The Local Government Finance Settlement 2021- 22 - UK ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

BRIEFING PAPER

Number 09129, 5 February 2021

The Local Government

Finance Settlement 2021- By Mark Sandford

Philip Brien

22

Contents:

1. The 2021-22 settlement:

outline

2. The settlement

3. Additional Government

support

4. The 2021-22 settlement:

statistical summary

www.parliament.uk/commons-library | intranet.parliament.uk/commons-library | papers@parliament.uk | @commonslibrary

2 The Local Government Finance Settlement 2021-22

Contents

Summary 3

1. The 2021-22 settlement: outline 4

2. The settlement 6

2.1 Grants 6

2.2 Business rates revenue 7

2.3 Visible Lines of Funding 7

2.4 Referendum thresholds 8

2.5 Adult Social Care precept 8

3. Additional Government support 10

4. The 2021-22 settlement: statistical summary 12

4.1 Settlement funding 12

4.2 Core spending power 14

4.3 Funding for Covid-19 costs 15

Cover page image copyright: Public services staff at work by Spencer S Eccles Health

Sciences Library. Licensed under CC BY 2.0 / image cropped.

3 Commons Library Briefing, 5 February 2021

Summary

This paper provides background to a debate in the House of Commons on the final Local

Government Finance Settlement 2021-22, scheduled for 10 February 2021. The House of

Commons must approve the settlement before it can take effect.

The provisional Settlement was published on 17 December 2020, and debated on the

same day in the House of Commons. 1 The final settlement documentation was published

on 4 February 2021.

Local government is devolved to Scotland, Wales and Northern Ireland. The Local

Government Finance Settlement, and this paper, apply to England only.

This paper sets out a statistical analysis of the proposed 2021-22 settlement; an

explanation of the Government’s decision-making process regarding the structure of the

settlement; and details of the proposed referendum thresholds for 2021-22.

A dashboard showing historical figures for local government finance settlements is

available on the House of Commons Library’s website. A dashboard containing details of

additional support for English local authorities, to respond to the Covid-19 pandemic, is

also being published.

1

See HCDeb 17 Dec 2020 c426-4454 The Local Government Finance Settlement 2021-22

1. The 2021-22 settlement: outline

The provisional 2021-22 Local Government Finance Settlement was

published on 17 December 2020, and debated on the same day in the

House of Commons. 2 Documentation for the final settlement was

published on 4 February 2021.

The final settlement is scheduled to be debated in the House on 10

February 2021. The House must approve the final settlement before it

can take effect. The settlement applies in England only, as local

government is devolved in Scotland, Wales and Northern Ireland.

Documentation related to the settlement is available on the MHCLG’s

section of gov.uk. This includes:

• The spreadsheet Key information for local authorities, which

includes allocations of funding for each local authority in England;

• Further reports setting out allocations of New Homes Bonus,

social care grant, and the new lower tier services grant to each

local authority in England;

• A paper explaining the operation of business rate retention in

areas that are permitted to retain 100% of business rate receipts

locally;

• Statutory reports setting out the ‘referendum principles’ relating

to council tax: that is, the thresholds above which local authorities

wishing to raise council tax must obtain local approval in a

referendum.

The 2021-22 local government finance settlement is a one-year

settlement, based on decisions in the November 2020 Spending Review.

The Government had planned to implement the Fair Funding Review,

and reset the business rate retention scheme, as of April 2021 (see the

Library briefing paper Reviewing and reforming local government

finance). This was postponed as a result of the Covid-19 pandemic. It is

not yet clear whether it will now take place in April 2022 or at a later

date. In the debate on the provisional settlement on 17 December

2020, the Secretary of State said “…there might be an opportunity to

do it next year, and my Department will work with the Treasury to

review that”. 3

Local government representatives cautiously welcomed the provisional

settlement, whilst expressing the view that a longer-term settlement for

local authorities would be beneficial. For instance, London Councils said:

…this year’s settlement is heavily geared towards short term

measures without much consideration for longer term

sustainability. The social care funding once again plugs a short-

term gap, and the long overdue social care long term plan,

expected next year, must provide a long-term solution for the

sector. The outcome of the Fair Funding Review, the future of

business rates as a tax (through outcome of the “fundamental

2

See HCDeb 17 Dec 2020 c426-445

3

HCDeb 17 Dec 2020 c4345 Commons Library Briefing, 5 February 2021

review” due in the Spring) and of business rates retention, are

other key policy areas the government will need to return to in

the next year or so… 4

The remainder of this paper sets out a statistical analysis of the

proposed 2021-22 settlement; an explanation of the Government’s

decision-making process regarding the structure of the settlement; and

details of the proposed referendum thresholds for 2021-22.

4

London Councils, Provisional Local Government Finance Settlement 2021-22,

December 20206 The Local Government Finance Settlement 2021-22

2. The settlement

This section sets out the main features of the provisional local

government finance settlement for 2021-22.

2.1 Grants

The provisional settlement documentation states that, from 2020-21 to

2021-22, Revenue Support Grant will be increased in line with the

Consumer Prices Index (CPI). The England total of Revenue Support

Grant for 2021-22 is £1.62 billion.

The Social Care Grant will be increased from £1.41 billion to £1.71

billion. Of the extra £300 million, £240 million will be allocated between

authorities so as to offset the effects of the adult social care precept on

council tax. Local authorities vary in the degree to which they can raise

additional council tax revenue via the social care precept. The remaining

£60 million will be allocated via the adult social care Relative Needs

Formula (this formula is used to distribute the existing grant).

The provisional settlement says that “this grant will not be ringfenced,

and conditions on reporting requirements will not be attached”. 5

The Improved Better Care Fund will be maintained at £2.1 billion. No

change will be made to how it is distributed. Allocations of the grant

can be found in the spreadsheet Core spending power: supporting

information.

The New Homes Bonus will be funded by £622m of funding top-sliced

from Revenue Support Grant for 2021-22. The NHB provides funding to

local authorities per new house built in their area above a baseline of a

0.4% increase in housing stock.

In previous years, NHB funding per house built has been provided for

periods of between four and six years. This practice has been known as

‘legacy payments’. Payments made in 2021-22 will not attract legacy

payments in future years. The provisional settlement documentation

says:

The Government has committed to reforming the NHB, and this

year will be the final year under the current approach. We will

publish shortly a consultation document on the future of the New

Homes Bonus, including options for reform. 6

A new Lower Tier Services Grant will be available in 2021-22. A total of

£111 million will be distributed to district and unitary authorities. Of

this, £86 million will top up the lower-tier allocations within the

Settlement Funding Assessment, and £25 million will be used to ensure

that no authority sees a fall in core spending power in 2021-22. This

grant will not be repeated in future years.

The Rural Services Delivery Grant will remain in place, increased by £4

million to £85 million. It will be distributed on the same basis as in

5

MHCLG, Provisional local government finance settlement 2021-22: consultation

paper, 2020, p13

6

Ibid., p157 Commons Library Briefing, 5 February 2021

previous years. Allocations of the grant can be found in the spreadsheet

Core spending power: supporting information.

Allocations of the ring-fenced public health grant to local authorities

were not published alongside the provisional settlement, and have not

appeared at the time of writing.

2.2 Business rates revenue

The Government will freeze the business rates multiplier from 2020-21

to 2021-22, in response to the pressure caused by the Covid-19

pandemic. Normal practice is for the multiplier to rise in line with the

CPI. The English multiplier will be 51.2p in 2021-22, and the small

business multiplier will be 49.9p. 7

Freezing the multiplier will lead to local authorities collecting less in

business rates revenue than they otherwise would. The Government will

pay additional grant to local authorities to take account of the lost

revenue, based on the amount local authorities would have collected if

the multiplier had risen in line with the CPI. 8

The Local Government Association’s briefing states that this specific

additional grant amounts to £650 million across England for 2021-22.

This also includes compensatory grants originating in previous years

when the Government has chosen to freeze the multiplier. 9

2.3 Visible Lines of Funding

In recent years the Government has published a series of ‘visible lines of

funding’ alongside the local government finance settlement. These are

not separate sources of funding. They represent notional allocations of

funding related to grants that, in the past, have been provided by the

Government for specific purposes. All of these grants were rolled into

Revenue Support Grant before 2016. Examples include homelessness

prevention grant, Early Intervention funding, and the learning disability

and health reform grant. The 2021-22 documentation describes them

as follows:

Visible Lines show a notional allocation for grants that were rolled

into the settlement at previous Spending Reviews, most of them

before 2016. These allocations are entirely notional as the core

settlement is not ringfenced and they do not impact on the

settlement distribution or represent an expectation from central

government of local expenditure levels. 10

The documentation states that the Government will not publish visible

lines of funding alongside the 2021-22 settlement, and will not do so

7

MHCLG, Business Rates Information Letter 9/2020, 15 Dec 2020

8

MHCLG, Provisional local government finance settlement 2021-22: consultation

paper, 2020, p9

9

Local Government Association, Provisional Local Government Finance Settlement

2021-22 On the Day Briefing, 17 December 2020, p9. See also the spreadsheet Core

spending power: supporting information.

10

MHCLG, Provisional local government finance settlement 2021-22: consultation

paper, 2020, p188 The Local Government Finance Settlement 2021-22

again for pre-2016 grants. It will consider publishing visible lines of

funding again following future spending reviews.

2.4 Referendum thresholds

The provisional settlement includes planned referendum thresholds for

the 2021-22 financial year. The following thresholds were proposed:

• Local authorities with responsibility for social care (county and

unitary authorities) must hold a referendum if council tax is to be

increased by 5% or more. Council tax for general spending

requires a referendum if it rises by 2% or more, alongside a

maximum 3% ‘social care precept’. Some or all of the adult

social care precept for 2021-22 can be deferred to 2022-23, in

which case it may be used on top of any thresholds set for 2022-

23;

• For district councils, a threshold was set of 2% or more or more

than £5.00 on a Band D property, whichever is the greater;

• For Police and Crime Commissioners (PCCs), fire and rescue

authorities, and the Greater London Authority: if council tax is to

be increased by more than £15 on a Band D property;

• No principles were set for Mayoral Combined Authorities or for

parish and town councils;

The principles for the Greater London Authority were set following

negotiation between the GLA and MHCLG. This took place in the

context of large-scale Government financial assistance for the GLA

group, in the light of the financial impacts of the Covid-19 pandemic.

A report in the Local Government Chronicle on 11 January 2021 stated

that the Mayor of London planned to seek a 9.5% rise in council tax for

2021-22. 11 In the event, the principle was set at £15 on a Band D

property. This was confirmed by a letter from the Secretary of State to

the Mayor of London on 4 February 2021.

2.5 Adult Social Care precept

The adult social care precept, noted above, will provide much of the

headline increase of 4.5% in core spending power. The Local

Government Association briefing says:

….more than 85 per cent of the potential core funding increase

next year is dependent on councils increasing council tax by up to

5 per cent next year. This leaves councils facing the tough choice

about whether to increase bills to bring in desperately needed

funding to protect services at a time when we are acutely aware

of the significant burden that could place on some households. 12

The Institute for Fiscal Studies’ December 2020 briefing states that 87%

of the headline increase derives from council tax. This also assumes that

all authorities choose to increase council tax by the maximum permitted

without a referendum, which some authorities may decide not to do. In

11

Sarah Calkin, “Mayor proposes 10% council tax hike”, Local Government Chronicle,

11 January 2021

12

Local Government Association, Provisional Local Government Finance Settlement

2021-22 On the Day Briefing, 17 December 2020, p19 Commons Library Briefing, 5 February 2021

addition, the IFS states that the figure assumes that current rates of new

housing are maintained, which may not occur:

Based on new housebuilding alone, we would expect tax base

growth of more like 1%, which would mean £200 million less

revenue than the government has assumed. If increases in receipt

of means-tested discounts were to offset entirely underlying

increases in the number of houses, there would be a revenue

shortfall of over £500 million relative to what the government has

assumed. And of course, growth in means-tested support could

exceed this. 13

In 2021-22, central grant funding for local government is planned to

rise by £292 million compared to 2020-21. 14

13

Kate Ogden and David Phillips, Assessing England’s 2021-22 Local Government

Finance Settlement, Institute for Fiscal Studies, 2020, p5

14

Kate Ogden and David Phillips, Assessing England’s 2021-22 Local Government

Finance Settlement, Institute for Fiscal Studies, 2020, p4-510 The Local Government Finance Settlement 2021-22

3. Additional Government

support

The Government has provided substantial additional funding to local

authorities during the 2020-21 financial year, to mitigate the impacts of

the Covid-19 pandemic. In the debate on the provisional settlement on

17 December 2020, Robert Jenrick, the Secretary of State for

communities and local government, said:

Early in the pandemic, the Local Government Association came

before the hon. Gentleman’s Committee and estimated that costs

incurred by local councils would be around £10 billion. We are

going to end this financial year having provided local councils

with, I suspect, about £10 billion, and we are providing further

billions of pounds into next year. 15

A number of additional sources of funding were announced on 5

January 2021. These include:

• £1.55 billion in un-ringfenced funding for local authorities. This is

to be distributed according to the ‘Covid Relative Needs Formula’.

In effect, it is a fifth tranche of the funding support summarised in

the 22 October announcement. The Government guidance does

not prescribe what use should be made of the funding, but

recommends priority be given to:

….adult social care, children’s services, public health services,

household waste services, shielding the clinically extremely

vulnerable, homelessness and rough sleeping, domestic abuse,

managing excess deaths, support for re-opening the country and,

in addition, the additional costs associated with the local elections

in May 2021. 16

• £670 million to be distributed to local authorities to support local

council tax support schemes. These are expected to face increased

pressure due to the economic effects of the pandemic.

• A Government commitment to reimburse local authorities for

75% of irrecoverable council tax and business rates shortfalls in

the 2020-21 financial year. Authorities must make claims for

reimbursement based on their forecast income;

• Compensation for lost income from sales, fees and charges,

originally announced on 24 August 2020, is to be extended to

cover April, May and June 2021.

Details of how this funding will be allocated between local authorities,

and other information, is available on the MHCLG section of gov.uk. 17

The IFS estimate that, in December, the Government had provided

“more than enough funding” for local authorities to address Covid-

related stresses. 18 This was before the latest support package,

15

HCDeb 17 Dec 2020 c431

16

MHCLG, COVID-19 funding for local government in 2021-22: consultative policy

paper, 11 Jan 2021, paragraph 20

17

Ibid.

18

Kate Ogden and David Phillips, Assessing England’s 2021-22 Local Government

Finance Settlement, Institute for Fiscal Studies, 2020, p911 Commons Library Briefing, 5 February 2021

announced in January 2021, which provided an extra £1.55 billion in

un-ringfenced grants for local authorities. They also warn that Covid-19

may lead to greater demand for council services, alongside other drivers

such as “the ageing population; rising numbers of younger adults with

learning disabilities; increases in the number of children under the

supervision or care of councils; and increases in labour costs, in part

because of increases in the National Living Wage”. 19

19

Kate Ogden and David Phillips, Assessing England’s 2021-22 Local Government

Finance Settlement, Institute for Fiscal Studies, 2020, p1112 The Local Government Finance Settlement 2021-22

4. The 2021-22 settlement:

statistical summary

This section provides a high-level statistical analysis of the provisional

2021-22 local government finance settlement.

Funding to local authorities is reported using two different sets of

figures:

• Settlement funding broadly represents the amount of money

allocated to local authorities from central government. It includes

the Revenue Support Grant, redistributed business rates, and

some specific grants, but does not include grants which are

passed straight through to recipients such as the Dedicated

Schools Grant.

• Core spending power is a concept created by central

government, and is intended to represent the total amount of

money over which local authorities can take spending decisions. It

therefore includes settlement funding, but it also includes other

grants such as the Improved Better Care Fund, the New Homes

Bonus and the Social Care Grant (although, as with settlement

funding, it does not include grants passed through to recipients).

Significantly, it also takes into account an estimate of the amount

of money that local authorities are expected to raise through

Council Tax, and assumes that they raise their Council Tax rates by

the maximum permitted without triggering a local referendum in

order to do this.

4.1 Settlement funding

The amount of settlement funding allocated to each local authority for

2021-22 is very similar in cash terms to the amount allocated for 2020-

21. 42% of all local authorities will see no change at all (that is, their

allocation is exactly the same as the previous year); no local authorities

were allocated less than in 2020-21, 20 while some had very small

increases. The largest cash-terms increase by percentage was 0.3%, for

the Isles of Scilly.

The provisional settlement documentation states that the Government

has provided “a uniform percentage increase in 2020-21 Revenue

Support Grant (RSG) allocations, based on the change in the Consumer

Price Index (CPI)”. 21

This very consistent distribution across local authorities means that their

longer-term funding position remains much the same as last year. As of

the 2021-22 financial year, settlement funding as a whole in England

20

There was one exception to this – Isle of Wight saw its funding decrease by 7%

compared to 2020-21. However, this is because responsibility for fire services will be

transferred to the new Hampshire and Isle of Wight Fire and Rescue authority from

2021; the change in funding reflects the transfer of responsibility.

21

MHCLG, Provisional local government finance settlement 2021-22: consultation

paper, 2020, p613 Commons Library Briefing, 5 February 2021

will have decreased by 30% in cash terms since 2015-16, and all but

two local authorities will have seen at least some decrease. 22

We cannot provide real-terms figures covering 2020-21 and 2021-22 –

this is because the large changes in how public services were delivered

during the Covid-19 pandemic (and the expected change back again as

life returns to normal) have had a serious effect on the government

consumption figures. This means that calculating real-terms figures

based on this data is not meaningful. 23

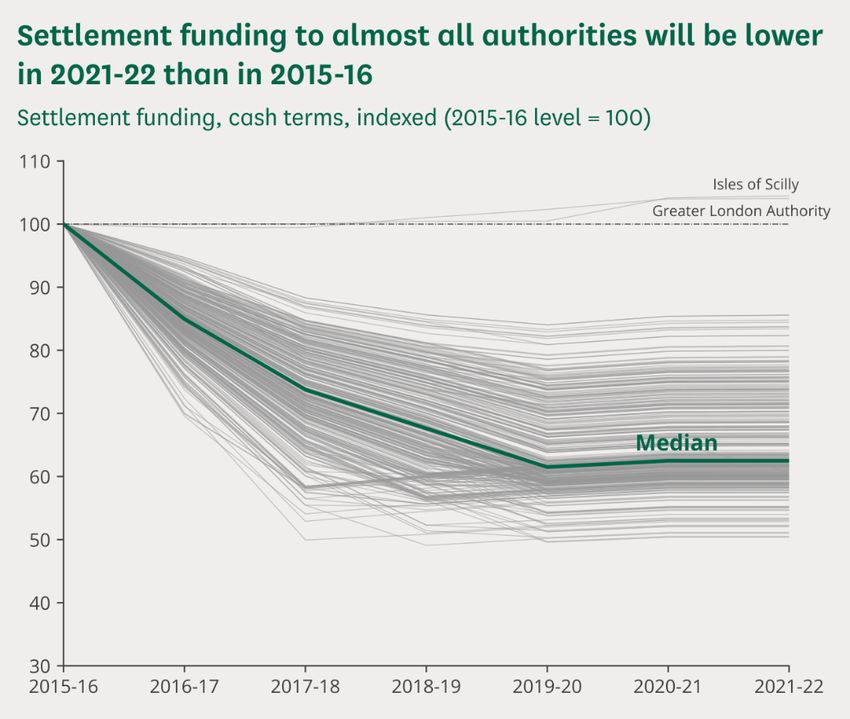

The grey lines in the chart below correspond to every local authority in

England which received funding every year from 2015-16 to 2021-22.

They show each authority’s funding as a proportion of its funding level

in 2015-16.

Note: The grey lines represent every local authority in England where we have a figure for

settlement funding in each year from 2015-16 to 2021-22. The median line indicates the point

where half of authorities have higher indexed settlement funding and half have lower – it does not

follow the same authority across all years.

Source: MHCLG, Local government finance settlement: England, 2021 to 2022, 4 February 2021

22

The two exceptions are Isles of Scilly, which has its level of funding set separately to

all other local authorities due to its unusual geographical situation, and the Greater

London Authority, which received a large increase in funding in 2017-18 reflecting

changes in the collection and retention of business rates. See paragraph 1.6 of the

GLA’s 2017-18 budget.

23

The difference between nominal and real government consumption is measured by

looking at the difference between the amount spent by government and the

amount of services actually delivered. The Covid-19 pandemic resulted in some

services being heavily affected (with the closure of schools, for example), and this

has had an effect on the GDP deflator which does not reflect actual increases in the

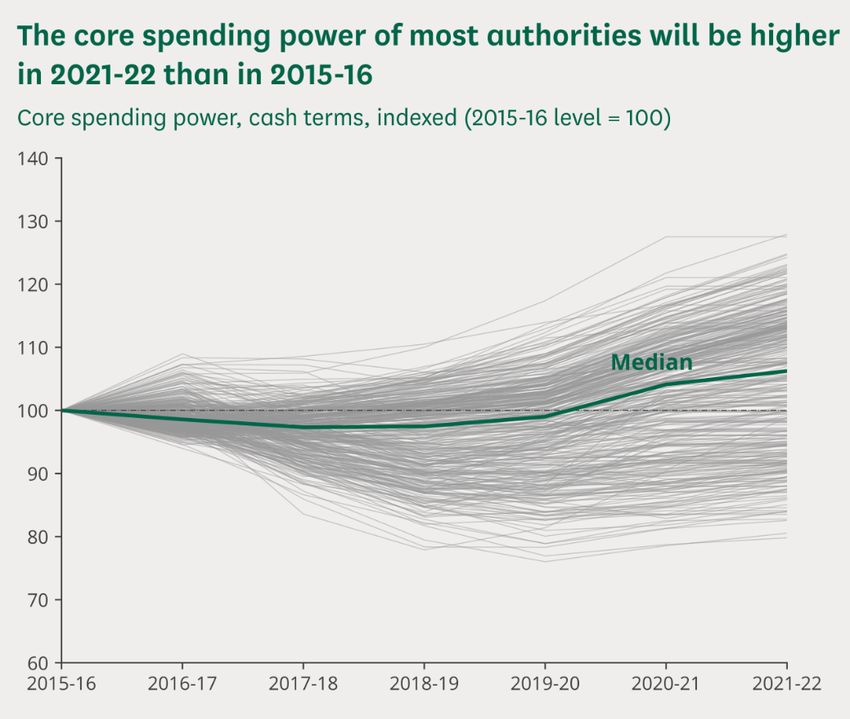

price of delivering these services.14 The Local Government Finance Settlement 2021-22 This shows that although there is considerable variation between local authorities as to how far their funding has been reduced, the overall trend is consistent – funding generally decreased in cash terms in every year between 2015-16 and 2019-20, although the decreases tended to get smaller each year, and has been essentially flat since then. 4.2 Core spending power In cash terms, core spending power in England as a whole will be 4.6% higher in 2021-22 than the previous year. The majority of this increase comes from a 6.7% increase in the expected council tax take (see section 2.5 above), which rises to £31.2 billion compared to £29.2 billion in 2020-21. No local authorities will see a cash-terms decrease in core spending power in 2021-22, but the variation between authorities is far larger than for settlement funding. The largest increase is 9.0% (for Braintree), while the median is 3.2%. As with settlement funding, we cannot calculate meaningful real-terms figures for the period covering 2020-21 and 2021-22. However, as the chart below shows, the cash-terms increase for all local authorities continues the trend from last year’s settlement. A small majority of authorities (63%) will now have spending power that is higher in cash terms than it was in 2015-16. Note: The grey lines represent every local authority in England where we have a figure for core spending power in each year from 2015-16 to 2021-22. The median line indicates the point where half of authorities have higher indexed spending power and half have lower – it does not follow the same authority across all years. Source: MHCLG, Local government finance settlement: England, 2021 to 2022, 4 February 2021

15 Commons Library Briefing, 5 February 2021

Core spending power for most classes of authority has followed a

similar path, but as the chart below shows, shire districts have seen

greater cuts and a slower recovery than other classes.

Source: MHCLG, Local government finance settlement: England, 2021 to 2022, 4 February 2021

Although shire districts have seen a cash-terms increase in spending

power in this settlement, they remain the only class of authority not to

have seen its spending power recover past 2015-16 levels.

4.3 Funding for Covid-19 costs

This settlement does not include specific extra funding to help local

authorities to cope with the impact of Covid-19 – this has instead been

provided through other sources. For example, £4.6 billion of emergency

un-ring-fenced funding for local authorities has been provided in four

tranches over the course of 2020, and further allocations have been

made for 2021. 24

MHCLG has been monitoring the financial impact of the pandemic on

local authorities. As of the most recent round of reporting in January

2021, local authorities in England have estimated that the total impact

of Covid-19 on their budgets in 2020-21 will be around £12.6 billion

(£6.9 billion of additional spending, and £5.7 billion of lost income). 25

By far the largest area of additional spending (making up 45% of the

total) has been additional spending on adult social care, particularly

from higher demand and supporting the market. The largest losses of

income have come from lower sales, fees and charges (37% of all

losses), followed by business rates (27%). These losses will be mitigated

24

See MHCLG, Coronavirus (COVID-19): emergency funding for local government in

2020 to 2021 and additional support in 2021 to 2022, 11 January 2021

25

MHCLG, Local authority COVID-19 financial impact monitoring information, 25

January 2021, round 8, tables 1 and 216 The Local Government Finance Settlement 2021-22 to some extent by the sources of support noted in section 3 above. The exact amount of support provided under those programmes will not be known until data becomes available later in 2021.

About the Library

The House of Commons Library research service provides MPs and their staff

with the impartial briefing and evidence base they need to do their work in

scrutinising Government, proposing legislation, and supporting constituents.

As well as providing MPs with a confidential service we publish open briefing

papers, which are available on the Parliament website.

Every effort is made to ensure that the information contained in these publicly

available research briefings is correct at the time of publication. Readers should

be aware however that briefings are not necessarily updated or otherwise

amended to reflect subsequent changes.

If you have any comments on our briefings please email papers@parliament.uk.

Authors are available to discuss the content of this briefing only with Members

and their staff.

If you have any general questions about the work of the House of Commons

you can email hcenquiries@parliament.uk.

Disclaimer

This information is provided to Members of Parliament in support of their

parliamentary duties. It is a general briefing only and should not be relied on as

a substitute for specific advice. The House of Commons or the author(s) shall

not be liable for any errors or omissions, or for any loss or damage of any kind

arising from its use, and may remove, vary or amend any information at any

time without prior notice.

The House of Commons accepts no responsibility for any references or links to,

BRIEFING PAPER or the content of, information maintained by third parties. This information is

Number 09129

provided subject to the conditions of the Open Parliament Licence.

5 February 2021You can also read