All articles are from www.zerohedge.com Mastermind Of Iceland's "Great Bitcoin Heist" Flees To Sweden After Brazen Prison Break - PortfolioBuilder.io

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

All articles are from www.zerohedge.com Mastermind Of Iceland's "Great Bitcoin Heist" Flees To Sweden After Brazen Prison Break One of the suspects in a high-profile theft that Icelandic media are calling "the big bitcoin heist" has escaped a low-security prison and fled to Sweden, the BBC and Guardian reported on Wednesday. The man, Sindri Thor Stefansson, who is suspected of masterminding the theft of 600 bitcoin-mining rigs as escaped from custody after he climbed out his window and somehow sneaked aboard an international flight. Stefansson used another man's passport during the escape, and was not identified until security footage was examined after he was reported missing.

The stolen rigs - which are still missing despite the police having arrest more than 20 people allegedly involved in the scheme - are worth some $2 million, per the BBC. Stefansson was among 11 people arrested in February. Stefansson and his crew purportedly stole the computers during four raids on data centers around Iceland.Iceland has become a favorite destination for crypto miners because of its abundant and cheap power that comes primarily from renewable sources. As we pointed out earlier this year, bitcoin miners are expected to consumer more energy than the roughly 350,000 people living in Iceland during the coming year. As one sociology professor at the University of Iceland pointed out to the Guardian, jailbreaks in Iceland, which has famously low crime rates, are extremely rare. Typically, when somebody flees one of Iceland's prisons it "usually means someone just fled to get drunk," said professor Helgi Gunnlaugsson. What's more unusual, according to Gunnlaugsson, is that such a high profile prisoner would be held in such a low-security environment. Professor Gunnlaugsson added that it's "extremely difficult" to flee Iceland, or to hide.

But it apparently wasn't a problem for Stefansson. Guards at his prison didn't even

notice that he was gone until his flight had taken off. And what's more surprising, he

somehow traversed the 60 miles of cold, hard terrain between the prison and the airport.

Yet police have made no other arrests in the case.

"He had an accomplice," police chief Gunnar Schram told local news outlet

Visir. "We are sure of that."

Hmmm. We wonder what tipped them off?

Stefansson has been in custody since February, but was transferred to the low-security

prison - an institution that more closely resembles what we in the US would call a "halfway

house" - where he had access to his phone and the Internet (and could also apparently

come and go as he pleased).

Iceland police issued an international warrant for Stefansson's arrest - but Swedish

police spokesman Stefan Dangardt said no arrest has been made in Sweden.

But in perhaps the most outrageous twist in an already incredible story, Stefansson traveled

to Sweden on the same plane that was carrying Icelandic Prime Minister Katrin Jakobsdottir,

who was traveling to Sweden to meet Indian Prime Minister Narendra Mohdi.

The "prison" from which Stefansson escaped is unfenced and and Stefansson was not

considered dangerous so he was afforded many privileges.

We wonder if Iceland will ever catch Stefansson? By the looks of it, he appears to have made a clean escape. And thanks to the ease with which bitcoin can be transferred internationally, we imagine that - if he's made it this far - it won't be long until he's reunited with his ill-gotten fortune. The Federal Reserve Has Done A Great Job Destroying The Middle Class Authored by Tom Lewis via GoldTelegraph.com, The Federal Reserve has been determined to create “Wealth Effects” throughout the economy since 2008, which has left the majority of Main Street on the sidelines.

The Fed’s objective was to make American households feel wealthier by pushing up the valuations of stocks and bonds. However, this paper wealth mentality has worked beautifully for Wall Street and the 1% but has destroyed much of the middle class as wealth inequality continues to skyrocket. In fact, former Federal Reserve Chairman Alan Greenspan has gone on record to warn of a massive bond and stock bubble thanks to historic low-interest rates. I guess, the idea of rising paper wealth to drive a wave of renewed borrowing and spending hasn’t quite worked out as planned. Sadly, as the below chart points out most households have been squeezed as the majority of the wealth created has only gone to the top 5% of households earning in excess of $200,00 annually, meanwhile the bottom 95% have suffered.

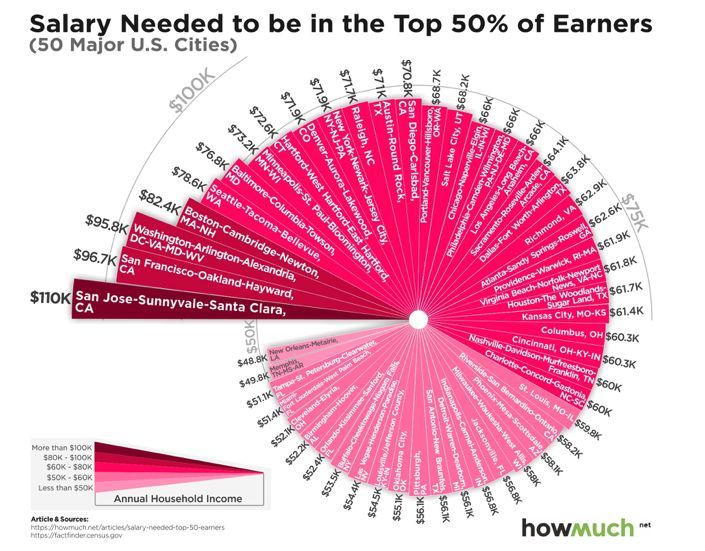

We used to live in a time where making a six-figure paycheck was a lot of money, but parts of the United States are simply unaffordable for most of middle America. In San Francisco, you have to earn as much as $110,040 to be even considered in the top 50% of earners, according to U.S Census figures.

It is evident that these “Wealth Effects” that the central bankers have been chasing does not drive inflation-adjusted wages of the bottom 95% which has stagnated for decades. It merely accelerates purchasing power decay where the 1% get the wealth first, and it then trickles down to the rest of the economy. The experiment of prolonged zero interest rates has destroyed savers and rewarded reckless spenders who have helped push household debt to unprecedented levels.

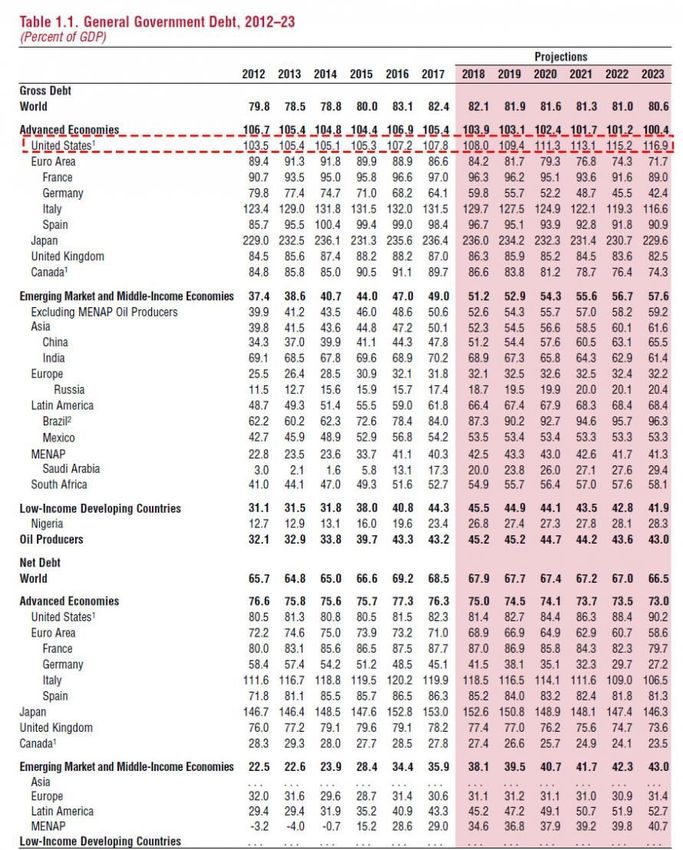

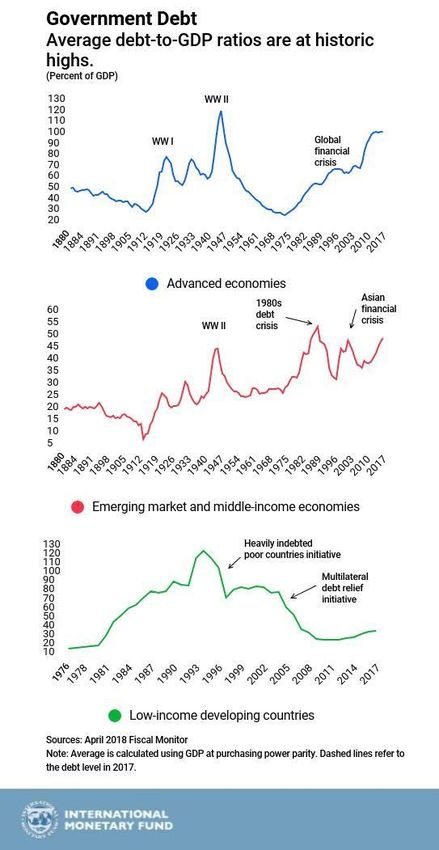

Unfortunately, the 2008 Band-Aid is going to be ripped off at some point which will further alienate the middle class and drive wealth and income inequality even further. Wealth Effect = Total Bust IMF Sounds The Alarm On Global Debt, Warns "United States Stands Out" Exactly one year ago, in its Global Financial Stability report, the IMF issued a stark warning when looking at the soaring level of private sector debt: it found that more than 20% of US

corporations are at risk of defaults once interest rates rise, and calculated that the combined assets of firms threatened by default - those who earnings do not cover their interest expense - could reach almost $4 trillion. Fast forward exactly one year to today, when the IMF once again sounded the alarm on debt, only this time on the public side of the ledger, warning about - what else - excessive global borrowing, and noting that with a total of $164 trillion of debt, or 225% of global debt to GDP...

... the world’s public and private sectors are more in debt now than at the peak of the 2008 financial crisis, when global debt/GDP peaked at 213%.

Some more details from the IMF: while advanced economies are responsible for most global debt, in the last ten years, emerging market economies have been responsible for most of the increase. In fact, as we showed several months ago, China alone contributed 43% to the increase in total global debt since 2007. In contrast, the contribution from low income developing countries is barely noticeable.

When looking at the big picture, needless to say it's all about the US, China and Japan: these three countries alone accounted for half of the $164tr total in global public and private

sector debt. And speaking again of China, its debt surged from $1.7 trillion in 2001 to $25.5 trillion in 2016, and was described by the IMF as the "driving force" behind the increase in global debts, accounting for three-quarters of the rise in private sector debt in the past decade. Here we should note that the IMF's definition of debt is clearly different from that of the Institute of International Finance (IIF), which last week calculated that global debt had hit $237 trillion in debt or 318% debt/GDP. Whatever the differences in debt calculating methodology, both agencies can agree on one thing: debt has never been greater and it once again poses an existential threat to the so-called "coordinated recovery", which of course, only exists thanks to said surge in global debt. In that vein, and continuing its warning from yesterday's World Economic Outlook, the fund warned there is an urgent need to reduce the burden of debt in both the private and public sectors to improve the resilience of the global economy and provide greater firefighting capability if things went wrong: "Fiscal stimulus to support demand is no longer the priority," the IMF said in the 156-page report. What we again find odd is how quiet everyone was for the past ten years when central banks, by keeping interest rates at record low levels, enabled the world's biggest debt

issuance spree, for both public and private debt, and now that debt is at a level that even Goldman recently said is no longer sustainable, suddenly everyone - from central banks, to bank CEOs, to NGOs - is screaming from the rooftops how dangerous debt really is. As an amusing aside, in a blog post posted alongside the Fiscal Monitor report, IMF director Vitor Gaspar said that the "United States stands out" and singled out the US for criticism, warning was the only advanced country that was not planning to have a falling burden of debt because tax cuts would keep public borrowing high.

“We urge policymakers to avoid pro-cyclical policy actions that provide unnecessary stimulus when economic activity is already pacing up,” Gaspar said; what he really meant

was "Trump, stop what you are doing before you lead to a debt funding crisis, that finally

bursts the global debt bubble. "

There is another threat: rising rates. The IMF said that the interest burden has doubled

in the past ten years to close to 20% of taxes, an escalating cost which "reflects in part

the increasing reliance on nonconcessional debt, as countries have gained access to

international financial markets and expanded domestic debt issuance to nonresidents."

Echoing its warning from April 2017, The IMF again noted it is was concerned that private

sector debts make the global economy more vulnerable to a new financial crisis started by

"an abrupt deleveraging process" where borrowers all tighten their belts simultaneously,

sending the economy into a nosedive.

“In the event of a financial crisis, a weak fiscal position increases the depth and duration of

the ensuing recession, as the ability to conduct countercyclical fiscal policy is significantly

curtailed."

So what should policymakers - having gotten used to flooding the world in debt - do? Why

the opposite, of course: as the FT summarizes, with the global economy growing strongly,

the IMF recommended countries stop using lower taxes or higher public spending to

stimulate growth and instead try to reduce the burden of public sector debts so

that countries have more leeway to act in the next recession.

Translation: no tax cuts, no increases to deficit spending, i.e. another dig at everything that

Trump is doing.

In fact, the IMF singled out the Trump administration’s tax cuts for criticism, since they left

the US with a deficit of 5% of national income into the medium term and a persistently

rising level of debt in GDP. It also explains why the IMF forecasts the US is the only nation

whose debt load will rise in the next 5 years.

"In the United States fiscal policy should be recalibrated to ensure that the

government debt-to-GDP ratio declines over the medium term. This should

be achieved by mobilising higher revenues and gradually curbing public

spending dynamics, while shifting its composition toward much-needed

infrastructure investment."

There was the obligatory dig at bitcoin, although the IMF at least conceded that unlike some

$500 trillion in derivatives, a few billion in bitcoin and ethereum do not currently appear to

pose any risk to financial stability, "But they could do if they become more widely used", in

other words, don't you dare even think of alternatives to fiat currencies.

Going back to "the debt problem" the IMF admitted that it was not only limited to advanced

economies, with middle-income countries also racking up borrowing higher than that which

led to the debt crises of the 1980s. There was also a particular warning about China whosegargantuan scale and opaque financial system poses a massive risk to stability, the IMF says. The silver lining, the report noted, is that Chinese banks have reduced their use of risky short-term borrowing, in response to tighter regulation. The report also judges that the global banking system is stronger now than it was at the time of the crisis. But it adds that reforms need to continue. As a result, the IMF again recommended that countries raise taxes and lower public spending to decrease annual borrowing and get the burden of debt on a firmly downward path now that there is no need for fiscal stimulus. The few exceptions to that advice included Germany and the Netherlands, which the IMF said had “ample fiscal space” to boost public investment in infrastructure and enhance the long-term resilience of their economies. Here, the Keynesian would probably go nuts, and say that such a policy promotes saving, and is tantamount to austerity, which for some reason, is equivalent to economic death in a world where total debt/GDP is either 225% or 316% depending on whose methodology one uses. Actually, come to think of it, it all makes sense when one considers that it is the very policies that define modern finance and economics, that have led the world to this precipice. In fact, reading the IMF report between the lines, it is nothign more than advance scapegoating for the inevitable global debt crisis that is coming, and which not even the IMF is hiding any more. What is most comical - if completely expected - is that the IMF is now blaming it all on Trump: not on generations of economists who steered the world to the point where there is more than $3 of debt for every $1 of GDP, and not on central bankers who flooded the world with debt so that the richest 0.01% can be richer than their wildest dream. Nope: it's all Trump's fault. Somehow we doubt this advance damage control will work after the next, and likely final, crash. Nearly One-Third Of U.S. Lottery Winners Declare Bankruptcy Authored by Fred Dunkley via SafeHaven.com,

Luck is a tricky thing. And when it comes to those lucky Americans who have won windfalls in the lotteries, it seems to be short-lived. Winners become losers at breakneck speed. Studies show that lottery winners are more likely to declare bankruptcy within three to five years than the average American. In fact, nearly one-third of lottery winners declare bankruptcy, and it doesn’t end there. It’s usually followed by depression, drug and alcohol abuse and estrangement from family and friends. Still, the average American will be riled by feelings of envious excitement at the stories of lottery winners in the early days when the elation is still real. The most recent story to gain widespread circulation was the March Mega Millions drawing that won an astounding $521 million for a single ticket sold in New Jersey, making it the fourth-largest payout of all time. The pressure of winning is often enough to send someone into depression, particularly when they are publicly outed and soon to become the best friend of anyone who is hoping for a handout. That fact alone has led to recent moves to keep their winning identities secret. The winner of the March Mega Millions drawing is a case in point, and it’s not easy. New Jersey—like many other states—makes it difficult to shield your identity because winners aren’t technically allowed to anonymously claim their prizes. Another massive lottery winning in January in New Hampshire netted a ‘lucky’ Powerball Jackpot ticket-holder $560 million. Citing concerns for safety, the winner requested anonymity and fought and won a legal battle in the process.

But security is only the initial issue faced by lottery winners - many of whom are not

equipped to handle a new breed of financing that runs into the hundreds of millions.

For many, sudden wealth is sudden despair. Everything from squandering earnings,

making bad investments and falling prey to con artists awaits the winner.

In one publicized case, a West Virginia man won $315 million in a 2002 Powerball drawing

and lost it all in about four years. His misfortune reportedly included thieves stealing

$545,000 from his car and lawsuits over gambling debts.

"I wish I'd torn that ticket up," he said afterwards.

It’s a high-stakes game for people who have no experience handling massive amounts of

cash.

"The average lottery winner is a blue-collar individual, and all of a

sudden you give them tens of millions of dollars and you post their

name across the world, and then you expect them to act

responsibly — it’s an unenviable expectation," attorney Andrew

Stoltmann, who has represented lottery winners, has said.

Of course, the lawyers and wealth managers are keen to descend on this unsuspecting crop

of lottery winners for the lucrative fees but trying to manage sudden wealth alone doesn’t

usually bear fruit.

Jason Kurland, who calls himself the "go-to" attorney for lottery winners, claim that most

important thing the winner can do is to stay low, avoid publicity and hire a financial planner.

Kurland said lotto winners should assemble a team of professionals who are experienced in

for that specific situation, and it shouldn’t just be a wealth manager. Everyone needs to

have checks and balances, with that team that includes a lawyer, accountant and financial

advisor.

Lottery-based investments also may tend to the high-risk, presumably on the

notion that the lucky streak is going to be sustained.

And rather than going on a spending spree, lawyers advise lottery winners to take their

winnings as an annuity—not all at once.

Hoarding a massive lump sum of cash is a losing move and taking it all at once means

getting less. The latest Mega Millions $521 million turns into $317 million if taken out all at

once.

This is one way to beat the bankruptcy forecast.Another study says that lottery winnings raises the risk of bankruptcy even among the winners’ neighbors by roughly 2.4 percent. Researchers say that lottery winner lifestyle upgrades then tempt their neighbors to boost their own spending on visible markers of prosperity, even though they haven’t had a sudden run of financial luck. None of this stops anyone from dreaming of winning the lottery, though. Lottery sale profits have consistently risen over the years: "It’s An Ominous Sign": Trader Reveals The "Nightmare Facing China's Leaders" With the market's attention focused on how the China-US trade wars impact the US stock market, many have forgotten to check in on China's markets. And it is here that Bloomberg commentator Kyoungwha Kim notes that things are going from bad to worse, as despite the

recent spate of good economic news, the local market just can't rally on good news, an

indication of the "nightmare facing China's leaders."

The reason: Trump may have accidentally stumbled on China's Achilles heal:

... the Shanghai Composite has failed to track the recent bounce in the

S&P 500. The selloff in Chinese stocks has deepened since Xi Jinping’s

speech in Boao to open up the world’s second-largest economy, increase

imports and protect intellectual property rights.

The case of ZTE being banned from buying American tech products

revealed the hurdles for the "Made in China 2025" strategy that’s

supposed to upgrade the economy from a manufacturer of quantity

to one of technology-driven quality.

Kim's full thoughts in the latest BBG Macro View:

Chinese Stocks’ Blues Show Nightmare Facing Leaders

It’s an ominous sign when a market can’t rally on good news. And that’s

exactly what’s happened to Chinese stocks recently.

The first quarter’s strong growth has done nothing for mainland equities.

Even a surprise large reduction in banks’ reserve requirement ratios only

prompted an underwhelming reaction.After moving in tandem in early 2018, the Shanghai Composite has failed to track the recent bounce in the S&P 500. The selloff in Chinese stocks has deepened since Xi Jinping’s speech in Boao to open up the world’s second-largest economy, increase imports and protect intellectual property rights. The case of ZTE being banned from buying American tech products revealed the hurdles for the "Made in China 2025" strategy that’s supposed to upgrade the economy from a manufacturer of quantity to one of technology-driven quality. Chinese consumption is growing but not by enough to take up the slack from dwindling exports if tech industries are going to sag while "old economy" manufacturers continue to cut investment amid ongoing supply- side reform. Pessimism stems from a government stuck between a rock and a hard place. China can follow Japan’s example from decades ago by bolstering property investment and adopting other stimulative policies and somehow hope to avoid the latters 1990s collapse. Or, it can endure a

low-growth period of reform in order to avert financial market

bubbles.

The Shanghai Composite is already 13% below January’s two-year high.

One has to wonder where the next buyer will come from if the

government fails to convince investors that it knows the optimal

path.

The Only Question That Matters: "Is

The Credit Cycle About To Crack" -

Here Is The Answer

When trying to determine the fate of equities over the next few months (or years) and

whether - as some speculated recently - the bull market has already peaked, investors

should divert their attention from the stock market and focus on a different asset class:

credit.

Why? Because as the sharp swoon in Goldman's stock this week demonstrated, when it

comes to the marginal buyer of stocks, it is all about corporate buybacks, or more

importantly, their absence. Recall that last month JPM forecast that thanks to low rates and

Trump's tax reform, in 2018 there will be over $800 billion in corporate buybacks this year,

a truly staggering, record number.But for that to happen, one thing has to be present: a vibrant credit cycle which allows

companies to issue hundreds of billions in net IG and junk debt. After all, the bulk of

buybacks are funded with new debt issuance (see the latest IBM results), and if the

credit cycle cracks - meaning if rates spike enough to cause a buyside panic and halt new

issuance - it's all over for both buybacks, and the bull market in stocks.

To answer the question we present two bank reports, which while similar reach somewhat

different conclusions.

The first is from Morgan Stanley, and explains why the bank "thinks a turn in the credit

cycle is near." The argument can be summarized in the three key points (from credit

strategist, Adam Richmond):

● First, we believe there has been way too much complacency in the expectation that

the Fed pulling back in untested ways after years of substantial stimulus would be

"like watching paint dry" as we heard so many times early this year. Very simply,

quantitative easing was hugely supportive of credit markets in this cycle, and wehave argued that the process in reverse has to cause a few large bumps in the road.

At the least, we have made the case that, in this environment, the technicals should

weaken and negative catalysts will get magnified. In our view, a key driver is

simply that global liquidity conditions are tightening, and markets are

coming to the realisation that the process will be rocky. Rising funding

stresses, weaker flows, weaker trading liquidity, higher volatility – this is arguably

what quantitative tightening feels like and, in our view, these dynamics will continue

to pressure credit spreads over the course of the year.

● Second, we argued that these headwinds were occurring with credit valuations very

rich – effectively pricing in a very smooth, seamless central bank unwind: Also

remember that tight spreads are much easier to justify when volatility is

low, and we believe that the vol regime has shifted higher. Put another way,

the move in IG spreads from 87bp to 113bp is largely a reset higher in risk premium

to account for a higher vol and tighter liquidity environment, but still does not come

close to pricing in the medium-term fundamental risks in the asset class, in our

opinion.● Third, markets are very late-cycle, an environment that is often not friendly to credit

and where the ‘margin for error’ is naturally lower: We continue to see evidence

that argues in favour of a very late-cycle environment. When we think about a

turn in the credit cycles, we tend to break it up into two phases. First, in a bull

market, leverage rises, credit quality deteriorates and ‘excesses’ build. These factors

provide the ‘ingredients’ for a default/downgrade cycle. But they don’t tell you much

about the precise timing of a turn. Leverage can remain high for years before it

becomes a problem. In the second phase, these excesses come to a head, often

triggered by tighter Fed policy, tightening credit conditions and weakening economic

growth.To be sure, Richmond does not want to come out as too alarmist, and notes that he

believes that the ingredients for a credit cycle are still in place. However, as to the

more important question of timing (and always the tougher question to get right), Morgan

Stanley thinks the evidence is mounting that "spreads have hit cycle tights – in other

words, that bigger fundamental challenges in credit are 6-12 months away, not

2-3 years down the road."

Still, Morgan Stanley concludes on a very bearish tone and notes that whereas the bank has

often heard the argument that weak growth for much of this cycle has prevented excesses

from building - and hence an already long cycle can last even longer - it disagrees and

see excesses all over the place, driven in part by years of ultra-low rates.

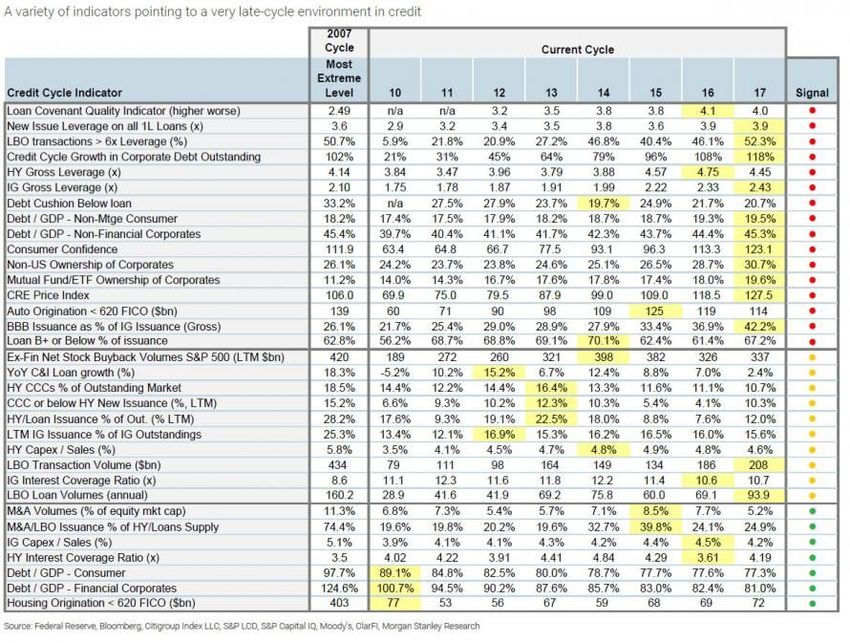

The bank lays out the details for its "credit cycle end is imminent" call in the table below,

and makes the following notable observations:

● Credit markets have grown by 118% in this cycle, and leverage is at

unprecedented levels for a non-recessionary environment (remember,

leverage tends to peak in or even AFTER a recession). If rated based only on

leverage, about 28% of the IG index would have a HY rating.● Low-quality BBB issuance was 42% of total IG supply in 2017, a record as far

back as we have data. The IG index had ~US$700 billion in BBB rated debt in 2008.

Today that number sits at ~US$2.5 trillion. Similarly, B rated or below loan issuance

is now two-thirds of total loan supply.

● LBOs levered over 6x are now a similar percentage of new LBO loans as in 2007.

Covenant quality is weaker across all categories than pre-crisis, while the

debt cushion beneath the average loan is much lower.

● Investors have reached for yield in fixed income in this cycle in a massive

way. Foreign flows have flooded into the asset class, arguably treating US credit as

a rates product, while liquidity needs have risen, with mutual fund/ETF ownership of

credit now over 19% versus 11% pre-crisis.

● Excesses are apparent even outside corporate credit, for example, with

underwriting quality deteriorating in auto lending in this cycle, while non-mortgage

consumer debt is at a high, and CRE prices are ~20% above prior-cycle peaks.

● Around two-thirds of the loan market is no longer captured in our leverage statistics

because these companies don’t file public financials, and this does not include all the

money that has flowed into direct lending in this cycle.

Finally, here is Morgan Stanley's checklist of "late credit cycle" indicators, which leads to the

bank's troubling conclusion:

In terms of timing, we think that enough signals are flashing

yellow and cracks are forming to indicate a credit cycle on its last

legs: For example, looking at credit markets more broadly than just

corporates, we have seen signs of weakness and tighter credit conditions

in places like commercial real estate. Additionally, consumer

delinquencies have risen in various places (i.e., autos, credit cards

and student loans).And in corporate credit, one sector after the next

has exhibited ‘idiosyncratic’ problems (e.g., retail, telecom and

healthcare to name a few). All this is consistent with other signals we

watch, some which have been discussed above (i.e., a flattening yield

curve, falling correlations in markets, rising volatility, a trough in financial

conditions, narrowing equity breadth, rising stress in front-end IG and

much weaker credit flows).And then, putting it all together, here is how Morgan Stanley sees the all important question

of timing, and what happens next:

"We expect idiosyncratic problems to keep popping up, slowly at

first, as the Fed continues to withdraw liquidity. Once growth and

earnings expectations turn lower, which may characterise 2H18, we expect

the process to accelerate, with the market starting to price in rising

defaults and rising downgrades, as the 'cracks' in credit quickly start

to feel bigger and much less idiosyncratic."

Needless to say, that's about as gloomy and pessimistic an outlook a bank can have without

outright telling its clients and traders to sell everything. Which, for those who watched

"Margin Call", will never happen as no bank wants to go down in history as having started

the next financial crisis.

So for readers who find Morgan Stanley's skepticism nauseating, we present another

perspective, this time from the credit strategists at UBS who while generally agree withMorgan Stanley that the credit cycle is (very) late, they disagree that the cycle is about to

crack, and is "unlikely to end in 2018." UBS explains below:

Where are we in the US credit cycle?

The US credit cycle is later-stage, but unlikely to end in 2018. Later-stage

credit indicators are present. Corporate leverage is very high, covenant

protections are very loose, lower-income consumer balance sheets are

weak, and NYSE margin debt is elevated. But the market trades off

changes in conditions, not levels. To this point, we do not see an

inflection to suggest the credit cycle is turning.

Our latest credit-recession model pegs the probability of a

downturn at 5% through Q4'18. Corporate EBITDA growth is running

at 5-8% Y/Y, enough to keep leverage and interest coverage from

deteriorating. Lending standards and defaults are only tightening and

rising, respectively, in select pockets, and the scale of tightening is not

enough to engineer broad stress.

Last, but not least, a quick shot to growth from significant fiscal

stimulus in 2018 should keep the cycle supported

So who is right? To get the best - if not necessarily right - answer, look not at credit, at

least not initially, but stocks, because if the credit pipeline is about to be clogged up, it is

the S&P that will be slammed first, long before all other asset classes. To be sure, the

recent surge in equity vol over the past month certainly gives Morgan Stanley the upper

hand in this debate, at least for now.

Stocks & Bonds Recouple - Now

What?

Historically, when stocks have risen and decoupled from bonds, and bonds have then sold

off to catch up to stocks; the recoupling has led to extended selling pressure in

stocks.

Will we see the same this time?Something else has shifted today: Tech is underperforming financials...

This Is How Easy It Is To Manipulate The Entire Stock Market Yesterday, for the umpteenth time in the last few years, we exposed the clear manipulation of VIX at the futures settlement auction - spiking VIX to favor the record long positioning of VIX futures speculators. With stocks quietly drifting sideways ahead of the US cash open this morning, VIX suddenly spiked reprising a pattern of jerky moves on days when futures on the gauge are settled in monthly auctions... As a reminder, VIX futures settle on Wednesdays at 9:20 a.m. New York time in an auction by Cboe Global Markets. As Bloomberg notes, VIX was heading for its longest streak of daily losses in almost a year in early New York trading, before it reversed direction and rose as much as 11 percent.

The gain occurred around the time of the settlement, which happened 13 percent above the VIX close on Tuesday and outside of today’s range. Both the settlement price and the high-water mark for the VIX occurred more than 10 percent above Tuesday’s close -- lucky, if you were betting on a gain. And as VIX was manipulated around the auction, so the option-market 'tail' wagged the broad-stock-market 'dog' - slamming the S&P down almost 20 points.

And don't forget, large speculators hold a record net-long VIX futures positions, according to the latest data from CFTC... So this settlement spike was very much in favor of all those speculators - after a week of crushing them - how convenient. So just how easy is it to do this?

How do 'traders' manipulate the options market, thus moving VIX in their favor, to

rig stock momentum one way or another?

Bloomberg reports that Pravit Chintawongvanich, head of derivatives strategy at Macro Risk

Advisors, says the VIX - a gauge of the implied volatility of the S&P 500 Index derived

from out-of-the-money options - was 'gunned'.

That is, it was intentionally pushed higher.

A massive bid for protection against a tumble in equities caused

the prices of put options to soar in early trading on Wednesday,

effectively forcing up the official settlement level for VIX.

“Around 9:15, suddenly a bid emerged for the extremely far

downside options, pushing the early indication [of the VIX] up 1

point," Chintawongvanich said.

“By 9:30, the early indication was around 17.50, up over 2 points

from the 9:00 a.m. level, despite S&P futures remaining

unchanged."

Bloomberg's Dani Burger highlights some of the S&P 500 options that were at the center of

yesterday's VIX rigging speculation.

One trade of 13.9k May puts with a 1200 strike during the VIX settlement (at a

total cost of $348,000).Tied to options that gain on a 50% SPX decline... and before Wednesday, the five-session average volume for this option was just 22!

Roughly $2.1 million was spent bidding up put options with strike prices that had 50 percent downside from current levels, the strategist calculates. To visualize this manipulation better... here is a chart of the premium traded in the April VIX settlement, by strike... And compare that to March VIX settlement...

So, to summarize: with speculators the longest volatility they have ever been - and facing some very recent pain from 5 days of volatility declines - the settlement level for April was manipulated over 2 vol points higher - potentially saving the 92,913 long vol futures contracts' traders millions of dollars (among others)... at a cost of just $2 million - buying deep, cheap OTM Puts to push up the skew (the outside volatility) and thus drive up VIX (which is calculated from a strip of OTM options). Further still, as VIX was monkey-hammered higher, so the reflexive - albeit slightly delayed - reaction in the stock market was a 20 point drop in the S&P 500 (120 point drop in The Dow), which could have garnered dramatic profits for anyone who was algorithmically buying the deep OTM Puts and sell equity futures simultaneously. Still think stocks are all about fundamentals? * * * Of course, as Bloomberg reports, Cboe Global Markets declined to comment.

Last month, Cboe CEO Ed Tilly said at a conference that “the integrity of

our VIX products and markets is paramount. And, if our regulatory

team were to uncover any manipulation, it would be rooted out,

swiftly and decisively. Period.”

But, as Reuters reports, France's market watchdog did make a statement this

morning with regard manipulation of European equity volatility markets, claiming

it was "very unlikely."

Any manipulation of Europe's main gauge of stocks volatility would be "very unlikely",

France's financial markets regulator said in a research note on Thursday, following

allegations that the equivalent U.S. "fear gauge" was being manipulated.

Europe's VSTOXX, the region's equivalent to the U.S. CBOE S&P 500 volatility index VIX,

would probably be protected from any possible rigging due to the different method

used to settle prices for the VSTOXX futures, the Autorité des Marchés Financiers

(AMF) said.

"As the index is calculated every 15 seconds, 61 points are used in

calculating the settlement price of the future (as opposed to a

single point for the VIX). Given the liquidity of Eurostoxx 50

options at this time of the day, it would thus appear much more

difficult and costly to manipulate VSTOXX futures," the report said.

The AMF also ruled out the possibility of manipulation of France's volatility index, VCAC.

"Since the VCAC is not an underlying of listed derivatives, a

manipulation scheme on the VCAC index similar to the alleged VIX

manipulation may thus be ruled out," the watchdog said, adding that

no products reference the VCAC index.

Translated: It couldn't happen here...

Hedge Fund 'Beta Males' Produce

More Alpha, New Report

Today in the little known academic world of hedge fund manager gender studies, it

has been researched and reported that i f you’re a beta-male running a hedge fund,

you’re likely to generate more alpha.So if you've been looking for the mystery behind why so many hedge funds are

underperforming over the last couple of years? Well, look no further, because CNBC has

shone a light on it: too much testosterone.

That’s right, the "need to know" story of the day today from the "Delivering Alpha" section

of CNBC is a report stating that:

Hedge-fund managers with high testosterone underperform those with low

testosterone by 5.8 percent each year, according to a study conducted by

University of Central Florida and Singapore Management University.

The researchers used software to measure the facial width-to-height ratio

— proven to be a proxy for testosterone levels — of more than 3,000

hedge-fund managers. After controlling for variables such as risk and

market environment, the researchers found that not only do funds of

higher-testosterone managers produce lower returns, but those managers

also have a greater propensity to be terminated.+The report goes on to note that men with too much testosterone often are too quick

to sell and too likely to hold onto their losers:

High-testosterone managers "trade more frequently, have a stronger

preference for lottery-like stocks and are more likely to succumb to the

disposition effect," the report said, referring to the tendency of investors

to sell assets at higher prices and holding onto those that have dropped in

value.

Finally, the report goes on to state that investors who manage funds of funds are most

likely to invest with people that are like-minded. In other words, the sheep are eating

their own shit for dinner:

The researchers also found that hedge-fund investors — specifically, hedge

fund-of-funds — select managers based on their own testosterone levels.

In other words, higher testosterone fund-of-hedge funds are more likely to

invest in higher-testosterone managers, while the reverse is true for lower

testosterone.We’re not sure where the hedge fund world could’ve gotten the idea that you need to be an alpha male to dominate in finance. The two former starting NFL linebackers that make daily appearances on CNBC? Having athletes as the selling point at "Real Estate and Bitcoin Expo" scams to fleece sheep from their hard earned coin? Or perhaps it is from articles like these? Regardless of whether or not this report holds any water, it can’t be doubted that hedge funds are performing piss poor in this environment where the overall "market" has continued to provide relatively consistent returns. For much of 2017, hedge funds - most of which again underperformed both their benchmark and the broader market - complained that they were not generating alpha for one reason: there was no volatility. Well, they got their wish in spades last month when after months of record low, single-digit VIX, equity vol exploded resulting in a 3.9% slide in the S&P 500 and as 10-year yields backing up. And so with volatility spiking, and what every commentator saying it was a "stockpicker's market" hedge funds surely had a blockbuster month, right? Well, no, quite the opposite in fact: according to the Bloomberg Hedge Fund database, in February hedge funds posted an overall drop of 2.19%, wiping out all of January's gains, and leaving them flat for the year. Yes, somehow the month that all hedge funds were waiting for lead to widescale losses and last month ended up being the worst month for hedge funds since January 2016, when they slumped 2.57%.

In February we ran down which hedge funds got hit to start off 2018. Many "marquee"

names started the year off by underperforming the S&P. For some big names, like

Greenlight Capital, things have gotten even worse since then.

In late February, Einhorn said on a conference call for his Greenlight Capital Re, that his

hedge fund was experiencing its worst underperformance ever, as it suffered a 12% decline

in the first two months of the year.

Greenlight has posted lackluster returns in recent years as markets,

especially for growth stocks, have risen while the hedge fund has stuck to

its value-investing strategy.

According to Bloomberg, Einhorn’s main hedge fund fell another 1.9% in March, extending

its loss this year to 14%.The moral of the story? Next time you look to invest in a hedge fund, you may

want to consider Bill Gates instead of Bill Ackman.

The Road To 2025 (Part 1) –

Prepare For A Multi-Polar World

If pressed to describe what I think the next several years will look like as concisely as

possible, I’d simply provide the following quote, often misattributed to Lenin:

“There are decades where nothing happens; and there are weeks

where decades happen.”

There will be many such weeks from now until 2025, with the end result an emergence of a

multi-polar world that will permanently unseat the unipolar U.S. imperial paradigm.

Since World War 2, the U.S. has successfully sustained a position of global dominance unlike

anything the world’s ever seen. Virtually each and every corner of the planet has been

subject to inescapable and overwhelming American influence, both culturally and

economically. This root of this power didn’t just emerge from GDP strength and the

USD, but from Hollywood, popular music and tv shows. The impact of the U.S. empireon the planet over the past 70 years has been extraordinary but, like all things, it too shall pass. I believe this end will be realized by around 2025. When I say this sort of stuff people think I’m calling for the end of the world. I suppose that’s what it may feel like to many, because a paradigm change of this magnitude will indeed have monumental global implications. Yet the world will go on, it’ll just be very different place. That said, Americans should not see this as an apocalyptic thing. It’s not healthy or sustainable for one nation to dominate the planet in such a manner. Many of us like to think that a benevolent global empire led by philosopher kings is just fine, but the problem is this is utter fantasy. What happens in real life, to quote Lord Acton, is that “power corrupts and absolute power corrupts absolutely.” This is precisely what’s happened in the U.S. The country’s been looted and pillaged with rapacious fervor in recent decades while a unaccountable class of people I refer to as top-tier predators operate at will with total impunity. The man on the street’s thrown in jail for the smallest offense, while financiers who destroyed the global economy with fraud retire comfortably to their

mansions. The U.S. empire no longer benefits the average American, but instead

systematically funnels all the spoils to a smaller and smaller segment of the population.

Most of the world already sees it, and the average U.S. citizen is starting to see it as well.

This is not good for the establishment.

This is also why the U.S. status quo constantly lies to the public with its nonsense

narrative that U.S. military action overseas is based on humanitarian concerns and

a desire to spread democracy. Nothing could be further from the truth. In fact, all

significant U.S. military action overseas is driven by money and power. Humanitarian

concerns play zero role. Not even a small role, zero.

Caitlin Johnstone recently summarized what’s going with geopolitics perfectly with the

following paragraph:

The mass media narrative factory tries to make it about chemical

weapons, about election meddling, about poisoned ex-spies, about

humanitarian issues, but it has only ever been about expanding

the power and influence of the oligarchs and allied

intelligence/defense agencies which run the western empire. All

the hostilities that we are seeing are nothing other than an

extremely powerful conglomeration of forces poking and prodding

noncompliant governments to coerce them into compliance before

global power restructures itself into a multipolar world.

The biggest problem for the U.S. establishment right now is people are no longer buying the

narrative. They certainly aren’t buying it overseas, and even here in America, U.S. citizens

are finally starting to see the “humanitarian bombings” for the shams they are. It’d be one

thing if your average American was benefiting from U.S. empire, but they aren’t.

Rather, the spoils are all going to a small handful of people from the top tier predator class,

while life for tens of millions is characterized by dilapidated infrastructure, a completely

broken healthcare system, continued unaccountable Wall Street looting, a decimation of of

civil liberties, and an overall precarious economic existence that seems modeled off of the

Hunger Games.

The only people who don’t see how dysfunctional the U.S. empire is are the people

running it. The U.S. establishment, which consists of a diverse assortment of elites from

Wall Street, American intelligence agencies, mass media, Congress, the Federal Reserve,

the military-industrial complex, etc., disagree on many things, but one thing they agree on

completely is the U.S. empire — that it should not only be preserved, but expanded. The

major problem for them is this isn’t 1995 anymore, they just haven’t got the memo yet.

The U.S. establishment is either too busy making boatloads of money or playing

keyboard warrior with other people’s lives to acknowledge what’s happening bothhere and abroad. A disconnected, greedy and unaccountable elite class filled with hubris and an insatiable hunger for power is a core ingredient in any imperial collapse, and this exists in America in droves at the moment. A reckoning is coming. Today’s piece focused on how the U.S. empire is no longer working for the average American citizen. Part 2 will focus on why it’s not working for the rest of the world either. The Road To 2025 (Part 2) – Russia And China Have Had Enough Authored by Mike Krieger via Liberty Blitzkrieg blog, Part 1 of this series focused on how the U.S. empire no longer provides any real benefit to the average American citizen. Rather, the spoils of overseas wars, the domestic surveillance state and an overall corrupt economy are being systematically funneled to a smaller and smaller group of generally unsavory characters. The public’s starting to recognize this reality, which is why we saw major populist movements emerge on both the traditional right and left of the political spectrum in 2016. As millions of Americans emerge from their long slumber, much of the world’s been aware of this reality for a long time. They don’t see the U.S. as a magnanimous humanitarian empire, that’s a fairytale more suited for children’s books and the mass media. In fact, it seems clear that the billions of humans who live in various sovereign nations around the world would certainly prefer to be in control of their own destinies as opposed to mere vassal states of the U.S., they simply haven’t possessed the military or economic power to stand up and chart their own course. But things are changing.

The most significant geopolitical change of the 21st century is the emergence of

China, and the reemergence of Russia, as globally significant military powers. This

is the core driver behind the establishment’s panic about Russia. It has nothing to do with

Putin’s authoritarianism or human rights abuses, that’s just marketing directed at a

heretofore extremely gullible public.

In reality, those determined to perpetuate a unipolar world run by the U.S. are appalled and

concerned about the fact Russia was able to become involved in Syria and prevent another

regime change operation. Russia very publicly, and very successfully, stood up and

said “no” to U.S. imperial ambitions in Syria. This isn’t just historically significant,

it’s seen as blasphemous and recalcitrant by the U.S. status quo.

With that out of the way, let’s revisit a few things I wrote over the weekend in my first

thoughts on the latest Syria strike:

Russian leadership are not a bunch of fools, nor will they back

down. After last night, they know for certain the U.S. empire is

determined to castrate them globally at all costs in order to

impede an inevitable emergence of a multi-polar world.

I don’t think Russia or Iran will respond with a shock and awe

attack any time soon, nor will this likely spiral out of control in thenear-term. It’s more likely we’ll see this all play out over the

course of the next 5 years or so.

I also don’t expect this to go nuclear, but I think the chances the

U.S. experiences an imperial collapse similar to that of the USSR

(or like any historically unmanageable and corrupt empire) has

become increasingly likely. My view at this point is the U.S. and its

global power position will be so dramatically altered in the years

ahead, it’ll be almost unrecognizable by 2025, as a result of both

economic decline and major geopolitical mistakes. This will cause

the public to justifiably lose faith in all leadership and institutions.

The more I reflect on what’s going on, the more I’m convinced the U.S. is trying to goad

Russia into a response with these provocations. I think the Russians know this, which is

precisely why they’re responding with cool heads to a blatantly illegal and unconstitutional

strike likely based on a fake narrative. In fact, we still don’t have any reliable or rock solid

evidence of what happened. Naturally, this didn’t stop Donald Trump from bombing without

consulting Congress, nor did it stop Theresa May from doing the same without consulting

Parliament.Please tell me again about our illustrious Western democracies. I

suppose that’s just another fairytale for public consumption.

Moreover, Russia’s lack of a military response shouldn’t be seen as a sign of weakness, but

as an intentional and well thought out strategy. The Russians seem to think the U.S. (and

UK) are acting like desperate feral lunatics and the best thing they can do is sit back, play

defense, and let the short-sighted fools running the American empire ruin themselves. The

erratic and demonstrably thuggish and shady manner in which the U.S., UK and

France behaved in this latest criminal act has not been lost upon the populations

of the world, including considerable portions of the American and British populace who are

disgusted at what these governments are doing in our names. Russia’s strategy is to look

reasonable on the global stage compared to a U.S. which seems increasingly crazy and

unhinged. It seems to be working.

That being said, Russia by itself isn’t capable of successfully standing up to the

U.S. empire in the long-run. This is where China comes into play. Chinese leadership

have also had enough but are, like the Russians, holding back and acting like the reasonable

adults in the room. We saw this most recently with the Chinese cooling down the trade

wars. U.S. pundits cheered this as a sign of weakness, but I think the opposite. China’s

playing the same game as Russia. Allow U.S. leadership to continue to look like

insufferable bullies on the world stage until everyone gets completely sick of U.S.

dominance.A reader who lives in Europe wrote the following comment on my last post, which seems

like a fair representation of global public opinion at this point:

The Soviet empire fell because the cost of the arms race depleted

the rest of the society to such a degree that a collapse was

inevitable. I believe the US are in a similar state now. The current

wars are carried out by technology at distance, or by proxy

warriors, and not by actual americans on ground. How long can the

citizens carry that burden? At the same time the US is losing the

moral support within the public among their allies, as I know first

hand, by being from a european allied country. Although our

domestic politic leadership and mainstream press are supporting

the US, especially when they launch some rockets, opposition and

disbelief is large and growing among normal people. The US has

lost its posiotion as our leading star, not just among the leftist, but

all over the spectrum. The insanity and lies are becoming so

evident that it is impossible to deny it.

The U.S. is rapidly losing support and confidence at the grassroots level, both at home and

abroad. We see the lies and we see the disregard for the Constitution. The U.S. and its pet

allies like the UK and France will all be increasingly seen as rogue states by much of the

world if they keep this up.

Finally, for those of you who doubt which side China is on in this global drama, let me point

out the following excerpts from a recent editorial published in the state-sponsored Global

Times earlier this week:

The facts cannot be distorted. This military strike was not authorized by

the UN, and the strikes targeted a legal government of a UN member

state. The US and its European allies launched strikes to punish President

Bashar al-Assad for a suspected chemical attack in Duma last weekend.

However, it has not been confirmed if the chemical weapons attack

happened or if it did, whether government forces or opposition

forces launched it. International organizations have not carried out

any authoritative investigation.

The Syrian government has repeatedly stressed that there is no need for it

to use chemical weapons to capture the opposition-controlled Duma city

and the use of chemical weapons has provided an excuse for Western

intervention. The Syrian government’s argument or Trump’s accusationsagainst the “evil” Assad regime, which one is in line with basic logic? The

answer is quite obvious.

The US has a record of launching wars on deceptive grounds. The

Bush government asserted the Saddam regime held chemical weapons

before the US-British coalition troops invaded Iraq in 2003. However, the

coalition forces didn’t find what they called weapons of mass destruction

after overthrowing the Saddam regime. Both Washington and London

admitted later that their intelligence was false.

Washington’s attack on Syria where Russian troops are stationed

constitute serious contempt for Russia’s military capabilities and

political dignity. Trump, like scolding a pupil, called on Moscow,

one of the world’s leading nuclear powers, to abandon its “dark

path.” Disturbingly, Washington seems to have become addicted to

mocking Russia in this way. Russia is capable of launching a destructive

retaliatory attack on the West. Russia’s weak economy is plagued by

Western sanctions and squeezing of its strategic space. That the West

provokes Russia in such a manner is irresponsible for world peace.

The situation is still fomenting. The Trump administration said it will

sustain the strikes. But how long will the military action continue and

whether Russia will fight back as it claimed previously remain uncertain.

Western countries continue bullying Russia but are seemingly not afraid of

its possible counterattack. Their arrogance breeds risk and danger.

China and Russia will work together, often behind the scenes, to convince the rest of the

world that the U.S. has become a rogue state, and will use this argument to build

international support for a multi-polar world. The only thing that could slow this

process down is if the U.S. stops acting like a rogue state, something that appears

increasingly unlikely with Mike Pompeo as Secretary of State and John Bolton as National

Security Advisor.

Part 3 will focus on the weak link in U.S. imperial dominance, the USD.

Michael Krieger@LibertyBlitzYou can also read