NTG Morning Comments www.nesvick.com - Wednesday, February 23, 2022 - Nesvick Trading Group

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Wednesday, February 23, 2022

NTG Morning Comments

www.nesvick.com

Weather

No big changes for the South American forecast. Still

looking at relatively limited precipitation in northern

Brazil with most areas seeing only near to below

normal rainfall over the next two weeks. Southern

Brazil will be dry today and early tomorrow, but

rainfall will return later tomorrow and after that we

should see an active pattern in place through at least

the end of the two week period. Eventually we should

see some above normal totals add up in RGDS and

surrounding areas. Today will be dry but tomorrow

morning we should wake up to find significant

showers and thunderstorms in Argentina. That

activity will kick off an active two week period with

the best rainfall amounts and coverage likely favoring northeastern portions of the country. 10-day

precipitation outlook at the right.

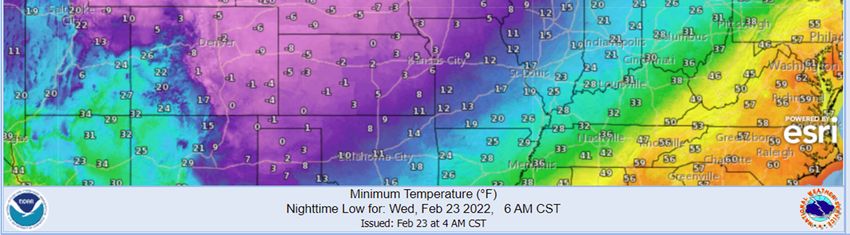

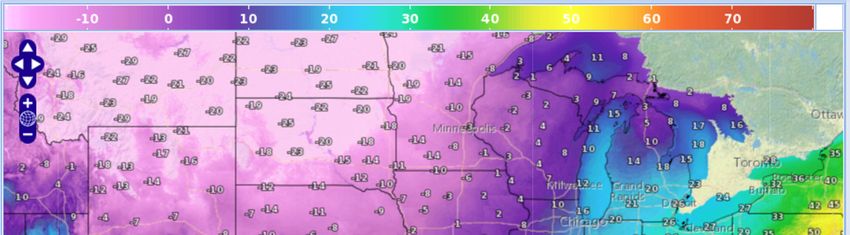

No changes to the US forecast either. Some snow in the ECB and into the Northeast while the Southeast has a

lot of precipitation on deck the next few days. The big story in the next 24 hours might be temps. Map below

shows low temps expected tomorrow morning, and note sub-zero lows dipping potentially into KS and maybe

even the OK Panhandle. Suffice to say there is no snow cover on the ground right now. I’m not one to get

worried about cold temps in the depths of winter, but the market might want to…

Crops

On Friday last week I broke down a few scenarios that pointed towards extremely big old crop soybean exports

based on the shortfall in production in South America this season. The “low” example pointed towards an

export total near 2,250 mil bu, which would be a full 200 mil bu larger than the current WASDE projection. I

1

Wednesday, February 23, 2022

NTG Morning Comments

www.nesvick.com

noted that I didn’t expect this year to be quite so strong, due mainly to smaller MAM exports relative to the

17/18 example cited on Friday. However, for the sake of argument let’s “pretend” that exports will wind up

being 100 mil bu larger than the current WASDE projection. What might that imply for calendar spreads?

The math is pretty simple…adding 100 mil bu to exports and keeping all else unchanged would give us a 225 mil

bu carryout equating to a 5% stocks/use ratio. The chart below plots the N/X spread vs. the June WASDE

stocks/use figure. The highlighted 2022 print takes the most recent Feb WASDE stocks/use. The chart is hardly

conclusive…at a 5% stocks/use we’ve seen several years with lower spread values and several years with higher

spread values. My bias would be to favor the higher side, however. For starters, I think there is a strong

argument that the final crush figure might be higher than the WASDE projection as well, further tightening

stocks/use. Even if the crush isn’t higher, however, we know crushers have good margins and can fight the river

for beans. We are likely to get to a point where the cheapest place for exporters to get beans will be through

the CBOT delivery mechanism…which leads me to believe that spreads will be supported from here. At a

minimum, I see very limited downside in N/X and believe a move close to 250 could be in the cards. Thoughts

appreciated.

End-June SN-SX Spread vs. June WASDE Stocks/Use

350 2013

300

2009

2014

250 2004

200

2022

SN-SX Spread

150

2012

100

2021 2010

50 2008 2016

2015

2011 2020

2017

2005

2018 2019

0 2006

2007

-50

-100 R² = 0.4962

-150

0% 5% 10% 15% 20% 25% 30%

June WASDE Stocks/Use

Livestock

A quick glance at the Cold Storage report numbers today…though there isn’t much new to report. I’ve got charts

showing total beef and total pork in cold storage below. Beef stocks are starting the year off at a very high level.

The last time beef stocks were this large at the end of January was 2017. That said, this is the typical timeframe

to see inventories contract, so again it does make some sense to expect seasonal beef strength to kick in at

some point in the coming weeks. No change in the trend on pork stocks. January inventories are up from

December, but as you can see below that is nothing unusual and we remain well under the norms of the past

2

Wednesday, February 23, 2022

NTG Morning Comments

www.nesvick.com

several years. Considering what appears to be a relatively weak export market, I think the interesting thing to

keep an eye on in the months ahead is to see if domestic disappearance is strong enough to prevent inventories

from building or if the soft export demand will finally allow us to see these inventories move back towards more

normal levels.

Beef in Cold Storage (Mil Lbs)

540

520

500

480

460

440

420

400

31-Jan 28-Feb 31-Mar 30-Apr 31-May 30-Jun 31-Jul 31-Aug 30-Sep 31-Oct 30-Nov 31-Dec

2017 2018 2019 2020 2021 2022

Pork in Cold Storage (Mil Lbs)

625

575

525

475

425

375

31-Jan 28-Feb 31-Mar 30-Apr 31-May 30-Jun 31-Jul 31-Aug 30-Sep 31-Oct 30-Nov 31-Dec

2017 2018 2019 2020 2021 2022

3Wednesday, February 23, 2022

NTG Morning Comments

www.nesvick.com

Financials

The Consumer Confidence report was out

yesterday and, as I’ve done in the past, I

thought we’d quickly look at some of the

internal numbers of the report focusing on

the labor market. The first chart at the top

right shows the jobs plentiful vs the jobs

hard to get indices in the top panel. The

bottom panel shows the spread between the

two. As you can see, while the jobs plentiful

index has backed off a bit from its highs, it

remains historically elevated. I’ve shown

before that the spread between the two

(bottom panel) is a good indicator of the

unemployment rate, and for now it

continues to point towards a relatively tight

labor market. The second chart shows a

breakdown of consumer expectations over

the next 6 months. In the top panel, the

white line shows responses indicating they

expect more jobs available in 6 months and

the orange line shows the respondents

expecting fewer jobs within 6 months. The

second panel again shows the spread

between the two. Interesting that this

spread is near its lowest level since even

before the pandemic. Looks like consumers

are starting to indicate expectations for

slowing growth?

Energy

Continuing a look at the consumer confidence numbers, I always find it interesting to look at the vacation

intentions portion of the report. As shown below, overall vacation expectations (over the next 6 months)

dipped last month but there is a seasonal component to that and I don’t think there is much more to it than

that. What still stands out to me is the ongoing below-average vacation by air travel intentions. We’ve

bottomed from the depths of the pandemic but are still below anything seen from 2011-2019. I will say that all

my recent airline experiences have been pretty full and airports have been bustling, so I do wonder if this is

really capturing sentiment. TSA checkpoint numbers are back to 2019 pre-pandemic levels…so obviously

someone is flying. I wonder what is the disconnect here…

4Wednesday, February 23, 2022

NTG Morning Comments

www.nesvick.com

Today’s Calendar (all times Central)

• Not much….

Thanks for reading.

David Zelinski

dzelinski@nesvick.com

901-766-4684

Trillian IM: dzelinski@nesvick.com

DISCLAIMER:

This communication is a solicitation for entering into derivatives transactions. It is for clients, affiliates, and

associates of Nesvick Trading Group, LLC only. The information contained herein has been taken from trade and

statistical services and other sources we believe are reliable. Opinions expressed reflect judgments at this date

and are subject to change without notice. These materials represent the opinions and viewpoints of the

author and do not necessarily reflect the opinions or trading strategies of Nesvick Trading Group LLC and its

subsidiaries. Nesvick Trading Group, LLC does not guarantee that such information is accurate or complete and it

should not be relied upon as such.

Officers, employees, and affiliates of Nesvick Trading Group, LLC may or may not, from time to time, have long

or short positions in, and buy or sell, the securities and derivatives (for their own account or others), if any,

referred to in this commentary.

There is risk of loss in trading futures and options and it is not suitable for all investors. PAST RESULTS ARE NOT

NECESSARILY INDICATIVE OF FUTURE RETURNS. Nesvick Trading Group LLC is not responsible for any

redistribution of this material by third parties or any trading decision taken by persons not intended to view this

5Wednesday, February 23, 2022

NTG Morning Comments

www.nesvick.com

material.

6You can also read