EVOLUTION OF RUSSIAN GAS SUPPLY TO EUROPE: CONTRACTS AND PRICES - SERGEI KOMLEV HEAD OF CONTRACT STRUCTURING AND PRICE FORMATION DIRECTORATE

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

EVOLUTION OF RUSSIAN GAS SUPPLY TO EUROPE:

CONTRACTS AND PRICES

SERGEI KOMLEV

HEAD OF CONTRACT STRUCTURING AND PRICE FORMATION DIRECTORATE

GAZPROM EXPORT

34th WS2 GAC

April 23, 2021

1

MAJOR TRENDS

1. Competition on the European Gas Market

LNG as Russian Pipeline Gas Main Competitor

2. Role of the Long-Term Contracts

Rational for Long-Term Contract: Security of Supply and Demand

plus the Superior Trading Opportunities

3. Evolution of Pricing Mechanisms

From Oil Indexation to Hub Pricing

Extreme Price Volatility

2EU GAS MARKET HEALTH METRICS (ACER*), 2019

Number of

550% 440% 330% 220% 110% 0% sources Over the last 10 years EU made the

Be-Lux NL NO QA OT 7 enormous progress in competition

- RSI, % enhancement on its natural gas market.

- HHI

- Threshold

Spain AL USA QA OT 11 Competition has strengthened both in terms

values France NO RU NL OT 12 of increased number of sources of supply

Netherlands NO D.P. RU OT 9 and the single supplier’s role reduction. Only

Italy RU AL QA OT 13 5 countries out of 22 surveyed by ACER

Greece RU TR AL OT 9 have less than three suppliers. Residual

United Kingdom D.P. NO QA OT 12

supplies index (RSI) is close to the EU Target

Poland RU D.P. DE OT 7

with the exception for several East and

Croatia RU D.P. AT 3

Germany RU NO NL OT 7

Central European countries. In 2018

Lithuania NO RU USA 3 Gazprom took legally binding commitments

Ireland UK D.P. 2 to address the EU Commission's concerns

Portugal NG USA AL OT 5 over its dominant position in these counties.

Hungary RU AT D.P. 4

Austria RU DE D.P. 3

ACER Gas Target Model

Slovenia AT RU D.P. 3

DK-SW D.P. DE 2 Metric Threshold values

Romania D.P. HU RU 4

Estonia RU LT 2 HHI HHI ≤ 2000

Bulgaria RU GR D.P. 4

RSI RSI ≥ 110%

Latvia RU LT 2

Finland RU 1 Number of sources Q≥3

10000 8000 6000 4000 2000 0 0% 20% 40% 60% 80% 100%

*The European Union Agency for the Cooperation of Energy Regulators 3

Source: ACER Annual Report on the Results of Monitoring the Internal Electricity and Gas Markets in 2019CONCENTRATION OF THE SUPPLIES TO EUROPE (HHI INDEX)

SUPPLIES TO EUROPE FROM THE THIRD COUNTIES SUPPLIES TO EUROPE INCLUDING INTERNAL PRODUCERS Herfindahl–Hirschman Index (HHI) is a

HHI i* 4241 4147 3335 3120 HHI t** 1919 1948 1745 1702 measure of the size of the suppliers and

100% 100% an indicator of the amount of competition

Others 6,9% 6,4% 5,7% Others

7,2% 14,6% 14,2% 14,9% 14,0%

2,2% 2,4% 3,6%

90% among them.

90% 2,7% Russia 6,1% 3,5% 3,4%

4,0% 4,0% 6,9%

Azerbaijan

2,1%

4,4% 4,5% 80%

4,2% 4,0% 5,1% 4,1%

4,7%

HHI points to ‘moderate concentration’ of

7,7%

7,2%

5,7% 5,6%

Netherlands 70% 8,6% 8,4%

5,4% 5,6% the European gas market when all the

Nigeria 80% 6,5% 6,6%

5,1% 7,8% 60% 7,9% 7,6% suppliers are taken into consideration.

USA 7,3% 7,9%

Russia 70% 15,9% 14,9% 8,9% 50% European gas market still remains in ‘high

9,2% 23,5% 22,7%

Qatar

40%

20,8% 22,0% concentration’ zone when domestic

USA 60% 10,8% supplier are taken out. However, HHI

10,9% Algeria (incl. LNG) 30%

index slashed nearly 1000 points over the

Qatar 20%

50% 62,4% 61,9% UK 33,9% 35,1% 33,4% 31,8% last 4 years and approaches ‘moderate

55,2% 52,8%

Algeria (incl. LNG)

10% concentration” terrain due to the LNG

Norway

40% 0% inflow.

2017 2018 2019 2020 2017 2018 2019 2020

Gazprom Gazprom With a declining indigenous production

LNG will become a main competitor to

HHI threshold values European Commission U.S. Department of Justice and FTC Gazprom.

Low concentration HHI < 1000 HHI < 1500

Introduction of carbon tax on the

imported gas puts LNG in a less

Moderate concentration 1000 < HHI < 2000 1500 < HHI < 2500 advantageous position in comparison

High concentration 2000 < HHILESSONS FROM 2020

• LNG spot deliveries are

extremely price sensitive.

20% When prices on the European

18%

gas market dropped to below

$2/mbtu most LNG suppliers

16%

14%

12% were unable to return their cash

10% costs.

8%

• Being a low-cost producer,

6%

4%

2% Gazprom was only moderately

0% affected by a prices meltdown

January February March April May June July August September October November December

and managed to uphold

deliveries when flows of flexible

LNG left Europe and created

gas deficit in H2 2020.

PJSC Gazprom LNG

Source: IHS, Gazprom 5LONG-TERM CONTRACTS RETAIN THEIR DOMINANT POSITION IN EUROPE

Term versus Spot Sales in LNG Trading

• Third Energy Package gave

suppliers a formal opportunity to

export the entire volume of gas on

a spot basis. However, this

opportunity remained unclaimed.

And this is not just a matter of the

“heritage” of the previously

concluded legacy LTCs, which, by

the way, could be terminated by

mutual agreement of the parties.

Parameters of the global portfolio of pipeline contracts

• LTCs facilitate development of the

50

Duration of entering into force contracts

30 European forward and futures

40 and weighted average contract length in world portfolio 28 markets by providing them with

backup physical liquidity.

30 26

Monetization of LTCs is a specific

years

bcm

20 24 feature of the European forward/

10 22

futures market that has a distinct

physical nature, not a financial

0

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

20 nature like in the United States.

< 10 years 10 - 20 years 20 years and more Weighted average length (world portfolio)

Source: IHS Waterborne, Cedigaz 6LONG-TERM CONTRACTS RECEIVED ADDITIONAL SUPPORT FROM TRADING

Rational for long-term S&P contracts

Assumes long-term offtake obligations taking into account the

prospective market needs. Reselling significant gas volumes on the

Buyer/importer

domestic market only on a short-term basis is impossible. Contract

Security of demand duration affects the efficiency of trading operations.

Is interested in guaranteed sales for long-term planning and long-

Seller/exporter

term borrowing.

Choice between term and spot deliveries depends on the

Buyer/importer

availability of gas in the market.

Security of supply

The LTC reduces the risks of supply interruptions. The exporter

Seller/exporter assumes obligations taking into account the long-term capabilities of this

resource base.

Source: Compiled by the author

7FROM PRICING BASED ON GAS-ON-SUBSTITUTE TO GAS-ON-GAS COMPETITION

EUROPE PRICE FORMATION 2005 TO 2019 • Europe is the region where

the most significant changes

in price formation

mechanisms have taken

place.

• In the total consumption there

has been a broadly

continuous move from oil-

indexation to pricing based on

gas-on-gas competition since

2005.

• Share of oil-indexation in

Europe dropped from 78% in

2005 to 22% in 2019.

Source: Wholesale Gas Price Survey 2020 Edition/ A Global Review of Price Formation Mechanisms 2005 to 2019, June 2020

8PRICE FORMATION MECHANISMS IN GAS IMPORTS TO EUROPE

GAS IMPORTS TO GAS IMPORTS TO

THE EUROPEAN FAR ABROAD THE EU-27 + UK

4,1%

0,0% 100% 3,4% 0,0%

5,6% 4,3% 7,2%

9,0% 12,3% 10,1%

26,3% 80%

30,7%

44,4%

34,1% 58,9% 48,9%

54,3% 61,3%

55,9% 73,9%

60%

40%

68,1%

60,3%

53,6% 51,4%

46,8%

41,1% 20% 38,5%

34,1% 35,3%

26,1%

0%

2016 2017 2018 2019 2020 2016 2017 2018 2019 2020

Oil-indexed Hub-indexed** Fixed price

* Norway considered as internal supplier

** From 2020 г. includes quasi-oil indexation and fixed price based on year-ahead forwards

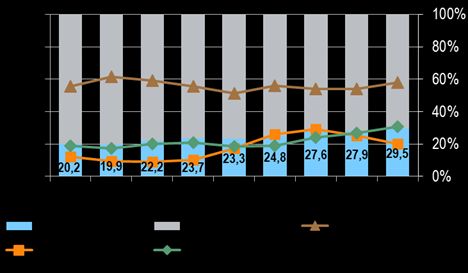

Sources: IEA, IHS Markit, Gazprom Export estimates 9GAZPROM EXPORT SALES PORTFOLIO COMPOSITION BY PRICING MECHANISMS

FOLLOWS THE EUROPEAN TRENDS

10CORRELATION OF GAS HUB PRICES WITH OIL PRICES IS STILL STRONG

Correlation between Year-Ahead Price on TTF and Oil indexes

Y-A Mid Price - Y-A Mid Price - Y-A Mid Price - Y-A Mid Price -

R-coefficient

Brent Brent 3-monthMA Brent 6-monthMA Brent 9-monthMA Why, despite significant shift

2010-2013 88% 90% 87% 86% away from oil indexation, natural

2014-2015 91% 89% 89% 93% gas prices retain strong

2016-2018 82% 89% 89% 84%

2019-2021 84% 77% 67% 56% correlation with oil prices?

2010-2021 91% 92% 91% 90%

Oil-indexation departed from the LTCs but inter-fuel competition cannot cease to exist Although oil-indexation has lost

its dominance, inter-fuel

competition still plays an

important role in pricing but

setting up a price corridor for

natural gas between oil products

and coal on an energy parity

basis*

*For discussion see: Komlev S. Foundations of Natural Gas Price Formation/ Misunderstandings Jeopardizing the Future of the Industry. Anthem Press. NY. 2020

11HYPER VOLATILITY OF DAY-AHEAD AND MONTH-AHEAD PRICES

Uncomfortable questions remain*.

Average Deviation of TTF Forward Prices from the TTF Day- Ahead Price Index

• Why integration of regional gas

market does not lead to the formation

of one price similar to global

benchmarks typical for other

commodities?

• What makes prompt prices so

volatile?

• What is behind the diversion of the

forward prices with different

longevity?

Source: Bloomberg

*For discussion see: Komlev S. Foundations of Natural Gas Price Formation. Misunderstandings Jeopardizing the Future of the Industry. Anthem Press. NY. 2020.

1213

You can also read