WHAT ARE THE BEST NORTH AMERICAN CREDIT CARD APPS?

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

March 2017 Issue 541 www.cardsinternational.com

WHAT ARE THE BEST

NORTH AMERICAN

CREDIT CARD APPS?

The biggest FIs in the region

go head-to-head

• PRODUCTS: Prepaid in Canada

• DISTRIBUTION: ATMs at 50

• GUEST COMMENT: ACI Worldwide

• COUNTRY SURVEYS: The Philippines, Estonia & Cambodia

CI 541.indd 1 06/03/2017 17:01:43

Simple, secure and effortless digital

solutions for financial services organisations

To find out more please visit:

www.intelligentenvironments.com

@IntelEnviro

Intelligent Environments is an international provider of innovative mobile and online solutions for financial services

providers. Our mission is to enable our clients to deliver a simple, secure and effortless digital experience to their

own customers.

We do this through Interact®, our single software platform, which enables secure customer acquisition, engagement,

transactions and servicing across any mobile and online channel and device. Today these are predominantly

focused on smartphones, PCs and tablets. However Interact® will support other devices, if and when they become

mainstream.

We provide a more viable option to internally developed technology, enabling our clients with a fast route to market

whilst providing the expertise to manage the complexity of multiple channels, devices and operating systems.

Interact® is a continuously evolving technology that ensures our clients keep pace with the fast moving digital

landscape.

We are immensely proud of our achievements, in relation to our innovation, our thought leadership, our

industrywide recognition, our demonstrable product differentiation, the diversity of our client base, and the calibre of

our partners.

For many years we have been the digital heart of a diverse range of financial services providers including Atom Bank,

Generali Wealth Management, HRG, Ikano Retail Finance, Lloyds Banking Group, MotoNovo Finance, Think Money

Group and Toyota Financial Services.

IE Adverts - 2017.indd 1 21/12/2016 11:53:12

Cards International EDITOR’S LETTER

CONTENTS EDITOR’S LETTER

6 DISTRIBUTION: ATMS AT 50

According to the ATM Industry

Time for credit card issuers

Association (ATMIA), there are

approximately three million ATMs

across the globe. As the self-service

to up their mobile game

kit hits its 50th birthday, Patrick

Brusnahan writes on how the

U

financial mainstay is still developing

K customers are connected in a far more modu- ly of – but as for the rest, how

7 MOBILE: CREDIT CARD APPS

i ncreasi ng ly w i l l i ng lar and component-based way many really good credit card

Canadian and US banks generally

provide a single mobile app for to mu lt i - b a n k , a nd across organisational bounda- account apps are out there?

banking and credit card account already more than a ries. A number of major issuers do

management, and the most half (53%) take their credit Making infrastructure avail- not even offer the most basic

advanced examples also include

fraud prevention. Robin Arnfield card from an alternative to able through standardised inter- account-management features

reviews leading North American their current account provider. faces will be a major trigger for on their mobile banking apps.

issuers’ offerings, and if one single

app is the key to success

Is there scope for credit card new competition, from many Too many banks have taken

issuers to win market share by different sources. the view that they aim for one

10 NEWS: ANALYSIS sharing consumers’ financial Open Banking will give rise to front door in terms of mobile

It is not often that a conference data with third parties in return new business models, with some interaction with the consumer

speaker gets up and delivers a

slating of a host country’s ecosystem for benefits? providers choosing to specialise – one app for all products with

– but that is exactly what happened A report released by PwC, in niche areas rather than offer the credit card added on as an

in Berlin at the Merchant Payment

Ecosystems conference. Anna Milne

Who are you calling a challeng- a traditional suite of products afterthought.

reports er? How competition is improv- or attempt to manage the cus- With annual credit card-

ing customer choice and driving tomer’s end-to-end experience. switching rates in the mid-teens,

11 PRODUCTS: PREPAID IN CANADA

innovation in the UK banking In the credit card sector, how- against the current miserable

While prepaid open-loop and

closed-loop transactions are the market, states that 39% of con- ever, there is much scope for rate of 3% for current accounts,

fastest-growing POS transaction sumers would agree such a deal improvement and optimisation consumers are already more

types in Canada, they still only

account for small proportions of POS

with their financial institution. of the customer experience. The than willing to shop around.

volume and value. But the prepaid Increasingly, retail customers majority of banks do not offer A decent credit card manage-

growth opportunities are significant, are not seeking more full-service separate apps for different prod- ment app is no longer a luxury.

especially in the open-loop segment,

reports Robin Arnfield banks, but rather providers that ucts such as credit cards. Expect issuers to offer apps

specialise in specific products or As customers shift to digital including travel notifications,

14 COUNTRY SURVEY: THE PHILIPPINES

segment needs. channels, issuers will be under the option to block and unblock

16 COUNTRY SURVEY: ESTONIA As the report notes, the pressure to optimise their mobile cards, and personalised rewards.

18 COUNTRY SURVEY: CAMBODIA advent of Open Banking, ena- and online channels to increase Or how about geo-location

20 GUEST COMMENT: ACI WORLDWIDE

bled by technology and regula- conversion rates. controls, enabling cardholders

With a new fast payments ecosystem, tory developments, will be par- Speaking purely as a to say their card can only be

how open is too open? Customers ticularly influential on competi- cardholder and not an editor, used within so many miles of a

will not sacrifice convenience for tive dynamics. the Amex app is outstanding, specific location in proximity to

security, so what is the best way to

strike an effective balance between Supported by a new regula- offering personalised notifica- their smartphone?

the two without sacrificing the tory regime, the initiative means tions for payment and spending We may even see issuers offer-

values of both? ACI Worldwide’s reminders, balance updates and ing an incentive to cardholders

Silvia Mensdorff-Pouilly writes

banks will be able – and required

– to share more customer infor- statements. As a non-customer, prepared to share financial data

mation than ever before. Barclaycard and Capital One with third parties.

This will be achieved via APIs also offer standalone credit card Douglas Blakey

which enable systems to be apps that colleagues speak high- douglas.blakey@cardsinternational.com

Editor: Douglas Blakey Director of Events: Ray Giddings For more information on Verdict, visit our

Tel: +44 (0)20 7406 6523 Tel: +44 (0)20 3096 2585 website at www.verdict.couk.

Email: douglas.blakey@verdict.co.uk Email: ray.giddings@verdict.co.uk As a subscriber, you are automatically

Financial News Publishing, 2012 entitled to online access to Cards

Deputy Editor: Anna Milne Head of Subscriptions: Sharon Howley International. For more information, please

Registered in the UK No 6931627 Tel: +44 (0)20 7406 6701 Tel: +44 (0)20 3096 2636 telephone +44 (0)20 7406 6536 or email

ISSN 0956-5558 Email: anna.milne@verdict.co.uk Email: sharon.howley@verdict.co.uk customer.services@verdict.co.uk.

Unauthorised photocopying is illegal. The

Senior Reporter: Patrick Brusnahan London Office

contents of this publication, either in whole or Sales Executive: Harry Hooker

Tel: +44 (0)20 7406 6526 71-73 Carter Lane

part, may not be reproduced, stored in a data Tel: +44 (0)20 3096 2586

Email: patrick.brusnahan@verdict.co.uk London

retrieval system or transmitted by any form or Email: harry.hooker@verdict.co.uk

EC4V 5EQ

means, electronic, mechanical, photocopying, Group Publisher: Ameet Phadnis

recording or otherwise, without the prior Customer Services: Asia Office

Tel: +44 (0)20 7406 6561

permission of the publishers Tel: +44 (0) 20 3096 2636 1 Finlayson Green, #09-01

Email: ameet.phadnis@verdict.co.uk

or +44 (0)20 3096 2622 Singapore 049246

Sub-editors: Patrick Fogarty, Nick Midgley Email: briefings@verdict.co.uk Tel: +65 6383 4688

Fax: +65 6383 5433

Email: asiapacific@verdict.co.uk

www.cardsinternational.com March 2017 y 1

CI 541.indd 1 06/03/2017 17:01:53

NEWS: DIGEST Cards International

DIGITAL

Grameen America, Citi and for over 86,000 low-income female entre- women entrepreneurs through access to capi-

MasterCard to unveil digital preneurs across the US. tal, credit and asset-building services.”

finance platform Citi and MasterCard will support the The upgrades includes the disbursement of

deployment of cloud-based management reloadable MasterCard cards issued by Citi

information system infrastructure to mod- Prepaid Services. These will be used by Gra-

ernise and boost Grameen America’s opera- meen America to provide microloans to its

tional capacity. members.

Grameen America will be able to standard- MasterCard’s president of the centre

ise and modernise its back-office processes, for inclusive growth, Shamina Singh, said:

achieve better efficiency, scale services, and “Connecting people to the networks that

launch new features. power the modern world will unlock their

Grameen America president and CEO economic potential and continue a cycle of

Andrea Jung said: “Solving the need for digi- equitable economic growth and poverty

tal banking services among low-income com- reduction.

Microfinance organisation Grameen Ameri- munities in the US is a pressing priority. “Working with Grameen America, we are

ca has partnered with Citi and MasterCard “This collaboration represents a perfect glad to join a partnership that will advance

to launch a range of fintech solutions to pro- marriage of the key players in technology and economic mobility through entrepreneurship

mote digital financial access and inclusion financial services, coming together to empower in the US.”<

STRATEGY DISTRIBUTION PRODUCTS

HNB, UnionPay agree to accept Doha Bank, MasterCard to offer CIBC FirstCaribbean to issue

card payments in Sri Lanka payment solutions in Qatar contactless cards

Hatton National Bank (HNB), a Sri Lankan Doha Bank and MasterCard have signed a CIBC FirstCaribbean International

lender, has teamed up with UnionPay Inter- long-term agreement to launch a range of Bank has decided to issue chip-and-PIN

national to accept card payments. payment solutions, including remittance contactless debit and credit cards for its Visa

The contract will enable Sri Lankan mer- offerings and contactless payments, in Qatar. cardholders.

chants which use HNB’s POS devices to According to Doha Bank, the agreement CIBC FirstCaribbean’s MD of customer

accept UnionPay cards. will enable both partners to provide innova- relationship management and strategy, Tre-

HNB senior manager of card centre tive products to the country’s workforce. vor Torzsas, believes the development is a

Roshantha Jayatunge commented: “By The new initiative backs efforts by the ‘significant milestone’ as it increases ease of

moving proactively to partner with Union- Ministry of Labour and Social Affairs, and use for small purchases while maintaining

Pay International, we believe HNB has taken Qatar Central Banks to provide a safe work- security.

a vital first step towards further integrating ing environment for workers, while ensuring Torzsas said: “We’ve introduced a series

Sri Lanka into the international economic wages are electronically transferred to their of innovations to our services, including our

system.” bank accounts. very popular Mobile Banking app, to give

UnionPay International senior head of Commenting on the agreement, Doha our clients more choice in how they bank

South Asia Derek Chang said: “We are Bank group CEO Raghavan Seetharaman and make payments. The app is performing

delighted to be partnering with HNB. Sri said: “Our partnership serves to bring the beyond our expectations.

Lanka is an important market for UnionPay best card products to our growing customer “We now have a banking solution to fit

International in South Asia. base and is in line with Doha Bank’s strat- everyone’s lifestyle, and our smart cards will

“We are uniquely positioned and ready egy to deliver the utmost value to employ- provide our cardholders additional com-

to contribute to the growth of the tour- ers and payroll customers within the entire fort that they can make payments in a safe,

ism industry by providing travellers with a framework of the Wages Protection System secure, yet flexible manner. Security is para-

secure and easy payment option.”< implementation.”< mount to our client base.”<

DIGITAL

Vibe, WEX sign virtual payments

agreement which allows automated supplier payments

in 24 currencies worldwide.

US-based payment technology firm WEX WEX Europe commercial director for vir-

has signed an agreement with Vibe Systems tual payments Ian Johnson said: “Our aim is

to combine travel technology and payments to make our payment solutions available to

for a better supplier payment experience. the travel industry, regardless of the systems

Vibe provides advanced front- and mid- they already use.”

office technology to travel businesses, includ- Vibe group e-commerce director Martin

ing online travel agencies, retail agencies, Eade said: “We are delighted to offer our cli-

travel management companies and consoli- ents the ability to enable WEX payment solu-

dators. tions on their Vibe online booking platform.

WEX’s virtual debit, prepaid and credit “Combining WEX’s payment expertise

cards will be directly integrated with either with Vibe’s technology is an exciting pros-

pre- or credit funding into the Vibe platform, pect and one we are excited to continue.”<

2 y March 2017 www. cardsinternational.com

CI 541.indd 2 06/03/2017 17:01:54

Cards International NEWS: DIGEST

RESEARCH

Visa launches new innovation through which Visa aims to ‘excite and create new, secure ways to pay’.

centre in London engage visitors’, including applications relat- Visa executive vice-president for innova-

ed to the Internet of Things in connected car tion and strategic partnerships Jim McCarthy

Visa has opened a new innovation centre in and home environments. said: “What makes the approach we take in

London, where the company will work with According to Visa: “Visitors will experi- our innovation centres unique is that they’re

financial institutions, merchants and other ence the future of retail using virtual reality all about collaborating with clients to solve

partners to develop the next generation of to pick just the right seat for an upcoming real-world consumer pain points or business

payment solutions. Formula E race and biometric authentication problems using digital solutions.”

The 1,000m2 facility is located at Visa’s to pay for tickets.” The new facility joins a global network

European headquarters in Paddington Basin. Coinciding with the opening of the cen- of innovation centres and studios located in

It is described as the largest of Visa’s global tre, Visa announced that fintech develop- technology hotspots, including Berlin, Dubai,

network of innovation centres. ers across Europe will now be able to take Miami, San Francisco, Singapore, São Paulo

It features practical demonstrations advantage of the Visa Developer Platform ‘to and Tel Aviv. <

MOBILE

UnionPay launches mobile

QuickPass in Hong Kong

UnionPay International has debuted Union-

Pay mobile QuickPass products in Hong

Kong, in collaboration with Bank of China

(Hong Kong).

The move follows the issuance of Union-

Pay HCE mobile QuickPass products in

Macau and South Korea. Cardholders can

now link mobile phones with UnionPay

dual-currency credit cards issued by Bank

of China to make daily transactions by

mobile phone. phone, wearable devices and UnionPay chip 20,000 POS terminals in Hong Kong by mer-

UnionPay said its mobile QuickPass facil- cards, as well as online mobile payments. chants such as Sogo, 7-Eleven, Mannings,

ity supports offline payments with smart- Mobile QuickPass is currently accepted at and Tsui Wah Restaurant. <

STRATEGY

Barclaycard, TMC sign fuel card The new programme integrates a fuel with Centrica, providing a fuel programme

agreement with Centrica expenses Barclaycard with accurate, audited that will not only be simpler for their drivers

mileage and comprehensive manage- and fleet managers but will also help the

Barclaycard Commercial Payments has ment information. business reduce its fuel costs.

secured a contract from Centrica – the par- In association with TMC, the “Securing this contract really

ent company of British Gas – to offer a single Barclaycard Fuel+ features chip & demonstrates the value of the

fuel card programme for its van and car fleets PIN security and Visa acceptance, Barclaycard Fuel+ in association

in collaboration with TMC, allowing Centrica drivers to refuel with TMC proposition for larger

The contract, which was awarded after a at virtually any petrol forecourt in fleets.”

competitive tender process, runs for three the UK. Centrica head of fleet Steve Winter

years, providing Centrica with a single fuel Barclaycard head of multinational said: “Barclaycard Fuel+ in association

programme for both its commercial and corporate business Michael Pechner com- with TMC is an exciting opportunity to take

company car fleets. mented: “We are delighted to be working our fuel programme to the next level.”<

STRATEGY

JCB becomes principal member versal card payment standards through new payment networks utilising SEPA-compliant

of nexo Standards protocols and the implementation of speci- terminals.

fications with integrated retail and terminal It also delivers a one-stop-shop for EMV

JCB International, a subsidiary of Japan- management systems. and SEPA -compliant terminal testing,

headquartered JCB, has become a princi- As a principal member, JCB will confirm decreasing the risk of interoperability obsta-

pal member of nexo Standards in its card that its technical requirements are supported cles emerging between payment applications,

schemes category. by nexo protocols, with a particular focus on and thereby promoting an open market for

Headquartered in Brussels, nexo Standards the nexo-Fast suite of specifications. EMV and SEPA terminals.

is the open standards association dedicated The specifications offer a clear description The move means that payment acceptors,

to the creation of implementation specifica- of the application on an EMV chip-and-PIN processors, payment service providers and

tions for card payment acceptance. payment terminal which provides compli- vendors will now be able to implement JCB

It works on behalf of all card stakeholders ance with the European Payments Council's contact and contactless transaction kernels

to harmonise payment acceptance. The asso- SEPA cards framework. nexo-FAST allows into their EMV and SEPA compliant termi-

ciation is developing a new generation of uni- a uniform transaction user experience on all nals, as specified by nexo-Fast. <

www.cardsinternational.com March 2017 y 3

CI 541.indd 3 06/03/2017 17:02:05

NEWS: DIGEST Cards International

REGULATION

Allpay’s cards pass Visa’s ment of the cards, access control, HR train- The original building will be modernised to

physical audit ing, credit and police checks. incorporate a larger manufacturing layout.

The audit follows a £1m ($1.2m) Hologram, chip embedding and card

UK-based payment specialist investment into the UK payment -inspection machinery will enable Allpay to

Allpay has passed the annual specialist’s design and produc- create custom-designed cards for clients.

physical audit of its card- tion facilities. New hires include a production planner

manufacturing bureau car- With the investment, Allpay and stock controller, a manufacturing and

ried out by Visa towards the obtained a new building, the bureau operation manager, and a new direc-

end of 2016. latest equipment, and expand- tor, Ceri Davies.

Against the highest stand- ed its card manufacturing Allpay head of card manufacturing and

ards of PCI Compliance, the team from 24 to 49 staff over a bureau operations Jamie Taylor said: “We

annual physical audit assessed 12-month period. are delighted with the near-perfect score

various security factors with regards Currently, the bureau facility is awarded to our card-manufacturing bureau,

to the building, physical control and move- operating from a new purpose-built building. following its annual physical audit.”<

MOBILE

MasterCard to empower MasterCard aims to foster a higher level of checkout with a smartphone, or by entering

150,000 Kenyan merchants with inclusion for MSMEs in East Africa through a merchant identifier code.

MasterPass QR the digital payment initiative. MasterCard division president for Sub-

The regional commitment to impact over Saharan Africa, and head of financial inclu-

MasterCard has committed to provide its 150,000 MSMEs in Kenya is part of Master- sion for international markets Daniel Mone-

MasterPass QR secure digital payment solu- Card’s global goal of connecting 40 million hin said: “Kenyans are entrepreneurial by

tion to more than 150,000 micro, small and micro and small merchants to its electronic nature and there are incredibly exciting busi-

medium-sized enterprises (MSMEs) in Kenya payment network by the end of 2020 – a ness ideas coming from the region.

during 2017. goal that MasterCard hopes it will be able to “We want to help business owners to grow

The mobile-driven person-to-merchant achieve before that date. and prosper by delivering solutions that meet

(P2M) payment solution will be launched Consumers can pay for in-store purchas- their needs. To this end we feel that Master-

through numerous financial institutions. es by scanning a QR code displayed at the Card’s commitment is a valuable one.”<

STRATEGY SECURITY SECURITY

Visa partners with IBM for POS MePIN launches biometric Santander UK enables payments

solution extensions to curb online fraud through voice command

Visa has collaborated with tech giant IBM Finland-based MePIN/Meontrust has intro- Santander UK has launched a feature on its

to incorporate POS solutions and commerce duced additional biometric authentication mobile app to allow users to authorise pay-

into any device, including watches and rings, options to its MePIN Universal Authentica- ments using voice commands.

using IBM’s Watson Internet of Things (IoT) tion platform. As well as enabling fund transfers, the new

platform. The new Human Recognition and User voice-recognition technology will also allow

Through the platform, businesses will Recognition authentication policies can be users to check balances, and report lost or

be able to connect to billions of connected used alongside traditional authentication stolen cards.

devices, sensors and systems wherever Visa methods. The technology is currently in the process

is accepted. The solution is currently used by The provider claims the new policies of being piloted on the iOS version of the

more than 6,000 IBM clients. extend the existing MePIN Public Key Infra- bank’s SmartBank app.

The partnership will allow companies to structure-based non-repudiation without Santander’s head of technology inno-

incorporate secure payments into various affecting the user experience. vation, Ed Metzger, said: “The worlds of

product lines using the Visa Token Service, MePIN/Meontrust CEO Markku Mehtala technology and banking continue to evolve

a technology that replaces sensitive account told Cards International: “Card-not-present at pace, working hand in hand to deliver a

information found on payment cards with a fraud has not been solved with clumsy friction-free user experience.

unique digital identifier. authentication solutions. “We are excited to be the first UK high

IBM Watson IoT general manager Har- “MePIN provides non-repudiation for street bank to enable customers to make

riet Green said: “IoT is literally changing transactions while minimising the friction of payments using just their voice, offering

the world around us, whether it’s allowing authentication. them another channel of choice in how they

businesses to achieve unimaginable levels of “It is important that consumer privacy is wish to bank.

efficiency or enabling a washing machine to not forgotten. Face recognition must be used “Appetite for simple, intuitive banking

ensure we never run out of detergent. wisely,” Mehtala continued. solutions has grown,” Metzger continued.

“This combination of IBM’s IoT technol- Available as a software development kit, “This pioneering technology has huge

ogies with Visa payment services signifies the MePIN biometric solution can be inte- potential to become an integral part of the

the next defining moment in commerce, by grated by the payment card issuers or pay- future banking experience, playing a trans-

allowing payments on any connected object ment service providers into mobile apps, or formational role in the industry and redefin-

with new levels of simplicity and conveni- used as a template to launch new payment ing how customers choose to manage their

ence,” Green added. < security apps.< money.”<

4 y March 2017 www. cardsinternational.com

CI 541.indd 4 06/03/2017 17:02:06

Cards International NEWS: DIGEST

DIGITAL PRODUCTS MOBILE

Billtrust unveils Virtual Card Yes Bank launches NFC-enabled MTS introduces new mobile

Capture for automated virtual debit cards for contactless wallet to integrate payment

credit card acceptance payments solutions

India’s Yes Bank has launched its latest range Russia-based Mobile TeleSystems (MTS) has

of NFC-enabled debit cards. launched its latest mobile wallet with ‘easy

Yes Prosperity and Yes First have, accord- one-click access’ to its financial services.

ing to the bank, been ‘designed around the The MTS Money Wallet combines all pay-

specific needs of debit card customers’. ment tools on a single platform, and custom-

The Yes Prosperity card range features ers have the option to make payments and

Payment cycle management firm Billtrust the Yes Prosperity Titanium, Titanium Plus, transfer money from the e-wallet by smart-

has launched the Virtual Card Capture ser- Platinum and Rupay Platinum debit cards, phone.

vice to improve efficiency and automate the whereas the Yes First range comprises the All MTS Money Wallet users will be auto-

cash application process for email credit Yes First World debit card. matically enrolled onto the MTS Bonus

card payments. The bank has also introduced two cards programme, which offers loyalty points and

The solution claims to address a grow- on India’s domestic card payment network, access to exclusive offers and discounts.

ing problem for account departments that Rupay. MTS vice-president for strategy and mar-

receive payments by email using virtual Cardholders can earn reward points on keting Vasyl Latsanych said: “Today we

credit cards from buyers. These are not only all expenditure, and benefit from access to are entering into a new era of mobile and

costly to manage, but also create a burden Yes InControl, which it operates through financial services. We created the unified

for organisations with limited resources. MasterCard, allowing users to set custom- ecosystem, which will become a convenient,

Payment instructions sent by banks and ised spending limits for different locations transparent, and secure alternative for cash

accounts payable platforms are rerouted to and categories. and bank cards.

Billtrust for processing through Virtual Card Yes Bank senior group president for retail “The initial functions included in the ser-

Capture. and business banking Pralay Modal said: vice only mark the beginning of our journey.

Funds are deposited into a supplier’s bank “Our debit card portfolio has been designed We will combine all possible payment solu-

the following business day, and remittances to offer superior features and benefits to our tions with leading loyalty programmes.

are consolidated for all payment sources and valued customers. “We believe that cash and cards will

matched to open invoices. “The launch will augment our efforts become redundant in the near future. All

The new solution claims to reduce the towards encouraging customers to move we’ll need for comfortable communications

burden of acceptance of virtual credit cards, towards a cashless economy. Digitalistion is and financial management is a smartphone.

which was previously a manual process. < the future, but cards are the present.” < We want to give people the future today.” <

DISTRIBUTION

Barclaycard signs new payments million contactless transactions to date – in 10 pay-as-you-go journeys on London’s

agreement with TfL covering journeys made by bus, Tube, tram, buses, Tube and rail services.

Docklands Light Railway, London Over- Commenting on the extension, TfL chief

Barclaycard has extended its contract to offer ground, TfL Rail, Emirates Air Lines, River technology officer Shashi Verma said:

contactless payment solutions to Transport Bus and most of London’s daily National “Contactless payments have completely

for London (TfL) for another seven years, Rail services. transformed the way people pay for travel

with the option to extend the agreement for The contract extension will enable in London, with more than 800 million jour-

a further three years. Barclaycard to support the introduction of neys already made and around 1.8 million

TfL and Barclaycard have been working the new Elizabeth line, while assisting the journeys being made every day.

together for more than 20 years and have launch of contactless payments for train “This new 10-year contract will help

transformed how users pay for travel across travel beyond London. ensure these numbers continue to grow while

the UK’s capital. As TfL’s merchant acquirer, According to Barclaycard, contactless also providing support to allow us to develop

Barclaycard has processed more than 278 transactions currently represent almost four our ticketing system.”<

MOBILE

BharatQR payments launched in issuing cards and establishing expensive POS

India terminals and infrastructure’.

Customers of any bank can use a smart-

BharatQR, a common quick response (QR) phone to make payments through the app by

code that allows consumers with debit or scanning the relevant QR code at the POS

credit cards to pay directly from a phone by and entering the transaction amount.

scanning a QR code, has been launched in Once authorised, the amount is transferred

India. directly from the customer’s account to the

The new payment system was developed merchant’s account.

by MasterCard, Visa, American Express and Leading Indian financial institutions,

the National Payment Corporation of India, BharatQR aims to reduce the country’s including Axis Bank, Bank of Baroda, Bank

which is responsible for operating the RuPay dependency on cards, with a goal of help- of India and HDFC Bank, all currently sup-

card network. ing to ‘disrupt the card network’s business of port the new app. <

www.cardsinternational.com March 2017 y 5

CI 541.indd 5 06/03/2017 17:02:06

DISTRIBUTION: ATMS AT 50 Cards International

Fifty years on, the ATM is still developing

Inaugurated by comedy actor Reg Varney in 1967, the ATM is still with us; according to the ATM Industry

Association (ATMIA), there are approximately three million ATMs currently in operation across the world.

However, one of the mainstays of modern banking is not resting on its laurels. Patrick Brusnahan writes

L

aunched by Barclays in its Enfield

Town branch, the automated tell-

er machine (ATM) has gone from

st reng th to st reng t h. From si m-

ple withdrawals to deposits to security

checks, features are constantly added

to the service. Some say the right ATM

could even replace a branch.

NCR has launched the SelfServ 80 Series of

ATMs which are set to do just that. Accord-

ing to the firm, it will ‘redefine the banking

experience and change the way consumers

interact with the ATM forever’. Hefty claims.

Rachel Nash, director for financial services

at NCR, tells CI: “The new 80 Series fam-

ily is really quite groundbreaking in terms of

how we can deliver services to consumers.

Just from an aesthetic feel, it’s very modern

and tablet-like, not your typical old grey

box, which really does fit into what custom-

ers expect from a digital experience and how

they want to interact and transact with every

organisation.”

Video banking

Features of the new hardware include an

advanced 19-inch multi-touch display and be very convenient for people to pop into a started to interact in that space has changed

built-in video banking. This will be crucial if branch, even when one isn’t there. how they wanted to interact in our space. It’s

the ATM is to replace branches, as research “In some cases, absolutely, if they want another digital touchpoint,” Nash continues.

from NCR states that 80% of the transac- to go to a full-service branch, they should. One of the biggest lessons we learned is

tions completed inside a physical branch We’re not saying one solution fits everything, that the change in mainstream consumer

would be a more complete experience if a we’re just providing a flexible platform that technology is impacting the solutions we

live video teller had a presence at an ATM. allows different types of format and deploy- deliver to market.”<

“What we’re really trying to think about is ment to suit the customers’ needs.”

how we can reposition self-service as part of Is the ATM takeover imminent? Not as

the whole experience. You may have a cus- soon as one might think, as there are issues Extreme locations

tomer that is perfectly happy to serve them- with wide-scale deployment. “We do have a

selves and interact in a 100% self-service lot of legacy across the globe. An organisa- As part its celebration of the 50th

way, and this enables that,” Nash explains. tion is not going to replace everything over- anniversary of the ATM, the ATMIA collated

“But there may be a time they might need night; it is going to be gradual,” notes Nash. some of the most extreme ATM locations:

local and in-person assistance, which is part So how has the ATM changed in the last

• The Antarctic ATM is located inside the

of the tablet banking solution, to alert a 50 years? Nash concludes: “Things that we

McMurdo Station near the South Pole.

member of staff to their call for remote assis- have tried in the past, such as video bank-

tance. These aren’t bolt-ons as they have ing, were cumbersome, clunky and difficult • A desert ATM in the Australian Outback

been in the past. It has helped streamline the to implement. is accessible only via Aboriginal

way staff members help customers.” “Now, advancements in technology mean tracks. On average it completes 500

withdrawals and 200 balance inquiries

One problem with an ATM replacing a we can incorporate mainstream technology

each month.

branch is that if customers want branch ser- across all platforms.

vices, they would surely visit a branch. Nash “The other thing we’ve seen is that none • An ATM in Sust, Pakistan is located

says: “I can see a branch-in-a-box-type envi- of us ever envisioned the idea of an iPhone, 2,375m above sea level, in sub-zero

ronment working in a retail outlet. It would a touchscreen in your hand. How customers conditions. <

6 y March 2017 www. cardsinternational.com

CI 541.indd 6 06/03/2017 17:02:08

Cards International MOBILE: CREDIT CARD APPS

Which North American credit card app

would make it onto your homepage?

Canadian and US banks generally provide a single mobile app for banking and credit card account

management, and the most advanced examples also include fraud prevention. Robin Arnfield reviews

leading North American issuers’ offerings, and their key features and innovations

“W

hen the mobile channel was Mobile card applications ware vendors have yet to catch on to includ-

first introduced, there was In her Aite Group report, US Credit Card ing card controls in their apps.”

a lot of d iscussion a mong Issuers’ Digital Account-Opening Processes, However, Malauzai has offered credit and

North American banks about Montez says most US credit card issuers have debit card control functionality within its

whether they should have standalone the basic foundational capability to accept mobile banking app for the last four years.

apps for different products,” says Tiffani online credit card applications, collecting the “The first generation of card control soft-

Montez, senior analyst at US-based Aite data required for the application, verifying ware just integrated with a bank’s core bank-

Group. applicants’ identity, and presenting disclo- ing system,” says Gaynor.

“Those credit card issuers that also have sures, and ensuring applicants qualify for a “Our software now offers integration with

other banking products primarily want one specific card. the card networks and processors for more

front door in terms of the mobile interaction “Aite Group’s assessment of the mobile effective controls. We find that around 15%

with the consumer. application shows the overall immaturity of of our clients’ active mobile bankers go in to

“Consequently, most US banks and credit the account-opening process,” Montez out- the card control module at some point each

unions don’t have separate apps for different lines in her report. month.”

products such as credit cards, mortgages or “Most mobile application experiences mir- Gaynor says Malauzai’s US banking and

chequeing accounts,” Montez continues. ror online application experience and, at this credit union clients are not using his firm’s

“It’s just one mobile app with access to all point, use few of the phone’s native features mobile banking and card control app yet for

accounts, depending on the type of relation- to optimise the experience.” credit cards. “Half of our 450 clients have

ship a customer has with that financial insti- Montez believes that, over the next rolled out debit card controls using our app,”

tution. few years, as customers increasingly shift he notes. “But it can definitely be used for

“Generally, the apps let cardholders obtain towards digital channels from branches and credit card controls.

balance information, make bill payments, see call centres, credit card issuers will be under “A useful feature which we offer is geo-

purchase information, view rewards, and pressure to optimise their mobile and online location controls, which allow cardholders

track spending. Some issuers, such as Capital channels to increase conversion rates. to say that their card can only be used within

One, have apps that allow you to view your a 10-mile radius of a particular location.

credit score.” Card fraud prevention apps Customers can also use our GPS control to

Montez expects issuers to increasingly Visa, MasterCard and major US card proces- specify that their card has to be used in prox-

offer more mobile-first credit card account- sors such as Vantiv offer standalone credit imity to their smartphone.

management features in their apps, instead and debit card control apps for issuers to “But we don’t see much uptake of that as

of just replicating features provided in their provide to their customers to prevent fraud. it’s heavy on phone batteries. Our most heav-

online services, given that customers always A key provider of card control software to ily used control feature is turning a card off

have their smartphone with them. the processors is US-based Ondot Systems. when it isn’t in use to prevent fraud.”

“For example, they are starting to intro- “Hundreds of US financial institutions are Gaynor notes that none of his firm’s cli-

duce the ability for cardholders to provide rolling out these standalone apps to their ents have asked them to provide a standalone

travel notifications, receive spending alerts, cardholders,” says Robb Gaynor, chief prod- app for card controls.

set spending thresholds, freeze and unfreeze uct officer at US-based mobile banking app “There’s a big question mark as to whether

cards, and report lost or stolen cards via vendor Malauzai Software. “The reason for standalone card controls make sense and as

mobile,” she says. this is that many of the mobile banking soft- to whether consumers will want a separate

www.cardsinternational.com March 2017 y 7

CI 541.indd 7 06/03/2017 17:02:10

MOBILE: CREDIT CARDS APPS Cards International

app for controlling their cards’ usage,” he

says. “Standalone is a strategy the banks and

credit unions are forced to pursue because

mobile banking vendors are behind. The

standalone phenomenon will be short-lived

as mobile banking vendors will build the nec-

essary card controls into their apps.”

Market research data

According to Lynda Lovett and Mary-

Anne Huestis of Canadian financial market

research firm MarketSense, 52% of Cana-

dian credit cardholders have downloaded

a mobile banking app, up five percentage

points from a year ago.

“Incidence is highest for TD with 12% of

cardholders, and Royal Bank of Canada

(11%), followed by CIBC (8%), ‘any credit

union’ (7%), BMO Bank of Montreal (7%),

Scotiabank (7%), Desjardins Group (7%),

and Scotiabank’s direct banking subsidiary:

Tangerine (7%).”

According to MarketSense, 48% of Cana-

dian survey respondents are interested in

❙❙Citi’s dispute-resolution feature: step one

using smartphones to redeem rewards, and

32% to book travel. “Both measures are sta-

ble over last year,” Lovett and Huestis say. customers when they are spending more, the free Fico [Fair Isaac Co.] scores and intro-

A survey of 3,000 US adults in June 2016 same, or less than usual. duced the ability to manage card rewards on

for Mercator Advisory Group’s US Con- Desjardins offers the InstaBalance feature mobile.”

sumers and Credit: Young Adults Return to which lets credit cardholders view balances BankAmeriDeals offers up to 15%

Credit Card Use report found that 47% of without having to log into the Quebec-based cashback when customers make purchases at

US smartphone and tablet owners indicated cooperative financial institution’s AccèsD selected retailers with BofA debit and credit

interest in mobile-enabled credit card fraud- mobile banking app. InstaBalance provides cards.

prevention controls, up from 44% in 2015 budget information such as maximum and

and 41% in 2014. Interest was highest in the minimum account limits and goals in graphi- Capital One Canada

25-34 age group, with 67% in this segment cal form. “Our team of over 80 Toronto-based soft-

indicating interest in 2016. ware studio associates aims to open up new

“We asked smartphone and tablet owners American Express Canada digital possibilities for customers to man-

if they would be interested in a new mobile “American Express Canada is focused on age their accounts,” a Capital One Canada

app from their issuer enabling them to con- reaching its mobile-first customers via the spokesperson says.

trol how and when their credit cards can be Amex App,” an Amex Canada spokesper- “Via our mobile banking app for iOS and

used, either to limit spending or avoid fraud, son tells CI. Android smartphones, Capital One Canada

by setting limits by dollar amount, location “In September 2016, we launched Use customers can view their credit card transac-

of the phone, or shopping category, that Points for Purchases, which lets cardmembers tions, check their balance and available cred-

can be turned on and off in real time,” says redeem points towards purchases made on it, see payment due dates and minimum pay-

Karen Augustine, Mercator’s manager, pri- an eligible American Express card via the ment required, view their credit card rewards,

mary data services. Amex Mobile App.” and contact customer service within the app.”

The Amex App offers personalised notifi- Capital One Canada’s mobile app recently

PFM tools cations for payment and spending reminders, added push notifications sending real-time

Several issuers provide credit cardholders such as payment due, balance updates and alerts to customers’ phones providing details

with personal financial management (PFM) statement ready. such as transaction amount and merchant;

tools to help with budgeting. and multi-factor authentication for security

CIBC offers the Personal Spend Manager Bank of America (BofA) verification.

tool which lets credit cardholders monitor “Credit card account management is built The app offers Live Chat and Second Look,

spending, set budgets and create alerts. Cur- into BofA’s mobile banking app,” a BofA which sends an automatic email alert when

rently, CIBC’s Personal Spend Manager is spokesperson says. a potential mistake is identified on a custom-

only available to online banking users. “Our newest feature is a spending and er’s account, such as a duplicate charge.

TD offers the TD MySpend app for its budgeting tool that tracks spending on cus-

bank account and credit card holders, which tomers’ BofA deposit accounts and cards, Citi

is based on PFM software from US-based fin- and helps them create budgets. In 2016, Citi launched 86 digital features in

tech Moven. TD’s MySpend offers real-time We recently enhanced our BankAmeri- the Citi mobile banking app, including Quick

notifications and virtual receipts and uses Deals program to show deals based on the Lock, which enables cardholders to lock and

red, yellow and green traffic lights to warn customer’s location. Last year, we rolled out unlock cards, file a dispute in-app, and track

8 y March 2017 www. cardsinternational.com

CI 541.indd 8 06/03/2017 17:02:11Cards International MOBILE: CREDIT CARD APPS

a replacement card. “As a result, in 2016

alone, North America mobile app custom-

ers grew by 50% and mobile app downloads

doubled,” a Citi spokesperson says. “We saw

over 3.25 million downloads in 2016.”

“Our ultimate goal is enabling the entire

customer experience – including everything

that a customer can do right now by phone

or in the branch – in mobile,” Alice Milligan,

chief customer and digital experience officer

for Citi Global Cards and Consumer Services,

tells CI.

Since January 2017, US Citi customers

have been able to scan their credit cards

using their mobile device’s camera in the

Citi Mobile App, instead of having to manu-

ally enter their 16-digit card number for

activation. Citi says it is the only major US

credit card issuer to offer the ability to scan

embossed and non-embossed credit cards

within a mobile app.

Other features offered by the Citi Mobile

App include the managing of replacement

cards, Fico scores, redeeming rewards, tem-

porarily locking and unlocking accounts,

and setting up alerts.

National Bank of Canada

“All credit card account management features

are offered in our mobile banking app, which

people who only have a credit card with us

can also use,” says Joel Pomerleau, National

Bank of Canada’s senior manager of digital

channel support and transformation.

“There’s no standalone credit card account-

management app. Features offered include

balance, transaction history, the ability to

off pay card balance, set transaction limits,

advise the bank when one is going abroad,

❙❙Citi’s dispute-resolution feature: step two

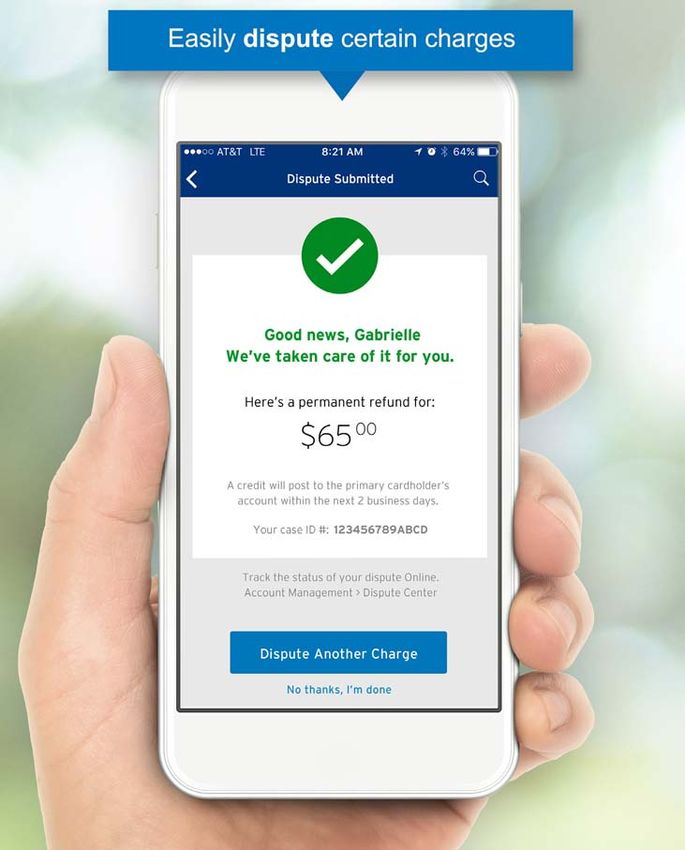

cash in points, cashback and loyalty points

balance. “Credit card accounts are much easier to ers to turn travel alerts on and off, and man-

“We don’t yet offer the ability to alert the open on mobile, while investment products age default cards for payments.”

bank via the mobile app if the card is com- are much harder.”

promised – we’re working on this.” Wells Fargo

Instead of developing a proprietary mobile RBC “In 2016, Wells Fargo redesigned its mobile

wallet, National Bank, Canada’s sixth-larg- RBC currently does not offer credit card app, which provides banking services to

est bank, plans to support the wallets offered account management features within its 19.6 million active customers, to be simpler

by the ‘Pays’, such as Apple Pay, says Pomer- mobile banking app or RBC Wallet. and more intuitive for customers, while

leau. “We’ll include a deep link within our “This is clearly an important capability that providing more content and features that

mobile app to these mobile wallets. we’re looking at developing to ensure we’re are better aligned to a customer’s needs,” a

“We’ve seen quite a lot of usage of our delivering to meet our clients’ expectations,” Wells Fargo spokesperson says.

mobile app by our credit cardholders,” an RBC spokesperson says. The app offers credit cardholders features

Pomerleau continues. The RBC Wallet is primarily a payment such as the ability to manage alerts for pur-

“There’s been a shift from online and call vehicle for RBC credit and debit cards, but chase amounts, decline transactions and

centre transactions to mobile, which is our allows cardholders to view their balance, report any suspicious card activity. It also

strongest growing channel now by far.” available credit, and RBC Rewards Point bal- lets users know when they are approaching

Pomerleau says National Bank is working ances. RBC offers a standalone app where their credit limit.

heavily on product origination across all its cardholders can redeem reward points. Cardholders can view spending reports

digital channels, without specifying which aggregated across multiple accounts, includ-

types of product. Scotiabank ing credit card, debit card and chequeing

“You can already apply online and via “We have a robust mobile banking app, which accounts. They can also access Wells Fargo’s

mobile for a bank account and credit card includes My Mobile Wallet,” a Scotiabank Go Far Rewards programme, and view their

with us,” he says. spokesperson explains. “It enables custom- credit score from the app. <

www.cardsinternational.com March 2017 y 9

CI 541.indd 9 06/03/2017 17:02:13NEWS: ANALYSIS Cards International

EPC chairman bashes Germany’s payments scene

It is not often that a conference speaker gets up and, off the cuff, delivers a single-handed slating of a host

country’s ecosystem that everyone would usually be there to promote – but that is exactly what happened

in Berlin at the Merchant Payment Ecosystems conference. Anna Milne reports

S

uch was the dire experience of Javi- accepted”; and the other three, Visa and less” POS system and German airport cabs

er Santamaría Navarrete, chair of MasterCard, “were not legible”. that do not take cards. Those that do, often

the European Payments Council “After half an hour of trying to pay for charge for the so-called privilege, accord-

(EPC), trying to buy a ticket on the a €3.40 ticket, I had to rush for the train,” ing to Sheri Brandon, Head of Transaction

Deutsche Bahn upon arrival in Berlin for whereupon he was promptly issued a pen- Banking at Tieto. Having been asked to pay

the Merchant Payment Ecosystems con- alty charge, which, of course, he had to pay a €1.10 charge to use a card for a €9 cab

ference, that he issued a dressing down of in cash. journey, she reached for her cash purse.

the highest order. Even in the words of the Emerging Pay-

For the hosts: embarrassing. And it was Money where your mouth is ments Association in a recent report on ideal

not the first reference to the fact that Ger- The EPC says it is committed to safe, reliable, European bases for fintechs, Germany was

many lags behind the rest of Europe in terms efficient, convenient, economically balanced seen as resistant to change.

of electronic payments. and sustainable payments, but some were not “Germany has built an impressive reputa-

For Navarrete, who freely shared that he convinced. tion for being antagonistic to the innovative

travels with several cards to avoid a scenario “Yesterday was not safe, not reliable, not European payments sector.

whereby one or more may not be accepted, efficient, not convenient, not economically “In nearly every aspect of interpretation of

the situation clearly warranted a rant. balanced and not sustainable,” Navarrete the key EU laws in this sector, Germany has

Despite several machines at the train sta- quipped. often excelled at taking the narrowest inter-

tion, he could not use cash because each “After this experience, the myths I had pretation.”

one accepted exact cash only. Handy when about Germany being developed have been If the world is going to be cashless by 2040,

you’ve just arrived in a country. obliterated,” he continued. Ouch. Germany looks like it might lag behind.

Of Navarrete’s seven cards, two are Dave Birch had kicked off proceedings in But, in the interests of balance, they’re

Amex, “so, no use”; two are debit, “so, not the morning with a rant against BA’s “point- alright at football, aren’t they?<

Don’t have online account details?

You and your associates may be entitled to online

login credentials. The benefits of full online

access are as follows:

• Timely daily news updates

• Access the latest analysis

• Monthly editions sent directly to your inbox

• News alerts direct to your inbox

• Comments from key industry influencers and leaders

• Search for specific, relevant content

www.

• Access the archive

To create or activate your account please contact:

customer.services@timetric.com

www.privatebankerinternational.com

CI 541.indd 10 06/03/2017 17:02:19

Digital touch briefings ad copy - MF 18042016.indd 1 18/04/2016 11:15:29Cards International PRODUCTS: PREPAID IN CANADA

Canadian open-loop prepaid

market open to growth

While prepaid open-loop and closed-loop transactions are the fastest-growing POS transaction types in

Canada, they still only account for small proportions of POS volume and value. Despite this, the prepaid

growth opportunities are significant, especially in the open-loop segment, reports Robin Arnfield

A

2016 report from Mercator based • The average load onto all categories responsible for running the country’s core

on a survey of issuers and pro- of corporate-funded prepaid card was payments infrastructure.

g ra m m e m a n a ger s c ondu c t e d C$125, and

with the Canadian Prepaid Pro- Corporate prepaid and GPR

viders Organisation (CPPO) estimates • The average load onto corporate-fund- Peoples is seeing the most growth in corpo-

that C$3.1bn ($2.37bn) was loaded onto ed cards used for consumer and employ- rate prepaid issuance, says Read.

Canadian Amex-, MasterCard- or Visa- ee/partner incentives was C$110. “This can be corporations giving pre-

? branded prepaid cards in 2015.

“The Canadian open-loop prepaid market Growth opportunities

paid cards to consumers as rewards for

buying one of their products, incentives, or

has eight active segments, compared to 17 in “My view is that there’s room for growth in corporate prepaid cards that are used for

the US, showing significant growth oppor- the Canadian prepaid card market,” says Peter B2B [business-to-business] activities such

tunity for Canadian prepaid programmes,” Read, president of Vancouver-based prepaid as receivables payments, purchasing/pro-

the report says. The Canadian market is card issuer Peoples Card Services. curement, payroll or controlling employee

expected to follow US trends, where open- “Excluding US government prepaid cards expenses,” he says.

loop prepaid cards are the fastest-growing the US open-loop prepaid card market is “There’s a lot of room for corporate B2B

form of electronic payment.” running at around $200bn a year in loads. prepaid cards to grow. There has always been

The Mercator study revealed that: Assuming that Canada is about 10% of a lot of business for corporate B2C [busi-

the US market, we should be seeing around ness-to-consumer] prepaid incentive cards,

• General-purpose reloadable (GPR) $20bn a year in prepaid loads, but we’re and this particular segment will continue to

card loads totalled C$1.84bn in 2015, nowhere near there yet.” grow. Another important segment in Canada

with the average load per card being According to Payments Canada’s 2016 is GPR prepaid cards.”

C$2,016; Canadian Payment Methods and Trends

Report, prepaid open- and closed-loop trans-

• Total loads onto open-loop gift and actions are the fastest-growing POS transac-

mall cards that use a restricted access tion type, but still only account for small pro-

network over open-loop rails amounted portions of POS volume and value.

to C$1.03bn, with the average load per In 2015, prepaid cards represented 1.1%

card being C$83; of total Canadian payments by volume,

accounting for 236 million transactions

• The average load onto all categories worth C$18bn says Payments Canada.

of consumer-funded prepaid card was Formerly known as the Canadian Pay-

C$218; ments Association, Payments Canada is

www.cardsinternational.com March 2017 y 11

CI 541.indd 11 06/03/2017 17:02:26

1:15:29You can also read