Falling Oil Prices: Past, Present and Future - Kent Bartell, CFA

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

March 2015 Falling Oil Prices: Past, Present and Future Kent Bartell, CFA®

Falling Oil Prices:

Past, Present and Future

The surprise drop in oil prices was the biggest economic story of 2014. After years

of $100 barrels of oil, the price plummeted by roughly half during the second half of

the year. This was a stunning turn of events for U.S. consumers, who had become

accustomed to paying $4 for a gallon of gasoline.

The economic implications are significant. Despite efforts to develop alternative sources

of energy, oil is the world’s primary commercial energy source and will likely remain

so for decades to come. Historically, since World War II, the strongest bursts of global

economic growth have coincided with relatively cheap oil. Likewise, high oil prices have

[Photo of

often brought economic stagnation and at times even spurred a recession.

author, if

available] The correlation of low oil prices and economic growth combined with recent price

volatility have caused many to ask, “What will oil prices do next?” While no one has a

definitive answer, this paper explores the possibilities over the upcoming years as well

Kent Bartell, CFA® as the likely impact on the U.S. economy and investments.

kent.bartell@standard.com

www.stancorpadvisers.com

The recent price decline should not be viewed as a solitary event; rather it is a

continuation of a power struggle between oil producers and consumers that has lasted

for more than 50 years. With that in mind, let’s explore oil’s past.

About Kent Bartell

Kent has more than 20 years of

Oil’s Past

experience in portfolio management Humans have been extracting oil from the ground for most of recorded history, primarily

and financial services. Kent specializes for kerosene lighting and construction purposes. In fact, asphalt was used more than

in the analysis of individual equities 4,000 years ago for the construction of the walls and towers of ancient Babylon.

for client portfolios and has expertise

in defined benefit pension plans. In While oil retained its value for lighting and construction for thousands of years, usage

addition to holding the Chartered surged after the invention and popularization of the internal combustion engine in the

Financial Analyst® and Associate of the late 1800s. Oil’s importance as a commercial asset grew, and it became increasingly

Society of Actuaries designations, Kent important politically as it provided a strategic advantage to nations with access to the

is an Enrolled Actuary. He graduated commodity. Prior to World War II, Japan’s incursion into the Asian mainland was driven

from the University of Michigan with primarily by their need for oil and other natural resources. Likewise, the surprise German

bachelor’s and master’s degrees in invasion of the Soviet Union during World War II was at least in part to secure enough oil

business administration. to keep Nazi tanks running and bombers in the air.

Following World War II, consumption continued to increase as oil was needed for the

rebuilding of Europe as well as to fuel the rapidly expanding U.S. economy. Commercial

aviation, increased use of plastics, much of the middle class moving to the suburbs

and the explosive growth of the automobile industry resulted in a seemingly insatiable

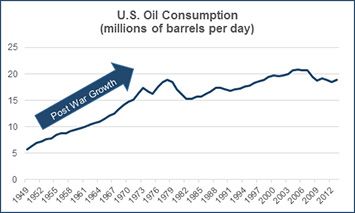

demand for the substance. Domestic oil consumption spiked from roughly 5.8 million

barrels per day just after the war’s end in 1949 to over 14.7 million barrels per day by

1970, according to estimates by the Energy Information Administration (EIA).

But while U.S. consumption skyrocketed, U.S. production failed to keep pace. In

1949, the U.S. produced most of what it consumed, but that didn’t last for long. U.S.

production peaked at just over 9.6 million barrels per day in 1970, forcing the U.S. to rely

on imports to make up the steadily increasing supply gap — a gap that became larger

and larger as time went on.

Saudi Arabia quickly took over as the largest producer in the world, leading to riches

unimagined by that country merely decades before. However, the Saudis, as well as

the other predominately Middle Eastern exporters, found they had little control over the

price. The market at the time was dominated by a handful of multinational corporations,

collectively known as the “Seven Sisters” that colluded with each other to dictate

Falling Oil Prices: pricing. In response, Saudi Arabia helped found the Organization of Petroleum Exporting

Past, Present and Future Countries (OPEC) as a competing power in 1960. OPEC’s stated aim was to ensure a

minimum price for each barrel of oil.

March 2015

The economic turmoil

caused by the oil embargo

of the 1970s caused the U.S.

and its Western allies to

turn to alternative energy

sources in an effort to

wean themselves from their

dependence on OPEC’s

imports.

Source: U.S. Energy Information Administration

Throughout the 1960s, OPEC was primarily successful in their mission and the price of

oil did not change much. All told, the average per barrel cost of oil barely budged from

$2.77 in 1949 to $3.39 in 1970, according to Plains All American and Inflationdata.com.

However, OPEC’s power grew significantly after U.S. production peaked in 1970. As

OPEC’s share of total world production increased, the organization shifted from a

primarily defensive stance to a more aggressive one. In 1973, OPEC declared an oil

embargo in response to the Western support of Israel in the Yom Kippur War. The result

was a sharp spike in oil prices from roughly $3 to $12 per barrel, leading to consumer

panic in the U.S. and a subsequent global recession.

OPEC realized oil could be used as an economic weapon. For the remainder of the

1970s, OPEC used this newfound weapon often. Global demand was so great that they

could achieve significant price increases whenever desired merely by withholding a

small amount of production from the market. As a result, the 1970s saw near-constant

increases in oil prices. The decade closed with an average oil price of $37.42 per barrel

— more than eleven times the price just ten years before.

The economic turmoil caused by the oil embargo of the 1970s caused the U.S. and its

Western allies to turn to alternative energy sources in an effort to wean themselves from

their dependence on OPEC’s imports. Industrial nations increasingly used other energy

sources such as coal, gas and nuclear power. Vast research budgets were devoted to

the development of renewable energy sources such as wind and solar, as well as new

domestic oil production methods like deep water drilling and hydraulic fracturing. As

global supply increased and demand decreased, oil prices dropped. This steady decline

lasted for the next 18 years, until around 1999.

Then, the balance of power tipped again. While oil consumption in the developed world

is still generally flat or declining, emerging markets such as China have been picking

up the slack, and more. Once again, global supply struggled to keep up with demand.

Except for briefly during the 2008-2009 global financial crisis, OPEC reasserted their

pricing power, driving prices up — at least until 2014.

Era Power Avg. Annual Reason

Price Change

1949 - 1972 Consumers +1.1% Seven Sisters dictate price

1973 - 1980 OPEC +34.3% OPEC capitalizes on supply shortage

1981 - 1998 Consumers -6.3% Developed nations cut dependence

1999 - 2013 OPEC +14.5% Increased demand from global growth

Falling Oil Prices:

Past, Present and Future 2014 - ? Consumers?

March 2015 Source: Plains All American, InflationData.com. Average annual price change per barrel of Illinois Crude.

The Present

The oil situation of today is similar to the end of the last OPEC era. Once again, high

oil prices have diminished global demand. While U.S. oil consumption peaked in 2005,

it has, for the most part, slowly declined since. The U.S. has renewed its commitment

to renewable energy sources, and these new sources have significantly contributed to

supply. Furthermore, technological innovations have unlocked domestic resources that

were previously uneconomical to develop. Deep water drillers are penetrating deeper, oil

sands are being developed, and new horizontal drilling techniques combined with better

hydraulic fracturing methods have resulted in a shale energy boom.

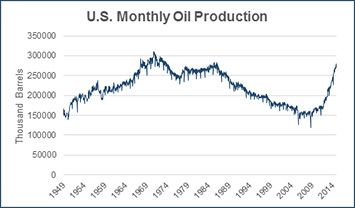

Seemingly, new oil projects come on line every month. After decades of slow decline,

only a few years were needed to regain monthly domestic oil production near the 1970

peak.

Source: U.S. Energy Information Administration

OPEC Response

From OPEC’s perspective, the increase in U.S. production has been alarming. Not only

is the U.S. adding new capacity nearly every month, but the pace of production increase

is accelerating as well. Additionally, OPEC fears other parts of the world might develop

oil producing capabilities using the same technologies.

With this as a backdrop, OPEC held a meeting in Nov., 2014. At that time, oil prices had

already slid approximately 20 percent. Analysts expected OPEC to cut production in

order to maintain high prices, which would have been consistent with their policy over

the prior three years. Instead, OPEC shocked markets by announcing that there would

be no production cuts, allowing the market to correct itself. Oil prices, which had been

in an orderly decline until that point, went into free fall for the rest of the year.

On the surface, some might think OPEC’s decision did not make financial sense. In

fact, the decision was not unanimous among OPEC members. Poorer OPEC member

states such as Venezuela, Iran, and Algeria argued — and still continue to argue — for

production cuts. However, Saudi Arabia has blocked their appeals. While it is possible

that the Saudis will eventually be won over, that is not expected any time soon for three

primary reasons.

First, Saudi Arabia has been unable to depend on other OPEC member nations to stay

below their production quotas. In fact, a recent study by Brown University professor Jeff

Colgan found that OPEC members pumped more than their permitted quota 96 percent

of the time. The Saudis would likely take the brunt of any overall production cuts.

Falling Oil Prices:

Past, Present and Future Second, while production cuts would undoubtedly increase profits in the short run,

Saudi Arabia is taking a long-term perspective. New shale drilling projects are only

March 2015profitable if oil prices remain in the $50 to $100 per barrel range, according to EIA

estimates. Recently, Goldman Sachs evaluated the largest 400 projects throughout the

world and concluded that fewer than one-third would be profitable at current prices.

By forcing lower oil prices, Saudi Arabia can eliminate these projects and protect their

market share over the long term.

Third, Saudi Arabia’s political motivations should not be discounted. Sectarian tensions

between the Shiite and Sunnis have been high, as Iran, which is primarily Shiite, and

We expect continued Saudi Arabia, primarily Sunni, have engaged in proxy conflicts throughout the region

oil price volatility in the for the past few years. Crippling Iran’s economy with lower oil prices can remove the

short run. For the long country’s ability to support neighbors in the region combatting Saudi-funded insurgent

groups.

term, whether the market

ultimately settles at $30, The Future

at $70, or somewhere in We believe a sudden rebound in oil prices to $90 or $100 per barrel in the near future is

between, we expect these highly doubtful. Even if OPEC decided to take action to push prices back up — and was

relatively low prices to be successful — higher prices would probably be short lived considering the vast quantities

of additional supply which would then be accessible at the higher price point.

maintained for years to

come. However, we do expect continued oil price volatility in the short run as the market

struggles to determine where prices will ultimately settle. Some analysts think that prices

could dip below $30, although it is unlikely such a low price would last long. At that cost,

the supply would shrink below global demand. Other analysts predict a partial recovery

to more than $70, but that is similarly unlikely because it would require OPEC fortitude

that has not been seen in the last few decades.

Looking at the Oil Price Eras chart, history shows that when the oil dynamic has shifted,

the new trend has tended to last for years, if not decades. So whether the market

ultimately settles at $30, at $70, or somewhere in between, we expect these relatively

low prices to be maintained for years to come.

Impact on U.S. Economy and Investments

Assuming we are correct, the first economic casualty will be the current U.S. shale

boom. It might be tempting to conclude that low oil prices are bad for the economy,

given that shale has been a significant part of gross domestic product growth over the

past few years. That would be true if the shale boom was the only factor affected.

When looking at the overall U.S. economy, lower oil prices also have a positive impact.

Despite calls for energy independence, the U.S. still unequivocally remains an importer

of oil. The U.S. economy is consumer-based and lower oil prices means lower gas

prices, which directly benefits U.S. consumers. And this consumer effect is immediate.

It is estimated that every one dollar drop in the price of gas leads to an immediate one

percent increase in consumer spending. If oil is a tax on economic growth, the U.S.

consumer is experiencing a significant “tax cut.”

While there certainly will be turmoil in the shale business, the U.S. is blessed with an

incredibly flexible economy capable of adjusting to problems in any one sector. Jobs will

be lost in the oil patch, but they will likely be replaced elsewhere in the U.S. economy. If

cheap oil has returned for the duration, it could ignite significant growth for the U.S.

Additionally, sectors that find oil to be a significant cost of doing business are

positively affected by lower oil prices. This means manufacturing and transportation

sectors should do well for years to come, especially airlines and trucking. Automobile

manufacturers may also thrive as less gas-efficient trucks and SUVs — autos that offer

higher profit margins — become more attractive to consumers. Likewise, retailers who

cater to the middle class may see the greatest boost as more discretionary money is

spent on goods rather than gas.

Conversely, the energy sector will experience the greatest pressure — specifically

alternative energy developers reliant on being a cost-efficient substitute for oil. Industries

that are dependent on the steady stream of new oil projects might also struggle, such

Falling Oil Prices: as drillers and exploration companies. Some regional banks heavy in loans to fund oil

Past, Present and Future projects could encounter trouble too, if those projects wind up in bankruptcy.

March 2015It is also true that low oil prices contribute to low inflation. If deflation fears surface, it

is possible that the Federal Reserve (Fed) may delay raising interest rates. While most

economists expect the Fed to raise rates in 2015, it could be postponed to as late as

2016 if inflation remains benign.

With low oil prices changing inflation expectations, the bond market will be affected

as well. Bonds rallied during the recent oil price drop and should continue to perform

well if oil prices stay low. However, this is true for only high quality holdings. Some junk

bonds could suffer if the issuing companies borrowed too much money assuming that

profitable oil-related projects would allow them to meet debt obligations.

From a global perspective, other oil dependent nations should receive an economic

boost. Low oil prices could be the impetus to finally pull Europe out of economic

doldrums. Emerging market countries that also heavily consume oil should benefit too,

such as India and China. Other emerging market countries, such as Brazil and Russia,

who produce oil will likely struggle.

Summary

We believe the balance of power between OPEC and consumers has now shifted and

relatively low oil prices will be maintained for at least the next few years, if not decades.

If history is any guide, we expect this to have a positive impact on global economic

growth for years to come.

Falling Oil Prices:

Past, Present and Future

March 2015About StanCorp Investment Advisers Helping you achieve lifelong financial well-being is the primary focus of StanCorp Investment Advisers, Inc. We have a fiduciary duty to act in your best interest and adhere to a prudent, unbiased approach to managing your money. Our asset management process starts with learning about you and your goals. Your advisor will recommend a portfolio structure that invests your assets according to your specific time frame. We go beyond your portfolio to take a comprehensive look at all aspects of your financial life and provide guidance to set you on a path to financial well-being. 800.378.5742 www.stancorpadvisers.com Falling Oil Prices: Past, Present and Future © 2015 StanCorp Investment Advisers, Inc. All rights reserved.

You can also read