Argentina as an investment opportunity - Rodolfo G. Villalba Executive Vice President

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Argentina as an investment opportunity

Rodolfo G. Villalba

Executive Vice President

Buenos Aires, May 2017

1

Argentina has strong fundamentals to become a regional economic engine

Large and • 3rd largest economy in LatAm, GDP of USD 586 Bn

diversified • 2nd highest GDP per capita in PPP terms in the region, USD 22,500

ECONOMY

• ~43 Mn pop (~60% under 35); access to 300 Mn pop in Mercosur

Vast availability of • 8th largest country in the world (2.8 Mn km2), with 53% of agricultural land

NATURAL • Abundant food, water and renewable energy resources

RESOURCES

• Large oil & gas and mineral reserves

• Qualified labor force, renowned for its technical skills, creativity & versatility

High quality

HUMAN • #1 in Latin America’s Indices of Human Development and Education

CAPITAL

• 98% literacy rate, ~110,000 higher education graduates per year

NATIONAL • Nationwide road & railroad systems (35,000+ km), 43 ports & 54 airports

INFRASTRUCTURE

• High connectivity, with 75% broadband and 141% mobile penetration

improvement

underway • Extensive natural gas pipeline and electricity grid coverage

2

Argentina has potential to capture USD 25 Bn/year+ in Foreign Direct Investment

Argentina has lagged behind its peers in capturing Now we have the opportunity to reach the level of

the strong FDI inflow growth in Latin America FDI correspondent to the size of our economy

Foreign Direct Investment ’08 - ’15 FDI/GDP

(Avg. USD Bn/Year) (%, average)

74.9

8.4%

’90-’00

’08-’15

6.0x 5.0%

Average

3.9% 4.5%

27.4 3.4%

2.9x 19.7 2.4%

1.4x 1.9%

12.5 5.8x 6.6x 12.4 5.4x

9.4 9.7 8.2

7.1

3.4 1.9 1.5

Brazil Mexico Chile Colombia Argentina Peru Chile Peru Colombia Brazil Mexico Argentina

Argentina’s share of regional FDI flows fell from 16% To reach the regional average, Argentina needs to

to 4% between the 90s and the last 7 years capture USD 25 Bn a year in FDI flows

Source: World Bank, IMF 3

President Macri’s Administration has taken concrete steps to resolve investors’ concerns

WEF Survey: Main Concerns for Argentina

(share of total responses) Key reforms and initiatives

Inflation 18 • Instituted inflation targeting policy to reach single–digit CPI by 2018

• Removed capital controls and repatriation restrictions

FX restrictions 17 • Floated exchange rate and recovered monetary reserves

Access to

13 • Resolved defaulted debt and regained access to global financial markets

financing

Tax levels 11 • Removed export taxes and import restrictions

• Government e-platform for tenders and public accounts

Corruption 11 • Introduced Central Bank independence

• Created the Argentina Investment & Trade Promotion Agency

Government

6 • New Public–Private Partnerships (PPP) regulatory framework

bureaucracy

• Re–launched the National Statistics Bureau (INDEC)

• Established 4–year plan to eliminate the primary fiscal deficit

Other 24 • Implemented an unprecedented tax amnesty scheme

• Country risk declined more than 100bp (-22%) in 12 months*

• Recent public and corporate debt issuances have been oversubscribed by 4-7x**

Source: World Economic Forum (2015), press releases

* JPMorgan, Embi+ 08/31/15 = 584, Embi+ 08/31/16 = 454. **Includes the Federal Government, Buenos Aires Province and corporations

4

The new administration was able to stop the decline and strengthen foreign exchange

reserves

Recovering

Foreign exchange reserves (USD million) reserves level to

pre FX restriction

policies in 2011

$ 60.000

USD 51.495 The

$ 50.000 unprecedented

tax amnesty

$ 40.000 scheme (for a

monetary value

$ 30.000

of USD 120 Bn so

far) will continue

to contribute to

$ 20.000

the growth of

foreign exchange

$ 10.000 reserves

$0

Source: Central Bank of Argentina. Dates are in dd/mm/yyyy format 5

Low leverage at the household, corporate and government levels increase potential for

investment and growth

Household Debt - 2014 Corporate Debt - 2014 Sovereign Debt - 2015

(% of GDP) (% of GDP) (% of GDP)

Latin America

125%

101%

249%

121%

105%

Emerging Markets

96%

Developed World

81%

89%

74%

86%

86%

71%

70%

69%

55%

67%

53%

65%

54%

52%

51%

54%

43%

45%

36%

40%

38%

30%

29%

24%

21%

18%

19%

15%

16%

9%

7%

7%

Chile

Chile

Chile

USA

USA

USA

UK

France

Argentina

UK

France

UK

France

Mexico

India

India

China

Mexico

China

India

Argentina

Argentina

Brazil

Peru

Brazil

Peru

Brazil

Japan

Russia

Japan

Russia

Japan

Germany

Germany

Germany

Colombia

Colombia

Colombia

Argentine households have significant Argentine corporations have the lowest The government has ample room to

room to borrow and increase spending debt to GDP ratio in the world, borrow from capital markets to fund

increasing opportunity for leverage infrastructure projects

Source: McKinsey Global Institute, BCRA, IMF 6

Argentina’s macroeconomic indicators are projected to improve markedly beginning in

2017, making this an ideal moment to invest in the country

Argentine GDP growth is expected to rebound According to IMF, Inflation is expected to decrease

strongly in the next few years significantly, reaching single digits by 2020

YoY GDP Growth (constant 2004 prices) YoY Consumer Price Change

Historical Projected 39%

11%

Argentina’s Central

6% Bank has set more

aggressive goals of

5%

12-17% for 2017

4% and 8-12% for 2018,

reaching 5% in 2019

3%

21%

2%

17%

1%

12%

0%

2008

2010

2011

2013

2015

2017

2018

2019

2020

2021

-1% 7%

5%

-2%

-6%

2016 2017 2018 2019 2020 2021

Sources: Historical – INDEC; Projections – IMF World Economic Outlook (October 2016) 7

Argentina offers investment opportunities of more than USD 250 Bn

Manufacture/ Value Added

Infrastructure Energy & Mining Agribusiness

Industrial Goods Services

$135 Bn $85 Bn $25 Bn $5 Bn $5 Bn

• Roads & highways: $48 Bn • Oil & Gas: $20 Bn+ (per • Irrigation: $18 Bn • Automotive industry • Tourism

• Water & sanitation: $22 Bn year) • Animal protein (beef, • Food & Beverage • Professional

• Education & health: $20 Bn • Mining: $30 Bn+ pork, poultry): $5 Bn • Consumer products services

• Urban mobility: $17 Bn • Renewable energy: $15 Bn • Forestry/Pulp: $2.5 Bn • Machinery & • Biotechnology

• Freight rail: $15 Bn • Hydro power: $10 Bn Equipment • Pharma

• Real estate: $5 Bn • Power grid: $5 Bn • Basic materials • Software

• Thermal power: $4 Bn development

• Telco networks: $5 Bn

• Airports & ports: $3 Bn • Nuclear power: $3 Bn

Note: All values are in USD 8

The Argentina Investment & Trade Promotion Agency

Contribute to the creation of quality jobs and sustainable economic development by

reinserting Argentina into the world, through investment and trade

➢ Single point of contact in the government for companies seeking to invest in Argentina

➢ Become a strategic partner throughout the investment period

➢ Facilitate investment processes and improve business climate

➢ Promote the highest ethical and professional standards, making Argentina

a better and more transparent place to conduct business

➢ Unlock SMEs and regional economies potential to strategic international markets

ECONOMIC JOB REGIONAL SOCIAL TECHNOLOGY STRATEGIC ENVIRONMENTAL

IMPACT CREATION ECONOMIES IMPACT TRANSFER SECTORS CARE

9

The Agency facilitates investment processes throughout the business ecosystem

Strategic issues Administrative issues

Sector-specific information, programs, regulatory framework Tax/legal paperwork, permits, registrations

Foreign Regional TAX LEGAL

Consultants Promotion

Agencies

Embassies & President

/Chief of Municipalities

Consulates

Staff

Ministry of

Foreign Provinces

Affairs

Private,

Financing state-owned,

Programs & multilateral

banks

Strategic CAPITAL FLOWS PERMITS

Ministries Partners

Big 4,

Secretariats Industry management

Chambers consultants

Ministerial Associations

IPAs

The Agency is a single-point-of-contact for investment projects, independently of sectors and origins

10Through the end of November, there have been investment announcements totaling

USD ~53 Bn, of which the Agency manages USD ~35 Bn

Investment Announcements

(USD Bn)

# Projects

55.4 360

Agribusiness 2.4 33

2.5 60

Technology & Other Services

Consumer Goods 5.4 53

Industrial Goods 6.6 49 # Projects

203

34.9

Financial Services 6.7 38

2.9 53

2.2 39

Transport & Infrastructure 8.0 28 4.2 33

1.3

29

4.6

25

5.9 8

Energy & Resources 23.9 99

13.7 32

Investments announced* Investments managed by the Agency

* From 11/12/15 to 11/12/2016. Includes only projects with a declared monetary amount

11We have a world-class team ready to assist you with your investment and trade needs

PABLO TARANTINI JUAN PABLO TRÍPODI FRANCISCO URANGA

VP Investments VP International Trade VP Investments

Infrastructure, Mining, Agribusiness, Consumer Agribusiness, Industrial

Consumer Goods, Innovation Goods, Services Goods

+54 11 5218 8571 +54 11 5218 2924 +54 11 5218 9332

ptarantini@invest.org.ar jtripodi@exportar.org.ar furganga@invest.org.ar

JUAN PROCACCINI

President

+54 11 5199 8572

Presidencia@invest.org.ar

RODOLFO VILLALBA ANDRÉS ONDARRA ANDRÉS TAHTA

VP Investments VP Investments VP Investments

Business in Asia Finance, Power Telecommunications,

+54 11 5218 9332 Generation, Real Estate, Renewable Energy, Health &

rvillalba@invest.org.ar Oil & Gas Professional Services

+54 11 5218 9332 +54 11 5218 8571

aondarra@invest.org.ar atahta@invest.org.ar 12Rodolfo G. Villalba

Executive Vice President

rvillalba@invest.org.ar

Miguel Mitre

Analyst Asia

mmitre@invest.org.ar

www.investandtrade.org.ar

InvestTradeARG

13APPENDIX

14According to private projections, economic growth combined with reduction in subsidies

to consumers should reduce the primary fiscal deficit from 4.8% to 0.9% of GDP by 2021

Relationship between primary revenues, expenditures

and fiscal deficit (% of GDP)

23.4

24 22.4

21.7

22 20.6

19.4 18.9

20 18.6 18.3 18.6 18.4 17.9 Expenditures

18 4.8

4.1 Primary revenues

4 3.1 18.0

2.2

1.5

2 0.9

Fiscal deficit

0

2016 2017 2018 2019 2020 2021

3.6% 3.8% 3.2%

3.1% 3.1%

GDP Growth

-2.0%

Source: Morgan Stanley 15A number of regulatory initiatives have been or are in the process of being

implemented to foster a better business and investment climate

UNDER CONGRESSIONAL

ALREADY IMPLEMENTED REVIEW UPCOMING

✓ Normalization of Foreign Exchange Market – removal of capital • “First Job” Law – tax • Cultural Patronage Law –

controls and exchange rate unification credits and subsidies for tax incentives for private

companies who employ 18 companies to finance

✓ Removal of Export Taxes on Mining and Industrial Products

– 24 year olds cultural projects

✓ Reduction of Agricultural Export Taxes

• “Simplified” Stock • Transparency in Public

✓ New Import Regime (“SIMI”) – clarification of goods requiring Company Law – new Works Law – stipulates a

non-automatic import licenses, all other goods require only an company type to facilitate requirement that all the

automatic license the establishment of start- administrative steps for

✓ Rural Land Law – implementation of a more flexible system for ups (online registration, public works be made

productive use of rural land by foreigners ability for employees to public

receive stock as

✓ Tax Amnesty Law – tax incentives for Argentines to repatriate compensation)

assets held abroad and invest in Argentina’s economy

• Venture Capital Law –

✓ SME Promotion Law – reduction of income tax and increase in creation of funds backed

financing options for SMEs by the government and

✓ Automotive Parts Production Law – incentives for automotive with incentives for

industry when buying local production investors to foster

Argentine

✓ Access to Public information Law – stipulates a requirement that

entrepreneurship

all public information requested of the government be provided

(or denied with a specific reason) within 15 days

✓ Public-Private Partnership (PPP) Law – measures to facilitate

and incentivize fruitful investment partnerships between public

and private sector

16Financial markets have been eager lenders to the government and Argentine

companies

RECENT DEBT PLACEMENTS

Bond Issuer Date of issue

Millons Maturity

Av. cost COMMENTARY

USD (years)

SOVEREIGN

✓ Argentina was the emerging market

Argentine Republic April 17, 2016 16.500 3, 5, 10, 30 7.2%

with the most debt placements in H1

5.625%

Argentine Republic January 26, 2017 7.000 5, 10

6.875% 2016 with USD 23 Bn in total

SUB-SOVEREIGN placements (20% share)

Buenos Aires Prov.

March 9, 2016

February 7, 2017

1.250

750

6–8

6

9.375%

6.6%

✓ Issuers included sovereign, sub-

Neuquén May 5, 2016 235 12 8.62%

sovereign and prime corporations and

Mendoza May 12, 2016 500 8 8.375% many of them were oversubscribed

Ciudad de Buenos Aires May 25 2016 890 11 7.625% ₋ The federal government

Córdoba June 3, 2016 725 5 7.125% received offers for USD 69 Bn,

Salta June 30, 2016 300 8 9.125%

implying an oversubscription of

Chubut July 18, 2016 650 10 7,75%

4.2x

Chaco August 11, 2016 250 8 9.5%

Santa Fe October 25, 2016 250 10 6,9%

₋ Buenos Aires Province was

Entre Ríos February 1, 2017 350 8 8.75% oversubscribed by 3x, Neuquén

CORPORATE by 6.3x, Mendoza by 4.6x

IRSA March 17, 2016 300 1–4 8.75% ₋ Cablevisión was oversubscribed

YPF March 23, 2016 1000 5 8.5%

by 7.0x

Cablevisión June 8, 2016 300 5 6.5%

Arcor S.A. June 22, 2016 300 4 9.125%

YPF June 30, 2016 750 4 9.125%

Arcor S.A. March 23, 2016 1000 5 8.5%

17Argentina has recently passed a law to promote Public-Private Partnerships

Objective: Increase private investor participation in a variety of

projects promoted by the Argentine government across sectors

• Public sector: access to the experience, efficiency and financing of the private

sector

Benefits

• Private sector: ability to participate as an investor in public projects under clear

guidelines and foreseeable streams of payments

• Any private or semi-private company and any public sector entity is allowed to

participate through a variety of investment vehicles (e.g. existing societies, trusts

etc.)

• Ample guarantees to ensure that contract obligations are met and payments made

• Limits the state’s ability to unilaterally change contract terms or alter the

Provisions economic equilibrium of the agreement (e.g. 100% compensation will have to be

paid prior to takeover of assets)

• Allows for contracts to be agreed to and payments to be made in foreign currencies

• Dispute resolution can be sought from technical panels and/or

national/international tribunals

18We have very attractive renewables and unconventional O&G markets under

development

Power generation: renewables target of 20% of Unconventional O&G: “Vaca Muerta” play has

consumption shall be met by 2025 world-scale potential

Installed Capacity Addt’l Capacity Shale Oil Reserves Shale Gas Reserves

(GW) 54 (Bill. Barrels) (Trill. Cubic feet)

10 10 GW 75 1,135

1 1,5 GW

33 58

Renewable 802

1 18 8 GW

707

Nuclear 665

10

Thermal 32

27

Hydro 22 25 3 GW

2015 2025 Russia USA China Arg China Arg AlgeriaRussia

• Investments of USD 15 Bn needed to meet renewables • Argentina holds the world’s 2nd largest technically

target recoverable shale gas and 4th largest shale oil reserves

• Great conditions for wind, solar, biomass and small hydro • Vaca Muerta has 4+ years of cumulative development

• Government commitment and support: - Area of 30,000 km2 with ~300m of shale layer at

~3,500m of depth (with 3-5% of total O&G content)

- Competitive prices under guaranteed long term PPAs

- JVs between YPF and Chevron, Dow, Pampa, Petronas

- Tax incentives (accelerated depreciation, levied import duties, etc)

- Financing for renewable energy projects • The Government has preagreed modifications to the

Vaca Muerta collective bargaining agreement: gas price

• >10GW of large baseload plants (thermal/hydro) needed

will have longer predictability, and labor costs and

productivity will be improved

Source: Ministry of Energy and Mining, EIA 19Argentina has 300+ GW potential in renewable energies distributed across different

regions in the country*

SOLAR

• High solar radiation levels found in

flat terrains with good altitude and

BIOMASS low humidity levels

• Wide availability of sugar cane • High capacity factors for Solar PV

bagasse and agricultural residue

• Significant forestry coverage and

wood production in NE and south MINI - HYDRO

regions (eg. Tierra del Fuego)

• Wide availability of

mini-hydro projects

with high capacity

GEOTHERMAL factors (over 50%)

• High quality geothermal resources

located in the Central Andes region.

• The area hosts almost every basic

WIND

geothermal element such as volcanoes,

fumaroles, hot springs and geysers • Year-round strong and stable

winds reflected in capacity

factors of 35%+

• Favorable terrain conditions

(include rounded hills, open

plains and extensive shoreline)

* Excluding biomass

Source: Universidad del Comahue, IEA, Enel

20Argentina has the highest wind power potential in the region

• Patagonia Region has very stable and strong winds throughout the entire year (with

average winds of over 9m/s)

• Windfarms with capacity factors ranging from 35% to 50%

Selected Countries: Wind Capacity Factors (%) Argentina: Average Windspeed Map

50

47

44

15

37

35

33

23

20 19

35

Arg Uru Per Bra Mex Chl USA Chi Ger

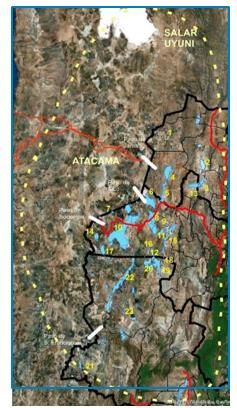

CF Source: Project public data / BNEF; Map: Centro Regional de Energía Eólica 21Argentina also has the second highest solar power potential in the region

• Northern Region has exceptional radiation levels and terrain conditions, comparable to

those in the Atacama desert in Chile

• PV capacity factors expected to range between 25% and 33% (with tracker)

Selected Countries: Solar Capacity Factors (%) Argentina: Average Solar Radiation Map

34 33

31

8

20 20

16 17

15

12

25

Mex Arg Chl Bra Per Uru Ger Chi Jpn

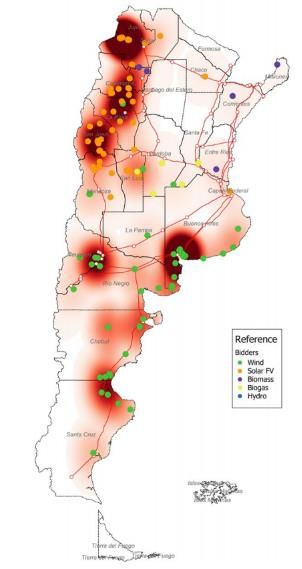

CF Source: Project public data / BNEF; Map: National Renewable Energy Laboratory (NREL) 22Recent tenders in renewable and thermal energy were heavily oversubscribed

Renewable Energy (RenovAr Rounds 1 and 1.5) Thermal Energy

1 GW Capacity called for tender Awards ✓ Auction initially contemplated

59 Projects increasing installed capacity by 1

TOTAL

123 Projects presented AWARDED

2,423 MW

8,268 MWh/yr

GW, but ended up awarding 2.8 GW

due to high demand

Wind

x 6.3 Oversubscribed 22 Projects

✓ Results:

1,472 MW

5,827 MWh/yr

• Total of 2.8 GW awarded

Solar PV 24 Projects

916 MW • 6.6x oversubscribed

2,192 MWh/yr

• 20% offers coming from new

Biogas 6 Projects players

9 MW

67 MWh/yr • Pricing ~32% cheaper than

Biomass 2 Projects previous auction

15 MW

117 MWh/yr

Small Hydro 5 Projects

11 MW

65 MWh/yr

For specific information on the Renewable Energy awarded projects, please see the RenovAr Brochure

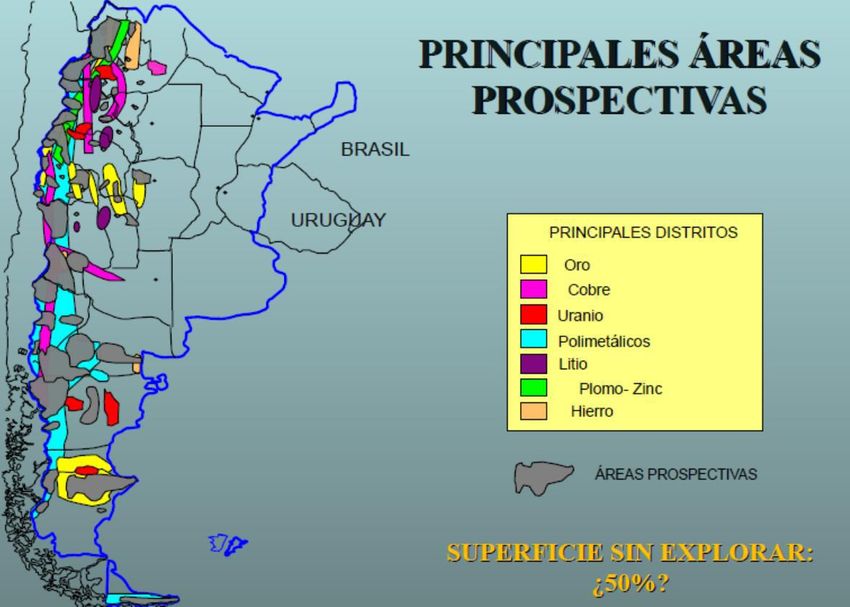

developed by the Udersecretariat of Renewable Enery, Ministry of Energy and Mines 23We have great mining potential, with abundant reserves of lithium, copper, silver, gold

and potassium

Significant mining potential with ~75%

unexplored surface Important opportunities in lithium, copper, silver and gold

World

• 750,000 Km2

of high Thousand tonnes

Ranking

potential mining areas 11x

Lithium Current 13 #3

• 183,000 Km2 of already Potential 148 #2

granted mining rights

- 25 advanced prospects Thousand tonnes

9x

# 20

- 14 production mines Copper Current 110

#6

Potential 856 100 956

Gold Tonnes

Copper

Current 3x # 10

Uranium Silver 756

Potential 1,417 800 2,217

#5

Polymetallic

Lithium Tonnes

Lead-Zinc

Iron Gold Current 53 2x # 14

Prospective areas Potential 76 31 107 #9

• ~65% of the mining surface remains unexplored • USD 30 Bn+ needed to develop copper, silver, gold, lithium,

potassium and other opportunities

• No export taxes for mining products

• There are 40+ projects with PEA and onward

Source: Ministry of Energy and Mining USGS • There are 340+ projects in initial stages 24There are at least 7 world class Copper projects in advanced stages, and 85 projects in early

stages underway

Our 7 projects in advanced stage are

85 projects in early stages in several provinces exploitable in the near future

• 23 in Salta • 8 in Mendoza • 1 in La Pampa

• 17 in San Juan • 7 in Jujuy

• 11 in Catamarca • 6 in Neuquen

• 10 in La Rioja • 2 in Chubut

Advanced Projects Company Metals Province State

Agua Rica Yamana Gold Cu, Au, Mo, Ag Catamarca Feasability

El Pachón Glencore Cu, Mo, Ag San Juan Feasability

San Jorge Solway Investment Ltd Cu, Au Mendoza Pre-Feas.

Taca-Taca First Quantum Cu, Au, Mo, Ag Salta Feasability

Josemaría (las Vicuñas, Las Flechas) NGEX Resources Cu, Au, Ag San Juan PEA

Los Azules McEwen Mining Cu, Au, Ag San Juan PEA

El Altar Stillwater Mining Corp. Cu, Au San Juan Adv. Exp.

25Argentina has the 3rd largest brine Lithium resource; alongside Bolivia and Chile we form the

Lithium Triangle

There are 7 projects in pilot stage

Company Salar Tn/yr

Orocobre Ltd. Toyota S. Olaroz Cauchari 20k

FMC S. Del Hombre Muerto 20k

Enirgi Group S. Rincón 20k

25 Projects in early stages Ganfeng Lithium S. Llullaillaco 20k

• 5 in Jujuy Eramet / Eramine S. Centanario 20k

• 15 in Salta SQM S. Cauchari Olaroz 20k

• 5 in Catamarca Galaxy Resources Ltd. S. Del Hombre Muerto 20k

26There are vast agribusiness opportunities in land irrigation, cattle raising, forestry &

cellulose and food industrialization

Argentina has excellent agriculture conditions and full There are still many opportunities for further

government support development

Argentina´s food production capacity 2016 Argentine production

(Million people) Development of more than 4 Mn Ha

56 Mn tons production with artificial irrigation

1.5X 1st soy oil exporter (6 Mt)

600 Potential investment: USD 8 Bn

2nd soymeal exporter (32 Mt)

3rd bean exporter (12 Mt)

400

Cattle raising expansion – 10 Mn head,

28 Mn tons production

200 K swine and 1,5 Bn poultry

3rd world exporter (17 Mt)

Potential investment: USD 10 Bn+

2.8 Mn Tons produced

11th meat exporter (265 MT) Expansion of the forestry and cellulose/

2015 2025 paper industry, biomass energy and

housing. Raw material: 4-5 Mn m3/year

• Farming conditions:

Potential investment: USD 2.5 Bn

- Mild Climate with abundant rainfall

Potential and incentives to consolidate

- Rich soils with low fertilizer needs

as significant player and develop 300k

- Exceptional human resources, long farming tradition tons of aquaculture

- High technology adoption in crop genetics (>65% GMO)

Potential investment: 1 Bn+

- Unparalleled logistics with 100% storage capacity

• Government support: one of the first measures adopted by Increased food industrialization (milling,

President Macri’s administration was the elimination of wine, canned and frozen food)

export taxes to wheat, corn, meat and regional products Potential investment: USD 0.5 Bn+

Source: Ministry of Agroindustry 27In professional services, we have become a hub for large companies’ shared service centers

Argentina has a number of distinct benefits for the Dozens of companies across industries have

establishment of shared service centers established their shared service centers in Argentina

• Ample supply of talented and English speaking workforce 40+ shared service centers in Argentina, including

- 110K higher education graduates per year

- 15th in the world in terms of English proficiency (1st in

LatAm)

- 98% literacy rate countrywide

• Located in a convenient time zone 1000 employees providing IT, 650 employees providing

- Entire Americas and Europe within +/- 5 hours* research, credit analysis and IT, tax & project

- NYC / Washington D.C. / Boston are at -1 hour processing services (opened management services

- London is at +4 and Continental Europe at +5 hours in 2015) (opened in 2012 )

• Availability of high-quality affordable urban office space

- Buenos Aires office space is cheaper than Rio de

Janeiro, Sao Paulo, Bogota, Santiago and Mexico City

- Tax incentives exist for companies installing themselves

in certain areas of Buenos Aires (e.g. new technology

district)

400 employees providing IT 120 employees providing

• Developed mobile and broadband infrastructure

and accounting services admin, procurement and

- 75% of population with broadband access (opened in 2006) billing services (opened in

- 141% mobile phone penetration with wide cell service 2006)

availability

*Differences can shift by +/- 1 hour during daylight savings time

Sources: UN, GSMA, press releases 28In infrastructure, we have ambitious development plans for roads & highways, railways

and airports

Roads: improvement and construction Freight rail: rehabilitation of the entire Airports: modernization & increased

of roads & highways network flight usage

• ~40% of roads are currently in poor • Only 5% of freight is transported by • Growth by 2x of air traffic expected

conditions railway (18 Mn tones) by 2020 (10 Mn to 20 Mn

• Only 2,800km of highways in place passengers)

• Average speed of ~12-15 km/h

• Plan 2027: • Expanded international connections

• Plan 2027:

- 11,400 km of total highways - 10,000 km of refurbished rails • Plan 2019:

- 13,000 km of roads in good conditions - 80-100 Mn tones transported - 14 airports modernized by 2019

- Investment of USD 28 Bn - Investment of USD 15 Bn - Investments of USD 900 Mn

2015 2027

Passenger rail: new developments

Ports

• The Regional Express Network (RER)

is a USD 8.5 Bn urban passenger • Port of City of Buenos Aires bid

investment

Source: Ministry of Transportation 29There are a number of public tenders planned in the short term across sectors

Transportation Federal Infrastructure Energy Real Estate & Tourism

Passenger rail rolling stock Thermal Tender (large high

efficiency projects -

Waste-to-energy electricity >700MW)

Nationwide road concessions plants Housing public works

First HV Transmission Grid

Stage 2 Belgrano Cargas Health related public works Tender Cafayate tourism project

H2 2016 & H1 2017

freight

Education related public “Portezuelo del Viento” Various real estate projects

works multipurpose dam in Buenos Aires City (e.g.

Regional Express Railway

Renewable energy (solar, Huergo Project, Colegiales

wind, hydro, biomass etc.) Station, Houssay Square…)

Port of Buenos Aires

concession Seismic evaluation for

offshore O&G

Buenos Aires Subway Nationwide irrigation

construction & renovation systems “Potrero del Clavillo”

multipurpose dam Various real estate projects

6-8 Vaca Muerta play tender in Provinces (e.g. North Port

Further freight rail projects

Rosario, Mendoza Station…)

(e.g. San Martin Cargas,

Urquiza Cargas)

H2 2017

RenovAr Plan Round 2

Note: All tender dates are tentative and approximate; includes only selection of opportunities. Thermal energy tenders to be determined. 30You can also read