RESEARCH Industrial Vacancy Report - South African Property ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

RESEARCH Industrial Vacancy Report

Results for the APRIL

12 months ended

December 2017 2018

KEY FINDINGS

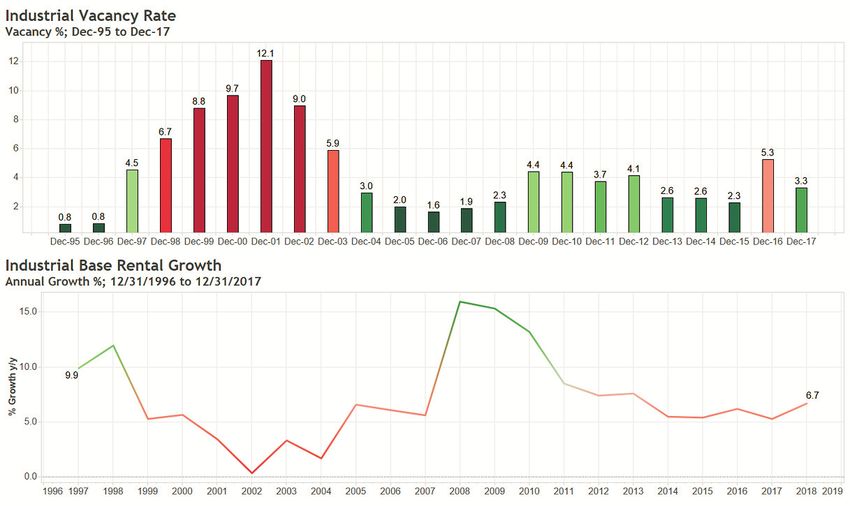

As at December 2017, the national industrial vacancy rate as recorded by IPD was 3.3%. While this is

down from a revised 5.3% at December 2016, it is 100bps up from December 2015. Historic IPD data

going back to 1995 suggests that rental growth has lagged shifts in vacancy rate as excess supply or

demand typically takes a period of time to filter through to pricing. The current point in the cycle is no

different as the lower vacancy rate experienced through 2017 hasnÕt had a pronounced impact on base

rental growth yet. Data out of the listed sector suggests that industrial escalation rates average 7-8%

which suggests that current rental reversions are on aggregate flat to marginally negative.

The basic rental growth of 6.7% recorded for the 12 months ended December hasnÕt translated into an

equal quantum of capital growth which suggests that valuers are still taking a cautious view on the sectorÕs

near term earnings

The current vacancy level and rental growth suggests that the industrial market is recovering well and

again nearing excess demand. The sectorÕs aggregate vacancy rate is hovering close to its long term

average while the above-inflation base rental growth suggests that the excess market supply has seemingly

all been mopped up.

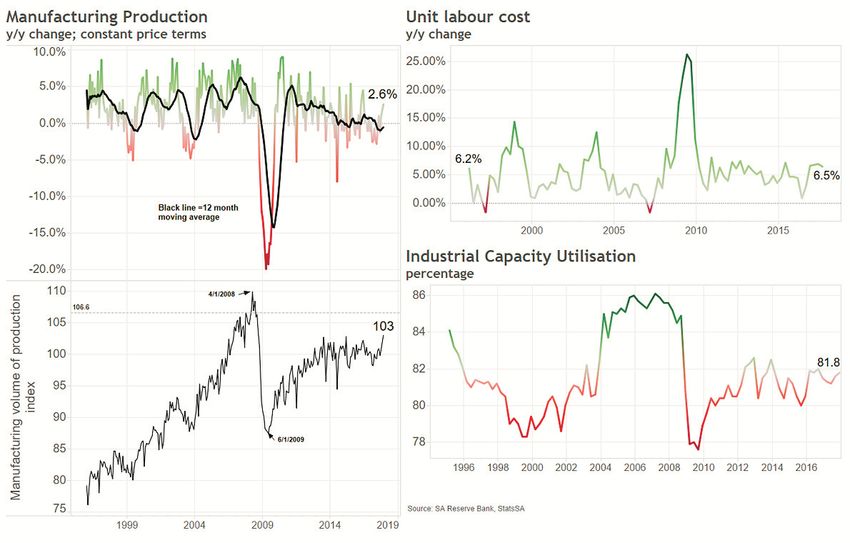

South African manufacturing production posted its highest year-on-year growth of 2.6% in December

2017. While the latest manufacturing growth figure is encouraging, the future growth potential of the sector

also depends on sustained improvements in efficiency measures like capacity utilisation and unit labour

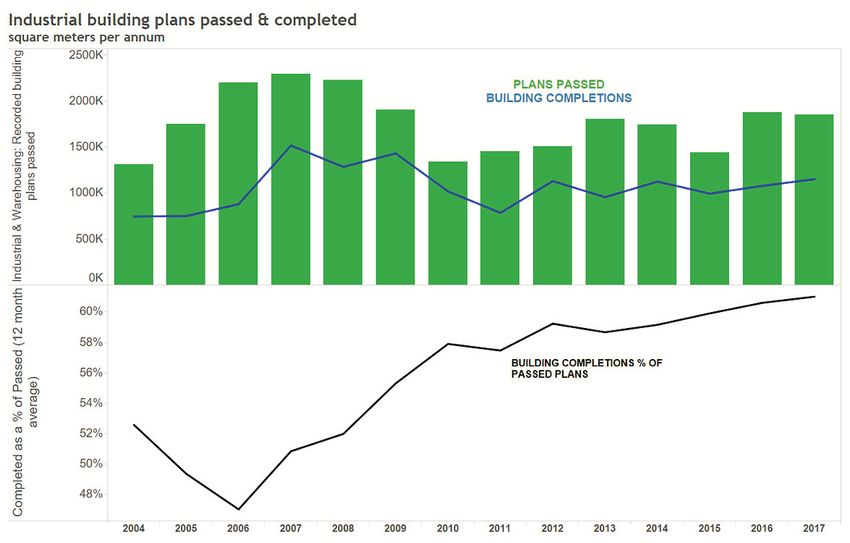

costs. Building plans passed for industrial property declined by 1.5% in 2017 after a year-on-year growth

of 30.6% in 2016. While an increasing number of plans are being passed relative to 2014 & 2015, supply

remains well below the peak levels of 2007/Õ08 and is the driving factor behind the low vacancy rate and

above inflation rental growth in selected segments and geographies.

With the exception of High Tech industrial property, all other segments saw vacancy rates improve during

the 12 months ended December 2017. High-tech industrial vacancies increased by 40bps off a lower

base relative to other segments. High tech industrial property still has the lowest vacancy rate of the

industrial segments at 1.8%. High tech industrial segment still seems to be in a sweet spot where demand

is seemingly quite strong and supply is hampered by a shortage of industrial land and electricity/zoning

difficulties.

Analysing industrial property by box size reveals that there is currently more space available in mid-sized

units. Small industrial units (0-2.5k sqm) saw an improvement in vacancy rate Ð ending 2017 at 3.2% off

4.2% at the end of 2016. The larger industrial size brackets saw vacancy rates improve during 2017

While the aggregate industrial vacancy rate remains low in historical terms at 3.3% there is significant

variance between nodes.ÊSome nodes currently offer virtually zero available space & in most cases, these

nodes are also seeing improvements in rental growth momentum.

T: (011) 883 0679 F: (011) 883 0684

Email: marketingmanager@sapoa.org.za 02

Web: www.sapoa.org.za

Results for the APRIL

12 months ended

December 2017 2018

NATIONAL INDUSTRIAL VACANCY

& RENTAL GROWTH TREND

As at December 2017, the national industrial vacancy rate as recorded by IPD was 3.3%. While this is

down from a revised 5.3% at December 2016, it is 100bps up from December 2015. Historic IPD data

going back to 1995 suggests that rental growth has lagged shifts in vacancy rate as excess supply or

demand typically takes a period of time to filter through to pricing. The current point in the cycle is no

different as the lower vacancy rate experienced through 2017 hasnÕt had a pronounced impact on base

rental growth yet. Data out of the listed sector suggests that industrial escalation rates average 7-8%

which suggests that current rental reversions are on aggregate flat to marginally negative.

The basic rental growth of 6.7% recorded for the 12 months ended December hasnÕt translated into an

equal quantum of capital growth which suggests that valuers are still taking a cautious view on the sectorÕs

near term earnings. Meanwhile, a net income growth of 4.6% was recorded for the industrial sector in

2017 suggesting that operating costs grew faster than rental income. Industrial sector capital growth for

2017 was recorded at 2.8% which means that the so-called income residual factor (or valuer sentiment)

detracted -5.9% from capital growth bearing in mind that yield compression also added +2.0% to capital

growth on the back of a 20bp strengthening in the base rental yield.

The current vacancy level and rental growth suggests that the industrial market is recovering well and

again nearing excess demand. The sectorÕs aggregate vacancy rate is hovering close to its long term

average while the above-inflation base rental growth suggests that the excess market supply has seemingly

all been mopped up.

T: (011) 883 0679 F: (011) 883 0684

Email: marketingmanager@sapoa.org.za 03

Web: www.sapoa.org.za

Results for the APRIL

12 months ended

December 2017 2018

ECONOMIC DRIVERS OF THE

INDUSTRIAL SECTOR

South African manufacturing production posted its highest year-on-year growth of 2.6% in December

2017. On an indexed basis, the latest uptick in growth puts manufacturing volumes back at 2008 levels.

While the latest manufacturing growth figure is encouraging, the future growth potential of the sector also

depends on sustained improvements in efficiency measures like capacity utilisation and unit labour costs.

If these measures do not improve it is likely that the aggregate industrial vacancy rate will continue to

hover between 3 & 5%.

The industrial sectorÕs capacity utilisation percentage ended 2017 at 81.8%. While this signals an

improvement since 2014, a level of at least 84-85% is needed to catalyse expansion in the sector as was

the case in the period 2003-2007.

Unit labour costs increased to 6.5% year on year to September 2017 Ð down from 6.9% in the quarter

before. This suggestsÊ that the cost of labour is increasing at a faster rate than manufacturing output

which could have negative consequences for industrial property demand as firms seek to optimise current

operations before looking to expand.

T: (011) 883 0679 F: (011) 883 0684

Email: marketingmanager@sapoa.org.za 04

Web: www.sapoa.org.za

Results for the APRIL

12 months ended

December 2017 2018

ECONOMIC DRIVERS OF THE

INDUSTRIAL SECTOR

Building plans passed for industrial property declined by 1.5% in 2017 after a year-on-year growth of

30.6% in 2016. While an increasing number of plans are being passed relative to 2014 & 2015, supply

remains well below the peak levels of 2007/Õ08 and is the driving factor behind the low vacancy rate and

above inflation rental growth in selected segments and geographies.

On an annual basis, building plans passed is getting closer to peak 2009 levels which may weigh on rental

growth Ð especially if occupiers of new space are leaving behind their old space vacant. Given flat

manufacturing production growth and sub-optimal capacity utilisation it is likely to be more challenging

for landlords to fill excess space.

Building plan completions have remained fairly stable since 2012. Bear in mind, industrial buildings

currently scheduled for completion could have had their plans passed at least a year ago, meaning that

the current decline in plans passed could possibly only reflect in completions a year from now. Apart from

a general contraction in demand for new, purpose built industrial space it could also mean delays in

speculative, tenant driven schemes.

T: (011) 883 0679 F: (011) 883 0684

Email: marketingmanager@sapoa.org.za 05

Web: www.sapoa.org.za

Results for the APRIL

12 months ended

December 2017 2018

PERFORMANCE BY INDUSTRIAL SEGMENT

With the exception of High Tech industrial property, all other segments saw vacancy rates improve during

the 12 months ended December 2017. High-tech industrial vacancies increased by 40bps off a lower base

relative to other segments. High tech industrial property still has the lowest vacancy rate of the industrial

segments at 1.8%. High tech industrial segment still seems to be in a sweet spot where demand is

seemingly quite strong and supply is hampered by a shortage of industrial land and electricity/zoning

difficulties.

Warehousing and light manufacturing property both saw vacancy rates improve by around 1.5% during

the year ended December 2017. Standard units/workshops saw the largest improvement in occupancy

with its vacancy rate improving from 8.0% to end the year at 3.7%.

The vacancy rate of light manufacturing property remains the highest among the industrial segments

suggesting that the weak manufacturing data & currency depreciation of the past year or two is now filtering

through to fundamentals underlying manufacturing related property.

T: (011) 883 0679 F: (011) 883 0684

Email: marketingmanager@sapoa.org.za 06

Web: www.sapoa.org.zaResults for the APRIL

12 months ended

December 2017 2018

PERFORMANCE BY BOX SIZE

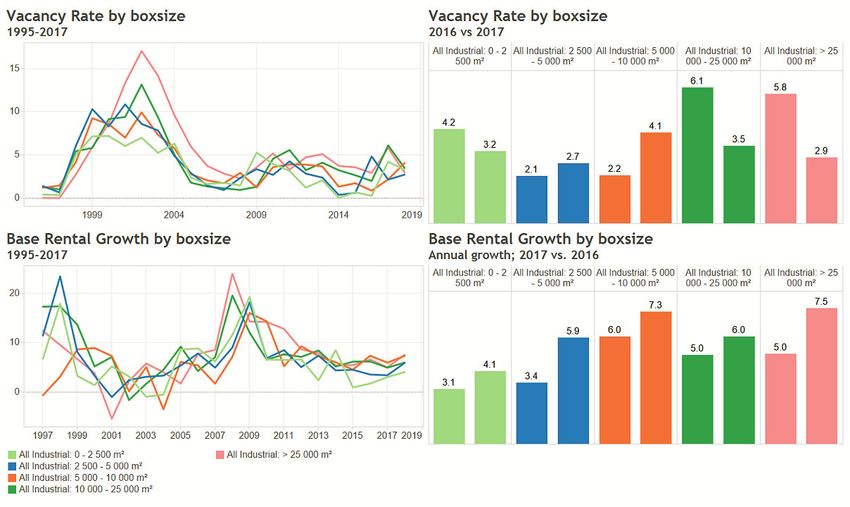

Analysing industrial property by box size reveals that there is currently more space available in mid-sized

units with industrial property sized between 2.5k sqm and 10k sqm seeing an increase in vacancy rate

relative to the year before. Industrial units sized between 5k-10k sqm ended the year with a vacancy rate

of 4.1% - the highest among the size segments.

Small industrial units (0-2.5k sqm) saw an improvement in vacancy rate Ð ending 2017 at 3.2% off 4.2%

at the end of 2016. The year ended December 2016 saw some pressure on the lower end of the size

spectrum as the difficult macroeconomic environment seemingly weighed heavier on smaller operations.

The larger industrial size brackets saw vacancy rates improve during 2017. Industrial units of 10-25k sqm

saw its vacancy rate improve to 3.5% off 6.1% while units large than 25k sqm saw an improvement from

5.8% to 2.9%. Notwithstanding the latest improvement in the occupancy rate of larger units, the currently

vacancy rates are well above 2014 levels which suggests that occupiers may currently be downsizing

their space requirements or splitting up different industrial operations in order to increase capacity utilisation.

This trend may continue since overall industrial capacity utilisation is currently at 81.8% - well off the highs

of 2006/07.

T: (011) 883 0679 F: (011) 883 0684

Email: marketingmanager@sapoa.org.za 07

Web: www.sapoa.org.zaResults for the APRIL

12 months ended

December 2017 2018

NODAL PERFORMANCE

SIGNIFICANT VARIANCE ON NODAL LEVEL

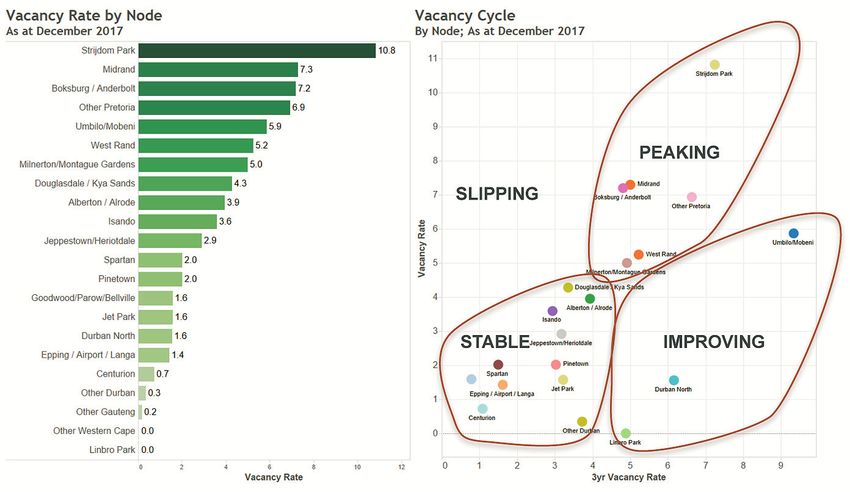

While the aggregate industrial vacancy rate remains low in historical terms at 3.3% there is significant

variance between nodes Ð illustrated below.Ê Some nodes currently offer virtually zero available space

& in most cases, these nodes are also seeing improvements in rental growth momentum. As at December

2017, 12 of 20 industrial nodes have vacancy rates below 4%.

Meanwhile there are others with vacancy rates in excess of 5%. Rental growth in these nodes are mostly

sluggish and in some cases slipping to levels below its 3 year average. Strijdom Park currently has the

highest vacancy rates at around 10% which ahs seen its base rental growth slip down to below 1% from

its 3-year annualised rental growth of 3.6%.

Active asset management with a focus on nodal selection as well as segmental and geographicÊ

diversification remain key during this phase of the property cycle - where it seems tenants are increasingly

adopting a wait-and-see approach.

The graphic below emphasises this point as the major industrial nodes are virtually evenly split in their

current position in vacancy cycle. Almost as many nodes are either seeing vacancy rates Improving,

Slipping, Bottoming out or becoming sluggish or sticky relative to 3 year average.

T: (011) 883 0679 F: (011) 883 0684

Email: marketingmanager@sapoa.org.za 08

Web: www.sapoa.org.zaResults for the APRIL

12 months ended

December 2017 2018

NODAL PERFORMANCE

Analysing basic rental growth on a nodal level reveals a similar pattern to that of vacancy rates. Some

nodes are seeing very strong growth while other nodes are seeing rentals come under pressure Ð

either as a result of vacancy rates increasing or negative rental reversions in the interests of retaining

existing tenants.

Categorising nodes into four quadrants according to their 1 year and 3 year annualised rental growth

rates reveal that rental growth in the majority of nodes can be said to be currently peaking.

Midrand and Bellville/Parow count among the nodes where the one year rental growth figure to

December has slipped well below the three year annualised level which suggests

JohannesburgÕs Linbro Park node, meanwhile, is the only area that saw a pronounced rebound in

rental growth momentum over the past 12 monthsÊ as their one year rental growth surpassed their

low three year rental growth rates.

There has been a pronounced increase in the amount of nodes where rental growth may be peaking

given that the latest year on year rental growth exceeds the three year annualised rate.

Given the fact that rental growth usually lags changes in vacancy rate by at least a year it should

follow that many of the nodes currently in the ÔSluggishÕ quadrant will see rental growth improve over

the next 6-12 months.

T: (011) 883 0679 F: (011) 883 0684

Email: marketingmanager@sapoa.org.za 09

Web: www.sapoa.org.zaResults for the APRIL

12 months ended

December 2017 2018

NODAL PERFORMANCE

Given where the industrial sector finds itself in the property cycle and the variance between individual

nodes with regards to vacancy levels itÕs worth looking at a slightly longer time period.

The map below shows 5 year average vacancy levels for individual industrial nodes in the Johannesburg,

Cape Town and eThekwini metro area. Industrial vacancy rates in the coastal markets remain low overall

with some exceptions. The Umbilo/Mobeni node in KZN has seen occupancy levels come under some

pressure in the last few years.

While 5-year occupancy levels in institutionally owned industrial property in the Western Cape and KZN

is low across the boardÐ this is not the case in Gauteng where a wide variance is observed in the underlying

nodes. This suggests that occupiers of industrial property are preferring certain nodes above others. This

could be for a variety of reasons, including access to main arterial routes, proximity to the airport and

possibly the location of eToll routes in Gauteng.

The peripheral Strijdom Park node has seen its overall vacancy rate increase as some large occupiers

have seemingly chosen not to renew leases. The major nodes around the airport meanwhile maintains

their low vacancy rates highlighting the value of proximity to ports in an environment where transport

costs are increasing faster than inflation.

T: (011) 883 0679 F: (011) 883 0684

Email: marketingmanager@sapoa.org.za 10

Web: www.sapoa.org.zaResults for the APRIL

12 months ended

December 2017 2018

SAMPLE COMPOSITION

AS AT DECEMBER 2017

T: (011) 883 0679 F: (011) 883 0684

Email: marketingmanager@sapoa.org.za 11

Web: www.sapoa.org.zaResults for the APRIL

12 months ended

December 2017 2018

ABOUT MSCI

For more than 40 years, MSCIÕs research-based indexes and analytics have helped the worldÕs

leading investors build and manage better portfolios.Ê

Clients rely on our offerings for deeper insights into the drivers of performance and risk in their

portfolios, broad asset class coverage and innovative research.

Our line of products and services includes indexes, analytical models, data, real estate

benchmarks and ESG research.Ê

MSCI serves 98 of the top 100 largest money managers, according to the most

recent P&I ranking.

For more information, visit us at www.msci.com

Report compiled by:

T: (011) 883 0679 F: (011) 883 0684

Email: marketingmanager@sapoa.org.za 12

Web: www.sapoa.org.zaResults for the APRIL

12 months ended

December 2017 2018

NOTICE AND DISCLAIMER

This document and all of the information contained in it, including without limitation all text, data, graphs, charts (collectively, the

ÒInformationÓ) is the property of MSCI Inc. or its subsidiaries (collectively, ÒMSCIÓ), or MSCIÕs licensors, direct or indirect suppliers or any

third party involved in making or compiling any Information (collectively, with MSCI, the ÒInformation ProvidersÓ) and is provided for

informational purposes only.Ê The Information may not be modified, reverse-engineered, reproduced or redisseminated in whole or in

part without prior written permission from MSCI.

The Information may not be used to create derivative works or to verify or correct other data or information.ÊÊ For example (but without

limitation), the Information may not be used to create indexes, databases, risk models, analytics, software, or in connection with the

issuing, offering, sponsoring, managing or marketing of any securities, portfolios, financial products or other investment vehicles utilizing

or based on, linked to, tracking or otherwise derived from the Information or any other MSCI data, information, products or services.Ê

The user of the Information assumes the entire risk of any use it may make or permit to be made of the Information.Ê NONE OF THE

INFORMATION PROVIDERS MAKES ANY EXPRESS OR IMPLIED WARRANTIES OR REPRESENTATIONS WITH RESPECT TO

THE INFORMATION (OR THE RESULTS TO BE OBTAINED BY THE USE THEREOF), AND TO THE MAXIMUM EXTENT PERMITTED

BY APPLICABLE LAW, EACH INFORMATION PROVIDER EXPRESSLY DISCLAIMS ALL IMPLIED WARRANTIES (INCLUDING,

WITHOUT LIMITATION, ANY IMPLIED WARRANTIES OF ORIGINALITY, ACCURACY, TIMELINESS, NON-INFRINGEMENT,

COMPLETENESS, MERCHANTABILITY AND FITNESS FOR A PARTICULAR PURPOSE) WITH RESPECT TO ANY OF THE

INFORMATION.

Without limiting any of the foregoing and to the maximum extent permitted by applicable law, in no event shall any Information Provider

have any liability regarding any of the Information for any direct, indirect, special, punitive, consequential (including lost profits) or any

other damages even if notified of the possibility of such damages. The foregoing shall not exclude or limit any liability that may not by

applicable law be excluded or limited, including without limitation (as applicable), any liability for death or personal injury to the extent

that such injury results from the negligence or willful default of itself, its servants, agents or sub-contractors.Ê

Information containing any historical information, data or analysis should not be taken as an indication or guarantee of any future

performance, analysis, forecast or prediction.Ê Past performance does not guarantee future results.Ê

The Information should not be relied on and is not a substitute for the skill, judgment and experience of the user, its management,

employees, advisors and/or clients when making investment and other business decisions.Ê All Information is impersonal and not tailored

to the needs of any person, entity or group of persons.

None of the Information constitutes an offer to sell (or a solicitation of an offer to buy), any security, financial product or other investment

vehicle or any trading strategy.

It is not possible to invest directly in an index.Ê Exposure to an asset class or trading strategy or other category represented by an index

is only available through third party investable instruments (if any) based on that index.ÊÊ MSCI does not issue, sponsor, endorse, market,

offer, review or otherwise express any opinion regarding any fund, ETF, derivative or other security, investment, financial product or

trading strategy that is based on, linked to or seeks to provide an investment return related to the performance of any MSCI index

(collectively, ÒIndex Linked InvestmentsÓ). MSCI makes no assurance that any Index Linked Investments will accurately track index

performance or provide positive investment returns.Ê MSCI Inc. is not an investment adviser or fiduciary and MSCI makes no representation

regarding the advisability of investing in any Index Linked Investments.

Index returns do not represent the results of actual trading of investible assets/securities. MSCI maintains and calculates indexes, but

does not manage actual assets. Index returns do not reflect payment of any sales charges or fees an investor may pay to purchase the

securities underlying the index or Index Linked Investments. The imposition of these fees and charges would cause the performance of

an Index Linked Investment to be different than the MSCI index performance.

The Information may contain back tested data.Ê Back-tested performance is not actual performance, but is hypothetical.Ê There are

frequently material differences between back tested performance results and actual results subsequently achieved by any investment

strategy.Ê

Constituents of MSCI equity indexes are listed companies, which are included in or excluded from the indexes according to the application

of the relevant index methodologies. Accordingly, constituents in MSCI equity indexes may include MSCI Inc., clients of MSCI or suppliers

to MSCI.Ê Inclusion of a security within an MSCI index is not a recommendation by MSCI to buy, sell, or hold such security, nor is it

considered to be investment advice.

Data and information produced by various affiliates of MSCI Inc., including MSCI ESG Research Inc. and Barra LLC, may be used in

calculating certain MSCI indexes.Ê More information can be found in the relevant index methodologies on www.msci.com.

MSCI receives compensation in connection with licensing its indexes to third parties.Ê MSCI Inc.Õs revenue includes fees based on assets

in Index Linked Investments. Information can be found in MSCI Inc.Õs company filings on the Investor Relations section of www.msci.com.

MSCI ESG Research Inc. is a Registered Investment Adviser under the Investment Advisers Act of 1940 and a subsidiary of MSCI Inc.Ê

Except with respect to any applicable products or services from MSCI ESG Research, neither MSCI nor any of its products or services

recommends, endorses, approves or otherwise expresses any opinion regarding any issuer, securities, financial products or instruments

or trading strategies and MSCIÕs products or services are not intended to constitute investment advice or a recommendation to make

(or refrain from making) any kind of investment decision and may not be relied on as such. Issuers mentioned or included in any MSCI

ESG Research materials may include MSCI Inc., clients of MSCI or suppliers to MSCI, and may also purchase research or other products

or services from MSCI ESG Research.Ê MSCI ESG Research materials, including materials utilized in any MSCI ESG Indexes or other

products, have not been submitted to, nor received approval from, the United States Securities and Exchange Commission or any other

regulatory body.

Any use of or access to products, services or information of MSCI requires a license from MSCI.Ê MSCI, Barra, RiskMetrics, IPD, FEA,

InvestorForce, and other MSCI brands and product names are the trademarks, service marks, or registered trademarks of MSCI or its

subsidiaries in the United States and other jurisdictions.Ê The Global Industry Classification Standard (GICS) was developed by and is

the exclusive property of MSCI and Standard & PoorÕs.Ê ÒGlobal Industry Classification Standard (GICS)Ó is a service mark of MSCI and

Standard & PoorÕs.

T: (011) 883 0679 F: (011) 883 0684

Email: marketingmanager@sapoa.org.za 13

Web: www.sapoa.org.zaSAPOA - South African Property Owners Association Tel: (011) 883 0679 Fax: (011) 883 0684 Email: marketingmanager@sapoa.org.za Web: www.sapoa.org.za Physical: Paddock View, Hunt's End Office Park, 36 Wierda Road West, Wierda Valley, Sandton Postal: P O Box 78544, Sandton 2146 Report compiled by:

You can also read