A Deep Dive into Growth Markets - Ryan Ivers Head of US Sales - Constant Contact

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

A Deep Dive into Growth Markets

Ryan Ivers

Head of US Sales

ryan.ivers@payu.com

Overview

Opportunity in Local insights

1 High Growth

Markets

4 Central and Eastern

Europe

Local insights Local insights

2 India 5 Russia

Local Insights Local insights

3 Latam 6 Africa

Why high growth markets? 90% of the global population under 30 lives in emerging markets. Source: Euromonitor, May 2014

Global Ecommerce Growth

Ecommerce in developing economies is growing twice as fast as in most developed markets

Central

&

Eastern

Europe

17.2%

Western

Europe

10.7%

North America

12.0%

Asia Pacific

36.8%

Latin America

19.8%

Middle & East Africa

25%

Cross-border online B2C sales will more than double in the next five years to reach $424 billion in 2021

Payment method breakdown developed markets

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%

USA UK Germany France Australia Canada

Credit Cards Debit cards Cash Payments Bank Transfers Wallets Payment to bank card Other

Source: http://www.expertmarket.co.uk/sites/default/files/filemanager/Payment_methods_online

53%

PayU payment method breakdown of total trx

use APM

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%

Argentina Brazil Chile Colombia Czech Hungary India Mexico Peru Poland Russia South Turkey

Republic Africa

Credit Cards Debit cards Cash Payments Bank Transfers Wallets Payment to bank card Other

PayU Market Data 2015

AMP: Alternative payment methods (anything apart from credit and debit cards)

*Mexico, Romania and Russia: credit cards and debit cards combined

Local Insights: India

India Overview

Cash on Delivery

RAPID INTERNET GDP GROWTH HUGE ECOMMERCE In 2015, 45% of total

PENETRATION India is far MARKET Ecommerce was

500 million internet outstripping Europe Ecommerce in India is CoD (Cash on

users by end of 2016. and US in GDP expected to grow to Delivery)

The next 15 years, growth $100 billion by 2020 ;

India will see more Cross-border

people come online ecommerce now

than any other accounts to over 20%-

country 25% of global

commerce sales

Payment options in India

OGSP Regulation In late 2015, the Reserve Bank of India allowed the import of goods and software using an Online Payment Gateway Service Provider (OGSP). • Cross-border of goods and software allowed and not necessary to have a local legal entity in India • Maximum value of $2,000 USD for cross-border

Local Insights: Latam

Latin America Overview

By 2020, Credit card Latam is

smartphones penetration expecting far

are expected and banking is greater GDP

to account for low, so growth

68% of all alternative compared to

phone forms of Europe over the

connections in payment next 5 years

the region methods are

KEYHigh growth in Latam

4 3.8 3.7

3.5

3

2.4

2.0

2

1.6 1.6 1.6 1.5 1.6

1

0

2016 2017 2018 2019 2020

Latam % GDP Growth Euro Area % GDP Growth

Latam is expecting far greater GDP growth compared to

Europe over the next 5 yearsBank account and

Credit card penetration in Latam

94

69

World

51

Account penetration 51

46 34 World money

Adults with an account (%), 2014 Account only

Financial institution

and mobile money

14

account

Financial institution

account only

East Asia Europe High-income Latin Middle South Sub-Sahara

& Pacific & Central OECD America & East Asia Africa

Asia economies

Caribbean

50/50 “chance” to have access to banks in LATAM.

“Mixed” / Informal economies rely on cash but at the same time, provide

opportunities for e-payments using bank accounts. More than 60% of those with

bank accounts have used them for payments.

Source: WORLD BANK. (2105) - The Global Findex Database 2014121 MM

Mexico Colombia

Banked:46.5% Banked: 60.8%

CCP:30.5%

46 MM CCP: 39.8%

Panama 3.5 MM

Banked:43.4%*

CCP: n.a. 204 MM

Regional

30 MM

context

Peru Brazil

Banked:41.6% Banked: 52,3%

CCP: 26.0% CCP: 60.1%

population and

banking

43 MM

Argentina

Chile 17 MM Banked: n.a.

Banked:65.2% CCP: 47.6%**

CCP: 44.8%

CCP: Credit Card penetration

Source: Tecnocom (2014) – informe medios de pago

* Asociación de investigación y Estudios Sociales (GUA) ** According to # carholders vs populationLocal Card acquiring vs cross-border

user

Will not get charged Will have control of the

extra Will not have installments chosen

by bank for international any FX risk (Case of Colombia that when

purchasing abroad everything gets

transaction defaulted to 24 installments)Offering Installments

The credit risk is always Approximately 60% of all retail

Enabled for Visa, ecommerce transactions using

MasterCard and Amex assumed by the bank

credit cards use installments.

48

People use installments even for Installments go from In some countries the expense

purchases as low as $10 USD. 1 to up to 48 months. of these installments can be

assumed by the merchant.Installments per country

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%

Argentina Brazil Chile Colombia Mexico

Installments Traditional

19Offering Installments

In Colombia and Chile

The installments cost is paid by the consumer on a month to month

basis. Its a deal completely between the bank and the customer.

20Installment Payment Process

Select the number of installments

Digital Retailers in Argentina that offer Installment

payments for Digital Purchases, Dec 2015

% of respondents

Offer installment payments Number of Installments

2%

10%

NO

30% 25%

YES 63%

70%

7 to 12 2 to 6 13 to 18 Other

Source: eMarketerInstallment Options Available

• Argentina – 3, 6, 9, 12, 18, 24 months

• Many Banks offer promotions with installments without

interest if use that bank’s card. Very powerful for buyer

• Brazil – 1 – 12 months

• Chile: 1 – 48 months

• Colombia: 1 – 36 months

• Mexico: 1, 3, 6, 9, 12 months

• Banks offer “months without interest” if buyer uses that

bank. Starting to gain a lot of demand from consumers.

24Local Credit Cards 8% of all transactions 9% of all transactions 7% of all transactions

Cash payments

How do they work in PayU?

1 2 3

Local store

Customer chooses the Customer goes to the Store notifies the PSP

cash payment method authorized local store or payment was made. PSP

and prints the voucher bank branch sends confirmation to

merchant to ship the

product and credits

merchant’s virtual account.Example of a cash

payment voucher in

Brazil

Efecty kiosks in Bogota,

ColombiaLocal Insights: CEE

CEE Overview

MCOMMERCE INTERNET SHOPPING HUGE ECOMMERCE MARKET

• Polish mobile In Turkey, 33.1% of 1 in 4 internet users in Poland

commerce is growing Internet users aged already shop online and plan

three times faster 16-74 bought goods to increase the amount of

than ecommerce. or services over the money they spend online

• In Turkey, over 40% of Internet for private making Poland and Czech

smartphone owners purposes. Rep. part of the top five most

already have important markets for e-

experience with commerce in Europe

mobile shopping (alongside U.K., France,

Germany).Credit card - Installments in CEE

Romania: 1 – 24 month installments options

Turkey: 2 – 9 month installment options

33High Growth in CEE

4

2.8

3 2.7

2.6

2.4

2.1

2

1.6 1.6 1.6 1.6

1.5

1

1

0

2016 2017 2018 2019 2020

CEE % GDP Growth Euro Area % GDP Growth

Central and Eastern Europe as a whole, is seeing steady

growth at nearly double the rate of its neighboring countries

to the west.

34Importance of Bank Transfers in

Poland

Share of Payment Methods (%)

89% 88%

3% 7% 3% 5% 4% 0%

Bank Transfers Debit Card Credit Card other cards

2014 2015

Real-time online banking transfers are key in Poland. To enable

this, PSP’s connect with many financial institutions in order to

create a network that facilitates online payments and

transactions.

35Key Facts for Turkey

60% of the population is 58 million Credit Cards

under 30 years old 108 million Debit Cards

Developing

countries

4.5% The

ecommerce

% share of

Developed

countries

6.5% total business

retail

Turkey 1.6%

0% 1% 2% 3% 4% 5% 6% 7%Offering Installments in Turkey

88% 7

Processing locally allows

88% of all ecommerce the user to have better 7 different connections to

transactions are made control of the conditions of Banks are required in

using Installments from his monthly fee and order to offer installments

credit cards issuers. connects directly with with all mayor Banks and

many loyalty programs, give Access to the Loyalty

2 – 9 month range which are highly popular programs

in Turkey.Single integration, less effort..

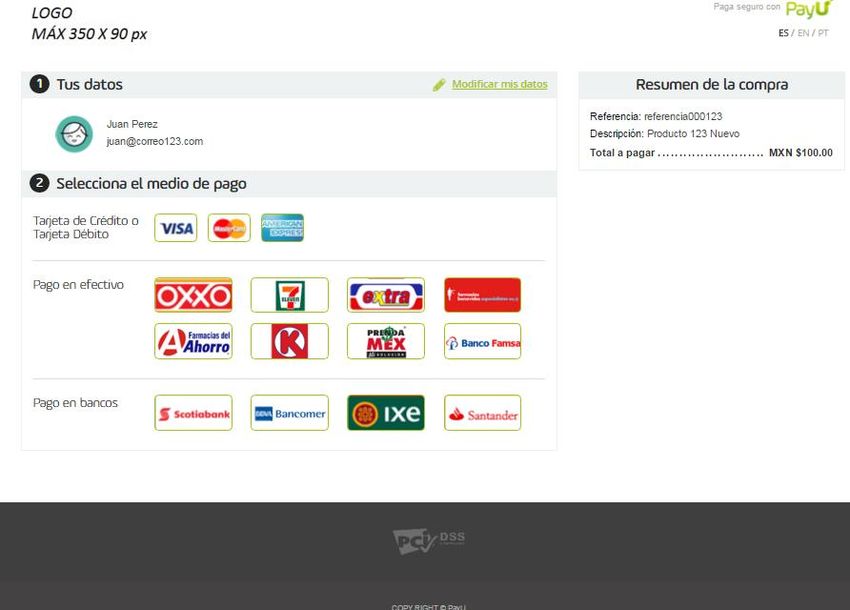

PAYU PAYMENT PAGE API

Consumers complete their purchases PayU Payment System can be integrated

easily by entering card information on easily into the site and designed payment

proven, user-friendly PayU Payment Page. page according to the needs.Local Insights: Russia

Russia Overview

MCOMMERCE eConsumers HUGE ECOMMERCE MARKET

• Polish mobile In 2015, there were 1 in 4 internet users in Poland

commerce is growing 31 million already shop online and plan

three times faster econsumers, up from to increase the amount of

than ecommerce. 14 million in 2012. money they spend online

• In Turkey, over 40% of making Poland and Czech

smartphone owners Rep. part of the top five most

already have important markets for e-

experience with commerce in Europe

mobile shopping (alongside U.K., France,

Germany).Russia Market Comparison

Russia provides an access to 31M eConsumers with strong

potential for further growth

Habitants

63,9 M 143,8 M

Spend per

capita

$ 22,3 k $ 4,5 k

Internet-

users, %

90 % 70 %

UK Russia

122 % M-users, %

155 %

CZ Online

57 % 16 % Banking, %

No of eConsumers in Russia

(2012-15) in millions

326 M

$ 35,1 k 14 19 25 31

US

86 % 2012 2013 2014 2015

101 %

63 %Russian Consumers

Internet Users’

Population of Russia

geography in Russia

12-64 years old: 5%

104,6 million people 6%

7%

57 %

25 %

Others Moscow

Use Internet 57%

Saint-Petersburg Novosibirsk

Ekaterinburg Kazan

61% of all Internet users in Russia are in

towns with one hundred thousand people or more.Russian Payment Methods

% of % of domestic

Payment method

all orders orders

Cash by delivery 52 66

Bank card at order stage 25 14 Key comments

Bank card by delivery 6 8

Almost 60% of orders are

Electronic payment systems 10 6 paid on delivery, 52% of

Specials (bonus or discount card) 1 2 which - cash

Bank or postal transfer 2 2

25% prefer to pay their

orders using bank card

eBanking, mobile banking 1 1 at order stage

Other 1 1

Other 10% purchases are

Payment terminal 2Pay on Delivery in Russia

At least 75% orders in 2015 made with POD. Share of POD not dropped by the last 5 years.

We see only rising of Card on Delivery option.

Stores special programs and discounts like M.Video’s 5% discount for prepaid orders have

no effect for all market. We even see a little increase of POD.

The main problem is the availability of POD for customers. As long as there is supply,

customers will want to use it.

2011 2012 2013 2014 2015

Pay on Delivery 75% 75% 74% 74% 76%

Cash on Delivery 74% 72% 68% 66% 68%

Card on Delivery 1% 3% 6% 8% 9%Pay on Delivery in Russia

Cash has lost its monopoly in Russia

72% have replenished the balance of their mobile phone cashless

61% have payed their public utilities cashless of the respondents who payed online have

57% numerous accounts in different e-payment

systems

57% use more than one credit

card for online payments

Only 5% of the respondents prefer

keeping their earnings for current

expenses in cash

Source: Data Insight (2015)Market trends

№1. mobile device is the main operational center of an ordinary

person

Every second user had an experience of paying via

mobile during the last year

Share of online-users who had experience of at least one case of

payment during the last 12 months with a smartphone or tablet

61% 43%

18-34 years inhabitants of large cities (with

population up to 100 ths)

41%

50%

35-54 years average share

59%

of respondents Moscow and Saint-

Petersburg

20%

55-64 years 39%

New users of Internet

(less than 5 years)

Source: Data Insight (2015)Data regulations in Russia

Summer of 2015 a new legislation forbidding

storage of Russian citizens’ personal data in

foreign countries came up.

Being on the ground and having local know-how

and connections allows companies to resolve

issues like the above in a speedy manner.

Helps our merchants comply to local regulations.All companies dealing with personal data must

comply with 5 fundamental rules.

Personal data may be collected, stored and used only with the consent of

1 the data subject (the person the data refers to).

Data operators storing personal data are liable for keeping such data

2 confidential (not permitted to transfer, share or disclose such data without

the consent of the data subject).

3 Full protection of personal data should be provided through a range of

organizational and technical measures defined by the law.

The Operator should work out and make publicly available an internal

4 policy for processing personal data. This document is obligatory for all

operators.

5 Starting Sept. 1, 2015, personal data should be processed by means of

information data bases that are physically located in the Russian territory.Local Insights: Africa

Africa Overview

In Sub-Saharan Africa 83% of consumers Africa is expecting

12% of adults (64 million plan to conduct far greater GDP

people) have mobile mobile commerce in growth compared

money accounts, the next 12 months to established

markets.

10% more than in the An increase of 15% Nigeria is growing at

rest of the world (2%). on the 2013 figure 2.8% compared to

(according to InMobi) Europe’s 1.6%.Smartphone penetration in Africa

60

52

48

45 42

36

30 32

30

30 27

24 25

22

19

15

0

2013 2014 2015 2016 2017 2018

Nigeria South AfricaInternet costs in Africa

Africa has skipped the PC era.

In Nigeria - 60% are youths and 49.2%

urban.

Nearly half of the adult population in

South Africa have smartphones.

Huge opportunity to enhance the

digital transactional uptake .

High internet costs is the main concern

for merchants and consumersCard penetration low but still the online king in

South Africa

Card Coverage in South Africa

100%

90% 83.30% 58%

80%

70%

60%

50%

Without Cards

40%

42% With Cards

30%

20%

10% 16.70%

0% 35.2 million

Credit Card Debit Card

Coverage Coverage

8 millionPayments landscape in South Africa

Cards 95% CC:DC = 70%:30%

Wallets 6% Subset of Cards total

At specific EFT merchants this

EFT 2.3% figure can be around 20%-30%

Loyalty &

Rewards 1.46%

Card

Recurring 1.07%EFT Solutions in South Africa

Smart EFT EFT Pro

• 4 Banks • 5 Banks +

• User enters payment details on • Service injects payment

bank site details on bank site

• Asynchronous transaction flow • Synchronous transactionLoyalty in South Africa

Discovery Miles eBucks Ucount

• Discovery loyalty • FNB card loyalty • Standard bank loyalty

product product product

• 2.3m users, 400k cards • 2m members, R1bn • 400k members, R170m

wallet value loyalty value

• Merchant sign up

• Merchant sign up • Merchant sign up controlled by

controlled by controlled by eBucks Standard bank

DiscoveryNigerian Payment Landscape

Preferred payment methods

19.57%

Cash

Obstacle for buying products online 38,81%

Credit Card

12.11%

Delivery time is the main problem (!) Debit Card

Mobile airtime

Cost

10.45% 29.52%

23.55% Delivery Time

Internet

6.30% 31.34% Connection

Lack of options

28.36% Lack of security

Source: http://paymentsafrika.com/payment-news/infographic-e-commerce-in-africa/#disqus_threadOverall Conclusions

Keys to Success – Understanding the buyer

eCommerce in emerging market countries is growing faster

than development countries

Credit & Debit Cards still play an important role but

understanding and offering installments is very important

Alternatives payments are critical to improving the

customers buying experience

• Cash payments in emerging markets to serve the under

banked

• Cash on Delivery in Russia market is massive

• Bank transfers in India, Poland, Czech Republic are

more popular than credit cards for online purchases

• Loyalty & Reward programs are a new important ways

consumers relate to credit card purchasesQUESTIONS?

Ryan Ivers – Head of US Sales Ryan.ivers@payu.com If you have any questions about the presentation, go to our LinkedIn Group (the Payments Education Forum) and request an invitation (this is a closed group specifically for the payments industry).

You can also read