TADAT REFLECTIONS: Impacts, Lessons and Beyond

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Secretaria de Estado

da Fazenda de Alagoas

TADAT REFLECTIONS: Impacts, Lessons and Beyond

International Monetary Fund Seminar

Panel Discussion 1: The TADAT Assessment Experience

Key Takeaways

Mr. George Santoro

Secretary of State for Finance – Alagoas/Brazil

June 2018

Summary

1. Socioeconomic Indicators: Brazil and Alagoas

2. Fiscal Federalism: Brazil

3. Alagoas Revenue Composition

4. The TADAT Program in Brazil

5. Evaluation of TADAT in Alagoas

6. TADAT and Strategic Planning

7. Conclusion

Secretaria de Estado

da Fazenda de Alagoas

Socioeconomic Indicators: Brazil

International

Comparative

Gross Domestic Product – GDP (2016) Russian GDP

US$ 1.7962 US$ 1.2832

in trillions in trillions

GDP per capita (2016)

US$ 8,649.95

Gini Index (2014) Mexico Gini

51.48 48.21

Population (2016)

207.7 112.33

in millions pop/km²

Source: World Bank Secretaria de Estado

da Fazenda de Alagoas

Socioeconomic Indicators: Alagoas

International

Comparative

Gross Domestic Product – GDP (2015) Nicaragua

GDP

US$ 12.86 20º/27 0.77% US$ 12.75

in billions Brazilian states ranking % Brazil GDP in billions

GDP per capita (2015)

US$ 3,854.70 25º/27

Brazilian states ranking

Human Development Index South Africa

HDI (2014) HDI

0.667 27º/27 0.666

Brazilian states ranking

Source: 1. IBGE –Brazilian Institute of Geography and Statistics. 2. Trading Economics -

https://pt.tradingeconomics.com

Secretaria de Estado

da Fazenda de Alagoas

Socioeconomic Indicators: Alagoas

International Comparative

Uruguay United Arab

Population (2017) Emirates

3.37 112.33 3.46 112.4

in millions pop/km² in millions pop/km²

Economy – GDP by Sector (2017) Highlights

The newest and fastest growing

Services and Public

66.79% Tertiary hotel chain in Brazil

Administration

From 2007/2017 83.1% growth in

hotel units and 74.9% in beds

Chemical, Plastics, Oil,

13.87% Industry Gas,

Sugar and Alcohol

Oil and Gas exploration

(land/sea)

Alagoas is the largest land gas

Sugar cane,

10.49% Primary producer in whole country

rock salt

Source: IBGE –Brazilian Institute of Geography and Statistics.

Secretaria de Estado

da Fazenda de Alagoas

Fiscal Federalism: Brazil

Tax Revenue – Levels of Government Brazil (2016)

Table 01

Brazil has a good level of fiscal Levels of Tax Revenue % of Tax

Government US$ millions Revenue

decentralization and this is a factor that

Federal 365,107.84 68.27%

underscores the importance of state and

135,841.98 25.40%

counties tax administrations and the need to States

33,882.50 6.34%

improve them. Counties

Total 534,832.32 100.00%

Source: Tax Burden in Brazil 2016: Analysis of Taxes and Bases

of Incidence Federal Revenue of Brazil.

Tax Revenue by Tax Relevance - Brazil (2016)

Table 02

Tax Revenue % of Tax

Tax

US$ millions Revenue The main Brazilian tax is ICMS - value added

ICMS - Value Added Tax 108,933.24 20.37% tax on goods and services - is a state tax.

Income Tax 102,055.21 19.08% Table 02 shows the importance of states

Contribution to Social

88,398.98 16.53% administrations, 20.37% of Brazilian tax

Security

revenue is competency of states tax

Cofins 53,170.79 9.94% administrations. In this sense, TADAT is a

Service Time Assurance

32,905.92 6.15%

important tool to improve this level of

Fund

Brazilian government.

Others 149,368.18 27.93%

Source: Tax Burden in Brazil 2016: Analysis of Taxes and Bases

of Incidence Federal Revenue of Brazil.

Secretaria de Estado

da Fazenda de Alagoas

Alagoas Revenue Composition – US$

2015 2016 2017

Revenue 2,220,222,378.63 2,733,048,006.56 2,639,281,519.96

Tax Revenue 990,162,630.14 1,167,739,943.20 1,220,210,790.53

ICMS – Value Added

828,223,119.25 976,731,784.71 1,016,390,769.52

Tax

IPVA - Property Tax on

54,670,913.55 76,532,578.26 71,492,259.38

Motor Vehicles

ITCD - Transmission

Tax Cause Death and

4,960,384.06 3,005,461.94 2,610,652.17

Donation of Any

Goods or Rights

IRRF - Withholding

90,236,553.30 98,035,174.07 114,211,178.46

Tax

Other Taxes 12,071,659.99 13,434,944.22 15,505,931.00

Transfers of Federal

1,114,756,277.86 1,280,759,442.84 1,199,932,896.27

Government

Other Revenues 115,303,470.63 284,548,620.52 219,137,833.15

Source: SEFAZ/AL - General Balance of the State.

Secretaria de Estado

da Fazenda de Alagoas

The TADAT Program in Brazil

2017: more than 300 trained advisers, moreover

carried out the evaluation in the State of Alagoas

2017: training for auditors from the state of Goiás and

São Paulo

2018: evaluation in the State of Rio de Janeiro and

Partnership of the TADAT Secretariat with planned evaluation in the State of Goiás in July, São

Paulo in August and Brasília in September

the IDB and ENCAT - National Meeting of

State Tax Coordinators and Administrators.

2018: training proposal for "assessment mission

leaders" and risk matrix

Secretaria de Estado

da Fazenda de Alagoas

Evaluation of TADAT in Alagoas

• Training of fifty public

servants from SEFAZ and

the Attorney General of

the State of Alagoas,

public legal body that is

responsible for judicial

collection for the State of

Alagoas.

• Presentation of the

diagnosis.

Secretaria de Estado

da Fazenda de AlagoasEvaluation of TADAT in Alagoas

“The tool provided a big picture of the current situation

of SEFAZ / AL as well as the training provided the

international best practices of tax administrations to

overcome the challenges and problems presented.”

Mr. Leopoldino Mello, Tax Administration Superintendent

“The great challenge of TADAT training was the

adaptation of expertise in income tax to the view of

value added tax (ICMS). This is the big issue of TADAT

for state level in perspective of TADAT for nations.”

Ms. Alexandra Silva, Tax Administration Superintendent

Secretaria de Estado

da Fazenda de AlagoasEvaluation of TADAT in Alagoas: Transparency for Results

TADAT is available

at SEFAZ Alagoas

and TADAT (IMF)

sites

The wide dissemination of the TADAT evaluation gives transparency to its taxpayers, which is a practical value for the fiscal

management of the State of Alagoas

Secretaria de Estado

da Fazenda de AlagoasEvaluation of TADAT in Alagoas: Lessons Learned

TADAT generated greater integration and engagement of

the SEFAZ Team with the current moment of the institution and with its future

It enabled the identification of strengths and weaknesses in the

Tax Administration and Accounting areas of SEFAZ, as well

the judicial collection of the State Attorney General's Office

The wide and unrestricted disclosure of the appraisal report positively exposes the Tax and

Accounting Administration, as it provokes the awareness of responsibility for results and drives the

performance for improvements in management

TADAT can be used as a basis for the formulation of a strategic planning of the Tax

Administration, considerably reducing the time for the preparation of strategic planning, as

well as improving the quality of the planning.

Secretaria de Estado

da Fazenda de AlagoasStrategic Planning: Next steps at the beginning of 2018

Improved Tax Revenue and Strategic Planning started in

Debt Profile February 19

2015 2017 2021

2016 2018

New Management of Secretary of TADAT on October End of Strategic Cycle

State for Finance George Santoro 23 until November 5 SEFAZ/AL 2018-2021

Secretaria de Estado

da Fazenda de AlagoasTADAT and Strategic Planning

Scores

Indicator Summary Explanation of Assessment Strategic Projects Projects/Activities Objectives

2017

POA 1: Integrity of the Registered Taxpayer Base

Information held in the registered taxpayer database

includes all relevant details. There are separate, but linked, 1. Improve taxpayer

P1-1. Accurate and reliable high integrity taxpayer identification numbers (TIN) at the information to analyze

C 1. Big Data -

taxpayer information. federal and state levels. Procedures exist and are regularly and monitor its fiscal

&

applied for identification, suspension and removal of activities, ensuring

Data Mining

inactive taxpayers, but audit reports are not available. effectiveness on tax

collect.

P1-2. Knowledge of the Actions to detect unregistered taxpayers are taken, but only

C -

potential taxpayer base. on an ad hoc basis.

POA 2: Effective Risk Management

P2-3. Identification,

The extent of intelligence gathering and research to identify 2. Artificial Intelligence

assessment, ranking, and

D compliance risks is not comprehensive and mostly limited to (AI) for Collection Tax 2. Ensure

quantification of compliance

internal data sources. Gap comprehensiveness in

risks.

the identification,

P2-4. Mitigation of risks assessment and

There is no structured process to identify, assess, rank and 3. Monitoring of the

through a compliance D 4. Compliance quantification of risks

quantity tax non-compliance risks and to manage them. largest taxpayers

improvement plan. of non-compliance

with taxes.

P2-5. Monitoring and 2. Artificial Intelligence 3. Encourage self-

There is no monitoring and evaluation of the impact on and regulation.

evaluation of compliance risk D (AI) for Collection Tax

changes in taxpayers’ compliance behavior.

mitigation activities. Gap

P2-6. Identification, 4. Mitigating risks

There is no structured and formalized process to identify,

assessment, and mitigation of D 4. Compliance - through a compliance

assess and mitigate institutional risks.

institutional risks. improvement plan.

Secretaria de Estado

da Fazenda de AlagoasTADAT and Strategic Planning

Indicator Scores 2017 Summary Explanation of Assesment Strategic Projects Projects/Activities Objectives

POA 3: Supporting Voluntary Compliance

Although there is a range of information on the main rights

5. Establishing best

and obligations of taxpayers, but these are not adapted to the

5. Best Practices in practices for

needs of disadvantaged groups.

Public Sector communication and a

P3-7. Scope, currency, and Information is kept current, although there is no written 6. Sefaz

C Communications: governance policy.

accessibility of information. procedures to ensure this. SEFAZ website, and other service Interconnected

Digital and 6. Providing

channels are provided to taxpayers at no cost. 62 percent of

Governance Strategies communication

the calls from the taxpayers were answered in less than six

services at no cost.

minutes.

7. Reducing taxpayer

compliance costs and

to give more

P3-8. Scope of initiatives to There is a simplified system of taxation for small taxpayers

7. Artificial Intelligence 8. Simplification of confidence to the tax

reduce taxpayer compliance B called Simples Nacional, and misconceptions of law and rules

for tax calculation Tax Legislation calculation.

costs. are analyzed to improve information products.

8. Improving the

business environment

of the state.

5. Public Sector

P3-9. Obtaining taxpayer

No survey is conducted to monitor taxpayers’ perception of Communications: 6. Sefaz

feedback on products and D -

taxpayer services and products. Digital and Interconnected

services.

Governance Strategies

POA 4: Timely Filing of Tax Declarations

9. Monitoring

72 percent of all taxpayers and 91 percent of large taxpayers 9. Artificial

P4-10. On-time filing rate. C - compliance with

filed their declaration for ICMS Normal on time. Intelligence

obligations.

P4-11. Use of electronic filing All taxpayers use electronic means to file declarations during

A - - -

facilities. the three years examined (2014, 2015 and 2016).

Secretaria de Estado

da Fazenda de AlagoasTADAT and Strategic Planning

Indicator Scores 2017 Summary Explanation of Assesment Strategic Projects Projects/Activities Objectives

POA 5: Timely Payment of Taxes

P5-12. Use of electronic payment All payments (ICMS) are made by the taxpayers by electronic

A - - -

methods. means.

P5-13. Use of efficient collection Advance payment system is used, and there is withholding at

A - - -

systems. source (reverse charge) of ICMS in specific cases.

10. Creating a new

10. New Accounts Receivable accounts receivable to

The number of ICMS payments made on time in 2016 was 29.29

improve fiscal information.

P5-14. Timeliness of payments. D percent of payments due, while the amount of payments was -

11. A New Framework for 11. Ensuring the

76.21 percent of payments due.

Supporting Tax Collection effectiveness of tax

collection.

P5-15. Stock and flow of tax SEFAZ does not have accurate data of tax arrears by age of

D 10. New Accounts Receivable -

arrears. arrears or by collectability of arrears.

POA 6: Accurate Reporting in Declarations

1. Improve taxpayer

The tax audit plan covers the core tax (ICMS) and all taxpayer

P6-16. Scope of verification actions 1. Big Data information to analyze and

segments but does not select audit cases based on identified

taken to detect and deter D & - monitor its fiscal activities,

risks. Additionally, there is limited use of large-scale automatic

inaccurate reporting. Data Mining ensuring effectiveness on

cross-checking to verify information provided in tax returns.

tax collect.

P6-17. Extent of proactive initiatives SEFAZ provides a system of binding public and private decisions

B - - -

to encourage accurate reporting. to guide taxpayers.

9. Monitoring compliance

with obligations.

12. Monitoring of the

P6-18. Monitoring the extent of No monitoring of the extent of inaccurate reporting in tax 12. Assesment Tax

D 9. Artificial Intelligence extent of inaccurate

inaccurate reporting. declarations using tax gap analysis is performed. Gap

reporting in tax

declarations using tax gap

analysis is performed.

Secretaria de Estado

da Fazenda de AlagoasTADAT and Strategic Planning

Indicator Scores 2017 Summary Explanation of Assesment Strategic Projects Projects/Activities Objectives

POA 7: Effective Tax Dispute Resolution

P7-19. Existence of an An appropriately tiered mechanism of administrative and

independent, workable, and judicial review is available to taxpayers. The dispute

A - - -

graduated dispute resolution mechanism is widely used and the administrative review

process. mechanism is independent of the audit process.

13. Virtualizing manual

P7-20. Time taken to resolve

D None of the disputes are resolved within 90 days. processes that have a

disputes.

direct impact on the

13. Digital

- relationship with the

Government

The tax administration undertakes some analysis of tax tax payer, i.e., improve

P7-21. Degree to which dispute

C disputes, but not regularly. The analyses often result in productivity of tax

outcomes are acted upon.

issuance of amendment to rules, procedures or notifications. administration.

POA 8: Efficient Revenue Management

SEFAZ actively participates in the preparation of revenue

P8-22. Contribution to 15. Artificial

forecasts for the budget, monitors results and estimates tax

government tax revenue C - Intelligence to forecast -

expenditures, but does not make projections on the level of

forecasting process. (under studies)

ICMS refunds.

14. Integrated

The tax accounting system is not yet fully automated and

P8-23. Adequacy of the tax Financial and 14. Automating

D taxpayer accounts updated manually at the end of the -

revenue accounting system. Accounting accounting processes.

month.

Administration System

Procedures for processing ICMS refunds do not use risk 10. Creating a new

P8-24. Adequacy of tax refund criteria or pre-refund audits for the most sensitive cases. 10. New Accounts accounts receivable to

D -

processing. Only an insignificant number of ICMS reimbursement claims Receivable improve fiscal

are paid or compensated within 30 days. information.

Secretaria de Estado

da Fazenda de AlagoasTADAT and Strategic Planning

Indicator Scores 2017 Summary Explanation of Assesment Strategic Projects Projects/Activities Objectives

POA 9: Accountability and Transparency

There is no internal audit unit within the SEFAZ to provide

internal assurance to the senior management of the soundness 4. Mitigating risks

P9-25. Internal assurance

C+ and adherence to internal controls. 4. Compliance - through a compliance

mechanisms.

SEFAZ has a well-developed and organizationally independent improvement plan.

internal affairs unit that has adequate investigative powers.

The external oversight of the tax administration’s financial

performance is solid, but oversight of its operational

P9-26. External oversight of

B performance is weak. - - -

the tax administration.

The external investigation process for suspected wrongdoing is

well developed and recommendations are acted upon routinely.

P9-27. Public perception of There is no mechanism to monitor public confidence in the tax

D 4. Compliance - -

integrity. administration.

5. Best Practices in

The annual report on the financial and operational performance 5. Establishing best

Public Sector

P9-28. Publication of of SEFAZ is elaborate and made public within three months of practices for

C+ Communications: -

activities, results, and plans. the end of the financial year. However, SEFAZ does not publish communication and a

Digital and Governance

their strategic corporate plan nor the annual operational plan. governance policy.

Strategies

Secretaria de Estado

da Fazenda de AlagoasConclusion

Problem Suggestions

Mechanisms of Verification of compliance methodology more

specific to the case of subnational entities -

internal controls in subnational inclusion of Tax Compliance Proposal or

entities something similar

Involvement in training between the treasury and

revenue areas and evaluation aiming at

Integration between Treasury and involvement and interdependence between

Revenue Administration in financial / accounting areas with the tax / fiscal

area, due to the need for interface of the

subnational entities accounting records.

Ex: Restitution, Compensation and Active Debt

Secretaria de Estado

da Fazenda de AlagoasSecretaria de Estado

da Fazenda de Alagoas

Governo do Estado de Alagoas

2018

gasantoro@sefaz.al.gov.br

Rua General Hermes, 80,

Centro, CEP: 57020-904

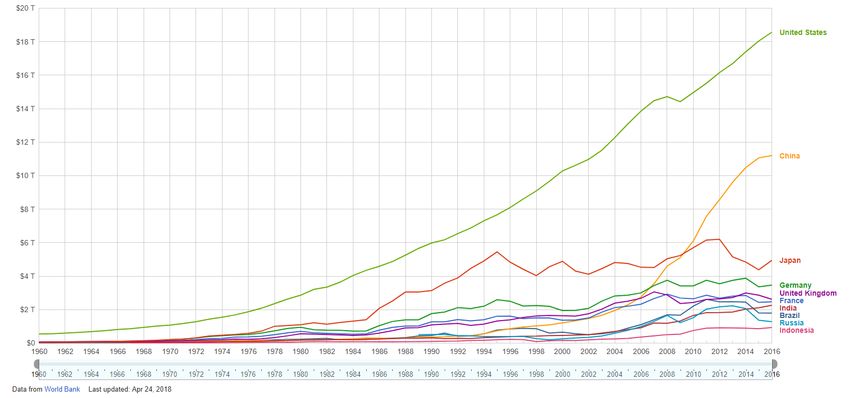

Maceió, AlagoasAppendix A – GDP in current U.S. dollars

Secretaria de Estado

da Fazenda de AlagoasAppendix B – GDP per capita in current U.S. dollars

Secretaria de Estado

da Fazenda de AlagoasYou can also read