The Australian Property Market - an Overview - Institute of Public Accountants

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

The Australian

Property Market – an

Overview

Kel Spencer –

Spencer Property Group

1

Global Economic Outlook

• Global Conditions area reasonable however tilted

towards downside over upside

• Growth in international trade has declined and

intentions have softened

• Forecasted global conditions are accommodative to

further growth – Equity markets strengthened & bond

yields are low

• Global inflation is expected to be subdued,

unemployment rates are low and wage growth has

picked up

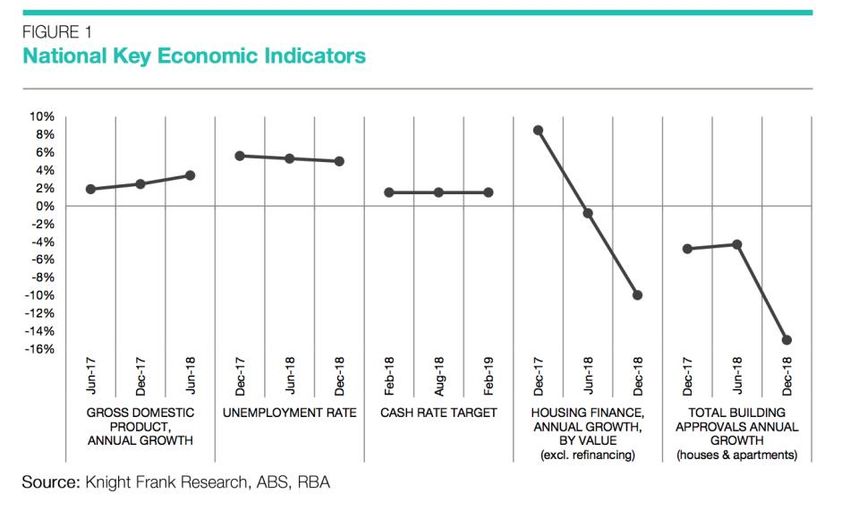

Australian Economic Review

• Australian economy expected to grow between 2-3% in 2019

• Growth has stemmed from increased investment in infrastructure,

pick-up in the resource sector and higher export prices

• Labour market remains strong, unemployment remains steady at

5% and set to decrease further by 2021

• Inflation has been lower than expected (1.3% March Qtr 2019) and

confirms subdued inflationary pressures across the economy

• Low income growth across the economy has resulted in lower levels

of household consumption

• More favorable labor conditions are needed to improve household

consumption and long term income growth

2

National Key Economic Indicators

Australian Residential Property Market

Overview

3

How Big Is The Correction?

• Melbourne and Sydney continue to experience price

correction falls and it is expected to continue throughout

2019

• House prices have been relatively stable in Perth,

Brisbane and Adelaide – however concerns of oversupply

in unit market.

• Hobart the only capital city to enjoy decent growth in

2018

• Unit Prices have also endured losses across all major

capital city’s

Australian Residential Property Market

Overview

4

Credit Availability & Royal Commission

• Credit availability has been a major headwind impacting

Australia’s residential market

• Banks have imposed stronger lending guidelines post royal

commission, decreasing the amount of approved loans

• Investors hurt the most, with a major decrease on credit

availability for investment loans

• House & unit price corrections have been driven by this

decrease in borrowing capability

Where Does the Market Go Now?

• Future Risks – Further impacts of the tightening of credit

• Market expected to bottom out in 2020 (Melbourne & Sydney)

however it may take longer due to uncertainty.

• Reasonable amount of factors (credit, taxation, decreasing foreign

investment) influencing the market that creates further

uncertainty.

• Australian property market is robust, correction falls had to be

endured on the back of extraordinary capital growth.

• Market not expected to ‘crash’ and should enjoy gains in the future

from increased population growth & increased wage growth

5

Australian Commercial Property Overview

Retail Overview & Outlook

• The Australian retail market continues to be supported by

strong population growth and a steady employment

market.

• Retail ‘Localism’ is rising with an increase of participation in

spending within local communities & shopping centres.

• Retail spending growth has been subdued in 2019 on the

back of higher debt and falling house prices.

• Retail spending is forecasted to improve in 2020 with

greater income growth and house price stabalisation.

• Large retail centres offering an overall experience have

performed well and the need for an experience remains

vital in the performance of shopping centres and

destination retail.

6

Retail Investment & Rents (National)

Rise of Online Retail Spending

7

Australian Office Market Review & Outlook

• Overall the Australian office vacancy dropped 0.7% in January

to 8.5%

• The tightest markets are the Melbourne CBD where vacancy

fell to 3.2% (down from 3.6%) and Sydney CBD which dropped

to 4.1% down from 4.6%

• Adelaide and Perth achieved net absorption with both

vacancies falling marginally to 14.1% and 18.5% respectively.

• More than 1 million sqm of office space will be added to the

Australian CBD markets over the next three years with half of

the new space added to the Melbourne CBD which is growing

rapidly

• All capital cities tracked a recorded vacancy rate increases

except for Hobart

Australian Office Investment (Transactions)

8

Australian Industrial Review & Outlook

• The Industrial investment market continues to grow across major

capital cities.

• Demand for industrial investments has benefitted from

expansions in global investment allocations towards the sector.

• Low interest rates and great online spending has generated

greater interest and growth in the sector for both investors and

manufacturers.

• Net face rents continue to grow across most capital cities and

this is forecasted to continue.

• Land values growing rapidly in Victoria and NSW due to the lack

of industrial zoned land coupled and strong leasing demand.

Industrial Investment & Yield

Compression

9

Thank You For Your Time

Are There Any Questions?

IPA TASMANIA CONGRESS 2019

THE AUSTRALIAN PROPERTY MARKET – AN

OVERVIEW

Sources – CBRE 2019, JLL 2019, RBA statement May 2019, Savills 2019,

Knight Frank 2019, The Property Journal Australia, Colliers International

2019, ABS Australia, Fairfax News.

Disclaimer – Past performance is not a reliable indicator of future

performance. Any forecasts given in this document are predictive in character.

Whilst every effort has been taken to ensure that the assumptions on which

the forecasts are based are reasonable, the forecasts may be affected by

incorrect assumptions or by known or unknown risks ad uncertainties. This

information has been produced in good faith and is to be used solely as a

general guide. No liability for negligence or otherwise is assumed by Spencer

Property Group for any loss or damage suffered by any party resulting from

their use of this information

1011

You can also read