Welcome to Harvest Financial Services presentation on Getting Your Retirement Strategy Right 12th May 2016

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Welcome to Harvest Financial Services

presentation on

Getting Your Retirement Strategy Right

12th May 2016

Who are Harvest Financial Services?

• 23 years in business

• 50+ highly qualified staff

• Circa €1 billion under administration

• Highly regulated

- MiFID/Pension Trustees/QFM

• Fee-based business model

• Pensions, investments and financial planning

Today’s Topics

• Why Pensions are important.

• Background to pensions and how to maximise the

opportunities – Emer Kirk

• Investment Options and the need for exposure to

real assets – Terry Devitt

The need for Retirement Planning

was never more critical

• Mortality improvements

– DB – employer took risk

– DC – now its down to us as individuals

• Age 60 or 65 target retirement date mindset – but

we have no idea what we can expect

• State Pension - we can’t assume it will be sustained

at anywhere near current levels

The Bad News

We’re living longer….

CSO: Census 2011

How much is enough?

Only YOU can answer this

• What income will you need in retirement?

• Will you carry debt in to retirement?

• Will your kids be independent?

• Will your parents need assistance?

• How are you going to fund it???

Emer Kirk Getting Your Retirement Strategy Right

What I hope to cover today • Planning for retirement – how to fund it? • Tax reliefs still available • Different pension structures • Protecting your plan

How are you going to fund it?

Savings &

Investments

Inheritance

Personal

Value of Business

Business

Private Pension

Income

Pension State PensionPersonal Wealth • Income from investments, e.g. will investment property provide rental income in retirement • Inheritances • Savings • Capital value of investments

Business Wealth • Will your business have any value at retirement? • Can it be sold? • What is it’s real value? • Do you intent to pass the business on to children? (PWC 2014 Irish Family Business Survey) • Will Retirement Relief be available? • Can you de-risk by taking cash out of the business tax efficiently throughout your working life?

Retirement Relief • EUR 750,000 tax free if over 55 and under 66 • EUR500,000 if over 66 • Nothing tax free if significantly over limits e.g. sell for EUR2m – no retirement relief • Family company (generally 25% minimum) • Must be full time working director for 5 years • Available to spouses individually

Tax Efficient Cash Extraction

a.k.a. Pensions

• Take value from business for own/family’s benefit

• Corporation tax deduction

• Income tax relief on personal contribution

• Funds are invested in tax exempt investment vehicle,

no income tax or CGT

• Portion paid tax free at drawdown

• Passes to spouse/children tax efficiently on your

demise

• With some restrictions, you can decide where to

invest the fundsThe Different Types of Pensions • Traditional pension – insurance company, managed funds • Self Directed Pension – insurance company, more investment choice • Self Administered Pension – held in trust, open architecture, wide investment choice

Why Self Administered? • Control • Flexibility • Security • Transparency

Self Administered Pensions –

Some Investment Options

• Investment funds – equities, bonds, multi asset

• Deposits

• Individual shares

• Property

– Direct property

– Development Partnerships

– Property Funds, e.g. IPUT, REITSTax Efficiency

Draw from Company now Contribute to Pension

Gross amount €100,000 €100,000

Income tax, USC, PRSI €52,000 €0

Net amount for investment €48,000 €100,000

Invest for 20 years @ 4% €105,174 €219,112

Net return (ignore CGT) €105,174

25% tax free lump sum €54,778

Balance @ 52% €85,454

Net return €133,659

Return on Gross Amount 105% 134%Pensions – What you need to know! • Most appropriate pension structure for you • Tax reliefs available, both corporation & income tax • Gross roll up on investment returns • Tax efficient lump sum at retirement • Passes to estate/beneficiaries on death • Standard Fund Threshold of €2M – per person (spouse’s pension?) • Costs…. All the costs! • Where it is invested and the impact of investment returns on your retirement income (pre & post retirement)

Need to protect the plan! • What happens to your income if you cannot work? • What happens to your family’s income if you die? • What happens to your business if one of your partners cannot work? • What happens to your business if one of your partners dies? • Need to look at protecting both family and the key individuals in your business that can impact on your plan!

How do Harvest help? • Indentify needs and objectives • Prioritise these needs and objectives • Work with your advisors (e.g. solicitor, accountant, tax advisor) • Put your financial plan in place – pension, protection, investment advice • Review regularly

Terry Devitt The Need for Risk

So What is Happening in the World? • Interest rates at all time lows • Inflation largely absent • Debt levels at all time highs • Equity markets volatile • Growth difficult to come by

The Geopolitical Landscape BREXIT….. The Rise and Rise of Donald….. Does QE actually work….? All eyes on China……

25 yr Performance of Major Asset

ClassesGetting Comfortable with the Risk in

your Portfolio

• Growth cannot happen without Risk

• Most important Ingredients are Time

and Diversification

• Learn to Ignore Market FluctuationsCash Fund vs. Equity Fund

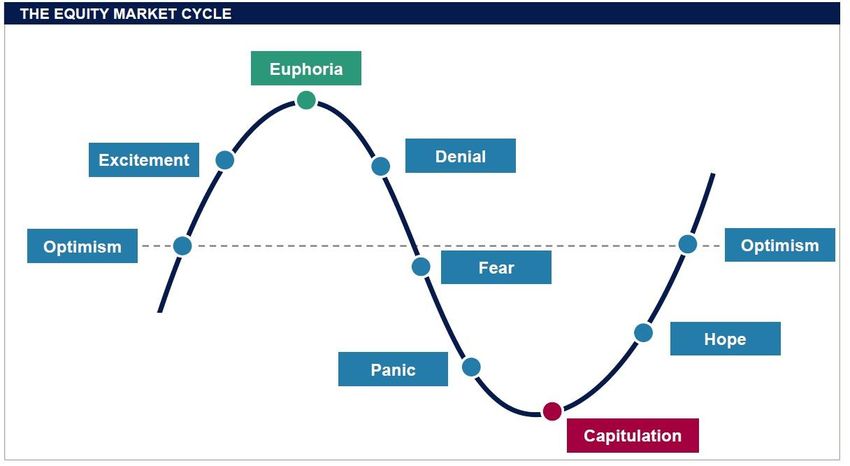

The Equity Market Cycle

FTSE 100 over 30 years

“Avoid trying to predict the markets. Remember We

have two classes of forecasters: Those who don't

know …and those who don't know they don't know”

J K GalbraithThe Passive vs Active Debate • Passive investing has exploded over the past decade • Relative costs and performance main drivers of this trend • But passive investing not the answer to all investment challenges

Passive vs Active 1 European Equities

Summary of investment Process

Geopolitics Age

Attitude to Risk Projections and

Market Review

Economics Market Valuations

Risk Profile

Conditions of

Investor

Suggested

Portfolio

Research and Analysis Monitoring and Review

Recommended

Funds ListHarvest’s Risk Rating of

InvestmentsFive Investment Pillars • Time Horizon • Asset Allocation/Diversification • Differentiate between Cyclical and Permanent Losses • 80:20 Rule • Income

1. Time Horizon • Exposure to Risk Assets (Equities, Property) requires a time horizon of five years minimum • This allows for market cycles to run their course

And We All have More Time than we Think …

Centenarians in Ireland

300

250

200

150

Centenarians in Ireland

100

50 Source: Human

Mortality database

(HMD)

0

1994

2004

1950

1952

1954

1956

1958

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1996

1998

2000

2002

2006

2008

20102. Asset Allocation and Diversification • Important to achieve appropriate balance between the major asset classes • Market timing is a very difficult thing to get right so at times of uncertainty phased investment is advisable

Balanced Asset Allocation

3. Cyclical and Permanent Losses

Portfolio Losses

Permanent

Cyclical

• Single Stocks

• Diversified Equities

• Geared Property

• Ungeared Property

• Debt of any Kind

• Private Equity4. Follow the 80:20 Rule • Ensure at least 80% of your portfolio is diversified, liquid and does not involve gearing • The corollary is that a maximum of 20% of the portfolio should run the risk of permanent loss

5. Income • Build in an income focus to a portion of your portfolio • Income a real measure of value • Compensation during volatile times • Currently not difficult to beat Income from cash

‘The biggest risk is not taking any risk. The only strategy that is guaranteed to fail is not taking any risks.’ Mark Zuckerberg

Conclusion •Important to have a plan •Maximise tax reliefs available •Invest for long term growth •Plan early to maximise opportunities •Need for advice never more critical

The information contained herein is based on Harvest Financial Services Limited's understanding of current Revenue practice as at May 2016 and may change in the future. The material is not intended to provide advice and is provided for general information purposes only. • Please note that the provision of certain products and services do not require licensing, authorisation, or registration with the Central Bank of Ireland and, as a result, are not covered by the Central Bank's requirements designed to protect consumers or by a statutory compensation scheme. Warnings: The value of your investment may go down as well as up. You may get back less than you invest. Past performance is not a reliable guide to future performance. If you invest in a pension product you will not have any access to your money until your retirement. These figures are estimates only. They are not a reliable guide to the future performance of these investments. Returns may be affected by changes in currency exchange rates.

Thank You

Terry Devitt

tdevitt@harvestfinancial.ie

Emer Kirk

ekirk@harvestfinancial.ie

Harvest Financial Services Limited is regulated by the Central Bank of Ireland.You can also read