Brazil: Bolsonaro's deep realignment - ING Think

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Economic and Financial Analysis

Global Economics

27 April 2020

Brazil: Bolsonaro’s deep realignment

Article

The departure of Justice Minister Sergio Moro was illustrative of a deeper

political realignment for the Bolsonaro administration. The question now is

whether Bolsonaro is also readying for an economic policy realignment. To

preserve its fiscal anchor, it is essential that Paulo Guedes stays on as

Economy Minister

Brazil's President Jair Bolsonaro, right, talks with his Economy Minister Paulo Guedes

Content

- Reassessing the three pillars

- Bolsonaro seeks a deeper political realignment

- Tweaking the economic policy pillar

- Is Economy Minister Paulo Guedes still in charge?

- Scope for change in monetary policy has been reduced

Reassessing the three pillars

President Bolsonaro was elected by emphasising three pillars: a conservative social agenda, an

anti-corruption platform, which proved especially effective in light of the practices unveiled by

the wide-reaching “Carwash” investigations, and the liberal economic policies advocated by

Economy Minister Paulo Guedes.

Of these three pillars, the first one is probably the only one that remains intact, even though

Bolsonaro has little to show for it, in terms of legislative accomplishments.

The President’s patronage of the anti-corruption agenda lost steam early on, after

investigations into his son, Senator Flavio Bolsonaro, dominated the front pages of Brazilian

papers. Legislative accomplishments on this front were also underwhelming, but Bolsonaro still could legitimately claim the anti-corruption political mantle thanks to the fact that he had Sergio Moro, the popular judge that spearheaded the “Carwash” investigations, as his Justice Minister. That second pillar came crashing down last Friday with Moro's surprising resignation, following the dismissal of the federal police chief, a Moro appointee, by President Bolsonaro. Moro’s acrimonious departure, which included claims of misconduct by the President, has caused immense political disarray, and its political impact is bound to be wide-ranging, but remains too soon to fully assess. Bolsonaro seeks a deeper political realignment For now, our main takeaway is that Bolsonaro has opted to pursue a deeper political realignment. With Moro’s exit, the President’s personal political capital should diminish, as he will likely lose a considerable segment of his popular support base that feels a closer attachment to Moro and the “Carwash” legacy. But Bolsonaro also appears to have negotiated the political backing of the parties comprising the so-called “Centrão”. These parties are often characterised as the large and less ideological segment of Congress that favour a more transactional political support system, typically involving the exchange of votes for power. Despite the apparent support of the “Centrão” parties, Bolsonaro’s political sustainability is now under question. The risk of an impeachment is real, but should not be overblown. We suspect the coronavirus crisis will take precedent in the nearer term, effectively buying the administration some time and delaying the risk of impeachment proceedings. Ultimately, however, Bolsonaro’s political vulnerability will be determined by his popular support. Should the President’s popular support drop from its typical 30-40% range to less than 20%, questions about his political sustainability should intensify. Tweaking the economic policy pillar Of the three pillars mentioned above, the economic policy pillar, personified by Economy Minister Paulo Guedes, has been, arguably, the most successful aspect of Bolsonaro’s term in office. Among its main achievements, we would highlight the approval of the social security reform last year and the market credibility achieved by its handling of fiscal and monetary policies, as evidenced by the sharp drop in interest rates and risk premium seen for Brazilian assets. Despite these successes, the recovery in economic activity has been frustratingly slow and the economic fallout from the coronavirus crisis appears to have exacerbated concerns over the general economic policy directives advocated by Guedes. It is evident that the looming recession has widened the scope for a clash between Guedes and other members of the cabinet. But it’s still unclear if the President is ready to dismiss his Economic Minister, of if Guedes is ready to ditch Bolsonaro. An eventual departure of Paulo Guedes and his pro-market agenda is not yet priced into local assets. Such an outcome would cause material weakness in all local assets. Is Economy Minister Paulo Guedes still in charge? Evidence that Bolsonaro is ready to move away from the third pillar of his campaign was most evident in the recent announcement of a pro-growth plan centred on boosting public

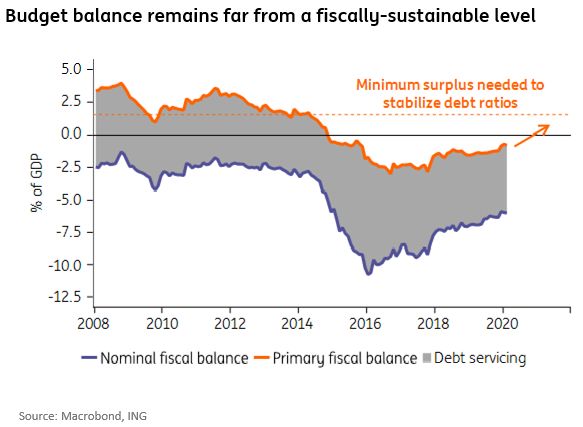

investment (“Pró-Brasil” plan). The public works programme spearheaded by Bolsonaro’s military-aligned chief-of-staff would represent a sharp departure for the current administration. This is both because it would pressure fiscal spending and because it would clash with Guedes’s overarching objective to reduce the presence of the state in the economy, with an ambitious agenda focused on privatisations and concessions. Few details were presented at the unveiling of the plan, which did not count with the presence of Guedes. Subsequent statements by government officials also suggested that the project remained in an embryonic state. Overall, it is too soon to say if Guedes will remain the primary formulator for economic policy in Brazil. Earlier this morning Bolsonaro reiterated his commitment to keep Guedes in charge of all economic policy matters in Brazil. The announcement of the “Pró-Brasil” plan was the most concrete example seen so far of a formal plan that has been forcefully rejected by Guedes. Its adoption remains uncertain however, and until we know the actual scope of the project, it will be hard to assess to what extent the administration is deviating from its original flight plan. Scope for change in monetary policy has been reduced Chief among the uncertainties created by an eventual departure by Guedes would be the sustainability of Brazil’s fiscal outlook. Brazil’s fiscal accounts remain a primary source of concern. As seen in the chart below, even though fiscal policy remains deeply contractionary, the fiscal deficit remains too large to stabilise debt-to-GDP dynamics. A deep fiscal deterioration is likely this year. Thanks to the fiscal spending needed to counteract the impact of the coronavirus outbreak, budget spending is set to surge in 2020, with the primary deficit likely surging towards 6-7% of GDP. But, thanks to Brazil’s fiscal framework, a deep fiscal contraction is expected for next year. However, should that change, the risk of the economic team's departure would rise considerably. In principle, the primary catalyst for that would be the de-facto elimination of the fiscal spending ceiling rule. This could be achieved through the outright elimination of the rule,

by Congress, or through the introduction of exemptions to the ceiling, rendering the ceiling

innocuous.

The rise in political uncertainties created (temporary?) damage to the fiscal outlook

and, as a result, reduced the scope for the central bank to cut the policy rate in the

upcoming meetings.

Market pricing is now incorporating another 50 basis point drop in the SELIC rate next

week, to 3.25%, followed by another partly-priced 25bp cut in June. This compares with

expectations of a 125bp drop in the policy rate (75bp + 50bp) seen before Minister

Moro’s resignation.

Confirmation that Minister Guedes remains firmly in charge of economic policy should

gradually help eliminate fears that the fiscal anchor will weaken. But the rise in political

uncertainty suggests that fiscal uncertainties should also remain elevated in the

foreseeable future. We now expect BACEN to cut the SELIC rate next week by 50bp,

from 3.75% now, with scope for future cuts largely dependent on the evolution of the

political crisis and the fiscal outlook.

For the currency, our expectation is that the USD/BRL should peak at 5.8, but

confirmation of a deeper realignment of economic policy, with the departure of

Guedes, would likely prompt an even deeper selloff, towards 6-6.5.

Gustavo Rangel

Chief Economist, LATAM

+1 646 424 6464

gustavo.rangel@ing.comDisclaimer

"THINK Outside" is a collection of specially commissioned content from third-party sources, such as economic think-tanks and academic

institutions, that ING deems reliable and from non-research departments within ING. ING Bank N.V. ("ING") uses these sources to expand the

range of opinions you can find on the THINK website. Some of these sources are not the property of or managed by ING, and therefore ING

cannot always guarantee the correctness, completeness, actuality and quality of such sources, nor the availability at any given time of the

data and information provided, and ING cannot accept any liability in this respect, insofar as this is permissible pursuant to the applicable

laws and regulations. This publication does not necessarily reflect the ING house view. This publication has been prepared solely for

information purposes without regard to any particular user's investment objectives, financial situation, or means. The information in the

publication is not an investment recommendation and it is not investment, legal or tax advice or an offer or solicitation to purchase or sell

any financial instrument. Reasonable care has been taken to ensure that this publication is not untrue or misleading when published, but ING

does not represent that it is accurate or complete. ING does not accept any liability for any direct, indirect or consequential loss arising from

any use of this publication. Unless otherwise stated, any views, forecasts, or estimates are solely those of the author(s), as of the date of the

publication and are subject to change without notice. The distribution of this publication may be restricted by law or regulation in different

jurisdictions and persons into whose possession this publication comes should inform themselves about, and observe, such restrictions.

Copyright and database rights protection exists in this report and it may not be reproduced, distributed or published by any person for any

purpose without the prior express consent of ING. All rights are reserved. ING Bank N.V. is authorised by the Dutch Central Bank and

supervised by the European Central Bank (ECB), the Dutch Central Bank (DNB) and the Dutch Authority for the Financial Markets (AFM). ING

Bank N.V. is incorporated in the Netherlands (Trade Register no. 33031431 Amsterdam).You can also read