Brexit | VAT in a post-Brexit world Pitfalls and opportunities - 25 February 2021 - Deloitte

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Brexit | VAT in a post-Brexit world Pitfalls and opportunities 25 February 2021

Agenda

1 Introduction & practicalities

2 Setting the scene

3 Belgian VAT perspective and insights

4 UK VAT perspective and insights

5 Insights from Belgian VAT authorities

6 Insights from a Belgian company

7 Questions & answers

8 Wrap-up

© 2021. For information, contact Deloitte Belgium. VAT in a post-Brexit world | Pitfalls and opportunities

Today’s speakers

Richard Doherty Jan Vrijsen Gareth Pritchard Alina Cozma Jean-Claude Semucyo Luc Lammertyn

Brexit advisor Senior Manager Tax partner Belgium VAT Belgium VAT Authorities Chief Logistics Officer

Deloitte Belgium Indirect Tax (VAT) Deloitte UK Administration VAT expert Sioen Industries

Deloitte Belgium VAT expert

© 2021. For information, contact Deloitte Belgium. VAT in a post-Brexit world | Pitfalls and opportunities

Practicalities

• The webinar is being recorded and will

be available afterwards on Deloitte's Brexit Readiness Centre

• The slide deck can be downloaded in pdf in the module

"Documentation & Links“ on your webinar console

• Don’t hesitate to drop questions or comments in the chatbox

(anonymously)

• Questions will be addressed towards the end of the webinar

or after the event

© 2021. For information, contact Deloitte Belgium. VAT in a post-Brexit world | Pitfalls and opportunities

Setting the scene Richard Doherty | Deloitte Belgium Brexit Advisor

The world has changed … From: METRO News © 2021. For information, contact Deloitte Belgium. VAT in a post-Brexit world | Pitfalls and opportunities

Deal avoids tariffs …

but UK has made a definitive move out of EU

EU Member State EU-UK Trade deal WTO

27 Member States UK Australia

Frictionless movement of goods, services & capital Yes No No

Big Brexit changes Absence of tariffs and quotas on goods trade Yes Yes No

Free movement of people Yes No No

Free to negotiate trade deals No Yes Yes

Influence Yes No No

EU laws and regulation

Compliance Yes Some No

Fiscal contributions Yes No No

Common Agricultural Policy (CAP) Yes No No

© 2021. For information, contact Deloitte Belgium. VAT in a post-Brexit world | Pitfalls and opportunities

What the UK-EU Trade and Cooperation Agreement tells us

Goods

Trade in goods Technical barriers to trade Rules of origin Customs and trade International road

and SPS measures facilitation transport

Services

Mutual recognition of Financial services Data and digital Cross-border trade in Intellectual property

professional qualifications services

People Government

Temporary entry and stay Social security coordination Tax Participation in Union

for business purposes & healthcare arrangements programmes

© 2021. For information, contact Deloitte Belgium. VAT in a post-Brexit world | Pitfalls and opportunities

Northern Ireland “iceberg” 30 January 2021 11 February 2021 EU reverses course after Irish border curbs for vaccines trigger uproar: Brussels fires warning shot at UK over N Ireland protocol: Brussels proposals raised deep concern in Dublin, Belfast and London EU urges action on customs rules ‘shortcomings’ From: Financial Times © 2021. For information, contact Deloitte Belgium. VAT in a post-Brexit world | Pitfalls and opportunities

Outstanding issue on Data Transfer Data flows – the European Commission has announced that it recognises the high data protection standards in the UK and that the UK should be found ‘adequate’. © 2021. For information, contact Deloitte Belgium. VAT in a post-Brexit world | Pitfalls and opportunities

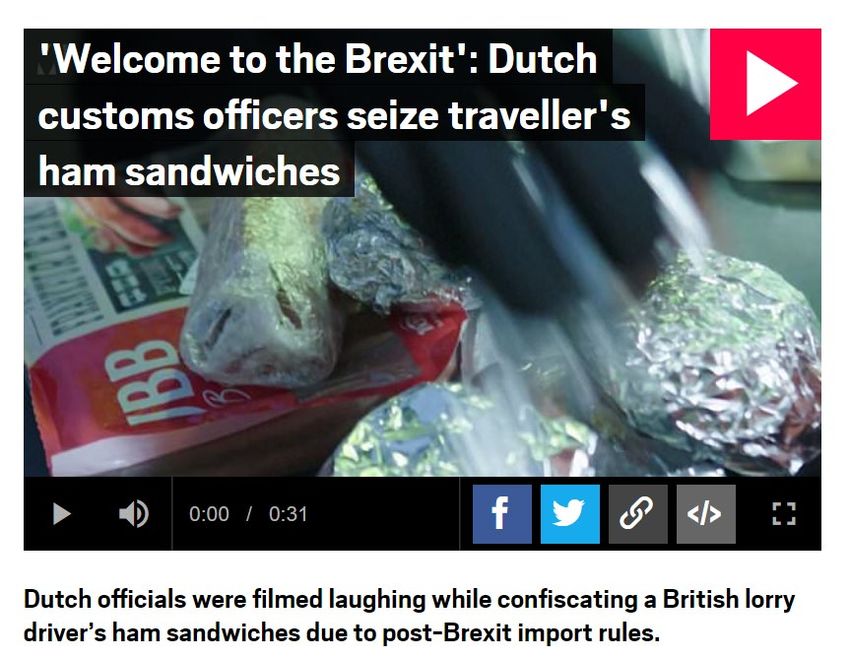

Early impact on business 19 February 2021 UK manufacturing hit by Brexit trade disruption: And UK shellfish exporters have suddenly found their main market Europe cut off UK’s small businesses struggle with Brexit red tape: many companies by a welter of new health rules. forced to shift operations to EU or risk sliding profits and lost sales. From: Financial Times © 2021. For information, contact Deloitte Belgium. VAT in a post-Brexit world | Pitfalls and opportunities

Financial Services

The future of the City of London

Having already picked up activity in

swaps and sovereign debt markets,

Amsterdam has ousted London as

Europe’s top share trading hub after

Brexit … The City of London's dominance

of European financial markets has also

come under threat from Paris and New

York.

But it’s still huge!

© 2021. For information, contact Deloitte Belgium. VAT in a post-Brexit world | Pitfalls and opportunitiesBelgian VAT perspective and insights Jan Vrijsen, Senior Manager Deloitte Belgium

Changes from 1 January 2021

Key VAT considerations REMOVAL OF EU

SIMPLIFICATIONS

OTHER

B2C SALES

(E-COMMERCE)

MOSS

REFUND FOREIGN VAT

TRANSACTIONS BRIDGING

31/12/2020

IMPORT INTO BE/EU

EXPORT OUT OF BE/EU

© 2021. For information, contact Deloitte Belgium. VAT in a post-Brexit world | Pitfalls and opportunitiesExporting out of EU/BE and importing into EU/BE

VAT considerations (continued)

Some key VAT issues

VAT exemption for export: proof?

Import VAT deduction: supporting documents

Incoterms and determination of (customs) roles

VAT prefinancing

ERP-system update

Services from logistics providers

© 2021. For information, contact Deloitte Belgium. VAT in a post-Brexit world | Pitfalls and opportunitiesExporting out of EU/BE and importing into EU/BE

Transactions bridging 31/12/2020

Key VAT considerations

Supply up to 31/12/2020 –

Invoice on or after 01/01/2021

TP corrections in 2021 relating to supplies

from 2020

Return of goods

© 2021. For information, contact Deloitte Belgium. VAT in a post-Brexit world | Pitfalls and opportunitiese-Commerce VAT package and Brexit

Distance sales of imported goods

B2C online sales of imported goods from outside the EU

Non-EU • January – June 2021

MS

Member State

− Import VAT exemption on low value goods, value < 22 EUR per item

− VAT registration obligations?

• July 2021 - …

EU or non-EU Seller − Introduction of Concept imported distance sales

Customer

or Electronic

Interface (EI) − Import of low value goods ( 150 EUR per item:

◦ Regular import

◦ VAT registration obligation

◦ Import VAT + local VAT

© 2021. For information, contact Deloitte Belgium. VAT in a post-Brexit world | Pitfalls and opportunitiesUK VAT perspective and insights Gareth Pritchard, Tax partner, Deloitte UK

Compliance issues

VAT registration and EORI numbers and Fiscal representation

VAT registration Fiscal representation

• Delays! • The UK-EU Trade and Cooperation Agreement includes a protocol

on VAT administrative cooperation and combating fraud, as well as

− Processing around 70 % of the VAT registration applications mutual assistance for the recovery of claims relating to taxes/duties.

within 30 days and the majority of those cases within 5 working

days. • In principle businesses established in the UK, be able to register for

VAT in EU Member States without the obligation to appoint a fiscal

− Expect to be processing 95 % of VAT Registrations within 30 days representative.

by the end of March 2021.

• If no mutual assistance legal instrument, Member States can (Art.

− Encouraging agents and businesses to check that all information 204, PVD) require such taxable persons established outside the EU

requested is included with their application – New VAT to appoint a tax representative.

registration application form.

• The European Commission is expected to conclude on the UK-EU

− Use the online VAT Registration service wherever possible – protocol’s equivalence in scope in April.

quicker.

• Until such time the requirement for UK taxpayers to appoint a fiscal

representative is still being determined at individual EU Member

EORI numbers State level.

• Delays

• Customs implications

© 2021. For information, contact Deloitte Belgium. VAT in a post-Brexit world | Pitfalls and opportunitiesPostponed Import VAT Accounting

Account for import VAT on the VAT return that relates to the

declaration that releases the goods into free circulation or from the

customs special procedures

VAT return:

Box 1: VAT due in this period on imports

Box 4: VAT reclaimed in this period on imports

Box 7: Total value of all imports of goods

An online monthly statement will be available to show the import

VAT postponed for the previous month

Single Administrative Document (‘SAD’) – C88

Non-established taxable persons must have someone deal with

customs for them, including submission of the customs declaration

© 2021. For information, contact Deloitte Belgium. VAT in a post-Brexit world | Pitfalls and opportunitiesB2C sales

E-Commerce

B2C sales of imported goods from outside the UK - 1 January 2021

• End of the current £15 VAT exemption threshold (Low Value Consignment

Non-UK UK

Relief)

• Overseas goods sold directly to customers in GB:

− Imported goods ≤ £135 subject to UK VAT i.e. output tax instead of

import VAT at the point-of-sale - UK VAT registration required

Non-UK Seller or

Customer − Goods above this value - normal VAT/customs rules

Electronic Interface

(EI) • Overseas goods sold to customers in GB using online marketplaces

(OMPs)

− Goods outside UK at time of sale:

◦ ≤ GBP 135 – OMP to charge UK VAT

◦ Goods above this value - normal VAT/customs rules

− Goods inside UK at time of sale:

◦ Non-UK seller liable for any import VAT and duty

◦ OMP is deemed seller and non-UK seller makes Z/R sale to OMP

• Northern Ireland – EU rules

© 2021. For information, contact Deloitte Belgium. VAT in a post-Brexit world | Pitfalls and opportunitiesUse and Enjoyment

UK Use and Enjoyment provisions

• Now UK – Non-UK

• Includes:

− Hiring of goods;

− Broadcasting services; and

− B2B Electronically supplied services, Repair services and

Telecommunication services

Potential issues

• Leased goods

• Impact for UK businesses making outbound supplies:

− Member States’ application of Art. 59a, PVD

− Issue for Art. 59, PVD, B2C supplies of professional services

◦ Denmark/Sweden

◦ Ireland for FS

◦ Possibly France/Malta

© 2021. For information, contact Deloitte Belgium. VAT in a post-Brexit world | Pitfalls and opportunitiesNorthern Ireland

Northern Ireland Protocol

Application of EU VAT rules for supplies of goods

Multiple issues arising in practice:

• Supplies between Northern Ireland and Great Britain

− Northern Ireland to Great Britain – unfettered access applicable to

‘NI qualifying goods’

− Great Britain to Northern Ireland:

◦ Onward Supply Relief

◦ Trader Support Service

◦ UK Trader Scheme

• XI EORI number

• Supplies between EU and Great Britain via Northern Ireland

− Import VAT accounted for as output tax

• XI VAT registration for NI / EU trade

© 2021. For information, contact Deloitte Belgium. VAT in a post-Brexit world | Pitfalls and opportunitiesInsights from Belgian VAT authorities Alina Cozma and Jean-Claude Semucyo, VAT experts Belgium VAT Administration

BELGIAN INSIGHT CONCERNING THE IMPACT OF THE UNITED

KINGDOM’S WITHDRAWAL FROM THE EU (BREXIT)BREXIT - BELGIAN INSIGHT

• Communication regarding Brexit

• Official information published by the Belgian tax administration on the FPS Finance website

• FAQs “Brexit and VAT” published in FR, NL and EN

• Open issues/work in progress

• VAT registration of British tax payers operating in Belgium

• Claims of Belgian VAT Refund by British businesses (13th Directive)

• Claims of British VAT Refund by Belgian businessesA. VAT REGISTRATION What are the rules applicable with regard to the obligation for a British company to register for VAT purposes in Belgium? • Taxable persons not established in the EU and carrying out operations in Belgium for which they are liable to VAT are obliged to appoint a fiscal representative (art.55,§1 of Belgian VAT Code, based on art.204 of Directive 2006/112/EC). • However, taxable persons established in a third country with which the Union has concluded an agreement on mutual assistance similar in scope to Council Directive 2010/24/EU concerning mutual assistance for the recovery of claims related to taxes, duties and other measures and to Regulation (EU) n° 904/2010 on administrative cooperation and combating fraud in the field of value added tax, are not obliged to appoint a fiscal representative in Belgium. • The EU-UK Trade and Cooperation Agreement concluded in December 2020 contains a Protocol on administrative cooperation in the field of VAT. • The Belgian authorities have questioned the Commission on the exact scope of the Protocol. The Commission is considering the issue but has not yet formulated an official position.

A. VAT REGISTRATION

Provisional position of the Belgian tax administration

• October 2020 => Belgian tax administration invited all British taxpayers which already have a direct VAT

registration in Belgium to appoint a fiscal representative (deadline: 31 March 2021) … BUT

• BUT in January 2021 => the Belgian tax administration informed all concerned British taxpayers of the:

• SUSPENSION of the obligation to appoint a fiscal representative (but it remains possible)

• Continuation of the direct registration procedure currently applied

• Consequence => All British companies introducing an application for VAT direct registration as from

1 January 2021 will receive (on a temporary basis) a direct VAT ID number.

• Once the European Commission publishes its official position, the Belgian tax administration will

communicate on this issue. This communication will be done via an update of the FAQs published on the

website of FPS Finance. British taxable persons will also be informed.B. CLAIMS OF BELGIAN VAT REFUND BY BRITISH BUSINESSES

(13TH DIRECTIVE)

Current rules

• Each claim of Belgian VAT refund, filed by a British taxable person who is not registered for VAT in Belgium,

related to transactions carried out as from 1 January 2021, can no longer be submitted to the British

Authorities via the VAT REFUND system

• This claim must be submitted directly to the Belgian VAT Authorities pursuant to the conditions for taxable

persons established outside the European Union (13th Directive)

• The 13th Directive current procedure requires that the claim and the originals of the paper invoices be sent

to the Belgian VAT Authorities - Center for Specific Matters (foreign center) by (postal) mail or courier serviceB. CLAIMS OF BELGIAN VAT REFUND BY BRITISH BUSINESSES

(13TH DIRECTIVE)

Draft modification of the 13th Directive procedure

• Considering that Brexit and the new e-commerce package entering into force as from July 1, 2021 will have a

very significant impact on the volume of claims of Belgian VAT refund, the Belgian VAT Authorities are

currently working on a modernisation of the 13th Directive procedure

This modification will consist of:

• a new royal decree setting the conditions for the application of the Belgian VAT refund claim under the 13th

Directive

• the transformation of the current paper/mail procedure into a fully digital procedure largely modeled on the

VAT REFUND procedureC. CLAIMS OF BRITISH VAT REFUND BY BELGIAN BUSINESSES • For transactions carried out during the period from 1 January - 31 December 2020, claims of British VAT refund can still be submitted to the Belgian VAT Authorities via Intervat - VAT Refund until 31 March 2021 at the latest • For transactions carried out on or since1 January 2021, claims of British VAT refund are no longer covered by European legislation. The conditions for refund and the procedures to be followed to obtain a refund are solely the competence of the British authorities

Managing post-Brexit VAT effects Luc Lammertyn, Chief Logistics Officer Sioen Industries NV

SIOEN INDUSTRIES NV

Fabriekstraat 23 – B-8850 Ardooie – Belgium –

sioen.comEU exports – UK imports:

our experience

Use of incoterms – Often depends on the size of the business or

type of transaction

Type of business/ Incoterm most likely used

transaction

Small customers with DDP (Delivered Duty Paid)

frequent deliveries

Import using your UK VAT number

(do not forget to apply postponed VAT

accounting)

If possible: intercompany flow (buy & Attention points when you use your own UK VAT number to

sell): invoice to UK customer with UK import in the UK:

VAT out of your UK sister company

You need a UK EORI number linked to this UK VAT number

Large industrial DAP (Delivery At Place) possible? Box 8: EORI number of Sioen and UK VAT number

customers and

Box 14: customs broker and his UK EORI number

distributors

Box 44: 9DCR = Sioen EORI number

Call-off stocks sold to DDP is advisable (and often the only Box 47A: B00 and in column E: G

customers possibility), so use your UK VAT number

(“consignatie”) A UK VAT number is not easy to obtain and interaction with UK

VAT authorities tends to be slowUK exports - EU imports

DAP incoterm

Customer is responsible for the import clearance

process in EU

VAT (financing) and import administration for

customer need to be organised for this. Focus on

preferential origin as included in the UK-EU agreement

Not all EU member states accept postponed VAT

accounting

Solution: importing first into BE (or NL)

DDP incoterm

A Belgian VAT number allows you to import into Belgium and

Supplier is also responsible for the import clearance on-sell into the EU using this VAT number (VAT exempt import

process in the EU + VAT exempt intra-Community supply so no prefinancing of

VAT registration for UK company in each EU member VAT)

state may be too complicated Attention points

− need to have a fiscal representative in BE?

− need to have a BE EORI number and ET14000

− if you import from UK to a non-Belgian port (e.g. Calais,

Rotterdam, …), you will need to have a transit document

valid all the way to the Belgian place of import clearanceQuestions & answers All

And remember – there are two sides to every story ITV News, 14 January 2021 BBC News, 17 January 2021 © 2021. For information, contact Deloitte Belgium. VAT in a post-Brexit world | Pitfalls and opportunities

Wrap-up

Brexit Readiness Centre

Your gateway to latest developments, analysis and insights

Featuring

• Latest developments

• Upcoming webinars and seminars

• Brexit Readiness Updates

• Business impact

• Industry insights

• How Deloitte can help

www.deloitte.com/be/brexit-readiness-centre

© 2021. For information, contact Deloitte Belgium. VAT in a post-Brexit world | Pitfalls and opportunitiesBrexit Readiness Centre How Deloitte can help | Brexit Readiness Workshop © 2021. For information, contact Deloitte Belgium. VAT in a post-Brexit world | Pitfalls and opportunities

Brexit Help Centre

Who to contact for help?

Brexit Task Force

• Corporate & withholding tax

• Customs and trade

• Legal

• Location strategy

• People

• Public funding

• Risk management

• SMEs

• Supply chain

• Technology

• VAT

Reach out to us by scanning the

QR code or by e-mailing us at

BeBrexit@deloitte.com

© 2021. For information, contact Deloitte Belgium. VAT in a post-Brexit world | Pitfalls and opportunitiesAbout Deloitte Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and their related entities. DTTL and each of its member firms are legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not provide services to clients. Please see www.deloitte.com/about for a more detailed description of DTTL and its member firms. Deloitte provides audit, tax and legal, consulting, and financial advisory services to public and private clients spanning multiple industries. With a globally connected network of member firms in more than 150 countries, Deloitte brings world-class capabilities and high-quality service to clients, delivering the insights they need to address their most complex business challenges. Deloitte has in the region of 330,000 professionals, all committed to becoming the standard of excellence. This publication contains general information only, and none of Deloitte Touche Tohmatsu Limited, its member firms, or their related entities (collectively, the “Deloitte Network”) is, by means of this publication, rendering professional advice or services. Before making any decision or taking any action that may affect your finances or your business, you should consult a qualified professional adviser. No entity in the Deloitte Network shall be responsible for any loss whatsoever sustained by any person who relies on this publication. Deloitte Legal - Lawyers CVBA in Belgium Deloitte Legal - Lawyers CVBA is part of a privileged multidisciplinary cost-sharing association with Deloitte Belastingconsulenten CVBA. © 2021 Deloitte BE. All rights reserved. Designed by the Creative Studio at Deloitte, Belgium

You can also read