Bajaj Allianz General Insurance - Incredible India - Property Insurance James Amberson, Global Risks Division 14 October 2014

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Bajaj Allianz General Insurance Incredible India – Property Insurance James Amberson, Global Risks Division 14 October 2014

Table of Contents

Bajaj Allianz General Insurance

Joint venture between Bajaj Finserv Limited

and Allianz SE.

Headquartered in Pune with a countrywide

network of over 200 branches spread

across the length and breadth of the

country

Offers technical excellence in all areas of

General Insurance as well as Risk

Management across all segments of the

industry Premium & Profit (INR billion)

50

45

40

35

30

Premium

25

20 Profit

15

10

5 Claims Network

0

2009-10 2010-11 2011-12 2012-13 2013-14 3

Global Risks Division

Virtual Allianz Global Corporate & Specialty

office in India

Launch in 2013 in Pune Head Office as a

collaboration between Bajaj Allianz and AGCS

Focus on development of International

Corporate Business in India with reinsurance

support from AGCS

Part of the Singapore managed Asian Region

Our Team

James Amberson – Head of Global Risks

Division

Annam R – Head of Property

Mudassir Khalil – Head of Financial Lines

Sahil Chadha – IIS Practice Leader

Sanjay Unny – Global Client Unit Manager

Khozema Filmwala – Account Technician

4

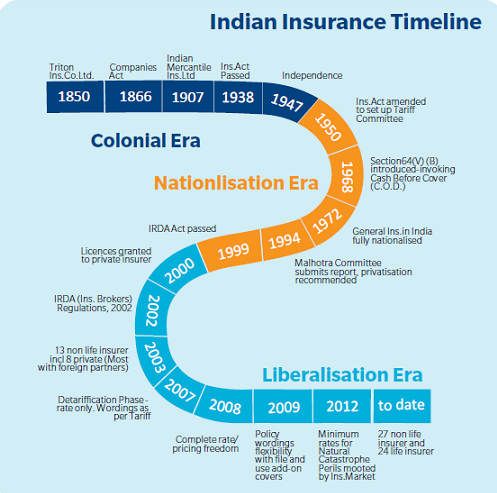

Non-life Insurance Market

India-top priority emerging market post

Liberalization in 2000

General Insurance growth has kept pace

with the GDP growth in the country

Compounded annual growth rate

(CAGR) 17.6 percent in 10 years

Penetration remaining stable in the

range of 0.55% to 0.75% over the last

10 years

Market size Euro 9.52 Billion

Net profit Euro 420 Million in 2012-13 Public - Private Sector Split*

27 Non-life Insurers- 6 Public, 21

Private

GIC -National Reinsurer Public

FDI Limit current 26%, proposed 43% Private

increase to 49% 57%

8099 Insurance Offices across the

country

5

Non-life Insurance Market

Market Background Regulatory Requirement/Initiatives

Scope of Distribution Channel ‘Cash before cover’

enlarged Solvency margin 1.5x

Agency & Direct are Common Insurance repositories and

modes of distribution electronic issuance of policies in

Insurance Broking community is April, 2011

just over a decade old ‘Place of Business’ gazette on

Detarification boosted broker 2013, new regulation for insurers

market share in Corporate Sector to open offices

There are 300 Licensed brokers in Grievance redressal and consumer

the market now awareness initiatives

Brokers’ direct market share of Monitoring Investments by

total non-life premium has grown insurers

from 16% in 2009-10 to 23.3% in Financial reporting & Data

2012-13 Standard regulation

The IRDA (Insurance Brokers) Anti Money Laundering

Regulations, 2013 came into effect (AML)/Know Your Customer(KYC)

from 10th December, 2013 regulations

6

Property Segment

Governed by All India Fire Tariff –laid

down Terms of coverage, Rates and

Conditions for decades

Profitable portfolio until Tariff

Fire policy renamed as “Standard Fire

and Special perils Policy” in 2001

Freedom of Pricing since 2007

Base wording unchanged

To file & use ‘add-ons’ covers bridge the

gap in local policy coverage with

International Standards

Business Interruption cover not much

opted Split of Business*

Coverage of underlying risk increased 12.19% 10.26% Property

due to price reduction 0.69% 4.44% Marine

Motor

Natural Catastrophe exposed 22.05%

Engineering

Valuation impacted by fluctuating Liability

FOREX Personal Accident

Health

42.91%

2.24% Aviation

Miscellaneous

7

1.63%

3.59%

Property Segment Premium Growth in 5 year

Market size Euro 985 million 10000 (in Million Euro)

Growth rate 15-22% 8000

4,160,000 NOPs in 2013-14 6000

NIC ratio 52.46% for Private 4000

71.55% for Public

2000

24% of the business through

0

Broker 2008-09 2009-10 2010-11 2011-12 2012-13 2013-14

Broker remuneration 12.5% Property Overall Market

Large risk 6.25%

Property-Combined Market

Capacity in EURO

On shore property EURO 1 Billion

Construction and

engineering EURO 0.8 Billion

Onshore energy EURO 42 Million

(combined single (sum insured

limit) basis)

8

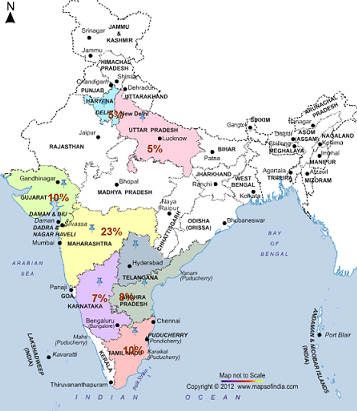

Property Segment

73% of Industry Property Premium is

contributed by 8 States of the Country

TIV for Property had gone up 11 times

from 2009-10 to 2012-13, while the

premium overall increase is hardly 1.6

times during the same period

Non-admitted policies prohibited

Sum Insured must be in INR

Language of the policy-English;

Public Sector Insurance Companies use

Bilingual-English & National Language

(Hindi)

Dispute resolution-Arbitration,

Ombudsman, Consumer Forum

Insurance clearance house for

coinsurance & reinsurance settlements

9

Thresholds

SFSP Policy IAR Policy Mega Risk Policy

Industrial all risk (IAR) -Reinsurance driven

Standard Fire and Special Wordings & pricing.

-all risks s.t Exclusions

Perils Policy- -unique benefit -Complete freedom for

Standalone policy of reinstatement value terms

even on total loss, -TIV (PD+BI)>

-TIV (PD+BI)< Euro 6mio Euro 300 mio

-Coverage and with broad property

definitions. - Coverage

-PD and BI separate -TIV (PD+BI)> 1) PD

-Deductible Euro 6mio at one location 2) MBD

-Coverage: 3) BI

5% of the claim amount

Section I - PD -Deductible

s.t. m of EUR 120 – 300 5% of the claim amount

Section II - BI (MLOP

Optional) s.t. m of EUR 60000

-Deductible

5% of the claim amount

s.t. m of EUR 300 – 30000

10UW Specific Regulation

Statutory Cession to GIC on each and every policy

underwritten

-GIC is the sole reinsurer of the domestic reinsurance market

-5% of sum insured is subject to a obligatory cap of Euro 62.50

million on sum insured per risk for fire,

GIC Re’s capacity for Property Business for Treaty and

Facultative basis :

Class Capacity

Domestic Business Euro 187.50 mio. Any one risk

International Clientele On PML Basis Sum Insured

Facultative Euro 15 mio Euro 38 mio

Treaty Euro 3 mio Euro 7.6 mio

Terrorism Pool- Managed by GIC- Combined limit for Property up

to Euro 117.5 million per location / compound

Insurance Premium is charged with 12.36% Service Tax

11UW Specific Regulation

REINSURANCE

Intend to Maximize retention within the country

To Develop adequate capacity

To Secure the best possible protection for the reinsc cost incurred

GIC Re is the national Reinsurer

A reinsurer should have a minimum credit rating of BBB ( S&P ) or an

equivalent for facultative reinsurance.

Limits allowed based on rating is as follows:

Rating of Reinsurers (as per Standard & Poor

and applicable to other equivalent Limit of cession allowed under Regulation 3(11)

• BBB of Standard & Poor 10%

• Greater than BBB and upto & including AA

of Standard & Poor 15%

•Greater than AA upto & including AAA of

Standard & Poor 20%

Cross border reinsures guidelines w.e.f. April 2012 by Regulation

Many global reinsurers like Swiss Re , Munich Re , Hannover Re have

representative office in India ( But not registered reinsurers )Claims Practice

Irda licensed surveyor for claims above Euro 250

In-house surveyor not used in Property as the onus of neutrality and

professionalism could be lost both in perception as well in the legal sense as

the Insurance Act would imply

The onus of proving that the loss is covered and payable is generally on

the insured in named peril policies

The onus that the policy does not cover the loss is on the insurer

interim payment in large claims to give cash infusion to the devastated

insured

If the technical violations result in exposing a real reason that a claim is not

payable, then the claim is to be repudiated

Repudiation may also involve more complex matters such as issues of non-

disclosure, misrepresentation and fraud.

Companies utilize the services of Tech Experts, Forensic, Fire Bridge and

detective agencies for understanding/probing the genuineness of claims

New concepts include treating customers fairly (TCF)

E-payment of claims

Fraud management

13Claims Specific Regulation

The Insurance Act stipulates all claims over Euro 250 should be

surveyed by a IRDA licensed surveyor

Earliest notice of claim by insured

Appointment of surveyor within 72 hours from intimation

Surveyors/Loss assessors are subject to ‘Code of Conduct’

Insurer to offer settlement/repudiation within 30 days on receipt of

survey report

Payment to be made within 7 days of acceptance of offer

Insurer and surveyor should seek from the insured only those

documents that are relevant to the duties of the insured

Surveyor to comment the grounds for repudiation if the claim is

found to be that

Surveyor to obtain a certificate of consent/ satisfaction about the

settlement of the claim from the insured

Surveyor to take expert opinion, if required

Surveyor to comment about the salvage realization efforts.

14General Regulations

Consumer/policyholder rights.

Right to proper

information and advice

Right to suitability of

products

Right to fair terms

Right to fair treatment

Right to redressal of

grievances and disputes

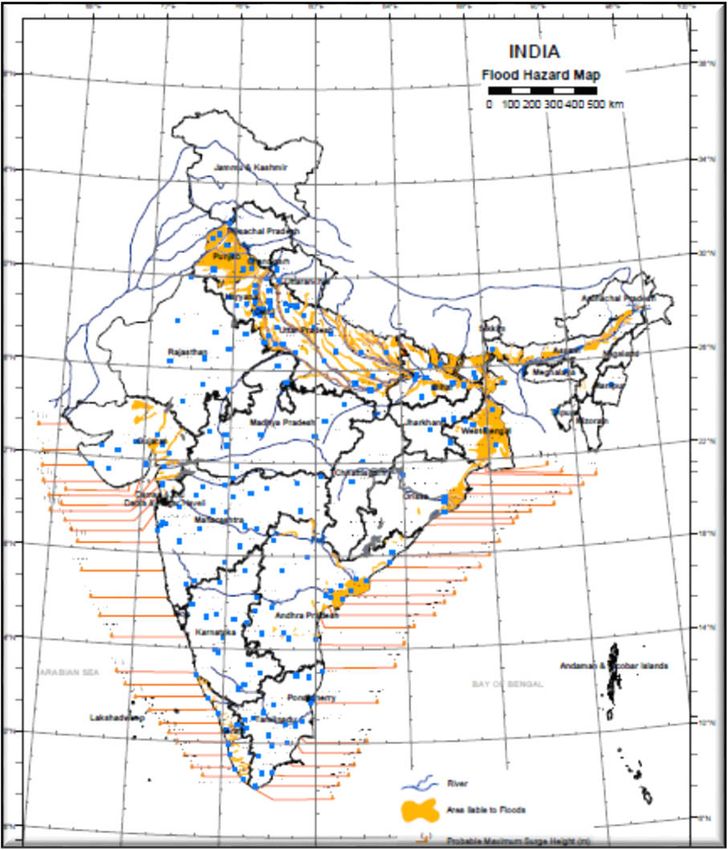

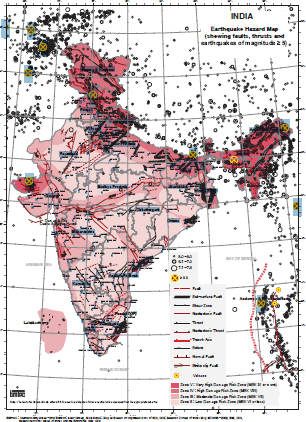

15NatCat Exposure

NATCAT ZONES-Hazard Vulnerability in India

Indian Subcontinent: among the world's most disaster prone areas

59% of land vulnerable to Earthquakes

8.5% of land vulnerable to Cyclones

5% of land vulnerable to Floods

> 1 million houses damaged annually + human, social, other losses

16NatCat Exposure

*1998 Gujarat Cyclone Natural Disasters from 1980 - 2010

500 million USD economic loss (250 million Overview

insured loss), No of events: 431

No of people killed: 143,039

*1999 Orissa Super Cyclone No of people affected: 1,521,726,127

2.5 billion USD economic loss (100 million Average affected per year: 49,087,940

insured loss), Economic Damage (Eur X 1,000): 36,972,177

Economic Damage per year (Eur X 1,000): 1,192,651

*2001 Gujarat (Bhuj) 7.7 Mw Earthquake

4.0 billion USD economic loss,

*2004 Sumatra Andaman 9.2 Earthquake

and Tsunami

1.0 billion USD economic loss (India),

16,000+ deaths (India)

*Sikkim 2011

Expected Economic Loss : US$ 22.3 billion

Magnitude 6.9 Mm

17NatCat Exposure

Vulnerability Atlas-Earthquake

10.9% land is liable to severe

earthquakes (intensity MSK IX or

more) ·

17.3%landis liable to

MSKVIII(similar to Latur/

Uttarkashi)

30.4% land is liable to MSK VII

(similar to Jabalpur quake)

Biggest quakes in: Andamans, Kutch,

Himachal, Kashmir, N. Bihar and the

North

East

18NatCat Exposure

Vulnerability Atlas-Flood

Floods · Floods in the Indo-

Gangetic-Brahmaputra plain are an

annual feature

Major Floods List:

Jammu & Kashmir Floods 2014

Uttarakhand Flash Flood 2013

Himalayan Flash Flood 2012

Brahmaputra Floods 2012

Ladakh Floods 2010

Orissa Floods 2009, Kerala, Karnataka, North -East

Bihar Floods, 2008

Gujarat Floods 2005

Mumbai Floods 2005

Chennai Floods 2005

Bihar Floods, 2004

19NatCat Exposure

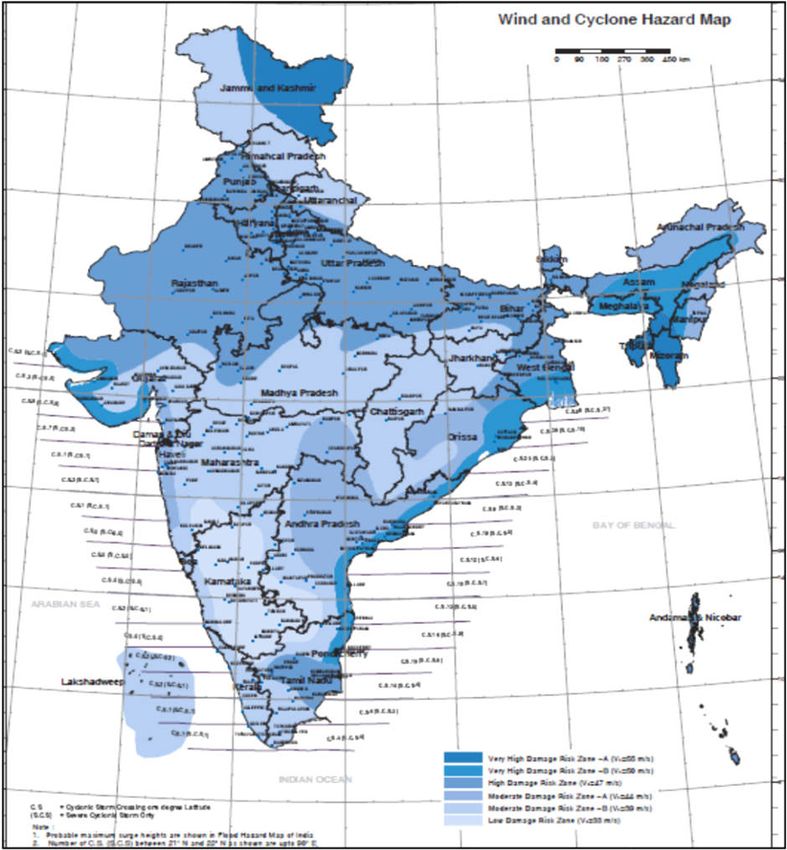

Vulnerability Atlas- Wind and

Cyclones

1877-2005: 283 cyclones (106

severe) in a 50 km wide strip on

the East Coast

Less severe cyclonic activity on

West Coast (35 cyclones in the

same period)

In 19 severe cyclonic storms,

death toll> 10,000 lives

In 21 cyclones in Bay of Bengal

(lndia+Bangladesh) 1.25 million

lives have

been lost

20Special Economic Zones

A designated duty free enclave to be treated as foreign territory

Domestic sales subject to full customs duty

Duty free import/domestic procurement of goods

100% Income Tax exemption on export income

Exemption from Central Sales Tax

Exemption from Service Tax

Impact during claim

Re-import may cause duty/taxes

Removal of damaged items out side the Zone requires duty/tax

payment

Duty/Tax to be taken care in Insured Value

21FEMA Regulation

FEMA-FOREIGN EXCHANGE (INSURANCE) MANAGEMENT REGULATIONS

PART A - GENERAL INSURANCE

15A.1 Persons, firms, companies, etc. resident in India are not permitted to

take general insurance of any kind with insurance companies in foreign

countries without prior approval of Reserve Bank.

Besides, permission of Government of India under General Insurance

Business (Nationalization) Act, 1972, is also required in such cases. Proposals

for direct insurance outside India should be submitted to Reserve Bank

explaining reasons for seeking such insurance cover and producing a

certificate issued by GIC or any of its subsidiaries to the effect that the

proposed insurance cover cannot be obtained from them.

22Fluctuating FOREX (INR versus EUR)

Valuation of assets should factor the volatility in the rupee exchange rate.

23DIC and Tax

European manufacturer

Global policy covering HQ and Overseas locations including India

Fire at warehouse in India

Two payments under the claim

Euro 7.69 million to India Branch

Euro 15.38 million to HQ under DIC/DIL

Indian Tax authorities levied tax on Euro 15.38 million

Any claim for the loss in India is taxable in the country

24You can also read