ESTATE PLANNING AFTER THE TCJA TO SAVE INCOME TAX AND ESTATE, GIFT AND GENERATION SKIPPING TAXES

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

ESTATE PLANNING AFTER THE TCJA

TO SAVE INCOME TAX AND ESTATE, GIFT

AND GENERATION SKIPPING TAXES

Houston CPA Tax Expo

Houston, Texas

January 7, 2019

Leonard Weiner, JD, CPA, MBA, AEP®

Leonard Weiner Law, PLLC

5599 San Felipe Suite 900, Houston, TX 77056

(713) 624-4294 / (800) 458-2331 National

LW@LWeinerLaw.com

#222291 / 1/2/2019Disclosure: These materials do not constitute and should not be treated as, legal, tax or other advice regarding the use of any particular estate planning or other technique, device, or suggestion, or any of the tax or other consequences associated with them. How much a client may benefit from any tax planning depends on their unique facts, goals, and choices. Although reasonable efforts have been made to ensure the accuracy of these materials and the presentation, neither Leonard Weiner nor Leonard Weiner Law, PLLC assumes any responsibility for any individual’s or entity’s (both referred to as an “attendee”) reliance on this written information or any oral information presented during the presentation. Because tax law is multifaceted, complex, and has many technical nuances and exceptions, each attendee should verify independently all statements made in the materials and during the presentation before applying them to a particular fact pattern, and should determine independently the tax and other consequences of using any particular strategy, technique, or suggestion before recommending it to a client or implementing it for themselves or for a client. #222291 i

Leonard Weiner, J.D., C.P.A., M.B.A, AEP®

Law Firm of Leonard Weiner Law, PLLC.

5599 San Felipe, Suite 900, Houston, Texas 77056

(713) 624-4294; LW@LWeinerLaw.com

Teleconference via Skype: Leonard.Weiner

CERTIFICATIONS:

Estate Planning and Probate Law - Texas Board of Legal Specialization

Tax Law - Texas Board of Legal Specialization

Certified Elder Law Attorney – National Elder Law Foundation

Certified Public Accountant – Texas

Accredited Estate Planner (AEP®) by the National Association of Estate Planners and Councils

EDUCATION:

Wharton School of Finance (BS)

Georgetown University Law (JD)

University of Maryland (MBA)

AWARDS:

Recognized in 2012 by Law.com as one of “Texas’ Top Rated Lawyers in Estate Planning”

Recognized in 2012 and 2013 by Texas Monthly as an outstanding Estate Planner

Named as a 2011 Texas Super Lawyer for Tax

President's Award - Houston Bar Association - Outstanding Service (1982-83)

Presidential Citation - Houston Chapter of Texas Society of Certified Public Accountants -

Valuable Contribution (1993)

Award for Outstanding Achievement - American Association of Attorney - Certified Public

Accountants, Inc. (2004)

AVVO rated 10 out of 10

*Peer Rated AV Preeminent® for Highest Level of Professional Excellence by Martindale-

HubbellSM from 1987 to 2018

*AV®, AV Preeminent®, Martindale-Hubbell DistinguishedSM and Martindale-Hubbell NotableSM are Certification Marks used

under license in accordance with the Martindale-Hubbell® certification procedures, standards and policies

(www.martindale.com/ratings).

LICENSED TO PRACTICE LAW WHERE APPROXIMATELY 94% OF AMERICA

LIVES: Texas ▪ California ▪ New York ▪ Florida ▪ Pennsylvania ▪ Illinois ▪ Ohio ▪

Michigan ▪ New Jersey ▪ North Carolina ▪ Missouri ▪ Wisconsin ▪ Maryland ▪ District of

Columbia ▪ Virginia ▪ Oregon ▪ Minnesota ▪ Oklahoma ▪ Kentucky ▪ Colorado ▪ Nebraska ▪

Georgia ▪ Alaska ▪ Massachusetts ▪ Connecticut ▪ West Virginia ▪ Montana ▪ Wyoming ▪

Tennessee ▪ North Dakota ▪ Iowa ▪ Indiana ▪ Arizona ▪ South Carolina ▪ Alabama ▪ Louisiana ▪

Washington ▪ Kansas ▪ Arkansas

#222291 iiHELP CLIENTS BY:

Designing trusts, entities and strategies to help medium to high net worth clients in many states

(where I am licensed to practice law) to achieve the following:

Using a trust we designed, a client and his family saved $70 million. The longer they live

the more they may save. Past performance is no guarantee of future success. How much a

client may benefit depends on their unique facts, goals and choices.

Increase wealth and investible assets in a trust where income and appreciation both

compound tax-free at higher pre-tax rates of return than lower after tax rates.

Allow clients to have their cake and eat it, too (1) using a trust to save income tax,

estate tax, gift tax and generation skipping tax (GST) and (2) still allow clients to be

their own trustee and beneficiary. Clients may access and spend trust assets for their

health, maintenance and support, a tax safe harbor.

Litigation to resolve tax controversies.

Estate planning to save time and costs, reduce complexity, income and estate tax, and to

protect clients, their loved ones, and what they own and inherit.

Business planning, including contracts, structuring entities, buying and selling

businesses, and succession, exit and retirement plans to benefit businesses and their

owners.

ESOPs to save taxes, recruit and retain key employees, and sell businesses for higher net

proceeds.

Captive insurance companies to save costs and consultation to avoid their less known

tax traps.

Pre-nuptial or post-nuptial agreements, and income tax saving basis step up spousal

trusts.

Charitable planning, including trusts and private foundations.

Establish self-directed investment IRAs and consultation to avoid their less known tax

traps.

Protect elder clients and their families from losing wealth due to financial abuse from

con artists or dishonest “friends”, relatives, and caregivers and from a divorce from a

second or subsequent marriage. These are growing problems.

A client-friendly Life Insurance Trust which is gift tax-free for larger premiums, estate

and GST tax-free for policy proceeds, easy to use, and often easiest to finance

premiums.

FORMER OFFICES:

National Chair of the Executive Committee of Synergy Summit (which is composed of (a) two

American Bar Association (“ABA”) Sections, (b) two American Institute of Certified Public Accountants

(“AICPA”) Sections, (c) American Association of Attorney – Certified Public Accountants, Inc. (“AAA-

CPA”), (d) National Association of Estate Planners & Councils (“NAEPC”), (e) National Association of

Elder Law Attorneys (“NAELA”), (f) Society of Financial Service Professionals (“SFSP”), (g) the

#222291 iiiPartnership for Philanthropic Planning (“PPP”), and (h) Society of Tax and Estate Professionals (“STEP”)) (2012) Board of Directors Member for the Texas Society of Certified Public Accountants (“TSCPA”) (2009-12) President of Houston Chapter of the Society of Financial Service Professionals (“SFSP”) (2010- 11) National President of the AAA-CPA and former President of its Texas Chapter (1984) President, Texas Chapter of the National Academy of Elder Law Attorneys, Inc. (NAELA) (1996) Houston Bar Association: Treasurer of Section of Taxation (1981-82); Director of Finance Committee (1981-82); Chairman of its Continuing Legal Education Committee (1982-83) MEMBERSHIP: American Bar Association (“ABA”) American Association of Attorney – Certified Public Accountants, Inc. (“AAA-CPA”) National Association of Estate Planners & Councils (“NAEPC”) Synergy Summit Executive Committee Texas Society of Certified Public Accountants (“TSCPA”) and its Houston Chapter WealthCounsel The College of the State Bar of Texas #222291 iv

#222291

ESTATE PLANNING AFTER THE TCJA TO SAVE INCOME TAX

AND ESTATE, GIFT & GENERATION SKIPPING TAXES

I. Introduction to Estate Planning

A. What clients want in their estate plan

1. As much control as possible

a. Of their life and assets during their lifetime

b. Estate goes to whom they want, when they want, and how they want

2. Protection

a. Protect client and loved ones in case of dementia and/or other health issues

b. Protect the inheritance for each beneficiary from:

i. Surviving spouse’s new spouse and their family

A. During surviving spouse’s lifetime

B. If surviving spouse divorces his or her new spouse

C. When surviving spouse passes away

ii. A spouse who divorces the client’s child or grandchild; and

iii. Other predators and avoidable costs

c. Protect beneficiaries who may have special needs and/or problems such as

addiction

3. Legally reduce two different types of taxes for clients and their heirs

a. Income taxes, which are familiar to most clients

b. Transfer taxes (estate, gift, or generation skipping transfer taxes (“GST”)), a

different tax system, which is not as well known to most clients

i. Estate tax now is 40% of the value of the taxable estate

#222291 1ii. Gift tax during lifetime is now 40% of value of a taxable gift

iii. GST (generation skipping transfer tax) for any gifts or inheritance to

grandchildren and their descendants

c. Transfer taxes apply to the amount of an estate or gift which is not “exempt”

from that tax

4. Without sufficient estate tax planning, a family with taxable estates loses

a. 64% Of a taxable estate when the second generation passes away

b. 78% When the third generation passes away

c. Estate tax planning has often been designed to pay the lesser of two different

taxes (income tax or transfer tax)

i. What saves income tax for heirs may increase estate tax and vice versa

ii. Estate tax has historically exceeded income tax

iii. Not today with the new temporary increased exemption

5. Include flexibility in all estate plans when possible because

a. Many estate tax saving techniques work only with irrevocable trusts

b. Changes occur over time

i. In clients’ family and goals

ii. In clients’ wealth, cash flow, and needs

iii. In estate tax law and in non-tax estate law, both of which are

voluminous and technical

c. No one knows in advance

i. When they or their spouse will pass away

ii. What the size of their estates will be when they pass

iii. What the estate tax exemptions and tax rates will be then

#222291 2iv. What the income tax laws will be then

v. Or what the applicable non-tax estate laws will be then

6. Clients say they want to keep it simple

B. The taxable estate or taxable gift

1. Equals the market value of the assets gratuitously transferred less any applicable

exemptions, exclusions, and deductions

2. Historically

a. The estate and other transfer tax exemptions

i. Were low for most of its history

ii. And increases were made in small increments

b. Estate planning to reduce income tax for heirs was often less valuable.

c. Before ATRA passed in 2013, it was more valuable for most clients who

had a taxable estate to save transfer tax than to save the income tax.

3. Today, with the temporary high exemption, estate planning to save income tax for

clients and for heirs is more important for the majority of our clients.

4. To plan for the future, consider the clues that indicate what the estate tax law will

likely be in the foreseeable future.

C. The Landscape

1. The Tax Cut & Jobs Act (“TCJA”) (which is not its official name)

a. The temporary exemption of $11,400,000 for 2019, is adjusted for chain

inflation

b. Until the earliest of the 3 D’s (date, Democrats, and deficits).

i. Date: December 31, 2025

#222291 3ii. When Democrats gain control of Congress and White House after

another regime change in DC.

A. The position of Democrats has been

1. Reduce the estate exemption to $3.5 million per person so

more families would pay estate tax

2. Raise the tax rate to 45% to 50% and for one 2020

Presidential candidate, up to a 75% maximum

3. Eliminate or severely restrict bona fide tax saving valuation

discounts for minority and unmarketable entity interests for

intra family transactions

iii. Will deficits likely ultimately force tax increases?

A. Medicare: projected to run out of money in less than eight years

B. Medicaid: Republicans could not recently significantly reduce it

even with control of Congress and the Presidency

C. Social Security: projected to run out of money in less than

sixteen years

D. Debt interest has increased when actual or projected deficits

increased

E. Defense spending

F. Disaster (hurricane) relief

G. Government costs and our deficit are increasing

H. The debt threat

1. High government (and non-government) debt increases

interest costs which also increases the deficit; and

#222291 42. May consume the credit available which may be needed to

sustain economic growth

c. The CBO said the Tax Cut & Jobs Act is pushing us to an unprecedented

level of debt, heightening the risk of another financial crisis

2. Historical evidence that deficits as a percentage of GDP has its limits before any

economy has serious problems

a. Increasing deficits influenced the passage of ATRA (1/1/13) which

increased income taxes

b. When the last 3 U.S. Presidents were elected

i. Their party also gained control of Congress and

ii. They passed new tax legislation in the first year of their administration

iii. With a simple majority using budget reconciliation instead of 60 votes

to stop a filibuster

c. Our deficits are now the highest percentage of GDP since World War II and

the Great Depression

3. A wounded IRS

a. IRS budget cuts but their workload increased

b. TCJA means much more work for IRS to provide Regulations, change tax

returns, train their staff, etc.

c. IRS’s ability to do its “normal” work will be affected

d. Politicians say IRS needs to do more with less. Critics say they are doing

less with less

D. Some techniques historically used to reduce the taxable estate, which reduces transfer

taxes

#222291 51. Valuation discounts for family entities such as partnerships, LLCs and

corporations

2. Gifts during lifetime to loved ones will use up the estate exemption may be only a

timing difference for some families other than saving transfer tax on appreciation

after the gift.

3. Gifts to charity during or after lifetime to make client poorer to reduce the taxable

estate

4. “Tax burn” from the use of grantor trusts for income tax purposes such as IDGTs,

GRATs, and IRC Sec. 678 Trusts, including BDOTs which are being used more

often

5. Other techniques including QPRTs, SCINs, CRTs, CLTs, BDITs, Graegin loans,

ILITs, and alternate valuation

E. Other valuable estate planning

1. Help clients and heirs increase wealth by compounding income and/or asset

appreciation tax-free to avoid “tax drag”

a. Using grantor trusts for income tax purposes which also increases

i. The equivalent of tax-free gifts which avoid gift tax and GST

ii. Tax burn to reduce the taxable estate

b. Using Roth IRAs in certain circumstances

c. Using GST exempt trusts for tax-free asset appreciation for many

generations even for some non-estate taxable estates

2. Non-tax estate planning

a. Is important to most clients

b. Is understood better by most clients than many tax techniques

#222291 6c. Needs to be integrated with each client’s tax planning

3. Clients should avoid counterproductive “simple” mirage solutions

a. Such as do it yourself tax return or document preparation software

i. Which make it “simple” for clients to make mistakes

ii. Because clients may not know what they do not know before it is too

late

iii. How many of your clients can prepare their own tax returns as well as

you can?

b. Tax law is much more complex than many clients realize until it is too late

F. The current estate tax was eliminated for only one year in its history

1. Earlier U.S. death taxes were eliminated four times and brought back all four

times

2. Clients who invest for the long term should also estate plan for the long term

3. The only two parts of our current transfer tax law (estate, gift and GST) which

changed most over time were

a. The exemption amount

b. The tax rate

II. Tax Basis Estate Planning to Save Income Tax For Heirs After the TCJA

A. Historic Paradigm for Most Clients

1. “A” Trust for the Marital “Deduction”, which is really only a “deferral”

2. “B” or “Bypass Trust” saved estate tax when the surviving spouse passed away

(now called a “Credit Shelter Trust” or “CST”)

a. The “B Trust”, which is in many clients’ wills and trusts, is almost always a

non-grantor trust (“NGT”)

#222291 7b. The B Trust increases capital gains tax for most of those who inherit the

assets in the B Trust when the surviving spouse passes because the B Trust’s

asset basis is carryover, not stepped up to date of death value for trust assets

c. An NGT (non-grantor trust) normally increases income tax during the life of

the surviving spouse. The highest tax bracket begins at $12,500 of trust net

income

i. For 2019 married filing joint, the highest tax bracket begins at

$612,350, a big difference

ii. Remind clients to timely distribute “B” income annually to reduce the

NGT’s income tax

iii. Or advise clients to consider adding provisions in their documents to

create a BDOT to automatically reduce the annual income tax for

NGTs

A. Compressed NGT tax rates cause higher taxes than for

individuals

B. Many other technical income tax disadvantages from using

NGTs

C. See discussion below about NGT income tax disadvantages and

the BDOT potential solution on pages 45 to 59

3. Encourage clients to consider including provisions in their wills and (NGT) trusts

a. So capital gains of NGTs are trust tax income vs. accounting income

b. Which may be distributed as DNI to beneficiaries, almost always saving

income tax

#222291 8B. Basis steps up for both spouses when the first spouse passes in a community property

state. It only increases basis for the deceased spouse in other states

1. When the surviving spouse passes away there is carryover basis for assets in the B

Trust

2. Therefore, no step up in “B” Trust when the survivor passes means

a. Higher capital gains tax and unhappy beneficiaries

b. Client’s decision: to B or not to B?

c. As long as we have the temporary increased exemption, most clients should

use estate planning to

i. Save income tax for heirs, often by stepping up basis, and

ii. Save income tax for themselves, when that is available

C. Portability vs. “B”

1. Compare basis step up (relying on portability) to save a tax up to 23.8% for

capital gains of assets at death of surviving spouse to:

a. Losing the entire estate or 100% to a second or subsequent spouse monster-

in-law or to their family

b. If a client lives in a state where spouses have an elective share, portability

forces a distribution to the “monster-in-law” absent a good prenuptial

agreement or a funded trust to bypass probate

c. Portability increases state estate tax of the surviving spouse in some states

2. Other benefits for the surviving spouse by using the B Trust

a. If he/she develops dementia the trustee can manage the assets

b. The surviving spouse has “cover” to make less or no distributions to or for

their new spouse or the family of the new spouse

#222291 9c. Asset protection for the surviving spouse if there is a later divorce or other

lawsuit

d. Client’s children are protected from new spouse (step parent) and the family

of the step parent when the surviving spouse passes away

e. There may be some potential partial protection from financial elder abuse

for the surviving spouse using a B Trust

3. “B” Trust also provides tax “hedge” protection

a. When the temporary exemption amount decreases such as after a D.C.

regime change.

b. Using algebraic Will and Trust provisions automatically adjusts to new

exemption amounts to save fees when it changes = a good formula clause

c. You or clients should review other automatic adjustments provided for in

their Wills and Trusts which may be counterproductive due to the current

large temporary exemption = a bad formula clause

D. How to Step Up Basis

1. Exhibit 9 lists many options to step up basis

2. The “Magic Wand” General Power of Appointment (“GPOA”) is my favorite

a. “Estate Inclusion” - Assets remain in the B Trust but trust assets’ basis is

stepped up when the surviving spouse passes away

b. Using a GPOA with a double formula dollar amount

i. Appoint as much as will not create or increase any estate tax

ii. Pick the assets which will save the most income tax

iii. Those assets with the biggest difference between basis and value.

c. See illustrations in Exhibits 1, 2, 3, and 4

#222291 103. Since no one knows now how much is needed to save tax when the surviving

spouse passes away until he or she passes

a. The auto-pilot power of appointment formulas protect clients and heirs if

they or their professionals forget or refuse to do something envisioned in

their estate plan such as making a timely disclaimer

b. You may want to explain to clients

i. To consider including in their will or trust the B Trust, the GPOA, and

BDOT provisions, and

ii. To review any automatic adjustments in their current estate planning

documents which may need to be revised due to the temporary

exemptions

iii. Save your copy of the warning

c. Or you may risk a bad result from unhappy heirs, including

i. Increased income tax risk when surviving spouse passes away with no

basis step up

ii. Lost inheritance risk if client relied solely on portability or two simple

“I love you” (“sweetheart”) wills

iii. Increased income tax risk by using a NGT instead of a BDOT which

can convert many NGTs to a more tax efficient grantor trust as to the

beneficiary for income tax purposes

E. When a client passes away recommend the family consider engaging you to prepare a

complete Form 706 (Estate Tax return) with all needed backup evidentiary documents

in case they are ever needed

#222291 111. To make a timely portability election so it is not lost (even if client uses a B trust

for less than the full exemption amount available)

2. No statute of limitations for a shorter “simpler” 706 used only to claim portability

or if no 706 is filed;

a. It is often difficult to later find evidence of needed basis or portability

amount from now if IRS challenges it for income tax basis or ported

amounts

i. Consider cost risk if no documented 706 prepared (even if not filed) if

records or needed information is not available later but is needed later.

ii. Taxpayer has the burden to prove date of death values

iii. There is now the Sower case challenging the portability amount

claimed. 149 T.C. No. 11

iv. May need to prove basis amount for income tax in later years

v. May need to prove portable amount when surviving spouse passes to

avoid estate tax

F. There is no GST portability

1. Many families who will pay no estate tax may benefit by using a GST exempt

subtrust in their Wills or Trusts

2. Clients should review their existing Wills and Trusts periodically since changes

occur in their lives

a. So assets do not pass to the wrong beneficiary(ies)

b. So the right beneficiaries inherit the amounts the client wants each of them

to receive

c. When tax and non-tax decisions laws change over time

#222291 12d. Other things may change such as client’s family, goals and choices

G. Some Additional Portability Risks in Addition to No Portability Benefit Without a

Timely Estate Tax Return

1. Risk losing portability in second marriage

2. Exhibits 5, 6, and 7 list portability and malpractice risks

a. Portability helps some; but rarely is the best planning option

b. The portable amount is not indexed for inflation

H. Non-Tax Estate Planning For All Clients

1. Important to all clients regardless of net worth

a. Risks of simple WROS or POD/TOD accounts

b. A proper Will is a death only plan but better than no Will during life and

afterwards

2. Multifunctional Trust:

a. Fifty potential advantages

b. Coordinate assets and beneficiary designations with the client’s estate plan

III. Transfer Tax Planning

A. For clients who may have a taxable estate now or when they pass away

1. Have increasing net worth now so likely to have a taxable estate when they pass

2. Will have a taxable estate when the temporary exemption amounts decrease

3. May have a larger taxable estate when there is another D.C. regime change

B. The Wealth Building and Preservation Trust has helped clients save transfer taxes

(estate, gift and GST) and save income tax. Includes many good techniques

1. This trust’s strategy includes and illustrates the benefits of many tax techniques

#222291 132. Clients are beneficiary and trustee to make distributions to themselves for their

own health, education, maintenance and support (“HEMS”), a tax safe harbor

a. Some trusts save estate tax but clients during their lifetime lose access, use,

and/or control of their assets – clients become poorer to reduce estate value

b. Other trusts, such as Living Trusts, allow access, control, and use of assets

but do not save enough estate tax and/or GST for many clients

c. This trust does both. It allows clients to have their cake and eat it, too

3. Help clients compare tax saving and non-tax benefits from using different

techniques and strategies

a. Which trust or strategy saves as much tax?

b. Which trust or strategy is as easy to use? Complex to structure, sophisticated

to maximize tax savings, but not complicated for clients to use

c. Ask clients who have a taxable estate but are reluctant to do estate planning

if their concern is

i. Loss of access to their assets. If so, they can plan without losing access

to their assets or

ii. If they want a plan that may also benefit them as well as their heirs

4. Total wealth increases by tax-free compounding in trust of

a. Retained business and investment income during a client’s lifetime

b. As long as trust is a grantor trust for income tax purposes as to the

i. Beneficiary who is the client during their lifetime; and

ii. Who may be the client’s descendant and/or spouse if BDOT provisions

are included

#222291 14c. This trust does not annoy clients paying income tax for their children’s

IDGT trust(s)

5. Tax-free trust compounded asset appreciation for many generations saves estate

tax and GST for many generations

6. Many clients may save estate and gift tax and many save GST even if client has

zero GST exemption

7. The earlier and longer clients use the trust the more they may save

8. Children and charity(ies) wait until clients want distributions made to them

9. Trust gift distributions for children or grandchildren may be free of all taxes so

transfer tax exemption is not consumed and those exemptions may be used to

allow stepped up basis to save future income tax

a. Clients may sell assets at a valuation discount now vs. gift now to the trust

b. Clients may do tax-free swaps to client of low basis assets for high basis

assets (or cash) before or on deathbed when it is a grantor trust for income

tax purposes as to the client who is the beneficiary.

10. Clients retain their current CPA, investment advisors, and financial planner

11. A client-friendly and easy to use life insurance trust with no gift tax for large

premiums, no estate tax for policy proceeds, no notices, no partitions, no separate

accounts needed, and no three year wait to save estate tax

12. How much each client benefits from this or any other strategy depends on their

unique facts, goals, and choices

a. One family is in position to save over $70 million based on client’s current

valuation of their business when the husband and wife pass away

#222291 15b. Past success is no guarantee of future results. How much each client may

benefit depends on their unique facts, goals, and choices.

13. May avoid the Powell case, a very significant recent case

a. No discount for family LLCs or partnerships at death per Sec. 2036(b)(2)

b. All Tax Court judges joined in the decision

i. Estate of Powell v. Commissioner, 148 TC No. 18 (2017)

ii. Commentators say they misread the U.S. Supreme Court decision,

made by the majority, in Byrum decided 45 years ago

c. Bad facts often lead to bad law which too often gets expanded to increase

tax for others.

d. Clients may lock in bona fide tax saving valuation discounts now before

they are eliminated for family transactions. The Treasury was working on

that near the end of the Obama Administration. Democratic legislators were

not in favor of these discounts.

i. The Powell doctrine applied at death; already cited and relied upon in

other cases

ii. Reports are that IRS is raising a Powell attack in estate tax audits

iii. There is a risk that this decision will ultimately be used to include

assets in an estate which clients thoughts were out of their estate at a

higher date of death value than the value at the time when the gift or

sale was made.

e. Some commentators say now is a golden opportunity to lock in bona fide

discounts. Waiting until death is now risky

f. Now we have good tax laws and a friendlier administration.

#222291 16g. The time to fix the roof is when the sun is shining.

h. We can only learn exactly what courts of appeal will decide if a case

applying the Powell doctrine is ever appealed. The Powell family did not

appeal. It is hard to get a tax case to the U. S. Supreme Court unless

different U.S. Courts of Appeal in different geographic circuits decide the

same issue differently. Law is not like math. Law is interpretive.

i. Most Tax Court cases are decided by one Tax Court judge. In Powell, all

seventeen Tax Court judges unanimously expanded the reach of 2036(a)(2).

A speaker at a tax seminar said that the full Court likely joins in an opinion

less than 1% of the time. When all Tax Court judges agree on a new

interpretation it is likely that Tax Court trial judges will not ignore that until

multiple appeals courts in different circuits say that interpretation is not

correct. IRS does not always acquiesce with an adverse decision from a U.S.

Appeals Court.

j. Some commentators say Powell contradicts what the Supreme Court

majority said forty-five years ago about 2036(a)(2) in the Byrum case. Law

Professor Mitchell Gans and Jonathan Blattmacher said in their article in the

prestigious ACTEC Journal that the Tax Court judges erred by conflating

the dissenting opinion in Byrum and treated it as if it were the majority

decision.

k. Maybe as a warning to future litigants, the Powell Court also talked about a

potential double tax. Commentators have criticized both parts of the

decision (expanding 2036(a)(2) and the potential double tax). Not all judges

agreed on the potential double tax issue.

#222291 17l. Jonathan Blattmacher and law professor Mitchell Gans said given the

number of judges who joined in the opinion, it is time to reconsider prior

case law on 2036(a)(2) and to adapt planning to accommodate the new line

of attack that IRS will presumably be pursuing.

m. Steve Akers, JD, CPA, a national speaker and commentator on tax matters,

said, “The law regarding applying Section 2036(a)(2) to FLPs and LLCs

(partnerships) has been turned on its head in Powell v. Commissioner.”

Other commentators have also expressed concern about this case.

n. IRC Sec. 2036 contains a string to bring assets previously gifted or sold

back into the estate at date of death value. Section 2036(a)(2) does not apply

to gift tax, only to estate tax.

o. A client’s risk from this case may depend on

i. The entity interest(s) (such as in an LLC, partnership, or Sub S) that

they own both at the time when they pass away and for three years

earlier and

ii. What rights and duties they had regarding the interests they owned in

those entities as it relates to Internal Revenue Code Section 2036(a)(2)

(“2036(a)(2)”)

p. There are risks for clients and their loved ones to defend against such an IRS

assessment of tax due. An IRS audit, followed by searches for and review

of documents, preparation for an audit and later, oral argument at IRS

Appeals, then a Tax Court case and then appeals to one or two higher courts

will take a long time, be expensive, and cause anxiety and frustration for

#222291 18those who try to defend their position. There is the additional risk of paying

a large amount of tax, interest and penalty.

q. Now that we know the Powell decision, we also know how one may avoid

or mitigate it at the beginning for new entities and new trusts. Just as some

tax planners figured out over time how to avoid most 2036(a)(1) risks, now

the challenge is to avoid the risks of 2036(a)(2) in view of Powell.

r. The Wealth Building and Preservation Trust can help clients avoid this risk.

s. The flipside is that for non-taxable estates the full value of the family entity

may be included at date of death values in the estate and receive a step up in

value. What is good for the goose should be good for the gander.

14. See Exhibit 10 for additional information about the benefits of this trust

C. Some Non-Tax Trust Benefit Opportunities of the Wealth Building and Preservation

Trust

1. The non-tax benefits may help some families more than the taxes saved

2. As the client grows older, this trust may help to protect them from con artists and

dishonest caregivers, “friends”, or relatives

a. Financial elder abuse cost $30 billion in 2016 and has increased each year

b. Too many families learned too late how vulnerable seniors may become

c. Can provide better protection than a revocable Living Trust or a Will

3. If needed, it may protect the client, protect the surviving spouse, and/or protect

the inheritance of the client’s loved ones if the surviving spouse remarries.

a. The divorce rate is highest for spouses over age 50

b. This trust is often better than a prenuptial agreement (“prenup”) for children

and grandchildren who do not want to ask their fiancé for a prenup

#222291 19c. This trust is also often better and less stressful than a prenup for surviving

spouses who remarry

4. Clients may include their spouse as a trust beneficiary without generating estate

tax when either spouse passes

D. Additional Trust Benefits

1. May own, buy, and sell businesses, investments, realty, and other assets

2. Can help eligible clients with a valid captive insurance company increase their

savings

3. Helps to avoid the estate tax lien which adds cost and delay to sell estate realty

4. Includes provisions to create some flexibility in this irrevocable trust

5. This trust works well with most, if not all, other good tax saving techniques

E. Clients often underestimate their estate, gift, and GST tax liability risk

1. Clients are not aware that

a. IRS taxes the market value of their business, not book value or any number

clients think may be reported

b. The estate tax return is signed under penalty of perjury

c. IRS multipliers increase the value and tax of businesses

d. Valuation discounts locked in early save tax

e. The estate tax system is different from the income tax system

f. The estate tax may be much larger than a client’s annual income tax

2. Estate taxes are due to be paid within nine months

a. Many inherited assets are non-liquid like real estate and businesses

b. Families had to sell non-liquid assets quickly and at a loss to pay estate

taxes

#222291 20c. That increased the cost and loss to loved ones

F. How this trust is established

Goal: Sale & Tax Burn to Reduce the Trust Allows Annual Economic Tax-Free

Value of Client’s Personal Asset Bucket So Transfers and Tax-Free Compounding

the Exempt Amount Allows Basis of Income to Increase Wealth

Step Up & Tax-Free Swaps

Sell appreciating assets at a

discounted price Tax-Free

to a Special Dynasty

Grantor Trust

(Grantor as to the client

only)

Exhibit 8: Income tax shifting doubled trust wealth and saved estate tax

Trust established by a third party with their $5,000 so it is estate tax-free to client’s heirs.

One example: Estate tax saved by components: 45% saved by being a Grantor Trust for

only the client (not kids); 23% from the valuation Discount; and 32% from the estate

value Freeze and Leverage of lower AFR interest rate than the IRR of client’s businesses,

realty, investments, and/or other assets transferred.

In the next example: Trust wealth increased double at an annual 5% rate of return and 28

times at an annual 10% rate of return by compounding income tax-free and paying the tax

outside the trust. Total (trust and non trust) wealth increases even though income tax is

paid by the client outside of the trust.

#222291 21G. Gift Tax-Free GRATs

1. A Grantor-Retained Annuity Trust (“GRAT”) is a special type of irrevocable trust

generally used to transfer tax-free a portion of investment profits and appreciation

to children and grandchildren and/or to their trust(s).

2. Clients may isolate losses as much as possible as discussed below so they do not

dilute investment gains.

3. The trustmaker (“grantor”):

a. Can have any number of GRATs simultaneously.

b. May use short-term GRATs to isolate bull market gains from bear market

losses.

#222291 22c. May use a single investment or a single category of assets for each GRAT

so losers are less likely to reduce the gains of winners

4. GRATs are like a tax-free non-recourse loan of assets, such as securities, so all

income and appreciation in excess of the IRC “Sec. 7520 rate computation” pass

income tax-free and free of transfer tax (gift, estate and generation skipping tax

(“GST”)) to beneficiaries or to their trust(s).

5. “Re-GRATs” may be done often so the winners’ gains are taken off the table and

preserved and what is left of any loser investments and the original investment

assets of winners may be GRATed again tax-free.

6. Other assets such as a business ownership interest may be GRATed.

a. If high appreciation is very likely to occur soon; and

b. If the annual payment to the donor (equal to the Sec. 7520 amount) will not

be due before the asset appreciates or converts to cash.

7. Taxpayers may combine a GRAT with any applicable valuation discounts to save

more tax.

8. Families may benefit from using a reverse GRAT and the exemption(s) of one or

more relatives with a lower net worth (who will not owe any estate or gift tax)

such as a parent or grandparent.

a. This shifts profits and appreciation to those relatives tax-free. They may

need or spend some of the appreciation.

b. Those relatives may later decide to gift (or leave in their Will) their

remaining GRAT profits and appreciation to the client’s descendants exempt

of gift tax, income tax, estate tax, and GST.

#222291 239. Since GST exemption may only be allocated at the end of a GRAT term, it is

desirable if a relative who has excess exemption to allocate without any adverse

tax consequence later decides to do that.

a. That will likely also save GST exemption for the wealthier generation to use

later.

IV. Strategies to Save Both Income Tax and Transfer Tax (Estate, Gift and GST)

A. Captive Insurance Company

1. A Captive Insurance Company is an insurance company owned and controlled by

its insured or the owner of the insured. A captive insures property, casualty,

liability and employee health care cost risks of its insured(s).

a. The main reasons to consider forming a captive are the same reasons why

most public companies use them: to reduce premium cost and provide

certain coverage not otherwise available. Any available tax benefits help.

b. Significant tax savings make it more beneficial for medium-sized companies

to establish and operate a bona fide captive.

#222291 242. “Micro-Captives”

a. An IRC §831b “micro captive” (which usually insures privately owned

entities) does not pay income tax on its premium income.

b. The insured operating company, however, may deduct the premiums paid,

which may be at a 21% to 37% tax rate.

c. Under current law, individual owners of a “micro captive” may pay only

15% to 23.8% for dividends from micro captives or for capital gain proceeds

when a micro captive is sold or liquidated.

d. That results in a favorable tax rate arbitrage.

3. IRC §831b “micro captives” are a transaction of interest to IRS but not a listed

transaction.

a. IRS has twice said that §831b micro captives are allowed by law (See IR

2015-19, Feb 3, 2015, and IR 2016-25, Feb. 16, 2016).

b. IRS also has said that problem cases are caused by promoters who sell

clients policies with inflated premium costs to create higher deductions.

i. Those policies are not priced or structured using proper insurance

standards, procedures, and practices.

ii. Because the captive and the insured have common ownership the

promoters attempt to create a tax windfall with an inflated deduction in

one company but no income tax in the other company since the micro

captive pays tax only on its investment (non-premium) income.

iii. The inflated captive premiums offered by promoters are only a mirage

and are not defensible when challenged by IRS.

4. Potential Cost Saving Benefits of a Bona Fide Captive Insurance Company

#222291 25a. Reduced cost of premiums

i. For less cost than retail

ii. A captive may insure part of a risk and buy reinsurance at lower rates

than retail for the balance of the coverage.

iii. A captive realizes the benefits of a mutual company owned by the

insureds.

iv. Better risk managers reduce losses and premiums.

A. Owners of captives are normally better risk managers than

employees of the insured.

B. Successful business owners are normally better risk managers

than others.

v. Clients can adjust coverage from other insurers of certain risks with

larger deductibles to save premiums paid to that insurer, which

deductible may be insured by a captive to save costs.

vi. The insured saves the amount of profit on premiums charged by a

retail insurance company.

vii. A captive can charge less premiums because it retains all of the cost

saving from better risk management compared to what occurs with an

insured buying retail insurance.

viii. No marketing or sales costs for captives.

5. A captive may allow the insured

a. To obtain coverage not otherwise available or not available in some

geographic areas at a reasonable cost such as

i. Earthquake insurance.

#222291 26ii. Mold coverage.

iii. Black Swan risks, which are those with a very low probability but a

big loss potential which often have much higher retail mark ups.

iv. To give the insured more control to reduce defense costs and the final

settlement amount.

b. Each captive may retain the client’s investment advisor and CPA.

c. Owners may be able to also save estate tax on the captive’s value when they

use the Wealth Building and Preservation Trust (i.e., the trust owns both the

operating company and the captive).

d. If the children of the owner of the insured or their trust(s) own the captive

but the insured (operating company) is owned by their parents, then the

captive cannot save income tax on premiums.

e. Beware of promoters touting policies with inflated premiums to artificially

increase tax benefits. Due diligence at the beginning is important.

6. Federal Income Tax Benefit to Help Build Reserves and Offer Coverage

Saved Tax** Annual

Premium 37% Operating Cost* Benefit Each Year

$400,000 $148,000 ($55,000) $93,000

$600,000 $222,000 ($55,000) $167,000

$800,000 $296,000 ($55,000) $241,000

$1,000,000 $370,000 ($55,000) $315,000

$1,200,000 $444,000 ($55,000) $389,000

$2,000,000 $814,000 ($55,000) $759,000

*Approximate cost. Costs may change over time

**Based on current law for pass through entities

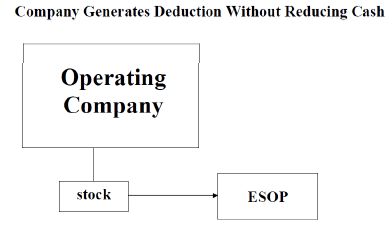

#222291 27B. Employee Stock Ownership Plan (“ESOP”) is a tax qualified retirement plan for

employees. An ESOP invests in and owns all or part of the employer entity and

provides benefits for the employer, its owner(s), and the employee(s).

1. ESOPs are often the best buyers of the business for a higher sale price with faster

payment and with better security to receive full payment over time compared to

other non-strategic buyers.

a. Many sellers of privately owned businesses must agree to receive

installment payments over time to sell their business.

b. Sometimes loans can be used to accelerate cash payments to the owner.

However, the lender may require the seller to personally guarantee payment

of the ESOP loan.

2. Helps recruit and retain highly skilled personnel in short supply who like this

fringe benefit

a. ESOPs provide “golden handcuffs” to recruit and retain valuable employees

which increases the businesses’ value for a sale.

b. To maximize the value, the business should be able to operate profitably

without the owner (who will retire).

c. Employees are secure that there is a succession plan and, better yet, they are

part of it.

d. A part-owner employee is more productive than a non owner employee.

3. The most used scenario:

a. An owner may sell business to an ESOP for cash taxed as a capital gain.

b. The company deducts cash paid to the ESOP which is used to pay the sales

price to the client seller.

#222291 28c. When an ESOP owns all of an S Corporation or another pass through entity

(such as a partnership) the entity has extra cash to pay the note to the owner.

The extra cash is the amount the owner would have received as any salary

(net of withholding) and employee benefits (cost) plus what he or she would

have paid for income tax as an owner and/or employee if the owner had not

sold and retired.

d. If the owner sells to an ESOP his or her stock in a C Corporation, he or she

may invest the sales proceeds in special debt securities to avoid capital gain

per IRC Sec. 1042. That allows the owner to defer capital gain income tax-

free until the basis of those securities is stepped up at the owner’s death so

no tax is due.

4. A less frequently used ESOP alternative when a business is sold years after the

ESOP is established instead of using a relatively new ESOP to make the sale:

#222291 295. Some improvements for ESOPs in TCJA and in a good economy:

a. An improving economy increases the sale price for owner.

b. The 21% tax rate makes a C corporation more attractive to some owners.

c. If currently a C corporation:

i. The owner may sell the corporation on or before December 31st to the

ESOP tax-free by deferring the capital gain with IRC. Sec. 1042

securities until he or she passes away, at which time the step up in

basis eliminates that tax.

ii. On January 2 of the next year, the company has the option to convert

to an S corporation.

A. If all S stock is owned by the ESOP, the S corporation pays no

income tax because the ESOP is tax exempt.

B. Cash increases in the company for all of what would have been

previously paid for the owner’s income tax, salary, and benefits.

C. The seller can be paid faster since the S corporation will have

more cash.

iii. A corporation changing from a C to an S need not go from cash basis

to accrual if gross receipts were less than $25 million.

#222291 30iv. If not, the recognition period has increased to six years.

v. If an S corporation switches to a C corporation before the sale, the

owner must wait 5 years for the corporation to again become an S.

vi. The cost of converting an “S” to a “C” and waiting 5 years to become

an “S” at 21% is normally low compared to the capital gain saved

using the special 1042 debt securities.

C. Charitable Remainder Trust (“CRT”)

1. A Charitable Remainder Trust (“CRT”) is a tax-exempt irrevocable trust that will

provide income to the trustmaker or his or her designee for life (or a different

allowable “term”) and the assets remaining at the end of the term pass to one or

more charities of the trustmaker’s choosing.

2. CRTs may save and defer income tax and save estate tax. One potential use is

avoiding an income spike in one year from a large sale of a business (interest) or

realty project.

a. Tax is saved by spreading and deferring the gain over many years at lower

annual income tax rates instead of reporting all income in one year.

b. The business or realty must be donated to the CRT before a sales contract is

made so the CRT may sell it.

3. Other Income Tax Saving Possibilities Using A Charitable Remainder Trust:

a. Donate appreciated and/or low basis eligible property which has appreciated

to defer income recognition.

b. Rebalance an investment portfolio tax-free in the CRT.

c. Income and appreciation compound retained income tax-free in the trust.

#222291 31i. Income is paid to the client or other trust beneficiary as fast or as slow

as the client designates in advance.

d. The charity may be client’s private foundation.

e. Income distribution order: ordinary first, then capital gain, and tax-exempt

last.

f. A higher IRS (AFR) interest rate at the beginning of a GRAT term generates

a higher remainder value which increases the charitable deduction.

g. The tax deduction money saved by making the charitable contribution of

assets to the CRT may be used to purchase life insurance in a separate trust

for the owner’s loved ones which makes policy proceeds free of income tax

and free of estate tax and GST. This often results in more money for the

client, their beneficiary(ies), and for the client’s charity; a WIN, WIN, WIN.

h. A CRT may reduce an IRA’s required minimum distributions (“RMDs”).

The CRT becomes the IRA beneficiary and the designated recipient(s) such

as the client’s children or grandchildren (not the client) become the CRT

beneficiary(ies) who receive distributions annually from the CRT (from the

distributions received by the CRT from the IRA).

i. This may allow the IRA funds to stretch tax-free longer than allowed

by law for an IRA.

ii. There has been a proposal for Congress to end the IRA stretch after

five years for all IRA beneficiaries other than the IRA owner or their

spouse. Using a CRT will be a valuable option if that proposal

becomes law.

#222291 32iii. A longer stretch is also valuable for children and grandchildren as

CRT beneficiaries.

i. Federal income tax (and often state income tax) may be saved and/or

deferred for clients living in states which also have a state income tax.

j. Each client’s investment advisor and CPA may be retained for the CRT.

V. Using Estate Planning to Save Income Tax

A. Private Placement Life Insurance (“PPLI”) can make investment income tax-free for

client

1. Client may ultimately borrow the cash value of the policy tax-free

2. When client passes the policy proceeds may be tax-free and used in part to repay

the tax-free cash loan advanced to client

B. Planning to Save Heirs Income Tax

1. To the extent that the temporary exemptions save estate tax,

a. Create estate inclusion of assets to get basis step up for incomplete gifts in

trust by including a limited power of appointment which also saves gift tax

b. Reverse estate planning using General Powers of Appointment for named

trust beneficiaries who are older with the amount of their exemptions which

will not be needed to save estate tax

c. A Community Property Trust created for clients not living in a community

property state

i. For clients in non-community property states who want to get a step up

in basis on both spouses’ assets when the first spouse passes away

ii. For Texans, it is easy to convert (transmute) separate property into

community when both spouses are alive

#222291 33C. Section 2038 Estate Marital Trusts – causes estate inclusion which causes basis step up

for clients in most states with separate instead of community property

1. Grantor (the “Grantor Spouse”) contributes assets to a trust for the benefit of his

or her spouse (the “Beneficiary Spouse”). The Grantor Spouse can be the sole

trustee or co-trustee of the trust.

a. The trustee has the discretion to distribute income and principal only to the

Beneficiary Spouse for such spouse’s lifetime. Upon the Beneficiary

Spouse’s death, the trust assets pass to the Beneficiary Spouse’s estate

b. The Grantor Spouse retains a right to terminate the trust prior to the

Beneficiary Spouse’s death. Upon such termination, the trust assets must be

distributed outright to the Beneficiary Spouse.

c. The Grantor Spouse retains the power, in a non-fiduciary capacity, to

reacquire or “swap” the trust corpus by substituting other property of an

equivalent value

2. The trust does not provide for distribution of all income annually or for the

conversion of unproductive property as would be required for a general power of

appointment marital trust or QTIP Trust. See Treas. Reg. §§20.2056(b)-5(f)(4)

and 20.2056(b)-5(f)(5)

a. The trust should qualify for the gift tax marital deduction because the trust

funds are payable only to the Beneficiary Spouse’s estate, and thus the

spouse’s interest is not a nondeductible terminal interest under §2523(b).

See Treas. Reg. §§25.2523(a)-1(b)(3), 25.2523(b)-1 and 20.2056(c)-

2(b)(1)(iii)

#222291 34b. The contribution of assets to the trust should be a completed gift

notwithstanding the Grantor Spouse’s right to change the manner or time of

enjoyment of the assets because the only beneficiary of the trust is the

Beneficiary Spouse or the estate of the Beneficiary Spouse. See Treas. Reg.

§25.2511-2(d)

c. During the lifetime of the Beneficiary Spouse, the trust will be treated as a

grantor trust for income tax purposes with respect to the Grantor Spouse

under section 677(a) which provides, in pertinent part, that the “grantor shall

be treated as the owner of any portion of a trust . . . whose income without

the approval or consent of any adverse party is, or, in the discretion of the

grantor . . . may be distributed to . . . the grantor’s spouse” (§677(a)(1)) or

“held or accumulated for future distribution to . . . the grantor’s spouse.”

§677(a)(2)

i. Because the Beneficiary Spouse and his or her estate is the sole

beneficiary of the lifetime and the remainder interests, grantor trust

treatment should be as to all of the assets in the trust and as to both

income and principal. Treas. Reg. §1.677(a)-1(g)

ii. Thus no portion of the trust’s income should be taxable as a non-

grantor trust. However, in order to ensure grantor trust status as to all

of the assets and tax items of the trust, practitioners might consider

having the Grantor Spouse retain the power, in a non-fiduciary

capacity, to reacquire the trust corpus by substituting other property of

an equivalent value. (See §675(4)(C) and Rev. Rul. 2008-22, 2008-16

I.R.B. 796)

#222291 35iii. If the Beneficiary Spouse dies first, the trust assets will be payable to

his or her estate and thus are includible in the gross estate under

section 2031 and entitled to a “step-up” in basis.

3. If the Grantor Spouse dies first, the trust assets will be includible in their gross

estate under section 2038. It provides, the gross estate will include the value of all

property “[t]o the extent of any interest therein of which the decedent has at any

time made a transfer . . . by trust or otherwise, where the enjoyment thereof was

subject at the date of his death to any change through the exercise of a power (in

whatever capacity exercisable) by the decedent alone or by the decedent in

conjunction with any other person (without regard to when or from what source

the decedent acquired such power), to alter, amend, revoke, or terminate, or where

any such power is relinquished during the 3 year period ending on the date of the

decedent’s death.” See §2038(a)(1)

4. Safest to be used by clients who have a good marriage

D. Deathbed income tax-free swaps with irrevocable grantor trust as to the client to get

1. Step up, such as with the Wealth Building and Preservation Trust

2. Exchange cash or high basis assets to the trust for low basis trust assets to the

client to be stepped up at his or her death. That saves income tax for heirs

3. For clients who save all or part of their estate tax exemption to be able to get basis

step up

E. Distribute non-grantor trust income including capital gain to save non-grantor trust tax

(with rapid bracket increase beginning at $12,500)

F. Types of Assets which benefit most from basis step up

#222291 361. Commercial real property limited partnership interests when partnership liabilities

exceed tax basis sometimes referred to as “negative basis” even though basis

never goes below zero;

2. Investor/collector-owned artwork, gold, and other collectibles;

3. Low basis stock or other capital asset;

4. Patents;

5. Roth IRA assets;

6. Qualified Small Business Stock (QSBS)

G. Additional Income Tax Planning Using Estate Planning Techniques To Save Tax For

Clients

1. Recommend that clients trusts allow the sprinkling of income in trusts or entities

to family members who have a lower income tax rate

2. Use non-grantor trusts (NGTs) to own part of pass through entities, one for all

beneficiaries or one for each beneficiary subject to interpretation of the new

proposed Section 199A and Section 643 proposed Regulations; see discussion on

pages 59 to 62.

a. So each NGT gets the benefit of the 20% deduction

b. Income can be distributed annually (DNI) to reduce taxes due to the

beneficiary’s tax bracket

c. Sell a minority or non-voting interest which is not readily marketable to an

NGT at a bona fide discount on a 9 year balloon note for principal and

interest (at the midterm applicable federal rate)

d. Gift 10% or 11% seed money to the new NGT

#222291 37You can also read