EARNINGS SEASON STARTS TO HEAT UP

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Forbes Real Estate Investor

commercial real estate news

New York, NY

August 2019

---

Q&A with Avison Young CEO Mark Rose p. 7

AUGUST 2019

EARNINGS SEASON STARTS TO HEAT UP

It is earnings season again and REITs are starting to report second-quarter earnings

results. Overall, I’m liking what I’m seeing.

For example, industrial giant Prologis (PLD) increased core funds from operations

(FFO) by $0.06 per share and Crown Castle International (CCI), which leases cell

towers, announced it is increasing its full year 2019 adjusted funds from operations (AFFO) per share

E DITOR, B RAD THOMAS

outlook by 8%. (For more, see Infrastructure REITs Towering Over The 5G Economy on page 21.)

IN THIS ISSUE: Corporate Office Properties (OFC), which I refer to as the “cyber security REIT,”

has returned 26.8% year-to-date. Earnings per share for the second quarter were $0.95,

COMMENTARY . 1 up from $0.19 for second-quarter 2018. Management increased full-year EPS guidance

DIVIDEND KING . 3

range to $1.52-$1.56 from $1.34-$1.38.

Q&A: AVISON YOUNG’S MARK ROSE . 7

There are always outliers and I want to call your attention to some specialty picks

REIT PORTFOLIO ALLOCATION . 8

we’ve made. Outfront Media (OUT), a billboard REIT, is up 44% year-to-date. Its

BROOKFIELD PROPERTY PARTNERS . 13

HOUSING MARKET CHECK-UP . 19

earnings will be released on August 5. Landmark Infrastructure Partners (LMRK),

5G AND INFRASTRUCTURE REITS . 21 which scheduled its second-quarter earnings release on August 7, is up 45%. Both have

DURABLE INCOME PORTFOLIO . 27 given the New Money Portfolio a strong boost (see portfolio on page 31). Essential

GROWTH & INCOME PORTFOLIO . 29 Properties Realty Trust (EPRT)—a net lease REIT recommended in December 2018—

NEW MONEY PORTFOLIO .31 has returned 49% so far this year. Earnings are scheduled to be released on August 7.

SMALL-CAP PORTFOLIO .33

Year-to-date, the Vanguard Real Estate ETF (VNQ) is up 18.8% and many property

PORTFOLIO COMPARISON . 34

sectors have become soundly valued. The top-performing REIT sectors so far this year

INDEXES . 35

include single family rentals (up 29.9%), industrial (gaining 25.2%), data centers (up

FREI REIT SECTORS . 36

BUY LISTS . 39

23.1%) and cell towers (increasing 22.8%).

GLOSSARY . 40 Manufactured housing, driven by the so-called “silver tsunami” (aging population),

FREI TERMS . 41 is also booming, up 28% excluding UMH Properties (UMH), which has made some

unwise investments of late.

W W W.FOR B E S N EWS LET TE R S.C OM

Several retail REITs also did well in the second quarter: Mountain (IRM). Shares in this box storage juggernaut are

Agree Realty (ADC) bumped its acquisition guidance to a down 5% in July, driven by a downgrade from Bank of

range of $625 million to $675 million, up from $450 to $500 America. However, we see value in the business model and

million; Retail Opportunity Investments (ROIC) saw same- growth in the data storage business.

store net operating income up 4.6% year-over-year; You may recall we included an article on the beaten-down

Taubman Centers’ (TCO) tenant sales increased 12% to prison REIT CorCivic (CXW) in last month’s newsletter. Since

$940 per square foot and Kimco Realty (KIM) raised the July 1 shares have been punished, down 24% through July 24.

full-year guidance range for same-site net operating income The controversary over the Trump administration’s detention

growth from 1.8% to 2.5% to 2% to 2.7%. policies has sparked a revolt as many banks (including

Uncertainties in retail are still present, however, SunTrust, Wells Fargo, JPMorgan Chase and Bank of America)

especially in the mall sector as more store closures are have opted to phase out lending to private prison companies

anticipated in 2019. In light of the retail challenges (and like CXW and Geo Group (GEO).

underperformance of the mall REITs), we have downgraded Finally, one of the ways to get a better handle on the U.S.

some of our BUY recommendations to HOLD or TRIM. commercial real estate market is by researching commercial

But this doesn’t mean it’s time to panic and sell everything. mortgage REITs. Year-to-date the specialty finance category

It means you have to become a more tactical REIT investor. is up 12.1%. We have six commercial REITs rated as BUY.

Within the shopping center sector, we still like the high- I recently spoke with Ladder Capital’s (LADR) CEO,

quality names like Kimco Realty, Regency Centers (REG) Brian Harris, and he said you have to be careful with hotels

and Brixmor Property Group (BRX). Our mall REIT list is because “they eat money like a teenager eats food.” He

limited to the best capitalized names, including Simon commented that you must be “selective” with hotels today

Property Group (SPG), Taubman Centers (TCO) and (which is the reason we’re underweight).

Tanger Factory Outlet Centers (SKT). I asked Brian if there are sectors he is avoiding in

While many property sectors are pricey, we still find preparation of the “next” recession and he said, “most

value in healthcare, which is up 15.4% year-to-date, where anything that deals with obsolescence.” He referenced movie

we maintain a number of BUYs. In addition, lodging may be theaters, short-term rentals and bank branches. But added,

a good place to park cash now, but again, you must be “there are no bad loans, there are only bad prices.”

tactical. Strong buys include Ryman Hospitality Properties Brian is a credit risk expert, and speaking of experts,

(RHP), which owns conference hotels, and VICI Properties this month’s issue includes a Q&A with the CEO of one of

(VICI), which specializes in casinos. the top commercial real estate service firms in the world (see

Another compelling strong buy on our list is Iron page 7).

Source: americannewsgroup.com

2 | FORBES REAL ESTATE INVESTOR | AUGUST 2019

DIVIDEND KING EXPANDS INTERNATIONALLY

I have owned shares in Realty Income (O) for almost in the U.K. under long-term net lease agreements with

ten years and during that time shares have returned an Sainsbury’s, a leading grocer founded in 1869 that

average of 13% per year. Some years the REIT operates more than 1,400 grocery and convenience

performed even better, like in 2011 when shares stores across the U.K. and Ireland.

returned more than 20%. On the flip side, in 2016 True to Realty Income’s acquisition strategies,

shares returned 3.6%. Sainsbury’s checks off a lot of boxes:

But one thing has been unwaivering—this is one of wBlue chip grocery operator with seasoned and

the most consistent dividend payers in the world, and highly-regarded management team

not just in the REIT sector. Regardless of market wTenant operates in defensive, non-discretionary industry

consitions, Realty Income has continued to reward its wProven strength through multiple economic cycles

shareholders, paying monthly dividends for more than Sainsbury’s same-store sales grew at an average

50 years. It has weathered multiple recessions without a annual rate of 4.7% during 2007 – 2010, significantly

dividend disruption and has increased dividends 26 outperforming U.K. retail and GDP growth during the

years in a row, with a compunded average annual dividend Great Recession. The Sainsbury’s deal is consistent with

growth rate of 4.6%. Realty Income’s approach of relationship-based

Simplicity has always been one the secrets to Realty transactions in partnership with industry leaders with

Income’s succesful track record. By investing in net strong management teams; geography is the only

lease properties it has engineered a highly- “difference” in this transaction.

diversified portfolio that consists of more than Realty Income’s portable business model, its cost of

5,800 properties, with 261 commercial tenants capital and its scalability represent core reasons for

operating in 48 industries, located throughout 49 making the move across the pond. According to the

states, Puerto Rico and now the United Kingdom. company, the U.K net-lease market is “ripe for sale-

Realty Income is expanding into international leaseback consolidation.” Realty estimates $11 trillion

markets starting with the acquisition of 12 properties of commercial real estate stock in the European market,

Source: Realty Income website

3 | FORBES REAL ESTATE INVESTOR | AUGUST 2019

only $3 trillion of which is owned by professional real public REIT market in the U.K. is estimated to be

estate firms. approximately $115 billion—roughly the size of the

As the Stansbury transaction demonstrates, Realty publicly traded net lease REIT universe in the U.S.

Income is uniquely positioned to build relationships by

leveraging its industry-leading scale, size and cost of DEBUNKING THE NARRATIVE

capital. The company estimates that corporate-owned Now that Realty Income has a new pool to fish in, so to

commercial real estate stock is 2x greater in Europe speak, expansion into the U.K should remove the narrative

than in U.S., representing a void for a well-capitalized, that the company is too big (in the U.S.) to grow. Now it can

sizable and scalable institutional investor to fill. increase its growth without increasing risk. The

Realty said it plans to establish an office in London international growth enhances Realty Income’s domestic

to grow its European portfolio. Incumbent competition business and it can now expand its market from a position

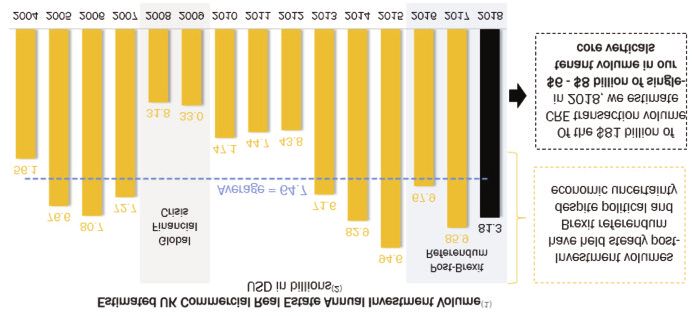

is modest in Europe and the enterprise value of the of strength. Below is a look at the historical U.S. volume.

Source: Realty Income investor presentation

Source: Realty Income investor presentation

4 | FORBES REAL ESTATE INVESTOR | AUGUST 2019

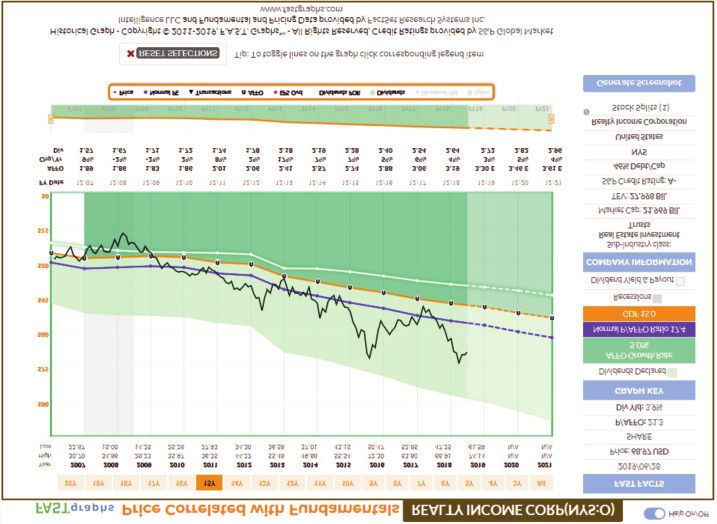

Source: FAST Graphs 5 | FORBES REAL ESTATE INVESTOR | AUGUST 2019

Source: Yahoo Finance. Dark blue (PLD) and light blue (O)

The Sainsbury sales-leaseback deal size is $550 due to valuations. We like them but they are too

million (U.S. dollars) with an initial cap rate of 5.8% (U.S. expensive right now. Wait for pullbacks to get in.

equivalent), which translates into a 200-basis point spread In conclusion, Realty Income has been one of the

to leverage-neutral WACC (weighted average cost of best holdings in Durable Income Portfolio. It

capital). The deal is $0.04 per share accretive to Realty represents 6% of the overall exposure. We believe the

Income’s AFFO (adjusted funs from operations). international expansion represents a tremendous

Realty Income shares are now trading near all-time opportunity for the company to scale its business

highs. Shares recently traded at $68.97 with a P/AFFO model utilizing its low cost of capital advantage.

multiple of 21.3x (normal is 17.4x) and a dividend This move also signals that there is less interest for

yield of 3.9%. Our Trim Target is $70.00 per share. the company to seek M&A opportunities with Spirit

Perhaps Realty Income should be compared with Realty (SRC), for example. There is greater opportunity

Prologis (PLD), another S&P A- rated REIT with to find higher-quality properties so the company can

international operations. Prologis now trades at 29.8x be more selective in growth with a much lower risk

P/AFFO with a dividend yield of 2.6%. profile. Kudos to the management team for making this

We currently have a HOLD rating on both REITs bold move.

6 | FORBES REAL ESTATE INVESTOR | AUGUST 2019

Q&A: AVISON YOUNG’S MARK ROSE

Mark Rose is CEO of Avison Young. He manages all Thomas: At a

strategic, financial and operational activities of this full- high level, what

service commercial real estate company, which provides are your concerns

solutions to real estate investors, owners and occupiers with regard to the

throughout the world. In his 11 years with the Toronto, next recession?

Canada-based company, Mark has overseen its growth from Rose: Recessions

290 real estate professionals in 11 offices in Canada to need to be caused

approximately 5,000 professionals in 120 offices in 20 by some sort of

countries. Mark holds a B.A. in accounting from Queens College. intervention.

Recently I caught up with Mark to get his take on today’s They are usually

market and which sectors he currently favors. caused by systemic

failures or new

Brad Thomas: Using a baseball analogy, what inning do you government

think we’re in now in terms of U.S. commercial real estate? regulations or

Mark Rose: The baseball analogy is too cliché right now. We are changes in law.

in a long-term, low-interest-rate, high-demand environment. This industry has

However, if you want to use that analogy, we are at the come a long way but is still subject to taking its eye off the

beginning of what will be an extended extra-inning ball game. ball. Rising interest rates looked like a sure bet and the

Pricing has eased a little, but we are at a pricing top. correction, if not a recession, was inevitable.

Stable-to-declining interest rates, when combined with Now, the economic data and the Federal Reserve are

significant demand, massive allocations to be committed to being pushed around and stable-to-lower interest rates will

real estate in equity and debt, and a stable macroeconomic keep the economy rolling. If there is a war or if the tariff

environment will keep cap rates low and keep the battle with China escalates, we will have problems and,

(desperately needed) correction away. unfortunately, less sophisticated real estate investors will be

caught off guard—again.

Thomas: What property sectors are you most concerned about?

Rose: The obvious answer is retail as it is being Thomas: In what top three property sectors you would

challenged by a change in how retailers will use property deploy capital today and why?

assets to promote and distribute goods. Many retailers Rose: Industrial, apartments and data centers. I’ll add a

are failing against e-commerce, but those who survive smaller fourth one—memory-loss care facilities. Industrial

still need to choose showroom space versus product, is obvious due to demand from e-commerce retailers, and

service and distribution space. Retail-sector pricing is demand for distribution and last-mile logistics. The

still facing a very negative outlook. fundamentals are aligned with the need. Again, I just worry

The other sector that is very healthy, but where we worry it’s getting too expensive.

about pricing topping out, is industrial. Industrial has As for apartments, the trends are clear—downtown-

everything going for it—fundamentals, demand, growth in living for Millennials and retirees are driving the market.

distribution and logistics, but active development and very The eat-work-play and socialize concept is a “thing.”

high prices are sometimes negative indicators. Young people are mobile and not interested in buying

right away.

Thomas: How do you view the capital markets today? Are With that said, family creation and lower pricing for

banks lending on commercial real estate properties? homes in the suburbs are starting to look inviting. Finally,

Rose: Yes, banks are lending, institutional money is lending, with three billion more people expected on the planet in the

insurance companies are lending, and private-equity firms are next 50 years, we have a major driver of demand/need. We

lending. There is very healthy demand and equal supply for debt might need to build a million square feet of housing per day

and equity in the current market. to match population growth.

7 | FORBES REAL ESTATE INVESTOR | AUGUST 2019

Data centers drive e-commerce and our insatiable use Thomas: Can you discuss ways in which your company has

of cloud-based technology. The U.S. is data-center- invested in technology?

advanced and, in some places, saturated, but there is huge Rose: That is a long conversation. We had the benefit of starting

opportunity globally. out on our growth path in 2008. All our systems are cloud based

Finally, try to find a bed you would put one of your parents and not beholden to legacy. We believe in the technology of the

in if they suffer from Alzheimer’s or other forms of dementia future but must invest in the technology of today to compete.

and you will understand the need. There is less than 1% We believe in PropTech (property technology), but artificial

availability of quality beds specializing in memory care. intelligence, virtual reality and augmented reality just do not

work yet and cannot be seamlessly tied into systems. We have

Thomas: Have you seen benefits related to tax reform? what we need, have invested in PropTech, but we are working on

Rose: Tax reform has been great for the economy and is part a much bigger play for the time when AI will actually work. We

of our strength and job growth. It’s not specific to any real have launched a project called Project 2021 and have a

estate class, or retail would benefit. It has been a very positive differentiated approach to what will be here soon—and who

influence on optimism and stock-market gains. When should actually support it.

equities grow and people are working, real estate is

supported and thrives. Thomas: Thank you.

WHAT'S THE RIGHT REIT EXPOSURE FOR YOUR PORTFOLIO?

By Dividend Sensei

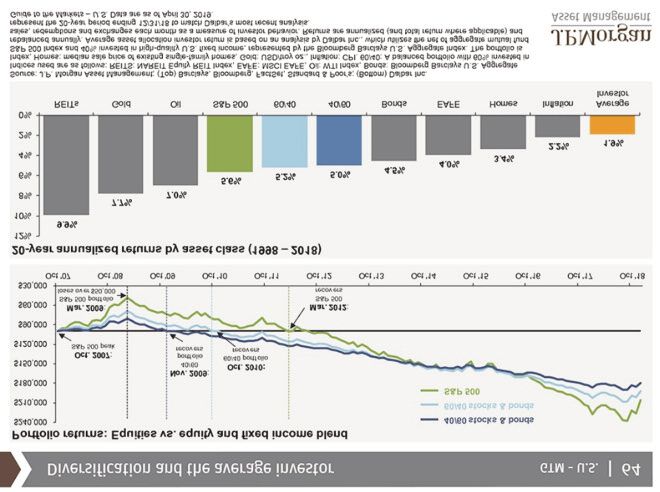

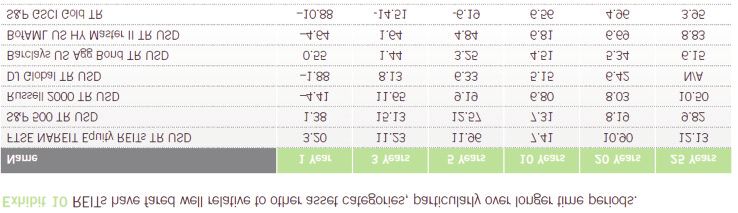

Historically, real estate has been a great way to become REITs, but avoid taking on more risk than is appropriate.

rich. In fact, according to College Investor, over the past Through May 2019 REITs have been the best

200 years, about 90% of the world’s millionaires have performing asset class of the past 20 years, delivering nearly

made their fortunes in real estate. The good news is that 10% annualized total returns over two decades.

REITs offer the average investor a totally passive, What’s more, a Fidelity study that looked at 1995 to

hands-off way to exponentially grow their income and 2015, found that about two thirds of REIT returns come

wealth over time. from dividends and dividend reinvestment.

But of course, this doesn’t mean you should be 100% In other words, in the modern era REITs have beat the

invested in any single stock sector or asset class even if, since market consistently over time and have done so mostly

1960, REITs have been the best performing asset class in through paying investors cold hard cash on a quarterly basis.

terms of inflation-adjusted total returns. While other kinds of stocks can sometimes outperform for

Diversification and proper asset allocation are crucial to several years, those total returns are mostly from fickle

good risk management, which is ultimately how you protect capital gains.

your portfolio from costly mistakes, such as the temptation In December 2018, when the S&P 500 crashed 17%

to panic sell during a severe market downturn (or sector within three weeks (and the tech-heavy Nasdaq plunged

bear market), or merely because of market envy (a few bad 20%) investors learned the hard lesson that stocks take the

years that scare you out of a sector entirely). escalator up, but the elevator down. Or to put another way,

So, let’s address the important issue of just how much years of capital gains can be wiped out quickly, but with

exposure to REITs is right for you, so you can make sure to REITs, the total returns you gain from safe and rising

cash in on the proven income compounding power of dividends, can never be lost.

8 | FORBES REAL ESTATE INVESTOR | AUGUST 2019

Dividends have been a significant portion of REITs’ total returns over time and have provided a source

of stability during equity bear markets.

Dividends Represent A High Percentage Of REIT Total Returns

Source: Fidelity study

9 | FORBES REAL ESTATE INVESTOR | AUGUST 2019

But how much REIT exposure is right for you to balance

Risk/Return Spectrum of Hypothe!cal Por"olios With REIT Exposure

the proven power of REITs to meet your income and total

return needs and the risks inherent to the industry? Por"olio Alloca!on Sharpe Ra!o Percent REITs

55% S&P 500

Here are the risk rules of thumb I’ve developed that

1 35% U.S. Aggregate Bond 0.58 10

are suitable for most investors. That’s based on my six 10 FTSE Nareit Equity REITS

years as a professional analyst/investment writer at the 40% S&P 500

2 40% Barclays U.S. Aggregate Bond 0.63 20

Motley Fool, Simply Safe Dividends, Seeking Alpha, iREIT 20% FTSE Nareit Equity REITs

and Adam Mesh Trading Group, as well as consulting with 33.3% S&P 500

3 33.3% Barclays U.S. Aggregate Bond 0.61 33

various asset managers (some with 50 years of experience 33.3% FTSE Nareit Equity REITs

in the financial industry). 4

60% S&P 500

0.55 0

40% Barclays U.S. Aggregate Bond

80% S&P 500

5 0.48 0

RISK MANAGEMENT RULES OF THUMB 20% Barclays U.S. Aggregate Bond

w Always maintain proper asset allocation (with Source: Fidelity Study

periodic rebalancing) meaning owning enough cash/bonds to

avoid having to sell stocks during inevitable market downturns stock/bonds that the 4% rule is based on) delivered lower

wOwn a diversified stock portfolio (ETFs or 20 to 30 stocks returns with the highest volatility.

in most sectors works best for most people) REITs, naturally a lower volatility sector (because of

wLimit individual holdings to 5% to 10% of your stock extremely stable cash flow that ultimately underpins share

portfolio (my personal long-term goal is 5%) prices, plus high-yield investors are less likely to panic sell)

w Limit sector concentration to 15% to 25% (my helped to significantly lower volatility over time.

personal long-term goal is 25%) Fidelity tested 10%, 20% and 33.3% REIT exposure, and found

that the more REITs you owned the better your total returns were.

REIT EXPOSURE IN YOUR PORTFOLIO But note that if risk-adjusted total returns (i.e. max

When it comes to a sector as high-quality as REITs, you want Sharpe Ratio) was your goal, then the ideal REIT exposure

to have at least 10% exposure in your portfolio. Think of it over this time period was 20%. That percent of REITs,

like this: There are 11 official sectors according to S&P. If combined with 40% stocks and 40% bonds (basically a

you were to equally weight them, then you would need at balanced portfolio with REITs replacing a third of your stock

least 9% in each. So, 10% is a slight overweighting based on allocation), delivered 0.63% of total returns per unit of volatility.

equal sector balancing. Ultimately, there is no absolute answer to what the

But of course, certain sectors are better than others at optimal REIT exposure is for all investors, as individual

meeting individual needs, which is why it’s often useful to goals, risk tolerances and time horizons differ. This is why I

overweight REITs. So, let’s take a look at the reasons you recommend 10% to 25% as a reasonable range for most

might want to own far more than 10% in REITs, as well as investors, with those seeking higher yields as a primary goal

the risks you might face if you do so. (such as retirees) overweighting in REITs. My

retirement portfolio is 18% REITs right now, and I’d happily

take it to 25% if I saw the right opportunities available.

SOME REASONS TO POTENTIALLY OVERWEIGHT Why is allocating your portfolio in 33% or more in

REITS AND RISKS TO KEEP IN MIND REITs potentially a bad idea?

Using market data from 1995 to 2015, Fidelity did a study Due to the silly belief that REITs are a bond proxy

examining how various amounts of REIT exposure affected (REITs are nothing like bonds except in that they pay you

not just total returns, but also portfolio volatility, as income) many REIT investors have come to fear rising

measured by various risk metrics, such as the Sharpe ratio interest rates. As Fidelity points out in its study (and

(see table above). When comparing different investments, historical data going back to 1972 confirms) there is actually

typically the higher the Sharpe ratio the better. no long-term correlation between REIT total returns and

The two portfolios with zero REIT exposure delivered long-term interest rates (inconsistent does not mean bad, it

the worst returns, and Portfolio 5 (standard 60/40 means very little correlation).

10 | FORBES REAL ESTATE INVESTOR | AUGUST 2019Source: Fidelity Study

Source: Fidelity Study

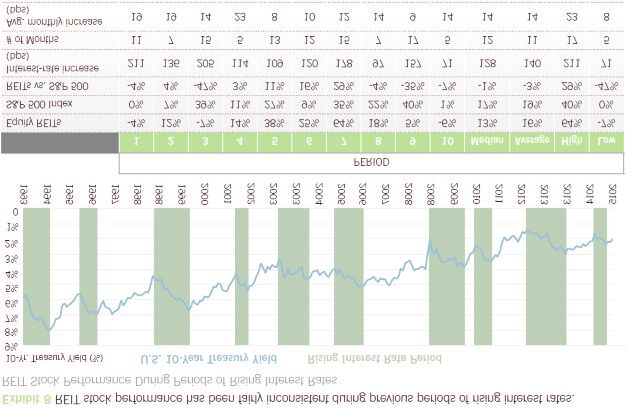

From 1993 to 2015 there were ten periods of rising example, below 0.14% per month, then REITs usually out-

interest rates, and in six of these, REITs delivered positive performed the S&P 500 by between 3% to 29%. In other

monthly returns. Ten-year yields increased a median of words, REITs (like most stocks) are not necessarily sensitive

1.28% and at a rate of 0.14% per month. During these times to rising rates, as much as the pace of interest rate increases.

REITs still returned 16% average total returns and 13% If 10-year yields soar quickly, then all stocks fall, as occurred

median total returns. In other words, rising rates were not during 2018’s first correction, which was mostly caused by

necessarily bad for REITs, because rates tend to rise during soaring long-term rates caused by an inflation scare.

strong economies. However, REIT total returns underper- However, REITs are not just one monolithic group of

formed the S&P 500 by a median of 1% during these times. companies. They are broken down by subsector/industry. As

But note that when rates rise more gradually, for Fidelity explains, various kinds of REITs tend to react

11 | FORBES REAL ESTATE INVESTOR | AUGUST 2019Source: Fidelity study - REITs 1990 to 2015

differently during periods of rising interest rates: “More actually normal, not just for all sectors, but all investing

economically sensitive and shorter-lease property sectors, strategies (i.e., value, dividend growth, low volatility,

such as hotels, apartments and self-storage facilities can small-cap, etc.).

more easily raise rental rates in stronger, inflationary

environments—a tailwind for these sectors. For their part, PROBABILITY OF ALPHA STRATEGY UNDER-PERFORM-

mall REITs have also fared well during periods of rising ING S&P 500 OVER ROLLING TIME PERIODS

interest rates as an improving economic backdrop has As you can see, even well proven long-term alpha generating

tended to buoy more discretionary sectors. On the flip side, strategies can spend many years, or even decades, under-

strip mall shopping centers have tended to underperform performing the broader market. That’s exactly why they

during rising interest-rate periods as tenants are generally keep working over time because periods of

more value-oriented, and their customers have shown a underperformance result in investors giving up due to

propensity to “trade up” during periods of economic “market envy,” what Wall Street calls tracking error. Well

strength. Furthermore, the health care REIT sector, which REITs, too, go through their periods of underperformance.

includes senior living facilities that tend to have longer-term For example, if you bought REITs in 1990 and just held on

contractual leases has more bond-like characteristics and and patiently collected your dividends through 2015, you’d

thus exhibits greater interest-rate sensitivity. However, it’s have crushed the S&P 500 and Russell 2000 (small-caps) and

important to note that REITs are not static yield investments achieved double the returns of bonds and three times that of

such as bonds, as REITs offer the potential for growth—a gold. But from 2010 to 2015 you’d have underperformed the

key distinction. Thus, the varied supply/demand dynamics S&P 500 by about 0.6% per year, and from 2012 to 2015 you’d

and lease durations found across commercial property have underperformed the broader market by 4% per year.

sectors is one explanation for the overall inconsistent sensitivity of And woe be to any income investor dumb enough to go

broad REIT stock performance to interest-rate changes.” all into REITs in mid-2016, the peak of the last REIT bubble.

So why do I bring up interest rates at all? Because for The two-year bear market that followed, and ended during

good or ill the popular idea that “rates up, REITs down” 2018’s first correction, meant that plenty of income

could result in several years of underperformance, especially investors (yield chasers with poor risk management) ended

if the U.S. ends up avoiding a recession (about 60% chance up buying high (when REITs were ridiculously overpriced)

of that) and long-term rates end up recovering. But that’s and selling low (when they were a screaming buy).

These people might have chalked up their painful

1-Year 3-Year 5-Year 10-Year 20-Year

losses to “bad luck,” the “rigged casino” nature of Wall

Market Beta 34 24 18 9 3

Size 41 34 30 23 15

Street or the popular “rising rates are bad for REITs”

Value 37 28 22 14 6 meme. In reality, it was forgetting that “quality first,

Momentum 28 16 10 3 0 valuation second and good risk management always”, is

Source: Advisor Perspectives how you invest the smart way.

12 | FORBES REAL ESTATE INVESTOR | AUGUST 2019These time-tested principles are so simple, that Charlie those three, possibly 3.33% allocations to each (thus

Munger, Buffett’s right hand at Berkshire for decades, 10% of your portfolio).

doesn’t even consider it “smart” investing, but rather Later, when your other seven quality REITs hit fair value

“consistently not stupid” investing. or better, you can buy them and take your REIT exposure up

There is no question that all investors should own to whatever level you are comfortable with. Just remember

REITs; the only question is how much is right for your that all sectors have their individual risk profiles (REITs are

portfolio’s goals, risk tolerances and time horizon. generally low volatility but economically sensitive) and will

Ultimately the right answer to how much REIT exposure is experience periods of underperformance.

optimal is a very personal one. So, factor your particular ability to avoid “market envy”

Ten percent to twenty-five percent is a good range, into your decision of how many REITs you want to own, if

depending on your individual portfolio income needs the quality and valuations are good enough.

(more yield requires higher REIT exposure) but also the Ultimately the goal of all investors shouldn’t be to try to

valuations at which the sector and individual quality REITs maximize absolute returns but follow a sound long-term

are trading at. strategy that’s most likely to meet their personal financial

For example, say you have a select list of blue-chip goals while letting them sleep well at night. And don’t just

REITs you consider SWANs (sleep well at night) income take my word for it. No less than Benjamin Graham,

payers. If that list consists of ten names you consider to Buffett’s mentor and the father of value investing wrote in

be excellent REITs, with very safe dividends, strong the Intelligent Investor, “The best way to measure your

long-term growth prospects and world-class manage- investing success is not by whether you’re beating the

ment teams you can trust with your hard earned money, market, but by whether you’ve put in place a financial

and just three of those ten are currently trading at rea- plan and a behavioral discipline that are likely to get

sonable/good valuations, then you will want to buy just you where you want to go.”

SPOTLIGHT ON BROOKFIELD PROPERTY PARTNERS

A few of the top global asset managers sponsor publicly stable cash flows, asset appreciation and annual

traded stocks meaning everyone, not just sovereign wealth distribution growth of 5%−8%.

funds, can invest alongside them. The diversity and scale of Brookfield Property REIT is a subsidiary of Brookfield

Brookfield’s publicly traded stocks stand out. Brookfield Property Partners and is structured as a U.S. REIT security

Property REIT (BPR) and Brookfield Property Partners instead of a partnership. The underlying assets and

(BPY) represent the real estate arm of Brookfield Asset payments to investors are identical. Investors wary of the tax

Management (BAM) and are what we’ll be evaluating today. implications of investing in foreign companies or partner-

Brookfield Property Partners is a global real estate ships should stick with BPR, which involves Form 1099-DIV

company that owns, operates and develops one of the rather than Form K-1.

largest portfolios of office, retail, multifamily,

industrial, hospitality, triple net lease, self-storage, REAL ESTATE POWERHOUSE BEHIND THE SCENES

student housing and manufactured housing assets. Its Brookfield is generally considered the largest real estate

investment objective is to generate attractive investor globally with more than $190 billion in real estate

long-term returns on equity of 12%−15% based on assets. Brookfield’s real estate division has 450 million

13 | FORBES REAL ESTATE INVESTOR | AUGUST 2019square feet of commercial space. That’s equal to 16.1 PRIVATE FUND INVESTMENTS

square miles or the equivalent of 4,205.6 average-sized Approximately 20% of BPY’s balance sheet is interests in

Walmart stores. Brookfield employs more than 17,000 Brookfield funds that are expected to deliver approximately

operating employees to manage its real estate assets, which $4.0 billion in proceeds to BPY over the next five years. The

encompass every major type from industrial parks to funds have performed well achieving internal rates of return

manufactured housing. (IRRs) in the high teens.

BPY and BPR are likely to receive at least $500 million a

EVOLUTION FROM FINANCIAL TO HARD ASSETS year in proceeds from private funds through 2022, an

Brookfield Property Partners was spun out of Brookfield impressive 50% of which are expected to be profits.

Asset Management in 2013 then merged with Brookfield

Office Properties creating the Brookfield Property Partners LOOKING UNDER THE HOOD OF THE 7% DISTRIBUTION

we know today. Brookfield engaged in several key Investors tend to concentrate on an investment’s yield

transactions, including the purchase of the remaining more than the cash flow behind it. Company funds from

stake in General Growth Partners (GGP), which went operations (CFFO) as cited in the diagram on page 15 and

bankrupt during the Great Recession. BPR and BPY issued most of Brookfield’s reports is defined as traditional FFO

160 million shares and 110 million units, respectively to with several adjustments to better model BPY and BPR’s

complete the transaction. This transaction led to the activities. The formula is a fair method to measure their cash

formation of Brookfield Property REIT as GGP flow. Given $0.32 and $0.38 per unit in net income and

shareholders were given the option of shares in the new CFFO, respectfully, the $0.33 distribution was fully covered

company structured as a U.S. REIT. This type of deal suits in the first quarter but let’s look at more data.

Brookfield perfectly: large, complex transactions of Using CFFO alone, the payout ratio has remained

discounted but quality assets. healthy and below 1 since inception. It’s trending lower

toward Brookfield’s target of 80% thanks in part to annual

PROJECT PIPELINE CFFO growth of 9% since inception.

The latest data from Brookfield indicates a 12 million square Full-year 2018 generated company FFO and realized LP

foot pipeline expected to add $500 million in net operating gains of $2.09 per unit against distributions of $1.26 per

income (NOI) over the next three to five years. Most unit or a conservative 60.3% payout ratio or 50.8% using net

development projects are pre-leased over 50% with many income. This data shows BPY and BPR tend to cover their

achieving 80% initial occupancy. distribution with a greater cushion than most REITs when

BPY’s Manhattan West project is an excellent including gains and losses.

demonstration of Brookfield unravelling a web of legal, Net income of $333 million declined from $530 million

engineering, regulatory and financial challenges. Brookfield in the first quarter of last year. Significant proceeds realized

invested approximately $5.0 billion into the deal with an in previous periods have been invested in new developments

expected value of $8.6 billion once the asset is fully leased. that have not yet begun generating meaningful cash flows,

which represents the bulk of the first-quarter decline.

Combining BPY’s various business activities results in FFO

Realized Gains On LP Investments (per unit) growth per unit of 5%-9% annually or from $1.33 to $2.00

$0.70 per share over the next five years. Management expects the

$0.60 distribution to rise similarly at 5%-8% annually or

$0.50 approximately double REIT averages.

$0.40

$0.30 DISCOUNT TO NAV: OPPORTUNITY OR WARNING SIGN?

$0.20

BPY and BPR have historically traded at a steep

$0.10

discount to their net asset values usually signaling trouble.

$0.00

BPY is more complex than many traditional REITs often

2014 2015 2016 2017 causing a “complexity discount.” Another is the shift in asset

Source: bpy.brookfield.com types over time as BPY started out 80% invested in the

14 | FORBES REAL ESTATE INVESTOR | AUGUST 2019Source: Brookfield first quarter BPY Press Release

Source: bpy.brookfield.com

securities of other publicly traded firms. It is now three to evaluate Brookfield’s actions in that context. I expect the

times the size of its IPO value and owns mostly physical discount to NAV to narrow if Brookfield performs well but

properties, which was its intention all along. remain significant. Management is transparent about the

Brookfield Asset Management receives substantial fees discount and believes buybacks, lower leverage and a simpler

from BPY and BPR and maintains a complex ownership business model will alleviate the discount.

structure in each entity. BAM’s fee structure is a minimum

fee of $50 million annually, 0.3125% of the increase in the BUYBACKS AND GLOBAL APPROACH

market capitalization, and up to a maximum of 25% of the Bro o k f i e l d Prop er t y Pa r t n ers p u rch a s e d

distribution. Brookfield has an incentive to grow BPY and approximately $400 million of the $500 million in units it

BPR’s market capitalization as well as their yield. Investors need offered to buy most recently. Another positive is Brookfield’s

15 | FORBES REAL ESTATE INVESTOR | AUGUST 2019global expertise with net operating income per city shown r atios and tig hter fixed charge cover age r atios

below. Despite challenging markets in the U.K. and that Brookfield will have to manage.

Br azil, BPY gener ated 4.2% same-prop er t y NOI

growth, excluding the impact of currency effects compared to CONCLUSION

6.4% growth in the U.S. Targeted asset level returns are 12%- Trading at only two thirds of book value, Brookfield

15% IRR, which are in line with Brookfield’s institutional track Property REIT and Brookfield Property Partners give

record shown below. investors the opportunity to own a piece of Brookfield’s real

estate empire at a significant discount. 2018’s company FFO

OCCUPANCY, RENTS & LEASE EXPIRATIONS and realized gains result in a 9.1x multiple assuming $19.00

Let’s take a quick look at occupancy over time. Rents per share. Estimates incorporating full year 2019’s earnings

improved from 92.6% to 93.3% on a portfolio level from push that multiple below 8.0x. How attractive is that?

first-quarter 2018 to first-quarter 2019. At least 27% of the The average price to FFO multiple for equity REITs per Nareit

properties have rents below market and are where has ranged between 15x and 19x since 2011 and is about 17x today.

Brookfield can substantial ly improve prop er t y The comparison is “oranges to clementines” given the

economics. In terms of lease expirations, they are manage- accounting differences used in the FFO calculation

able at 5%-10% annually but higher than some other REITs. discussed previously. Brookfield’s large investment in the two

entities helps mitigate conflicts of interest but not entirely. No

A UNIQUE BUT FITTING LEVERAGE STRATEGY

matter how the data is evaluated, BPY and BPR trade at about

BPY and BPR’s encumbered asset base can be a strength

half price compared to peers. They also pay nearly double the

or weakness. Most quality REITs avoid this to lower interest

equity REIT average dividend yield of 3.75%.

expense. For BPY and BPR, however, the ability to walk away

There are plusses and minuses to every investment, but

from a development project with no recourse is extremely

the problematic aspects of BPY and BPR are a lot more

valuable and only possible using this strategy. Brookfield is

bearable after taking into account its globally diversified and

positioning the portfolio to survive deep recessions or

quality asset base, compelling valuation, fully-covered 7.0%

unexpected project failures. It’s taking the long-term view as

yield, and highly attractive growth projections.

it has since its inception in the 1800s. BPY and BPR’s

massive asset growth has resulted in substantial leverage Williams Equity Research assisted with this article.

Source: Brookfield first quarter 2019 supplemental

16 | FORBES REAL ESTATE INVESTOR | AUGUST 2019Source: Brookfield first quarter 2019 supplemental

Source: bpy.brookfield.com

17 | FORBES REAL ESTATE INVESTOR | AUGUST 2019Source: Brookfield first quarter 2019 supplemental

Source: IRM presentation

18 | FORBES REAL ESTATE INVESTOR | AUGUST 2019CHECKING THE PULSE OF THE HOUSING MARKET

By Alex Pettee, CFA, Director of Research & ETFs at Hoya Capital Real Estate

As goes the housing market, so goes the economy. For the most roughly 30% dip for the largest single-family homebuilding

critical asset class in the world, the last 12 months have been the ETFs—SPDR S&P Homebuilders (XHB) and iShares U.S.

most interesting—and unsteady—since the end of the financial Home Construction (ITB)—in 2018.

crisis as a plethora of headwinds came to a head at the end of By the end of the year, growth in single-family housing

2018. The combination of significantly higher mortgage rates starts, new home sales and existing home sales all turned

and the lingering, and perhaps lasting, effects of tax reform negative on a trailing 12-month basis for the first time since

stunted single-family housing demand at the end of 2018, late 2011. Home prices, particularly in the high-tax coastal

sending the housing markets into a brief but notable “housing markets, began to inflect lower and even turn negative by

recession” with home sales and housing starts data turning early this year in a handful of once-hot markets. These clear

negative for the first time since early this decade. signs of softness in the single-family markets prompted calls

Interestingly, this relatively weak demand came amid the from the financial media and analysts—which has long been

best year for total household formations since the 1980s, bearish on the single-family housing sector—of “peak

which breathed new life into the rejuvenated residential housing” and an end to the post-recession housing recovery.

rental REIT sectors. In the first quarter of this year, If indeed this was the end, it would come at a time when

apartment REITs delivered the best quarter in years, as total housing starts are still more than 20% below the 1970-

same-store net operating income (NOI) growth is again 2000 average and more than 40% below those levels on a

running ahead of the broader REIT

average for the first time since 2016.

Rent growth and leasing metrics have

reaccelerated sharply since bottoming

in 2018 despite still-plentiful supply

growth in the multifamily markets.

Fundamentals are even stronger in the

single-family rental and manufactured

housing REIT sectors, which are seeing

a similar demand tailwind without

meaningful supply growth as higher

mortgage rates in 2018 kept the

marginal household in the rental markets.

For the single-family building

sector, softening demand was only part

of the issue. On the supply-side, higher

construction costs and tight construction

labor markets throughout 2018

depressed single-family homebuilding

margins further, making new single

family development largely

unprofitable for all but the biggest

single-family builders. By the end of

2018, all five “Ls” of homebuilding—

lending, lumber, labor, land and

legislation—were acting as stiff head-

winds for builders, reflected in the

19 | FORBES REAL ESTATE INVESTOR | AUGUST 2019population-adjusted basis. It would come at a time when points, prompting a significant slowdown in single-family

new home sales are more than 50% below their pre-bubble housing data over the next year before bouncing back

peak and well below their long-run averages. If we’re indeed strongly in 2015 as rates again pulled back.

at peak housing, it would somehow come ahead of an By nearly every metric, single-family housing markets

impending demographic-driven boom of Millennials, who remain significantly undersupplied, a vastly different

are just now entering the housing markets as the largest age fundamental scenario than the pre-recession period.

cohort in the country—25- to 30-year-olds—are seeing the Household formations outpaced new housing starts by more

strongest wage gains in a generation, getting promoted, and than 100,000 in 2018 as the vacancy rate for both owner-

beginning to get married and settle down. Compared to the occupied and renter-occupied homes reached multi-decade

historically small Gen X generation, Millennials are more lows in the fourth quarter. The U.S. has been under-building

numerous and far wealthier during this critical age as it homes since the early 1990s, and that trend has intensified

relates to housing demand. dramatically since the housing bubble burst in 2008. On a

Regardless, the outlook for the single-family housing rolling ten-year average, residential fixed investment as a share

marked looked pretty bleak last December with mortgage of GDP is the lowest since the end of WWII, a function of

rates at post-recession highs and housing data showing a underinvestment in both new home construction and existing

sharp pullback in both demand and appetite for new home repair and renovation activity.

construction. Through the storm

clouds, the sun began to reemerge in

early 2019, prompted by the sharp pull-

back in interest rates, which peaked

above 5% last November and dipped

below 4% earlier this year, which erased

perhaps the most significant headwind

facing the sector last year. Combined

with the sharp decline in lumber prices,

single-family builders have become

quite a bit rosier in their outlook over

the last two quarters, reflected in the

n i ce re cove r y i n h o m e b u i l d e r

sentiment and a solid second quarter

earnings season for the sector.

Forward-looking metrics like

mortgage demand, homebuilder

sentiment and commentary from home-

builders themselves has painted a bright

picture for the second half of 2019 even as

the slower-reacting metrics like homes

sales, housing starts and home prices

continue to be uninspiring. We continue

to view the slowdown in 2018 and

pending reacceleration in 2019 as more

akin to the post-tap er-tant r um

conditions of 2014 and 2015 than to any-

thing like the pre-bubble period of 2007.

In the wake of the “taper tantrum,” the 30-

year mortgage rate shot higher by 120 basis

20 | FORBES REAL ESTATE INVESTOR | AUGUST 2019While there are obviously pockets of ample supply and sectors. As it relates to the REIT sector, I see continued

soft demand scattered throughout the country, at the upward pressure on rents and home values as the growing

national level, the housing shortage is very real and likely to number of Millennial households compete over a still-

get worse before it gets better as the demographic wave of limited supply of available housing units. Already the largest

Millennials enters the housing markets in-full-force during spending category for the average American, I see housing

the 2020s. The implications of this housing shortage and costs and rents continuing to rise as a share of total

broader underinvestment in residential housing over the spending. So, if you think the “rent is too damn high” now,

past decade, I believe, will be a continued persistence of you may not love what the next decade has in store.

“real” housing cost inflation, which has been responsible for

nearly half of total inflation since 2012.

At the investment level, I see a long runway for growth

in new residential housing construction in order to equalize Disclosure: Hoya Capital Real Estate is the index provider

this supply/demand imbalance, driving the performance of for the Hoya Capital Housing 100 Index (ticker: HOMZ

the single-family homebuilding sector. In the meantime, I Index), a rules-based index composed of the 100 companies

forecast the continued realization of hundreds of billions of that collectively represent the performance of the U.S.

dollars in deferred home improvement spending that housing industry. The index is designed to track total

accrued over the last decade, having positive implications annual spending on housing and housing-related services

for the home improvement retail and home furnishings across the U.S.

INFRASTRUCTURE REITS TOWERING OVER THE 5G ECONOMY

Over the next decade, wireless applications powered by networks, with early rollouts in select cities starting

firth-generation (5G) network technologies are expected to this year.

disrupt nearly every sector of the economy, requiring 5G technology works in tandem with existing 4G

massive investments in communications infrastructure. networks to deliver speeds similar to wired fiber

We believe cell tower and data center owner- connections, while essentially eliminating lag times and

operators will be key beneficiaries of 5G-related drastically reducing power consumption. Initial 5G smart-

spending, providing critical assets to carry economies phones are expected to consume 270 times the data of 2G-

into the next digital era. era feature phones and roughly three times the data of

current phone models (exhibit 2).

WHAT 5G IS AND WHY IT’S A GAME CHANGER We believe that deploying 5G networks will require not

The introduction of 4G wireless broadband paved the only increased investments in traditional “macro” cell

way for smartphones that could access the web at high towers, but also small-cell nodes, interspersed to provide

speeds, creating a surge in data consumption (exhibit capacity in areas of higher population density. These nodes

1). In response, wireless carriers have invested in con- can be placed on macro towers or existing structures, such as

tinuous upgrades to relieve network stress and satisfy traffic lights, street lamps and rooftops, connected to local

consumer demand. But even as they continue to data centers via underground fiber.

expand and improve 4G coverage, these companies are Once in place, these networks will have the potential to

looking ahead to deliver even faster data speeds and open entirely new commercial applications that are already

other enhancements through the development of 5G taking shape.

21 | FORBES REAL ESTATE INVESTOR | AUGUST 2019As of June 30, 2019. Sources: Cisco VNI Mobile Visual Networking Index 2017-2022, American Tower, Ericsson Mobility

Report. Cohen & Steers estimates based on average use per device and projected increasing penetration of wireless devices

based on historic trends.

As of June 30, 2019. Sources: Cisco VNI Mobile Visual Networking Index 2017-2022, American Tower, Ericsson

Mobility Report. Cohen & Steers projections based on historic trends assuming step change in demand with each

new device version.

22 | FORBES REAL ESTATE INVESTOR | AUGUST 20195G USE CASES individual tower sites—more than ten times the number

• The Internet of Things (IoT): Embedded 5G hardware will built in the U.S. during that period. In all, China has

enable any computerized item to interact with other objects earmarked $400 billion solely for 5G investment under its

over the internet, creating a global wireless network of current five-year plan, not only for domestic infrastructure

interconnected “things.” needs, but also to develop standard essential patents that may

• Autonomous vehicles: A single driverless car could consolidate market leadership as 5G expands worldwide.

generate as much data in a typical day as about 30,000 The relative spending shortfall in the U.S. has led to calls

current-model smartphones (as of June 28). That means to accelerate investment to close this gap, or potentially face

high data speeds, reliable connections and low lag times will longer-lasting economic effects. Consulting firm Accenture

be critical to allowing cars, buses, trains and ambulances to estimates that U.S. wireless companies will invest $275

communicate with other vehicles or with existing city billion in building 5G networks, which is expected to create

infrastructure—roads, bridges, parking garages and traffic three million new jobs and add $500 billion to the economy.

lights, all fitted with sensors to direct and reroute traffic.

• Smart cities: Connected infrastructure could become the INVESTING IN 5G INFRASTRUCTURE REITS

backbone of entire smart cities, able to deliver targeted, In our view, rapid growth in data usage in the late-4G

hy p er-efficient municipal ser v ices, from public environment and the urgent demands of the approaching

transportation to snow removal, based on granular 5G era are likely to require massive investments to expand

real-time information. communications infrastructure capacity over the next

• Augmented reality (AR) and remote robotics: AR is decade. We believe this stands to directly benefit the cell

expected to be a $100 billion market by 2020, powering tower industry, where public U.S. companies hold dominant

applications as diverse as surgical tools, immersive market positions. In addition, we expect the spike in both

entertainment, educational simulations and virtual tourism, wireless and wired data traffic to drive sustained demand for

delivered through simple headsets. data centers.

• Smart manufacturing: Entire factories could become 5G- Public data center and tower operators, which are

enabled through a single roof antenna, letting manufacturers structured as real estate investment trusts, span both the

monitor every aspect of the production process in real time— listed infrastructure and real estate universes. Their sector

from the assembly line to quality control to equipment weights over the past decade reflect a broader evolution of

troubleshooting—correcting costly inefficiencies early in the the U.S. REIT market, which increasingly consists of new

fabrication stage and shortening the production cycle. and differentiated property types. The first data center REIT,

• Agriculture monitoring: Real-time monitoring of crop, soil Digital Realty (DLR), was listed in 2004, while American

and livestock conditions and precision forecasting of Tower (AMT) was the first tower company to convert to

weather patterns could help farmers optimize crop yields, REIT status in 2012. Today, tower and data center REITs

identify early signs of livestock disease and manage acreage make up nearly a quarter of the U.S. REIT market, valued at

while controlling farm labor costs. $1.1 trillion (see below).

Meanwhile, communications infrastructure—tower

Economic Competition Driving 5G Urgency operators alone—represent around 8% of the listed

Increasing mobile connectivity has historically benefited a infrastructure market.

country’s economic output, and we expect that to be even

more important with 5G. Global auditing and consulting Year Data Centers Towers Market Cap

fir m Deloitte projec ted that early adoption and U.S. REITs

development of 5G technologies could bring more than a 2000 0 0 $139 billion

2012 2% 6% $548 billion

decade of GDP growth leadership for first-mover countries. 2019 7% 15% $1.1 trillion

One country in particular has recognized this potential and

Global Infrastructure

has moved aggressively to establish early dominance. 2015 5% $1.9 billion

Between 2015 and 2018, China outspent the U.S. by $24 2019 8% $2.7 billion

As of June 30, 2019. Source: Nareit, FTSE, Bloomberg , Cohen & Steers

billion on 5G-ready infrastructure and built 350,000

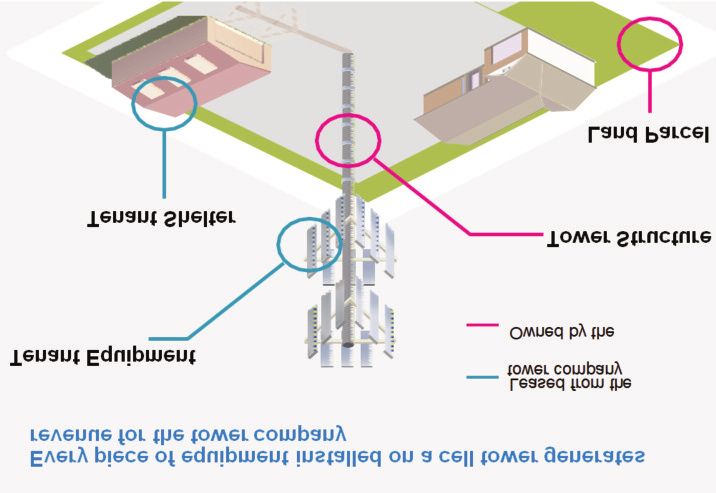

23 | FORBES REAL ESTATE INVESTOR | AUGUST 2019CELL TOWERS: THE CORE OF 5G Tenants

Cell towers are the physical foundation of nearly all wireless • Wireless carriers (Verizon, AT&T, Sprint, T-Mobile)

connectivity. Tower companies own the vertical real estate— • Government agencies (police, emergency medical services)

usually a tower or pole—often with the land parcel underneath • Broadband data providers/cable companies

and the dark fiber cable underground. Wireless carriers lease

space on the tower to mount equipment such as cell transmitters Barriers to supply: Two major barriers stand in the way of new

or antennas. In addition to these traditional towers (known as entrants into the tower business, starting with local zoning

macro towers), tower companies may own small-cell nodes, restrictions. There is a legacy of municipal opposition to new

designed for short-range, high-frequency 5G signals. towers, enforced under “eyesore laws” designed to protect

property values. This often induces carriers to install equipment

Company Examples on existing towers to avoid drawn-out zoning battles. Secondly,

• American Tower (AMT): Converted to a REIT in 2012, tower customers tend to be sticky, rarely moving equipment

surpassing Simon Property Group (SPG) as the world’s between tower operators. So new market entrants have fewer

largest REIT by market capitalization. potential customers to target in a market where an incumbent

• Crown Castle International (CCI): Converted to a REIT in tower company is already in operation.

2014, with roughly 40,000 towers and 60,000 route miles of fiber

across the U.S.; America’s largest operator of small-cell networks. Cash flow profile: Cell tower leases typically start at ten years

• SBA Communications (SBAC): Owns tower assets in all 50 with rolling five- to seven-year opt outs. Tenants have

states, throughout Canada and in Central and South tended to experience a 98%–99% renewal rate upon

America; filed as a REIT in 2016. expiration, resulting in relatively stable cash flows for the

24 | FORBES REAL ESTATE INVESTOR | AUGUST 2019You can also read