Cus Zomato: Delivering convenience - Edelweiss

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

June 2021

Sector Report

Internet

f

cus

Zomato: Delivering convenience

Pranav Kshatriya Nihal Mahesh Jham

+91 22 4040 7495 +91 22 6623 3352

Pranav.Kshatriya@edelweissfin.com Nihal.Jham@edelweissfin.com

Sandip Agarwal Pulkit Chawla

+91 22 6623 3474 Pulkit.Chawla@edelweissfin.com

Sandip.Agarwal@edelweissfin.com Edelweiss Securities Limited

Internet

Contents

Executive Summary ................................................................................................. 2

Ordering frequency- Key Driver of LTV .................................................................... 5

Quality of Network Effects .................................................................................... 12

Dissecting disintermediation ................................................................................. 15

Large addressable market ..................................................................................... 20

QSRs: Beneficiaries with a caveat .......................................................................... 24

Business Model ...................................................................................................... 30

Financial Outlook ................................................................................................... 34

Valuation ............................................................................................................... 41

Key Risks ................................................................................................................ 46

Global Peer Set ...................................................................................................... 47

Management Overview ......................................................................................... 62

Financials ............................................................................................................... 64

Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset Edelweiss Securities Limited

Internet

Executive Summary

Zomato IPO is shaping up as a landmark: the first IPO of an India-based

large-scale consumer platform. In its essence, the upcoming IPO

shows investors’ hunger to pay top dollar, at rich valuations, for a fast-

growing food delivery business in a large addressable market. Indeed,

Zomato is well-entrenched and fast-growing, but also loss-making.

Our menu for this note includes sizing up emergence of food delivery

platforms globally (Meituan, Doordash, Deliveroo) and decoding

Zomato’s success recipe using our proprietary three-pronged

framework, comprising: i) quality of network effect; ii) consumer

lifetime value (LTV); and iii) total addressable market. (Link)

Food delivery platforms presuppose network effects, which drive

scale. But that’s much weaker than other global platforms due to local

clustering, which means food platforms seldom have pricing power—

thereby curtailing profitability. Global insights indicate consumers

love the sheer convenience of online food ordering, leading to higher

ordering frequency, which drives growth and – eventually – profits.

For restaurants, delivery platforms are a necessary evil: a lower-

margin channel that also cannibalises dine-in, but expands catchment

and drives incremental business. Restaurants/QSRs (McDonald’s,

Domino’s) are hence trying to disintermediate delivery platforms, but

it’s a tall order—to emulate convenience, variety and experience

offered by platforms. Meanwhile, we do view Swiggy as a worthy

competitor: smaller, backed by marquee investors and growing faster.

Zomato’s success rests squarely on its execution vis-a-vis Swiggy.

On balance, we have an optimistic growth outlook for food delivery

platforms in India and their unit economics. Zomato’s valuation has

high sensitivity to average order value (AOV), and we peg its valuation

at USD7–9bn (base case: USD8.1bn, 49% premium to its last funding

round). A notable dip in AOV due to single orders – instead of family

orders – and rising discounts due to increased competitive intensity

are the key risks to unit economics, and valuations.

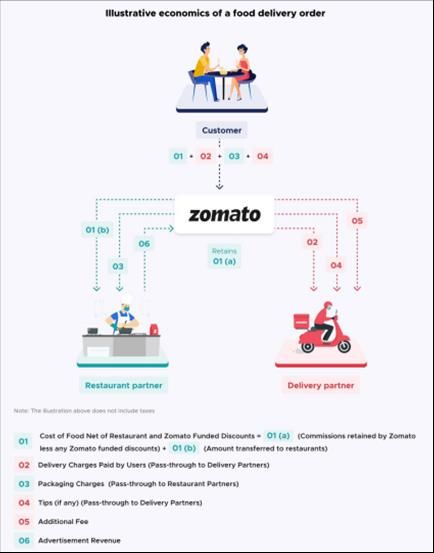

A plateful of levers: A classical aggregator model

For a small fee, food delivery platforms offer consumers a variety of food choices,

ease and a consistent ordering experience. Restaurants gain from starkly larger

catchment and an on-demand delivery fleet. But, since food delivery platforms have

higher market power, they can tweak commissions for restaurants as well as delivery

partners, or even delivery charges levied on consumers, to drive profitability.

A platform’s stickiness also drives higher advertising revenue from restaurants. Food

delivery platforms also typically run loyalty programs that reduce delivery charges,

but ensure higher ordering frequency. Hence, we see food delivery platforms

operating on an asset-light model with high consumer loyalty, which gives them a

plateful of levers to drive unit economics.

2 Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset Edelweiss Securities Limited

Internet

Main ingredient: Convenience drives ordering frequency, LTV

Food delivery platforms’ LTV is driven by: i) average order value (AOV); ii) take rates;

iii) delivery charges; iv) average ordering frequency; and v) churn rate. Of these, we

note that ordering frequency is the key driver of LTV; other parameters largely settle

at a steady state after initial improvements.

In this way, convenience of online ordering and an array of food options on tap are

the key drivers of increasing ordering frequency. In fact, AOV has remained broadly

flat in most geographies. Take rates tend to increase during initial years and then

plateau as platforms focus on on-boarding restaurants. Delivery charges decline as

order volumes rise, kicking in efficiencies. However, since these are point-to-point

orders, there are limits to efficiencies. Churn typically dips as customers tend to

gravitate towards one platform after tasting a few.

Mild flavour: Network effect modest…you get scale, not pricing power

Network effect in food delivery platforms is limited due to local clustering,

commoditised offerings and vulnerability to multi-homing. Network effect for food

delivery platforms are somewhat similar to ride-hailing and is lower than global

platforms in messaging, social media, etc. Typically one large player dominates even

in large markets, such as the US and China, but they have limited pricing power and

hence low profitability. Local clustering thus has had a fallout: even reasonably well

established players in a local market can lose market share as newer players with

more efficient offerings enter. Hence, operational excellence by driving down

delivery costs, among others, is critical to maintaining leadership and profitability.

Alternative recipe? Yes, but risk of disintermediation low

With restaurants’ revenue from food delivery platforms rising materially during the

pandemic, their profitability was hit due to high take rates. Hence, restaurants are

trying to orchestrate the direct food delivery platforms by collaborating with SaaS-

based ordering platforms and third-party delivery services. While overall consumer

experience is satisfactory, we believe most standalone restaurants do not have the

financial and marketing wherewithal to drive orders through their own platforms.

Many payment apps such as PhonePe, Paytm and GPay are aggregating direct

delivery platforms, restaurant discovery and ordering experience remain much

poorer than specialised food delivery platforms. On the whole, risks of

disintermediation are low for food delivery platforms, although a portion of high-

value ordering such as gourmet food and bulk orders may shift to direct delivery.

Stomach for more? Indian food delivery market can gulp lots more

Online food delivery platforms are at a nascent stage in India with an industry size

of meagre USD4.2bn (USD21bn for USA, USD90bn in China). It is, however, growing

rapidly in the country with food delivery reporting a staggering 147% CAGR over

FY18–20. However, with the pandemic nibbling away at the business, the industry

had to swallow a 41% decline. Even so, growth is phenomenal and driven by

increasing adoption of food delivery platforms, rising ordering frequency, and an

expanding proportion of restaurant food consumption versus home food.

We believe adoption of food delivery platforms in India will be a function of user

education, availability and ease of payment options, and reach of platforms. Since

India has only 45–55mn online food delivery users compared with 740mn mobile

data connections, online food delivery platforms has swathes of space for

penetration that can fuel its growth for a long time.

Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset Edelweiss Securities Limited 3

Internet

Culinary comparison: QSRs are beneficiaries with a caveat

Zomato’s public filing has some interesting trends from the restaurant/QSR

perspective. We note the following. i) Jubilant FoodWorks’ recovery has been similar

to Zomato’s GOV, pointing to the strength of its delivery-based model. (QSR: The

Right Combo) ii) Active competition has not reduced as initially thought. iii)

Platforms are a long-term enabler for the sector. That said, it is a lower-margin

channel than dine-in. Incremental business drives profit but cannibalization impacts

negatively. We also compare JFL with Zomato —similarities aside, the two business

models are fundamentally different with Zomato’s being more scalable.

Tempting aroma: Consumers globally are loving food delivery

We note that evolution of online food delivery is different across players and

geographies, but with a few similarities. Many companies such as Uber, Grab and

Gojec got into food delivery because they already had riders that could deliver food.

Players such as Zomato went from restaurant listing to delivery, while a few like

Swiggy and DoorDash started as online food delivery platforms. Almost all delivery

platforms across the globe have seen a huge spurt in delivery volumes riding on

consumer convenience. However, we also note that most delivery platforms make

losses at operating level; even the most matured ones work at meagre operating

margins, e.g. Meituan at 4.2%.

Foodies can surprise: High growth driving up valuation

Zomato’s global peers trade at 2–12x 1-year forward price to sales. The multiple is

contingent on growth potential of a market and market share of the player. For

Zomato, we use a two-stage DCF model, which yields a value of INR581bn

(USD8.1bn). Our assumptions: 32% revenue CAGR over FY21–30, 10% FCF growth

for next eight-years and 10% for second-stage, and 4% terminal growth. The

valuation has high sensitivity to AOV; for instance, a 10% lower AOV will suppress

valuation by 22%. We believe Zomato’s valuation depends on its ability to sustain

and fortify its leadership in the Indian food delivery market.

For perspective, Swiggy is slightly smaller than Zomato, but has delivered stronger

growth; hence, for Zomato to sustain valuations, it must gear up.

Rigours of recipe: Key risks

As online food delivery, and the gig economy in general, is at an early stage of

development, the ecosystem is evolving and there are risks to watch out for: i)

unfavourable regulations curtailing pricing or increasing delivery costs etc; ii)

increase in competition, leading to weaker unit economics and higher costs, would

impact profitability; iii) deeper-than-anticipated fall in AOV; iv) delivery and other

cost escalations and inability of platform to pass them through; and v) despite low

odds of success for direct delivery, an unlikely success can potentially disrupt food

delivery platforms’ business models, including Zomato’s.

4 Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset Edelweiss Securities Limited

Internet

LTV = f(ordering frequency)

Convenience of online ordering is driving ordering frequency, which is the most

important driver of LTV.

LTV = [Average order value (INR) X take rate (%) – Delivery charges (INR) –

Discounts (INR)] X Average ordering frequency/ Churn

Average order value (AOV) tends to remain steady under normal circumstances.

Zomato savoured an AOV surge during the pandemic as: i) more family ordering

took place than individual ordering; ii) premium dine-in restaurants joined the

food delivery platform bandwagon; and iii) consumers showed increasing

preference for hygienic restaurants, even though more expensive. To be sure,

some of these factors are temporary, and might reverse.

Delivery charges tend to dip as ordering volume rises, bringing in efficiencies.

However, as these orders are point-to-point orders, there are limits to which

efficiencies can be extracted.

In our last Internet report Decoding platform economy, we had laid out the

framework for evaluation of platform businesses on the basis of three parameters:

i) LTV of customers; ii) the quality of network effect; and iii) total addressable

market. We are using the same proprietary framework for evaluating Zomato.

Ordering frequency: Biggest driver of LTV Convenience of online ordering driving LTV

Consumer lifetime value is one of the crucial parameters in determining the

valuation of the company. Below equations shows the LTV of customers, which is a

function of the following terms: i) AOV; ii) take rates; iii) delivery charges; iv) average

ordering frequency; and v) churn rate.

LTV= {Average order value (INR) X take rate (%) – Delivery charges (INR) –

Discounts (INR)} X Average ordering frequency/ Churn

We note that LTV is largely a function of AOV and ordering frequency since other

parameters largely settle at a steady state after initial improvements. Globally, we

have seen improving average ordering frequency as the biggest driver of LTV while

churn dips as customers tend to gravitate towards one platform after trying a few of

them.

Average order value has largely remained flat in most geographies. Besides,

platforms have cut down on the discounts for attracting consumers and driving

repeat orders. Besides, these platforms have increased the take rate as restaurants

also see the benefit of higher asset turnover. Delivery charges are seen declining

with increasing ordering volume bringing in efficiencies. However, as these orders

are point-to-point, there are limits to which efficiencies can be extracted.

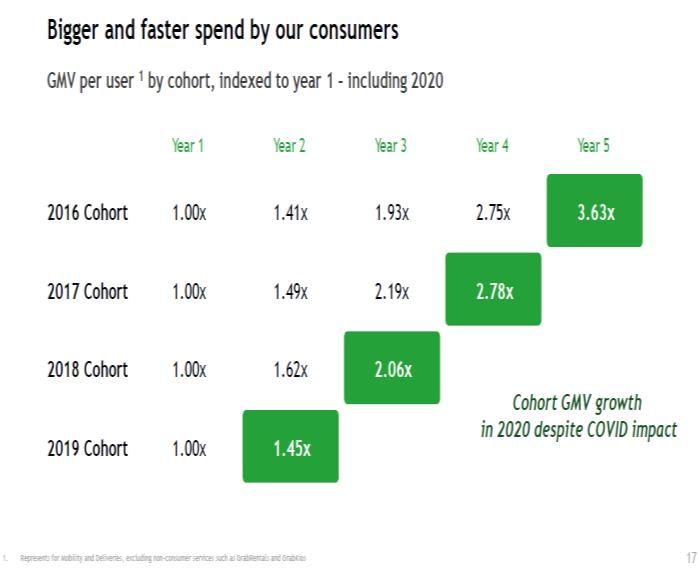

Average ordering frequency is rising across the globe

Across the globe, cohorts tend to indicate that popularity of food platforms

continues to be on the rise. This trend has been consistent across both developed

and emerging countries. Not only are the total number of users rising rapidly, the

frequency of ordering has been on an uptrend across the world. GrabFood, which

has seen a sharp increase in GMV per user cohorts across users. While average order

value grew substantially only in 2020, average ordering frequency has been the

major driver of GMV per user cohort.

Similarly, the cohort for Doordash shows that the marketplace GOV from each

customer cohort has gone up year after year. Also newer cohorts are spending

Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset Edelweiss Securities Limited 5

Internet

higher. For instance, spend of 2018 cohort in Year 2 is higher than that of spend of

2016 cohort in year 4 and 2017 cohort in year 3.

GrabFood – GMV per user cohort DoorDash – Marketplace GOV cohort

Source: Company Source: Company

In China, Meituan’s ordering frequency almost tripled over the last five years.

Coupled with rapid growth in new users, this has been the primary driver of growth

for its gross merchandise value (GMV).

Meituan – Rising average transactions per user Meituan – Transaction cohort

30 28.1

27.4

25 23.8

20 18.8

15 12.9

10.4

10

5

FY15 FY16 FY17 FY18 FY19 FY20

Source: Company, Edelweiss Research Source: Company, Edelweiss Research

Average order value (AOV) trends are mixed

While GMV has increased across companies, not many of them have seen any

meaningful increase in their AOV. Rather, there is no clear trend in the AOV across

the board. DoorDash and Delivery Hero in developed markets have seen a drop in

their AOVs over the last few years. On the other hand, Meiutan has seen a 14.3%

AOV CAGR over the last five years, but the AOV spurt was in the initial two years

while the three-year CAGR is barely 3.7%.

6 Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset Edelweiss Securities Limited

Internet

No clear trends in AOV across global companies (rebased to 100)

200

170

140

110

80

50

FY15 FY16 FY17 FY18 FY19 FY20

Meiutan Doordash Just Eat Takeaway Delivery Hero Grubhub

Source: Company, Edelweiss Research

Zomato AOV spurt led by family, premium ordering

Zomato’s AOV increased 32% in Q1FY21 to Zomato witnessed a 32% increase AOV post lockdown announcement as highly

INR378, from INR287 in Q4FY20 as lockdown mobile young professionals started working from home and they tended to order

resulted in larger ordering for family, and for the family, instead of ordering for an individual. Also, premium restaurants,

ordering from premium restaurants which were solely for dine-in patrons, were forced to list on food delivery platforms

in the wake of pandemic. Yet another reason that can be attributed to the increase

in order value is customer preference for premium restaurants, which tend to have

higher hygiene standards.

Spike in Zomato's AOV during pandemic

450

407

394

378

360

292 287

265 273

270

(INR)

180

90

0

Q1 FY20 Q2 FY20 Q3 FY20 Q4 FY20 Q1 FY21 Q2 FY21 Q3 FY21

Source: Company, Edelweiss Research

That said, we expect AOV to trend down once the economy starts opening up and

more individuals start ordering (as opposed to families). Furthermore, expansion

into newer cities is expected to exert pressure on the average order value. However,

we expect AOV to come down by only 6% in FY22 to INR360 (from INR381 in FY21)

and remains higher than the pre-pandemic level. We note that the low pre-

pandemic AOV was also supressed due to food delivery platforms promoting flat-

priced meals and affordable single-serve meals, which may not come back.

Moreover, we expect the pandemic to drive more users to more hygienic

Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset Edelweiss Securities Limited 7

Internet

restaurants, which tends to be more expensive. Hence, we do expect AOV to reduce

to INR360 in FY22, but will remain higher than the pre-pandemic level of INR280.

Take rates tend to stabilise

We observe that take rates tend to increase initially and then settle at a steady state.

Food delivery platforms begin with lower take rates to incentivise restaurants in a

bid to on-board them. As they business starts picking up, they tend to increase take

rates to cover the cost of delivery, promotions, etc.

There can be a difference among take rates across platforms in a country. While

companies such as Deliveroo and Delivery Hero have the highest take rates in the

world (25–30%), the take rate for DoorDash and Uber Eats would be in the vicinity

of 11–14%. Meituan’s take rate (13–14%) is also among the lowest across countries.

We attribute the lower take rates in China to higher penetration, denser population

driving down costs, and higher competition.

Take rates – A global view

35

29

28

22.8

21

(%)

13.6 12.9

14 11.7

7

0

Deliveroo Zomato Meituan Uber Eats DoorDash

Source: Company, Edelweiss Research

While take rates have been rising over the last few years, we need to be cognizant

that this trend is unlikely to continue for long. There has been opposition from

restaurants and regulators alike, who feel the need to protect restaurants from

higher take rates charged by aggregators. In fact, several cities including New York,

San Francisco, Las Vegas, Washington, etc. had put a temporary cap on delivery

commission to protect interests of restaurants during the pandemic.

8 Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset Edelweiss Securities Limited

Internet

Meituan – Monetization rate Uber Eats – Take rate

15% 14.0% 25%

13.5% 13.6% 22%

12.3% 20%

12% 20% 18%

9.0%

9% 15% 12.90%

9.70%

6% 10%

3% 5%

1.1%

0% 0%

FY15 FY16 FY17 FY18 FY19 FY20 2016 2017 2018 2019* 2020*

Source: Company, Edelweiss Research Source: Company, Edelweiss Research

*Uber started combining Uber Eats in Delivery segment and changed

the definition from 2019 onwards. Hence, prior years are not

comparable

Deliveroo – Take rate DoorDash – Take rate

32% 12%

11.7%

31% 12%

30% 30%

11.0%

29% 29% 29% 29% 11%

28%

28% 11% 10.3%

27% 10%

26% 10%

FY15 FY16 FY17 FY18 FY19 FY20 FY18 FY19 FY20

Source: Company, Edelweiss Research Source: Company, Edelweiss Research

Take rates of Indian companies: Already elevated

Take rates of Indian companies, including Indian companies such as Zomato and Swiggy currently charge a take rate of 22–

delivery charges, are 22–25%, while for 25%, which is on the higher side globally and among the highest in developing

global peers they range from 11–30% countries. Higher take rates can spur risk of disintermediation, as well as new

competitors entering the segment. Amazon is also eying this segment by offering

half of the current take rate. However, since Amazon does not have a different cost

structure, we believe these introductory take rates will be neither sustainable nor

scalable. This, at best, may keep industry profits low till competition wanes out.

Zomato follows a different commission structure based on the type of restaurant.

While non-chain restaurants pay a much higher commission, outlets part of a chain

pay lower. At present, the commission rates vary anywhere from 18–40% of the

order value. The amount depends on parameters such as order size and restaurant

type. Companies such as Jubilant FoodWorks (JFL), which lists on the platforms like

Zomato to receive orders but deliver through their own fleet, pay a 6–8%

commission.

Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset Edelweiss Securities Limited 9Internet

Estimated commission take rate

30

24-26

24

18

14-16

(%)

12

6-8

6

0

Only Listing/Self Delivery Large Chains Non Chain Restaurants

Source: Edelweiss Research

One of the key concerns of restaurants has been a potential further increase in take

rates by food platforms would eat into their margins. However, a comparison of

Zomato’s historical take rate trends, comparison with global peers and also

Amazon’s potential entry in this segment (pilot underway in Bangalore), we expect

steady take rates.

Delivery costs economises with scale

Companies have been focused on reducing delivery cost per order by taking several

initiatives. For instance, Zomato has seen a steady decline in its last-mile delivery

costs. The delivery cost comprises payment to delivery partners along with an

availability fee. Reduction has been achieved by a combination of higher throughput

and lowering of availability incentives.

Zomato – Delivery cost per order trending down

100

88 86

76

(INR)

65

64

52

52

45

40

FY18 FY19 FY20 9MFY21

Source: Company, Edelweiss Research

However, once companies undertake steps to optimize delivery costs per order,

these costs generally stagnate at a certain level. For instance, Meituan in China has

seen its delivery rider costs now stabilize within RMB4.5–5. Given these are point-

to-point deliveries, optimization and economies of scale can be improved only to a

10 Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset Edelweiss Securities LimitedInternet

certain extent and idleness of a rider cannot be reduced beyond a degree. Due to

this, cost per order has started increasing for Meituan.

Meituan- Delivery cost per order

6

4.8 4.9

4.7

4.8 4.5

3.6 3.2

(RMB) 2.4

1.2

0.4

0

FY15 FY16 FY17 FY18 FY19 FY20

Source: Company, Edelweiss Research

Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset Edelweiss Securities Limited 11Internet

Quality of network effect is modest

The network effect in food delivery platforms is curtailed due to local clustering,

commoditised offerings and vulnerability to multi-homing.

Network effect for food delivery platforms is somewhat similar to ride hailing

and is lower than global platforms in messaging and social media.

Typically a large player dominates food delivery, even in large markets (US,

China), but nevertheless has limited pricing power and hence low profitability.

Restaurants are trying to disintermediate food delivery platforms by going direct,

but considering challenges of on-boarding customers on individual restaurant

platforms, they may succeed only in gourmet food or high-order value cases.

Network effect helps achieve scale, but pricing power is limited

Various factors determine the quality of network effect, such as: i) network

clustering (local or global clustering); ii) commoditized or differentiated supply; iii)

vulnerability to multi-homing; and iv) risk of disintermediation. Besides, the gradient

of customer acquisition cost (CAC) over time series is a good measure of the quality

of network effect. Exhibit 14 summarises network effects in case of food delivery

platforms.

Scorecard for quality of network effect for food delivery platforms

Parameter Score Remark

Food delivery platforms are local in nature as a limited

Network clustering Low

number of restaurants can cater to a cluster

Commoditized or

Medium Few exclusive cloud kitchen and restaurants tie-ups

differentiated supply

Vulnerability to multi- Multi-homing is possible but only a few platforms are there

Medium

homing and consumer can be locked into with loyalty program

Risk of

High Risk of disintermediation is real only in high-value items

disintermediation

Network effect strong enough to drive scale but not pricing

Overall Medium

power

Source: Edelweiss Research

Network clustering

In terms of network clustering, food delivery platforms are local in nature; these

platforms may boast a large number of restaurants but for a customer, only the

number of restaurants which can deliver to him matters. Hence, if in one locality a

platforms can onboard higher number of restaurants, and have sufficient delivery

fleet to match another platform, consumers in that area will want to migrate to that

platform basis the better choice. Hence higher number of restaurants at overall level

does not add value to the network if the size of the network in certain area is weak.

Localisation reduces the barrier to entry and hence there have been examples of

existing players losing market share to newer and more efficient players. Despite

DoorDash’s late entry in the US food delivery market, it captured a 55% market share

on the back of its efficiencies.

Food delivery platforms are local in nature

Initially, the US too had more localised monopolies, creating an oligopolistic

as limited number of restaurants can cater structure at a national level. Grubhub was a leader at the national level. However,

to a cluster DoorDash managed to scale up much faster than any other player during the

pandemic with better execution, which was largely around the number of

restaurants, delivery speed, etc. This resulted in a nearly 55% market share for

12 Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset Edelweiss Securities LimitedInternet

DoorDash, whereas other players lost market share. We note that even in larger

markets, superior execution can rapidly drive market share. Hence in a market like

India, which has a long growth runway, better execution to drive growth is key to

value creation.

Food delivery market share in US

Source: Bloomberg Second Measure

Commoditized or differentiated supply

Food delivery platforms can differentiate via

Food delivery platforms tend to fall somewhere between commoditized and

exclusive ties-up with local popular differentiated supply. On the one hand, the supply is differentiated because there

restaurants, but it comes at a cost are many restaurants and type of foods to choose from. Some platforms even have

an exclusive partnership with popular restaurants. But, on the other hand, if all of

these food delivery platforms provide more or less the same menu—all restaurants

are available across platforms—the supply would get commoditized. The point

of differentiation therefore shifts to delivery cost, delivery speed, ease of use

and other features.

Vulnerability to multi-homing

Food delivery platforms are addressing Multi-homing measures the switching cost of a platform. It simply means how easy

multi-homing issues by introducing loyalty is it for users to switch between platforms that provide similar services. Food

programs delivery platforms may see multi-homing on both – consumer and delivery

personnel side. To reduce multi-homing, companies can opt for loyalty bonus or

membership offerings that promotes frequent ordering on one platform, or they can

enter into exclusive partnerships with popular restaurants. Some platforms also

introduce their own cloud kitchen, which not only increases choice, but also captures

a higher portion of value from the transaction.

Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset Edelweiss Securities Limited 13Internet

Swiggy Super and Zomato Pro – A comparative snapshot

Swiggy Super Zomato Pro

INR89 (Bit)/ INR169 (Bite)/ INR329

Price INR200/3 months

(Binge) per month

Bit' plan - Five free deliveries

per month.

'Bite' plan - Ten free Up to 30% extra off on food

deliveries per month and one deliveries

'Buy One Get One free' from up to 40% off on each dining

Features

restaurant partners experience

'Binge' plan - Unlimited free Faster delivery with top-rated

deliveries and unlimited 'Buy valets

One Get One free' offers from

partner restaurants

Cities 80 41

Partner

> 7,000 >25,000

Restaurants

Source: Company, Edelweiss Research

Risk of disintermediation – Low in most cases

Since impromptu and frequent ordering

Food delivery platforms, for a small fee, offer consumers choice, ease and consistent

drives the bulk of order value on food ordering experience, which has led to rapid adoption among consumers. However,

platforms, we believe the risk of for restaurants, food delivery platforms charge a significant commission for availing

disintermediation is low a higher catchment area and an on-demand delivery fleet. High take rate impacts

profitability of restaurants, especially for high-value orders. Hence, premium

restaurants are increasingly looking to connect directly with consumers for food

delivery. However, since impromptu and frequent ordering drives the bulk of order

value, we believe the risk of disintermediation remains low.

Weaker network effect has kept profitability under check

Due to local clustering of food delivery platforms, the risk of disruption by a new

player remains high. Hence, we note, largest players typically command a market

share of 50%-plus in most geographies, but they still operate at low margins. Despite

over a 65% market share in the Chinese market, Meituan’s operating profit margin

in food delivery is a meagre 4.3%. Most other companies have a negative operating

profit. That said, we expect profitability to improve as market matures and larger

players create efficiencies of scale, which act as an entry barrier for new players.

Operating margin of global companies are low

10

3.6

0

Meituan Just Eat Takeaway DoorDash Delivery Hero

-5.2

-10

(%)

-15.1

-20

-30

-40 -36.2

Source: Bloomberg, Edelweiss Research

14 Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset Edelweiss Securities LimitedInternet

Dissecting disintermediation

Restaurants are keen on exploring solutions to reduce their dependence on food

delivery platforms considering high take rates that eat into their profitability.

SaaS-based ordering platforms such as Dotpe and Thrive are creating ordering

platforms for restaurants, along with integration of third-party logistics players

for order fulfilment.

While deploying these solutions is relatively easy, pushing consumers to adopt

direct ordering is the biggest challenge for restaurants.

We see large QSRs and chain restaurant with enough resources to drive direct

ordering; other restaurants will find it challenging to market their platforms.

Direct delivery – Crucial to restaurants’ profitability

Shift in restaurant business in favour of

Although food delivery platforms help restaurants drive volumes, they also create

delivery, from dine-in in the wake of the two challenges: i) food delivery platforms do not share customer data with

pandemic has eaten into their profitability restaurants; hence restaurants find it difficult to create patronage; and ii) food

delivery platforms charge a high fee, which significantly impacts profitability. High

fees is a significant challenge for premium restaurants. Many dine-in restaurants do

not offer home delivery due to high charges levied by delivery platforms. However,

the pandemic has significantly altered the revenue mix for restaurants with dine-in

revenue almost entirely going away.

In order to address the issue of consumer data and high commissions, some

restaurants are working with SaaS platforms such as DotPe and Thrive to create

seamless ordering systems. These ordering systems, if required, can also source

delivery fleet from third-party delivery partners such as Dunzo, WeFast and

Shadowfax. In order to drive usage of their own platforms, restaurants are

leveraging social media platforms, such as Instagram and Facebook for popularising

their services. Indian Hotels has also launched their own app “Qmin” offering food

delivery from their restaurants and kitchens, which have INR1,000 as the ordering

threshold.

Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset Edelweiss Securities Limited 15Internet

DotPe – Direct delivery

Source: Company

Discovery and variety – A key challenge for customers

On the consumer experience side, we note consumers are likely to go to the

restaurant portal to order only if they are aware of the direct ordering facility, are

sufficiently incentivised, and the experience is as good as ordering on a food delivery

platform. To incentivise, restaurants offer no delivery fee apart from other

discounts. Since the address and payment details are stored by SaaS platforms,

despite their web-based interface, user experience is reasonably smooth.

While direct-to-consumer has numerous advantages for restaurants, the main

challenge continues to be pertaining to discovery. These companies have also

realized this problem and have consequently tied up with popular payment

platforms such as GPay, PhonePe and Paytm. Using these apps, customers can

search for restaurants and order directly via these apps without the hassle of

searching them individually.

Although this adds discoverability, but the experience is not as sophisticated as on

food delivery platforms as there are no options to sort the restaurants according to

various parameters, there is no visibility on how much time restaurant will take for

delivery, rating of the restaurants, etc. Considering payment apps are not sufficiently

integrated with restaurants’ and third party logistics providers, we do not expect

discovery platforms to become as sophisticated as food delivery platforms, and thus

the experience offer is likely to be sub-par.

16 Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset Edelweiss Securities LimitedInternet

Direct food ordering is available on platforms like Google Pay, Phonepe and Paytm

Source: Company

Consumer experience, outside discovery, is seamless

Technology integration for direct delivery works in such a way that SaaS platforms

can on-board restaurants in a matter of days by creating digital menus, integrating

the billing system and offering third-party delivery platforms on-the-go. For high-

ticket size, third-party delivery platform costs work out lower than those charged by

delivery platforms. Since SaaS platforms work this through an Application

Programing Interface (API), consumer get a fairly seamless experience with a

WhatsApp or SMS update on food dispatch with a link to track delivery personnel in

real time.

Direct delivery – Impact varies for players

We believe different segments of restaurants face their own set of challenges –

resource availability and dependence on food delivery platforms is different – due

to which their possibility and success in adoption of direct ordering will be different.

Hence, we are evaluating the opportunities and success possibilities for each

segment separately. We are broadly classifying restaurants into three categories: i)

large QSR chains and cloud kitchens; ii) large chain restaurants; and iii) standalone

restaurants and eateries.

Large QSR chains and cloud kitchens

Large and popular QSR chains such as McDonald’s, Domino’s and KFC as well as large

cloud kitchens such as Rebel Foods (which owns brands such as Faasos, Behrouz

Biryani and Oven Story), Poncho Hospitality (which owns Box8 and Mojo Pizza),

typically have their own apps for food delivery. These companies also possess

enough financial, marketing and logistics muscle to provide full-stack services.

Furthermore, they can drive discovery through digital marketing branding

campaigns. However, customers are unlikely to download many QSR or cloud

kitchen apps; hence food delivery platforms will continue to drive the bulk of

delivery business.

Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset Edelweiss Securities Limited 17Internet

We note that success of direct delivery has been mixed for different companies.

Domino’s has been particularly successful with ‘30 minutes delivery’ attracting

customers’ craving at breakneck speed. Other QSR chains and cloud kitchens are

relatively less successful due to their inability to match this speed and other factors.

However, with food aggregators gaining prominence, most of these companies have

been unable to match the ease of use provided by aggregators. User experience for

food aggregators has been far superior to those provided by these apps. We believe

that this section of restaurants will be able to get 20–30% food delivery on their own

platforms. The proportion of direct ordering will be a function of strength of the

brand and their execution capabilities.

McDonald’s, Domino’s and Faasos food delivery

Source: Companies

Popular chain restaurants

Popular chain restaurants are characterised by high patronage, repeat customers

and relatively high AOV. They typically rely on dine-in patrons for revenue, but the

pandemic changed this dynamic. Since the take rate for aggregators is high, these

restaurants have faced a major brunt, having to pay a significant amount to the likes

of Zomato and Swiggy. Discovery is not a major issue for these restaurants as they

are anyway well-known.

Consequently, these restaurants have been at the forefront of the direct delivery

campaign. While these restaurants do have a certain connect with customers, their

ability to drive these customers to direct delivery portal, by discounting, by

marketing will determine their success. We note that chain restaurants will have to

invest sufficient marketing resources to drive traffic to their own portal.

Some of SaaS based ordering platforms suggest high adoption by restaurants –DotPe

claiming 150k partner restaurants and Tribe suggests another 15k. However, we

believe that some of these on-boarding would be for features other than delivery

and only a handful of restaurants would promote their own delivery. In terms of

cost, Tribe indicated 3% of the GMV as platforms fees and third-part delivery may

18 Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset Edelweiss Securities LimitedInternet

charge ~INR100 for delivery. Hence, assuming a 10% marketing cost and a 10%

discount, own platform breaks even at an order value of INR1,000. This is

significantly higher than Zomato, whose AOV would be lower than INR400. Hence,

we believe that only a handful restaurants would opt for standalone delivery

platforms and it would drive 15–20% of their delivery volumes.

Breakeven analysis: Own platform vis-a-vis Zomato/ Swiggy

(INR) Own Platform Zomato/ Swiggy

AOV 1000 1000

Platform Fees/ Commission 3% 30%

Platform Fees per order 30 300

Delivery Charges 70

Marketing Costs 100

Discount 100

Total Costs 300 300

Source: Edelweiss Research

Standalone restaurants

For small standalone restaurants, while implementing order management platform

is relatively easy, diverting orders to their own platforms will be challenging. We

believe that restaurateurs will find it challenging to attract consumers to their

platforms. Hence, we believe that this segment is unlikely to see any traction with

direct ordering. Consequently, they will continue to remain dependent on food

aggregators for both discovery and delivery.

We believe that most restaurants are not adequately equipped for driving the

marketing campaigns for online ordering platforms. From consumers’ side, while the

ordering experience is seamless, discovery will be a challenge. We believe that

consumers are likely to order from standalone platforms only in case they are aware

exactly what they are looking to order and are adequately informed about the

benefits thereof. Standalone restaurants will require significant marketing support,

which smaller restaurants will not be able to manage. Hence, we believe adoption

of the standalone platform will be limited to premium restaurants or larger chains

that can afford enough.

Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset Edelweiss Securities Limited 19Internet

Large addressable market

Food delivery platforms have made online food discovery and ordering

experience very convenient. This is fuelling growth of online food delivery

platforms across the globe.

Indian food delivery market at ~INR300bn (USD4.2bn) is only a fraction of the

INR4.2tn (USD67bn) out-of-home food eating out market. Restaurants in India

are highly fragmented with chain restaurants accounting for only 6.2% of the

value; standalone restaurants account for the rest of the pie.

Low penetration of online food delivery ordering in India offers a mouth-

watering opportunity.

Non-home cooked food or restaurant food is only ~10% of the overall USD670bn

food consumption market in India (54% in United States and 58% in China).

Changing consumer behaviour, reduced dependence on home-cooked food and

increasing disposable income are further expanding the addressable market.

Indian food delivery market: Long growth runway

Online food delivery platforms are at nascent stage in India with an industry size of

meagre USD4.2bn (USD21bn in US, USD90bn in China). It is, however, growing

rapidly. Food delivery grew at an eye-opening 147% CAGR over FY18–20. However,

with pandemic impacting the business, the industry had to swallow a 41% decline in

FY21. Even so, growth is phenomenal and driven by increasing adoption of food

delivery platforms, rising ordering frequency, and an expanding proportion of

restaurant food consumption versus home food.

Food Services defined as non-home cooked food or restaurant food currently

contributes only approximately 10% to the overall USD670bn food market. This is

starkly lower than global economies such as the United States and China with

respective figures of 54% and 58% (of the total food consumption).

According to RedSeer, the total addressable food services market opportunity of

USD65bn (INR4.6tn) would growing at 9% per annum to USD110bn (INR7.7tn) in

2025. It particularly notes highly under-penetrated restaurant food-eating

behaviour today. While Food Services in India is highly under-penetrated, it is likely

to grow steadily, eating into home-cooked food much like the trend in the past.

Growth will be driven by changing consumer behaviour, reduced dependence of

millennials on home-cooked food/kitchen set-up, increasing consumer disposable

income, and higher adoption among smaller cities.

20 Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset Edelweiss Securities LimitedInternet

Indian markets nascent; comparative snapshot of India, US and China

Source: Zomato DRHP

India has only 45–55mn online food delivery We believe adoption of food delivery platforms will be a function of user education,

users compared with 740mn mobile availability and ease of payment options, and reach of platforms. Since India has only

broadband subscribers 45–55mn online food delivery users compared with 740mn mobile broadband

connections, penetration of online food delivery platforms has a long runway for

growth in the country.

Ease of usage driving adoption

Online food delivery apps have fundamentally altered the food ordering experience.

Restaurant food ordering, pre-food delivery apps era, was cumbersome: i)

restaurant discovery was challenging as consumers had to have the restaurant

contact number and should have been aware of the menu for ordering food, which

limited the choice; ii) restaurant food delivery was subject to in-house fleet and thus

limited to a much smaller geography; iii) payment option was mostly restricted to

cash; and iv) there was no way to track food delivery progress.

Online food delivery platforms have solved all of these problems. These platforms

aggregate multiple restaurant menus with all the relevant details, including pricing,

and reviews, making ordering a seamless experience. They also provide a delivery

fleet to restaurants, thereby significantly widening their catchment area. In most

cases, consumers get real-time updates on the progress of their order, such as

whether the food has left the restaurant and contact details of the delivery person.

And there is a customer friendly helpdesk to check in case something goes wrong.

Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset Edelweiss Securities Limited 21Internet

Zomato – Ease of usage

Source: Company

We believe higher food tech platform usage can increase India’s eating out

frequency, which is much lower than comparable global peers. Even a comparison

of Zomato’s GOV by cohorts points to increasing frequency or usage/eating out.

Currently Zomato completes close to 30–35mn deliveries every month. Swiggy,

which operates on a similar scale, also does roughly the same number of deliveries.

For perspective, Meiutan, the largest food delivery company in the world, makes

850mn deliveries in a single month (65% market share). The largest company in the

US fulfils close to 70mn orders a month (55% market share).

While we do expect the user base to grow significantly, it would be incorrect to

assume the orders at similar levels of these countries without taking into account

the difference in demographics of the aforesaid countries. India has a much larger

population and relatively low penetration, but it is unlikely to scale up to the levels

of other countries, considering India’s huge rural population. Nevertheless, we

expect Zomato’s total orders to grow strongly north of 30% for the next four–five

years to about 130mn orders a month.

Globally, the online food delivery industry has grown rapidly over the last few years.

The Chinese market has been at the forefront clocking a 40% CAGR over 2015–20 to

RMB664.4bn largely driven by increased penetration as more consumers moved

online en masse. Developed markets of Europe have also grown at a brisk pace over

the last few years. OC&C (Strategy Consultants) reckons a 19% CAGR for the online

home delivery segment from 2017–19.

The pandemic has also significantly catalysed online deliveries. In South Asia, GMV

of food delivery surged by 183% in FY20 to USD11.9bn. As highlighted earlier, this

rapid growth has been driven by increased penetration and higher number of

transactions per user.

In the past year, both Zomato and Swiggy have outgrown all major global companies

(except DoorDash) as more users have logged onto food aggregators. However, on

an absolute basis, the GMV of both Zomato and Swiggy remains well below these

global companies.

22 Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset Edelweiss Securities LimitedInternet

Comparison of food delivery companies’ GOV and GOV growth

80 250

64 200

(USD bn)

48 150

(%)

32 100

16 50

0 0

JET

Meituan

Doordash

Delivery Hero

Grubhub

GrabFood

Zomato

GOV % Growth

Source: Company, Edelweiss Research

GMV for both Zomato and Swiggy has soared over the last few years. Zomato’s GMV

more than doubled from USD0.7bn to USD1.5bn over FY19 to FY20. Swiggy has also

seen equally strong performance over the last couple of years with order growth of

320% and 145% in FY19 and FY20, respectively.

Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset Edelweiss Securities Limited 23Internet

QSRs: Beneficiaries with a caveat

Zomato’s public filings throws up some interesting trends from the

restaurant/QSR perspective. We deduce: i) JFL’s recovery has been similar to

Zomato’s GOV, corroborating the strength of its delivery-based model. ii) Fall in

active competition is not as intense as believed initially. iii) Platforms are a long-

term enabler for the sector. iv) Take rates in the industry remain high, even in

context of a global comparison.

We also evaluate profitability of online channel versus dine-in —this remains a

lower-margin channel and incremental business drives profit, but cannibalization

impacts negatively.

While JFL and Zomato are fundamentally different business models, we compare

the two on certain key parameters.

JFL’s recovery has been in sync with Zomato; other have lagged

A comparison of Zomato’s GOV and sales of the three major Indian QSRs shows that

JFL managed to report recovery similar to Zomato on the back of its delivery

excellence. While recovery for burger QSRs has been higher than the industry, it has

lagged Zomato’s given the higher dine-in share.

Sales recovery comparison

125

100

75

50

25

0

Q3FY20 Q4FY20 Q1FY21 Q2FY21 Q3FY21

Zomato (GOV) JFL WDL BKI FS Industry

Source: Zomato DRHP, Company, Edelweiss Research

Note: For Zomato, considered its GOV, for JFL, WDL and BKI considered their reported sales.

Industry competition is nearly back to pre-covid levels

Our business is built around the core idea

In its report on the restaurant industry in August 2020 (Link), Zomato mentions that

that, over time, people in India are going out it expects ~40% of restaurants to shut down. While this was based on a survey by

to eat at restaurants more than they cook at the company (~15,000 restaurants), looking at the bounce back in restaurants on its

home.” platform points to majority of the network bouncing back.

Zomato DRHP

24 Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset Edelweiss Securities LimitedInternet

Active food delivery restaurants

150000 1,43,089

1,32,769

120000

94,286

90000

(#)

60000

33,192

30000

0

FY18 FY19 FY20 9MFY21

Source: Zomato DRHP

Zomato’s customer evolution points to expanding eating frequency

Overall though, online partnerships have been a boon for restaurants as they have

helped increase overall top line by ~30% via a larger consumer base. With improved

kitchen utilisation, online partnerships have also enabled restaurants to improve

their bottom lines, considering the bulk of their costs are fixed (with only 25% of

restaurant costs being food related, i.e. variable).

75% of restaurants costs are non-food/ fixed Ordering online drives a sharp improvement

EBIT

Margin, 5

D&A, 5

Food, 25

Post-Online 70 20 10 30

Other

costs, 20

Pre-Online 70 20 10

Marketing,

5

Labour, 25

Rent, 15 0 50 100 150

Dine in Phone based Take away Online ordering

Source: Prosus, Edelweiss Research Source: Company, Edelweiss Research

Online aggregators also influence consumption behaviour and lead to a significant

increase in ordering.

Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset Edelweiss Securities Limited 25Internet

Evolution of customer using apps

Source: RedSeer Consulting

We believe higher food tech platform usage, can increase India’s eating out

frequency, which is much lower than comparable global peers. Even a comparison

of Zomato’s GOV by cohort shows increased frequency or usage/eating out.

GOV retention by cohort

Source: Zomato DRHP

Per capita spend on food services

Country CY15 CY20

USA 1,735 2,239

China 659 684

Saudi 665 769

Brazil 634 707

South 170 282

Indonesia 219 253

Turkey 124 181

India 94 122

Source: Burger Kind India DRHP, Edelweiss Research

26 Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset Edelweiss Securities LimitedInternet

Take rates/commissions: Limited scope to increase

Zomato follows a varied commission structure based on restaurant’s presence.

While non-chain restaurants pay a much higher commission, outlets that are part of

a chain, shell out lower. At present, commission rates vary anywhere between 18–

40% of the order value. The amount depends on parameters such as the size of the

order and restaurant type. Companies such as JFL, which only use the app for

origination (and not delivery), only pay commission.

One of the key concerns in the industry has been the potential to further increase

take rates of food platforms, which will dent restaurants’ margins. However, a

comparison of Zomato’s historical take rate trends and its comparison with global

peers, not to mention Amazon’s potential entry in this segment (pilot on in

Bangalore), indicates the current levels are more or less the ceiling for take

rates/commissions.

Estimated commission rates

30

24-26

24

18

14-16

(%)

12

6-8

6

0

Only Listing/Self Delivery Large Chains Non Chain Restaurants

Source: Edelweiss Research

One of the key concerns in the industry has been the potential to further increase

take rates of food platforms, which will dent restaurants’ margins. The focus on

commission/take rates has increased recently, especially in the backdrop of higher

sales from these platforms, post covid.

As highlighted above, Zomato’s take rates are among the highest globally and imply

limited scope for further expansion. Also, while pick-up in the Direct Delivery model

remains a debate, it will definitely be an added factor in keeping any further addition

in take rates under check

Foodtech platforms: An incremental business driver, but still lower margin

FoodTech delivery players have been able to provide value to partner restaurants.

Even after factoring in platform commissions (~20%), the incremental business

drives up restaurant profitability. However, business generated from food tech

players is naturally lower margin. If any outlet is generating incremental business,

then food tech is a profitable channel, but substitution of the same customer online

dents margins (refer to Exhibit 34).

Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset Edelweiss Securities Limited 27You can also read