API Industry Outlook First Quarter 2020 - March 19, 2020 - American Petroleum Institute

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

API Industry Outlook First Quarter 2020 March 19, 2020

Key points – Q1 2020

Even before the coronavirus (COVID-19) appeared, strong U.S. oil & gas productivity plus new pipelines

enabled February 2020 production records despite low prices and less drilling activity. Implications:

➢ WTI-Brent price differentials narrowed with Permian pipeline growth – to par in March with oil near $20/Bbl

➢ EIA projects U.S. oil & natural gas production to decrease year-on-year starting in Q4 2020

Markets have responded to COVID-19 prevention measures that EIA projects will dissipate in coming

quarters, but with oil prices that could remain low due to OPEC supply increases. Implications:

➢ EIA and IEA forecasts previously assumed OPEC would increase supply cuts, rather than supply

➢ Low oil prices have corresponded with a more rapid decrease in U.S. drilling – and less expected

associated natural gas and natural gas liquids (NGL) production per EIA

Silver linings that have reinforced market resilience:

1. Low energy prices bolster household budgets and disproportionately benefit low-income households

2. New U.S. trade agreements with China, Mexico and Canada should eventually boost U.S. energy exports (EIA)

3. IMO 2020 regulatory changes since January 1 have been smooth

4. Natural gas generation rose to a record 38% of U.S. net electricity generation in 2019

www.api.org

API industry health dashboard – Q4 2019

Increase vs. Decrease vs.

Key to the graphic: prior quarter prior quarter U.S. petroleum

demand

5-year range Revenues

20.7 mb/d

minimum maximum Quarterly increase to $680 B

top of 5-year range

Quarterly highlights

Demand at the top of the 5-year range U.S. refinery Net

throughput income

Despite drilling activity at a 5-year low and having fallen in Q4

16.9 mb/d U.S. drilling $(14.6) B

2019, record oil & gas production continued due to activity

821 rigs

productivity gains and new pipeline capacity enabling drilled

but uncompleted wells to come on stream

Capital expenditures increased along with ongoing project

commitments U.S. oil & total Capital

gas production expenditures

Net income fell with fourth quarter write-offs that were in the 33.7 mb/doe Q4 2019 averages $69.0 B

middle of the 5-year range (vs. 2015 lows) Brent $63.41/bbl

WTI $56.96/bbl

NGL composite $5.36/mmbtu

* Financial compilation based on API 200 companies with shares listed on U.S. stock exchanges Henry Hub $2.40/mmbtu

sources: EIA, API MSR, Bloomberg, Baker Hughes, API Team Analysis

www.api.org

Investing for the long-haul: the industry’s capital expenditures

totaled $69 billion in Q4 and $266 billion for 2019

Capital expenditures increased by 6.0% between the third and fourth quarters, with increases in most sectors but

less in the midstream due to major pipeline completions

Capital expenditures by industry segment

Billion dollars

100

Q4 2019 change

(%q/q)

80

Total: 6.0

60

Global Integrated 18.0

40

Upstream -7.4

20

-9.6

Midstream

Downstream +31.5

Specialty Petrochemical -+41.1

Equipment, Services and EPC +8.6

0

Mar-18 Jun-18 Sep-18 Dec-18 Mar-19 Jun-19 Sep-19 Dec-19

* All other oil & gas industry companies

sources: Bloomberg, publicly-available company reports

www.api.org

Industry capital projects map

Across the energy value chain, an estimated 161 oil & gas-related projects are under construction

24

76

Refinery

Pipelines

expansions

$27.3 B

$20.1 B

36

14 LNG PetChem

$189 B $108 B

Refineries

11 Gas

storage 344 Billion

in estimated industry

$145 M

LNG projects under construction

Petrochemical

Gas Storage

Pipeline sources: S&P Market Intelligence, Oil & Gas Journal, American

www.api.org Chemistry Council, API Team calculations as of Feb. 1, 2020

Global economy & oil markets www.api.org

Petroleum demand uncertainties and Non-OPEC production

growth

www.api.orgAPI’s economic indicator: The API D-E-I™ - Feb. 2020

The D-E-I™ value of -0.3 for February 2020 and three-month average of -0.2 suggests a continued slowing of

industrial production

Industrial production API D-E-I™

Percentage change year-over-year (3-month average) Percentage change year-over-year (3-month average)

15 3

Recession (left axis) Industrial production (left axis) DEI (right axis)

10 2

5 1

0 0

-5 -1

-10 -2

-15 -3

-20 -4

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

sources: API Monthly Statistical Report, EIA, CME Group, Moody’s, Federal Reserve Board

www.api.orgThe U.S.-China phase one trade deal calls for

increased U.S. energy exports

China’s commitments to buy U.S.

energy exports China committed cumulatively to purchase $52.4 billion of

Billion dollars U.S. energy over two years, over and above a 2017 baseline

50 amount, including crude oil, LNG, metallurgical coal and

Crude oil Refined products LNG Coal specific refined products*

40

$33.9 B API estimates the two-year commitment could include more

than 1.0 mb/d of crude oil, 0.5 mb/d of refined products

30 and 100 LNG cargoes, but these volumes rise as prices fall

$18.5 B

20 Given EIA’s expected growth in U.S. production, export

capacity and marine logistics – including ability to utilize the

Panama Canal – at least some of China’s purchases are

10 likely not to be incremental growth of U.S. exports, but

directionally should boost U.S.-China energy trade, provide

a welcome de-escalation of trade tensions, and spur new

0 opportunities for engagement on phase two trade issues

2017 Baseline Year 1 Year 2

sources: ITC , China customs statistics * Refined products under the agreement include naphtha, methanol, petroleum coke, propane, butane and other LPGs

source: API Monthly Statistical Report (Dec. 2019)

www.api.orgGlobal economic growth has consistently required

fossil fuels

Linkages between global GDP growth and energy demand in total and for oil and natural gas have remained consistent

Global primary energy demand versus GDP*

Quadrillion Btu

750

Total primary energy

Oil 2019

Natural gas Great Financial Crisis

600 (2008-2009)

450

300

1970

150

0

15 35 55 75 95

Real GDP (Trillion 2010$) *Market exchange rate basis

www.api.org sources: EIA, IEA, Bloomberg, IMF, API Team calculationsEIA’s short-term projected changes in global oil

demand and supply

Global oil demand changes - EIA Global oil supply changes - EIA

Million barrels per day Million barrels per day

0 0.5 1 -4 -2 0 2

China’s demand OPEC expands

2019 picks up in 2021 2019 production

China 2020 OPEC 2020

2021 2021

U.S. demand U.S. supply

grows slightly contracts in 2021

U.S. U.S.

Rest of World

Rest of World demand growth Rest of Non-OPEC Non-OPEC

hampered in growth in 2020

2020

source: EIA source: EIA

www.api.orgAfter a near-term dip, EIA expects the global oil

market to rebalance by Q4 2020

EIA global supply/demand and Brent price estimates as of March 2020

Million barrels per day 2020$/Bbl

2.5 120

Supply less demand Brent crude oil prices Column1 EIA estimates

2.0

100

1.5

80

1.0

0.5 60

0.0

40

-0.5

20

-1.0

-1.5 0

2015 2016 2017 2018 2019 2020 2021

sources: EIA STEO (Mar. 2020), Bloomberg

www.api.orgU.S. oil cost effectiveness and productivity improved, but

market prices have recently fallen

BTU Analytics’ estimated breakeven prices fell among most major crude oil production areas, while EIA’s productivity

estimates rose

Oil estimated breakeven prices by production U.S. oil productivity – monthly new well

area – Feb. 2020* production per rig

Dollars per barrel ($/Bbl.)

0 20 40 60 Barrels per day oil-equivalent

3,000

Feb. 2020

Eagle Ford - West Eagle Ford

Feb. 2019 2,500

Bakken 2,000

WTI spot price Bakken

Mar. 9, 2020 1,500

Eagle Ford - East

1,000

Permian - Delaware

500

Permian

Permian - Midland 0

*Half cycle breakevens assuming 10% discount factor and play-specific costs

2015 2016 2017 2018 2019 2020

source: BTU Analytics source: EIA Drilling Productivity Report(Mar. 2020)

www.api.orgDuring initial months of IMO 2020, the refining

industry has been flexible to consumers’ benefit

IMO 2020: Maximum marine fuel

As we have suggested since 2018, the U.S. refining industry has been well sulfur content

positioned for IMO2020 Sulfur content, %

5

4

Initial months of IMO2020 implementation show the industry has flexibly been 3 Outside emissions control

2 areas (ECAs)

able to produce less residual fuel oil and more ultra-low sulfur fuel oil, with a 1 Within ECAs

muted price response and inventory adjustments 0

2005 2010 2015 2020 2025

Residual fuel oil inventories and production U.S. residual fuel oil and diesel prices

Million barrels Million barrels Dollars per gallon

50 300 4

Rest of World inventories

40 Ultra-low sulfur diesel (ULSD)

3

U.S. inventories 200

30

2

20

100 Residual fuel oil No. 6 (1% sulfur) *

U.S. production 1

10

0 0 0

2010 2013 2016 2019 2010 2013 2016 2019

sources: JODI Oil World Database, EIA sources: New York Harbor prices, CME Group and Bloomberg

www.api.orgMotor gasoline and diesel fuel prices have generally moved

with crude oil, and EIA expects limited impact from IMO 2020

Crude oil, retail gasoline and diesel fuel prices, adjusted for consumer price inflation

2020$ per gallon

4

EIA estimates

3

2

1

sources: EIA, AAA, Bloomberg, BLS

0

2015 2016 2017 2018 2019 2020

West Texas Intermediate crude oil Gasoline - U.S. average Diesel - U.S. average

www.api.orgU.S. household spending is disparate by income group

Seven spending categories account for the majority of household expenditures

The lowest 40% of households by income generally outspend their after-tax income, so every dollar matters

2018 U.S. household spending by category as a share of after-tax income

% Housing ex energy Food Transportation ex fuels Healthcare Energy Education Personal insurance Entertainment

200

175

150

125

100

75

50

25

0

Average U.S. Lowest 20% income Second 20% income Third 20% income Fourth 20% income Highest 20% income

www.api.org

household

source: BLS Consumer Expenditure SurveyLower household energy spending since 2014

has helped low-income households the most

For the average U.S. household, decreased energy prices and expenditures freed 1.6% of after-tax income for other

spending needs between 2014 and 2018

The percent of income freed up for non-energy spending was twice as high for the lowest 20% income quintile

Change in household energy spending as a share of after-tax income, 2014-2018

Average U.S.

Change in percent of after-tax income

household Lowest 20% income Second 20% income Third 20% income Fourth 20% income Highest 20% income

0

-1

-2

-3

Electricity Gasoline and motor fuels Natural gas Fuel oil

www.api.org

-4

source: BLS Consumer Expenditure SurveyNatural gas www.api.org

Global LNG prices have been below historical

levels but still generally twice those of the U.S.

Global natural gas landed prices (dollars per million Btu) – December 2019

UK

$4.66

Belgium

Canada $5.32

$6.83 Spain Korea

$4.53 $5.42 Japan

Lake Charles China $6.70

$2.21 $5.42

Mexico India

$4.60 $5.22

Argentina

$5.05

sources: U.S. FERC (Mar. 2020) and METI

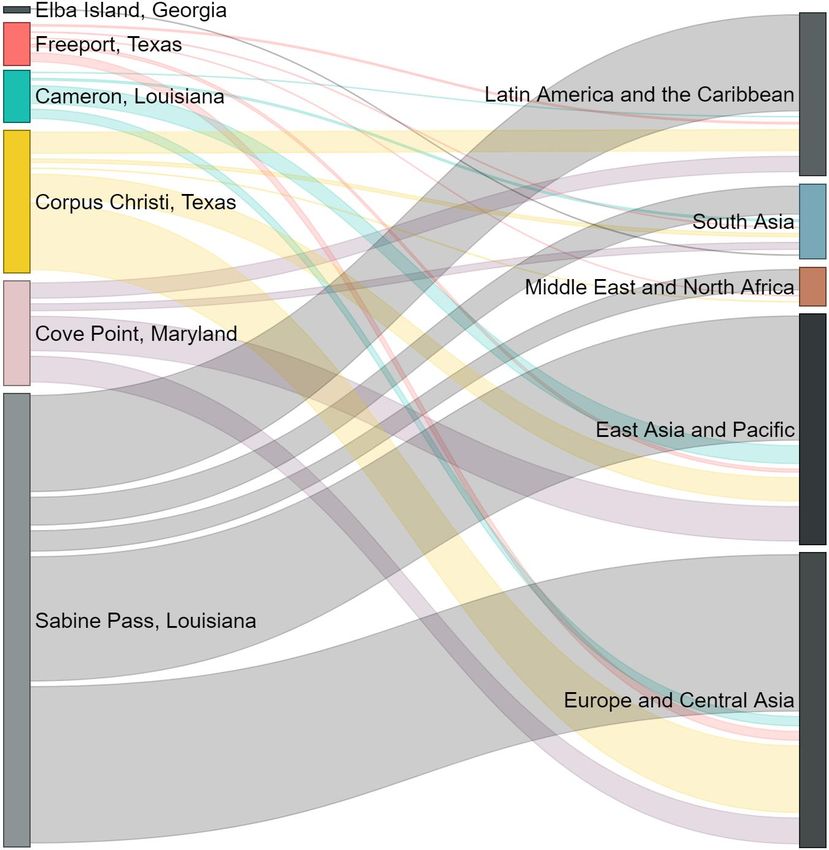

www.api.orgIn 2019, U.S. LNG exports were from just six

terminals, but served global markets

2019 U.S. LNG exports by terminal

Trillion cubic feet (Tcf)

1.20

0.90

0.60

0.30

0.00

Sabine Corpus Cove Point Cameron Freeport Elba Island

Pass Christi

source: U.S. DOE

www.api.orgU.S. natural gas production growth has been

supported by cost effectiveness and productivity

BTU Analytics estimates breakeven prices among most natural gas-producing regions improved over the past year

EIA estimates Appalachia’s new well productivity slipped in Q1 2020

Natural gas estimated breakeven prices by U.S. natural gas productivity – new

production area – Feb. 2020* production per rig

Dollars per million Btu (mmBtu)

0 1 2 3 Thousand cubic feet per day nat. gas-equivalent

25,000

Feb. 2020

Haynesville

Feb. 2019

Henry Hub spot 20,000

price Mar. 9, 2020 Appalachia

Appalachia - Northeast

PA 15,000

Appalachia - Southwest Haynesville

10,000

PA

5,000

Appalachia - Ohio

0

*Half cycle breakevens assuming 10% discount factor and play-specific costs

source: BTU Analytics

2015 2016 2017 2018 2019 2020

source: EIA Drilling Productivity Report (Mar. 2020)

www.api.orgReal natural gas prices in Q1 2020 have been the

lowest on record for the quarter in 45 years

Since the advent of shale gas production, which accelerated after 2010, U.S. natural gas prices and price volatility

have fallen by about half compared with history

U.S. natural gas spot prices*

2020 dollars per million Btu

20

16

12

Lowest Q1 prices

8 on record

4

0

1976 1981 1986 1991 1996 2001 2006 2011 2016

* sources: EIA spot prices at Henry Hub (1997-Present), WSJ and Reuters (1989 to 1996), EIA wellhead (1976-1988)

www.api.orgWhere enabled by pipeline connectivity, the energy revolution

has lowered prices across the eastern United States

Dawn

In 2010, before the energy revolution, prices at most natural

Chicago

gas hubs were greater than those at Henry Hub, Louisiana Algonquin

As Pennsylvania and Ohio became major gas producers,

prices fell across the eastern U.S. except in New England,

Dominion South Point

which largely failed to expand its pipeline infrastructure

Rockies East

Natural Gas Spot Price Differences from Henry Hub Florida Z2

(annual averages)

Henry Hub

Dollars per million Btu New England: A higher premium due

1.0 to a lack of infrastructure

0.5 Paid a premium above Henry Hub 2010 2019

0.0

-0.5

Received a discount below Henry Hub

-1.0

Chicago Florida Gas Transmission Rockies Express Pipeline Dominion South Point Dawn Algonquin

Zone 2 (East) into Midwestern

source: Bloomberg

www.api.orgIn 2019, natural gas grew to a 38% percent share of

U.S. electricity generation and led gains by all sources

Natural gas achieved a record 38% share of U.S. net electricity generation in 2019

As natural gas and renewables have replaced coal in power generation since 2010, U.S. power sector CO2 emissions fell

by 22%, while the region’s SO2 and NOx emissions decreased by 71% and 40%, respectively

U.S. electricity net generation Power sector emissions by pollutant (million metric tons)

(million megawatt hours) CO2 SO2 and NOx

5,000 Renewables

2400 6

Solar

4,000 Wind

Hydroelectric

2000 4

3,000 Natural gas

Oil

2,000 Other Nuclear

1600 2

1,000

Coal

0 1200 0

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2010 2011 2012 2013 2014 2015 2016 2017 2018

source: EIA sources: EIA Electric Power Annual (2018)

www.api.orgResources: Chief Economist’s section at www.api.org www.api.org

You can also read