BROADBAND KOREA: INTERNET CASE STUDY - March 2003 - International Telecommunication Union

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

International Telecommunication Union

BROADBAND KOREA:

INTERNET CASE STUDY

March 2003

This report was prepared by Tim Kelly, Vanessa Gray and Michael Minges. It is based

on research carried out from 23 to 30 May 2002 as well as articles and reports noted

in the document. The assistance of the Ministry of Information and Communication,

particularly Sang-Hak Lee, was indispensable and highly appreciated. The assistance

of colleagues within ITU is also noted particularly Nathalie Delmas, who formatted the

report and created the cover. Both Jin-Kyu Jeong and Chinyong Chong provided detailed

comments.

The report would not have been possible without the cooperation of the many Korean

organizations who offered their time to the report’s authors. The report is one of a

series examining the Internet in developing nations. Additional information is available

on ITU’s Internet Case Study web page at http://www.itu.int/ITU-D/ict/cs/.

The report may not necessarily reflect the opinions of ITU, its members or the

Government of the Republic of Korea.

The title refers to Korea’s top ranking in broadband Internet penetration.

NOTE: UNLESS STATED OTHERWISE, ALL REFERENCES TO KOREA IN

THE REPORT REFER TO THE REPUBLIC OF KOREA ALSO COMMONLY

KNOWN AS SOUTH KOREA.

© ITU 2003

ii

Contents

1. From rags to riches in ICT .................................................... 1

1.1 The Korea miracle ....................................................................... 1

1.2 What explains Korea’s success? ..................................................... 2

1.3 ICT in the Korean economy ........................................................... 3

2. ICT market .......................................................................... 5

2.1 The end of circuit switching? ......................................................... 5

2.2 Another broadband path to the home ............................................. 9

2.3 Broadening Internet .................................................................. 10

2.4 Mobile Communications .............................................................. 14

3. Sector absorption and ICT applications ............................. 31

3.1 E-government ........................................................................... 31

3.2 Education ................................................................................. 39

3.3 Health ...................................................................................... 45

3.4 Electronic commerce in Korea ..................................................... 46

4. The Information Society in Korea ...................................... 53

4.1 The Vision of a Creative, Knowledge-Based Society ........................ 53

4.2 The Policy Push – creating an information society .......................... 54

4.3 Information society lifestyles ...................................................... 57

5. Conclusion ......................................................................... 63

5.1 State of the Internet .................................................................. 63

5.2 Lies, Damned Lies and Statistics ................................................. 64

5.3 Learning from Korea .................................................................. 65

Annex 1: List of meetings ........................................................ 71

Annex 2: Acronyms and abbreviations .................................... 72

Annex 3: Framework dimensions ............................................ 75

iii

Figures

1.1 Korea catches up … ..................................................................... 1

2.1 Network transition ....................................................................... 8

2.2 More and more bandwidth ............................................................ 8

2.3 Top Internet countries ................................................................ 10

2.4 Internet drivers: Content and Broadband ...................................... 11

2.5 Internet exchanges and international bandwidth ............................ 13

2.6 Korea's domain name structure ................................................... 14

2.7 Catching up and overtaking ........................................................ 15

2.8 Mobile evolution in Korea ........................................................... 16

2.9 How are they related? ................................................................ 17

2.10 Growing the mobile data market ................................................. 20

2.11 Mobile data usage patterns ......................................................... 22

2.12 The top five most popular mobile data services on KTF's 2G

and 1x services ..................................................................... 25

2.13 Ahead of the pack ..................................................................... 27

3.1 Korea's ICT plans ...................................................................... 33

3.2 Korean youth online ................................................................... 39

3.3 A nation of online shoppers ........................................................ 47

3.4 E-commerce usage in Korean companies ...................................... 49

4.1 Korea's IT industry .................................................................... 53

4.2 Korea's broadband users ............................................................ 54

4.3 Information society: lost opportunities and job opportunities .......... 58

4.4 Information Society: hopes and fears ........................................... 59

5.1 State of Internet in the Republic of Korea ..................................... 63

5.2 Recomparing Korea and Switzerland ............................................ 66

Tables

1.1 Socio-demographic indicators ....................................................... 2

1.2 Korea's ICT Sector ....................................................................... 3

2.1 Telephone service competition in Korea .......................................... 5

2.2 Korean mass media indicators ....................................................... 9

2.3 Implementations of mobile data services ...................................... 20

3.1 Korean government ICT budget ................................................... 31

3.2 e-Government initiatives ............................................................ 35

3.3 Ranking e-government ............................................................... 39

3.4 e-education indicators in Korea ................................................... 40

3.5 Summary of Korea's General Plan for Promoting e-Commerce ......... 48

4.1 Korean Government budget for informatization projects ................. 55

5.1 Ranking Korea .......................................................................... 65

5.2 Which factors can be exported? ................................................... 67

ivBoxes

2.1 The Republic of Korea's path to universal service ............................. 6

2.2 One big Intranet? ...................................................................... 11

2.3 Broadband drivers ..................................................................... 12

2.4 1x, 1x EV-DO, IMT-2000: What's the difference? ........................... 19

2.5 Handset wars ............................................................................ 21

3.1 The Korean equilibrium - public and private harmony ..................... 32

3.2 ETRI — Korea's innovation driver ................................................. 37

3.3 From mechanics to web design .................................................... 42

3.4 Dot.school ................................................................................ 44

3.5 Computerizing medical claims ..................................................... 46

3.6 Measuring e-commerce .............................................................. 51

4.1 Critical infrastructure protection .................................................. 56

4.2 The dark side of the information revolution ................................... 60

5.1 And what of the North? .............................................................. 69

v1. From rags to riches in ICT

1. From rags to riches in ICT

1.1 The Korea miracle the world’s fifth largest Internet mar-

ket, with 26 million users. Korea has

The Republic of Korea (Korea) has made the third highest Internet penetration

major strides in Information and in the world and ranks top in Asia

Communication Technology (ICT) over (see Figure 1.1, bottom left).

the last four decades: • Korea leads the world in broadband

• In 1960, Korea had a telephone pen- Internet access penetration. At De-

etration of 0.36 per 100 inhabitants, cember 2002, Korea’s penetration of

barely one tenth of the then world Digital Subscriber Line (DSL) and ca-

average. By 1981, Korea caught up ble modem Internet access was first

with the world average and at the end in the world (see Figure 1.1, bottom

of 2002, its teledensity was 48.8, or right).

almost three times more than the Korea is the leading example of a country

world average (see Figure 1.1, top rising from a low level of ICT access to

left). Today 92 per cent of Korean one of the highest in the world. Is Korea

households have a fixed telephone a miraculous exception or are there

and 79 per cent have a mobile one. lessons to be learned for other

countries? This case study examines the

• In 1995, Korea had less than one factors that have accelerated ICT

Internet user per 100 inhabitants. In development. This chapter looks at the

1999, it surpassed the developed extent to which ICT has permeated

nation average (see Figure 1.1, top Korea in its efforts to transform towards

right) and by the end of 2002 was a knowledge-based society.

Figure 1.1: Korea catches up …

Fixed line telephone subscribers per Internet users per 100 inhabitants

50 100 inhabitants 60 Korea

45

50 Advanced: Western Europe,

40

Korea North America, developed

35 40

30 Asia-Pacific

30 Advanced

25

20

20

15

10 World 10

5

0 0

1960 65 70 75 80 85 90 95 2000 1995 1996 1997 1998 1999 2000 2001 2002

… and starts to take the lead

Top 5 Asian economies by Internet Top 5 economies by broadband

penetration, 2002* penetration, 2002

Korea (Rep.) 55

Korea (Rep.) 21.3

Singapore 52 Hongkong, China 14.6

Japan 45 Canada 11.5

Hongkong, China 43 Iceland 8.6

Taiwan, China 37 Denmark 8.6

Note: *PC-based users.

Source: ITU World Telecommunication Indicators database.

1Korea Internet Case Study

1.2 What explains Korea’s language. Koreans have their own

success? language. Therefore, the country

cannot easily leverage the vast

Korea is not demographically suited amount of content developed in more

to have the highest Internet widely spoken languages. The Korean

penetration in Asia. It is the largest alphabet, known as Han-gul, uses a

of the so-called Four Tigers (the others pictographic font that is not ideally

being Hong Kong, China; Singapore suited to computerization.

and Taiwan, China) both in terms of

land area and population. The Republic On the other hand, Han-gul is phonetic

of Korea’s population stood at with one character representing a

47.7 million in 2001, twice as large sound, making it easy to learn: “Han-

as Taiwan, China, seven times bigger gul is a simple, scientific language.

than Hong Kong, China and more than Learning how to read it is easy, which

11 times larger than Singapore. is probably one of the reasons why

Korea has one of the highest literacy

Korea is also not economically suited rates in the world.”1 This is where the

to have the highest Internet tide starts turning in Korea’s favour.

penetration in Asia. All the other Its literacy rate of 97.6 is the highest

Tigers have a higher per capita income among the Asian Tigers.

than Korea’s US$ 9’400 in 2001 as do

50 other economies. The World Bank Korea also excels in education. Its

classifies Korea as an upper-middle- overall school enrolment rate

income country, one category down (primary, secondary and tertiary) of

from the high-income classification. 90 per cent is the highest among the

Therefore, though Korea is not poor, Asian Tigers. Primary school is

it is not among the world’s wealthiest compulsory (and free) and soon

nations. Hence, Korea’s high level of secondary will be. Korea’s tertiary

Internet penetration is not strongly school enrolment is quite high at

correlated to its income level. 68 per cent. Korea has the highest

level of secondary school graduates

Another factor seemingly weighing among all high-income Asia-Pacific

against Korea’s ICT development is economies.

Table 1.1: Socio-demographic indicators

Selected socio-economic indicators for Asia-Pacific economies

Gross Tertiary

National Population students

Income Land per 100

per capita, area Total Density School inhab- Second

US$, (km2, (000s) Per % enrol- itants -ary+

2001 000s) 2001 km2 Urban Literacy -ment d) c)

Korea (Rep.) 9’400 99 47’676 482 82 97.6 90 5.0 71.8

New Zealand 12’380 268 3’912 15 87 99.0 99 4.6 72.4

Taiwan, China a) 14’188 36 22’406 619 84 95.6 83 3.3 58.2

Australia 19’770 7’682 19’604 3 85 99.0 116 5.4 67.3

Singapore 24’740 0.682 4’131 b) 6'055 100 92.5 75 2.5 55.0

Hong Kong, China 25’920 1.099 6’760 6'151 100 93.3 63 1.6 52.1

Japan 35’990 365 127'370 340 79 99.0 82 3.1 66.2

Note: a) Data for Taiwan, China from Bureau of Statistics. b) Mid-year. c) Per cent of adult population with

at least a secondary education. d) 1995 or latest year available.

Source: National statistics (Population, Secondary+), World Bank (GNI, land area, urban population), UNDP

(literacy, school enrolment), UNESCO (Tertiary students).

21. From rags to riches in ICT

Korea’s high rate of literacy and school the ICT industry in the Korean

enrolment are essential prerequisites economy was 13 per cent in 2000, up

for the widespread adoption of ICTs. from 8.6 per cent in 1997 and the

These factors have helped contribute highest among the Organization of

to the growing impact of ICT in Korean Economic Cooperation and

economy and society. Development (OECD) countries.2

1.3 ICT in the Korean ICT is also adding value to the

economy economy at a rate higher than other

sectors. ICT contributed 50 per cent

Korea’s economic growth is often of the growth in overall GDP in 2000.

described as a miracle. Starting with Apart from the direct benefits to

a per capita income of less than people and companies, ICT has the

US$ 100 in 1960, Korea averaged an indirect benefit of contributing to

annual economic growth rate of eight overall economic wealth and

per cent a year for the next four employment. The ICT sector in Korea

decades. By 2000, per capita income employed 1.3 million people at the end

was US$ 8’910 and Korea’s economy of 2000 and is forecast to grow around

ranked 13th in the world. The focus of fi v e p e r c e n t t h r o u g h 2 0 0 5 ,

growth has been manufacturing and compared to only two per cent for

exports. As Korea’s economy has overall employment.

matured, its manufacturing base has

shifted from textiles, to chemicals, Manufacturing has underpinned

then machinery and later electronics. Ko r e a ’s e c o n o m i c g r o w t h . T h e

Today knowledge and information manufacturing sector has

products and services play an traditionally been dominated by large

important and increasing role in the chaebols that today are known

Korean economy. around the world (e.g., Samsung,

LG, Hyundai, etc.). 3 They produce

Korea divides its ICT sector into three everything from television sets to

segments: Telecommunication semiconductors to mobile phones.

Services, Information Communication W i t h i n t h e Ko r e a n I C T s e c t o r,

Equipment and Software. The ICT equipment forms the biggest market

market accounted for US$ 103 billion segment, accounting for 74 per cent.

in 2001 (see Table 1.2). The share of Exports make up 41 per cent of ICT

Table 1.2: Korea's ICT Sector

Production value of Korea's Information and Communication industry, US$ billion

1997 1998 1999 2000 2001

Information communication services 13 14 16 22 26

Information communication equipment 35 37 54 67 68

Communication equipment 10 9 12 14 13

Information equipment 5 5 8 12 10

Broadcasting equipment 0 1 0 1 1

Electronic components 19 23 33 40 43

Software 3 4 5 9 10

Total 51 54 75 97 103

Rate of increase 37% 6% 40% 29% 7%

Note: Converted to US$ at rate of 31 December 2001.

Source: KISDI.

3Korea Internet Case Study

equipment production. Furthermore, Unlike other nations such as India

ICT products account for a third of that are heavily promoting their

Korea’s total exports. The large offshore software industry, Korea is

equipment industry and its export more focused on hardware. Korea

orientation have a strategic impact on only accounted for 1.3 per cent of

Korea’s ICT sector. It helps explain the global software market in 2000

why Korea has been quick to exploit and runs a large trade deficit in that

new ICT technologies. First, they c a t e g o r y. O n e d i s a d va n t a g e i s

create new domestic markets driving language. Unlike India, which has a

demand for telecommunication strategic advantage by using English

equipment to be produced by local in higher education, Korean is not a

manufacturers. Second, they can give global language. Nonetheless,

Korea a strategic edge in high Ko r e a ’s s o f t w a r e i n d u s t r y a n d

technology exports. Instead of being exports have been growing. Indeed

reliant on other nations, if Korea can software showed the highest rate of

be among the first to develop and use growth among ICT market segments

a new technology, its manufacturers in 2000. Furthermore, there are

will gain experience that can then be certain niche markets, such as online

translated to higher exports. Korean games, where Korea is taking a lead.

companies are already benefiting from The Korean company, NCSoft, is

supplying the domestic broadband already the largest independent

market by winning export orders.4 online gaming company in the world.

Its popular Lineage game has some

One area where Korea does not have two million users in Korea and is sold

an apparent advantage is software. in four other countries.

1

Korean Educational Development Institute. Let’s Learn about Korea. Seoul, 2002.

2

The OECD rankings are based on older data but it is unlikely that Korea’s position would have changed much.

See OECD. Measuring the ICT Sector. http://www.oecd.org/pdf/M00002000/M00002651.pdf.

3

Samsung had the world’s fastest growing brand image in 2001. See “The Best Global Brands.”

BusinessWeek. 5 August 2002. www.businessweek.com/magazine/content/02_31/b3794032.htm.

4

Samsung is the fourth largest ADSL manufacturer in the world. See Samsung. “Samsung is one of the world-

leading ADSL vendors.” Press Release. 9 February 2001.

42. ICT market

2. ICT market

2.1 The end of circuit government fully divested itself of the

switching? company.

Korea’s telecommunication history Korea progressively liberalized its

began in August 1885 when a telecommunication sector during the

telegraph line was installed between 1990s. The first market segment to

Seoul and Inchon. The first be opened was international long

telephones were installed in 1902 distance with the entry of Dacom in

and the first automatic exchange December 1991. Onse Telecom

introduced in 1935. Korea joined the entered the market in October 1997.

International Telecommunication National long distance services were

Union in 1952. By the end of the opened to competition in January

1980s, Korea had achieved a high 1996 when Dacom extended its

level of universal service (see services to this sector of the market

Box 2.1). It signed the World Trade (followed by Onse in December 1999).

Organization (WTO) agreement on Finally, local telephone services were

basic telecommunication services that opened in April 1999 with the entry

became effective in November 1997, of Hanaro. This was notable as it

committing the country to would prove to have a major impact

liberalization of its telecommunication on Korea’s broadband development.

sector. Though KT is still dominant, its market

share has dropped, particularly in

The nation’s historical operator is international long distance (see

Korea Telecom Corporation (KT). It Table 2.1).

began as the government-owned

Korea Telecom Authority in January The Ministry of Information and

1982. Its statute was changed in 1989 Communications (MIC) is

allowing it to be privatized and in responsible for telecommunication

November 1993 the government and broadcasting policy and

began selling its shares in the regulation. This mandate also extends

company. Ten additional share sales to certain areas of information

ensued over the next decade with the technology. The MIC is active in

final one in May 2002 when the promoting and developing the

Table 2.1: Telephone service competition in Korea

Year Korea Telecom

competition market share

Service was introduced 2001

Local (1) 1999 96.9%

Domestic long distance (2) 1996 85.5%

International long distance (2) 1991 67.1%

Note: (1) in terms of subscribers. (2) in terms of revenue.

Source: KT.

5Korea Internet Case Study

Box 2.1: The Republic of Korea's path to universal service

There are around a dozen developing economies technology because of the investment already made

that have graduated to the ranks of the universally in analogue telephone switches in cities. The

served: 90 per cent or greater of households with government also pushed the development of a

a telephone. How did they succeed in achieving locally produced telephone exchange—the TDX—

universal service? The composition of the group to reduce dependency on foreign imports and

tends to reinforce the importance of wealth as well alleviate capacity limitations.

as highlight the advantage that small countries

have. All are high-income economies with GNP per Tariffs were modified to enhance accessibility. The

capita in the range of US$ 11’450 to US$ 23’790. number of local call areas was reduced from about

Hong Kong, China, for example, has a higher 1’600 to about 150 and a national flat-rate usage

GNP per capita than the United Kingdom. Several tariff became a policy goal. Installation charges were

are oil-rich states (Brunei, Kuwait, Qatar, United standardized and used to reduce the gap within

Arab Emirates) and most are relatively small the country by raising urban installation charges

(Bahrain; Cyprus; Hong Kong, China; Macao, China; and lowering rural ones.

Malta, and Singapore).

Money for telecommunication investment was raised

Of these developing countries, the Republic of Korea from several sources. Various laws were established

stands out. It has the largest land area of any to raise funds from bonds. Tariffs were structured

country in the group and has developed its economy to maximize investment funding. Telecommu-

without the benefit of natural resources such as nications was given priority in the Fifth Five-Year

oil. Until the 1960s, telephone services were mainly Socio-Economic Development Program (1982–86),

used for political and military purposes. The rising from less than three per cent of total national

country’s rapid economic growth and consequent investment in the 1970s up to seven per cent in

rise in living standards led to a surge in demand the 1980s.

for telephone service in the 1970s. Waiting lists

grew and the backlog emerged as a social problem. Because of these policies, the country achieved

rapid telecommunication growth through the 1980s.

As a result, upgrading the telecommunication Household telephone penetration increased from

network became a priority and a one-phone, one- 21 per cent in 1980 to 90 per cent by 1990.

family policy was pursued. Korea Telecom was Domestic and international pressure to open the

separated from the Ministry of Communications in telecommunication market began to grow in the

1982 to give it more flexibility to eradicate the 1990s. As in many developed countries, a high level

waiting list. Investment was directed to rural areas of universal service has allowed the Republic of

to minimize disparities with urban regions. Rural Korea to progressively liberalize its

areas were also targeted for the latest digital telecommunication market.

Box Figure 2.1: The way to universal service in the Republic of Korea

Waiting list, percentage of households with telephone and telecom investment,

US$ billion, Republic of Korea

Strong growth… …funded by network investment

Waiting list (000s) (left scale) Telecom investment (US$ b) (left scale)

Households with telephone (%, right scale) As % of GFCF (right scale)

$3.5 8%

500 100

$3.0 7%

400 80 $2.5 6%

5%

300 60 $2.0

4%

$1.5

200 40 3%

$1.0 2%

100 Waiting list 20 $0.5 1%

eliminated

0 0 $- 0%

1982 83 84 85 86 87 88 89 90 91 92 198283 84 85 86 87 88 89 90 91 92

Note: In the right chart, GFCF refers to Gross Fixed Capital Formation.

Source: ITU World Telecommunication Indicators Database.

62. ICT market

communication industry in Korea. One move aggressively into fiber-to-the-

tool it has had at its disposal is home by 2005 (i.e., replace copper

requiring telecommunication lines with fiber) (see Figure 2.2). It

operators to contribute to government forecasts some 5.6 million broadband

programmes for industry subscribers of its own by 2003 (out of

development. Unlike other countries, a nationwide total of 11.9 million).

this money is reinvested in the

telecommunication sector instead of Faced with intense competition from

being transferred to other areas of the new broadband providers, KT

government. abandoned Integrated Services Digital

Networks (ISDN) as its strategy for

Korea’s telecommunication market is data communications over circuit

arguably as open as any in the Asia- switched telephone networks. This

Pa c i f i c r e g i o n . M a r ke t e n t r y i s was a significant move since in other

contingent upon government countries, operators have been

approval and essentially depends on unwilling to rapidly introduce high-

the nature of the service provider. speed Asymmetric Digital Subscriber

Three different classifications exist: Line (ADSL) technologies or price it

(1) Network Service Provider (NSP) competitively for fear of cannibalizing

who build their own facilities and their lucrative ISDN and leased line

which requires a license; (2) Specific offerings. The attraction of ADSL for

Service Provider (SSP), such as KT was that it could leverage its

resellers, who use the facilities of already installed copper lines.

others and which requires Furthermore the economics were

registration; and (3) Value-added compelling. Average Revenue Per User

Service Providers (VSP), such as (ARPU) is seven times higher with

Internet Service Provider (ISP), ADSL than for local and long distance

which requires a simple notification. voice telephone calls. The pay back

period for the ADSL investment is also

Though Korea’s telecom market is fairly quick at a little over a year. At

probably as liberal as any in the Asia- the end of 2001, revenues from

Pacific region, most companies would broadband connection services

have little incentive for entering accounted for eight per cent of total

infrastructure-based segments. First, telecommunication revenues, a higher

the market is already well served with share than long distance.

high penetration levels. Second, Furthermore, local circuit-switched

revenues and profits are declining for telephone services have seen their

traditional circuit-switched voice share of telecommunication revenue

services (see Figure 2.1, left chart). decline from one quarter in 1997 to

Except for KT and one of the mobile 11 per cent by 2001. By 2005,

operators, none of Korea’s facilities- broadband access revenues are

based telecommunication providers forecast to surpass those of local

made a profit in 2001. Third, Korea is telephone service.

inadvertently transitioning to a next-

generation network whose eventual ADSL traffic is separated from circuit-

structure is uncertain. switched traffic and routed over

Internet Protocol (IP) networks. At the

The rapid take-up of broadband has same time, Voice over Internet

radically altered conventional network Protocol (VoIP) is increasingly being

thinking and evolution. By June 2002, used in Korea and bundled into

there were some 10 million broadband offerings by operators. The

subscribers with a broadband Korean VoIP market is expected to

connection. There is now a need to grow around 50 per cent between

offer subscribers increasingly higher 2000 and 2005 while conventional

bandwidth by locating fiber optic cable circuit-switch telephone conversations

closer to the end user. KT plans to offer will show no growth. Thus an

Very high bit rate Digital Subscriber increasing portion of Korea’s

Line (VDSL) services (at up to 26 communication traffic is traversing IP

Mbps) over the next few years and networks and not the circuit- switched

7Korea Internet Case Study

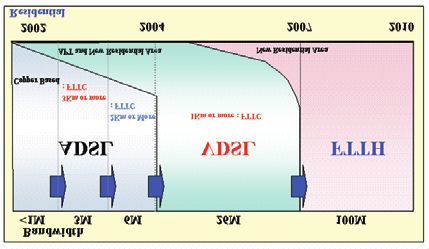

Figure 2.1: Network transition

Distribution of telecommunication market revenue by segment and percentage of telephone lines

connected to digital exchanges and percentage of households with broadband access

Share of revenue Mobile 100%

100% Other 90%

Broadband Internet 80%

80% Leased Circuit

International 70%

60% Long-distance 60% % telephone lines

Local 50% connected to

40% 40% digital

30% exchanges

20% 20% % broadband households

10%

0% 0%

'97 '98 '99 '00 '01 '02 '03 '04 '05 1998 1999 2000 2001 2002 2003 2004 2005

Source: KISDI, ETRI.

network. It is only a matter of time telephone network. Ironically, though

before the packet-switched network Korea has one of the lowest levels of

will replace the conventional local telephone line digitization—only

telephone network. 87.5 per cent in December 2001, one

of the lowest in the world1 —it is at

Broadband Internet access and the same time moving towards a next

growth of IP-related services is having generation communication network.

a great impact on the technical Indeed by the time it would have

evolution of the Korean fixed probably connected all its local

Figure 2.2: More and more bandwidth

Evolution of KT's access network

Source: KT.

82. ICT market

telephone lines to digital exchanges, despite the limited number of

they may not be around any more. terrestrial-based channels and the

lack of satellite television. Only 20 per

2.2 Another broadband path cent of homes subscribed at the end

to the home of 2001. One reason is that relatively

inexpensive alternatives such as

Cable television has been available in videotapes and Digital Video Discs are

Korea since the 1960s. However, these widely available.

so called cable-relay networks simply

provided retransmission of terrestrial The development of cable television

stations in order to improve reception. infrastructure has provided Korea with

True cable television, that is the another method for high speed Internet

provision of additional programming not access. Some 8.3 million Korean

available on terrestrial-based stations, homes—57 per cent of the total—are

started relatively late, in March 1995. passed by cable television.2 Internet

access via cable television was launched

Korea’s cable industry has a by Thrunet in July 1998. At

fragmented structure with exclusive December 2002, there was 3.7 million

licenses awarded on a regional basis. subscribers to broadband cable modem

77 regional system operators provide services. The market leader is Thrunet;

service and deal with customers. The in addition, there are five other cable

electricity company—KEPCO—and KT modem providers. Unlike most other

were charged with building fibre countries, cable ISPs are not system

backbones, which the system operators. They either build out a Hybrid

operators in turn lease to connect their Fibre Coaxial (HFC) cable network or

networks to the source of lease it from system operators. Thrunet

programming. Pay cable television has for example collaborates with 74 of

not proven highly popular in Korea 77 system operators to provide its cable

Table 2.2: Korean mass media indicators

Indicator Value Year Note

Newspaper circulation 40.6% 1996 Population aged 15+ who read

newspaper every day. Source:

National Statistical Office.

Radio sets 47.5 million 1997 Source: UNESCO.

-Per 100 inhabitants 103.9

% of households with a television 94.3% 2000 Colour TV less than 30 inches.

Source: National Statistical

Office.

Households passed by cable television 8.3 million 2001 Source: Thrunet.

-As % of total households 57%

Subscribers to “relay” cable television 7.0 million 2001 Source: Korean Broadcasting

-As % of total households 43% Comission.

Subscribers to “pay” cable television 3.3 million 2001 Source: MIC.

-As % of total households 20%

Cable modem subscribers 3.7 million 2002 Source: MIC.

Source: ITU adapted from sources shown under “Note.”

9Korea Internet Case Study

modem service. It reimburses them a compared to just 0.7 million Internet

portion of the fees it receives from cable users. This anomaly is explained by

modem service. Pricing is competitive with demand for Korean content. Internet

ADSL service. Thrunet charges a monthly content in Korean was lacking so users

fee of Won 38’000 (US$ 28.93), which utilized the services of proprietary

includes unlimited access, an e-mail online services that provided a

account, 50 Mbps of storage and speeds plethora of services in a language they

of up to 10 Mbps. understood. Koreans were wary of

venturing into the Internet world,

2.3 Broadening Internet where most content was in English and

there was a lack of structure to finding

2.3.1 Market information. As the volume of Korean

With 26.3 million users at the end of Internet content expanded—reflected

2002, Korea represents the world’s by a six-fold rise in Korean Internet

fifth largest Internet market hosts between 1996 and 2001—users

(Figure 2.3, left). Its Internet moved over to the Internet

penetration rate, 55.2 per cent at end (Figure 2.4, left). Most online

of 2002, makes it the third highest in providers have now converted to web-

the world (Figure 2.3, right). These based services.

are astounding statistics considering

that five years previously, it had less A second factor driving Internet use

than a million Internet users for a was the growth in broadband access.

penetration rate of 1.6 per cent. When broadband launched, it came

Furthermore, the growth came at a with Internet access. Since the

time of a severe economic downturn. launch of broadband Internet access

What explains this dramatic in July 1998, the number of

turnaround? subscribers has risen to ten million

by the end of 2002. Most services

First, the statistics are a bit that needed broadband access such

misleading. While Korea’s Internet as audio and video streaming,

user population has grown gaming and e-commerce were only

dramatically, it has had a high level of available on the Internet so this

subscribers to non-Internet online created many new Internet users.

services for sometime. For example Today 78 per cent of Internet users

in 1996, it had 1.7 million subscribers log in via a broadband connection

to so-called PC-based services (Figure 2.4, right).

Figure 2.3: Top Internet countries

Top five countries by number of Internet users, 2002 and top five countries by

Internet users per 100 persons, 2002

Top 5 countries by number of Internet Top 5 countries by Internet penetration,

users, 2002, million 2002

USA 155 Iceland 61%

Japan 57 Sweden 57%

China 48 Korea 55%

Germany 35 USA 54%

Korea 26 Netherlands 53%

Source: ITU World Telecommunication Indicators database.

102. ICT market

Figure 2.4: Internet drivers: Content and Broadband

Number of .KR hosts and type of access

Number of .KR hosts Type of Internet Connection, 2002

694

Thousands

548 CATV Dial-up Other

461 10% 2% 2%

Leased

line

18%

203

131

73 xDSL

68%

1996 1997 1998 1999 2000 2001

Source: KRNIC.

Box 2.2: One big Intranet?

Korea is an exception to the argument that limited budding dot-com went public with an offering on

English fluency or non-Latin character alphabets the Korean venture capital stock exchange

are barriers to Internet access. The development (KOSDAQ). The number of its users grew from

of Korean content has been astounding and today 5.7 million at the end of 1999 to 19.6 million at

the nation has one of the highest usage ratios of the end of 2002. Some 90 per cent of all Korean

home grown content. The top 10 web sites accessed Internet users log onto Daum, ranking it first.

by Korean users are all in Korean. The number of Around 450 million pages of Daum’s content is

domains registered using .KR—almost exclusively viewed on an average day. Daum ranks tops in

in the Korean language—ranks the nation fifth in pages per user and session time in the world. Daum

the world.6 Not only has this driven use, but it has is really not much different than other portals except

also reduced the need for expensive international that its business model works. It offers familiar

circuits. It also suggests that in many ways the portal content: e-mail, instant messaging, news,

Internet in Korea is actually one big Intranet with information, shopping, music, videos, etc and

most users preferring to access local sites. makes money from advertising, e-commerce

transactions and members-only portions of its site.

Korea’s top web site is Daum, a start-up company But what allows it to earn money is that it is Korean.

founded in 1995. In 1997, it began operating a Few Koreans surf abroad because of the lack of

web-based email service filling a void created by Korean content and lack of ease with English. So

the slowness of Korea’s proprietary online services Daum has just been better than other Korean

to provide Internet-based content. In 1999, this portals in attracting customers.

2.3.2 Connectivity in this category. The country is criss-

Korea’s local, national and crossed by several nationwide, gigabit

international Internet connectivity is fibre-optic backbones operated by

both qualitatively and quantitatively telecommunication operators,

substantial. Its Internet network today Internet providers and the electric

is very different from its initial company. International connectivity

connectivity to the global network by has been growing rapidly over the last

way of a 56 kbps link to the United several years.

States in 1991. Today, the majority

of Korean users access the Internet Until the mid-1990s, there was no

via broadband and it leads the world national Internet exchange in Korea

11Korea Internet Case Study

Box 2.3: Broadband drivers

43 per cent of the Republic of Korea’s households loop unbundling was not implemented. Hanaro also

had a broadband Internet connection at March faced barriers that discouraged KT customers from

2002, the highest ratio in the world. Korea’s high switching network providers. This included no

broadband penetration can be attributed to the number portability and users having to pay a higher

following factors: connection and subscription charge if they switched

to Hanaro and later reconnected to Korea Telecom.

Geography. 80 per cent of Korea’s population lives One way for Hanaro to break into the market was

in urban areas. Though this figure is not as high as to offer a broadband Internet access service. This

island economies such as Hong Kong, China or exploited KT’s unwillingness to enter the ADSL

Singapore, Korea’s urban geography is dense, market due to its large investment in ISDN. Faced

simplifying broadband access.3 Apartments account with a declining market share, KT entered the ADSL

for 48 per cent of Korea’s housing stock and provide market in June 1999. At October 2001, there were

dwelling for 40 per cent of its population. Another seven companies providing broadband Internet

factor is the proximity of telephone exchanges. The access service. Competition among broadband

average distance of a customer from a telephone technologies has also grown the market through

exchange is 2.2 kilometres, with 95 per cent of greater choice and lower pricing. ADSL is readily

customers within four kilometres, the target range available to the 90 per cent of Korean households

of ADSL. with a fixed telephone line. Some 57 per cent of

Korean homes are passed by cable television,

Competition. Consumer broadband access in Korea providing them with another broadband option

began in July 1998 with the launch of cable modem through cable modem. In addition, there are other

service by Thrunet. The introduction of local loop broadband options such as Local Area Networks

competition with the entry of Hanaro Telecom in (LAN), broadband Wireless Local Loop (WLL) and

April 1999 further fuelled the broadband market. satellite-delivered solutions. As a result of both

With most Koreans already subscribing to market and technological competition, prices are

incumbent Korea Telecom, the market was saturated among the lowest in the world (see right chart

for traditional telephone service. In addition, local below).

SingTel

111

Korea 43% (Singapore)

Telstra

(Australia)

53

Hong Kong,

36% BellSouth

China 50

(USA)

Taiwan, BT (UK) 41

31%

China Monthly ADSL

PCCW (HK,

38 subscription

Ch.)

Singapore 20% Percentage of charge, 2002,

Telecom (N.

households with Zeal.)

34 US$

Japan 16% broadband, 2002 Hanaro (Korea

Rep.)

30

Government support. The government has A growing number of subscribers created economies

facilitated broadband development through an early of scale, which also reduced equipment prices. KT’s

commitment to high-speed infrastructure with specific ADSL equipment purchase cost per line dropped

programs. This has included a positive and supportive from US$ 574 in 1999 to US$ 132 in 2001.5

relationship with the private sector, low interest loans

and a certification program for apartment complexes Mentality. Though more difficult to measure, it is

with high-speed access (for more detail on the widely agreed that Korean “mentality” is also a key

government’s support see Box 3.1). factor. Many Korean Internet users first got a taste

of high-speed access at Internet cafés (so-called

Equipment. Korea’s manufacturing industry has “PC bangs”) and subsequently wanted the same

been an advantage with local suppliers eager to rapidity at home. There is also a “copy-cat”

get into the ADSL market. 4 This has minimized syndrome; once one person gets something

shortages and helped keep equipment prices low. everyone else wants it, too.

122. ICT market

Figure 2.5: Internet exchanges and international bandwidth

Korea's national Internet exchanges and international Internet bandwidth (Mbps)

6’743

Korea's international Internet

bandwidth (Mbps)

2’623

661

3 3 20 116 202

May- 1995 1996 Mar- 1998 1999 2000 2001

95 98

Note: In the right chart, data is for three facilities-based operators.

Source: ITU adapted from KRNIC, NCA.

a n d d o m e s t i c t ra f f i c b e t w e e n Ko r e a h a s a m o n g t h e l o w e s t

different ISPs was routed abroad. broadband Internet prices in the

The National Computerization world. Broadband pricing is flat rate

Agency led the drive to establish a and compared to other countries, the

public exchange, the Korean Internet bandwidth on offer is above average.

Exchange (KIX) in 1995.6 However, Broadband pricing is uniform across

traffic soon exceeded capacity. This providers in Korea. Most packages

led to the Korean Internet Neutral are around US$ 30 per month. The

Exchange (KINX) in June 1999. In variations depend on the amount of

addition, Korea Telecom and Dacom bandwidth. One plan offered by

have established exchanges, KTIX Thrunet proposes users a lower price

a n d D I X r e s p e c t i v e l y. A l l f o u r (US$ 26 per month) in exchange for

exchanges are inter-connected (see receiving e-mail advertisements.

Figure 2.5, left) and most ISPs

connect with each other through the Dial-up Internet prices are not so

exchanges rather than private r e l e va n t c o n s i d e r i n g t h a t m o s t

peering arrangements. subscribers now use broadband. One

important motive for switching to

Korea’s international Internet flat-rate broadband is to avoid the

connectivity has expanded local telephone charge imminent

tremendously and stood at 5.2 Gbps with dial-up subscriptions. A dial-up

at December 2001 (Figure 2.5, right). Internet subscriber must pay local

It has benefited from its proximity to t e l e p h o n e c h a r g e s o f 3 9 Wo n

the sea and hence fibre-optic (3 US cents) per unit (three minutes

submarine cables (it is connected to during peak times and 4.3 minutes

around ten different systems). in off-peak periods). By contrast, an

entry plan ADSL subscription costs

2.3.3 Pricing 30’000 Won (US$ 22.84). After

30 hours of monthly use, it is

The most relevant data to use for cheaper to switch from dial-up to

comparing Korea’s Internet pricing broadband access in Korea. With the

are rates for broadband access (e.g., a v e r a g e Ko r e a n I n t e r n e t u s e r

DSL and cable modem) since the logging on for some 40 hours a

majority of Koreans connect to the month, it is no surprise that so many

Internet in this way. In that regard, have switched to broadband access.7

13Korea Internet Case Study

Leased lines also are being impacted the Internet in Korea.

by consumer broadband technologies.

Former users of ISDN or other low 2.3.5 Regulation

bandwidth leased line services are Korean government involvement in

switching to ADSL and cable modem. the Internet is oriented towards

Only users with very high bandwidth consumer protection and reducing the

requirements (above eight Mbps) are Digital Divide. Entry into the ISP

continuing to lease lines in the market is straightforward. As value-

conventional sense. added service providers, ISPs must

simply notify the government that

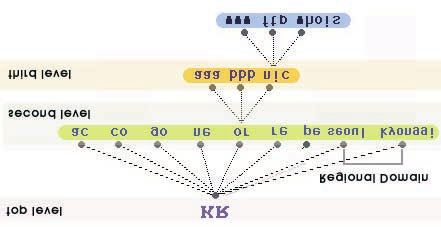

2.3.4 Domain they want to go into business. An ISP

The Korea Network Information must lease facilities from licensed

Center (KRNIC) is responsible for infrastructure providers or obtain their

administering Korea’s .KR domain own facilities-based license.

name. Korea uses second level

domain names based on five common 2.4 Mobile Communications

identifiers depending on the type of

organization. In addition, users can 2.4.1 Mobile market players

select the PE or personnel second level Although Korea’s success in

domain name. There are also broadband networks and services has

16 regional domains used by different stolen the headlines, mobile

regions in Korea (see Figure 2.6). communications development has

Charges are KRW 11’000 (US$ 8.36) proved almost as successful. Korea

per year for personal users and 22’000 was relatively slow to introduce digital

for organizations. A person or services, and when it did so it opted

organization must have an address in for the CDMA standard rather than the

Korea to register a domain name. more widely used GSM. 8

Furthermore, businesses require a Nevertheless, Korea now has one of

certification. the highest levels of mobile

penetration in the world. Korea was

KRNIC’s domain name registration is one of the first countries in the Asia-

just one small part of its activities. It Pacific region where mobile phone

is also involved in research and users overtook fixed-line subscribers,

development, industry promotion as an event that happened in

well as compiling information about October 1999. Subsequently, mobile

Figure 2.6: Korea's domain name structure

Source: KRNIC.

142. ICT market

penetration has continued to grow. tober 2000 (although commer-

Korea overtook Australia, Japan and cial services only arrived a few

New Zealand in terms of mobile months later). During this period,

penetration during the late 1990s and penetration grew rapidly to cross

is today ranked fourth in the region the symbolic 50 lines per 100 in-

(Figure 2.7, left chart). As of the end habitants. Few countries have

of 2002, there were some 32.3 million transformed their mobile com-

mobile subscribers compared with just munication sectors so rapidly.

23.3 million fixed-line users.9 This period saw the introduction

of four new operators all using

The evolution of mobile in Korea has CDMA: Shinsegi Telecom

gone through three distinct phases (800 MHz) and three Personal

(see Figure 2.8): Communication Services (PCS)

operators at 1.8 GHz: Korea

• 1984-1994: between the launch Telecom Freetel (now KTF); LG

of Korea Mobile Telecommunica- Telecom and Hansol (later

tion Service’s (KMTS) analogue M.Com).

cellular service in 1984, as a sub-

sidiary of Korea Telecom, and the • 2001 to date: corresponds with

sale of the company to SK Group somewhat slower growth in the

in 1994. 10 During this period number of mobile voice subscrib-

KMTS, which now trades as SK ers, as the market approaches

Telecom, enjoyed a monopoly in saturation. Instead the focus has

the provision of cellular services. shifted to the development of

By 1995, cellular penetration mobile data applications.

rates had reached only two sub- CDMA2000 1x mobile data serv-

scribers for every 100 inhabit- ices were launched in Octo-

ants, one of the lowest levels ber 2000, CDMA2000 1x EV-DO

among the advanced Asia-Pacific in May 2002 and services in the

economies. IMT-2000 2.1 GHz band (for an

explanation of the different

• 1995-2000: between the launch terms, see Box 2.4) were li-

of CDMA digital voice services censed in December 2000 for

(IS-95A) in January 1996 and the launch in 2003. This period also

launch of CDMA2000 1x, in Oc- has seen a consolidation in the

Figure 2.7: Catching up and overtaking

Cellular mobile penetration in Korea, compared with other Asia-Pacific economies, 2002 and with

Australia, Japan and New Zealand, 1995-2002

Japan 62.1 Cellular 70 Cellular subscribers per

subscribers 100 inhabitants

60

New Zealand 62.2 per 100 1995-2002

Korea

inhabitants 50

Macao, China 63.1

year-end 2002

40

Australia 66.6 Japan Australia

30

Korea (Rep. of) 67.9

20 New Zealand

Singapore 77.9

10

Hongkong, China 91.8

0

Taiwan, China 106.4 1995 1996 1997 1998 1999 2000 2001 2002

Source: ITU World Telecommunication Indicators Database.

15Korea Internet Case Study

Figure 2.8: Mobile evolution in Korea

Cellular subscribers per 100 inhabitants, compared with fixed-line teledensity and

tracked against major landmarks in the development of the sector

Penetration rate of fixed and mobile, Mobile evolution in Korea (cellular density)

per 100 inhabitants 70

70 Jan 2002: SK Telecom

60 merges with Shinsegi

60

50 Jan 1996:

50 Fixed telephone lines May 2001:

40 commercial

40 KTF created

CDMA service

30 thru merger

30 Mobile start

overtakes 20

20 1994: KMTC Dec 2000: IMT-

Mobile cellular fixed in Oct.

10 sold to SK 2000 licences

10 subscribers 98 Group awarded

0 0

1990 1992 1994 1996 1998 2000 2002 1990 1992 1994 1996 1998 2000 2002

Source: ITU World Telecommunication Indicators Database and case study research.

number of operators, with SK services (in 1984, as Korean Mobile

Telecom acquiring Shinsegi and Telecommunication Services) and

KT Freetel acquiring Hansol to also the first to offer digital CDMA

become KTF. services (in 1996, after its

acquisition by the SK Group).

Although the IMT-2000 licenses in the

2.1 GHz band introduces some new SK Telecom is considered by the

investors, it effectively locks in this Ministry of Information and

three-company market structure. Communication (MIC) to be the

There are linkages between the three dominant mobile operator, and for

different operators both at a horizontal this reason its prices are regulated.

level and through vertical integration In January 2002, it completed the

with the activities of different chaebol takeover of Shinsegi Telecom, its

and equipment manufacturers. The leading competitor in the CDMA 800

recent acquisition by SK Telecom of MHz field. In order to satisfy MIC

an 11 per cent stake (the biggest requirements for allowing the

single shareholding) in KT further acquisition, SK Telecom had to

complicates competition policy issues reduce its combined market share to

that are raised by the market below 50 per cent. This they did for

structure. Figure 2.9 attempts to one month (June 2001) by a process

summarise the status as of May 2002 they called demarketing (getting rid

with regard to cross-ownership, but of their least profitable subscribers

the situation remains a dynamic one, and not advertising for new ones).

subject to change. Subsequently, market share has

started to grow again.

2.4.1.1 SK Telecom

SK Telecom < www.sktelecom.com> SK has investments in several Asian

is currently the major player in the economies, including Mongolia

Korean mobile market with a 53 per (SkyTel) and Uzbekistan and most

cent market share, as of December recently they have gained a CDMA

2002 and net income in 2001 of license to operate in Viet Nam

Wo n 1 . 1 b i l l i o n Wo n ( U S $ 8 6 8 ( S Te l e c o m ) a n d i n C a m b o d i a .

million) on a turnover of SK Telecom also has technology

Won 6.2 trillion (US$ 5 billion). SK sharing agreements with China

Telecom was the first company in U n i c o m a n d Pe l e p h o n e ( I s ra e l )

Korea to offer analogue mobile related to CDMA technology.

162. ICT market

SK Telecom was the first in the world Like its rival, SK Telecom, KTF has its

to offer mobile data services over its roots in Korea Telecom, which owns a

standard CDMA network (IS-95). In 40 per cent stake. This came about

October 2000, it launched its through KT FreeTel, which merged

CDMA2000 1x service, under the with M.Com (now KTM.Com) in May

brand name Nate, and in 2001. KTF has a CDMA licence to

January 2002 it commercialized its operate in the 1’800 MHz band.

CDMA2000 1x EV-DO (1x Evolution,

data optimized) service. As of KTF claims that it was the first to

December 2002, it had 14.8 million introduce segmented marketing to the

wireless Internet-enabled handsets in Korean market. Among the different

use and 8.4 million regular Nate users segments it identifies and targets are:

(defined as using the service at least up to age 13 (Kid’s market); 13-

once a month). 18 year-olds (Bigi); 18-25 year-olds

(Na); 25-35 year olds (Main); older

2.4.1.2 KTF age groups (silver market); women

KTF is the second (Drama) and corporate sector (Viz).

largest mobile network operator with Average Revenue Per User (ARPU) is

a 32 per cent market share in highest in the “Main” group, but

December 2002 and a turnover of mobile Internet usage is highest

Won 4.49 trillion (US$ 3.7 billion). among the Na and Bigi groups.

Figure 2.9: How are they related?

Selected links between fixed-line, mobile and IMT-2000 operators in the Korean market, May 2002

Fixed-line

SK Group, a major Other KT (Korea Telecom), LG Group, major telecom operators

chaebol with diverse corporate incumbent fixed-line operator equipment manufacturer and

interests investors with 97% market share in basic chaebol

Retains 26.6%

Owns voice services & 49% in BT, UK

Controlling interest, ownership

7% broadband incumbent

acquired since 1994 Other operator

KT and SKT each own DACOM, corporate

Hanaro, Acquired ownership stake

around 11% of each int’l carrier investors

broadband carrier (now 21.7% ) in 1998

other

Owns

40% stake

SK Telecom KTF LG Telecom

SK Telecom (created in KT Freetel (created in LG Telecom (created in

1994 as KMTS), with 53% 1997), with 33% market 1996), with 14% market

market share and a licence share and a licence to share and a licence to

to operate CDMA services operate CDMA services at operate CDMA services at

at 900 MHz. 1’800 MHz. 1’800 MHz.

Shinsegi Telecom acquired KT M.Com (created as

by SK Telecom in January Hansol DACOM) and

CDMA

2000 merged KT Freetel in May Mobile

2001). operators

SK IMT, awarded a wideband KTI.com, awarded a wideband LG TeleCom , awarded a

CDMA licence in Dec. 2000. CDMA licence in Dec. 2000. CDMA2000 licence in August

Ownership consortium has 783 Ownership consortium has 636 2001. Ownership consortium has

members, led by SK members led by KT and KTF. 1’049 members led by LG Group,

Telecom/Shinsegi and POSCO. and including Hanaro and

DACOM.

IMT-2000

operators

Note: Only selected ownership links are shown and these are subject to change.

Source: ITU Korea case study research.

17Korea Internet Case Study

Like SK Telecom, KTF records wireless companies was later awarded a

Internet users as all those that have CDMA2000 licence in August 2001, for

suitably equipped handsets. This which it paid around US$ 900 million.

amounts to 10.2 million in

December 2002, of which 4.9 million In terms of commercial services, it is

are CDMA2000 1x users. not expected that IMT-2000 services

in the 2.1 GHz band will be available

2.4.1.3 LG Telecom until the second half of 2003. By then,

LG Telecom it is likely that the commercially

is the third mobile operator, with a available alternative CDMA2000 1x

market share of 15 per cent in EV-DO service will have stolen a

December 2002. As its name suggests, march on the market and it may be

it is part of the LG Corporation with LG difficult for W-CDMA to make up the

holding a 36 per cent share and BT of lost ground.

the UK a further 17 per cent (though it

is reportedly looking to sell this stake). 2.4.2 Mobile data

LG missed out on the consolidation that 2.4.2.1 What makes Korea

has taken place in the mobile market different?

since the year 2000; being neither In some ways, Korea is ahead of the

acquired not acquiring. It also missed rest of the world in mobile data. Korea

out on the W-CDMA licences for IMT- probably has a higher penetration of

2000, but has a CDMA-2000 licence in users of high-speed mobile Internet

the 2.1 GHz band. service than any other country in the

world. But, on the other hand, until

LG relies heavily on its sister companies recently Korean mobile operators

for distribution. These include, for generated a lower percentage of their

instance, gas stations and revenue from non-voice services than

supermarkets. It has a 1’800 MHz PCS other operators, for instance in Europe

licence, which it markets under the or Japan (see Figure 2.10). How can

brand name “PCS 019”. As of this apparent contradiction be

December 2002, LG Telecom had explained?

3.5 million wireless Internet users and

1.7 million CDMA2000 1x users. One reason is because of the particular

Korean way of counting mobile data

2.4.1.4 IMT-2000 players users. As no subscription payments

There are three IMT-2000 licensees are required, the number of

in Korea. As shown in Figure 2.9, they subscribers recorded are those that

are each aligned with one of the have suitably-equipped handsets. So,

existing mobile operators and also as most Korean subscribers like to

with fixed-line operators, chaebol and have the most up-to-date terminals,

other investors. Indeed, each IMT the recorded number of mobile data

licensee is really a consortium rather users is high. On the other hand, short

that a single company and the message service, which provides the

consortia have 783 (SK IMT), bulk of non-voice revenue for mobile

636 (Kti.Com) and 1’049 (LG operators in the GSM world, is

Telecom) members respectively. relatively modest in Korea. For

instance, SK Telecom reports that on

The licensing of IMT-2000 proceeded basic second generation (2G) SMS-

in two stages. Consortia led by the enabled handsets, average revenue

two major mobile operators were per user (ARPU) from mobile data is

initially awarded two W-CDMA only 1’756 Won (around US$ 1.40) per

licences, in December 2000, at a cost month. In Europe, SMS generates

of around US$ 1 billion each, through many times this level of revenue.

a hybrid beauty contest/auction. The

unsuccessful bidders in this round But the signs are that the situation is

included LG Telecom (the third mobile changing. Mobile data ARPU from

operator) and Hanaro Telecom (a CDMA2000 1x subscribers is more

broadband network operator). A than twice the level of that from basic

consortium including these two 2G users, and for CDMA2000 1x

18You can also read