-DR. A total of $3.9 billion

to a negative $1.2 billion forecast by FISCAL YEAR 2039.

in CDBG funding from FISCAL YEARS 2020 – 2032 is estimated to

Real GNP Growth be allocated to offset the Government’s and its entities’ expected

cost-share requirements under federal programs.

The real GNP growth rates estimated are as follows:

The amounts of funds, in particular of CBG-DR funds to be

They are quite lower than those estimated in the Certified Fiscal

disbursed, are lower from those in the Certified Fiscal Plan of May

Plan of May 2019:

2019, in particular for fiscal year 2021, increasing in FISCAL YEAR

2022 through 2014, and then decreasing (Table 3). This accounts

Table 1: Forecasts of Real GNP Growth for Puerto Rico: Comparison

for the lower growth rates.

On the other hand, according to a recent report from FEMA

(2020), the total amount of funds allocated was $44.1 billions

(excluding private insurance), out of which $15.2 billions have

been outlayed/disbursed as of December 31st. If we exclude from

Exhibit 10 private insurance, the amount is $73 billions.

Table 2: Certified Fiscal Plan May 2019

Projected Private and Public Disaster Relief Funding Roll Out

FY18, FY19, FY20, FY21, FY22, FY23, FY24, FY25-FY32

$M, % $M, % $M, % $M, % $M, % $M, % $M, % $M, % Total, $M Total, %

FEMA Public Assistance, 6,400 5,112 3,439 3,197 3,489 3,489 3,489 17,228

Hazard Mitigation, 45,843 55.2%

Mission Assignments 14.0% 11.2% 7.5% 7.0% 7.6% 7.6% 7.6% 37.6%

1,996 604 604 0 0 0 0 0

FEMA Individual

3,204 3.9%

Assistance

18.9% 18.9% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

0 170 2,059 3,446 4,999 4,870 3,096 1,305

CDBG 19,946 24.0%

0.3% 4.9% 21.0% 23.5% 23.0% 16.6% 9.1% 0.0%

4,299 1,851 1,851 0 0 0 0 0

Private insurance 8,000 9.6%

53.7% 23.1% 23.1% 0.0% 0.0% 0.0% 0.0% 0.0%

1,924 1,373 617 489 341 204 189 915

Other federal

6,051 7.3%

funding

31.8% 22.7% 10.2% 8.1% 5.6% 3.4% 3.1% 15.1%

Total 14,619 9,109 8,570 7,133 8,829 8,563 6,774 19,447 83,044 100%

Spending as a % of GNP 21.4% 12.7% 11.7% 9.7% 11.8% 11.2% 8.7% 3.0%

CDBG cost share 0 100 333 357 390 390 390 390

Disaster aid by source of funding, $M

15,000 FEMA PA Private Insurance FEMA IA CDBG Other Fed funding

12,000

9,000

6,000

3,000

0

FY18 FY19 FY20 FY21 FY22 FY23 FY24 FY25 FY26 FY27 FY28 FY29 FY30 FY31 FY32

Continúa en la página 4

3

Perspectivas marzo 2020

Viene de la página 3

Table 3: Certified Fiscal Plan May 2020

Projected Private and Public Disaster Relief Funding Roll Out

Table 4: Disaster Funds Allocated , Obligated and Outlayed for Puerto Rico (as of December 31, 2019)

4

Perspectivas marzo 2020

According to COR3, as of February 24th total funds disbursed Other supplemental federal funding: Additional federal allocated

(Public and individual, plus other funds), amounted to $15.1 billions.1 to various agencies and projects in Puerto Rico following the

Private insurance funding: Analysis of data from the Office of the hurricane.

Insurance Commissioner of Puerto Rico, adjusted for self-insured • The Plan estimated the rate of pass-through to the economy

and other types of coverage, was used to determine the total as follows (P. 32): A 100% pass-through rate assumed for

amount that will be paid out to individuals and businesses for funding that is used directly and in full to replace income or

major damages. stimulate spending on goods and services originating on

Table 5: Detailed Tax Reform Initiatives and Offsets

Table 6: Implied Debt Capacity Based on Range of Interest Rates and Risk

Continúa en la página 6

5

Perspectivas marzo 2020

Viene de la página 5

the Island; An 18% pass-through rate assumed for all other There are additional ones (Pp. 37ss).

funding, including funding used to construct, repair, and Revenue Enhancement (P. 43):

replace buildings, utilities, and other physical goods, or funding

directed toward programs and services on the Island. • The Plan includes a revenue neutral tax model. The projected

Structural reforms, which are also adopted in the Certified Fiscal value of tax reductions and offsets are presented in Table 5

Plan of May 2019: Debt (p. 88)

• The reforms are expected to have a cumulative GNP impact • An implied debt capacity was estimated based on a range

of 0.15% by FISCAL YEAR 2025. The impact is enhanced of interest rates and 2020 Fiscal Plan risk factors under an

in the long-term as K-12 education reforms begin adding assumed illustrative 20-year term and level debt service.

an additional 0.01% GNP impact per year, resulting in an The risk factor was calculated by reducing the amount of

additional 0.07% by FISCAL YEAR 2039. projected cash flow available per year for debt service by a

certain percentage. For example, a 20% risk factor case would

– The EITC: Originally proposed in 2018, it was not enacted use only 80% of the projected cash flow available to pay debt

due to the lack of implementation of a requirement of service on fixed payment debt.

the FOMB of adopting work requirements for the NAP. It

is now available. Additional Risk – the COVID-19 (P. 82): It is added as a significant

risk to the outlook, potentially impacting on the negative side

– NAP Work requirements: The Government will now tourism. No quantitative estimate is provided.

institute the requirements.

– Ease of Doing Business: Not new. Expected to have a Note:

cumulative impact on real GNP of 0.4% through FISCAL 1. COR3 (2020). Datos destacados de la recuperación de los huracanes Irma

y María. At: https://recovery.pr/es. Accessed on March 3, 2020.

YEAR 2025.

Repensando los municipios

Por Estudios Técnicos, Inc.

El debate sobre el futuro de los municipios tiene que trascender Pool Resources” era más eficiente cuando se hacía por las

las posturas que le han caracterizado por años: que hay comunidades directamente afectadas.

demasiados y que son ineficientes e inefectivos. Este punto de ¿Qué se puede decir sobre la situación de los municipios? Lo

partida no es el que conducirá a soluciones que sean efectivas primero es que han replicado la organización del gobierno central

y perdurables. Para eso es necesario contar con una perspectiva con un ejecutivo y una legislatura y con oficinas que replican las

sistémica que establezca claramente cómo se distribuyen las del gobierno central. En efecto, los municipios operan como “mini

funciones relacionadas al manejo de lo público entre municipios gobiernos estatales”, aunque su posición en el “nested system”

y el gobierno central. del que habla Ostrom los debe diferenciar del gobierno central

Los trabajos de Elinor Ostrom (q.e.p.d.) sobre el manejo de en cuanto a funciones y organización.

sistemas complejos ofrecen un excelente punto de partida para La colaboración entre municipios permite aprovechar economías

dilucidar lo que debe ser el papel de los municipios en el Puerto de escala y lograr mayor eficiencia. Por ejemplo, el que una

Rico actual y futuro. Ostrom, profesora de Ciencias Políticas en oficina de permisos sirva a varios municipios, como es el caso del

la Universidad de Indiana recibió el Premio Nobel en Economía consorcio Aibonito, Barranquitas y Comerío, o que un grupo de

en el 2009. En sus trabajos, ella indica que los sistemas de municipios se unan para desarrollar un “minigrid” que les provea

manejo se organizan en múltiples niveles, que llamó “nested electricidad son pasos muy positivos. La Junta de Supervisión

systems” (en español, sistemas anidados), donde cada nivel tiene Fiscal, correctamente, ha otorgado una alta prioridad a lograr

competencias particulares, se organiza para poder aprovechar esos acuerdos colaborativos. Lo que falta en Puerto Rico es una

esas competencias y desempeña funciones diferentes de los ley orgánica que establezca claramente la relación gobierno

otros niveles. Los señalamientos de Ostrom son muy útiles central y municipios, y la delimitación de lo que debe asignarse

para entender la realidad y el potencial de los municipios como a cada cual o, posiblemente, a una estructura regional, siguiendo

entidades capaces de manejar lo local. Su organización y las el concepto de “nested systems” de Ostrom.

funciones que llevan a cabo los diferencian de los otros niveles

(regional y nacional). Ostrom, además, hizo otras contribuciones, A través de los años se han llevado a cabo estudios dirigidos

entre ellas demostró que el manejo de lo que ella llamó “Common a evaluar la situación de los municipios y a buscar soluciones.

6

Perspectivas marzo 2020

Uno fue el trabajo que Estudios Técnicos, Inc. (ETI) completó

para la Fundación del Colegio de CPA sobre la estructura y

las finanzas municipales, otro fue el Informe de la Comisión

sobre Descentralización y Regiones Autónomas del 2015,

también completado por ETI. En ambos se introdujeron análisis

relacionados al tema de esta nota, aunque ambos mantenían

la estructura actual de relación gobierno central/municipios

y el esquema organizativo vigente. En ambos informes se

recomendaron los acuerdos colaborativos entre municipios y

no su consolidación, algo que la Junta de Supervisión, como

indicamos, también ha impulsado.

¿Qué se puede proponer? Una ruta es repensar a los municipios

como si se tratara de entidades de base comunitaria organizadas

para atender necesidades locales. En municipios de mayor tamaño La manera como se maneja la relación gobierno central/municipios es

como San Juan la atención a las necesidades comunitarias se una manifestación de esa obsolescencia y es por eso que resulta tan

necesario reconceptualizar la institución municipal y su relación con el

puede atender con mecanismos distintos como, por ejemplo, gobierno estatal.

unidades comunitarias encargadas de la seguridad, limpieza,

ornato y otras funciones en sus vecindarios. Este replanteamiento primer paso sería separar las elecciones municipales de las

tiene varias implicaciones, siendo uno la transformación de estatales, algo que parcialmente existe, pero es insuficiente

las estructuras de gobierno municipal y la reasignación de para desligar lo local de lo central. De esa manera se enfocaría

funciones y recursos a los disintos niveles de gobierno. No hay el liderato municipal en asuntos locales y eso, que también se

que subestimar las dificultades que esa tranformación conlleva. desprende de los trabajos de Ostrom, conllevaría el manejo más

En el caso de determinados servicios sociales, las normas eficiente y efectivo de asuntos de distinto tipo.

que les rigen pueden ser acordadas central o regionalmente, Se ha aseverado en múltiples ocasiones que el marco institucional

pero los servicios rendirse por los gobiernos locales. Lo que es de Puerto Rico es obsoleto. La manera como se maneja la

necesario reconocer en un nuevo esquema de municipalización relación gobierno central/municipios es una manifestación

es que hay muchas funciones que pueden llevarse a cabo más de esa obsolescencia y es por eso que resulta tan necesario

eficientemente a nivel municipal o, en las ciudades grandes, a reconceptualizar la institución municipal y su relación con

nivel vecinal: mantenimiento de residenciales, arreglo de calles, el gobierno estatal. El sistema municipal como está hoy fue

mantenimiento de escuelas, servicios sociales de distinto tipo y diseñado mayormente en el Siglo 19. Hoy la situación es muy

muchos otros. La evidencia es extensa de que esa aseveración distinta y no hay por qué suponer que lo que nos sirvió hace

es correcta. dos siglos siga siendo adecuado en un contexto muy distinto.

Concebir a los municipios de esta manera, obliga a que los Fue concebido para enfrentar los retos de una economía y una

procesos de elección del liderato municipal se modifique. Un realidad social y política que ya no nos define.

Falling oil prices and COVID-19

will damage Caribbean growth

por David Jessop

The Saudi induced oil price collapse, the impact of COVID-19 on coronavirus, COVID-19, has created a global shock that will touch

tourism, and a world rapidly moving towards a recession means, the Caribbean in ways that may suppress growth for years to

David Jessop writes, that the Caribbean is about to experience come.

an economic shock that will require a significant economic In essence, what the Saudi Prince decided to do, just as

adjustment. international markets were going into free fall and global demand

In normal times a sudden drop in the price of oil would elicit for oil was in decline as a result of the Corona virus, was to flood

a collective sigh of relief among Caribbean governments and an oversupplied world energy market with 12.5m barrels a day

Central Bankers. However, these are not normal times. of crude. His aim was to try to take market share away from

The ill-judged decision by Crown Prince Mohammed bin Salman, OPEC rivals, particularly Russia which has little spare capacity

the de facto ruler of Saudi Arabia, to pump more oil at just the to compete.

moment the global economy is reeling from the impact of the Continúa en la página 8

7

Perspectivas marzo 2020

Viene de la página 7

His decision at such a critical juncture for the world economy While Caribbean nations that import energy are likely to benefit

stemmed from fear that a virus led recession would damage his from lower prices, this is unlikely to offset the fall in visitor arrivals

ambition to modernise the Kingdom, and in the longer term to and taxes now widely anticipated as a result of the coronavirus.

obtain greater strategic advantage in the Middle East and globally, Caribbean governments have agreed a common response to

in a world in which he believes he should be a major player. COVID-19, but a growing reported incidence of imported cases of

Unusually, and despite the uncritical support he continues to the virus in The Bahamas, the Dominican Republic, Cuba, French

receive from President Trump and in particular his son in law, Guiana, Guyana, Jamaica, Martinique, Puerto Rico, St Barts, St

Jared Kushner, even the US Department of Energy was moved Martin and St Vincent, suggest that the region may be unable to

to issue a statement suggesting that the Saudi created price avoid the broader public health consequences.

war amounted to an attempt ‘by state actors to manipulate and The US Government has already suggested that its citizens should

shock oil markets’. avoid all cruises and overseas travel, and the airlines and the cruise

The consequence was that the benchmark price of Brent Crude companies have begun to dramatically reduce their services. In

fell by as much as thirty per cent to US$30 per barrel before the last week the US President announced unilaterally that the

recovering slightly at the time of writing to US$32.55, but with the “foreign virus” meant that air travel from the EU Schengen zone by

markets expecting the price to remain below US$40 for some “most foreign nationals” will be halted. It is a decision that will not

time to come. only impact directly on the tens of thousands of European visitors

Far from having the more normal effect of stimulating the global who daily transit the US to Caribbean destinations and ignores

economy, analysts suggest the effect will be the opposite. They the evidence of how rapidly the virus is spreading in the US, but

say that because the induced oversupply is occurring at just the bodes ill for any other nations that he regards as posing a risk.

moment that COVID-19 continues to spread globally reducing In an indication of how serious COVID-19 could be for Caribbean

demand, the two together will cause a recession of unpredictable tourism, St Lucia’s Prime Minister, Allen Chastanet, recently said

dimensions and duration. They believe the consequence will be that his government is modelling various scenarios including

to further suppress energy consumption, delay investment, and a potential fall in arrivals of between 50 to 80%. In addition,

cause the retrenchment of workers in both the manufacturing Jamaica’s Prime Minister Andrew Holness, has indicated that

and services sectors. some thought has been given to halting flights from the UK

For oil and gas producers the loss of revenue is likely to be given the rapidly rising incidence of cases in Britain: a politically

substantial. In a clear indication of what it will mean if energy complex decision if taken, given the regular travel ‘home’ by

prices stay at their present level, Trinidad’s Finance Minister, Colm the island’s large older diasporic community, and the country’s

Imbert, believes that the collapse in oil prices and lower projected growing British tourist market.

revenue from natural gas will lead to the Republic experiencing a At the same time, Barbados’ Prime Minister, Mia Mottley has

further budget shortfall of US$560m, increasing significantlythe warned that the economic consequences will be difficult to

Republic’s existing budget deficit. contain and may affect the positive progress the island has been

If the Saudi decision is sustained and no accommodation can be making with its IMF programme.

reached with OPEC members, it is also likely that upstream growth The Caribbean is in dialogue with the major International Financial

in Guyana, Suriname and hoped for investment in exploration Institutions including the World Bank and the IMF about possible

elsewhere in the region may decelerate. A much lower oil price responses and support, but it is hard to avoid the conclusion

and demand will also see Guyana’s hoped-for revenues fall, even that between the Saudi induced oil price collapse, the impact

though, according to the CEO of the Hess corporation, John Hess, of COVID-19 on tourism, and the probability, in a world rapidly

the current break-even price for Guyana’s oil at US$35 per barrel moving towards a recession and a loss of global confidence, the

is low by world standards. Caribbean is about to experience an economic shock that will

Another potentially dire consequence is the impact on Venezuela. require significant economic adjustments.

Although it is reportedly selling oil at a heavy discounted price to

overcome US sanctions and a falloff in demand from its principal Note:

remaining markets including China, a collapse in oil revenue David Jessop is a consultant to the Caribbean Council and can be contacted at

coinciding with COVID-19, and a severely weakened health care david.jessop@caribbean-council.org. Previous columns can be found at www.

system, could result in an even worse humanitarian crisis and caribbean-council.org. We are very grateful to Mr. Jessop for permission to

reproduce his columns.

refugee outflow should the virus take hold.

34

Puede acceder las ediciones anteriores de Perspectivas escaneando el

Síguenos en código desde su dispositivo móvil o a través de la siguiente dirección:

Estudios Técnicos, Inc. http://www.estudiostecnicos.com/es/publicaciones/perspectivas.html

años

8

You can also read