FOOD-FOR-THOUGHT WEEKLY - 12 February 2021 - Rand Agri

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

12 February 2021

WEEKLY

FOOD-FOR-THOUGHT

Weather

- South African weather forecast

- International weather forecast

Parities

- Import and export parities for yellow maize

FOOD-FOR-THOUGHT International Agriculture

- South American crop conditions

CONTENTS - Agricultural News: February WASDE Report

- Agricultural News: Ending stocks to exports

Local Agriculture

- Imports and exports

- Producer deliveries

- Agricultural News: Dam levels

Currencies

- Overview - USD/ZAR

LOCAL

WEATHER 14-day weather forecast

According to the weather bureau, rainfall is forecast for parts of Mpumalanga and

Limpopo due to the presence of tropical low pressure systems near Mozambique.

Warmer, sunny weather is expected over the western parts of the country in the coming

week.

USA Drought Monitor

9 February 2021 11 February 2020

Weather conditions in the US are still very dry in the

central to western areas moving towards the mid-west.

These dry conditions will only have an effect on prices as

soon as the US starts to plant. Keep in mind that this

monitor changes weekly

Follow the link to stay up to date with the latest drought

conditions in North America:

https://droughtmonitor.unl.edu/CurrentMap.aspx

INTERNATIONAL

WEATHER

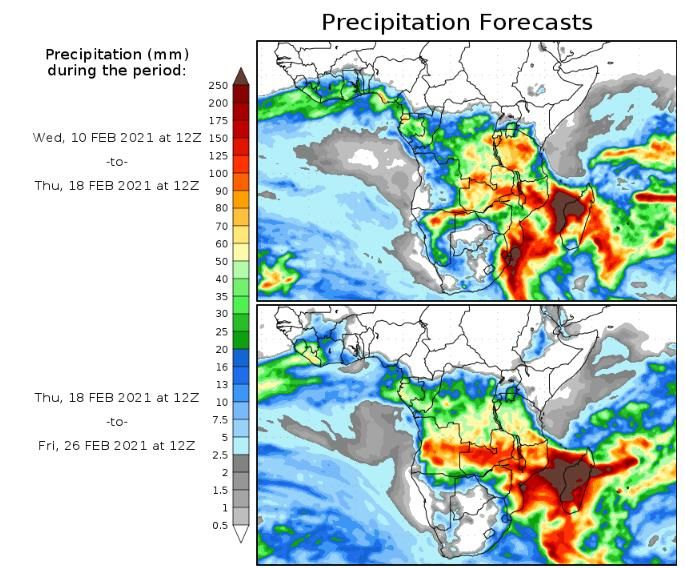

10-day weather forecast: South America

More a rainfall is expected in Mato Grasso and

central parts of Brazil, currently still favouring

developing crops.

Argentina’s main producing areas can expect below

normal rainfall.

INTERNATIONAL WEATHER Extremely low temperatures are expected over the central parts of the US. The average snowfall must be monitored, as it is the most important factor determining soil moisture.

INTERNATIONAL WEATHER

IMPORT & EXPORT

PARITIES

Mar’21 May’21 Jul'21 Sept'21

PMB import parity R 4 370 R 4 221 R 4 505 R 4 183

CPT export parity R 4 200 R 4 018 R 4 229 R 3 897

SAFEX yellow maize R 3 453 R 3 260 R 3 187 R 3 247

DBN export parity R 3 211 R 3 260 R 3 187 R 3142

SOUTH AMERICA

AGRICULTURE

South American crop conditions as at 5 February 2021

Maize Soybeans

9% 9%

24% 19%

Good to excellent Good to excellent

Average Average

Poor Poor

67%

72%

3%

0%

10%

22% 38% 35%

18% 17%

59%

65%

68% 2019/20

2019/20

65%

Previous Week

Previous Week

Crop conditions improved over the past week due to

favourable weather conditions

BRAZIL

AGRICULTURE

11,2 % of

It is

soybeans

33,31%

in Mato

below the

Grosso

2019/20

have been

pace.

harvested

INTERNATIONAL

AGRICULTURE

February ’21 WASDE

SOYBEANS

MAIZE

WHEAT

US ending stock: US ending stock: US Ending stock:

January – 1 552 billion bushels January – 0,140 billion bushels January – 0.836 billion bushels

Expectation 1 384 billion bushels Expectation 0,123 billion bushels Expectation 0.834 billion

bushels

February – 1 502 billion bushels February – 0,120 billion bushels

February – 0.836 billion bushels

World ending stock: ➢ World ending stock: ➢ World Ending stock:

Volwasse stadium

January – 283.83 million ton January – 84.31 million ton January – 313.19 million ton

- Expectation 279.79 million ton Expectation 83.30 million ton Expectation 312.86 million ton

February – 286.53 million ton February – 83.36 million ton February – 304.22 million ton

The adjustments were considerably less than expected and prices came

under pressure after the USDA’s publication.INTERNATIONAL

AGRICULTURE

February ’21 WASDE

US Ending stocks for Corn US Ending stocks for Soybeans

Volwasse stadium

-

The USDA adjustment of maize resulted in the lowest carryover stock in seven years. The current South American soybean harvest can add support to the stock levels in the

(Source: @karenbraun *twitter) coming weeks.INTERNATIONAL

AGRICULTURE

US Ending Stocks to Exports

Volwasse stadium

-

Source: https://twitter.com/KevinVanTrumpINTERNATIONAL

AGRICULTURE

Chinese imports far from slowing down!

China is one the world’s largest importers

of maize and soybeans and this shopping

spree is far from over, according to Cargill

CEO, Dave MacLerman.

China’s local pork herd, which is growing at

an exponential pace, is one of the main

factors contributing to these high levels of

buying in recent months.

According to market analysts, roughly

Volwasse stadium 20 million tons of imports are needed to

meet the feed demand and to build

- stockpiles as a way to ensure food security.

*Read More:

https://www.google.co.za/amp/s/www.bloomberg.com/

amp/news/articles/2021-02-05/world-s-top-crop-trader-

says-chinese-buying-spree-has-more-to-goLOCAL EXPORTS 2020/21

AGRICULTURE

Destination for most exports:

• Exports week ending 5 February: 20 962 t

WMAZ exports:

White Maize •

•

Previous week: 25 940 t

Imports: 0 t 11 128 t

• Export intentions: 151 861 t Zimbabwe

(Next 8 weeks)

• Exports week ending 5 February: 8 722 t

• Previous week: 10 771 t YMAZ exports:

Yellow Maize • Imports: 0 t 2 941 t

• Export intentions: 63 562 t Zimbabwe

(Next 8 weeks)LOCAL

AGRICULTURE

Cumulative local deliveries up to 5 February 2021

White maize Soybeans

Week ending 5 February: 5 870 t Week ending 5 February: 738 t

Previous week: 10 071 t Previous week : 839 t

Total: 8 110 510 t (92,1%) Total: 1 215 503 t (96,4%)

Yellow maize Sunflower

Week ending 5 February: 2 679 t Week ending 5 February: 57 t

Previous week: 10 802 t Previous week: 239 t

Total: 6 079 132 t (91,8%) Total: 786 022 t (100%)Production forecast

2021

FINAL FINAL CROP CEC CEC FINAL CROP

AREA PLANTED 2020 AREA PLANTED FINAL ESTIMATE1) vs

CROP

2020 TONS NOV 2020 NOV 2020 FINAL ESTIMATE

HA HA TONS %

(A) (B) (C) (D) (B) ÷ (D)

White Maize 1 616 300 8 547 500 1 616 300 8 666 310 -1,37

Yellow Maize 994 500 6 752 500 994 500 6 741 870 +0,16

Total Maize 2 610 800 15 300 000 2 610 800 15 408 180 -0,70

Sunflower seed 500 300 788 500 500 300 785 910 0,33

Soybeans 705 000 1 245 500 705 000 1 245 500 -

Groundnuts 37 500 50 080 37 500 50 080 -

Sorghum 42 500 158 000 42 500 155 560 +1,57

Resource: SAGISLOCAL

AGRICULTURE

Dam Levels: 9 February 2021

Vaal Dam Bloemhof Dam

Percentage: Percentage:

101,5% 108,4%

Previous week: Sterkfontein Dam Gariep Dam Grootdraai Dam Previous week:

79,8% 108,1%

Previous year: Percentage: Percentage: Percentage: Previous year:

56,9% 96,9% 112,9% 104,2% 73,2%

Previous week: Previous week: Previous week:

96,6% 120,5% 108,4%

Previous year: Previous year: Previous year:

92,0% 70,9% 100,9%EXCHANGE RATE

R/$

The South African rand has strengthened

further over the past week.

The currency received good support after the

business confidence index for January 2021

increased from 93,4 to 94,5.

The dollar lost momentum against other

major currencies in the first 5 weeks of the

year due to high fiscal spending and a 1,9

trillion-dollar COVID relief bill.

USDZAR Trades Lower As SA Business Confidence Index

Improves; Targets 14.54 (investingcube.com)

Current resistance: 15,40

Current support: 14,50Market overview: Maize

Previous season:

• With the exception of early deliveries, there is almost no • South Africa is currently pricing for exports

yellow maize carryover stock. In addition, two vessels from May to August. This only allows for

with YM (yellow maize) for export in April / early May has 1,7 million ton of exports. To be able to

been booked, which should support previous-season YM export the necessary volumes, South

prices. Africa will have to continue exporting until

• The 1 042 million ton of WM carryover stock (white October and maybe even later, depending

maize) is sufficient. The availability of white maize might

nevertheless pose problems, since it is concentrated in a

on the yield. Brazil and Argentina are

currently cheaper than South Africa for the

RAND AGRI

same period, hence there is a downward

•

number of western silos.

Internationally, US CBOT prices drastically increased from

December. This was due to a number of circumstances. •

risk of $20 on the SAFEX market.

The exchange rate is yet another factor

Trader Snapshot

Argentina temporarily closed its borders for maize that will affect the price of maize. If

exports, the USA adjusted their previous season yields president Biden’s US stimulus package

downward and there were unexpectedly large exports succeeds, the rand might strengthen

from the USA to China. further against the dollar, but on the other

hand, CBOT prices will increase as a result

New season: of a weakening dollar.

• Internationally, the market should find support thanks to

lower world carryover stock levels. The question is Summary

whether China will continue its current large imports from Production for the current season is above

the USA or whether they will produce more grain locally. average and prices are good. My view is that

• The current La Nina system that brought good rains to farmers should be able to hedge 40-50% of their

South Africa, is expected to cause dryer conditions in the expected production at current levels. Options

USA. Soil moisture levels in the UA are currently much also present a good opportunity to further

lower than during the previous season, with the planting exploit the upward potential of the market whilst

season imminent. covering downward price risks.

• Planting season in the USA starts in March and we will

have to keep a close eye on its progress. Any movements Planting progress in the USA should be closely

towards more soybean plantings at the expense of maize, monitored so that any possible marketing

or drought, should support CBOT maize prices. opportunities can be taken advantage of, to

• The production potential appears to be above average, market a further 25% of the expected

and my expectation is a production of around 16,5 million production. SAFEX currently does not sufficiently

ton. This implies that 2 million ton of deep sea exports will cover the spread to enable profitable storage of

be required to keep the South African balance sheet in the production, so it makes financial sense to

equilibrium. market either before or during the harvest.

Overview compiled by: Ampie Rossouw – Rand Agri Grain Trader.• Chinese record imports continue.

• Dam Levels: Many of the country’s important

dams, including the Vaal Dam, are currently

at full capacity after very good rains over the

SUMMARY catchment areas.

• The South African rand traded stronger

against the dollar due to optimism about

emerging markets.CONTACT US

Tel: +27 (0) 13 243 1166

E-mail: info@randagri.co.za

Web: www.randagri.co.za

Address: 24 Samora Machel Street

Middelburg, MpumalangaYou can also read