Budget 2021 Review - TA ONLINE

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

MARKET STRATEGY

Friday, November 06, 2020

FBMKLCI: 1,519.64

THIS REPORT IS STRICTLY FOR INTERNAL CIRCULATION ONLY*

Budget 2021 Review

Comprehensive Budget to Revitalise the Economy

Kaladher Govindan Tel: +603-2167 9609 kaladher@ta.com.my www.taonline.com.my

Executive Summary

Budget 2021 lived up to our expectations. It contained sufficient measures to revitalize

the economy and alleviate rakyat’s burden, imposed by the negative effects of Covid-19

that trickled down to harm every aspect of daily work and life. We expect this budget to

get the final endorsement when tabled for approval on 23rd November after going

through many rounds of policy debates and ministerial replies as the current economic

reality should sink in and present ample opportunity in finding a common ground among

the members of parliament. As such, reiterate our “ Buy-on-Weakness” view to ride on a

market rally next year underpinned by 1) strong liquidity driven by positive policy

measures globally to reboot the economy, 2) clearer political landscape, both locally and

in the US, after the dust settles on majority support, 3) brighter chances for an effective

Covid-19 vaccines, potentially by end 1Q21, and 4) less combative foreign policy among

key trading nations, especially if Joe Biden wins the US Presidential elections.

Government’s official GDP forecast of 6.5%to 7.5% in 2021 appears realistic with

multi-billion allocations for development expenditure going into high impact projects and

more incentives going into reviving consumption. It is considered within our in-house GDP

projection of 6.4%.

A total gross expenditure of RM322.5bn is budgeted for 2021, including the

RM17bn allocation for Covid-19 fund, which is 2.5% higher than the 2020

allocation. This comprises RM236.5bn or 73.3% of total expenditure for operating

expenditure (+4.3% YoY due to increase in debt service charges, higher payment for supplies

and services, and emoluments). Gross development expenditure increased by 38% YoY to

RM69bn as allocation for all components increased between 36.3% and 40.7% with the

economic sector getting the highest allocation of RM38.9bn, social sector RM18.4b, security

M7.8bn and general administration RM4bn.

Total revenue of RM236.9bn (+4.2% YoY) consists of RM174.4bn in tax revenue

(+13.8% YoY) and RM62.5bn in non-tax revenue (-15.5% YoY). Since the spending

exceeds revenue by RM84.8bn, including the RM800mn from loan recovery and RM17bn

allocated for Covid-19 fund, the fiscal deficit of 5.4% (-6.0% in 2020), which is in-line

with our forecast 5.5%, will be funded by borrowings and assets sale.

We are Neutral on Budget 2021 impact on the equity market. Maintain our end-2020

and 2021 FBMKLCI target of 1,550 and 1,720 based on CY21 and CY22 PER of 15.5x and

17x respectively.

Consumer staple is one of the biggest direct beneficiaries from various budget

measures. Likely beneficiaries are F&N (Buy, TP: RM40.00), AEON (Buy, TP: RM1.25),

Hup Seng (Hold, TP: RM1.00), Johore Tin (Buy, TP: RM2.10), Leong Hup (Buy,

TP: RM0.91), Nestle (Hold, TP: RM143.00) and QL Resources (Hold, TP: RM7.00).

No hike in tax is positive for brewers like Carlsberg (Buy, TP: RM24.50) and Heineken

(Buy, TP: RM26.00). The absence of windfall tax is positive for glove players although the

big four committed to RM400mn in donations. Telcos like Axiata (Buy, TP: RM4.50), Digi

(Buy, TP: RM4.50), Maxis (Hold, TP: RM5.20) and TM (Hold, TP: RM4.35) will

benefit from JENDELA, multibillion allocation for broadband and Jaringan Prihatin

Programme. Measures for the Construction and Property sectors largely within

expectations.

Page 1 of 42

06-Nov20

Budget 2021 – Key Highlights

Budget 2021 themed as “Resilient as One, Together We Triumph” focuses on three integral

goals, i) Rakyat’s Wellbeing, ii) Business Continuity and iii) Economic Resilience. It is the fifth phase

in government’s phased economic recovery plan known as 6R approach, which includes Resolve,

Resilience, Restart, Recovery, Revitalise and Reform. The 12th Malaysia Plan that will be revealed

next January will focus on the last 6R stage, which is Reform.

Key highlights of the budget are,

1) RM17bn allocation to Covid-19 Fund in 2021versus RM38bn in 2020.

2) The tax relief limit on medical expenses for self, spouse and child for serious diseases

increased from RM6,000 to RM8,000 ringgit and tax relief limit for expenses on full

medical check-up from RM500 to RM1,000 ringgit.

3) Bantuan Sara Hidup will be replaced with the Bantuan Prihatin Rakyat with higher rates

of assistance.

4) The Government will allocate RM1.5bn ringgit to implement the Jaringan PRIHATIN

Programme to alleviate the financial burden of the B40 group in accessing internet

services.

5) The first initiative is the income tax reduction for resident individuals which will be

reduced by 1 percentage point for the chargeable income band of RM50,001 to RM70,000

ringgit

6) The minimum employee EPF contribution rate is reduced from 11 to 9 percent beginning

January 2021 for a period of 12 months to increase take-home pay.

7) The facility to withdraw EPF savings from Account 1 on a targeted basis. The amount

allowed will be RM500 a month with a total of up to RM6,000 over 12 months.

8) The formation of a National Employment Council which will be chaired by YAB Prime

Minister.

9) To further encourage old-age savings through Private Retirement Scheme, individual

income tax relief of up to RM3,000 on the PRS contributions will be extended until the

year of assessment 2025.

10) The Government will allocate RM500 to implement the National Digital Network

initiative, JENDELA to ensure the connectivity of 430 schools throughout Malaysia

covering all states.

11) Full stamp duty exemption on instruments of transfer and loan agreement for first time

home buyers is extended until 31 December 2025.

12) Stamp duty exemption on loan agreements and instruments of transfer given to rescuing

contractors and the original house purchasers is extended for another 5 years.

13) The Government will provide training and placements for 8,000 employees of airline

companies in Malaysia with an allocation of RM50m

14) RM15bn will be allocated to fund the Pan Borneo Highway, Gemas-Johor Bahru Electrified

Double-Tracking Electrified Project and Klang Valley Double Tracking Project Phase One.

15) The Government will also continue the High-Speed Rail Project or HSR as this project is

expected to generate a positive multiplier effect to the country's economy. However, it

is subject to further discussion with Singapore.

16) To continue with Rapid Transit Link from Johor Bahru to Woodlands and MRT 3 in the

Klang Valley.

(Please refer economic and sector reports, and budget details in the following pages)

Page 2 of 42

06-Nov20

Budget 2021– Source and Application of Revenue

Figure 1 : Source of Revenue

RMmn Change (%)

Federal Government Revenue

2018 2019 2020e 2021f 2019 2020e 2021f

Tax Revenue 174,061 180,566 153,260 174,370 3.7% -15.1% 13.8%

Direct Tax 130,035 134,723 115,105 131,870 3.6% -14.6% 14.6%

% of Total revenue 55.8% 51.0% 50.6% 55.7%

CITA 66,474 63,751 59,385 64,596 -4.1% -6.8% 8.8%

Individual 32,605 38,680 35,906 42,439 18.6% -7.2% 18.2%

PITA 20,082 20,783 8,551 13,000 3.5% -58.9% 52.0%

Indirect Tax 44,026 45,843 38,155 42,500 4.1% -16.8% 11.4%

% of Total revenue 18.9% 17.3% 16.8% 17.9%

GST/SST 25,680 27,669 24,533 27,900 7.7% -11.3% 13.7%

Excise Duties 10,779 10,511 8,507 8,768 -2.5% -19.1% 3.1%

Import Duty 2,897 2,733 2,035 2,050 -5.7% -25.5% 0.7%

Export Duty 1,725 1,126 802 922 -34.7% -28.8% 15.0%

Non-Tax Revenue 58,821 83,849 74,010 62,530 42.5% -11.7% -15.5%

% of Total revenue 25.3% 31.7% 32.6% 26.4%

Total Revenue 232,882 264,415 227,270 236,900 13.5% -14.0% 4.2%

Nominal GDP 1,446,914 1,510,693 1,439,374 1,568,104 4.4% -4.7% 8.9%

Share of GDP (%) 16.1% 17.5% 15.8% 15.1%

Source: Ministry of Finance, TA Securities

Figure 2: Application of Revenue – Operating Expenditure (OE)

RMmn Change (%)

OE

2018 2019 2020e 2021f 2019 2020e 2021f

Emoluments 79,989 80,534 82,611 84,532 0.7% 2.6% 2.3%

Retirement charges 25,177 25,894 27,055 27,583 2.8% 4.5% 2.0%

Debt service charges 30,547 32,933 34,945 39,000 7.8% 6.1% 11.6%

Grants to state government 7,605 7,574 7,749 7,745 -0.4% 2.3% -0.1%

Supplies and services 35,283 31,507 30,101 32,770 -10.7% -4.5% 8.9%

Subsidies 27,516 23,901 20,145 18,853 -13.1% -15.7% -6.4%

Asset Acquisition 447 770 650 542 72.2% -15.6% -16.6%

Refunds & Write-offs 883 893 987 511 1.1% 10.5% -48.2%

Grant to statutory Bodies 13,763 13,780 14,040 15,430 0.1% 1.9% 9.9%

Other Expenditure 9,750 45,557 8,437 9,574 367.3% -81.5% 13.5%

Covid-19 Fund 38,000 17,000

Total Operating Expenditure 230,960 263,343 226,720 236,540 14.0% -13.9% 4.3%

% of Total Expenditure 80.5% 82.9% 72.0% 73.3%

Figure 3: Application of Revenue – Development Expenditure (DE) and Overall Deficit

Source: Ministry of Finance, TA Securities

Page 3 of 42

06-Nov20

Budget Impact on Stocks and FBMKLCI

Budget 2021 came largely within our expectations. It addressed the three pertinent goals

highlighted earlier and spelled out precise measures and allocations to achieve those objectives. In

ensuring the Rakyat’s wellbeing it covered a variety of subjects that include allocations to fight

Covid-19 pandemic and tax relief for not only for a few types of vaccinations expenses but also

higher tax relief for various existing medical treatment categories that should benefit the

healthcare players under our coverage like IHH (Hold, TP: RM6.00), KPJ (Buy, TP: RM0.95)

and DuoPharma (Sell, TP: RM1.97). Insurance player like Allianz (Buy, TP: RM17.08) will

benefit from green light to purchase life insurance products via EPF Account 2.The RM8.7bn

financial assistance for vulnerable groups, the potential injection of RM9.3bn into system with a 2

percentage points reduction in EPF contribution and RM500 monthly withdrawal over a period of

12 months from EPF Account 1 are positive for Consumer Staples like F&N (Buy, TP:

RM40.00), Nestle (Sell, TP: RM143.00), QL Resources (Hold, TP: RM7.00).

The RM500mn ringgit to implement the National Digital Network Initiative and RM7.4bn allocation

for 2021 and 2022 to build and upgrade broadband services are positive for telcos like Axiata

(Buy, TP: RM4.50), Digi (Buy, TP: RM4.50), Maxis (Hold, TP: RM5.20) and TM (Hold,

TP: RM4.35). The absence of windfall tax is a pleasant surprise for glove players and the

combined RM400mn donations from Top Glove (Buy, TP: RM10.80), Hartalega (Buy, TP:

RM25.97), Supermax (Buy, TP: RM12.33) and Kossan (Buy, TP: RM10.30) to fight Covid-

19 is negligible for these players that raked in huge profits from high demand for gloves.

Construction players should benefit from various urban and rural development projects involving

infrastructure, road maintenance, sports facilities, hospitals, flood mitigation projects, etc.

However, much of it, including new mega projects to be implemented like MRT3 and JB-Singapore

Rapid Transit System are within our expectations. Thus, there is no change in our Underweight

call on the sector. The same applies to measures announced for the Property sector that came

largely within expectations.

(Please read the review by sectors for more details)

Page 4 of 42

06-Nov20

Figure 4: Some Projects Earmarked Under Development Expenditure

No. Section Item description Amount (mn) Sector

1 104 Community Centers as transit centres for children to 20 Community

attend after school

2 105 RM1.3bn to implement rural and inter-village road 2,700 Rural development

projects spanning 920km; RM632mn allocated for rural

and alternative water supply; RM250mn provided for rural

electricity supply; RM55mn for the Home Assistance

Programme to the poor; and 121 million ringgit to install

27 thousand units of lamps as well as to cover operational

and maintenance costs of 500k units of street lights in

villages

3 116 Implementation of the National Digital Network 500 Telecommunication

initiative, JENDELA to ensure the connectivity of 430

schools throughout Malaysia covering all states

4 116 Allocation of RM7.4bn for year 2021 and 2022 by MCMC to 7,400 Telecommunication

build and upgrade broadband services

5 121 Upgrade of buildings and infrastructure in 50 dilapidated 725 Community

schools

6 121 Implementation of 184 construction projects and install 120 Rural development

tube well water for schools in rural Sabah and Sarawak

7 124 Upgrade of the Malaysian Research & Education Network 50 Telecommunication

access line to 500Mbps to 10Gbps

8 132 Provision of comfortable and quality housing, especially 1,200 Housing

for the low-income group

9 142 Construction of 1000 new units of Rumah Keluarga 500 Housing

Angkatan Tentera

10 143 Upgrade of facilities at RELA training centre to strengthen 153 Community

the role of RELA.

11 156 RM100mn for the maintenance of ithe infrastructure of 187 Infrastructure

industrial parks; RM42mn under JENDELA to improve

internet connectivity in 25 industrial parks; Development

of a water treatment plant in Kubang Pasu district; and

allocation of RM45mn to meet the water supply needs in

the Gebeng Industrial Zone.

12 198 Allocation of RM2.5bn for contractors in Class G1 to G4 to 2,500 Infrastructure

carry out small and medium projects across the country

including additional RM200 for maintenance projects for

Federal Roads and 50 million for PPR houses.

13 205 Implementation of transport infrastructure projects to 15,000 Infrastructure

increase the mobility of rakyat. In 2021, RM15bn will be

allocated to fund the Pan Borneo Highway, Gemas-Johor

Bahru Electrified Double-Tracking Electrified Project and

Klang Valley Double Tracking Project Phase One. In

addition, several key projects will also be continued such

as Rapid Transit System Link from Johor Bahru to

Woodlands, Singapore and MRT3 in Klang Valley.

14 206 Continuation of KL-Singapore High Speed Rail, subject to na Infrastructure

further discussion with Singapore

15 207 Construction of the Second Phase of the Klang Third 3,800 Infrastructure

Bridge in Selangor; Continuing the Central Spine Project

with the new alignment from Kelantan to Pahang;

Upgrading the bridge across Sungai Marang, Terengganu;

Upgrading of Federal Road connecting Gerik, Perak to

Kulim, Kedah; To continue building and upgrading Phase

of the Pulau Indah,

Klang Ringroad Phase 3, Selangor; Construction of the Pan

Borneo Highway Sabah from Serusop to Pituru; and

Construction of the Cameron Highlands Bypass road,

Pahang

16 208 Rapid Transit Bus Transport System at 3 High Capacity 780 Infrastructure

Routes and construction of busway at IRDA in Johor;

Construction of the Palekbang Bridge to Kota Bahru,

Kelantan under ECER; Construction of infrastructure and

related components of the Special Development Zone

project in Yan and Baling, Kedah under NCER;

Infrastructure Project in the Samalaju Industrial Area,

Sarawak under SCORE; and Continuation of the Sapangar

Bay Container Port Expansion Project, Sabah under SDC.

17 210 Raw Water Transfer Project from Sungai Kesang and Tasik 150 Infrastructure

Biru to the Jus Reservoir, Jasin , Melaka.

18 212 For 2021, Sabah and Sarawak will receive Development 9,600 Infrastructure

Expenditure allocation of RM5.1bn and RM4.5bn

respectively. These allocation among others are for

building and upgrading water, electricity, and road

infrastructure, health and education facilities

Page 5 of 4206-Nov20

As for the FBMKLCI, it has come under consistent selling pressure since last October due to

worries about the outcome of US elections and rumbling in domestic politics, where some viewed

the impending parliamentary proceedings to table and approve Budget 2021 will be used to display

political support and destabilise the current government. The index dipped from a high of 1532.53

in October to a low of 1,452.13 on 2nd November before rebounding strongly to close at 1,519.64

on Budget day. The rebound was mainly driven by high expectations for Joseph Biden’s victory in

the US presidential election as he is widely seen to be less combative on trade policy and in

relations with the region's growth engine China, and investors hope that may clear the way for

Asia's stronger recovery from the coronavirus crisis.

With the outcome of US elections hanging in balance after President Trump contested the results

in certain states and filed lawsuits, we may see some profit taking pressure ahead as investors

choose to liquidate some of their gains next week. This is not surprising and is perfectly in sync

with the historical trends. Post 1997 Asian Financial Crisis data showed probability for corrections

in the two-week period post-budget is high at 60.9% with an average total return of -1.1% and

greater average losses of 3.0%. From a total average return perspective, the FBM KLCI tends to

underperform during the first two months of post-budget announcement before bouncing back

for a year-end window dressing or New Year rally. This trend should persist as investors wait for

the outcome of US elections and the 23 November voting day to pass the Budget 2021, while

more cases of Covid-19 as winter approaches affect market sentiment in the interim period.

We maintain our end-2020 FBMKLCI target at 1,550 based on CY21 PER of 15.5x and

EPS of 100.1 sen. In comparison, FBMKLCI’s current valuation of 16.1x CY21 PER based on

consensus EPS of 94.59 sen is at 2.3% premium to regional average of 15.7x (vs. Thailand, Jakarta

and Philippines). The premium valuation should dwindle as we progress into later part of 2021 as

the economic and corporate earnings growth gain traction and consensus earnings are revised

upward. With foreign shareholding in Malaysian equities trending below 21% level currently, there

is high probability for them to return in a big way in later part of 2021.

Figure 5 : FBMKLCI's Historical Performance - Pre and Post Budget

FBMKLCI Historical Performance - Pre and Post Budget

Before After

BUDGET

3 Month 2 Month 1 Month 2 Weeks 2 Weeks 1 Month 2 Month 3 Month

-3.7% 0.2% 2.0% 1.7% 2021 (06-Nov-20)

-6.7% -3.6% -2.8% -1.7% 2020 (11-Oct-19) 0.8% 3.4% 0.3% 2.2%

-3.7% -5.5% -4.6% -1.1% 2019 (02-Nov-18) -0.4% -2.0% -1.4% -1.8%

-1.2% -1.3% -0.7% -0.5% 2018 (27-Oct-17) -0.2% -1.7% 0.8% 6.2%

0.8% -1.2% 0.0% 0.3% 2017 (21-Oct-16) -1.3% -2.8% -2.1% -0.3%

-0.6% 11.7% 6.1% 0.3% 2016 (23-Oct-15) -1.5% -2.9% -4.0% -5.0%

-3.9% -2.2% -3.1% -1.7% 2015 (10-Oct-14) 0.6% 0.8% -3.9% -4.2%

1.7% 5.5% 2.4% 2.3% 2014 (25-Oct-13) -0.7% -1.3% 1.0% -0.8%

2.3% 0.7% -0.5% 1.4% 2013 (28-Sep-12) 1.5% 2.2% -2.4% 2.3%

-12.2% -6.5% -4.7% 2.5% 2012 (07-Oct-11) 2.8% 5.5% 5.8% 8.1%

11.5% 8.7% 1.1% 1.6% 2011 (15-Oct-10) 1.1% 0.7% 1.4% 5.4%

9.6% 7.9% 4.0% 2.7% 2010 (23-Oct-09) -0.5% 0.6% -0.5% 2.6%

-13.8% -7.3% -5.1% 0.5% 2009 (29-Aug-08) -5.1% -7.3% -24.4% -21.3%

-3.5% -5.0% -0.2% 2.5% 2008 (07-Sep-07) 0.1% 5.2% 6.5% 10.4%

3.2% 5.0% 2.8% 2.0% 2007 (01-Sep-06) -0.2% 0.7% 2.9% 12.5%

3.7% -1.1% 1.5% 0.6% 2006 (30-Sep-05) -0.2% -2.3% -3.1% -2.9%

3.2% -0.4% 3.5% 3.5% 2005 (10-Sep-04) 0.6% 1.3% 3.1% 5.3%

7.4% 2.4% 2.3% -0.3% 2004 (12-Sep-03) 0.2% 6.7% 7.3% 7.1%

-9.5% -7.4% -8.0% -3.1% 2003 (20-Sep-02) -4.2% -3.0% -5.2% -5.3%

-5.2% -6.0% -2.3% 1.0% 2002 (19-Oct-01) -3.0% 3.3% 8.0% 13.6%

-1.0% -0.7% 9.7% 5.5% 2001 (27-Oct-00) -4.9% -9.8% -14.1% -9.6%

-3.4% -3.2% 10.0% 3.0% 2000 (29-Oct-99) -2.9% 0.4% 7.4% 25.9%

0.3% 32.3% 8.3% 12.8% 1999 (23-Oct-98) 8.0% 10.0% 28.0% 47.4%

-20.6% -9.7% 1.0% -0.3% 1998 (17-Oct-97) -16.4% -16.0% -31.5% -32.1%

41.7% 37.5% 58.3% 70.8% Gain Frequency 39.1% 56.5% 52.2% 56.5%

58.3% 62.5% 41.7% 29.2% Loss Frequency 60.9% 43.5% 47.8% 43.5%

4.4% 8.3% 3.9% 2.6% Average Gain 1.7% 3.1% 6.0% 11.5%

-6.4% -4.1% -3.2% -1.2% Average Loss -3.0% -4.9% -8.4% -8.3%

-1.9% 0.6% 1.0% 1.5% Total Average Return -1.1% -0.4% -0.9% 2.9%

Source: , TA Securities

Page 6 of 4206-Nov20

Figure 6: FBMKLCI Performance, Price Ratio and Earnings Growth Comparison

ROE (%) ROA (%) Price/ Book (X) EPS Growth (%) Div.Yield (%) PER (X)

CY19 CY20 CY21 CY19 CY20 CY21 CY19 CY20 CY21 CY19 CY20 CY21 CY19 CY20 CY21 CY19 CY20 CY21

Malaysia 9.4 8.1 8.4 1.48 1.27 1.34 1.5 1.5 1.4 -5.1 -10.4 10.4 3.6 3.4 3.6 15.9 17.7 16.1

Thailand 9.5 5.0 7.0 2.56 1.22 1.64 1.4 1.4 1.4 -12.7 -41.5 44.7 3.9 2.6 3.1 13.5 23.0 15.9

Indonesia 14.4 11.6 14.3 2.75 2.36 3.01 1.8 1.9 1.7 1.8 -29.6 44.5 2.6 2.3 2.2 13.9 19.8 13.7

Philippines 11.5 6.4 8.9 2.65 2.29 3.09 1.5 1.6 1.5 9.9 -40.4 37.7 1.9 1.7 1.6 14.4 24.1 17.5

Singapore 9.6 6.5 8.3 1.59 1.35 1.75 0.9 0.9 0.9 0.1 -39.3 35.4 5.2 3.8 4.5 10.5 17.4 12.8

Source: TA Securities

Figure 7: Budget Impact by Sector

Sector Impact of Budget Rationale

AUTOMOTIVE Neutral There are no significant measures that would affect Automotive companies under our coverage.

As communicated earlier, targeted financial assistance could help sustain asset quality. Additional guarantees by

government agencies could help spur some lending activities, although the impact will not be significant to the

BANKING Neutral

system’s loan growth. Similarly, we do not foresee the Rent-to-Own Scheme, involving 5,000 PR1MA houses

to move the needle on mortgages.

BUILDING MATERIALS Neutral Demand of building materials will be supported by on-going mega infrastructure projects.

No major surprise with mega infrastructure projects to be rolled out, i.e. MRT3 and JB-Singapore RTS,

CONSTRUCTION Neutral

together with the intention to implement KL-Singapore High Speed Rail are within expectations.

Aids and measures offered towards low-income group and implementation of business-friendly policy would

likely benefit F&B players and retailers with large domestic exposure, resulted from follow-through demands,

CONSUMER Positive

.Separately, BAT is set to benefit from the regulation over vape and the more holistic measures to combat

trade of illicit cigarettes.

GAMING Neutral There are no significant measures that would affect gaming companies under our coverage.

Positive due to no windfall tax. The RM400mn contribution by the big 4 to the Covid-19 fund only accounts for

HEALTHCARE Positive

3.47%-4.3% of 2020 earnings, which is minimal in our view.

Some of the measures such as allowing the EPF members to purchase life insurance products via withdrawal

INSURANCE Positive

from Account 2 will help to drive the sales for life insurers.

MEDIA Neutral There are no significant measures that would affect media companies under our coverage.

OIL & GAS Neutral There are no significant measures that would affect O&G companies under our coverage.

PLANTATIONS Neutral There are no significant measures that would affect Plantation companies under our coverage.

POWER & UTILITIES Neutral There are no significant measures that would affect Power & Uttilities companies under our coverage.

Low-to-middle income earners and first time buyer to benefit from stamp duty exemption and RTO financing.

PROPERTY Neutral

No incentives to private developers as expected.

We expect the allocation of RM7.4bn by MCMC for expanding broadband services to bode well for telcos as it

would enhance the commercial viability of expanding especially into underserved sub-urban and rural areas.

TELECOMMUNICATIONS Positive

Meanwhile, we also expect the government's provision of telecommunication credits worth RM180 to B40

group to help keep telcos ARPU resilient.

While investment and tax incentives for clusters including electronics is positive, for companies under our

TECHNOLOGY Neutral coverage, we do not expect any significant impact on top of the existing benefits that they will continue to

enjoy in the coming years.

TRANSPORTATION Neutral There are no significant measures that would affect transportation companies under our coverage.

Page 7 of 4206-Nov20

Figure 8: Budget Impact on Stocks

Last Price Target Price Upside Budget

Company Call Rationale

(RM) (RM) (%) Impact

Domestic based operations with majority retail revenue derived from food-line items, most

AEON 0.70 1.25 78.6 Buy Positive

likely to benefit from improving disposal income

HUAYANG 0.23 0.27 20.0 Buy Positive Beneficiary of Stamp Duty Exemptions for property priced below RM500k/unit

GLOMAC 0.30 0.36 22.0 Buy Positive Beneficiary of Stamp Duty Exemptions for property priced below RM500k/unit

MMC-GAMUDA JV likely to be appointed as PDP for above ground section and contractor for

GAMUDA 3.69 3.50 (5.1) Sell Positive

underground works. Potential beneficiary of JB-Singapore RTS and KL-Singapore High Speed Rail

Potential beneficiary of MRT3, JB-Singapore RTS, KL-Singapore High Speed Rail and Kwasa

IJM 1.45 1.48 2.1 Sell Positive

Damansara development

Potential beneficiary of MRT3, JB-Singapore RTS, KL-Singapore High Speed Rail and Kwasa

SUNCON 1.82 1.84 1.1 Sell Positive

Damansara development

Potential beneficiary of MRT3, JB-Singapore RTS, KL-Singapore High Speed Rail and Kwasa

WCT 0.395 0.34 (15.2) Sell Positive

Damansara development

GDB 0.69 0.95 37.7 Buy Positive Potential beneficiary of Kwasa Damansara development

GADANG 0.395 0.29 (26.6) Sell Positive Potential beneficiary of MRT3, KL-Singapore High Speed Rail and Kwasa Damansara development

PESONA 0.255 0.235 (7.8) Sell Positive Potential beneficiary of Kwasa Damansara development

INTA 0.30 0.53 76.7 Buy Positive Potential beneficiary of Kwasa Damansara development

Potential beneficiary from some of the budget measures such as allowing the EPF members to

ALLIANZ 13.16 17.08 29.8 Buy Positive

purchase life insurance products via withdrawal from Account 2.

AMWAY 5.10 6.00 17.6 Buy Positive Domestic based operations, most likely to benefit from improving disposal income

PADINI 2.04 2.90 42.2 Buy Positive Domestic based operations, most likely to benefit from improving disposal income

FOCUSP 0.61 0.76 24.6 Buy Positive Domestic based operations, most likely to benefit from improving disposal income

Being a manufacturer of staples products, it is likely to ride on improvement of consumer

HUPSENG 0.92 1.00 8.7 Hold Positive

disposal income.

Being a manufacturer of staples products, it is likely to ride on improvement of consumer

NESTLE 140.10 143.00 2.1 Sell Positive

disposal income.

Beneficiary of regulation over vape and the more holistic measures to combat trade of illicit

BAT 10.22 14.50 41.9 Buy Positive

cigarettes.

Potential beneficiary if selected to play a key role in development owing to its past experience in

TM 4.20 4.35 3.6 Hold Positive

rolling out HSBB and SUBB.

Source: Budget 2020 Speech, TA Securities

[ TH E RE M A ININ G OF T H IS P A GE IS IN TE N TI O NA L L Y L E F T BL AN K]

Page 8 of 4206-Nov20

THIS REPORT IS STRICTLY FOR INTERNAL CIRCULATION ONLY*

Malaysian Economy

Economic Report 2020/2021

shazma@ta.com.my

Shazma Juliana Abu Bakar Tel: +603-2167 9608 www.taonline.com.my

farid@ta.com.my

Summary

On 6 November 2020, Finance Minister Tengku Zafrul Aziz presented the 2021 Budget, a

first for the Perikatan Nasional government since taking over Putrajaya in March this year.

Among the key highlights in the Economic Report 2020/21:

Malaysia’s real GDP is expected to grow between 6.5% and 7.5% in 2021, after a 4.5% contraction

in 2020 due to the Covid-19 pandemic. The strong rebound will be driven by the anticipated

improvement in global growth and international trade. On top of that, the impact of the stimulus

packages implemented by the government is anticipated to have spill-over effects and provide an

additional boost to the economy in 2021.

Gross export earnings are expected to rebound 2.7% in 2021 after a projected 5.2% decline in 2020,

helped by the recovery in global trade and supply chains. For 2021, exports of manufactured goods

are anticipated to grow 2.5%, supported by improved demand for electrical and electronics (E&E)

and non-E&E products.

Malaysia's inflation, as measured by the Consumer Price Index (CPI), is projected to normalise at

2.5% in 2021, after the domestic economy slipped into deflation as a result of the Covid-19 outbreak

in 2020. The inflation forecast in 2021 is in line with better economic prospects and higher crude oil

prices.

2021 Budget would allocate RM322.54bn for all government expenses (or 20.6% of GDP),

RM25.5bn more than 2020’s revised allocation of RM314.72bn. Of this total, RM236.5bn or 73.3%

will be channelled to Operating Expenditure (OE), RM69bn (21.4%) to Development Expenditure

(DE) and RM17bn (5.3%) is for the COVID-19 Fund.

2021 total revenue is envisaged to turn around by 4.2% in 2021 to RM236.9bn versus the lower

than expected revenue of RM227.3bn this year. Tax revenue remains as the main contributor with

expected total collection of RM174.4bn, an increase of 13.8% than 2020. As a percentage to GDP,

tax revenue constitutes 11.1% while non-tax revenue at 4%.

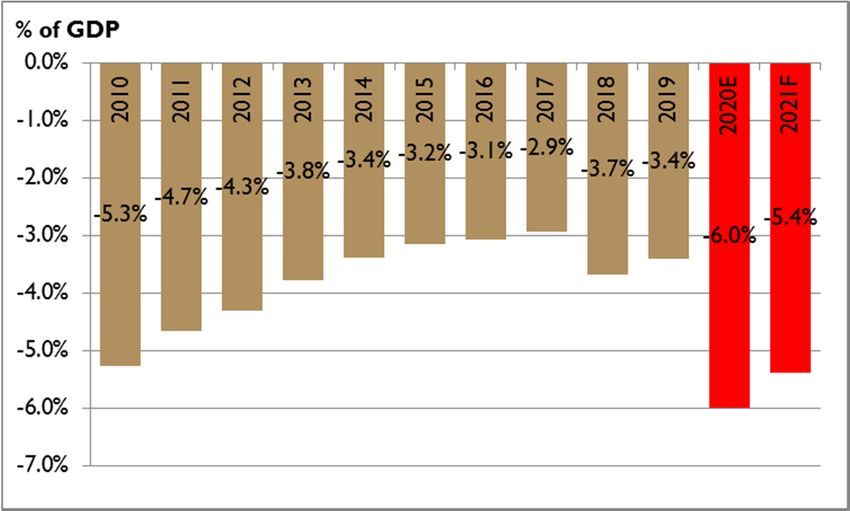

2021 fiscal deficit is expected to be at 5.4% of GDP, almost in line with our expectation of -5.5% of

GDP. We find the target is realistic and achievable especially with the current economic scenario and

volatile oil prices. Under the Medium-Term Fiscal Framework (MTFF), which provides a macro-fiscal

projection over three years, Malaysia’s fiscal deficit is expected to be lower at -4.5% of GDP by 2023.

The government is raising more debt to finance a wider fiscal deficit as it is in the driver seat to steer

the economy out of recession. The national debt is expected to inch up further to hit 61% of GDP in

2021, up from 60.7% in 2020 and 52.5% in 2019.

Figure 1: Key Macroeconomic Projections (2019E vs 2020F)

Ministry of Finance TA Securities

Forecast for 2019 - 2020

2020E 2021F 2020E 2021F

Real GDP Growth (%) -4.5% 6.5% - 7.5% -4.5% -6.4%

Fiscal Balance (% of GDP) -6.0% -5.4% -7.4% -5.5%

Consumer Price Index (%) -1.0% 2.5 -0.9% 3.0%

Source: Economic Report 2019/2020, TA Securities

Page 9 of 4206-Nov20

2021 Growth Outlook - Transitioning from Crisis to Recovery

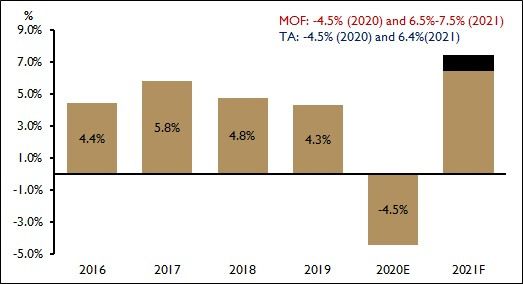

• Taking into consideration of current environment and rising downside risks to growth, the

government predicts that Malaysia’s real GDP to contract by 4.5% in 2020 before

rebounding in a range of 6.5% to 7.5% next year. This is in line with the proactive

measures undertaken by the Government through the economic stimulus packages, the

Budget 2021 initiatives and supported by the recovery of the global economy, which is

forecasted to rebound by 5.2% according to the IMF. Previously the government predicts 2021

GDP to be the range of 5.5% to 8.0%.

• In comparison to other multilateral agencies, the International Monetary Fund (IMF) forecasts

Malaysia’s GDP to bounce back to 7.8% next year while the World Bank expects a growth of

6.9%. The Asian Development Bank (ADB) keeps its forecasts for Malaysia’s GDP growth at

6.5% for next year although it downgraded 2020 GDP growth to -5% from -4% previously. All

projections assumed a mass COVID-19 vaccine deployment probably later next year.

• For now, we do not intend to change our 2021 GDP projections of 6.4%. We would

like to see further economic assessment especially towards the fourth quarter of this year

before making any revision. We will update the key macroeconomic projections in our

upcoming 2021 Annual Strategy report soon.

• The strong rebound in GDP growth will be driven by the anticipated improvement in global

growth and international trade as indicated. On top of that, the impact of the stimulus

packages implemented by the government is anticipated to have spillover effects and provide

an additional boost to the economy in 2021.

• Still, risks remained to the downside as the favourable outlook hinges on two major factors

— the successful containment of Covid-19 and sustained recovery in external demand.

Figure 2: Malaysia’s Real GDP Growth (2016 – 2021F)

Source: Economic Report 2020/2021, TA Securities

Page 10 of 4206-Nov20

Vibrant Private Sector Activity

• The strong outlook is premised on resilient domestic demand, which is forecast to

expand by 6.9% in 2021 after a 3% decline in 2020. This is amid expectation that the key

growth engines, mainly consumer spending, private investment and public investment, all

would be functioning as expected.

• Growth will be steered by sustained private consumption at 7.1% in 2021 versus a 0.7%

decline in 2020. The growth will be primarily driven by higher disposable income stemming

from buoyant economic activities, accommodative financial stance, an extension of tax relief

on childcare and healthcare and favourable stock market conditions. Better job prospects on

an improving economy will also improve household spending, as well as recovery in tourism-

related sectors that will contribute to better private consumption next year. The

unemployment rate is projected to decrease to 3.5% in 2021, compared with an estimated

4.2% in 2020.

Further supporting growth are various measures by the government to uplift disposable

income, as per Budget 2021 speech, which include:

- Allowing a monthly withdrawal of RM500 from Account 1 of the Employees’ Provident

Fund (EPF) to assist those who have lost their jobs due to the Covid-19 pandemic. The

withdrawal is up to RM6,000 for a period of 12 months, aimed at alleviating financial

hardship faced amongst its 600,000 members.

- EPF contribution for employees reduced from 11% to 9% for 12 months beginning

January 2021.

- Tax relief increased to RM8,000 for parents' medical, special needs and care expenses.

- To be renamed Bantuan Prihatin Rakyat, with RM6bn allocated to benefit 8.1mn people.

Households with monthly income below RM2,500 with one child will receive RM1,200,

while households with two children will receive RM1,800. Households with monthly

income between RM2,501 – RM4,000 will with one child will receive RM800, while

households with two children will receive RM1,200. Single adults with monthly salary

below RM2,500 will receive RM350. The age limit for single individuals is also reduced to

21 years old from the previous 40 years old.

- Special RM600 for civil servants Grade 56 and below. Meanwhile, for retired civil servants

and veterans with no pension, the government will provide RM300 special aid.

- Increase of allowance from RM6 to RM8 an hour for 1,900 volunteer firefighters.

- 1% decrease in income tax for those earning between RM50,001 to RM70,000 per year.

• Private investment is expected to rise by 6.7% in 2021 after an 11.7% contraction in 2020.

The government mentioned that there would be more private investment next year as

government-led initiatives such as tax incentives to attract foreign direct investment (FDI) and

the establishment of the Project Acceleration and Coordination Unit (PACU) will help to

drive private investments, on top of spill-over effects from fiscal injections.

• Meanwhile, public investment is likely to rebound by 16.9% in 2021 after contracting by

9.3% in 2020. The continuation of mega projects, such as Mass Rapid Transit 2 (MRT2), and

the Pan Borneo Highway will provide the impetus for public investment. Public corporations

are also expected to continue investing in new and on-going projects, among others,

development of O&G related projects, upgrading of digitalisation-related activities and

construction of energy plants.

• On top of that, the government will be spending more in 2021. A 2% rise in public

consumption is expected from an expected 1.6% increase in 2020.

Page 11 of 4206-Nov20

Figure 3: Malaysia’s Real GDP Growth Performance by Demand Side (2018 – 2020F)

Actual TA MOF

Demand Side (% YoY)

2019 2020E 2021F 2020E 2021F

Private Expenditure 7.60% -4.50% 6.30% -0.70% 7.10%

Public Expenditure 2.00% 3.00% 2.40% 1.60% 2.00%

Gross fixed capital formation -2.10% -7.60% 9.90% -11.10% 9.50%

Private Investment -10.90% -12.70% 5.50% -11.70% 6.70%

Public Investment 1.60% -5.70% 11.40% -9.30% 16.90%

Net Exports 9.70% -17.30% 0.10% -24.90% 4.10%

Exports -1.30% -6.80% 5.50% -13.40% 8.70%

Imports -2.50% -5.50% 6.10% -11.90% 9.20%

GDP 4.30% -4.50% 6.40% -4.50% 6.5% - 7.5%

Source: Economic Report 2019/2020, TA Securities

Broad-based Growth

• On the supply side, growth is expected to be broad-based next year will all

economic sectors recording a positive growth after a contraction in 2020. This year,

the construction sector is expected to contract the most at 18.7%, followed by the mining

industry at 7.8%. Meanwhile, the services, manufacturing and agriculture sectors are

anticipated to contract by 3.7%, 3% and 1.2% respectively,

The outlook is expected to be better in 2021 with the construction sector is expected to

grow the most at 13.9% on account of the acceleration and revival of major infrastructure

projects, coupled with affordable housing projects. The civil engineering segment will also spur

the recovery.

This is followed by the services and manufacturing industries’ expansion of 7% each.

Breakdown showed all sub-sectors within the industry are projected to grow in 2021 as

economic activities normalise led by wholesale & retail trade backed by food-related

industries. As for the manufacturing sectors, growth next year will be driven by steady

improvement in both the export and domestic-oriented industries. The E&E segment is

projected to accelerate in line with the digital transformation as WFH (work-from-home) and

virtual communications become part of new business practices. Further, higher demand for

integrated circuits, memory and microchips within the global semiconductor market will

further support the E&E segment

Meanwhile, the agriculture is expected to grow by 4.7% next year, supported mainly by

higher production of palm oil and rubber. And, the mining sector to seen growing by 4.1%

in 2021 supported by the recovery in global demand for crude oil and condensate as well as

LNG.

Figure 4: Malaysia’s Real GDP Growth Performance by Supply Side (2018 – 2020F)

Actual TA MOF

Supply Side (% YoY)

2019 2020E 2021F 2020E 2020E

Agriculture 2.00% -1.90% 1.40% -1.20% 4.70%

Mining -2.00% -6.70% 1.30% -7.80% 4.10%

Manufacturing 3.80% -1.90% 10.70% -3.00% 7.00%

Construction 0.10% -14.20% 1.50% -18.70% 13.90%

Services 6.10% -4.60% 6.30% -3.70% 7.00%

GDP 4.30% -4.50% 6.40% -4.50% 6.5% - 7.5%

Source: Department of Statistics, Economic Report 2019/2020, TA Securities

Page 12 of 4206-Nov20

2020 Deficit to Hit 6.0%

• The revenue performance for 2020 to be negatively affected, as widely expected, amid slower

economic activities and lower crude oil price assumption due to the COVID-19 pandemic. As

such, total revenue is revised lower to RM227.3bn or 15.8% of GDP as compared to the

budget estimate of RM244.5bn.

• In contrast, total expenditure is expected to increase by 6% or RM17.7bn to RM314.7bn. This

is due to the fiscal stimulus injection of RM38bn off-set by savings of RM20.3bn from the

revision of existing programmes and projects as well as the shortfall in spending from budget

estimates. The OE for 2020 is now estimated at RM226.7bn from original allocation of

RM241bn while the DE is seen at RM50bn (initial allocation: RM56bn).

• With lesser revenue projection amid higher expenditure including the RM38bn COVID-19

Fund, 2020 fiscal balance is projected to increase to RM86.5bn as compared to earlier forecast

of RM52.5bn. With that, this year’s fiscal deficit as percentage of GDP is higher at -

6.0% of GDP (2019: -3.4% of GDP). Statistics showed federal government position had

already registered a deficit of RM52.7bn as of 1H20, much higher than RM22.4bn deficit

recorded in the same period last year. That is equivalent to -7.9% of GDP. In 2Q20 alone,

total deficit was -8.1% of GDP.

Figure 5: Federal Government Financial Position (2018 – 2020F)

Economic Report 2020/2021

Financial Position RMbn Change (%)

2019 2020E 2021F 2019 2020E 2021F

Revenue 264.42 227.27 236.90 13.5% -14.0% 4.2%

Operating Expenditure 263.34 226.72 236.54 14.0% -13.9% 4.3%

Current Deficit/ Surplus 1.07 0.55 0.36 -44.2% -48.7% -34.5%

Gross Development Expenditure 54.17 50.00 69.00 -3.4% -7.7% 38.0%

Less: Loan Recoveries 1.60 1.00 0.80 103.4% -37.6% -20.0%

Net Development Expenditure 52.57 49.00 68.20 -4.9% -6.8% 39.2%

Covid-19 Fund 38.00 17.00 -55.3%

Overall Surplus/ Deficit -51.50 -86.45 -84.84 -3.5% 67.9% -1.9%

% Share of GDP -3.4% -6.0% -5.4%

Source: Economic Report 2020/2021, TA Securities

A More Targeted Fiscal Support for 2021 and Years Ahead

• The government would continue to focus on the recovery measures to revitalise the economy

at the same time remained committed to maintain a path of fiscal consolidation. As the Budget

2021 marks the beginning of the 12th Malaysia Plan (12MP), allocations will be channelled

towards more targeted programmes and projects with high multiplier impact to ensure value

for money.

• 2021 fiscal deficit is expected to be at 5.4% of GDP, almost in line with our

expectation of -5.5% of GDP. We find the target is realistic and achievable especially with

the current economic scenario and volatile oil prices.

• Under the Medium-Term Fiscal Framework (MTFF), which provides a macro-fiscal projection

over three years, Malaysia’s fiscal deficit is expected to be lower at -4.5% of GDP by

2023. That is based on assumption that: 1) real GDP growth of 4.5% to 5.0% (nominal GDP:

5.5% to 6.5%); 2) crude oil price forecast of between USD45 to USD55 per barrel; and 3)

crude oil production of 580,000 barrels per day.

• In the medium-term period (2021-2023), total revenue is expected to reach RM731bn or

RM14.7% of GDP, contributed mainly from non-petroleum revenue, which is forecast at

RM609.7bn (12.3% of GDP). Meanwhile, petroleum-related revenue is estimated at

Page 13 of 4206-Nov20

RM121.3bn or 2.4% of GDP. Within these 3 years, the government will enhance its revenue

by exploring new sources, widening the revenue base, improving tax administration and

adopting the Medium-Term Revenue Strategy (MTRS).

• The total indicative ceiling for the three-year expenditure, including COVID-19 Fund

allocation, is estimated at RM959.8bn or 19.3% of GDP. OE allocation is projected at

RM730.3bn while DE at RM212.5bn.

Figure 6: Malaysia’s Fiscal Balance (2010 – 2021F)

Source: Economic Report 2020/202, TA Securities

Figure 7: Medium Term Key Macroeconomic Projections

2021-2023

RMbn Share of GDP (%)

Revenue 731.0 14.7

Petroleum 609.7 12.3

Non-petroleum 121.3 2.4

Operating Expenditure 730.3 14.7

Current Balance 0.7 0.0

Gross Development Expenditure 212.5 4.3

Less: Loan Recoveries 2.0 0.1

Net Development Expenditure 210.5 4.2

Covid-19 Fund 17.0 0.3

Overall Balance -226.8 -4.5

Primary Balance -102.8 -2.1

Underlying assumptions

Real GDP Growth (%) 4.5-5.5

Nominal GDP Growth (%) 5.5-6.5

Crude Oil Price (USD per Barrel) 45-55

Oil Production (Barrels per day) 580,000

Source: Economic Report 2020/202, TA Securities

Page 14 of 4206-Nov20

Enhancing Revenue Sources

• As the nation to shift from the recovery phase towards achieving its growth potential in the

new normal, 2021 total revenue is envisaged to turn around by 4.2% in 2021 to

RM236.9bn versus the lower than expected earnings of RM227.3bn this year. Initially, our

total revenue was expected to be at RM244.5bn for 2020 before COVID-19 pandemic hit the

economy. Current revenue allocation is roughly equivalent to 15.1% of GDP. It is within of

expectation (close to our 2021 revenue forecast of RM238.4bn) on the back of improving

economic growth and business prospects.

• Tax revenue remains as the main contributor with expected total collection of

RM174.4bn, an increase of 13.8% than 2020. As a percentage to GDP, tax revenue constitutes

11.1% while non-tax revenue at 4%.

• In terms of growth, expect a higher direct tax collection by 14.6% to RM131.9.1bn,

constituting 55.7% to total revenue (2020E: RM115.1bn) with assumption of better collection

from individual and companies’ income tax.

- Companies income tax, or CITA, is expected to contribute the most by RM64.6bn or

8.8% increase than before. This is in tandem with improving economic activities and higher

earning expectations, coupled with continuous efforts by the Inland Revenue Board (IRB)

to enhance auditing and tax compliance.

- Similarly, Petroleum Income Tax, or PITA, is anticipated to rebound by 52% on account

of improved demand and slightly higher average crude oil assumption of USD42 per barrel

(2020E: USD40 per barrel).

- Also, expect higher individual income tax of RM42.4bn attributed to stable employment

prospect and sustained wage growth. This is despite lower income tax rate by 1%- point

for those earning taxable wages from RM50,001 to RM70,000 which only expected to

benefit 1.4mn taxpayers. According to the IRB, the tax rate for this income category for

Year Assessment 2020 is 14%. This would make the rate to be 13% for Year Assessment

2021. (See Figure 10)

- Revenue from other direct tax consists of stamp duty, RPGT and other taxes is

provisioned at RM8.8bn or 7% increase than 2020.

• Meanwhile, indirect tax collection is also expected to be higher by 11.4% to RM42.5bn

(2020E: RM38.2bn) mainly contributed by higher SST collection of RM27.9bn in line with

improving consumer spending, Likewise, excise duties are estimated to expand by 3.1% to

RM8.8bn in tandem with higher demand for motor vehicles (2021F: +17%) following the

introduction of new models and ongoing promotional campaigns in the industry. Meanwhile,

export duty is expected to remain stable at RM0.9bn.

• We also noted lesser non-tax revenue by 15.5% to RM62.5bn next year (2020E: RM74bn),

primarily due to lower proceeds from investment income. Dividends from PETRONAS and

Khazanah are estimated at RM18bn and RM1bn, respectively. In addition, the government will

continue to receive a special payment from KWAP amounting RM5bn to partly finance the

retirement charges. Petroleum royalty is forecast to reach RM4.3bn in consonance with higher

crude oil price.

• A more diversified revenue has resulted non-oil revenue contribution to be more much

higher, to 84% for next year versus less than 78% in 2020 and 68.3% in 2018. This will help to

limit volatility and strengthen the sustainability of its fiscal position over the medium term. It

is estimated that for every USD1 per barrel increase in crude oil price, the government’s

revenue will go up by about RM300mn (vice versa). Petroleum-related revenue is forecast to

be lower at RM37.8bn or 2.4% of GDP, compared with RM50bn of 3.5% in 2020.

Consequently, non-petroleum revenue is envisaged to increase by 12,3% to RM199.1bn.

Page 15 of 4206-Nov20

Figure 8: Federal Government Revenue (2019 – 2021F)

Economic Report 2020/2021

Revenue RMbn Change (%) Share (%)

2019 2020E 2021F 2019 2020E 2021F 2019 2020E 2021F

Tax Revenue 180.6 153.3 174.4 3.7% -15.1% 13.8% 12.0% 10.6% 11.1%

Direct Tax 134.7 115.1 131.9 3.6% -14.6% 14.6% 8.9% 8.0% 8.4%

CITA 63.8 59.4 64.6 -4.1% -6.8% 8.8% 4.2% 4.1% 4.1%

Individual 38.7 35.9 42.4 18.6% -7.2% 18.2% 2.6% 2.5% 2.7%

PITA 20.8 8.6 13.0 3.5% -58.9% 52.0% 1.4% 0.6% 0.8%

Indirect Tax 45.8 38.2 42.5 4.1% -16.8% 11.4% 3.0% 2.6% 2.7%

GST/SST 27.7 24.5 27.9 7.7% -11.3% 13.7% 1.8% 1.7% 1.8%

Excise Duties 10.5 8.5 8.8 -2.5% -19.1% 3.1% 0.7% 0.6% 0.6%

Import Duty 2.7 2.0 2.1 -5.7% -25.5% 0.7% 0.2% 0.1% 0.1%

Export Duty 1.1 0.8 0.9 -34.7% -28.8% 15.0% 0.1% 0.1% 0.1%

Non-Tax Revenue 83.8 74.0 62.5 42.5% -11.7% -15.5% 5.6% 5.1% 4.0%

Total Revenue 264.4 227.3 236.9 13.5% -14.0% 4.2% 17.5% 15.8% 15.1%

Nominal GDP 1,510.8 1,440.8 1,571.1 4.4% -4.6% 9.0% 100.0% 100.0% 100.0%

Source: Economic Report 2020/2021, TA Securities

Figure 9: % Petroleum-Related and Non-Petroleum Revenue (2009 – 2021F)

%

100.0

20.4 17.6 16.0 Petroleum

80.0 41.3 35.4

60.0 43.1 46.8 50.2

32.2 37.8 Non-

40.0

Petroleum

14.8 20.4 22.0

20.0 19.0 19.2 10.4

11.3 10.8 11.8

0.0 7.5 7.6 4.4

2009 2010 2019 2020 2021

Petronas Special Dividend SST Others

Direct Tax (Exc. PITA) Petroleum Revenue

Source: Economic Report 2020/2021, TA Securities

Figure 10: Chargeable Income Band for YA 2021

Chargeable Income New Tax Rate (%)

0-5,5000 0

5,001-20,000 1

20,001-35,000 3

35,001-50,000 8

50,001-70,000 13

70,001-100,000 21

100,001-250,000 24

250,001-400,000 24.5

400,001-600,000 25

600,001-1,000,000 26

1,000,001-2,000,000 28

Exceeding 2,000,000 30

Source: IRB, 2021 Budget Speech, TA Securities

Page 16 of 4206-Nov20

Higher Expenditure to Revitalise Growth and Restore Confidence

• 2021 Budget would allocate RM322.54bn for all government expenses (or 20.6% of

GDP), RM25.5bn more than 2020’s revised allocation of RM314.7bn (TA forecast: RM324bn).

We noted a new category of allocation was created in 2020 and 2021, namely the COVID-19

Consolidated Fund, intended for dealing with the pandemic. Under this provision, the

government has allocated RM38bn for 2020 and RM17bn for 2021 along with expectation of

better pandemic situation and vaccine development. To recap, the COVID-19 Fund was

established with a validity period of three years ending 31 December 2022. Excluding the

COVID-19 Fund, total expenditure would be at RM305.5bn.

• Of this total, RM236.5bn or 73.3% will be channelled to Operating Expenditure

(OE), RM69bn (21.4%) to Development Expenditure (DE) and RM17bn (5.3%) is

for the COVID-19 Fund. Malaysia's OE is normally bigger than DE and that under our

Constitution, the government cannot finance OE using borrowings. The government can

borrow only for DE.

• By sectoral excluding the COVID-19 Fund, 37.7% is allocated for programmes and projects

under the social sector, followed by the economic (18.3%), security (11%) and general

administration (7.7%) sectors. By Ministries, the top three recipients constituting 38.5% of

total expenditure or RM117.5bn are the Ministry of Education (MOE), Ministry of Finance and

Ministry of Health (MOH).

• The allocation for 2021 OE is equivalent to 15.1% of GDP, slightly higher by 4,3% from

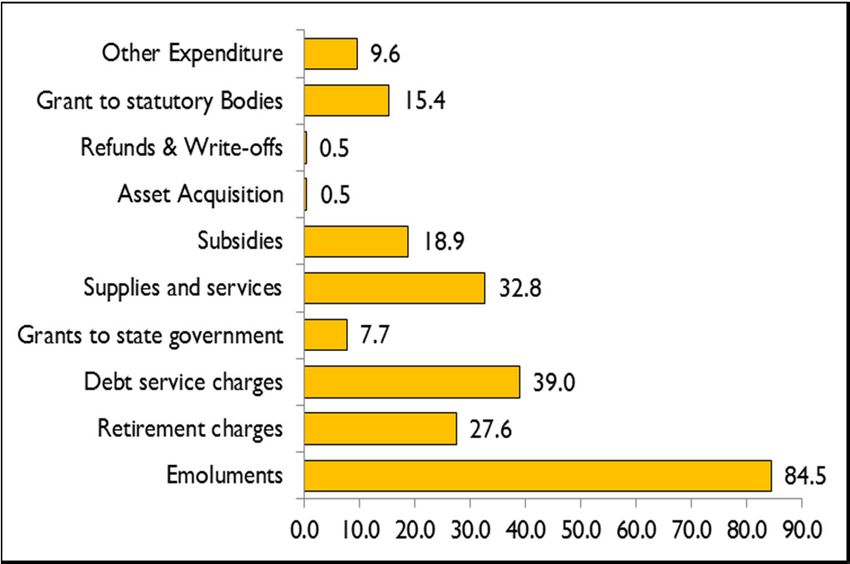

the revised budget of RM226.7bn in 2020. About 70% of total OE is provided for emoluments

and charged expenditures, which includes debt service charges, retirement charges as well as

grants and transfers to state government under the Federal Constitution. As usual,

emoluments alone are estimated to contribute the biggest, about 35.7% of total OE, with an

allocation of RM84.5bn for next year versus RM82.6bn this year.

• The provision for subsidies and social assistance next year is seen lesser by 6.4%

to RM18.9bn versus this year’s revised allocation of RM20.1bn. The decline is mainly due to

consolidation of cash assistance programmes under BSH and BPN. During the tabling of

Budget 2021, the Bantuan Sara Hidup (BSH) assistance programme will be replaced with the

Bantuan Prihatin Rakyat (BPR) programme. Under the new BPR programme, aid to B40 and

M40 groups will be increased and allocated according to the household income as well as

number of children in each household.

Figure 11: Operating Expenditure vs. Development Expenditure (2005 – 2021F)

RMbn

350.0 DE OE

300.0

250.0

200.0

150.0

100.0

50.0

0.0

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020E

2021F

Source: Economic Report 2020/2021, TA Securities

Page 17 of 4206-Nov20

Figure 12: % Share of Total Expenditure Figure 13: Malaysia Total Expenditure – RMbn

(2021F) (2021F)

Source: Economic Report 2020/2021, TA Securities

Figure 14: Federal Government Operating Expenditure (2019 – 2021F)

Economic Report 2020/2021

Operating Expenditure RMbn Change (%) Share (%)

2019 2020E 2021F 2019 2020E 2021F 2019 2020E 2021F

Emoluments 80.5 82.6 84.5 0.7% 2.6% 2.3% 30.6% 36.4% 35.7%

Retirement charges 25.9 27.1 27.6 2.8% 4.5% 2.0% 9.8% 11.9% 11.7%

Debt service charges 32.9 34.9 39.0 7.8% 6.1% 11.6% 12.5% 15.4% 16.5%

Grants to state government 7.6 7.7 7.7 -0.4% 2.3% -0.1% 2.9% 3.4% 3.3%

Supplies and services 31.5 30.1 32.8 -10.7% -4.5% 8.9% 12.0% 13.3% 13.9%

Subsidies 23.9 20.1 18.9 -13.1% -15.7% -6.4% 9.1% 8.9% 8.0%

Asset Acquisition 0.8 0.7 0.5 72.2% -15.6% -16.6% 0.3% 0.3% 0.2%

Refunds & Write-offs 0.9 1.0 0.5 1.1% 10.5% -48.2% 0.3% 0.4% 0.2%

Grant to statutory Bodies 13.8 14.0 15.4 0.1% 1.9% 9.9% 5.2% 6.2% 6.5%

Other Expenditure 45.6 8.4 9.6 367.3% -81.5% 13.5% 17.3% 3.7% 4.0%

Total Operating Expenditure 263.3 226.7 236.5 14.0% -13.9% 4.3% 100.0% 100.0% 100.0%

Source: Economic Report 2020/2021, TA Securities

Higher Development Expenditure to Spur Growth

• The allocation of Development Expenditure (DE) is seen higher next year at

RM69bn, along with the government’s pledge to churn economic activities by roiling out

mega projects. Indeed, the government pledged to channel the DE to programmes and

projects with high multiplier impact to promote economic growth and support the livelihood

of the rakyat.

• The DE allocation is the highest so far in history and also beat our estimates of RM60bn. We

also noted that 2020’s DE allocation has been reduced to RM50bn as compared to initial

allocation of RM56bn announced during Budget 2020 last year. This is due to the deferment

and slower progress of several projects during the Movement Control Order (MCO) period.

• Of the total DE, RM67.3bn is in the form of direct allocation, while RM1.7bn is for loans to

state governments and government-linked entities. By sector, the Economic Sector received

the highest allocation of RM38.9bn under the DE encompassing transport, trade, industry,

energy and public utilities and agriculture. The Social Sector would receive RM18.4bn,

followed by the Security Sector, RM7.8bn and General Administration, RM3.9bn.

• The health subsector remains a priority which will receive an allocation of RM4.7bn or 6.8%

of total DE. The focus of spending under this subsector will be to expand the health sector

and provide an effective national healthcare system, according to the report. More new

Page 18 of 4206-Nov20

hospitals and clinics will be built, it said, especially in small districts to ensure an affordable,

equitable and accessible healthcare system. In addition, outlays will also be provided for the

upgrading and maintenance of hospitals and clinics as well as procurement of medical service

vehicles and equipment. Major ongoing projects under this subsector include the construction

of Serdang Hospital Cardiology Centre, Putrajaya Hospital Endocrine Complex and Lawas

Hospital, in addition to the upgrading of Kajang hospital and Tawau hospital.

Figure 15: Federal Government Development Expenditure by Sector (2019 – 2021F)

Economic Report 2020/2021

Development Expenditure RMbn Change (%) Share (%)

2019 2020E 2021F 2019 2020E 2021F 2019 2020E 2021F

Economic Sector 31.3 28.5 38.9 -13.3% -8.9% 36.3% 57.8% 57.1% 56.4%

Transport 13.8 10.2 15.0 -19.1% -25.9% 47.5% 25.4% 20.4% 21.8%

Trade & Industry 3.1 2.4 3.1 21.6% -20.2% 28.0% 5.6% 4.9% 4.5%

Public Utilities & Energy 2.8 3.6 3.3 22.4% 29.9% -7.1% 5.1% 7.2% 4.8%

Agriculture & Rural Development 2.3 3.0 2.9 8.5% 30.3% -4.0% 4.3% 6.0% 4.2%

Social Sector 14.5 13.1 18.4 12.5% -9.8% 40.7% 26.7% 26.1% 26.6%

Education & Training 7.6 5.9 8.9 17.3% -23.0% 51.1% 14.1% 11.7% 12.9%

Health 1.8 2.9 4.7 3.0% 57.8% 63.9% 3.4% 5.8% 6.8%

Housing 2.1 1.5 1.8 65.4% -29.9% 23.0% 3.9% 3.0% 2.7%

Security 5.6 5.6 7.8 13.9% -1.0% 40.0% 10.4% 11.1% 11.3%

Defence 2.9 2.7 4.9 -10.1% -9.1% 82.4% 5.4% 5.3% 7.0%

Internal Security 2.7 2.9 2.9 60.9% 7.8% 1.0% 5.0% 5.8% 4.2%

General Administration 2.8 2.9 4.0 26.7% 3.1% 38.6% 5.1% 5.7% 5.7%

Gross Development Expenditure 54.2 50.0 69.0 -3.4% -7.7% 38.0% 100.0% 100.0% 100.0%

Source: Economic Report 2020/2021, TA Securities

Federal Government Debt to Increase to 61% of GDP in 2021

• The federal government is raising more debt to finance a wider fiscal deficit as it is in the

driver seat to steer the economy out of recession. The national debt is expected to

inch up further to hit 61% of GDP in 2021, up from 60.7% in 2020 and 52.5% in 2019.

In Budget 2020, the federal government debt was initially estimated to hover around 53% of

GDP, with the targeted fiscal deficit at 3.2% of GDP. Despite the growing debt figures, the

government noted that most of the measures taken to stimulate growth are short-term in

nature and do not fundamentally change the principles of debt management.

• The national debt had already expanded to RM874.3bn or 60.7% of GDP as at end-

September 2020 — from RM793bn or 52.5% of GDP in 2019. Domestic debt, mainly

Malaysian Government Securities (MGS) and Malaysian Government Investment Issues

(MGIIs), made up 96.7% of the country’s borrowings, according to the Ministry of Finance’s

(MoF) Fiscal Policy Review 2021.

• Moving forward, the government is committed to continuing the debt consolidation path in

the medium term once the economy recovers from the current crisis. The government also

pledged to strike a balance between addressing development needs and consolidating the

debt-to-GDP level once the crisis subsides.

Page 19 of 4206-Nov20

THIS REPORT IS STRICTLY FOR INTERNAL CIRCULATION ONLY*

Construction Sector Neutral

A Reasonable Allocation for Infrastructure Development

Ooi Beng Hooi Tel: +603-2167 9612 benghooi@ta.com.my www.taonline.com.my

Largely Within Expectation

The proposed allocation of RM69bn for development expenditure in Budget 2021 was significantly

higher (+23.21%) compared to RM56bn previously tabled for Budget 2020. In this Budget, the

coverage on the construction sector was much within ours and market expectations. Key

construction-related items mentioned in Budget 2021 include:

1) RM15bn will be allocated to fund the ongoing Pan Borneo Highway, Gemas-JB Electrified

Double Tracking Project and Klang Valley Double Tracking Project Phase 1;

2) Implementation of JB-Singapore Rapid Transit System and MRT3 in the Klang Valley;

3) Continuation of KL-Singapore High Speed Rail, subject to further discussion with Singapore;

4) Allocation of RM3.8bn for:

a) 2nd Phase of the Klang Third Bridge in Selangor;

b) Continuation of Central Spine Project with the new alignment from Kelantan to Pahang;

c) Upgrading of Sungai Marang Bridge, Terengganu;

d) Upgrading of Federal Road linking Gerik, Perak and Kulim, Kedah;

e) Construction and upgrading of Phase 3 of Pulau Indah Ring Road, Klang, Selangor;

f) Construction of Pan Borneo Sabah for package from Serusop to Pituru; and

g) Construction of Cameron Highlands Bypass.

5) Allocation of RM780mn for infrastructure development at 5 economic corridors:

a) 3 Bus Rapid Transit lines in development area of Iskandar Regional Development

Authority;

b) Construction of Palekbang bridge to Kota Bahru, Kelantan under East Coast Economic

Region;

c) Construction of infrastructure and related components at the Special Development

Zone at Yan and Baling, Kedah, under Northern Corridor Economic Region;

d) Infrastructure project in Samalaju Industrial Area under Sarawak Corridor of Renewable

Energy; and

e) Continuation of Sepangar Bay Container Port Expansion Project in Sabah under Sabah

Development Corridor.

6) Allocation of RM150mn for raw water transfer from Sungai Kesang and Tasik Biru to Jus Dam,

Melaka;

7) Continuation of Kwasa Damansara development with an estimated GDV of RM50bn;

As usual, there was a budget of RM2.7bn allocated for infrastructure development at rural areas.

This includes:

a) RM1.3bn to implement rural and inter-village road projects spanning 920km;

b) RM632mn for rural and alternative water supply;

c) RM250mn for rural electricity supply:

d) RM355mn for House Assistance Programme which builds and repairs houses for the poor;

e) RM121mn to install 27k units of lamps as well as to cover the operational and maintenance

costs for 500k units of street lights in village.

Separately, there was a development expenditure allocation of RM5.1bn and RM4.5bn for Sabah

and Sarawak respectively, to build and upgrade water, electricity, roads, healthcare and education

facilities.

Page 20 of 42You can also read