Financial rules in Horizon 2020 - ETNA 2020 training workshop, Athens September 6, 2016

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Financial rules in Horizon 2020

ETNA 2020 training workshop, Athens

September 6, 2016

Katarina Rohsmann

Austrian Research Promotion Agency (FFG),

NCP Academy Partner

Overview

Funding instruments and funding rates

The project budget in the proposal

Eligibility of costs

Cost categories

Financial reporting and payments

Audits

Frequent mistakes

FFG, September 6, 2016

Financial information in the Grant Agreement

derived from

the proposal

Grant Agreement

H2020

Eligibility of costs: mainly in art. 6 (art. 10 to 15 for Third Parties)

http://ec.europa.eu/research/participants/data/ref/h2020/mga/gga/h2020-mga-gga-multi_en.pdf

FFG, September 6, 2016

Funding instruments and funding rates

Instrument Funding rate

Research and innovation actions (RIA) 100%

Innovation actions (IA) 70% / 100%

Coordination and support actions (CSA) 100%

SME instrument phase 1 € 50.000 (lump sum)

SME instrument phase 2 70 %

Fast Track to Innovation 70% / 100%

Prizes fixed amount (see ‚rules

of the contest‘)

• Innovation Actions, Fast track to innovation: 100% for ‚non-profit

organisations‘

• The total costs (direct and indirect costs) are multiplied with the funding

rate

FFG, September 6, 2016

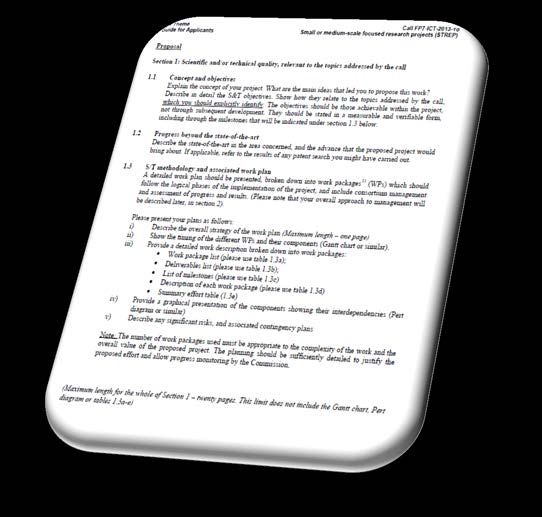

Budget for the proposal

Starting point:

• What are the organisation’s tasks in the project? and/or

• How many people from the organisation will work for the project?

part A

(tables)

part B

(narrative part)

Make sure that the two parts match!

FFG, September 6, 2016

Budget table in part A (full proposal)

25 % flat-rate, except subcontracting

and ‚in-kind contributions not used on the premises‘

transport

only if projects:

explicitly n/a

mentioned

total requested

• Only the white fields must be completed amount

• RIA, CSA: Costs of Linked Third Parties are added to the beneficiary’s costs

• IA: separate column for costs of Linked Third Parties

FFG, September 6, 2016Budget table in Part A (stage 1 of

a two-stage proposals)

• Only the total requested amount for the action must be indicated

• No major deviations allowed between stage 1 and 2

FFG, September 6, 2016Budgetary information in part B

3.4 Resources to be committed

Please provide the following:

• a table showing number of person/months required (table 3.4a)

• a table showing ‘other direct costs’ (table 3.4b) for participants

where those costs exceed 15% of the personnel costs

------------------

4.2: Third Parties involved in the action

• include information on subcontractors, Linked Third Parties and

third parties providing in-kind contributions (must be indicated in

Annex 1 of the Grant Agreement in order to be eligible costs)

FFG, September 6, 2016Table 3.4a: staff effort

Table 3.4a: Summary of staff effort

Please indicate the number of person/months over the whole duration of the planned

work, for each work package, for each participant. Identify the work-package leader for

each WP by showing the relevant person-month figure in bold.

WPn WPn+1 WPn+2 Total Person/

Months per Participant

Participant Number/Short

Name

1 PM: 1/12 of

ParticipantNumber/

the annual

Short Name

productive

Participant Number/

hours

Short Name

Total Person/Months

FFG, September 6, 2016 9Table 3.4b: other direct costs

Table 3.4b: ‘Other direct cost’ items (travel, equipment, other goods and

services)

Please complete the table below for each participant if the sum of the costs for’

travel’, ‘equipment’, and ‘goods and services’ exceeds 15% of the personnel

costs for that participant.

Participant Number/Short Cost (€) Justification

Name

if below 15%: can

Travel be completed

Equipment voluntarily

Other goods and services

Total

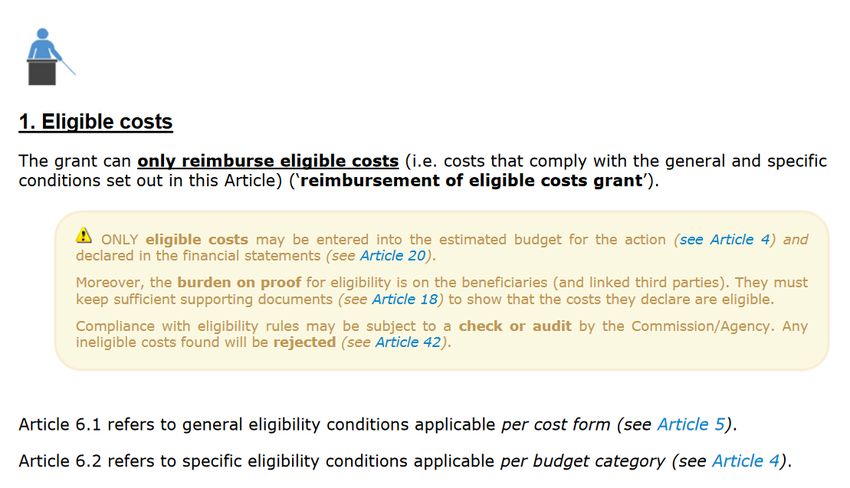

FFG, September 6, 2016 10Eligibile costs: overview

FFG, September 6, 2016General eligibility criteria for actual costs

• Incurred by the beneficiary

• incurred during the duration of the action (except travel costs

for kick-off meeting and costs for final reporting)

• indicated in the estimated budget of the action

• identifiable and verifiable

• necessary for the action as described in the GA

• in compliance with national laws on taxes, labour and social security

• in compliance with beneficiary's usual accounting practice (may not

contradict the rules of the Grant Agreement)

• reasonable, justified, sound financial management

N.B.: Non-refundable VAT is eligible

FFG, September 6, 2016Personnel costs: overview

UNIT COSTS

ACTUAL

PERSONNEL

COSTS

Calculated by the Fixed by

beneficiary according Commission for

Calculation to its usual accounting SME owners

method defined practices and natural

in the model (‘average personnel persons without

grant agreement costs’) a salary

FFG, September 6, 2016Calculation of personnel costs

on a yearly basis

personnel costs = hourly rate x hours worked for the project

Annual gross salary:

Calculation of the hourly rate: basic salary

social security contributions

taxes and duties

annual gross salary other mandatory compo-

------------------------------------------- nents of the basic salary

annual productive hours

(3 options) ≠ bonuses, extra payments for

participating in the project…

FFG, September 6, 2016Annual productive hours

Option 1: „1720 fixed hours“:

• standard number which may be used by any

beneficiary (pro-rata for part-time employees)

Option 2: „Individual annual productive hours“:

• calculation: ‘annual workable hours’ of the individual employee

+ overhours – absences (sick leave etc. – not [bank] holidays)

Option 3: „Standard annual productive hours“

• calculated according to the usual accounting practises

• must correspond to at least 90 % of the ‚standard annual workable hours‘

No more hours than the „annual productive hours“ may be

charged on all EU-funded projects per person and year

FFG, September 6, 2016‚Last closed financial year‘

• Only for calculation of personnel costs on a yearly basis:

• If the financial year is not closed at the time of reporting, the

beneficiary must use the hourly rate of the last closed financial year

available

• No adjustments!

salary rises lead to

financial losses

FFG, July 6, 2016Calculation of personnel costs

on a monthly basis If parts of the remuneration are

generated over a period longer

monthly gross salary than a month, the beneficiaries

------------------------------------------- may include only the share which

annual productive hours / 12

(option 1 or 3)

is generated in the month

(irrespective of the amount

actually paid for that month)

Each beneficiary must use only one option (per full financial

year or per month) for each full financial year for all H2020

projects

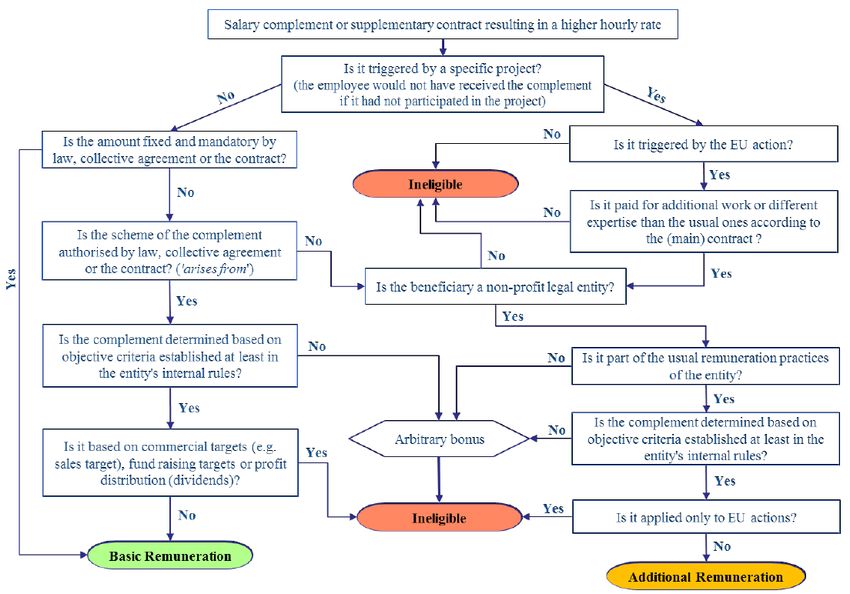

FFG, September 6, 2016‚Standard‘ and ‚additional‘ remuneration

Standard remuneration

Additional remuneration

Mandatory complements

Bonus payments

• resulting from law, collective

agreement or working contract • only eligible for non-profit

organisations

Basic • mandatory fixed complements (e.g.

• payed for additional work or

remuneration holiday pay, complement for hazardous

expertise

work)

• mandatory variable complements (e.g. • strict requirements – see

for merit or performance) not triggered Annotated Grant Agreement

by the work in specific projects

FFG, September 6, 2016Personnel costs – decision tree

See: Annotated Model Grant Agreement, p. 52

FFG, September 6, 2016Situation 1

Mr A is the founder of the start-up company „A Ltd“. He is self-employed and doesn‘t receive a salary.

The company „A Ltd“ has four employees, however its tasks in the project shall mainly be carried out by

A himself.

A says: „If I participate in this project, I cannot accept anything less than my standard hourly rate of

EUR 75.“

Solution:

• A cannot charge his “standard hourly rate“

• „A Ltd“ can claim “costs of SME owners who do not receive a salary” for A

• These costs are unit costs which must be calculated according to the rules of the Grant Agreement

• Further information: Annotated Grant Agreement on art. 6.2.A.4 (p. 71-72 of v.2.1.1 of the AGA):

http://ec.europa.eu/research/participants/data/ref/h2020/grants_manual/amga/h2020-

amga_en.pdf

FFG, September 6, 2016Situation 2

Ms B has been working for „ABC cars“ (a large company in the automotive industry) since 2005.

Due to an internal headcount limit of „ABC cars“, B is employed by the temporary work agency

„PeoplePower“, which is responsible for the payroll tasks.

B says: „This is just a formality. I consider myself as a full member of my team at ABC cars“.

Solution:

• B is not employed by the beneficiary, but by a Third Party

• Rules regarding secondment of personnel do not apply because the Third Party is a temporary work

agency

• The beneficiary cannot charge B‘s costs as personnel costs, but only as costs of a service (other

direct costs) or subcontracting

• Further information: Annotated Grant Agreement on art. 6.2.A.2 (p. 64 of v.2.1.1 of the AGA):

http://ec.europa.eu/research/participants/data/ref/h2020/grants_manual/amga/h2020-

amga_en.pdf

FFG, September 6, 2016Situation 3

Dr C is a specialised researcher at „ABC electric vehicles“, an affiliate of „ABC cars“.

Her expertise is needed for one task of a project in which „ABC cars“ participates.

C says: „I will contribute to this task and ABC cars will charge my personnel costs in its financial

statement – after all we are from the same company group“.

Solution:

• Dr C is not employed by the beneficiary, but by a Third Party (affiliate of the beneficiary)

• His personnel costs cannot be included in the financial statement of the beneficiary as if he was an

employee of the beneficiary

• The affiliate could join the project as a Linked Third Party and claim Dr C‘s costs in its own financial

statement (there are more possibilities, but this is the most obvious solution)

• Further information: Annotated Grant Agreement on art. 14 (p. 135 ff. of v.2.1.1 of the AGA):

http://ec.europa.eu/research/participants/data/ref/h2020/grants_manual/amga/h2020-amga_en.pdf

FFG, September 6, 2016Situation 4

Mr D is a freelancer and supports different organisations in the management of international

projects. He works from his home office, using his own office equipment. „ABC cars“ is looking for

someone to support the management of a H2020 project on a freelance basis.

D says: „I always wanted to be my own boss. Working under someone‘s instructions just isn‘t my

thing.“

Solution:

• In principle, D‘s costs could be claimed as „costs for natural persons working under a direct

contract”

• However, one of the requirements would be that D works “under the beneficiary’s instructions”

• N.B.: In some countries, it is legally impossible to fulfill this requirement

• Further information: Annotated Grant Agreement on art. 6.2.A.2 (p. 64f. of v.2.1.1 of the AGA):

http://ec.europa.eu/research/participants/data/ref/h2020/grants_manual/amga/h2020-

amga_en.pdf

FFG, September 6, 2016Situation 5

Prof E works for the „University of E-City“. Like all professors in his country, he is employed by the

government and receives his salary directly from the government. Prof. E is supposed to act as a head

scientist in a H2020 project.

E says: „The university does not incur any costs for me. Does this mean that I must do all the work for

free?“

Solution:

• Prof E is considered an „in-kind contribution provided by a Third Party free of charge“

• The Third Party and its contribution has to be identified in Annex 1 of the GA (otherwise, the costs

could be approved retroactively, but at the full discretion of the EC/agency)

• Rules regarding „receipts“ do not apply in this case, because Prof E was not provided to the

beneficiary „specifically for the action“ (all professors are employed by the government)

• Further information: Annotated Grant Agreement on art. 12 (p. 126 ff. of v.2.1.1 of the AGA); receipts:

AGA p. 31 f.: http://ec.europa.eu/research/participants/data/ref/h2020/grants_manual/amga/h2020-

amga_en.pdf

FFG, September 6, 2016Types of personnel costs in H2020

A.1: Costs for employees (or equivalent)

A.2: Costs for natural persons working under a direct contract

(observe requirements – legally impossible in some countries)

A.3: Costs for personnel seconded by a third party against

payment

A.4: Costs of SME owners

A.5: Costs of ‘beneficiaries that are natural persons’

NOT personnel employed by a temporary work agency

Details: see Annotated Grant Agreement

FFG, September 6, 2016Natural persons working under a

direct contract

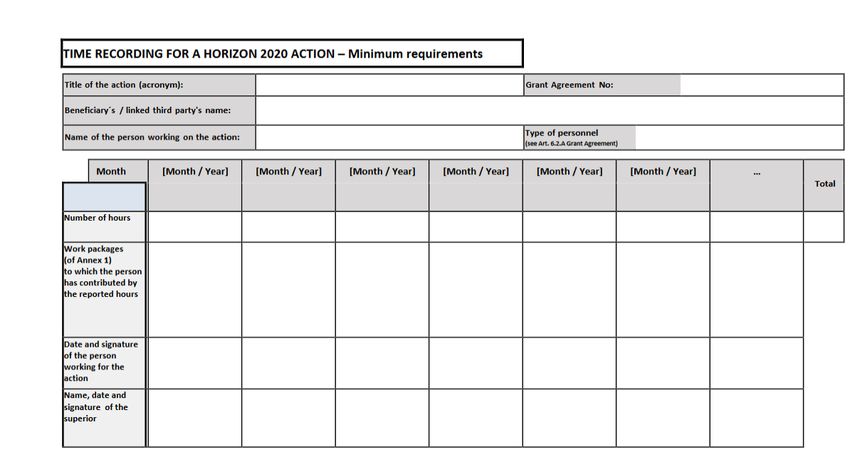

FFG, September 6, 2016Time records

• Only the hours worked for the project must be recorded

• Exception: persons working exclusively on one project (‚declaration‘

• Time records are the proof that the personnel costs have incurred

• if the time recording system is not deemed to be ‚reliable‘, all

personnel costs may be rejected

FFG, September 6, 2016Time records

Minimum requirements: signature

• title and number of the action • reference to task or work package

• beneficiary’s full name

• full name, date and signature of

the person working for the action

• number of hours worked for the

action

• supervisor’s full name and

FFG, September 6, 2016Subcontracting

• A purchase of goods, works or services that are identified in

Annex 1 as action tasks

• Tasks to be implemented and estimated costs must be set out in the

proposal (table 4.2)

• Based on ‘business conditions’: best value for money or lowest price,

• Subcontracting to affiliates: only allowed if ‚usual provider‘ or

framework contract

• No indirect costs on subcontracting

FFG, September 6, 2016Other direct costs (1)

Travel costs and related subsistence allowance:

• must be necessary for the action and

• in line with the beneficiary‘s usual practises on travel

Equipment, infrastructures and other assets:

• only the depreciation costs are eligible

• only the part of the equipment‘s „full capacity“ used for the

project can be charged (must be recorded)

• rent/lease eligible if not exceeding depreciation costs

FFG, September 6, 2016Other direct costs (2)

Costs of other goods and services:

• the beneficiary carries out a task itsself and is supported by

third party (unlike subcontracting)

• best value for money or lowest price

• e.g. consumables and supplies, dissemination costs, rent for

meeting rooms, IRP-related costs, certificates on the financial

statements

FFG, September 6, 2016Costs of Linked Third Parties

• May carry out work in the project and report its own costs

• rules regarding eligibility of costs, funding rates and third

country participation apply

• Name and tasks of the Linked Third Party must be indicated in

the proposal

FFG, September 6, 2016Exercise on eligibility and budget

categories (1)

• costs for drafting the CA before the project starts: ineligible (not incurred during the

duration of the action)

• catering during full-day project meeting: eligible (other direct costs/costs of other

goods and services)

• 1st. class train ticket - company usually books 2nd. class: ineligible (not in line with

the beneficiary‘s usual practises)

• test series performed by external company (task 4.2): eligible (subcontracting –

purchase of a service identified as an action task)

• costs for attending a conference (no ‚active‘ contribution): ineligible (no ‚active

contribution‘, therefore not necessary for the project)

• costs for Certificate on the Financial Statement (CFS): eligible (other direct costs/

costs of other goods and services)

FFG, September 6, 2016Exercise on eligibility and budget

categories (2)

• consulting service on IPR issues: eligible (other direct costs/costs of other goods

and services)

• non-refundable VAT included in hotel bill: eligible (other direct costs/travel costs)

• tickets for visiting Acropolis during kick-off meeting: ineligible (social activity, not

considered necessary for the project)

• article processing charge (APC) for open access publication eligible (other direct

costs/costs of other goods and services)

• costs for externalising the coordinator‘s tasks to a project management agency:

tasks of the coordinator (as defined in art. 41.2 of the GA) may not be subcontracted

FFG, September 6, 2016Reporting and Payments

Pre-financing Interim Interim

Balance Payment

payment payment

30 days after GA enters 90 days 90 days 90 days

into force/10 days before

the project starts

Reporting Reporting Reporting

Period 1 Period 2 Period 3

Periodic Periodic Periodic Final

report report report + report

The coordinator distributes the payments FFG, September 6, 2016 35Periodic reporting

Two parts to be completed:

• Periodic technical report

• Periodic financial report:

→ Individual financial statement, explanation on the

use of resources

→ Periodic summary financial

statement (= request for interim payment)

To be submitted within 60 days after the end of a

reporting period

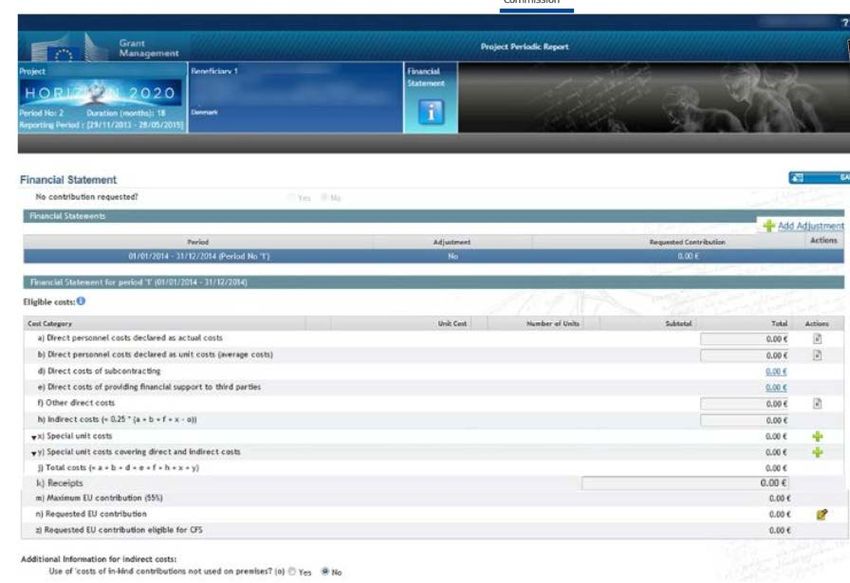

FFG, September 6, 2016Financial reporting in the

Participant Portal

• Click to complete

‚use of resources‘

• Other direct costs

only need to be

explained if they

exceed 15% of the

personnel costs

FFG, September 6, 2016Certificate on the Financial Statements (CFS)

• Required at the end of the project if funding per partner

(or Linked Third Party) exceeds 325.000 EUR (only actual

costs and ‚average personnel costs‘)

• may be performed by any qualified auditor

• costs are eligible as other direct costs

• template/further info: Annex 5 of the Grant Agreement

FFG, September 6, 2016EU audit (2nd. level audit)

• May take place within two years after the balance payment

• Possible consequences: rejection of costs, reduction of the

grant, recovery; extension to other projects in case of

‘systematic errors’

N.B.: records and supporting information must be kept for

five years after the balance payment

FFG, September 6, 2016Frequent mistakes

• Costs claimed are not substantiated (no proper documentation…)

• Costs claimed are not linked to the project

• Third parties and subcontracting costs are not properly reported

• Depreciation costs are not correctly charged/full price is charged

• Personnel costs:

• incorrect calculation of productive hours

• charging of hours not worked for the project

• errors related to time records (inconsistent with information on sick

leave/travels/holidays, ‚signed‘ while a person was absent…)

FFG, September 6, 2016Guarantee Funds

• Similar to an insurance between all beneficiaries – no „collective

financial responsability“ of the consortium

• 5 % of the pre-financing payment are transferred directly to the

fund (and released at the balance payment)

• Cases covered: amounts owed by a beneficiary to the funding

body (e.g. due to bancruptcy)

• Cased not covered: amounts owed by a beneficiary to

another beneficiary (e.g. due under-/owerspending)

FFG, September 6, 2016When in doubt…

• Have a look at the H2020 Online Manual:

http://ec.europa.eu/research/participants/docs/h2020-funding-guide/index_en.htm

• Look for information in the Annotated Grant Agreement:

http://ec.europa.eu/research/participants/data/ref/h2020/grants_manual/amga/h2020-amga_en.pdf

• Ask your legal and financial NCP:

http://ec.europa.eu/research/participants/portal/desktop/en/support/national_contact_points.html

• Contact the Research Enquiry Service:

http://ec.europa.eu/research/participants/portal/desktop/en/support/research_enquiry_service.html

FFG, September 6, 2016THANK YOU FOR YOUR ATTENTION

Katarina Rohsmann

Expert for legal and financial issues

in the EU framework programme

Austrian Research Promotion Agency (FFG)

Sensengasse 1, 1090 Vienna, Austria

phone: +43/5/7755-4009

email: katarina.rohsmann@ffg.at

FFG, September 6, 2016You can also read