DATA AND ANALYTICS IN INSURANCE: P&C VIEW THROUGH 2020 - Martinexsa

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

DATA AND ANALYTICS IN INSURANCE:

P&C VIEW THROUGH 2020

Hortonworks has been granted distribution rights to this

SMA research report

An SMA Research Report

Author: Karen Pauli

July 2017

An SMA Research Report © 2017

2016 SMA All Rights Reserved | www.strategymeetsaction.com

TABLE OF CONTENTS Executive Summary 3 Insurer Usage and Plans 5 New Data Sources and Emerging Technology 13 SMA Call to Action 17 About Hortonworks 18 Strategy Meets Action Commentary 18 About the Research and Strategy Meets Action 19 An SMA Research Report © 2017 SMA All Rights Reserved | www.strategymeetsaction.com 2

EXECUTIVE SUMMARY

SMA conducted a comprehensive research study on

This report is a continuation of research SMA has been engaged in since 2012. While

data and analytics in the property/casualty industry in

prior reports showed steady progress in data and analytics adoption, external forces and

insurer actions are altering that view. Most specifically, the pace of change within the North America in 2017. Survey participants included

industry has materially escalated, yet insurer response relative to data and analytics has personal and commercial lines insurance executives and

not reflected this, and the gaps are emerging. professionals from both business and IT.

SMA survey results indicate that 92% of insurers have data and analytics initiatives in 2017, This SMA research report identifies where there are

the number two focus, only 3 percentage points behind customer experience. No one measurable differences in various P&C segments. In

denies the value of data and analytics. However, evolving past traditional and into advanced some cases the most relevant views are personal and

capabilities has become imperative. Emerging technology such as AI and big data platforms, commercial lines, while in other cases it is more useful

and new data sources such as IoT, geospatial, drones, and wearables represent the next to review the behaviors and plans of large companies

generation of data and analytics. Critical points evidenced in this research are:

(over $1B in premium) and small companies (under

Insurers continue to invest heavily in basic BI and reporting while nominally investing in $1B).

advanced analytics, data and text mining, and cognitive computing. Predictive analytis

Personal lines organizations allocate 8.6% of IT budgets

is the one category of advanced analytics that is swiftly joining the maturity ranks.

to data and analytics and commercial lines allocate

Specific uses of data and analytics are mature, and have historic investment, but 9.3%, with most organizations increasing spending over

uses related to customer experience and claims are reflective of growing gaps. time.

Not surprisingly, personal lines are ahead of commercial lines in data and analytics “Data is now the source of competitive advantage, and

use. Insurers over $1 billion in premium are more advanced than insurers under insurers must commit capital and talent to the emerging

$1billion, which is cause for concern given the competition for the same business. technologies that will transform silent and disconnected

data into new opportunities.” – Karen Pauli, SMA Principal

Regardless of the size of an organization, a shortage of data and analytics talent

and skills sets are now a significant barrier to advancing capabilities.

There is a small percentage of insurers who are utilizing IoT, wearables, and drone

data, but as much as 82% of insurers have no current plans to do so.

In response to changes in the data and analytics landscape, the SMA Data and Analytics

Spectrum has evolved into its next generation. This report provides a framework for

benchmarking, planning, and executing the spectrum, and provides guidance on how

insurers should respond.

An SMA Research Report © 2017 SMA All Rights Reserved | www.strategymeetsaction.com 3

New SMA Analytics Spectrum

Figure 1. New SMA Analytics Spectrum

DESCRIBE DIAGNOSE DISCOVER PREDICT PRESCRIBE

How do we gain information and What are our new How do we capitalize How do we capitalize on

insights from historical data? opportunities? on new opportunities? advanced opportunities?

What What is Why is it What if it What is the best course of

Where is the problem? What is likely to happen?

happened? happening? happening? continues? action to take?

Dashboards

Ad hoc Advanced Data & Text Predictive Predictive Preventive Cognitive

Reporting & Analysis Scenarios

Queries Analysis Mining Analytics Models Analytics Computing

Scorecards

Geospatial Platforms

AI and Machine Learning

Big Data Platforms

Source: Strategy Meets Action 2017

The SMA Analytics Spectrum was developed to assist insurers in their efforts in developing strategies and plans for BI and analytics. The Spectrum

has been available for several years. However, as the role of data and analytics has grown in importance, and the available tools and technology have

increasingly become more sophisticated, the Spectrum has evolved as well. The categories of Describe and Diagnose are somewhat mature – this is

the domain of traditional BI. The Predict category, historically the task of actuaries and underwriters, has been the recipient of significant spending to

drive more advanced outcomes in 2016-2017. It is the areas of Discover and Prescribe that represent gaps that insurers must address. This research

will provide insights on where and how insurers should focus to take data and analytics initiatives to the next level.

An SMA Research Report © 2017 SMA All Rights Reserved | www.strategymeetsaction.com 4

INSURER USAGE AND PLANS

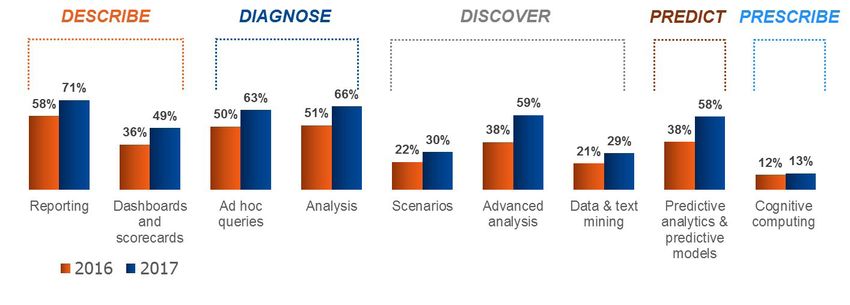

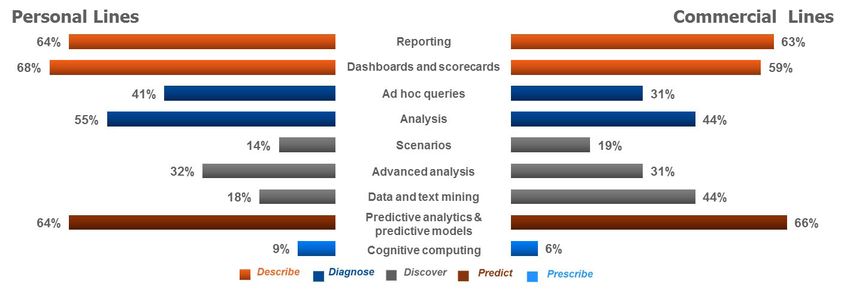

Adoption of BI and Analytics Solutions – Advanced Usage

Figure 2. Adoption of BI and Analytics Solutions – Advanced Usage

Percent of P&C Insurers Citing Source: SMA Research, Data and Analytics in Insurance, n=87

The insurance industry continues to build capabilities with tools under the Describe and Diagnose areas – foundational business intelligence and

dashboards and scorecards. A significant percentage of the industry describes themselves as advanced users, with the reporting category reaching 71%

in 2017. It is important that the industry continue to do this to support day-to-day operations.

Predictive analytics – under the Predict category – saw a significant adoption and capabilities increase in 2016-2017. This is important because the

industry does need to understand the potential or probable outcomes emanating from advanced analysis and new data.

Despite positive developments in BI and predictive analytics, insurers are not focused on building advanced capabilities. 80% of responders indicate

they have no plans or are just starting to plan for cognitive computing, and 37% have no plans for data and text mining. These trends must be reversed

to shift the balance from a heavy reporting focus to innovation.

An SMA Research Report © 2017 SMA All Rights Reserved | www.strategymeetsaction.com 5

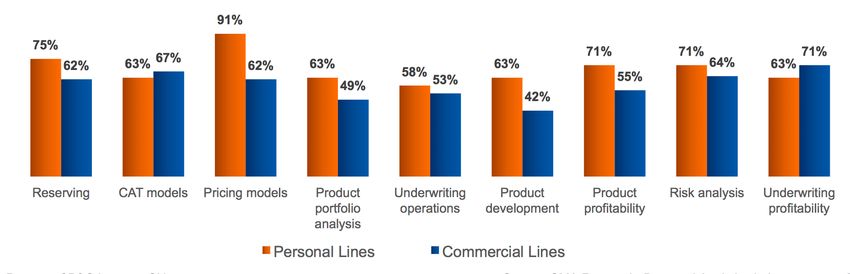

Investment in BI and Analytics – By Personal and Commercial

Figure 3. Investment in BI and Analytics

Percent of P&C Insurers Citing Source: SMA Research, Data and Analytics in Insurance, n=87

Personal lines organizations are a bit more mature in investing in BI and analytics than commercial lines, particularly in the Diagnose category. However,

given the pervasive nature of data standards and core system modernization, personal lines should be shifting investment to the Discover category

particularly in data and text mining to maximize insights from data.

Commercial lines insurers recognize that the data they receive is highly unstructured, and frequently is only captured in core systems for rating

purposes. Because of this, some insurers have found value in investing in data and text mining (44%). Due to the rapidly evolving nature of risk, all

commercial lines insurers will need to make this a priority.

Correlating the advanced usage indicators from the prior slide with the investment indicators above, the lack of capabilities in the Discover and the

Prescribe categories is a self-fulfilling prophecy, that is, you can’t reach advanced capabilities without investing in tools. Insurers, both on the personal

lines side and commercial lines side, must invest in advanced tools or be relegated to only having visibility into the past.

An SMA Research Report © 2017 SMA All Rights Reserved | www.strategymeetsaction.com 6

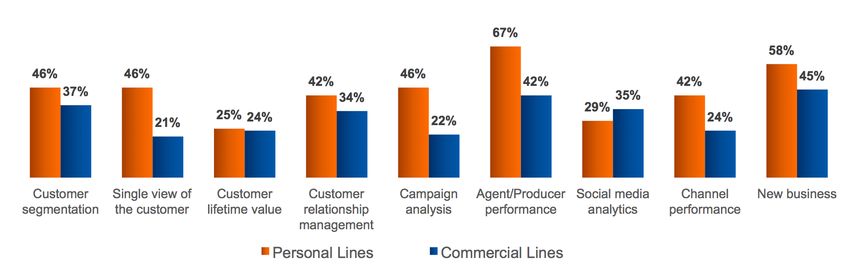

Use of Data and Analytics: Customer-Oriented

Figure 4. Customers, Marketing, and Distribution – In Use/Implementing

Percent of P&C Insurers Citing Source: SMA Research, Data and Analytics in Insurance, n=87

Not surprisingly, personal lines is ahead of commercial lines in terms of using data and analytics for customers, marketing, and distribution. However,

given the urgency around customer expectations and changes in distribution, commercial lines insurers need to focus resources in equal measure to

personal lines.

In terms of the specific data and analytics use cases within insurers, certain uses are dominant and others are under-supported. As shown above, new

business and agent/producer performance are primary in the customer/marketing/distribution group. Investment in these areas are historically higher

than other categories.

The significant point of concern are the gaps – which have been historical gaps – and must be addressed. The most significant gap illustrated above is

the single view of the customer and customer lifetime value. SMA’s 2017 Strategic Initiatives survey showed that the number one initiative is customer

experience. Without a single view of the customer and an understanding of a customer’s lifetime value, it is difficult to execute successfully on customer

experience. Social media analytics is also a gap. Given the wealth of customer information lying within social media, tackling the lack of insight requires

a change in analytics usage.

An SMA Research Report © 2017 SMA All Rights Reserved | www.strategymeetsaction.com 7

Use of Data and Analytics: Risk-Oriented

Figure 5. Actuarial, Underwriting, Product – In Use/Implementing

Percent of P&C Insurers Citing Source: SMA Research, Data and Analytics in Insurance, n=87

Given the historical use of data and analytics by actuaries across reserving, models, and product development, the relatively high levels of usage of

data and analytics are not surprising. Additionally, there is not the significant gap between personal lines and commercial lines that are exhibited in

other areas.

While underwriting operations does not reflect as high a usage percentage as other scenarios for both personal lines and commercial lines, portfolio

analysis and product development are two areas that commercial lines organizations do need to concentrate on. Commercial lines are hyper-competitive,

and commercial lines insurers will benefit from bringing more science into outcomes. Focusing on individual risk pricing is, of course, critical. However,

as commercial lines insurers grow into new risk coverage areas, understanding how portfolios and products are performing is very important.

New sources of data in the connected world will bring even more potential in the future to this area, especially for CAT modelling, underwriting

operations, and risk analysis.

An SMA Research Report © 2017 SMA All Rights Reserved | www.strategymeetsaction.com 8

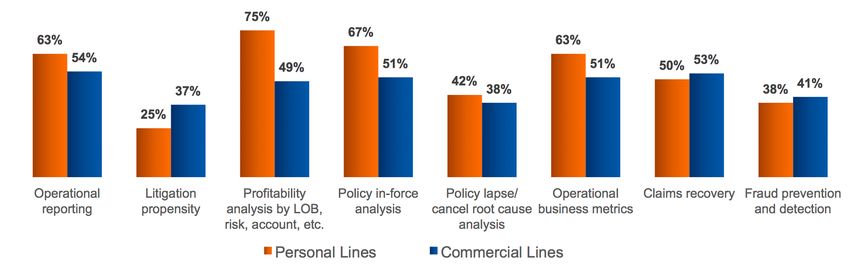

Use of Data and Analytics: Service-Oriented

Figure 6. Policy, Billing, Claims – In Use/Implementing

Percent of P&C Insurers Citing Source: SMA Research, Data and Analytics in Insurance, n=87

Given the high usage of data and analytics by personal lines organizations around operational reporting, profitability analysis, policy in-force analysis,

and operational metrics, there is opportunity for reallocation of resources to claims outcomes. In particular, litigation propensity and fraud prevention/

detection are highly under-invested. The significant point is that improved outcomes in both these areas have a direct bottom-line impact. While

commercial lines would also benefit from increased usage in litigation propensity and fraud, frequency in personal lines would be positively impacted,

and there are more commercially available solutions in both areas for personal lines which can be leveraged for speed to business value.

A correlated survey question in the policy, billing, and claims areas relates to analytics and core technology. Almost 30% of survey responders indicated

that stand alone analytics vendors completely satisfied their needs. Comparatively, about 20%, depending on the core system indicated, responded

that embedded core analytics completely satisfied needs. While insurers get speed to business value with embedded core analytics, it is important that

insurers consider all analytics opportunities to assure a broad strategy of analytics adoption relative to their business initiatives.

An SMA Research Report © 2017 SMA All Rights Reserved | www.strategymeetsaction.com 9

Key Drivers for Success in BI/Data Initiatives – By Size of Insurer

Figure 7. Key Drivers for Success in BI/Data Initiatives

Percent of P&C Insurers Citing Source: SMA Research, Data and Analytics in Insurance, n=87

Insurers under $1billion indicate “data readiness” as the number one driver of success. Because many insurers under $1billion tie core system suite

adoption and initial phases of BI and analytics together, the data readiness success factor is hyper-critical.

Regardless of the size of the organization, two other success factors rise to the surface – new solutions/tools, and talent and human resources

investments. Given the vast quantities of emerging data, only new platforms and tools can successfully deal with it. Traditional analytics skills can handle

foundational BI. But insurers, particularly in the large, complex organizations with multi-layered analytics needs, recognize that new skills are pivotal.

An interesting trend surfaced this year related to organizational structure/design: 31% of insurers under $1billion indicate that organizational structure

is a success factor. Aligning with this is our finding that smaller insurers have developed either enterprise data/analytics organizations (45%) or

teams centralized in IT (55%). These insurers have not developed teams in business units – finding greater impact with centralized organizations.

Comparatively, 38% of large insurers have centralized teams.

An SMA Research Report © 2017 SMA All Rights Reserved | www.strategymeetsaction.com 10Primary Barriers to Successfully Executing Data Initiatives – By Size of Insurer

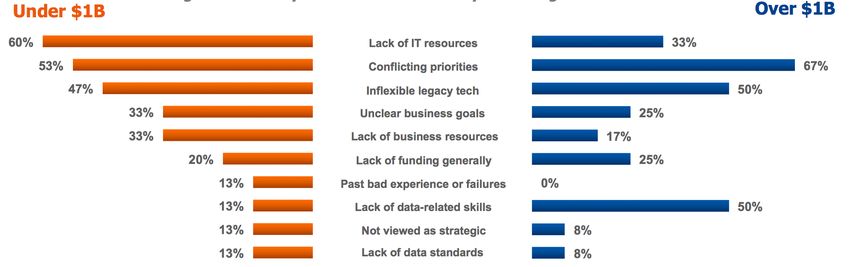

Figure 8. Primary Barriers to Successfully Executing Data Initiatives

Percent of P&C Insurers Citing Source: SMA Research, Data and Analytics in Insurance, n=87

Given that insurers of all sizes believe that new solutions/tools and talent/human resources investments are key success factors, as shown on the prior

chart, it is a significant problem that the number one barrier for insurers under $1billion is lack of IT resources, and 50% of insurers over $1billion (tied

for #2) see the lack of data-related skills as a barrier. Additionally, inflexible legacy technology is a top barrier for all insurers.

Due to the pressing need to move from traditional BI/analytics responses to complex analytics and cognitive computing, all insurers must invest in

talent, and/or partner with technology and service providers who can bring business value in shortened time frames.

Insurers have been addressing inflexible legacy technology for years, and efforts continue with varying degrees of urgency. This constraint on insurers’

abilities to adopt advanced analytics and manage exploding volumes of data must be eliminated, and insurers should reconsider lengthy project

timelines.

An SMA Research Report © 2017 SMA All Rights Reserved | www.strategymeetsaction.com 11Tech Spending, Data and Analytics – By Personal/Commercial

Figure 9. Primary Barriers to Successfully Executing Data Initiatives

Percent of P&C Insurers Citing Source: SMA Research, Data and Analytics in Insurance, n=87

On the average, personal lines insurers spend 8.6% of their total IT budget on data and analytics. For commercial lines insurers, it is 9.3%. However,

the more important story is – are the budgets increasing or decreasing?

Personal lines insurers are more mature in their adoption of data and analytics, largely due to automobile lines that were earlier adopters of analytics.

41% of personal lines insurers are increasing their spending year over year by 6-10%. An additional 41% are increasing budgets by 1-5%. This indicates

that personal lines insurers recognize the value of data and analytics and want to continue to optimize their investments and business outcomes.

Commercial lines insurers exhibit a different picture: 26% indicate they will increase spending by +10%, with 18% increasing by 6-10%, and 29% by

1-5%. Those in the 26% category clearly understand that they have to catch up to demands for new insights and opportunities.

The critical issue across both segments is that spending on data and analytics is not “once and done.” Given the urgent needs, almost all insurers should

be assessing budgets for increases in spending above what the averages suggest.

An SMA Research Report © 2017 SMA All Rights Reserved | www.strategymeetsaction.com 12NEW DATA SOURCES AND EMERGING TECHNOLOGY

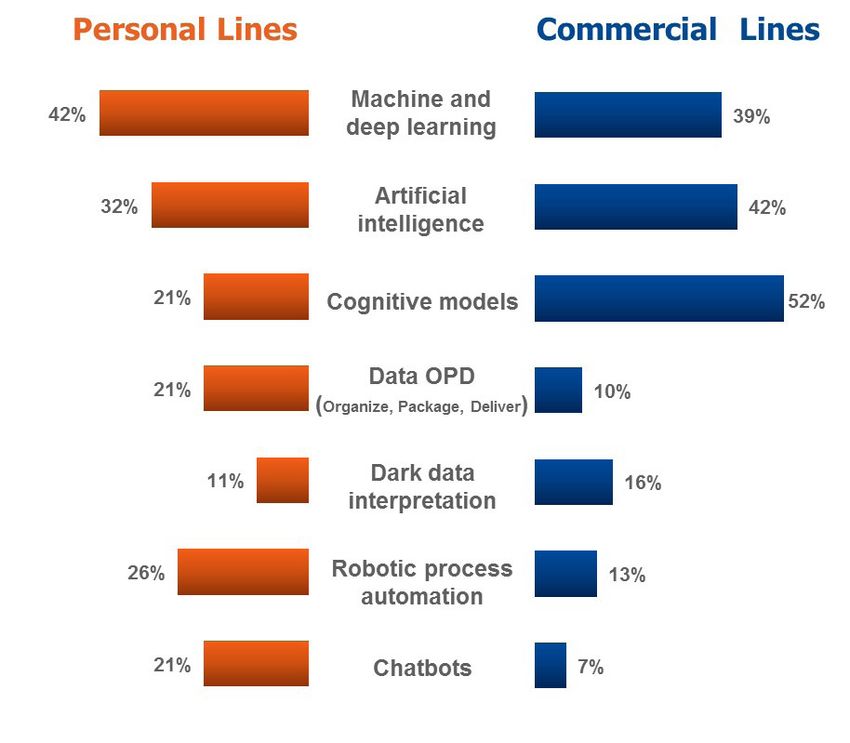

Expected New Wave of Innovation in Data and Analytics – By Personal and Commercial

Figure 10. Expected New Wave of Innovation in Data And Analytics

Given the hype and the significant reality, it is

not surprising that machine and deep learning,

artificial intelligence, and cognitive models are at

the top of the lists for personal and commercial

lines. However, there are some differences.

Commercial lines of business are fraught with

complexity. Because the risks and exposures are

Percent of P&C Insurers Citing

complex, and many underwriters believe that

“art” makes up the decisioning process, it makes

sense that enlightened insurers (52%) believe

that cognitive models which emulate human

thinking would be number one on the list. The

possibilities for process and service improvement

are extensive.

While not at the top of the list, it is significant

that personal lines responders believe that robotic

process automation (26%) and chatbots (21%) are

the next wave. The use cases across the lifecycle of

a personal lines account are numerous, spanning

from new business submission support through

billing questions to claims FNOL and services

execution.

Source: SMA Research, Data and Analytics in Insurance, n=87

An SMA Research Report © 2017 SMA All Rights Reserved | www.strategymeetsaction.com 13Preference for Obtaining New and Emerging Data Sources

Figure 11. Preference for Obtaining New and Emerging Data Sources

The current data explosion is almost audible.

Options for collecting and managing new and

emerging data are morphing as well.

51% of insurers want to collect and manage

their own data via their own systems. While this

might be a preference, given the noted barriers of

legacy technology and IT/data related skills, until

these barriers are eliminated, the reality is that

data volumes will be constrained and insights/

Percent of P&C Insurers Citing

opportunities will be limited to the traditional.

49% of responders indicated that industry

consortiums and exchanges are a preference. For

smaller insurers in particular, these sources are

an excellent choice for securing data they might

not be able to gather by themselves.

Choosing to work with InsurTechs is an excellent

way to mitigate all of the above noted barriers.

However, 60% of responders did not see this as

a preference.

Source: SMA Research, Data and Analytics in Insurance, n=87

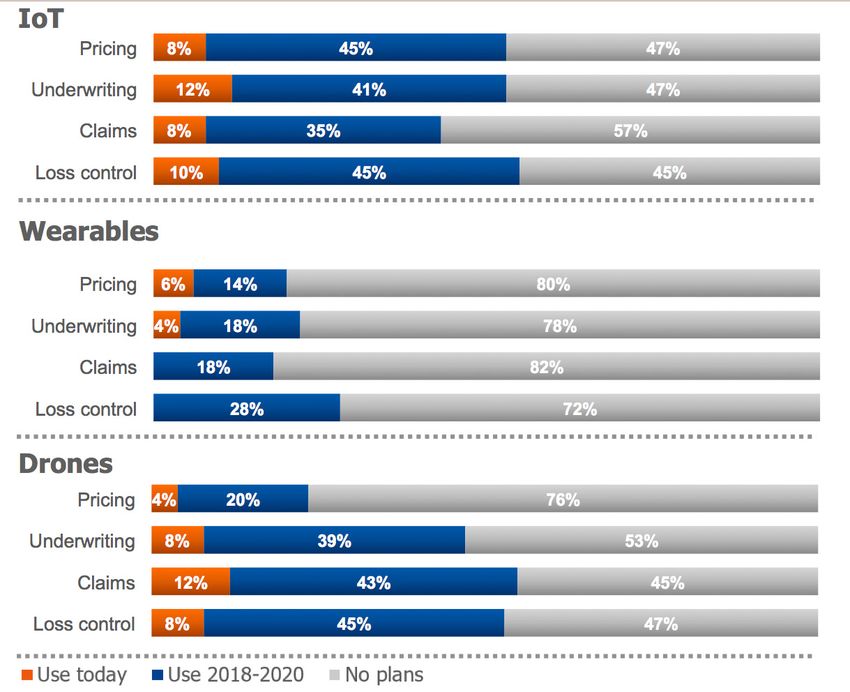

An SMA Research Report © 2017 SMA All Rights Reserved | www.strategymeetsaction.com 14Top Uses of Data from Emerging Tech (Through 2020)

Figure 12. Top Uses of Data from Emerging Tech (Through 2020)

Across the 3 categories of emerging tech,

underwriting is finding the greatest current use of

these new data sources. Underwriting is followed

by claims, and loss control and pricing are tied.

2018-2020, IOT and drones represent the highest

opportunity areas. Wearables have yet to bubble

up into higher opportunity areas for P&C, though

the use cases in commercial lines are meaningful,

particularly for underwriting, claims, and loss

Percent of P&C Insurers Citing

control.

The overwhelming story coming from this survey

data is the very high percentage of insurers that

have no plans for using emerging tech data. The

success factors, barriers, and spending trends

noted in this research foreshadow these results.

Insurers in the “no plans” category should

recognize that there are insurers - largely over $1

billion - that are already utilizing these new data

sources. The gap they are creating is one that

those without plans may find exceedingly difficult

to close. Insurers in the 2018-2020 planning

process must accelerate adoption to assure they

too are not left behind.

Source: SMA Research, Data and Analytics in Insurance, n=87

An SMA Research Report © 2017 SMA All Rights Reserved | www.strategymeetsaction.com 15New SMA Analytics Spectrum with Data Sources BI/Advanced Tools & Big Data Platform

Figure 13. New SMA Analytics Spectrum with Data Sources BI/Advanced Tools & Big Data Platform

DESCRIBE DIAGNOSE DISCOVER PREDICT PRESCRIBE

Dashboards

Ad hoc Advanced Data & Text Predictive Predictive Preventive Cognitive

Reporting & Analysis Scenarios

Queries Analysis Mining Analytics Models Analytics Computing

Scorecards

Geospatial Platforms

AI and Machine Learning

Big Data Platforms

Embedded Chips, Sensors, Drones, Wearables etc.

External Datasets (Risks, Demographics, Geospatial Data, etc.)

Unstructured Corporate Data

Social Media/Web

Transaction Data (Historical, Current)

Source: Strategy Meets Action, 2017

It is intuitive that BI and analytics sits on top of transaction data, both historical and current. The insurance industry has focused on leveraging

operational data, and adoption and spending have likewise been focused on this. However, given the rapid growth in IoT data, new external data sets,

unstructured corporate data, and social media/web data, business and IT initiatives must take a broader approach.

Insurers need to look past traditional data warehouses and data stores to big data platforms that are fully capable of handling the new, data-driven

world and are architected for AI and machine learning. Geospatial platforms will also have increasing importance in the connected world, with use cases

for insurance expanding way beyond risk analysis.

Due to the rapidly accelerating pace of change in consumer expectations and the global business environment, the time horizon for adopting advanced

analytics and cognitive computing, that can derive new opportunities hiding in emerging data, is shrinking. Insurers of all sizes, without plans across all

lines of business, will potentially face insurmountable challenges in the marketplace.

An SMA Research Report © 2017 SMA All Rights Reserved | www.strategymeetsaction.com 16SMA CALL TO ACTION SMA Call to Action for IT Solution Providers

Being a data-driven organization has taken on an entirely different Be clear – Messaging about what your technology can do relative

meaning. Traditional BI, reporting, and analytics are table stakes. Advanced to data and analytics is critical, but be upfront if data and analytics

capabilities are urgently required to compete. Data and analytics are not execution is not part of your solution.

“once and done” nor a science project – they are fundamental capabilities

Partner for capabilities – Solutions that are tangential to data and

that all insurers must have, both in business and IT. The timeline for

execution has condensed because technology is advancing at a rapid analytics will benefit from partnerships that are directly aligned.

pace, and customers expectations and risk complexity have matched that

Create use cases – Develop use cases that identify exactly what

pace. Finding opportunities lying within new emerging data demands

your solution can accomplish to help insurers visualize.

sophisticated technology. Skills are critical and scarce; partnerships with

experts in data and analytics are imperative to jump-start execution Teach – Help insurers learn. Make your data and analytics expertise

horizons. available so that insurers can grow.

SMA Call to Action for Insurers

Accelerate adoption and investment – Business ownership is critical.

Data and analytics must be a top priority supported by robust funding.

“Insurers understand that data and analytics will drive business

Advance skill development and staffing – Hiring plans must include

value. Some insurers are aggressively pursuing execution plans.

analytics skills specifically. Existing staff must be trained to handle

Others are still searching for a path. Fundamentally, however, for

new data and analytics driven needs. Partnering for data and analytics

all insurers, until legacy system barriers are eliminated, results will

capabilities must be an additional tactic to assure appropriate levels

be constrained.” – Karen Pauli, SMA Principal

of capabilities.

“The preponderance of data/analytics activities and investments

Expand plans for new and emerging data – Seek new sources and

are still for structured data. The great potential of harvesting

access, including consortiums. Explore uses, initiate pilots, and then

insights from unstructured data is largely untapped. A wide range

deploy.

of unstructured sources offers new possibilities for text mining and

Explore the big data and geospatial platforms – Experiment and big data usage, including e-mails, underwriter and adjuster notes,

recognize that there is learning in failure. Establish partnerships to images from cameras and drones, social media and many other

gain expertise. sources.” – Mark Breading, SMA Partner

An SMA Research Report © 2017 SMA All Rights Reserved | www.strategymeetsaction.com 17ABOUT HORTONWORKS and combine that with their historical data repositories to drive new insights

that are differentiating, actionable, and timely. Recently introduced to the

Company Overview market as components of HDF are Streaming Analytics Manager and Schema

Registry. This allows developers to easily build streaming analytics apps

Hortonworks®, founded in 2011, is a leading without writing code, increasing developer productivity. Business analysts

innovator in the data industry, creating, can create dashboards and data visualizations for descriptive analytics of

distributing, and supporting enterprise- streaming data. And IT operations teams can manage the entire streaming

ready open data platforms and modern application lifecycle. Schema Registry further enhances streaming application

data applications. The company leverages a business model based on development by providing a shared repository of schemas that can be shared

open source projects such as Apache™ Hadoop®, Apache™ NiFi, and and reused to maximize governance and security.

Apache™ Spark®. Additionally, a network of over 2100 partners worldwide

provides open and connected data platforms designed for enterprise use. Implications for Insurers

Hortonworks solutions and platforms enable customers to build data-

This report has illustrated that data, new solutions/tools, and talent

driven applications that maximize the value of all data, including historical

are key success factors in data and analytics initiatives. Yet, significant

data-at-rest and emerging big data sources such as data-in-motion. The

barriers keep these success factors at bay for many insurers. IoT, drones,

combined expertise, training, and services allow Hortonworks’ customers

wearables, and a host of other emerging data provide the source of new

to unlock transformational value for their organizations across any line of

opportunities. However, without a platform that can handle the massive

business. Hortonworks has a strong footprint in the insurance industry

amounts and variety of data, and deliver integrated streaming analytics

that includes key implementations by leading industry innovators.

capabilities, insurers will find it difficult, if not impossible to compete.

Data and Analytics Offering

Hortonworks’ two foundational offerings are Hortonworks Data Platform

(HDP®) and Hortonworks DataFlow (HDF®). They are, by design, connected STRATEGY MEETS ACTION COMMENTARY

data platforms built to manage and analyze the massive volumes of

Hortonworks was born in and for the big data world. The volume and variety

data from both new and traditional sources – whether in the cloud or

of data is already staggering, and with the pace of change exponentially

on-premises. The HDP, powered by Apache Hadoop, addresses the full

escalating every day, insurers must be able to innovate and find new

needs of data-at-rest (data stored in digital form in a physical location

opportunities, in real time or near real time. Virtually all technology providers

such as a database or data warehouse). HDF is an integrated platform

are seeking ways to deliver value in a big data world, one way or another.

that securely collects, curates, and analyzes real-time data-in-motion.

However, as their heritage, Hortonworks offers a comprehensive, open

The unique combination of HDP and HDF enables companies to collect

source, big data platform with tools designed specifically to drive ease of use

data and capture insights from the furthest reaches of their landscape,

and speed to business value across all lines of business.

Hortonworks, the Hortonworks logo, HDP, HDF, SmartSense, Cloudbreak, and Powering the Future of Data are registered trademarks or trademarks of Hortonworks, Inc. and/or its subsidiaries

in the United States and/or other countries.

Apache, Apache Hadoop, Apache Spark and Apache NiFi are either registered trademarks or trademarks of The Apache Software Foundation in the US and/or other countries. No endorsement

by The Apache Software Foundation is implied by the use of these marks.

An SMA Research Report © 2017 SMA All Rights Reserved | www.strategymeetsaction.com 18ABOUT THE RESEARCH AND STRATEGY MEETS ACTION

Survey Demographics

Figure 14. Size Figure 15. Line of Business

Figure 16. Role

Source: SMA Research, Data and Analytics in Insurance, n=87

An SMA Research Report © 2017 SMA All Rights Reserved | www.strategymeetsaction.com 19SMA Research Methodology Report Usage

The findings and analyses in SMA’s Data and Analytics series and other SMA research The entire content and context of this research report

reports reflect our analysts’ considerations, opinions, and insights, which are based on is subject to copyright protection, with all rights

their experience and research. SMA analysts use a basic research model: reserved. Reproduction or distribution of the report,

Data gathering: A combination of primary and secondary research data is collected in whole or in part, without written permission is not

through surveys, interviews, demos, publicly available materials, and onsite advisory work. allowed.

SMA analysis: The market trends, data, and the information gathered in the research The material and observations contained in this

are analyzed, vetted, and validated. publication have been developed from sources

believed to be reliable. SMA shall have no liability

The report: Findings and insights are documented. Source information for all data

from third parties or opinions is attributed. When formal survey results are cited, as for omissions or errors and no obligation to revise

much information as possible about survey methodology and participants is provided, or update any data or conclusions should new

within the limits of confidentiality. All other material appearing in this report is created information become available or future events occur.

by the analysts and is derived from the sources listed above and SMA’s experience. The opinions expressed in this report are subject to

Figures and charts based on this analysis are labeled either “Source: SMA Research, change without notice.

Data and Analytics in Insurance, n=87” or “Source: Strategy Meets Action 2017.”

© 2017 Smallwood Maike & Associates, Inc. USA.

May not be reproduced by any means without

express written permission. All rights reserved.

An SMA Research Report © 2017 SMA All Rights Reserved | www.strategymeetsaction.com 20About SMA

Karen Pauli, Principal, has comprehensive knowledge SMA is an independent, privately owned, strategic advisory

about how technology can drive improved results, firm that provides business and technology insights, research,

innovation, and transformation within insurance operations. and actionable advice to the insurance industry. SMA blends

Her areas of focus include claims, underwriting, business unbiased research findings with expertise and experience

intelligence and analytics, distribution, and customer to deliver game-changing intelligence. Analysis of industry

management. She has real-world experience with digital trends, best practices, technology investment patterns and

transformation projects, which has given her unique insight levels, and solution availability and fit are segmented by key

into the changing customer and distributor experience in industry interest areas. SMA’s research reports are written

the digital age. By aligning business goals and perspectives entirely by SMA Partners who have extensive experience at

with technology roadmaps, Karen helps insurers to support a variety of top global financial services firms, technology

evolving business models and create competitive advantage. vendors, and consultancies. Clients of SMA include insurers,

solution providers, brokers/agencies, and consulting firms.

Karen can be reached at 1.774.462.7820 or kpauli@strategymeetsaction.com.

Founded in 2007 and Boston-based, SMA offers services

Follow Karen @kpauliSMA on Twitter.

for the Property and Casualty and Life and Annuity industry

segments. SMA’s services are actionable, business-driven,

and research-based – where strategy meets action – enabling

companies to achieve business success. The SMA suite of

advisory offerings includes retainers, research, consulting,

events, and innovation.

Additional information on SMA’s research and services can be

found at www.strategymeetsaction.com.

An SMA Research Report © 2017 SMA All Rights Reserved | www.strategymeetsaction.com 21You can also read