Corporate Presentation - November 2018 - Eros International

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Corporate Presentation November 2018

1 Eros the leading Indian film studio

Executive Summary

Eros: A global leader in Indian film entertainment with #1 box office market share

1 130+ new releases in the last 3 fiscal years

2 Large content library of Indian language films, 2,000+, and music

3 Multi-platform model for content monetization

4 ErosNow(1) strategically positioned to capture large digital opportunity in India

5 Highly attractive market opportunity driven by secular tailwinds

6 Culture of innovation and partnerships with leading international talent

Note: (1) ErosNow is Eros International Plc’s, OTT entertainment service

PAGE 2

Unrivalled Library & Film

Production Capability

New film •Hindi

mix 40-50 Co-production Acquisition Own IP Creation •Regional language

Films Each •ErosNow Originals,

Year Short films

2,000+ film library

(1 year after Theatrical Release)

PAGE 3

Eros: A Multi-channel monetization

Model

Leading player in a growing and underpenetrated film market

Theatrical Investing in content driven films with high ROI potential

Film pre-sales facilitated by long-standing Eros brand, reputation and industry relationships

Cable digitisation and rising Pay TV penetration drive market growth and demand for premium content

Eros’ film library of over 2,000+ films is a stable source of revenue growth with high margins

Television & Others Television rights are often sold before box-office releases

Other streams through theatrical and catalogue rights include Music, Cable and broadband syndication, in-flight sales,

DVD sales, etc.

Exclusive content supplier to the fast growing OTT platform - ErosNow

Digital ErosNow, with 13m paying subscribers and over 128m registered users globally, is the leading Indian Film SVOD Platform

Expanding aggressively into digital content with ErosNow originals and short films

Sale of international distribution and digital rights to the parent company benefits de-risking and cash flows

Overseas Pre-determined recovery of significant film production cost through Eros International Plc

Parent Company enjoys wide international distribution network across 50 countries

Eros International is strategically positioned to monetise film content through multiple channels globally

$$$ $ AD $

Theatrical TV Syndication Freemium Pay Per View Subscription Advertising Bundled Services

PAGE 4

Deep and Longstanding Talent

Relationships

Select Leading Actors

Amitabh Shah Rukh Salman Ranveer Deepika Priyanka Anushka

Bachchan Khan Khan Singh Padukone Chopra Sharma

3 IIFA Awards 5 IIFA Awards 1 IIFA Award 3 IIFA Awards 4 IIFA Awards 3 IIFA Awards 3 IIFA Awards

4 NFA Awards 2 NFA Awards 1 NFA Award 1 NFA Award

Select Leading Directors

Sanjay Leela Anand Kabir Raj & DK Anurag Sujay

Bhansali L. Rai Khan Kashyap Dahake

4 IIFA Awards 1 BIG Award 1 IIFA Award 2 IIFA Awards 1 NFA Award

2 NFA Awards 1 Stardust Award 1 NFA Award

Note: IIFA = International Indian Film Academy. NFA = National Film Awards.

PAGE 5

Industry defining partnership

with Reliance Industries

⚫ Eros International Media and Reliance

Industries Ltd (“RIL”),India’s largest private A Mutually Beneficial Strategic Partnership with India’s

sector company, announced the creation of Largest Conglomerate to Consolidate Indian Content

a joint film fund to co-produce and

consolidate Indian content Content Distribution Capital Engagement

o The new partnership will look to

invest Rs 1,000 crore ($150mn) in Investment to dramatically scale Eros’ capabilities in content

the near-term to produce and production, marketing, and distribution

acquire Indian films and digital

originals across all languages Symbiotic relationship with Reliance’s Jio to create high efficient

unit economics for the ErosNow OTT platform

⚫ RIL, as per an agreement in February

2018, has acquired 5% equity stake in our Reliance’s production expertise to further bolster expansion and

parent company, Eros International PLC at development of Eros’ original and short form content

a price of $ 15 per share (18% premium to

the then close price)

PAGE 6

Successful Penetration into China,

expansion into new Geographies

Indo-Chinese Co-Production Bajrangi Bhaijaan in China Indo-Turkish Co-Productions

2 films created and produce by

in-house, will be co-produced

with a Chinese Studio

• First for an Indian studio

• Set in India and China

• Shot in both languages

Eros’ Influential Partnership in China

Partnerships with three major Chinese state-owned film and

entertainment companies to promote, co-produce and distribute

Indo-Russian Joint Content Distribution

Sino-Indian films across all platforms in India and China

Central Partnership and Eros Int’l to distribute and promote Indian

and Russian content across multiple platforms in both countries

PAGE 7

2 Our markets

India: Fast Growing Film and

Television Market

Indian Film and Television Market Projected to Grow at 9%

(Rs. In Billions)

’16 – ’20E CAGR

9%

1,054

900 192 7%

816

166

156

9%

862

734

660

2017A 2018E 2020E

TV Filmed Entertainment

(1) Source: FICCI – EY Report.

PAGE 9India: Leading Economic and

Population Growth

Fast growing economy Massive Population

Projected GDP Growth CAGR (2017A-2021E) (2017, in billions)

~18% of world

13.1% population

1.3

3.3%

0.3

India US India US

Highly favorable demographics Increasing annual consumer expenditure

Median age (Rs. billion)

39.3 37.1

31.6 101,146

27.6 83,858 90,016

74,967 80,266

71,324

Russia China Brazil India 2012 2013 2014 2015 2016 2017

Over the next 15 years India is expected to be the largest contributor of global GDP growth

World Bank, IMF, OECD, CIA World Factbook, Euromonitor International, United Nations, Wall Street Research

1. Number of Eros Now subscriptions purchasable in India for each Netflix subscription purchasable in the India. Services’ costs based on Rs.500 Netflix Standard monthly subscription plan for India and Rs. 50

Eros Now monthly subscription plan for India, respectively

PAGE 10Rapid Growth for India’s Film

Industry

More Movies Made, and More Tickets Sold in India Than

India - a highly underpenetrated market

Any Other Country

2,500 (2016A1) Theatre screens per million population

125

Number of Movies

2,000

India

Produced

1,500

1,000 60

Japan USA 40

China

500 France

UK 10 16

South Korea 8

0

0 500 1,000 1,500 2,000 2,500

India Brazil China South UK US

Annual Tickets Sold (mm) Korea

Multiplex rollout fueling growth …and substantial room to increase pricing

Number of Multiplexes in India (Rs.)

Average Admissions Price

1,028

2,750

2,100 635

458 517

1,500 393

1,225 308

925 190

India China Brazil Russia US UK Japan

2009 2011 2013 2015 2017

Eros Plc data, UNESCO Institute for statistics, Film Federation of India, Wall street research - Size of circles scaled to represent Number of Movies Produced x Annual Tickets Sold, FICCI-E&Y

2018 Report, India ticket price represents average ticket price at two leading multiplex chains as on 2017.

PAGE 11Growing Indian Television Market

Increasing television household penetration…(1) …is Expected to Fuel Growth in the Indian TV Industry (1)

(Rs in billion)

Paid C&S TV Household Penetration (%)

862

84%

81%

594 494

351

243 368

Total # of 2016A 2021P 2016A 2020E

TV 175m 200m Advertising Revenue Subscription Revenue

Households:

Willingness to pay for content…(1) ...is Supported by Favorable Viewing Preferences(1)

(in millions)

Paid C&S TV Household Percentage of viewing time spent

45%

42%

36% 70+%

22%

164

12% 11%

147 7% 7%

2016A 2021P Hindi GEC + Regional GEC + Kids + Music News

Movies Movies

2014 2015

1) Source: FICCI Report 2017, 2018

PAGE 12India: Compelling Digital Trends,

Underpinned by Mobile

In December 2017 India Reached 1.2 Billion Mobile Phone Subscribers, with Only 25% Smartphone Penetration

A Young, Technologically Savvy Demographic Strong Mobile Internet User Growth

27% Internet Median Age 87% Internet Millions2

Penetration1 Penetration1

37.9 829

481

27.6

2017A 2021E

Video Dominates Mobile Internet Usage in India A Handful of Telcos Control the Market

Mobile Internet Usage in India (2017E) Wired & Wireless Broadband Market Share (Jun-2018A)

File Sharing

95% Wireless Subscribers

Streaming Audio 2% 48%

10%

21%

14% 10%

Video 5%

49%

→ 75% by 2021E

Web and Other

Data Jio Airtel Vodafone Idea BSNL

39%

Source: FICCI Report, CIA World Factbook, Telecom Regulatory Authority of India, Ericsson Mobility Report, Statista. Note: Vodafone India and Idea Cellular merger pending.

1. 2016A.

2. Includes non-smartphone mobile internet users.

PAGE 13The Big Regional Opportunity

Language No. of films Top Grossing Worldwide Box Typical Typical

released in Film Office INR & Production Print &

2017 USD Budgets Advertising

Hindi 120 Dangal 1,870 cr ($291m) $ 12 -15m $3.0m

Tamil 198 Enthiran 283 cr ($44.2m) $ 10 -12m $0.7m

Telugu 156 Baahubali 2 1,560 cr ($238m) $ 8 – 10m $0.5m

Kannada 183 Aptharakshasa 55 cr ($8.6m) $ 4 – 5m $0.2m

Malayalam 132 Drishyam 75 cr ($11.7m) $ 1.5 – 2.5m $0.2m

Marathi 98 Sairat 110 cr ($16.7m) $ 1 – 2m $0.2m

Bengali 36 Chander Pahar 15 cr ($2.3m) $ 0.5 – 1m $0.1m

Punjabi 40 Chaar Sahebzaade 70 cr ($11m) $ 1.5 – 2.5m $0.2m

Over 1,000 films are released in The box office numbers suggest these are Varying Budgets. Low P&A. High

India each year across languages not niche films. Contributions are significant Margins and Presales

In the context of shortage of theatres, the Regional strategy adds scale, market share and margins without cannibalization

Source: BookMyShow, KoiMoi, Market reports

PAGE 143 A digital opportunity

ErosNow(1) : #1 SVOD Platform for

Indian Content

11,000+

Films Rights

5,000+

Into Perpetuity

100+

Originals over next 18 months

Rapidly Growing Paid Subscriber Base…

Eros now Paying Subscribers2 16.0+

(mm) 13.0

10.1

7.9

5.0

2.9 3.7

2.1

FY'17A Q1' FY'18A Q2' FY'18A Q3' FY'18A FY'18A Q1' FY'19A Q2' FY'19A FY'19E

(Mgmt Guidance)

Eros International produces/acquires content for ErosNow (1)

Note: (1) ErosNow is Eros International Plc’s, OTT entertainment service(2) Paying subscribers means any subscriber who has made a valid payment to subscribe to a service that includes

the Eros Now service either as part of a bundle or on a standalone basis, either directly or indirectly through a telecom operator or OEM in any given month be it through a daily, weekly or

monthly billing pack, as long as the validity of the pack is for at least one month

PAGE 16ErosNow(1) : World’s Leading Indian

Digital Entertainment Platform

✓135

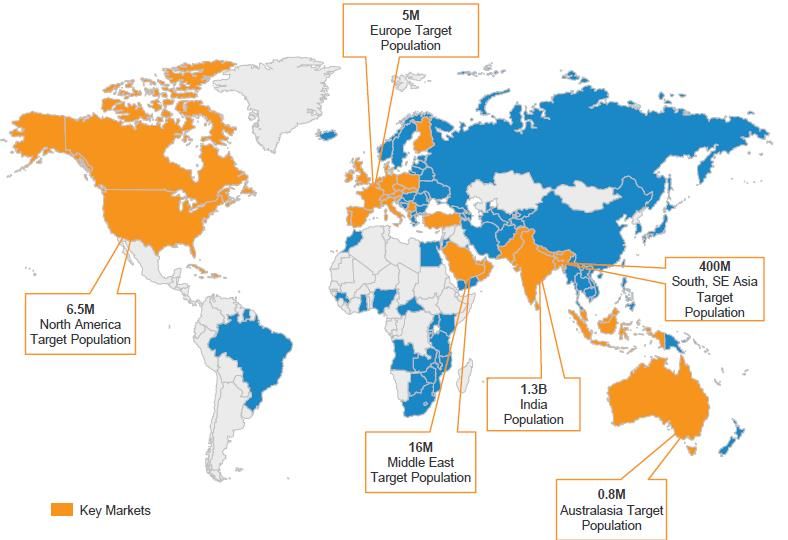

Our Addressable Market is a Quarter of the World Population

Countries inc. India

✓128M

Registered Users

✓13M

Paying Subscribers

✓11,000+

Digital Rights

Note: (1) ErosNow is Eros International Plc’s, OTT entertainment service

PAGE 17ErosNow(1) - Unique distribution

model

Major Indian Telco Partnership Director to Consumer and Other

OEM Streaming

215mm 223mm 345mm 221mm

Subs Subs Subs Subs

(Partner

Channel)

Parent Company Market Capatilization1 $80bn $75bn $26bn $5bn Other

EROS Now Exclusive SVOD Partner

WALLETS

Long-Standing Partnership

TELCO / ISP

➢ Major Indian Telco Partnerships Underpin Sustainability

of ErosNow’s Moat

➢ Exclusive Partnerships for ErosNow, and Access to the

Largest and Most Linguistically Diverse Digital Indian

Film Library for Telcos

International

Note: (1) ErosNow is Eros International Plc’s, OTT entertainment service

PAGE 18Strong pipeline of ErosNow(1)

originals under Production/release

December 2018 / March 2019 March 2019 March 2019

January 2019

April 2019 May 2019 June 2019 June 2019 TBD

Note: (1) ErosNow is Eros International Plc’s, OTT entertainment service

PAGE 193 Forthcoming Content

Select Forthcoming Releases

Tentative

Film Name Star Cast/(Director/Producer) Language

Release

Amar Akbar Anthony Ravi Teja, Ileana D’Cruz and others (Mythri Movie Makers) Telugu FY2019

Ottakkoru Kamukan Jojo, Shine Tom Chacko and others (Dazzling Movie Land) Malayalam FY2019

Kaptan Saif Ali Khan, Zoya and others (Navdeep Singh / ColourYellow Productions) Hindi FY2019

Mumbai Pune Mumbai 3 Swapnil Joshi, Mukta Barve Marathi FY2019

Cobra Gautam Ghulati, Tarun Khanna, Nyra Banerjee, Ruhi Singh, Director - Munesh Rawal Hindi FY2019

Kaamiyab Drishyam Films Hindi FY2019

Ticket to Bollywood Amyra Dastoor, Diganth Manchale / (Eros) Hindi FY2019

Haathi Mere Saathi Rana Dugabatti (Prabhu Soloman) Hindi / Tamil / Telugu FY2020

Guru Tegh Bahadur (Harry Baweja) Punjabi FY2020

Jaita Harman Baweja (Harry Baweja) Hindi FY2020

Untitled Ravi Vasudevan Malayalam FY2020

Untitled Vijith Nambiar Malayalam FY2020

Untitled (Homi Adajania / Maddock Films) Hindi FY2020

Ankhen 2 Amitabh Bachchan & Others Hindi FY2020

Nervazhi Nayanthara (Bharath Krishna) Tamil FY2020

Shubh Mangal Savdhan - 2 (Colour Yellow Productions) Hindi FY2020

Panda (Indo-China) (Kabir Khan) Hindi FY2020

Tannu Weds Manu 3 Anand L Rai Hindi FY2020

Roam Rom Mein Nawazuddin Siddiqui & others (Tanishtha Chatterjee / Rising Star Entertainment) Hindi FY2020

The Body (Overseas) Emraan Hashmi, Rishi Kapoor (Viacom18 Motion) Hindi FY2020

Time to Dance (Overseas) Sooraj Pancholi, Isabelle Kaif (Super Cassettes Industries) Hindi FY2020

- The above list is indicative and subject to change

Strong releases YTD set to be bolstered by additional highly anticipated titles in the coming years

PAGE 21Select Forthcoming Releases

Tentative

Film Name Star Cast/(Director/Producer) Language

Release

Raw (Overseas) John Abraham (Viacom18 Motion) Hindi FY2020

Untitled Kartik Aaryan (Anees Bazmee) (Next Gen Films) Hindi FY2020

Untitled- (Hindi remake of

Kartik Aaryan / Jacqueline Fernandez (Kyta Productions) Hindi FY2020

Kirik Party)

Chandamama Door Ke Sushant Singh Rajput, Nawazuddin Siddiqui (Sanjay Puran Singh) Hindi FY2020

Pitch White (Vipul Shah) Hindi FY2020

Untitled (Rahul Dholakia / Next Gen Films) Hindi FY2020

Heer (Colour Yellow Productions) Hindi FY2020

Fake (Raj & DK) Hindi FY2020

Re-Union (Sujoy Ghosh) Hindi FY2020

Hera Pheri -3 Suniel Shetty and others Hindi FY2020

Phobia 2 (Next Gen Films - Pawan Kriplani) Hindi FY2020

2 Guns (Krishna Jagarlamudi) Hindi FY2020

R. Rajkumar 2 (PrabhuDeva / Next Gen Films) Hindi FY2020

Khalifey Sanjay Dutt, SaifAli Khan, Arshad Warsi (Prakash Jha) Hindi FY2020

Make in India (Next Gen Films) Hindi FY2020

Jugaadu Harman Baweja Hindi FY2020

1234 (Part 2) Suniel Shetty, Paresh Rawal (Ashwni Dhir) Hindi FY2020

- The above list is indicative and subject to change

Strong releases YTD set to be bolstered by additional highly anticipated titles in the coming years

PAGE 224 Financial Overview

H1 FY2019 EBIT up by 26.4%, PAT

higher by 31.7%

Figures in INR million H1 FY2019 H1 FY2018 Growth (%)

Total Income 5,441 5,473 (0.6)%

EBIT 2,033 1,609 26.4%

EBIT Margin 37.4% 29.4% +800 bps

Adj. EBITDA (1)

2,395 1,917 24.9%

Adj. EBITDA Margin 44.0% 35.0% +900 bps

PAT (after minority) 1,363 1,035 31.7%

PAT Margin (%) 25.1% 18.9% +620 bps

Diluted EPS (Rs.) 14.17 10.82 31.0%

• Eros released 31 films (5 medium budget, 26 small budget) & 1 Digital Series in H1 FY2019 as compared to

12 films (1 high budget, 3 medium budget , 8 small budget) in H1 FY2018

• Margin expansion driven by a content - driven films, strong pre-sales strategy and catalogue monetization

1) Adjusted EBITDA is defined as EBITDA adjusted for (gain)/impairment of available-for-sale financial assets, profit/loss on held for trading liabilities (including profit/loss on derivative

financial instruments), transactions costs relating to equity transactions, share based payments, Loss / (Gain) on sale of property and equipment, Loss on de-recognition of financial assets

measured at amortized cost, net, Credit impairment loss, net, Loss on financial liability measured at fair value through profit and loss, Loss on deconsolidation of a subsidiary and

Impairment of goodwill (as applicable).

PAGE 24Conservative Balance Sheet: Leverage

and liquidity improve further

All figures in Rs. Million

Particulars As on Sept 30, 2018 As on March 31, 2018 As on Sept 30, 2017

Cash 2,106 1,872 1,887

Net Debt 5,112 5,557 5,854

Networth 24,936 22,559 21,188

Net Debt / Equity 0.21 0.25 0.28

Net Debt / EBIT 1.25 1.51 1.63

• Eros’ investments are focused on enhancing its position as a premium content owner of Indian film and

digital content while maintaining a conservative balance sheet

• Capital structure, liquidity and coverage ratios improve further and are well within the prescribed norms.

PAGE 25Consistent Profits; strong growth

in margins

Diversified Revenues Streams FY18

Revenue EBITDA PAT

Television

Figures in Rs. million & Others

46.3% Theatrical

16,257

42.8%

14,453

14,410

Overseas

10.9%

11,396

10,744

10,100

9,632

7,159

3,768

3,679

3,615

3,549

2,997

2,575

2,471

2,293

2,257

2,387

2,262

1,997

1,613

1,545

1,478

1,172

FY'11 FY'12 FY'13 FY'14 FY'15 FY'16 FY'17 FY'18

EBITDA (%) 22.5 23.4 21.1 26.3 25.1 21.8 26.1 36.4

PAT (%) 16.5 15.5 14.5 17.5 17.1 14.7 17.8 22.7

PAGE 26Important notice and disclaimer

Certain statements in this presentation concerning the future growth prospects are forward looking statements, which involve a number of risks and

uncertainties that could cause actual results to differ materially from those in such forward-looking statements. In some cases, these forward-

looking statements can be identified by the use of forward-looking terminology, including the terms “believes”, “estimates”, “forecasts”, “plans”,

“prepares”, “projects” “anticipates”, “expects”, “intends”, “may”, “will” or “should” or, in each case, their negative or other variations or comparable

terminology, or by discussions of strategy, plans, objectives, goals, future events or intentions. These forward-looking statements include all

matters that are not historical facts. They appear in a number of places throughout this presentation and include, but are not limited to, statements

regarding the Company’s intentions, beliefs or current expectations concerning, among other things, the Company’s results of operations, financial

condition, liquidity, prospects, growth, strategies, business development, the markets in which the Company operates, expected changes in the

Company’s margins, certain cost or expense items as a percentage of the Company’s revenues, the Company’s relationships with theater

operators and industry participants, the Company’s ability to source film content, the completion or release of the Company’s films and the

popularity thereof, the Company’s ability to maintain and acquire rights to film content, the Company’s dependence on the Indian box office

success of its films, the Company’s ability to recoup box office revenues, the Company’s ability to compete in the Indian film industry, the

Company’s ability to protect its intellectual property rights and its ability to respond to technological changes, the Company’s contingent liabilities,

general economic and political conditions in India, including fiscal policy and regulatory changes in the Indian film industry. By their nature, forward-

looking statements involve known and unknown risk and uncertainty because they relate to future events and circumstances. Forward-looking

statements speak only as of the date they are made and are not guarantees of future performance and the actual results of the Company’s

operations, financial condition and liquidity, and the development of the markets and the industry in which the Company operates may differ

materially from those described in, or suggested by, the forward-looking statements contained in these materials. The forward-looking statements

in this presentation are made only as of the date hereof and the Company undertakes no obligation to update or revise any forward-looking

statement, whether as a result of current or future events or otherwise, except as required by law or applicable rules.

PAGE 27You can also read