ZARA TECHNOLOGY: GO TO MARKET STRATEGY - Version 1.3 5/20/2008

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

ZARA TECHNOLOGY: GO TO

MARKET STRATEGY

Version 1.3

5/20/2008

Professor Arun K. Jain prepared this case solely as the basis for class discussion rather than

to illustrate either effective or ineffective handling of an administrative situation. This case

was made possible through the generous support of Zara Technology Pte. Ltd., Singapore;

SIM, Singapore; Spring Singapore; IDA, Singapore; SUN Microsystems, Singapore; SingTel,

Singapore; 1-Net, Singapore; Chee Fatt Co. Pte. Ltd., Singapore; Matco Asia Pte. Ltd.,

Singapore; Singapore Department of Statistics, Singapore; Center for Entrepreneurial

Leadership, School of Management, University at Buffalo; and Samuel P. Capen Professorship

in Marketing Research Funds. The author made extensive use of published information about

the industry and acknowledges contributions of numerous IT experts playing a critical role in

the development of the IT industry.

© 2008 Arun K. Jain, Executive MBA Program, University at Buffalo, New York, 14260.

1

Zara Technology: Go to Market Strategy

It was a balmy morning in September, 2007 as two entrepreneurs, Francis Lim

and Christopher Harvey, were sipping their robust Singapore Coffee with Kaya butter

toast at the nimble office of Zara Technology. Chris, the Group CEO and computer

wizard, fired his Apple and instinctively logged on to listen to the Podcast of Eweek.com.

AMR Research’s President and CEO, Tony Friscia, and Chief Research Officer, Bruce

Richardson, were discussing the resurgence of the enterprise software market and its

affect on small and medium-sized businesses:

Hi, I’m Tony Friscia, CEO of AMR Research, and I’m here with

Bruce Richardson, our Chief Research Officer. Bruce, I wanted to talk

today about the overall technology economy because clearly what we’re

seeing is a resurgence in many ways.

………..Tony, most of our listeners, uh, today, are small, are

executives at small or mid-size companies. I think that they’re looking to

invest in probably two areas. One is in driving efficiencies in their

business, and this is leading to huge investments in software as a service.

The second thing is continuing to invest in productivity tools, and this is

leading to small and mid-sized companies spending a lot more money than

they have in the past on Blackberries and other devices that allow

employees to sort of be in touch 24/7 to the business, and I think those are

sort of two critical trends.

One thing that’s happened when we look at the small to mid-sized

players, five or six years ago, we kept hearing the internet changes

everything. When you look at the big spending in the late ‘90’s into 2000,

it was largely driven by the mega-companies, the big companies making

multi-hundred million dollar investments in software and new

infrastructure. What the internet has really done now is open the door for

the small and mid-sized companies to get into the game.

On the business systems side though, I’m not convinced that the

large companies, SAP included, can do it organically that, I think that

what you’re going to have to do is buy a market leader and move into this

space, and one of the things I’ve always questioned I mentioned earlier

that, Oracle’s Larry Ellison owns, you know, three-quarters of Net Suite,

does that become Oracle’s play within the mid-market? Do they buy a

company like Net Suite? I think it’s way too hard for a fifteen-billion or

an eighteen-billion-dollar company to try and guess what the needs of a

small or mid-sized company are. It’s just a much more different market

and perspective, and the channels are completely different, so I think

you’ve got to buy the channel capabilities, I think you’ve got to buy the

product, you’ve got to buy the easy-to-use technology, you have to simplify

the message. Small and mid-sized business owners, they don’t know what

you’re talking about if you start talking about grids and APservers and

XML and Middleware and Vizdal. You’ll send them running from the

building if you start talking about things like that. You have to talk about

2

business value, you have to talk about cost-effective operations, and you

have to talk about productivity.

I was talking to Greg G. in Forte who is the founder and CEO of a

company called Right Now Technologies which provides on-demand

software or software as a service for managing customer services types of

applications. He has a mix of on-demand software and on-premise

software meaning that it runs on the server in his IT shops, and he woke

up one day and said, you know, “This is crazy”. “Here I am building a

global presence.” He said, “I have more people in my internal IT group

than I have in my externally-facing customer support group”. He said, “I

got, you know, we just have to stop the nonsense here”, and I think you’re

right. As a small business owner, what you’re looking to do is invest in

the areas that are critical to you, and you want IT functionality. You don’t

necessarily need to build a huge IT staff to be able to get at that. What

you want is innovation, not complexity, and not a bureaucracy or not

another layer of support in there, and I think software as a service has an

incredible future ahead of it.

Chris and Francis were elated and concerned about what to do as they absorbed

implications of the comments of Frisca and Richardson. Their intuition was right, a big

opportunity awaited Zara in the market for backroom data management for Small and

Medium Size Enterprises (SMEs). “We needed to decide where and how to position

ourselves in this emerging market” explained Francis. Chris and Francis wondered how

they should enter the market. Throwing his steel tip dart on the big regulation-size

Piranha dart board, “Waiting is not an option for us,” said Chris. As Francis picked the

second dart, he said, “We need to hit the eye of the fish.”

The Market for Business Data Management

Early in the ‘60’s as main-frame computers became ubiquitous in the corporate

world, software was developed to help businesses achieve efficiency and competitive

advantage in the market place through inventory control. Systems software was designed

to handle inventory based in traditional inventory concepts. The initial success of such

applications led to a shift of focus in the 1970’s towards MRP (Material Requirement

Planning). In the ‘80’s, this software encompassed the role of manufacturing resource

planning to optimize plant production processes. In more recent years, such software has

sought to integrate all departments and functions across a company into a single

computer system. Commonly referred to as ERP (Enterprise Resource Planning)

systems, at an average cost of over $15 million, large businesses use ERP software to

capture data about historical activity, their current operations, and future plans to develop

strategic options in market place. According to Forrester Research, most large companies

and governmental organizations have committed to one or other ERP systems and the

market for ERP systems has achieved a “high level of maturity”. As the growth in

market for large businesses is slowing down, attention is shifting towards newly

emerging economies and smaller businesses. As such, a battle is brewing for the growing

small and medium-size ERP business application market.

3

Software for SMEs

With the success of ERP at large businesses and wide availability of inexpensive,

PCs, SMEs also started integrating computers to better manage their enterprises. A wide

variety of business application software is available for use by SMEs. They differ in

terms of functionality, required user expertise, hardware requirement, comprehensiveness,

integration with internet, connectivity with other software, and cost. Besides, numerous

industry specific software (e.g., Parking Lot Management for managing parking lots) are

available which focus on the needs of a specific industry. At the lowest level, a small

business may elect to use the standard Microsoft’s Office Suite (or the free OpenOffice

from the open-source project) to manage their books using the spread sheet, writing,

drawing, presentation, and data storage features. Except for preparation of very simple,

basic documents, presentation, and spread-sheet, prospective users require significant

expertise in computing to develop specialized modules for performing managerially

critical repetitive tasks.

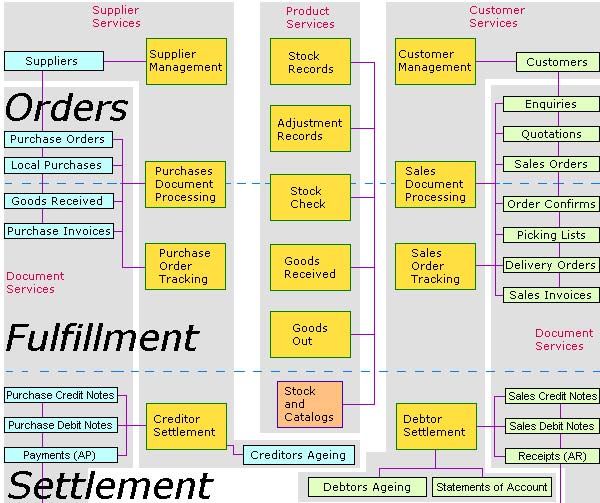

A popular option among SMEs has been the use of accounting software to

computerize accounting related functions. These functions include identification of

accounts receivable/payable, maintenance of general ledger, billing, keeping record of

inventory, and management of purchase/sale orders. Such software serves as an

accounting information system which can be used to perform accounting audit and

prepare tax returns. Developed internally or acquired externally, most offer optional add-

ons which can perform functions such as payroll, debt collection, response to inquiries,

maintenance of employee timesheet, etc. Most are bought off the shelf with the buyer

responsible for implementation. Many, such as Quicken, have “certified” experts who

can assist the buyer in implementing the software. Often, this task is performed by the

CCA (equivalent to a CPA in the US) as an add-on service or gratis in anticipation of

future revenue. According to Wikipedia, users can normally expect on paying roughly

50-200% of the price of the software in implementation and consulting fees. Table 1

provides a comparison of the top 10 accounting software developed by TopTenReviews

(A more exhaustive comparison is provided by Wikipedia.)

A third option is primary function plus, where a prominent software developer

invites smaller, lesser-known software developers to develop missing functionality in

their software. Thus, for example, SalesForce, software developed for managing

customer relationship (CRM), invited independent software developers to design

software for functionalities missing in SalesForce, e.g., finance and accounting, project

management, inventory control, etc. Towards this, a platform is created (e.g.,

Appexchane for SalesForce) where such add-ons are listed. Thus, instead of the

software company investing their own resources to develop full-fledged ERP software,

others are asked to supplement the missing features. It is accomplished by creating an

Application Programming Interface (API), and providing developers with a free Software

Developer Kit (SDK). The specific functionality and its implementation are left to the

developer while integration with the parent software becomes the responsibility of the

user. Thus, an SME with little or no IT background and resources is left with the task of

4

selecting from among hundreds of independent software to perform critical business

functions and integrating it with the parent software. The three leading single function

SME oriented software are : SalesForce, PeachTree, and QuickBook .

A fourth option is to buy an ERP type of software dedicated to SMEs. The

leading software is NetSuite. Although it was initially launched under the name of

Oracle Small Business Suite to benefit from the brand equity of Oracle, it has no

technical relationship with Oracle with the exception that Oracle’s CEO, Larry Ellison, is

a major investor in the company. NetSuite can be accessed over a Web browser which

permits users to log on the system from anywhere internet is available. Furthermore, it

permits all employees to access business data in real-time. The data is backed up every

night at a central site. There are no upgrades to buy, and thus need for maintenance on the

part of the customer is eliminated. Smelling the aroma of opportunity, Oracle launched

E-Business Suite Special Edition (EBSE) at a price tag of about $100,000. It is a watered

down version of their E-Business Suite which allows small companies to manage

financials, inventories, purchasing, and sales orders. The target market for EBSE is a

company with 100 to 500 employees and sales revenue not exceeding USD $250 million.

Meanwhile, Microsoft has packaged their family of Microsoft Business Solutions as

Dynamics to cater to SMEs. Not to be left out, SAP purchased TopManage Financial

Systems, an Israel -based developer of business applications and branded it as SAP

Business One. Borrowing from the strategy of single function software, these ERP

packages are also offered in unbundled versions (i.e., user can get single function

software) and permit third party add-ons to their software. For example, a business may

adopt NetSuite as the main platform but could elect to use Onsite developed by Another9

LLC to automate their point of sale activities. A comparison of the leading software

offering single functionality and ERP is provided in Table 2.

Over the years, NetSuite has been bundled and re-bundled in six different

versions/platforms: NetSuite, NetSuite Small Business, NetSuite CRM, NetSuite CRM+,

NetERP, NetCommerce, and NetSuite Limited. The various incarnations of NetSuite

differ primarily in terms of the functionality offered and the usage fee.

User Experiences

Discussions in the US and Singapore with SMEs, System integrators (SI),

government officials, and content analysis of User Forums offers valuable insights into

SME concerns and evaluation of current options in the market place. In general, first,

there is significant concern regarding the cost of acquiring and using the software.

SMEs find the usage cost of ERPs to be high. Comments such as: “NetSuite came back

with $20,000 for 3 years of license. In all, these companies who are pitching their

solutions for small and medium companies are not realistic”, “$60,000 is not an

enterprise-wide deal for a fortune 1000, but, at the same time, it's not a solution you are

going to get many 10-persons, 2-year-old companies to bite on”, “While I did like the

iCode software, they just lost me with pricing”, “They just don't seem to understand that

a 2-year-old business with 7 employees cannot invest $40-50K in software and then

5

spend another $10-15K on hardware and implementation. I believe someone over there

needs to recognize that there are companies like us who want a full soup-to-nuts solution

for 10 users for $10-15K”, “NetSuite was impressive but we needed the complete version

and price quickly added-up. Over a 3-year period, we expected it would cost

considerably more than iCode. If we added more staff than expected, it's per user/per

month/year-after-year cost would outstrip a purchased license even quicker”, “NetSuite:

pretty much the same experience as SalesForce. Multiple pushy sales reps. I really

wanted to buy this software at the beginning - it looked perfect for us. But the attitudes of

the reps and the avoidance of quoting prices just made me feel I was being lined up to be

suckered”, “”the cost to add on new licenses or modules is very expensive”, “I see that

NetSuite raised their price for their "distribution" edition yet again from $399/mo for the

first user to $999/mo. Given their triple digit yearly price increases why would anyone

want to take a chance on giving the complete control over their system?”, “They have

been raising the fees to users so much each year (latest increase from $399/mo first user

to $999/mo first user)”, “I suspect that there are very few companies with 1-25

employees for which NetSuite, Oracle, SAP and the like are appropriate or economical.

Just yesterday I spoke to one of our new users who left NetSuite because it was much too

complex and because they were charging him $600 per month for one user”, “Why do

these software guys think you'll go from a few hundred dollars for QB [Quick Book] or

PT [Peach Tree] to $50k or more?”, “Why should anyone need to purchase version

upgrades, if the version they're using now works just fine? If the version they're using

now doesn't work fine, why won't the S/W Company fix the problems? These things

(forced upgrades) are just a mechanism to introduce artificial scarcity into a marketplace

to generate more income” express concerns regarding high (a) base cost, (b) additional

user cost, (c) price inflation in later years, and (c) upgrade cost. There is also concern

about lack of software ownership and future inflexibility to move to different software:

“If I buy a software package, and the vendor refuses to give me the source code or easy

access to my data at any time, then migration to a different package is difficult.”

Second issue deals with the cost of implantation/adoption of the software.

Users, particularly those not competent in IT or lacking time/trained personnel to

implement are either reluctant to adopt a system or become frustrated. Comments such

as these are frequently made: “...As do all the software companies, sell licenses at 20% of

the list and make your money on the services. The fact they would not do that sent me a

message that they are not really out there for the small business like us, they want the

medium sized businesses”, “Implementation costs had doubled and they wanted over

$16k with a possibility it could hit $20k. I was going to go ahead, but they were booked-

up till early '05. We called them early in Jan. Now, they wanted to send a new quote! It

came in at $37k not counting the add-ons we still needed. After adding those, the bill

would be $45k with more due for the 2 new seats I wanted by that time”, “You can't get

any service or qualify for the annual maintenance plan until you pass a 23 page exam

and pay them $2700 per try for a remote system-analysis performed by their engineer

until you finally pass (probably after you've spent thousands more guessing what you'll

need to fix)”, “.. they wanted $5,000 plus for unlimited support and maintenance on 10

seats per year. I am an experienced user and don't need that sort of hand holding”, “We

paid more than $100K for an iCode "implementation" and we are still not up and

6

running more than two months after our scheduled completion date. All attempts to work

with iCode to try to fix the situation have been met with a "not our problem" attitude, and

their proposed solution to every concern has been to ask us to pay large additional fees.

They are also very specific about letting us know that despite their recommendations and

regardless of what we spend, they will not provide any guarantees that anything will

work”, “the cost to add on new licenses or modules is very expensive (we were able to

negotiate a great price for the first 10 licenses, yet their costs to add more licenses and

modules are absolutely crazy)”, “fail to recognize (as do many other vendors) that a

$50,000++ initial investment + training, hosting and maintenance fees is a very large

investment for a $2million company”. According to industry experts, SMEs often to turn

to ERP as a method of planning for future growth, and it tends to be a watermark project

for many. "These companies are often smaller, with less experience, and it’s often the

first major project they’ve done on their own,” said Maria E. Anzilotti, vice president and

CIO at Camden Property Trust, a real estate construction and management company in

Houston. "It is a bit of a challenge." Among the issues: many IT employees lack

experience in large-scale implementations such as these, while subject matter experts

(SMEs) on the business side of the house are already strapped for time and find it

difficult to get heavily involved in ERP. "What makes this different for SMEs is the

limited SME time, and how to scale ERP as the business grows while being cognizant of

budget”, said Tom Cullen, CIO at Peet's Coffee & Tea Inc. in Emeryville, Calif. "We

can't build a 30-person development team to run ERP.” According to industry experts,

ease of use, acquisition cost (subscription cost) and cost avoidance are important criteria

for selection of an ERP system.

Inability to easily upgrade from accounting software, integrate with different

software, and lack of comprehensive functionality necessary for business functions

are also mentioned as a critical limitations of the currently available software. It is not

unusual to hear comments such as: “One size doesn't fit all... being a hosted solution you

lose certain functionality such as POS, which is sole functionality requirements for retail

industry”, “the technical support basically doesn't exist. The downloadable software

used for integration with Microsoft Outlook is not compatible with Windows Vista or

Microsoft Windows Mobile 5.0/6.0, which means you have to pay for an extra service to

access data through your mobile phone. The representative neglected to mention this,

even after explaining that it was an interregnal part of my business”, “when I asked the

sales representative if certain things could be done using NetSuite, he replied simply,

“Yes, they can be done” but neglected to mention it required scripting”, “be careful with

NetSuite. They have a technologically beautiful system, but we discovered alarming

errors, omissions, and shortcomings. To make a long story short, they signed us up

cheap, made clear promises that they failed to deliver, and attempted to raise our

renewal fees at alarming rates”, “my impression was they are only interested in fast sales

and don’t have the internal or external resources to modify the program to suit the

client”, “the deal killer was that it had no facility to generate quotes/order/invoices

online”, “a little nervous to base our company functions on a package that is largely

developed and is supported out of India”, “they currently do NOT work with outside

analytics software because they have an advanced analytics package of their own, yet

their analytics cannot provide us with accurate ROI on our PPC campaigns”, “Software

7

packages for small businesses solve limited issues and leave you with multiple islands of

data and expensive integration projects that never work. Information has to be manually

re-entered or batched into other applications—wasting time and money.”

There is also concern about lack of software ownership and future inflexibility

to move to different software. Typically, SMEs raise concerns such as: “If I buy a

software package, and the vendor refuses to give me the source code or easy access to my

data at any time, then migration to a different package is difficult”, “With companies

such as NetSuite and Microsoft, customers can't switch to another vendor because the

current vendor makes it difficult to do so (thus removing the customer's Perfect Liberty,

and disobeying the laws of the free market)”, “You’re locked into Netsuite with no

portability out of NetSuite once you moved your business on to their platform. They

control you’re operational costs, when you upgrade and what you can do with every

aspect of your business accounting, inventory and ecommerce. Most businesses cannot

afford to give up that much control”, “a little nervous to base our company functions on

a package that is largely developed and is supported out of India.”

Despite their promotional campaigns, many small businesses users believe that

major software vendors do not adequately address their needs. SMEs frequently

lament: “Microsoft talks about SMB [SME] having fewer than 50 PCs. IBM pegs it at

100 to 1,000 employees, Oracle at $500 million or less. But what about the one-person-

part-time companies, and those with up to 10 or 15 employees?”, “NetSuite and Everest

are totally inappropriate for companies like [these]. They need tools that are designed

for the way they do business, and priced within their budgets”, “Anyone who serves the

tech needs of "small business" needs to be able to help that small business owner define

his or her tech needs in terms of industry and size -- and do so in business terms, not tech

jargon”, “I suspect that there are very few companies with 1-25 employees for which

NetSuite, Oracle, SAP and the like are appropriate or economical”, “NetSuite .. [is] not

a solution you are going to get many 10 person, two year old companies to bite on.”

Above all, there is persistent fear among SMEs of losing control of proprietary

information, particularly financial data, should the information be placed off the

premises. There is also concern regarding virus/worm attacks and

hacking/information theft. Most small businesses lack IT personnel and computer

skills (and time to attend to IT functions). Owners fear that a virus attacks will force

them to shut down their business resulting in loss of business. Hacking could result in

loss of customer financial data (e.g., credit card numbers, bank account numbers) causing

serious problems with their customers. Keeping information on computer data base also

opens the possibility of rogue employees stealing information to sell to competitors

and/or establishing a competing business of their own. Concern is also expressed

regarding potential for disconnection (denial) of service due to high traffic in the

system. This happens when simultaneously lot of high end activities happen on the

network. In such situations, local routers put on the premises of SMEs are unable to

handle the traffic resulting in a jam and hence requiring frequent restart of the system, a

pain for unsophisticated SMEs. However, it is well understood by SMEs that these issues

are not directly related to any specific software, they are part and parcel of going digital.

8

SMEs frequently advance these as rationale/concern when making decision to go digital.

They express need to balance these concerns against increasing pressure from both

suppliers and customers for web presence and computerization of their business

operation. Large suppliers increasingly want access to inventory related information on

the web to replenish stock, process orders, settle bills, and capture up-to-the-minute

information about sale trends. Similarly, large customers want to bypass sales staff to

directly view inventory levels, progress on orders, find price, place orders, and settle

bills. “If we ignore our customers and suppliers, we will become history,” observed

president of a small wholesaler, “but I don’t have the resources to do what they want. I

am caught between a rock and a hard place.”

The Company

Zara technology was formed in 1997 by two entrepreneurs, Francis Lim and

Christopher (Chris) Harvey. Born in England, Chris is a technology wizard and straight

arrow shooter. In 1984 he obtained his degree in computing Science at Staffordshire

University, England and faithfully joined the PhD program in Computer Science at Aston

University, Birmingham. Dissatisfied with the pure academic orientation of Aston and

finding himself in the midst of sea of opportunities in the industrial town of Birmingham,

Chris quit the PhD program in 1986 and, with two associates, formed his own company,

Bright Associates Limited. It followed by formation of three additional companies,

Binary Star Ltd, Veytan Enterprises Pte Ltd, and Harvey Software Pte Ltd (later

renamed as Zara Technology Pte. Ltd.), each focused on serving the needs of small and

medium sized enterprises. In each venture, Chris was the technical guru behind the

organization contributing cutting-edge technology. He learned about “open-system” in

software design and became a champion of it. Chris moved to Singapore in 1993 and

experienced how co-workers could fleece unsuspecting partners. While working as a

principal of Veytan, Chris met with Francis Lim, a Singapore based entrepreneur who

had a housing rental business, MacKenzie Housing Services, Pvt Ltd. MacKenzie with

an employee base of 30 was growing fast and needed to move beyond a spreadsheet to

effectively manage their backroom data base.

Francis Lim was born with a silver spoon in his mouth in an affluent Singapore

family. Lims had numerous business interests with annual revenue of over S$200

million. They lost everything during the energy crisis of the 70’s. With nothing left, the

Lim family had to live literally out of their suitcases through the generosity of friends and

relatives. Francis managed to obtain undergraduate degree in Economics from Indiana

and worked for seven years as a bond and foreign exchange trader in Singapore with

frequent overseas stints. Later, he obtained his MBA from University at Buffalo in 1993

and returned to Singapore and launched his accommodation service business. He quickly

built it up to a $10 million revenue base only to be confronted with the Asian financial

crisis when he was forced to shut down the business and in the process lost his highly

leveraged home.

Ever an entrepreneur, Francis joined with Chris to tightly focus their attention on

the SME market. “I knew the market and experienced the consequences of not having

9

access to any software to help me. I was forced to use a patchwork of unworkable

software secured from a variety of suppliers. I figured, I was no exception and other

SMEs must be facing similar challenges. If we could develop something which will meet

the needs of this large neglected market, we could be winners,” recalled Francis. As the

Asian financial crisis faded, Francis brought in several external angel investors and, with

Chris as in charge of technology, Zara started developing Window based software, later

christened as SteelClaws (SC), to help SMEs. Francis became the business face of Zara,

concentrating his energy on marketing and finance while Chris was focused on the design

and development of software. “We did not take just any client who called us. Instead,

we focused our attention on those SMEs where we could learn about their business

operations and procedures. We wanted to fully integrate ourselves into the operations of

our clients so that we may develop software which reflects their needs and not our

theoretical vision,” explained Francis. The Dot Com bubble of 2000 convinced Zara that

they needed to move to an internet based software. “We saw how the legacy software

companies were collecting huge licensing fee from users. On top of it, they imposed

requirements for expensive hardware. It increased the usage cost to SMEs by some 40%.

This shrunk the number of potential customers.” The entire software was re-written in

the open source Java promoted by SUN Microsystems. Instead of hiring a permanent

staff, Zara outsourced portions of the coding work overseas to contacts of Chris in

England and others in Asia and thus kept their payroll very lean. The burst of Dot-Com

and outbreak of SARS in Asia slowed down business in Singapore and that of Zara. A

decision was made to cut cost by shifting operations from a rental facility to their home.

As Singapore was emerging from SARS, Zara embraced Web 2.0 promoted by O'Reilly

Media. It had the attractive feature of ability of users to work with the data stored on

servers. “We figured this feature could eliminate the need for PCs for the users of SC

and provide better protection to them against viruses lurking on the web,” said Chris.

“We also wanted to wring out any excess fat from the usage cost of SteelClaws.”

A New Approach: SUN Ray Thin Client

In 1997, Oracle chief executive Larry Ellison and SUN Microsystems' chief

executive Scott McNealy proposed thin client computer as a replacement for the

corporate PC. They envisioned a client device which will be used to access applications

and information running on a back-end server. Towards this, in September, 1999 SUN

launched Sun Ray I aimed at corporate environments.

10Figure 1

SUN Ray I

Source: Sun Microsystems

It featured a smartcard reader which was connected to a flat panel display, a key

board, and mouse. Sun Ray I was connected via an Ethernet network to a Sun Ray

Server on which resided all the software and hard drives to store data. Sun Ray Server

Software (SRSS) was offered for the Solaris Operating System and Linux. Rather than

using the X Display protocol, SUN developed a separate secure bitmap-based network

protocol Appliance Link Protocol (ALP) for the Sun Ray system.

The server was connected to internet via LAN. In order to perform any operation,

all a user had to do was slip in the card, enter their password when prompted, and they

were able to perform any operation they would otherwise do on a PC. In the background,

applications run on the server with the results displayed on the quiet monitor. Sun Ray

made any session portable. The users could move from any Sun Ray client to another

and resume their desktop sessions with instant right-where-they-left-off access. SUN

asked the potential users to “think of freezing live TV and then driving to your friend's

house to restart the program in the exact same spot.” Just, “you pull your ID card out of

one Sun Ray Client without saving or pausing anything on your desktop and move to

another Sun Ray Client—across the office, down the hall, in the conference room, or

across the ocean, wherever there’s an authorized network connection—without losing a

single thing.” Without the smartcard, the procedure is almost identical, except the user

has to specify their username as well as password to get their session. In either case, if a

session did not yet exist, a new one is created the first time they connected. SUN Ray

provided multi-channel audio and video input and output capabilities. Dubbed as SUN

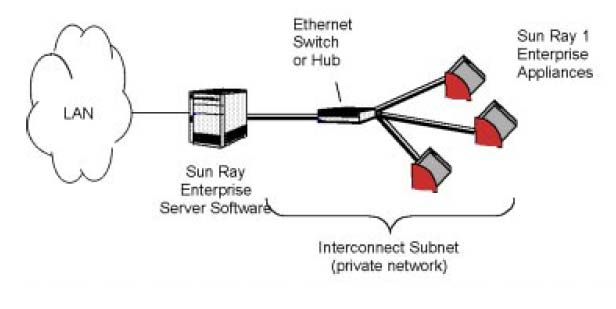

Ray enterprise system, it was essentially a Solaris server running the SUN Ray Enterprise

server software. The system provided the user access to all Solaris applications including

11those based on Java. The following represents a schematic of the SUN Ray Enterprise

System:

Figure 2

Schematic of SUN Ray Enterprise System

Source: Sun Micro Systems

The system had limited success. In addition to a lack of Windows support,

network latency proved to be a technical hurdle. It caused a time delay between a user’s

command and the actual response on the screen. When a window was dragged to a new

position, for instance, it took a short while before it actually moved on the screen because

the command and response had to travel through the network.

In 2006, SUN unveiled an ultra-thin version of its SUN Ray, SUN Ray II:

Figure 3

SUN Ray II

Source: SUN Microsystems

12SUN Ray II won the prestigious 2007 innovations Design and Engineering

Award given by the International Consumer Electronics Association for environmentally

friendly design and use of environmentally sustainable technology. Network Computing

bestowed upon it the Well-Connected Award for Best Design, Innovation, or

Enhancement in the Network Infrastructure category at their 12th Annual conference.

Unlike the previous incarnation, SUN Ray II provides instantaneous, seamless access to

users operations without any delay. Sun Ray Software enables users to display full-

screen Windows, Linux and Solaris OS desktops on the monitor. With Sun Secure

Global Desktop software, users can access all other types of legacy applications, such as

those running on HP-UX, AIX, mainframe, and midrange systems. So, whatever the

users operating environment or application needs are, they can access and display just

about anything on a Sun Ray Client. Priced at $249, it offers an inexpensive alternative

to a Microsoft Environment. The Smart Card used with SUN Ray II costs approximately

$10.

SUN Ray II offers a big contrast to the traditional Window based PCs used by

SMEs. It offers significant cost savings since there is no need to pay for the hardware

(e.g., hard drive, memory, etc.) and software (e.g., operating system, application

software) needed for each PC user. Instead, the user only needs a monitor, keyboard, and

a mouse. The power consumption by SUN Ray II is only 4 Watts- about 5 percent of a

PC. Sun Ray II client doesn’t produce as much heat or require the noisy fan of a PC.

It’s silent and runs cooler, which improves reliability. Any updates in the software are

installed on the server thus eliminating the time and cost of installing and maintaining

desktops. Users can unpack a Sun Ray device, plug it in, and be running in minutes,

without administrative assistance. Theirs is no need for the System Administrator to visit

the user desk—for maintenance or administration—unless the entire unit needs

replacement, indicated by a status light. An administrator can manage from a central

location 1000 Sun Ray II clients almost as easily as one unit.

A Sun Ray Client contains no resident operating system or applications, which

makes it virtually immune to viruses and service attacks. Since a Sun Ray terminal

doesn’t contain a disk drive or any means of persistent data storage, it’s not an attractive

target for theft. All of the data and applications displayed on screen disappear the instant

the client is turned off or the access card is removed. Firm’s intellectual property can be

secured by eliminating access to USB mass storage devices. The Administrator only

needs to secure the server. Using internet a user can access the Sun Ray Enterprise

system from any corner of the world via telephone, satellite, or cable.

13Figure 4

Schematic of SUN Ray Enterprise System

Source: SUN Microsystems

Hundreds of schools, colleges, universities, and libraries around the world are

deploying Sun Ray technology. It is particularly well suited for cost-sensitive

environments such as call centers, education, healthcare, service providers, and finance.

Verizon wireless has replaced thousands of call center PCs with Sun Microsystems’ thin

client terminals. With about 5,000 Sun Ray terminals installed at three Western call

centers, and a fourth in progress, Verizon has seen a 60% to 70% drop in desktop

problems and a 30% decline in electrical use at each center. The carrier plans to keep

rolling out Sun Rays in new and existing call centers. SUN Microsystems has partnered

with General Dynamics (formerly Tadpole), Naturetech, and Accutech to manufacture

laptops which can serve as SUN Ray II mobile work stations using smart cards.

14Figure 5

Work Stations for SUN Ray Enterprise System

Gobi 7 Portable Thin Client Naturetech 747 Unix

For SUN Ray by Accutech Portable Work Station by Naturetech

Comet 12 Portable Work

Work Station by General Dynamics

Since 1999, thin clients market has grown steadily. According to IDC, total sales

of thin client PCs in the Asia/Pacific, including Japan (APJ), market reached 279,513

units in 2005, representing an increase of 64 percent over the previous year. Revenue

increased 65 percent over the same period. IDC expects IT managers across the region

to consider thin clients as desktop PC replacements, helping drive a compound annual

growth rate of 34 percent through 2010. In terms of market share, according to IDC,

Wyse leads APJ sales with 35% share in 2005, followed by HP with 16%, VXL with

10%, and Changchun Xinyu and HCL both with 8% share - the latter two vendors

garner most sales from the PRC and India.

15According to analyst firm IDC, the worldwide market for thin clients is gaining

momentum. The devices make up less than 1 per cent of overall desktop shipments, but

are growing twice as fast as PCs. The analyst firm projected last year that by 2008, thin

clients might account for a 10 per cent share of the enterprise client market. Although

SUN Microsystems was a key player in the promotion of thin computing and SUN Ray

offers real advantages over the competition, it has remained a minor player in APJ and

the world market. When asked, SUN executives in Singapore pointed out thin profit

margins on SUN Ray 2 as compared to other products in their portfolio as a factor

contributing to relatively modest number of units sold. However, given the increased

focus of SMEs towards IT to enhance their market place effectiveness, SUN has revived

their commitment to partner with companies who could help them sell more SUN Rays

and servers. During a strategy meeting with Zara Technology executives, Allen Lai,

executive responsible for the development of market in APJ and Jean Tee, Partner

Marketing Manager, reiterated that Zara Technology is an attractive partner in their

efforts to expand sales of SUN Rays.

SUN Microsystems

SUN Microsystems is a Silicon Valley based IT Company with a market

capitalization of $17.6 billion and sales revenue of $13.87 billion in fiscal year 2006-

2007. It was established in 1982 by three fellow Stanford graduate students Vinod

Khosla, Scott McNealy, and Bill Joy. It is active in more than 100 countries worldwide.

SUN is known as the developer of Java platform and Network File System protocol. It

has recently emerged as one of the leading proponents and contributors of open source

software. Its products include computer servers and workstations; storage systems; and,

a suite of software products including the Solaris Operating System. Open source refers

to the creative practice of appropriating software codes of others without payment of any

royalty and making public new codes written. According to market research firm IDC,

SUN commands 13% of the worldwide server market, trailing IBM with 31% and

Hewlett-Packard Co. with 28 %. Fortune magazine ranked SUN Microsystems as one

of the world’s most admired 350 companies in 2006. Zara Technology has been

designated by SUN Microsystems as a Principal Partner in Asia Pacific, including

Japan (APJ), region by meeting their stringent criteria for excellence as an IT solutions

provider for SMEs and by committing to tight strategic and technical alignment with Sun.

In 1999, SUN acquired the German software company Star Division and with it

StarOffice. In 2000 it created OpenOffice.org with the objective of providing free, open

source productivity suite for the world. Towards it, SUN released StarOffice as the

office suite by OpenOffice.org. The suite includes word processing, spreadsheet,

presentation, drawing, database, and other modules. The software uses the ODF as its

native file format and fully supports other common file formats (including Microsoft

Office). The software runs on all major platforms, including Windows, Vista, Linux,

Solaris, Mac OS X, and is available in over 100 languages.

As an international team of volunteer and sponsored contributors, the OpenOffice.org

community has created what is widely regarded as the most important open-source project in the

16world today. However, the technology reporter of the British newspaper, the Guardian, Mr.

Andrew Brow has questioned the so-called global effort: “Despite the open source rhetoric

…almost all the work on it is now done by about 100 full-time Sun programmers.” Although

himself a user of Open Office “long before it was usable,” Mr. Brown writes, “More than

50,000 bugs have been reported. And how many have been fixed by open source’s uniquely

efficient processes? According to the (public) bugs database, at last count, there were more than

6,000 unfixed bugs, and more than 5,000 feature requests.” Notwithstanding Mr. Browns

ranting, nearly 100 million users have downloaded Office Suite and thousands contribute to it.

As a matter of fact, according to the Yankee Group analyst Laura DiDio, the free Office Suite

has attained a 19% market share among the cost conscious SMEs. According to Prianka

Srinivasan, a market analyst for IDC, SMEs “... perceived open source technology as providing

better security compared to proprietary products.” The study also concluded that more SMEs

were using open source software as compared to large businesses. Although cost-efficiency

remained a key decision factor, according to Ms Srinivasan, SMEs were selecting open source

software due to their ability to fulfill their requirements for specific software functionalities. In

September, 2007 IBM joined Openoffice.org community to collaborate on the development and

promotion of the software. SUN Microsystems has partnered with General Dynamics (formerly

Tadpole), Naturetech, and Accutech to manufacture laptops which can serve as SUN Ray 2

mobile work stations using smart cards.

Data Center

A data center is like a bank vault. It is a safe storage space for data which are

constantly being accessed and modified. It houses computers system and all associated

components such as telecommunication system and data storage devices. It has

redundant or backup power supply, environmental controls, and security system (See

Figure 6):

17Figure 6

Schematic layout of an internet data center

Source: Sun Microsystems

A typical data center occupies one or more rooms in a building (Figures 7 and 8).

The room is partitioned into cages, with each cage belonging to individual user. Cages

have racks which contain servers, computers, and hard drives to store data.

18Figure 7

Data Center Building

Figure 8

Data Center Cages

Most of the equipment is often in the form of servers racked up into 19 inch rack

cabinets, which are usually placed in single rows forming corridors between them. This

allows people access to the front and rear of each cabinet (Figure 9)

19Figure 9

Data Center Access to Cages

Data centers typically have raised flooring made up of 60 cm (2 ft) removable square tiles

(Figure 10). These provide a plenum for air to circulate below the floor, as part of the air

conditioning system, as well as providing space for power cabling. Data cabling is

typically routed through overhead cable trays in modern data centers. Smaller/less

expensive data centers without raised flooring may use anti-static tiles for a flooring

surface.

Figure 10

Data Center Flooring

20Electronic equipments in a confined space generate significant amount of heat.

Air-conditioning is used to keep humidity within acceptable level. Generally temperature

is kept between 67 and 72 degrees Fahrenheit. Data centers often have elaborate fire

prevention and fire extinguishing systems so that a fire can be easily detected and

extinguished. Like a bank vault, access to the site is restricted to selected personnel.

Data Centers use Video camera surveillance (Figure 11) and permanent security guards to

protect centers hosting sensitive information. Data centers communicate with the

external word via networks running the IP protocol suite. To enable this, data centers

contain a set of routers and switches which transport traffic between the servers and to

the outside world.

Figure 11

Security Systems at Data Centers

While large corporations maintain their own data centers, many businesses,

particularly smaller ones find it more cost effective to store most of their computational

equipment and data at a third-party data center. It provides security at a very affordable

cost. The system servicing is also outsourced to cut down IT personnel cost. Outsource

companies keep personnel at such data centers to service systems of their clients hosted at

the center and thereby minimize their own cost and as such fee charged from their

customers.

Singapore

Country

Singapore is a diamond shaped island of 699 Square Kilometers located at the

southern tip of Malaysian Peninsula between Malaysia and Indonesia. It is slightly more

than 3.2 times of Washington D.C in terms of land mass. Singapore has a population of

214.48 million as estimated by 2005 census. It is a multiracial city state with a majority

population of Chinese with substantial Malay and Tamil Indian minorities.

The country is a parliamentary republic where a Prime Minister is the head of the

government. It has a multiparty system and an independent judiciary. Since its

inception, Singapore has been lead by People’s Action Party (PAP). Government

bureaucracy is managed by national Civil Service. A hallmark of good governance by

PAP has been relentless focus on service to the various constituencies and an uncorrupt

bureaucracy. This has spanned into a large bureaucracy organized to serve individual

constituencies within business community and citizenry at large. The Civil Service seeks

to attract the best and brightest in the country to serve the public at a salary benchmarked

with the private sector. Leadership is required to clearly enunciate the agenda and

measure outcomes as they believe appropriate. In terms of accountability, any criticism

of the bureaucracy, particularly in media, is vigorously defended. Leadership in civil

service is regularly rotated to infuse new blood and prevent possible encroachment of

corruption as a result of longevity of leadership in a decision making position. The Wall

Street Journal and The Heritage Foundation, Washington’s preeminent think tank, have

for over a decade tracked the march of economic freedom around the world with their

influential Index of Economic Freedom. Singapore ranks 5th out of 158 countries in their

Corruption Perceptions Index for 2005.

Relationship with Business

Singapore Government is generally considered to be pro-business, in a unique

partnership with them. One senior Civil servant has gone so far as to describe business as

government’s “customer.” Following the recommendations of the United Nation’s

Development Committee, in 1961 the Ministry of Trade and Industry (MITI) established

the Economic Development Board (EBD) to foster economic growth in the country. It

has served as “one stop shop” for international investors. EBD has been very successful

in its mission. Singapore is home to 3,000 multinational corporations (MNCs) from the

United States, Japan, and Europe engaged in almost all sectors of the economy. They

account for more than two-thirds of manufacturing output and direct export sales,

although certain services sectors remain dominated by government-linked corporations.

Despite its small size, Singapore is now the tenth-largest trading partner of the United

States.

Rewards of Government’s pro-business policies have been spectacular. Although

Singapore’s economy is small by global standards, it is a relatively rich country. In 2006,

Singapore’s GDP was US$141 billion with a per capita GNP of US $31,400. The per

capita GDP of the tiny island nation equals that of the four largest European countries

and is five times that of its nearest neighbor, Malaysia. Singapore’s economy grew at the

7.9% in 2006. In the face of increasing global competition, Singapore continues to build

on its core advantages--a good geographical location, developed infrastructure, a good

communications system, political stability and a disciplined workforce--while always

looking to develop new economic strengths.

22SMEs in Singapore

While MNCs have contributed significantly to Singapore's GDP, according to

Yasmin Aladad Khan, General Manager, DHL Express (Singapore) Pte Ltd, “it is the

Small and Medium –sized Enterprises (SMEs) that have been the building blocks of the

Singapore economy. Over three decades of export-led growth, they have helped make

Singapore a vibrant trading hub”. Singapore’s SME sector, comprising more than

135,000 local companies, employs up to half of the working population, generates over

one third of value-added in the local economy and contributes a over 25% of national

Gross Domestic Product. The National Committee on Singapore’s Competitiveness has

issued a clarion call to nurture locally owned SMEs, make them more efficient and

competitive in the market place. Focusing on the role of SMEs in national economy, Mr.

Png Cheong Boon, deputy chief executive of Spring Singapore said, “(SMEs) provide a

source of products and services to the domestic market, so we need them to be

competitive. Or else, Singaporeans will pay more for these products and services”. “And

if they are not competitive, they also cannot pay their employees well.”

The important role played by SMEs in Singapore’s economy is evident from the

recent data released by DP Information Group through its annual SME 500 publications.

It selected and ranked SMEs based on their audited financial figures i.e. Sales/Turnover

or Net Profit for financial period ending between June 1, 2004 and May 31, 2005.

Among the top 500 SMEs ranked in terms of sales, 53 companies (10.6%) have achieved

a turnover of $50 million or more. Furthermore, 30 (6.0%) of these companies have

average monthly turnover of above $5 million per month. (Table A).

23Table A

Performance of Top 500 SMEs in Singapore

SME Sales

Rank of

Company with Company

Total No Total Section Highest with

Total No of of Turnover Turnover Highest

BUSINESS CLASSIFICATION Companies Employees SGD '000 SGD '000 Turnover

Wholesale 194 5,417 5,993,972 $ 79,582.00 1

Manufacturing 90 9,483 2,184,644 $ 73,486.00 6

Construction 59 3,936 1,358,714 $ 50,072.00 53

Services 57 2,053 7,242,259 $ 65,022.00 18

Communication, Transport, & Storage 46 1,458 1,124,054 $ 64,304.00 19

Retail 19 742 571,544 $ 73,224.00 7

Property 13 335 476,818 $ 66,577.00 16

Finance 15 398 367,900 $ 54,780.00 41

Holdings 4 20 108,618 $ 52,911.00 47

Hotel/Food Establishments 3 452 57,225 $ 28,271.00 175

TOTAL SME 500 COMPANIES 500 24,294 13,485,749

Composition and Operation Characteristics of SMEs

According to the Economic Survey Series published by Statistics Singapore , an

agency of Singapore Government, in 2005 SMEs were distributed in the following

sectors of the economy:

Table B

Distribution of Business Types in 2005

Business Type Freq %

Whole sale (WS) 36121 26.04

Retail (RT) 19959 14.39

Transportation (TS) 9258 6.67

Accommodation (AS) 249 0.18

Food and Beverage (FB) 4476 3.23

Information and Communication (IC) 5733 4.13

Finance and Insurance (FI) 8440 6.08

Real Estate and Business (RB) 31159 22.46

Community, Social, and Personal Services

(CSP) 23310 16.81

24Economic Surveys of Singapore Department of Statistics further classifies establishments

within each sector in terms of the number of employees hired by the enterprise and their

realized revenue. Tables 3 and 4 present such breakdowns for 2005.

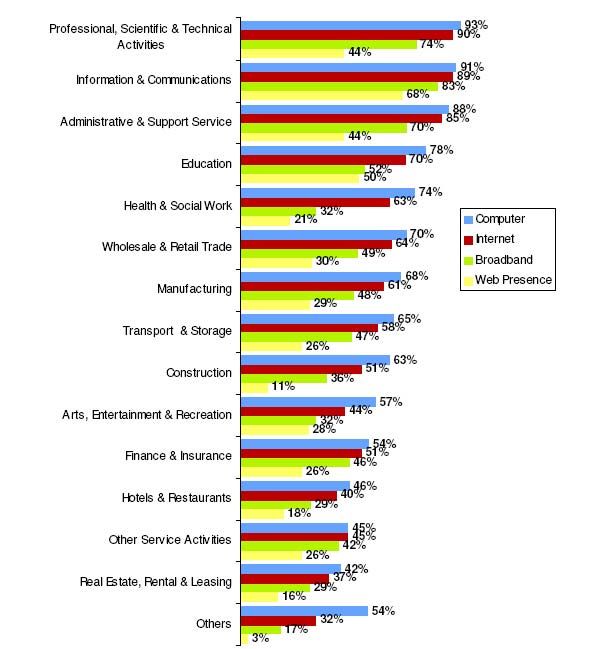

According to a study conducted by IDA in 2006, the extent of IT usage by SMEs

significantly differs depending upon the number of employees at the business. Figure 12

depicts such differences in terms of usage of computers, internet, access to broadband,

and web presence.

Figure 12

Information Technology Adoption by SMEs in Singapore

Adoption of information technology varies significantly across industries.

According to the IDA study (Figure 13); it ranges between 93% for professional,

scientific, and technical activities to a low of 42% among enterprises dealing with real-

estate and rentals:

25Figure 13

IT Usage by Industry Sector

Not surprisingly, smaller the numbers of employees at an SME, a higher proportion of

them use computer and internet for business purposes (Figures 14 and 15):

26Figure 14

Proportion of Employees Who Used the Computer at Work at least once a week

Figure 15

Proportion of Employees Who Used the Internet at Work at Least Once a Week

Besides e-mailing, as shown in Table C, Internet is primarily used by SMEs to deal with

government agencies in Singapore:

27Table C

Uses of Internet

Use Proportion of Companies

Broadband

Internet Narrowband

Internet Access Internet

1 For Sending or receiving mails 95.0% 90.4% 80.4%

2 For Information search 90.7% 87.6% 73.8%

For obtaining information from government

3 organizations (e.g. for web sites of via e-mail) 70.0% 68.8% 48.9%

4 For downloading or requesting government forms 67.5% 66.3% 48.3%

For completing government forms online or sending

5 completed government forms 60.5% 60.1% 39.7%

6 For banking and financial services 44.2% 45.8% 25.9%

For making online payments to government

7 organizations 42.0% 42.5% 27.8%

8 For placing orders for goods/ services 35.3% 36.4% 22.2%

9 For receiving orders for goods/ services 33.8% 34.8% 20.7%

10 For marketing/ promotion activities 32.8% 33.9% 18.2%

11 As a platform to deliver contents/ services 30.8% 30.8% 18.2%

12 For monitoring purposes 28.9% 30.3% 15.1%

13 For payment of goods/ services 26.8% 27.7% 16.2%

14 Other communications (e.g. instant messaging) 24.2% 26.6% 8.0%

For Finding information about employment

15 opportunities (recruitment and search) 24.1% 25.7% 10.5%

16 For telephoning over the phone (VOIP) 21.1% 22.7% 6.5%

17 For access collaborative tools (e.g. file sharing) 20.7% 22.3% 7.6%

18 For telecommuting/remote access 17.0% 18.3% 5.8%

19 For formal education or training activities 12.8% 13.5% 6.7%

20 Video-conferencing 10.9% 11.8% 4.0%

21 Video-streaming 9.7% 10.2% 4.1%

22 For rich media creations 9.2% 9.8% 4.8%

23 Internet Data Centre (IDC) services 0.5% 9.3% 3.9%

24 Blogging 7.8% 8.2% 2.7%

28You can also read