Allianz UK Opportunities - UK Domestics - a phoenix from the ashes? - Allianz Global Investors

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Allianz UK

Opportunities

UK Domestics – a phoenix

from the ashes?

For professional investors only Q1 2018

In a longer report on UK equities, Matthew Tillett, manager of the Allianz UK Opportunities

Fund, looks at the UK domestic debate: the myths and realities, the opportunities and risks. What is

driving UK domestic share prices, their valuations, and what the Fund has been doing as a result

Matthew Tillett, Portfolio Manager

D uring 2017 the Allianz UK Opportunities Fund returned a

respectable 15.5% net of fees and expenses, ahead of the

FTSE All Share 13.1% total return. It was certainly an eventful year

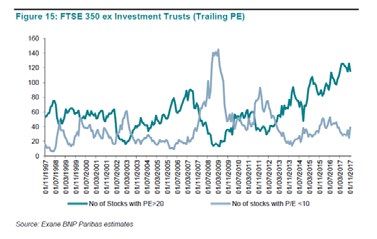

FTSE 350 ex Investment Trusts (Trailing PE)

for UK investors. There was a surprise general election with an

even more surprising result, plus a number of mildly concerning

geo-political developments for investors to worry about –

although clearly not enough to stop the markets continuing their

bull run with remarkably low volatility.

What is most interesting to me is that despite the apparently

calm market environment at the index level, there has actually

been an unusually high level of sector and stock specific

Source: Exane BNP Paribas estimates.

divergence. This has been (and still is) a very momentum driven

market. There seems no limit to the valuation multiples the stock As a contrarian value driven investor, I love this sort of

market is prepared to ascribe to companies that are in sexy environment because invariably there are opportunities within

sectors such as technology. Meanwhile other areas that are out of those stocks that are deeply out of favour. Here I want to hone in

favour seem even more depressed than usual. Indeed the FTSE on one area in particular: UK domestic stocks, and specifically the

350 currently has the highest number of stocks with valuations in consumer facing companies.

excess of 20x p/e that it has ever had in its history. Yet it also has a

many stocks with p/e ratios below 10x, at least as many as its long

Undervaluing the domestic consumer?

run average. This is an unusual situation, and arguably not a This is a group that, with a few notable exceptions, has

particularly healthy one. It suggests a lack of market breadth with performed poorly since the EU Referendum vote. Over this

investors chasing momentum stocks ever higher at the expense period, the Fund has been increasing its exposure to UK domestic

those that are out of favour. stocks through the addition of a number of new holdings, many

To find out more please visit

www.allianzgi.co.uk

Allianz UK Opportunities

of which have some degree of consumer exposure. The shape of of them are operating in a much smaller market than their

the Fund has changed quite materially as a result of this. Prior to international peers. For me, as someone who is completely

the EU Referendum vote, the Fund had a very low exposure to UK agnostic to the composition of the benchmark, the domestically

domestic stocks (and virtually nothing in the consumer space), focused group of companies offer one of the largest hunting

whereas today this is one of the more significant exposures in the grounds investment ideas.

fund. So far this change has not added much in the way of alpha,

however looking forward I am optimistic that over the next few

Post-referendum depression

years these holdings can contribute significantly to the Fund’s There has been a lot of share price volatility amongst these

performance. companies since the surprise EU Referendum result in June 2016

as investors have downwardly reappraised their short- and long-

This report will explain the thinking behind this view. I will start by

term expectations for the UK economy. Sentiment has soured.

introducing the “UK domestic” universe, detailing the main

Most observers expect the economy to deteriorate or even fall

companies and sectors that make up this broad group. I’ll then

into recession. Moreover, many domestic companies, particularly

discuss the high level macro concerns that are depressing

those in the consumer sectors, are now under an ever darkening

valuations and why I believe these concerns to be misplaced.

structural cloud as Amazon and other online operators threaten

Honing in specifically on the consumer cyclical group – probably

to drive a truck through their business models.

the worst affected – I’ll show why I am still finding compelling

investment opportunities, although the outlook varies These are legitimate concerns. However, I believe the now

enormously by company and as a result it is important to have a widely-held bearish view is an over simplification of the reality.

robust framework to help identify the winners and avoid the For sure Brexit has created short term economic and political

losers. I will then cover each of the six investments the Fund has uncertainty and it is a logistical nightmare for all those tasked

within the domestic consumer cyclical group, concluding with with implementing it. But the long-term economic impact

some comments on what this means for the Fund’s overall remains to be seen. And yes there are plenty of domestic

positioning. consumer companies that will continue to struggle or die, but

there are also those that can survive and thrive in the Amazon

Domestic or domiciled? era. Valuation is the ultimate harbinger of long-term returns and

When I am asked my view on the prospects for the UK stock in this respect domestically focused companies have one big

market, I almost always begin my reply by pointing out that the thing going for them today: they are almost universally lowly

UK stock market is not the UK economy. Those of us who live and valued. Finding the long-term winners and investing in them at

breathe the UK stock market are well aware of this, but many low valuations has the potential to be very profitable, but to do

people I speak to are surprised to discover that domestically this requires first having a robust framework to identify who the

focused companies actually account for only a minority of the winners are.

overall stock market capitalisation. This is because so many of

the big “mega cap” companies – household names such as Shell,

Identifying the real domestics

Unilever, Glaxosmithkline and HSBC – are predominantly What does the domestic group look like once it is broken down

international businesses with very little domestic UK exposure. into its component parts? There are many ways to try and cut

Furthermore, most of these companies have, over the years, this. The approach I have taken is to include only companies that

become ever larger beasts as they have merged or acquired their derive at least 75% of their revenues from within the UK. This is

rivals in their bids for global dominance and scale. The top ten admittedly quite a tight criteria but it is still a significant number

companies in the FTSE All Share by market capitalisation account of companies. Apply it to the FTSE 350 and around 35% make the

for a whopping 42% of its overall market capitalisation and none cut. The breakdown is as follows.

of them are domestically focused1.

Consumer cyclical, 28%

However this observation does not negate the importance of

Financials, 19%

having an effective investment strategy for the domestically

Real estate, 16%

focused companies. They may be in a minority but it is Housing and housing related, 12%

nevertheless a significant minority. Most estimates I have seen Consumer staples, 8%

suggest somewhere between 25% and 30% of the FTSE All Share Utilities, 5%

by revenue is domestic. Remember also that the FTSE All Share is Commercial services, 4%

weighted by market capitalisation which means the larger the Telecommunications, 3%

company the more important it becomes within the index. If Transport, 3%

Construction, 2%

instead every company were given an equal weighting, a more

balanced picture emerges. This is because domestically focused

companies tend to be smaller in size, reflecting the fact that most

Source: Bloomberg, January 2018.

Allianz UK Opportunities

This is clearly a vastly different picture to the broader market, These valuation moves imply that market expectations for the

where sectors such as energy, mining, pharmaceuticals and domestic group of companies, and particularly the consumer

consumer staples dominate. It is also more cyclical. Consumer cyclicals, are very depressed. Why is this the case and is it justified

cyclical, which includes retail, leisure and entertainment, accounts by the facts on the ground?

for more than a quarter of the group. Housing and real estate are

also notoriously cyclical sectors. Financials is a diverse group that

Why are domestics so undervalued?

includes the highly cyclical domestic banks. At a macro level, I think there are three assertions that underpin the

current bearish narrative. Firstly, in the short term Brexit has created

How have domestics performed? an environment of economic and political uncertainty in which

Looking at share price performance reveals how starkly these businesses will delay or cancel investment spending while they

companies have underperformed over the past two years. In the await clarity on the final exit deal that the UK does (or doesn’t!) end

chart below you can see the share price performance of the FTSE up signing. The Government is weak without a majority, whilst the

350 index compared to “All domestics” (both in bold), with the opposition Labour party appears to making ground with its left-

latter having fallen by 6% whilst the former has risen nearly 20%. wing agenda. Consumer spending will also be under pressure in

This underperformance is all the more apparent when you this weaker economic environment, compounded by weak sterling

consider that the domestic group is included within the FTSE 350 which causes inflation to run ahead of wage growth. Secondly,

index itself, which implies non domestic companies have returned whatever the final Brexit agreement ends up being, it is very likely to

more that 20%. One important caveat here is the role of currency. be negative because there will be restrictions on access to all or part

Sterling has depreciated by 10% against the dollar and 16% against of the single market with the inevitable consequence that jobs and

the euro over this period2. This has obviously been a boon for the industry will move to the continent. This could well be a drag on the

earnings of the non domestic companies, but it is clearly not economy for many years to come. Finally, irrespective of Brexit, the

sufficient on its own to explain these divergent moves. UK economy is in a fragile state anyway. Both the consumer and

government are highly indebted, limiting the flexibility of the

Domestic UK share price performance versus FTSE 350 index

economy to respond to economic pressures.

Unpicking the Brexit effect

130

120

110

It is certainly not difficult to find purveyors of this narrative. The

100

90

economics profession seems more or less united that Brexit will be

80 bad for the economy. Most of the mainstream financial press such

70 as the Financial Times and the Economist seem vehemently anti-

60

Brexit. The Treasury famously predicted imminent recession if the

50

country voted leave. At times it can be difficult to extricate oneself

Oct 2016

Mar 2016

Oct 2017

May 2016

Mar 2017

Jun 2016

Jan 2016

Feb 2016

Aug 2016

Sep 2016

May 2017

Jun 2017

Apr 2016

Aug 2017

Sep 2017

Jul 2016

Nov 2016

Dec 2016

Jan 2017

Feb 2017

Apr 2017

Jul 2017

Nov 2017

Dec 2017

FTSE 350 Domestic banks

from this torrent of negativity, but staying objective in these

Domestic real estate All domestics situations is critical to successful long-term decision making. To my

Domestic consumer cyclical Domestic house building & housing related

mind, the economic situation is far more nuanced, and certainly

less bad than suggested by many of the bears.

Source: Bloomberg, AllianzGI estimates, January 2018.

It is important to remember - especially for those of us living in

It is also striking how dreadful the consumer cyclical group has

liberal-leaning London - that over half the country voted to the

been, languishing nearly 15% below the level of two years ago and

leave the EU. Many live in poorer parts of the country, they don’t

trailing the index in relative terms by over 35%. You might be

read the liberal press and have little interest in Westminster

thinking this reflects a deteriorating earnings profile in the wake of

politics. They are not unhappy about the Referendum result and

a weaker UK economy and consumer. There certainly have been

there is little reason to expect them to change their behaviour

some high profile profit warnings amongst these companies, but

because of it. For sure, the consumer environment has weakened

many have actually held up surprisingly well. A lot of the

moderately since the vote, but much of this can be explained by

underperformance can be explained by a valuation de-rating: The

negative real wage growth. The fall in sterling has caused import

median price-to-earnings (p/e) ratio for the consumer cyclicals

prices to rise, resulting in inflation in excess of wage growth. This is

group has fallen from 16x at the beginning of 2016 to 13x today,

certainly a head wind but it may prove a temporary one. Sterling is

although there is a wide range with some high street retail and

well off the lows - $1.35 as I write this - so the outlook for next year

leisure companies languishing well below 10x. Over the same

is much improved on this front. Moreover, employment itself has

period, the p/e ratio for the overall market has actually risen

remained buoyant. Real wages did not grow during 2017 but total

modestly from 15.5x to 16.0x3.

hours worked have continued to show a steady rise, and looking

Allianz UK Opportunities

forward the ongoing rises in the minimum wage should provide the UK will have the opportunity to change the way it trades with

some support to the consumer and the economy. the rest of the world, potentially for the better – although actually

achieving this this is far from guaranteed. I personally voted

UK employment – total weekly hours worked

Remain because I think the supposed benefits from being

outside the EU are unproven, very long term and will involve a lot

of “execution risk”. But I remain open minded as to how this may

play out and I certainly wouldn’t write off the long-term

prospects for the UK economy.

Interpreting sterling moves

Another misunderstood factor at play is the fall in the pound.

Some commentators have interpreted this as a sign of the

weakness of the UK economy, resulting in higher inflation and

potentially forcing the Bank of England to raise interest rates. I see

the fall in the pound as part of the adjustment process - a one off

correction that improves the UK’s terms of trade in response to a

Source: Office for National Statistics, Bloomberg, January 2018

negative external development. In economics jargon, this is

Look at business investment and a similar picture emerges. At the known as “the home market effect”. In a free trade area, in which

time of the Referendum vote, there was no shortage of dire there are products or services that can easily be produced in

warnings from the doom mongers predicting a mass exodus of different countries, the home market effect says that production

business and a collapse in investment spending. The reality is will tend to gravitate towards those areas with geographic

that business life has plodded along in a somewhat subdued economies of scale because this minimises the frictional costs

state – not great but certainly no disaster. Most companies I such as transportation and logistics. Production may still

speak to are nervous about Brexit but they have not radically continue in other areas but there will need to be some offset

altered their investment intentions. Of course this could change such as lower wages in order to compensate for the higher

for the worse depending on what ultimately happens, but for frictional costs.

now at least the situation appears manageable.

Now think about the UK’s financial services sector in the context

UK business investment of the home market effect. Many commentators expect a mass

exodus to Europe in a post Brexit world as the City of London

loses its relevance. More likely in my view is the downward

adjustment in the pound serves to compensate (through lower

costs) for the increased frictional costs of doing business in a City

of London that is outside of the EU. Of course this doesn’t mean

all is well for the financial sector. There will be some jobs that

have to move for regulatory reasons and the pound may yet need

to fall further in the event the exit deal is very bad for the UK. But

ultimately I expect the pound to do most of the heavy lifting here.

It is also worth keeping in mind those parts of the UK economy

that stand to benefit from a weaker pound, such as the poorer

manufacturing areas or the tourist industries. These areas could

Source: Office for National Statistics, Bloomberg, January 2018 see a renaissance in a post Brexit Britain.

The longer term outlook is clearly much harder to call. The EU is a The political reality

large free trade area in which the UK conducts a significant Some have argued that domestic politics – the fear of Jeremy

volume of its trade. The country is also deeply embedded within Corbyn - rather than Brexit explains the low valuation of domestic

intra European supply chains, many of which rely on standardised stocks. But this is not convincing either. First of all it would need

practices, rules and regulations (“non tariff barriers”). Other the Government to fall. The ruling Conservative party is

things being equal, losing access must be an economic negative desperate to keep Labour out and ensure that they can push

because the cost of trading with the EU will go up. But, as is through their version of Brexit. They will do everything they can

usually the case with economics, other things are not always to avoid an election, which paradoxically strengthens the Prime

equal. The EU is itself a protectionist block. The region’s taxpayers Minister’s position even though many in her party would like to

incur significant costs subsidising industries such as agriculture replace her if they could. Secondly, it is true that Labour did

which are not competitive internationally. Leaving the EU means surprisingly well in the 2017 General Election, but this was against

Allianz UK Opportunities

very low expectations. With hindsight the Labour vote benefited because companies have to pay workers more so that they can

from a surge in turnout amongst young voters attracted by the afford their living expenses.

prospect of free university tuition and disaffected Bremainers that

wanted to punish the Tories. These swings may not be sustained. It would obviously be a gross simplification to say that housing is

More importantly, they have little if anything to do with some of the only issue that matters, but I do believe that many of the UK

the supposedly hard left anti-capitalist policies that Labour have economy’s structural problems stem from housing. It is certainly

proposed. Finally, even if Labour were to get elected, it is not clear not a great situation, but equally it is not a disaster, and certainly

to me that this would even be that bad for the economy. I have not bad enough to preclude looking for investment opportunities

read the Labour manifesto and it is a long way from the scare amongst some very cheap domestic stocks. It leads me to focus

stories that I hear people talking about. There is a suggestion of my attention on strong franchises with distinct business models,

raising taxes, but this would fall on the richest 5% of the population companies that have a good chance of doing well even in a weaker

(those earning over £80,000 per year), and the proceeds would be environment. Where might these opportunities lie and how to go

used to fund increased spending and support for poorer sections about sifting the wheat from the chaff?

of society. Not great news if you’re a highly paid banker, but Since they account for nearly 25% of the total, the consumer

possibly not such a bad thing for an economy where inequality has cyclical companies are the obvious place to start when

been rising and consumer spending has been under pressure. formulating a stock picking strategy for the UK domestic group.

Overall the tone of the Manifesto reminds me of the mixed The valuation case is clearly compelling, both in absolute terms

economy models in Europe. This may not be everyone’s cup of tea but particularly relative to market. However there is another factor

but it’s hardly a disaster. holding the consumer cyclical companies back, in addition to

The economic prognosis Brexit related concerns: their business models are under varying

degrees of pressure from the ongoing online channel shift.

Putting Brexit to one side, it is the health of the UK economy itself

where I have the most concerns. This, combined with valuation Specific threats: online disruption?

considerations, was the main reason for the Fund’s very low The problem is most apparent for traditional “bricks and mortar”

weighting to UK domestic stocks in the period prior to the EU retailers. These companies are heavily reliant on in-store sales and

Referendum. Today, with valuations having de-rated so far, the must maintain an expensive store base to support this part of their

question now is whether the UK economy’s predicament is so bad business. Unfortunately their customers are increasingly choosing

as to justify these valuations. to do their shopping online, which means they must invest heavily

in online capabilities. But this is also an expensive business to be

The primary problem facing the UK economy is the high level of

in. A slick website backed up by an efficient logistics and delivery

consumer debt. The housing market is critically important in the

service are necessities just to have a seat at the table.

UK, much more so than in other countries. Hampered by a

sclerotic planning system and numerous vested interest groups, Furthermore, online is usually more competitive due to the price

successive governments have totally failed to deal with the supply transparency it gives to the consumer. Amazon’s entire business

issue causing house prices, particularly in the south east, to keep model is based around providing the lowest prices possible

on rising to ever higher multiples of household income. combined with the best service and the company is happy to run

Government support schemes such as Help to Buy have made it at wafer thin margins to achieve this. Many traditional retailers

easier for people to buy but have done nothing to aid supply and find themselves stuck between “the rock” of stagnant or declining

so arguably have made the underlying situation worse. The result store sales and “the hard place” of brutally competitive online

is highly indebted consumers and a financial system whose competition. For many it is hard to see an obvious solution. Some

primary purpose is to fund and support the housing market. won’t survive whilst others will be weakened, forced to invest

more and operate at lower profitability. Valuation alone will not be

I am not in the camp that sees this all collapsing in on itself,

a defence here. The good news is that the outlook is far from dire

primarily because I don’t see how this can be allowed to happen.

for all domestic consumer facing companies, even amongst the

The country is limit-long the housing market - it is too big to fail.

traditional bricks and mortar retailers. The potential investment

But this fact has other implications. It means that interest rates are

opportunity lies in finding those companies with business models

likely to stay low for a very long time so that the debt can easily be

that are misunderstood, where low valuations imply cyclical and

serviced. I expect this to remain the case in the event inflation

structural problems but where fundamental analysis shows these

were to rise again. The currency may also stay weak as interest

fears to be misplaced. The retail sector itself offers an interesting

rates lag other developed countries. And high housing debt means

case in point.

the outlook for consumer spending is likely to remain subdued

since consumers must keep diverting large chunks of their Identifying vulnerable businesses

disposable income to debt service. Finally persistently high house

prices weigh on corporate competitiveness and productivity To understand how vulnerable a retailer’s business model is, a

sensible place to start is the product itself. Here I think there are

Allianz UK Opportunities

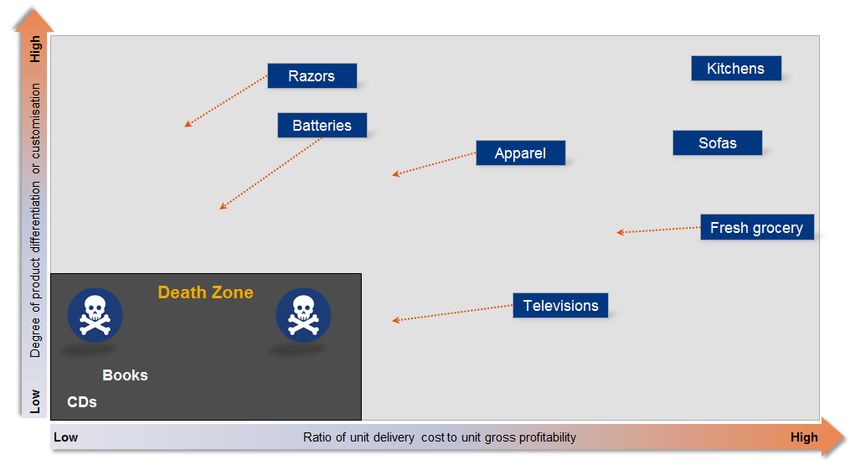

two critical variables to consider: Is it easy to deliver? How unique profitable gross margin sale for store based retailers. But books

or differentiated is it? are easy to deliver and most consumers are very happy to buy

them online. No surprises that this was one of the first products

The economics of delivery matter enormously because this is

that saw its profit pool decimated by Amazon.

one of the main costs for a pure online business model. Note that

it is the total cost of delivery that matters here – i.e. including the There are a number of product categories in the middle ground,

cost of returns and the amount of stock that has to be held to such as apparel and grocery where online delivery works but it’s

service the customer base. Also delivery cost needs to be not that profitable, however the danger is that these categories

expressed in terms of the product’s profitability. A high gross may be moving to the left over time as logistics systems and

margin product lends itself better to a pure online model supply chains improve. That doesn’t mean its curtains for the

because there is a larger in-store profit pool for the online retailer traditional store based retailers, but they will need to make sure

to go after. they keep up with the pure online operators which could prove to

be expensive in terms of capex and margin.

Product differentiation matters because this may indicate how

likely consumers are to become comfortable with a pure online The traditional consumer staples categories are also under threat

sale. Branded products typically fare better, particularly when from online models. These products have high gross margins

consumers like to touch or feel the product. And even if sales do and many are easy to deliver. Historically consumers have been

move online, the brand owner has a better chance of controlling prepared to pay a premium for these trusted differentiated

the distribution and pricing than they would for a homogenous brands (top left quadrant), but there is increasing evidence that

product. Some product sales also involve a degree of assistance this is changing now as consumers are more willing to trust

or support due to the product being unique or customised to online only brands. Amazon for example is already one of the

some extent. Again this is less well suited to pure online models largest retailers of batteries via their own brand.

because the customer will often need to be in a physical space

Products that are most likely to weather digital disruption best

anyway to see the product and discuss the options.

are those that score well on both of these variables (top right

The schematic above combines these two variables together. By quadrant). It is here where consumers will be less likely to opt for

locating where a particular product sits and, importantly, where a pure online sale and, even if they do, fulfilling that sale much

it may be moving to in future, it is possible to gauge how exposed more profitably than a store sale is difficult to achieve with

it is to the threat of online disruption. consistency, making the traditional retailer less vulnerable to a

lower cost online competitor. This thinking partly explains the

The worst place to be is in the bottom left quadrant. This is the

two UK retail companies owned in the fund today.

graveyard of online disruption. Books used to be a relativelyAllianz UK Opportunities

Two undervalued UK stocks: DFS and Howden buy it. It is an infrequent sale that requires a high degree of

assistance and customisation. The gross margins are relatively

DFS Furniture is the UK’s leading retailer of upholstered

attractive compared to many other sectors, but delivery is

furniture. The company has 30% market share which it has built

expensive due to the bulky nature of the product. Much like sofas,

up over many decades of organic and acquisitive growth. Sofas

these attributes are specific to a kitchen and are unlikely to

are bulky, heavy items that are expensive to deliver. Most people

change much in future. Howden’s business model is vertically

like to sit on a sofa before they buy it, which is why companies

integrated. They design and manufacture much of their own

trying to sell sofas usually have some sort of physical presence. It

product and ensure that they always have excellent availability of

is also not really possible to run an in-stock model. Consumers

stock for their customers. That they sell only to the building trade

like to have a lot of choice when buying a sofa, making it

provides the business with a degree of insulation from online

impractical for a sofa retailer to hold everything in stock. Instead

price transparency – a subtle but important point. Trade

the industry operates a made-to-order model which relies on the

customers all receive a confidential discount from Howden and it

retailer having a strong supply chain that can reliably fulfil

is then up to them how to price the kitchen to the end customer,

customer orders. Importantly these attributes are intrinsic to the

who as a result never really knows the actual price that was paid

sofa itself and help to explain why online only models have not

to Howden for their kitchen.

really taken off. It seems unlikely to me that this will change

greatly in the future. For sure, over time customers will do more Much like DFS, the financials show a clear picture of scale leading

and more research online and may become more comfortable to superior economic returns. Howden has consistently delivered

buying online. But this fact alone should not be sufficient to higher organic growth and higher returns on capital that all of its

undermine DFS’s strong market position since any online only peers. Our own regular Grassroots research has shown that this is

competitor would still need to replicate DFS’s supply chain, not coming at the expense of customer service, price or quality.

distribution and advertising reach - the latter alone amounting to Indeed Howden usually scores best in class overall when we

some £80m in spend per year, more than three times the size of speak to trade customers. At the time of writing Howden shares

the next largest competitor. are valued at 13.5x cash adjusted earnings. This is higher than

DFS and most other domestic UK retailers, which reflects the

Looking at DFS’s long-term financials reveals a consistently

more consistent organic growth the company has delivered.

higher level of profitability than smaller peers, suggesting that

However, in my opinion, it is still not especially expensive in

the company is deriving a genuine financial benefit from scale.

absolute terms and particularly compared to the market as a

Most recently the company has been using the current weaker

whole.

trading environment to further strengthen its market position by

mopping up struggling competitors at knock down prices. Looking forward, I am optimistic that both DFS and Howden will

Management aim to run the business at 1.5x net debt / EBITDA, deliver strong returns for the Fund through a combination of

which some analysts have argued is too high for a cyclical retailer. dividends, earnings growth and a re-rating. The latter may require

I have some sympathy with this, however this is not a show some patience as market sentiment could remain depressed as

stopper because the business model itself is resilient. Even during Brexit negotiations drag on and the consumer environment

the global financial crisis, when a number of its competitors went remains subdued. But in the meantime both companies have

bankrupt, DFS produced an EBITDA margin of 8%. In the unlikely been improving their competitive advantages, generating strong

event this happens again, the company would be well within levels of cash flow and paying healthy dividends.

their debt covenants and should have no difficulty at all servicing

their debt. DFS shares have performed poorly over the past two Opportunities in Leisure

years. Like for like sales fell during 2017, impacted by a weaker Another area that greatly intrigues me is leisure and

consumer environment and very unfavourable weather over the entertainment, where share prices have also been hit hard in the

critical bank holiday trading periods. This has caused a substantial period since the EU Referendum result. This is understandable

de-rating of the shares, which now sit on 10x cash backed and consistent with the stock market’s broader worries as to the

earnings. I think this is a very compelling valuation for the market health of the UK economy and consumer. In contrast to the retail

leader in an industry that, whilst mature, is not structurally sector however, the long-term outlook for most of these

challenged and which I believe has the potential to grow over the companies is brighter for two reasons.

long-term at least in line with GDP.

Firstly, online disintermediation is a much less serious risk. Most

Howden Joinery is the UK’s leading designer and retailer of leisure or experience-based activities still happen somewhere

fitted kitchens, with 25% of the overall market and over 50% of the and involve some physical participation or interaction with other

trade market. Kitchens also don’t lend themselves well to online people. Whatever one thinks about the prospects for virtual

only sales. Aside from the very low end, most customers like to reality, it is hard to imagine a world in which consumers no

touch and feel the kitchen they are going to live with before they longer want to consume any traditional leisure andAllianz UK Opportunities

entertainment. Companies that sell these products and services to cost inflation that the company has struggled to absorb. Finally,

should be able to prosper over the long-term provided they as often happens in these situations, structural concerns relating

invest in their assets and make sure ensure they are offering what to pubs as an industry have returned to the fore. The first two

customers actually want. factors are clearly not helpful but I believe they are largely cyclical

in nature and already reflected in the extremely low valuation of

Secondly, there is evidence consumers are increasingly

the shares. It is true that on-trade spending on beer has been

preferring to spend their discretionary incomes on leisure

declining, but this has been the case for over twenty years now.

activities at the expense of physical goods. It is not clear exactly

Well run pubs have offset this trend by convincing consumers to

why this is happening, although in part it probably reflects the

spend more on other drinks and food. I see no reason why pubs

behavioural preferences of Millennials, a group which is growing

cannot continue to do well provided they are offering an

in importance demographically. Whatever the reasons, the

experience that consumers actually want. I am confident, that if

trend, as shown in the chart below is pretty clear.

Greene King management understand they will make the right

Consumer spending growth by category investment decisions across their asset base.

10% The Fund’s investment in Greene King has so far been

8% disappointing with the shares having de-rated further from our

6% initial purchase price. At the time of writing, the free cash flow

4% yield is well north of 10% and the price to book value is 0.75x, on

2% an asset base a large part of which has not been revalued for

0%

many years. This is a huge margin of safety for a largely asset

-2%

backed business and certainly sufficient to compensate for the

-4% Apparel Foodservice

Bars and cafes Restaurants prospect of a short term period of weaker trading.

-6%

Store retailing Department stores

-8%

Ladbrokes-Coral is a betting company I have followed closely

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

for a number of years. The company struggled with their online

Source: Euromonitor, Berenberg, January 2018 offering for a number of years, causing them to lose a lot of

market share to competitors. But the combination of the merger

Whilst valuations here are generally higher than in the domestic

with Coral (which has a superior online platform) and increased

retail sector, in most cases they are still low by historical

investment has now largely rectified this problem. Momentum

standards. There is also wide range of companies in different end

within the business has turned positive, evidenced by a run of

markets, some of which are quite niche with their own internal

earnings upgrades over the past 12 months. I bought shares for

dynamics and long-term drivers. All of this makes for fertile

the Fund in September of 2016 after a very strong meeting with

ground for stock picking and it has been key area of focus for me

management which convinced me that the operating

over past 18 months. The Fund currently has 10% exposure across

momentum within the business would continue. At the time the

four quite different companies, three of which have been added

shares were languishing on a very low valuation due to the

since the EU Referendum vote.

political cloud hanging over the entire sector. The long-running

Four from the fund: regulatory review into fixed odds betting terminals (FOBTs) is

likely to recommend a reduction in the maximum stake to

Greene King is a diversified UK pub company with both a anything from £2 to £40 and where this comes in will have

tenanted and managed portfolio of pubs, the latter including a significant implications for the profitability of the retail shops

number of brands across different price points. This is a capital since FOBTs are a key component of shop profitability. But the

intensive industry because the pubs are mostly owned outright shares were already pricing in the worst case scenario, hence

and when they are managed internally they must be invested in buying in the face of this uncertainty was entirely logical. Since

continually to ensure they are appealing to consumers. Greene then Ladbrokes-Coral has been the subject of a bid approach at a

King has demonstrated a strong long-term track record of capital substantial premium from GVC Holdings, a pure online

allocation stretching back many decades. The combination of competitor that is more geographically diversified. The deal logic

organic and inorganic growth has allowed a steady is consistent with the broader trends within the industry that

compounding of asset value, free cash flows and dividends. point towards increased benefits from scale. The demands of

However since the EU Referendum vote, the shares have found technology, marketing and regulatory compliance are likely to

themselves under a dark storm cloud, hit by a number of grow over time, in my view, and if so, this will favour the larger

negatives. Firstly, sentiment towards the UK consumer has existing incumbents.

deteriorated and this has, to some extent, been reflected in

weaker trading at the company, at least during the second half of Ten Entertainment is the owner and operator of the “Tenpin”

2017. Secondly, the mandated rise in the minimum wage has led brand in the UK ten pin bowling market. The company is the no.2Allianz UK Opportunities

in the market behind Hollywood Bowl. The industry has gone two main reasons for this. Firstly, with the benefit of hindsight, it

through something of a renaissance since the depths of the is clear that the company had been mismanaged for a number of

2008-9 recession when the combination of a consumer years. Previous management was overly focused on opening

downturn and the impact of the smoking ban led to a near death new centres and neglected to invest in their existing estate which

experience for most ten pin bowling operators. Long gone are had become increasingly tired and uncompetitive. Secondly, in

the days of dark and dingy bowling alleys, uncomfortable shoes order to support the growth of the market, the Football

and unwelcoming arcade halls. Tenpin and Hollywood Bowl have Association made funding available for low cost competitors

been moving the offering away from a niche specialism so that it entering the market. This further exacerbated the problem by

appeals more to families and friends as a leisure activity. This has making it even harder for Goals to justify their premium pricing.

meant making the venues more visually attractive, with The good news is that all of this is in the process of being

improved food and beverage offering and a different arcade rectified. The company has a refreshed and high quality Board

offering. It has cost a lot of money to do this, but the results speak that has taken what I feel are the necessary steps, including

for themselves. Both companies have delivered impressive raising a small amount of equity in order to fund an extensive

organic growth, taking significant market share from the tail of reinvestment programme to upgrade all the pitches and

under-invested independent operators. Moreover they are also clubhouses. Much of the capital expenditure has already been

now highly profitable, which makes it seem likely in my view that spent but I believe it will take until 2018 and 2019 until the impact

this process could continue. really becomes clear in terms of improved sales growth, however

early signs are encouraging. In addition, Goals has recently

Unusually, I bought shares in Ten Entertainment at the company’s

announced a 50 / 50 joint venture partnership for its US business

IPO earlier in the year. The price, which came right at the very

with City Football Club, the owner of Manchester City, one of

bottom of the range, was a very attractive one. The free cash flow

largest and well known football brands in the world. This joint

yield was well above 10% and the company had very little debt on

venture arrangement provides the funds to roll out the US

its balance sheet. The shares did very little until the company

business to 6 centres and also the use of all CFG’s branding and

reported half year results in September 2017, which showed

marketing relationships. It was also done at a valuation very

continued organic growth and profits growth. This caused them

substantially in excess of that which the shares trade on. So whilst

to rally nearly 50% into the year end, and I believe the company

this investment has been very frustrating and disappointing for

has the potential to grow further.

the Fund, it is potentially one of the holdings I am most excited

Goals Soccer Centres is the UK’s leading operator of outdoor about.

small sided soccer centres. The company has 46 centres in the The overall strategy

UK and 3 in the US. The end market is small and niche but it is

growing. In the UK, soccer remains a key hobby for many people What does all this mean for the Fund as a whole? The chart below

both recreationally and on a competitive level. The small sided shows how much of the Fund has been invested in UK domestic

format is more practical for most people and as a result has been stocks over the past three years. From a very low base in 2015, the

taking share from 11-a-side, a trend which seems likely to exposure has risen to just shy of 40%, most notably during the

continue. In the US the dynamics are even more attractive latter half of 2016 and 2017 as the Fund has added new positions

because soccer is very popular but the market is underserved, such as those in the consumer sector outlined above (the pink

giving Goals an excellent opportunity to roll out their model. bars), but also a number of other interesting companies in other

Goals has a unique business model in that most of their centres domestic sectors. But it is important to remember that over 60%

are held on long leasehold land that is owned by public bodies. of the Fund is still invested predominantly outside of the UK

Goals provide the facility which is available for use by local economy. This has been an important shift but the Fund is not

schools during the day with the commercial operation running in betting the farm on the UK economy.

the evening and at weekends. It is has taken many years to build

Portfolio exposure to UK domestic stocks

up this position. Public bodies are typically conservative, slow

moving and not keen on letting go of their land unless it is to an 45%

40% UK domestic defensive

established operator. The same is true in the US where Goals had 35% UK domestic cyclical

been operating a test site in Los Angeles for many years and only 30% Domestic consumer cyclical

25%

now is commencing a broader roll out. 20%

15%

10%

Of the four companies that the Fund owns in the leisure and 5%

entertainment space, Goals is the only one that was held before 0%

12/31/2013

12/31/2014

12/31/2015

12/31/2016

29/12/2017

3/31/2014

6/30/2014

9/30/2014

3/31/2015

6/30/2015

9/30/2015

3/31/2016

6/30/2016

9/30/2016

3/31/2017

6/30/2017

9/30/2017

the EU Referendum vote, although most of the current position

has been bought in the past year. It has not been a successful

investment so far. At the time of writing, the shares are valued at

9x p/e and are languishing close to their all-time lows. There are Source: AllianzGI 29 December 2017Allianz UK Opportunities

A natural question to ask is why the Fund hasn’t gone further, capitalise on potential opportunities should this occur. And

given the arguments I’ve put forward in this report. One of the outside of the UK, the Fund is still finding compelling investment

most challenging aspects of fund management is to achieve the opportunities in specific areas such as energy, aerospace and

appropriate balance of aggression and defensiveness for any defence (a subject for a later report). Whilst these have mostly

particular environment. Although I see very compelling value now outperformed the Fund’s UK domestic holdings, they

in UK domestic stocks, there is no escaping the fact that the UK is nevertheless continue to be attractive.

still in a highly uncertain situation. The situation is fluid and liable

to change for better or for worse. Investor sentiment is jittery to

say the least and I would not be surprised to see valuations fall Matthew Tillett

even lower in the short term in the event of political or economic

setbacks. It is important the Fund holds back some firepower to January 2018

To find out more please visit www.allianzgi.co.uk

Allianz Global Investors GmbH, UK Branch, 199 Bishopsgate, London, EC2M 3TY

1 Source: Bloomberg, January 2018.

2 Source: Bloomberg, January 2018.

3 Source: Bloomberg, AllianzGI estimates, January 2018

Investing involves risk. The value of an investment and the income from it may fall as well as rise and investors might not get back the full amount invested.

Investing in fixed income instruments may expose investors to various risks, including but not limited to creditworthiness, interest rate, liquidity and restricted

flexibility risks. Changes to the economic environment and market conditions may affect these risks, resulting in an adverse effect to the value of the

investment. During periods of rising nominal interest rates, the values of fixed income instruments (including short positions with respect to fixed income

instruments) are generally expected to decline. Conversely, during periods of declining interest rates, the values of these instruments are generally expected to

rise. Liquidity risk may possibly delay or prevent account withdrawals or redemptions. Allianz Global Multi-Asset Credit is a sub-fund of Allianz Global Investors

Fund SICAV, an open-ended investment company with variable share capital organised under the laws of Luxembourg. Past performance is not a reliable

indicator of future results. If the currency in which the past performance is displayed differs from the currency of the country in which the investor resides, then

the investor should be aware that due to the exchange rate fluctuations the performance shown may be higher or lower if converted into the investor’s local

currency. This is for information only and not to be construed as a solicitation or an invitation to make an offer, to conclude a contract, or to buy or sell any

securities. The products or securities described herein may not be available for sale in all jurisdictions or to certain categories of investors. This is for distribution

only as permitted by applicable law and in particular not available to residents and/or nationals of the USA. The investment opportunities described herein do

not take into account the specific investment objectives, financial situation, knowledge, experience or specific needs of any particular person and are not

guaranteed. The views and opinions expressed herein, which are subject to change without notice, are those of the issuer companies at the time of publication.

The data used is derived from various sources, and assumed to be correct and reliable, but it has not been independently verified; its accuracy or completeness

is not guaranteed and no liability is assumed for any direct or consequential losses arising from its use, unless caused by gross negligence or wilful misconduct.

The conditions of any underlying offer or contract that may have been, or will be, made or concluded, shall prevail. For a free copy of the sales prospectus,

incorporation documents, daily fund prices, key investor information, latest annual and semi-annual financial reports, contact the management company

Allianz Global Investors GmbH in the fund’s country of domicile, Luxembourg, or the issuer at the address indicated below or www.allianzgi-regulatory.eu.

Please read these documents, which are solely binding, carefully before investing. This is a marketing communication issued by Allianz Global Investors GmbH,

www.allianzgi.com, an investment company with limited liability, incorporated in Germany, with its registered office at Bockenheimer Landstrasse 42-44, 60323

Frankfurt/M, registered with the local court Frankfurt/M under HRB 9340, authorised by Bundesanstalt für Finanzdienstleistungsaufsicht (www.bafin.de).

Allianz Global Investors GmbH has established a branch in the United Kingdom, Allianz Global Investors GmbH, UK branch, 199 Bishopsgate, London, EC2M 3TY,

www.allianzglobalinvestors.co.uk, which is subject to limited regulation by the Financial Conduct Authority (www.fca.org.uk). Details about the extent of our

regulation by the Financial Conduct Authority are available from us on request. This communication has not been prepared in accordance with legal

requirements designed to ensure the impartiality of investment (strategy) recommendations and is not subject to any prohibition on dealing before publication

of such recommendations. The duplication, publication, or transmission of the contents, irrespective of the form, is not permitted. 18-1143You can also read