Global, European and Belgian pharmaceutical market trends

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Global, European and

Belgian pharmaceutical

market trends

Prepared for CIB

27th February 2019

Patrick Bervelt, Sales Director, Account Management

Patrick Van Dooren, Director Commercial & Technology Services

Copyright © 2019 IQVIA. All rights reserved. IQVIA® is a registered trademark of IQVIA Inc. in the United States and various other countries.

Agenda

Patrick Van Dooren, Principal, Director Commercial & Technology Services IQVIA

Global and European pharmaceutical market trends

Patrick Bervelt, Sales Director, Sales, BEL & LUX, IQVIA

Belgian pharmaceutical market trends

1

IQVIA Belgium & Luxembourg across our 7 key business areas

Domain Expertise Unparalleled Data

Institutional knowledge and domain expertise across One of the world’s largest curated healthcare data

diseases, geographies and scientific methods sources with innovative privacy protections

Transformative Technology Advanced Analytics

Leading technologies to provide real-time access to Faster, more precise decision-making generated by

operations-critical information advanced analytics designed for healthcare

Research and Real-World Insights Healthcare Solutions Information Offerings Services Contract Sales and Technology

Development Solutions • 20 Real World • 30 hospital consultants • Wholesaler, retail, • Commercial services Medical Solutions Solutions

• 150 staff, including Evidence scientists hospital panel • 170 staff • Leading CRM,

• Market leader for • Technology services

70 CRA • World class in health hospital analytics • Longitudinal patient • Medical sales and Key MCM & MDM

• Data science Account Teams

• Yearly 800 new economic modelling • Benchmarking data • Compliance & quality

patients enrolled • Strategic advice • Nursing and Home care solutions

solutions for hospitals • HCP database

• Marketing services services for patients

• The Brussels OneKey • Business Intelligence

support

Prime Site

2

+ Global and European pharmaceutical market trends

+ Belgian pharmaceutical market trends

3

Global and European pharmaceutical

market trends

4

Global growth is forecast at 4.8% per annum, led by developing markets and

the US in particular

Sales Evolution and Forecast - Global

1.600 (2016-2022) 8%

1.447

1.373 Forecasted annual

1.400 1.304 7%

growth 2017-2022

1.245

1.205

1.200 1.139 6%

Sales ($US bn)

Annual growth

1.108 +4.8%

1.000 5%

+5,5%

800 4%

600 3% +3.9%

400 2%

200 1%

0 0%

2016 (a) 2017 (a) 2018 (f) 2019 (f) 2020 (f) 2021 (f) 2022 (f)

Global sales Global growth US growth Europe growth

IQVIA Health Market Prognosis Q3 2018

6

In Europe, growth will be more modest and in Belgium slightly weaker still

Sales Evolution and Forecast - Europe

350 (2016-2022) 10%

300 Forecasted annual

300 290

279 growth 2017-2022

269 8%

259

248

Sales (US$ bn)

250 238 +3.9%

Annual growth

227

6%

200

+2.9%

150

4%

100

2%

50

0 0%

2015 (a) 2016 (a) 2017 (a) 2018 (f) 2019 (f) 2020 (f) 2021 (f) 2022 (f)

Europe sales Europe growth Belgium growth

IQVIA Health Market Prognosis Q3 2018

7

Global growth is expected to be primarily driven by developed markets, and

to a lesser extent by expanded access and use in pharmerging markets

Contribution to Global Sales by Region

(2017-2022)

+5.5% +5.0% +7.4% +3.8% +3.6% +5.1% +1.6% CAGR % (2017-2022)

1.500

11 1 1.447

57 13

1.400 16

61

149

1.300

Sales (US$ m)

1.200

1.139

1.100

1.000

900

800

2017 sales N. America W. Europe E. Europe & CIS Asia L. America ME & Africa RoW 2022 sales

IQVIA Health Market Prognosis Q3 2018

8The US will continue to be the largest market but we expect to see changes

in rankings lower down the top 20

Source: IQVIA Institute

9By therapy area, oncology, antidiabetics and autoimmune disease products

dominate the global market

Top 15 Therapy area ranked by sales 5 year CAGR

(Global sales, $US bn MAT 11/2018)

Oncologics $103bn 9%

Antidiabetics $92bn 11%

Autoimmune Diseases $69bn 18%

Pain $64bn 1%

Respiratory Agents $46bn 2%

Antihypertensives $43bn -6%

Antibacterials $38bn -2%

Anticoagulants $37bn 6%

Mental Health $34bn -6%

Antivirals $30bn 9%

Multiple sclerosis $28bn 13%

Nervous system disorders $27bn 5%

Other cardiovasculars $25bn 2%

Viral hepatitis $24bn 27%

Lipid regulators $22bn -9%

Source: IQVIA MIDAS

10The current drug pipeline reflects this emphasis on oncology

Top 10 Therapy Areas by Molecule Count

10.000 315

Number of Molecules in Development

8.000

6.000

186

222

4.000

150 107

2.000 47 100 82 92 66

0

Discovery Clinical Phase 1 Clinical Phase 2 Clinical Phase 3 Clinical

IQVIA Market Analytics and ReSearch, IQVIA Institute

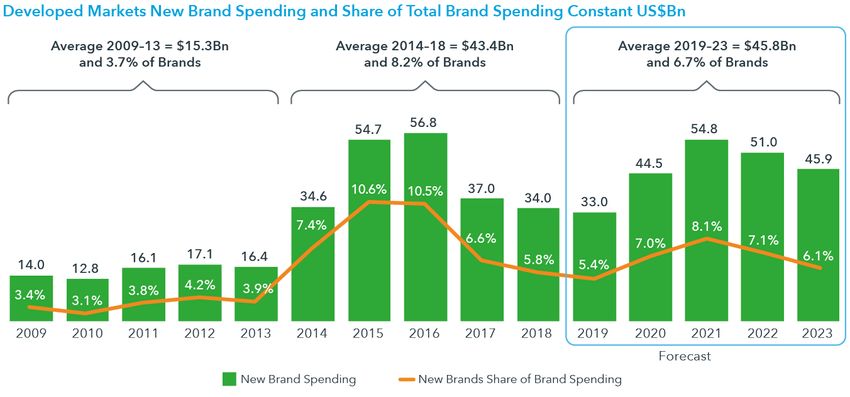

11Over the past five years there has been a significant increase in the number

of and spending on new active substances

12Fewer than half of the world’s top 20 pharmaceutical companies generated

>15% of their 2018 sales from products launched in the last 5 years

Global – Top 20 refreshment index

Total absolute growth Q3MAT 2012-2018 (Bn LCUS$)

22

J&J Abbvie

20 Gilead

16 BMS

14

12 Novo Nordisk

Roche GSK

10

Amgen

8 Novartis Merck & Co Lilly

Sanofi

6

Bayer Pfizer

4

Allergan Boehringer Ingelheim Takeda

2

Mylan Bubble size represents recently

-4 Astrazeneca launched* product sales in Q3MAT 2018

Teva

-6

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 19 20 21 27 28 29 30 31 69 70 71

Share of Q3MAT sales from recent launches* (%)

Notes: Recent launches: Innovative branded products launched in the last 5 years.

14

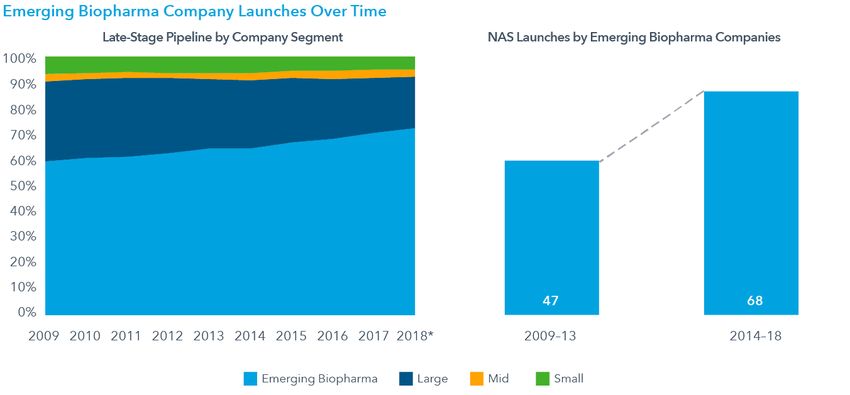

Source: IQVIA MIDAS MAT Q3 2018Small players, the ‘emerging biopharma companies’, are expected contribute

a larger share of new active substance launches

Source: IQVIA Institute

15Specialty products are accounting for more and more of new active

substance launches and will make up over half of spending

Share of Specialty Launches Specialty medicine share of spending

2004-2008 2009-2013

38% 50%

2014-2018 2019-2023

61% 65%

Source: IQVIA Institute

18Growth in specialty spending will be disproportionately driven by five

therapeutic classes

Source: IQVIA Institute

19Biologics growth continues to outstrip small molecules

Global biologics sales and trends (Bn of US$, MAT 06/2013-06/2018)

300 30%

MAT 06/18 Biologics sales

250

25% (Total 2018: 295 Bn US$)

20%

Sales (Bn US$)

200

12% 17% 19%

Growth

15%

150 7%

10% 5% 42%

18%

100

5%

50 59% 4% 17%

0%

0 -5% EU5 Autoimmune

2013 2014 2015 2016 2017 2018 US Diabetes

Biologics sales Small molecule growth Japan Oncology

Biologics growth Pharmerging MS

RoW Others

21

Source: IQVIA; European Thought Leadership; MIDAS MAT Q2 2018; Rx only; Note: growth in LCUS$Biologics are on the cusp of being shaken up

Global Rx Value (MAT Q2 2018) LCUSD Global Biologics Top 10 (MAT Q2 2018)

Threatened by LOE

$296bn Other Value Added Medicines

3% 3% bn USD

Innovative SM Top 10 biologics

(2018)

Humira 24

Biologics

29% Lantus 11

Enbrel 10

MIDAS

41% Remicade 8

Global Rx

$1.0tn Novorapid 7

Herceptin 7

1% Mabthera 7

Biosimilars

Opdivo 7

22% Avastin 6

Generics Humalog 6

Total threatened: $90bn, 30% of biologics

Notes: Pathway biosimilars only 22

Source: IQVIA MIDAS MAT Q2 2018Originators begin taking back share from certain markets. Adalimumab

latest and most anticipated entrant

Biosimilar penetration – October 2018

insulin

infliximab glargine etanercept rituximab trastuzumab adalimumab

EU5

UK 92.2% 9.0% 82.0% 91.5% 60.7%

Germany 51.3% 13.3% 56.8% 60.9% 28.3% 1.4%

France 59.1% 14.6% 17.9% 63.6% 27.5% 0.08%

Italy 78.5% 19.2% 45.6% 74.5% 9.2% 0.01%

Spain 55.8% 12.0% 30.2% 27.8% 10.6% 0.02%

High

High penetration

uptake

Denmark 98.5% 9.3% 90.6% 67.2% 99.3%

Finland 17.8% 6.0% 6.1% 6.2% -

Netherlands 76.1% 10.8% 24.1% 93.4% 95.0% 3.2%

Norway 97.6% 5.8% 90.1% 0.0% 81.2%

Poland 95.2% 35.6% 36.6% 34.4%

Canada 9.8% 7.8% 11.0% 0.2%

Japan 9.0% 50.2% 6.8% 30.6% 30.6%

USA 6.2% 31.7% Low

uptake

Notes: trastuzumab and rituximab subcutaneous form excluded from calculations 23

Source: IQVIA MIDAS Restricted MTH October 2018Originators use devices as one of their most successful defences

Trastuzumab forms (2014-17) Treatment days Trastuzumab volume share (2018) Treatment Days

SC Herceptin IV Herceptin Biosimilar

5 NL

EU5

Germany UK

Treatment days (Mio.)

4

3

2

1

0

Q2/14 Q4/14 Q2/15 Q4/15 Q2/16 Q4/16 Q2/17 Q4/17

Reformulated Subcutaneous injection: less invasive,

Original faster administration

28

Source: IQVIA European Thought Leadership; IQVIA MIDAS Restricted MTH July 2018Defences hold strong: no significant switch from SC -> IV

Rituximab Subcutaneous share Treatment days Trastuzumab Subcutaneous share Treatment days

Biosim Launch May-17 Biosim Launch May-18

35% 80%

30% 70%

60%

25%

50%

20%

40%

15%

30%

10%

20%

5% 10%

0% 0%

France Germany Italy Spain UK France Germany Italy Spain UK

29

Source: IQVIA European Thought Leadership; IQVIA MIDAS MTH December 2018What to watch 2019 to 2023

Next-generation Biotherapeutics: expanding use and new approvals

30

Source: IQVIA European Thought LeadershipBelgian pharmaceutical

market trends

31Recent measures impacting the Belgium market

• Easing of conditions for reimbursement of hep C

drugs (Jan 2019)

• Incentivization of biosimilar prescription (Jan 2019)

• Liberalization of the distribution network for medical 2019

devices in Belgium (Feb 2019)

• Elections (May 2019)

• Creation of the Federal Observatory

of Biopharmaceutical sector

2018 • Belgian Medicines Verification

• Low Variable Care System goes Live

• Hospital Networks

• BeNeLuxA – initiative to

facilitate information sharing

and streamline Health

Technology Assessments

2017

• Agreement to boost uptake of biosimilars

• Introduction of patent cliff system for medicines in cat A, B, C, Cs,and Cx

2016 • Reduction of the security margine

• Application of patent cliff

• Implementation of the “180 + 1” measure

32The hospital channel has made the strongest contribution to Belgian

pharmaceutical market growth

Total Pharmaceutical market – Belgium

(MNF Euro value; MAT December 2018)

Total Pharmaceutical Market €5.401m

Delta Absolute growth +€357m 1yr growth +7.1% 5yr CAGR +4.2%

Hospital €2.321m Rx bound sales €2.618m

+€346m abs value +0.3% 1y growth

+17.5% 1y growth

43%

+10.9% 5y CAGR

57% 85% Non Rx bound €462m

Retail €3.081m 15% +0.5% 1y growth

+€10m abs value

+0.3% 1y growth

+0.4% 5y CAGR

Source: IQVIA Retail & Hospital audits

33Hospital sales growth is led by original products, whilst in the retail channel

generics are performing best

Total Pharmaceutical market – Belgium

(MNF Euro value; MAT December 2018)

Total Pharmaceutical Market €5.401m

Hospital €2.321m Generic €107m

5% +11.0% 1yr growth Protected

88

Original €2.208m %

+17.9% 1yr growth

12% Unprotected

95%

Retail €3.081m Generic €506m Protected

+5.9% 1yr growth 40

17% %

Original €2.572m

60% Unprotected

-0.7% 1yr growth

83%

Source: IQVIA Retail & Hospital audits

34Retail

35In retail, immunotherapy and haematology are the best performing

categories, whilst angiotensin products have seen the greatest decline Retail

Top 10 ATC2 classes in values with growing and declining – Retail

(MNF Euro Value (Mio.); MAT December 2018)

Immunosuppressants (L04) Humira, Stelara, Psycholeptics (N05)

330 +9,3% Cosentyx, Cimzia 163 -2,7%

Antithrombotics (B01) 226 +9,3% Eliquis, Lixiana, Brilique Analgesics (N02) 140 -4,4%

Antihistamines and COPD

177 +5,1% Inuvair, Revlar Elipta, Xolair Renin-Angiotensin agents (C09) 119 -3,8%

products (R03)

Antidiabetics (A10) 148 +5,3% Toujeo, Trulicity, Jardiance Lipid modifying agents (C10) 117 -25,6%

Systematic antivirals (J05) 146 +6,2% Genvoya, Tivicay, Odefsey Psychoanaleptics (N06) 94 -3,8%

Sex hormones and modulators of

Other nervous system drugs (N07) 100 +1,4% Tecfidera, Aubagio 76 -0,9%

the genital system (G03)

Antiinflammatory and

60 +13,4% Xeljanz, Olumiant Urology (G04) 68 -4,1%

antirheumatic products (M01)

Vaccines (J07) 56 +10,3% Gardasil, Bexsero Systematic antibacterals (J01) 58 -3,4%

Cough medications (R05) 55 +2,6% Bronchosedal, Toularynx Nasal preparations (R01) 46 -4,8%

Antiepileptics (N03) 53 +2,6% Vimpat Antihemorrhagics (B02) 45 -8,9%

Source: IQVIA Retail Audit

36In retail, immunotherapy and haematology are the best performing

categories, whilst angiotensin products have seen the greatest decline Retail

Top 10 ATC2 classes in values with growing and declining – Retail

(MNF Euro Value (Mio.); MAT December 2018)

Immunosuppressants (L04) Risperdal, Zolpidem, Psycholeptics (N05)

330 +9,3% 163 -2,7%

Lormetazepam, Abilify

Antithrombotics (B01) 226 +9,3% Dafalgan, Durogesic, Perdolan Analgesics (N02) 140 -4,4%

Antihistamines and COPD

177 +5,1% Coversyl, Preterax, Exforge Renin-Angiotensin agents (C09) 119 -3,8%

products (R03)

Antidiabetics (A10) 148 +5,3% Crestor, Inegy, Ezetrol Lipid modifying agents (C10) 117 -25,6%

Systematic antivirals (J05) 146 +6,2% Sipralexa, Cymbalta Psychoanaleptics (N06) 94 -3,8%

Sex hormones and modulators of

Other nervous system drugs (N07) 100 +1,4% Mireva, Nuvaring, Yasmin 76 -0,9%

the genital system (G03)

Antiinflammatory and

60 +13,4% Vesicare, Tamsolisine SDZ, Cialis Urology (G04) 68 -4,1%

antirheumatic products (M01)

Vaccines (J07) 56 +10,3% Amoxicilline EG, Amoclane EG, Tetralysal Systematic antibacterals (J01) 58 -3,4%

Cough medications (R05) 55 +2,6% Otrivine, Sofrasolone, Rhinospray Nasal preparations (R01) 46 -4,8%

Antiepileptics (N03) 53 +2,6% Refacto AF, Benefix Antihemorrhagics (B02) 45 -8,9%

Source: IQVIA Retail Audit

37The top 20 companies account for 63% of the market share

and display variable performances over the last year Retail

Top 20 companies performances and growth – Retail Growth since last MAT Market growth

(MNF Euro Value (Mio.); MAT December 2018) 0.2%

EG GENERICS 219,3 1,4%

PFIZER 164,4 Enbrel -7,5%

ABBVIE 140,8 +1 Humira 9,1%

NOVARTIS PHARMA 131,3 +1 4,9%

GLAXOSMITHKL.PHARM 125,3 +1 2,3%

SANDOZ 122,8 +1 3,1%

BRISTOL-M. SQUIBB 114,6 +3 Eliquis, Orencia 7,3%

MSD BELGIUM 113,7 -1 Inegy, Ezetrol -6,8%

JANSSEN-CILAG 113,7 +1 Stelara 20,0%

BAYER PHARMACEUTIC 106,2 +1 -1,9%

SANOFI BELGIUM 101,7 -2,8%

ASTRAZENECA 92,0 -9 Crestor -33,3%

BOEHRINGER INGEL. 73,9 5,0%

GILEAD SCIENCES 68,8 +1 Genvoya, Odefsey 10,6%

TAKEDA BELGIUM 63,8 -1 Pantomed Nycomed -6,7%

TEVA PHARM.BELGIUM 62,1 6,6%

J&J CONS. 22,1 -2,2%

VIIV HEALTHCARE 49,1 2,0%

NOVO-NORDISK 47,3 -0,1%

SERVIER 47,2 +1 0,1%

Source: IQVIA Retail Audit

38On the Belgian market, 162 retail products have been launched between

January 2017 and September 2018 Retail

In total, 162 products were launched on the Belgian market between

162 January 2017 and September 2018

Influenza vaccines, Imported products, Generics

139 Original products with monthly sales below €30k

Original products with monthly sales above €30k recorded at least once

23

39HIV drugs, biologics in psoriasis, rheumatics and diabetes markets, and

respiratory products show the fastest growth Retail

Original products launched between January 2017 and September 2018

with monthly sales above 30,000 EUR recorded at least once

(Value (MNF/EUR); 24 months as of launch)

1.400.000

1.200.000

J05C - ODEFSEY - 201701

1.000.000

Sales (MNF/EUR)

J05C - SYMTUZA - 201804

800.000

600.000

400.000

200.000

0

MONTH 1

MONTH 2

MONTH 3

MONTH 4

MONTH 5

MONTH 6

MONTH 7

MONTH 8

MONTH 9

MONTH 10

MONTH 11

MONTH 12

MONTH 13

MONTH 14

MONTH 15

MONTH 16

MONTH 17

MONTH 18

MONTH 19

MONTH 20

MONTH 21

MONTH 22

MONTH 23

MONTH 24

Source: IQVIA LMPB data

40HIV drugs, biologics in psoriasis, rheumatics and diabetes markets, and

respiratory products show the fastest growth Retail

Original products launched between January 2017 and September 2018

with monthly sales above 30,000 EUR recorded at least once

(Value (MNF/EUR); 24 months as of launch)

600.000

M01C - XELJANZ - 201712

M01C - OLUMIANT - 201711

500.000

Sales (MNF/EUR)

400.000

300.000

200.000

100.000

M01C - KEVZARA - 201803

0

MONTH 1

MONTH 2

MONTH 3

MONTH 4

MONTH 5

MONTH 6

MONTH 7

MONTH 8

MONTH 9

MONTH 10

MONTH 11

MONTH 12

MONTH 13

MONTH 14

MONTH 15

MONTH 16

MONTH 17

MONTH 18

MONTH 19

MONTH 20

MONTH 21

MONTH 22

MONTH 23

MONTH 24

Source: IQVIA LMPB data

41HIV drugs, biologics in psoriasis, rheumatics and diabetes markets, and

respiratory products show the fastest growth Retail

Original products launched between January 2017 and September 2018

with monthly sales above 30,000 EUR recorded at least once

(Value (MNF/EUR); 24 months as of launch)

250.000

A10C - FIASP - 201809

200.000

A10C - XULTOPHY - 201808

Sales (MNF/EUR)

150.000

100.000

50.000

0

MONTH 1

MONTH 2

MONTH 3

MONTH 4

MONTH 5

MONTH 6

MONTH 7

MONTH 8

MONTH 9

MONTH 10

MONTH 11

MONTH 12

MONTH 13

MONTH 14

MONTH 15

MONTH 16

MONTH 17

MONTH 18

MONTH 19

MONTH 20

MONTH 21

MONTH 22

MONTH 23

MONTH 24

Source: IQVIA LMPB data

42HIV drugs, biologics in psoriasis, rheumatics and diabetes markets, and

respiratory products show the fastest growth Retail

Original products launched between January 2017 and September 2018

with monthly sales above 30,000 EUR recorded at least once

(Value (MNF/EUR); 24 months as of launch)

250.000

R03L - TRIMBOW - 201804

200.000

Sales (MNF/EUR)

150.000 R03L - TRELEGY ELLIPTA - 201807

100.000

50.000

0

MONTH 1

MONTH 2

MONTH 3

MONTH 4

MONTH 5

MONTH 6

MONTH 7

MONTH 8

MONTH 9

MONTH 10

MONTH 11

MONTH 12

MONTH 13

MONTH 14

MONTH 15

MONTH 16

MONTH 17

MONTH 18

MONTH 19

MONTH 20

MONTH 21

MONTH 22

MONTH 23

MONTH 24

Source: IQVIA LMPB data

43HIV drugs, biologics in psoriasis, rheumatics and diabetes markets, and

respiratory products show the fastest growth Retail

Original products launched between January 2017 and September 2018

with monthly sales above 30,000 EUR recorded at least once

(Value (MNF/EUR); 24 months as of launch)

1.400.000

1.200.000

J05C - ODEFSEY - 201701

1.000.000

Sales (MNF/EUR)

J05C - SYMTUZA - 201804

800.000 D05B - TREMFYA - 201807

M01C - XELJANZ - 201712

600.000 D05B - TALTZ - 201704

M01C - OLUMIANT - 201711

400.000

R03M - FASENRA - 201809

A10C - FIASP - 201809 R03L - TRIMBOW - 201804

200.000 A10C - XULTOPHY - 201808

R03L - TRELEGY ELLIPTA - 201807

D05B - KYNTHEUM - 201809 M01C - KEVZARA - 201803

0

MONTH 1

MONTH 2

MONTH 3

MONTH 4

MONTH 5

MONTH 6

MONTH 7

MONTH 8

MONTH 9

MONTH 10

MONTH 11

MONTH 12

MONTH 13

MONTH 14

MONTH 15

MONTH 16

MONTH 17

MONTH 18

MONTH 19

MONTH 20

MONTH 21

MONTH 22

MONTH 23

MONTH 24

Source: IQVIA LMPB data

44Specific patterns cannot be traced when looking at generic products

separately Retail

Generic products launched between January 2017 and September 2018

with monthly sales above 30,000 EUR recorded at least once

(Value (MNF/EUR); 24 months as of launch)

500.000

450.000

Gx launched betwen Jan17 & Dec18 = 18,9M€

400.000

350.000

Sales (MNF/EUR)

75% coming from 4 molecules :

300.000 - Tadalafil

250.000 - Rosuvastatine

- Ezetimibe

200.000

- Ethinylestradiol

150.000

100.000

50.000

0

MONTH 1

MONTH 2

MONTH 3

MONTH 4

MONTH 5

MONTH 6

MONTH 7

MONTH 8

MONTH 9

MONTH 10

MONTH 11

MONTH 12

MONTH 13

MONTH 14

MONTH 15

MONTH 16

MONTH 17

MONTH 18

MONTH 19

MONTH 20

MONTH 21

MONTH 22

MONTH 23

MONTH 24

Source: IQVIA LMPB data

45Hospital

46On the hospital market, Antineoplastic drugs lead in sales and growth,

adding €229m additional sales for the period Hospital

Top 10 ATC2 classes in values with growing and declining – Hospital

(MNF Euro Value (Mio.); MAT December 2018)

Antineoplastic agents (L01) Opdivo, Keytruda, Systemic antivirals (J05)

908 +35,4% Revlimid 83 -22,9%

Immunosuppressants (L04) 123 +8,7% Remsima, Inflectra Systematic antimycotics (J02) 20 -3,1%

Antihemorrhagics (B02) 104 +19,6% Novoseven, Advate, Kovaltry Psycholeptics (N05) 17 -1,3%

Ophthalmologicals (S01) 84 +12,8% Lucentis, Eylea Analgesics (N02) 17 -8,1%

Antiseptics and disinfectants

Immunoglobulins (J06) 79 +10,7% Multigam, Privigen 15 -2,3%

(D08)

Antianemics (B03) 78 +10,9% Aranesp, Injectafer Other gynecologicals (G02) 11 -0,7%

Drugs for acid related disorders

Other nervous system drugs (N07) 75 +15,6% Gilenya, Lemtrada, Bridion 10 -5,2%

(A02)

Imaging diagnostics (T01) 74 +16,3% Iomeron, Dotarem, Visipaque Psychoanaleptics (N06) 7 -1,1%

Piperacilline/Tazobactam,

Systematic antibacterials (J01) 65 +6,5% Plasma expensers (K02) 4 -14,4%

Meropenem Fresenius Kabi

Hormono therapy (L02) 63 +26,8% Xtandi, Zytiga Lipid modifying agents (C10) 4 -21,6%

Source: IQVIA Hospital Audit

47On the hospital market, Antineoplastic drugs lead in sales and growth,

adding €229m additional sales for the period Hospital

Top 10 ATC2 classes in values with growing and declining – Hospital

(MNF Euro Value (Mio.); MAT December 2018)

Antineoplastic agents (L01) Epclusa, Viekirax, Systemic antivirals (J05)

908 +35,4% Daklinza 83 -22,9%

Immunosuppressants (L04) 123 +8,7% Cancidas Systematic antimycotics (J02) 20 -3,1%

Antihemorrhagics (B02) 104 +19,6% Xeplion Psycholeptics (N05) 17 -1,3%

Ophthalmologicals (S01) 84 +12,8% Paracetamol Fresenius Kabi, Dafalgan Analgesics (N02) 17 -8,1%

Antiseptics and disinfectants

Immunoglobulins (J06) 79 +10,7% Iso-Betadine 15 -2,3%

(D08)

Antianemics (B03) 78 +10,9% Syntocinon, Prostin E2, Dostinex Other gynecologicals (G02) 11 -0,7%

Pantomed Nycomed, Nexiam, Drugs for acid related disorders

Other nervous system drugs (N07) 75 +15,6% Losec Mups

10 -5,2%

(A02)

Imaging diagnostics (T01) 74 +16,3% Sipralexa, Cymbalta Psychoanaleptics (N06) 7 -1,1%

Systematic antibacterials (J01) 65 +6,5% Volulyte, Voluven, Geloplasma MRX Plasma expensers (K02) 4 -14,4%

Hormono therapy (L02) 63 +26,8% Crestor, Inegy, Ezetrol Lipid modifying agents (C10) 4 -21,6%

Source: IQVIA Hospital Audit

48The leaders on the hospital market remain consistent compared

to last period Hospital

Top 20 hospital companies sales and annual growth Growth since last MAT Market growth

(MNF Euro Values (Mio.); MAT December 2018) 19%

ROCHE 233,5 15%

MSD BELGIUM 185,8 +2 Keytruda 37%

NOVARTIS PHARMA 170,6 -1 12%

BRISTOL-M. SQUIBB 164,9 -1 Opdivo, Sprycel 20%

JANSSEN-CILAG 138,8 Imbruvica, Darzalex, Zytiga 34%

CELGENE 104,0 +1 Revlimid 25%

AMGEN 90,8 -1 3%

PFIZER+PFE BE 87,5 +9 Ibrance, Inflectra, Sutent, Ecalta 85%

SANOFI BELGIUM 75,2 -1 5%

TAKEDA BELGIUM 66,4 +3 Entyvio 34%

BAYER PHARMACEUTICALS 63,6 -1 9%

FRESENIUS KABI 59,9 -1 7%

ABBVIE 56,6 Maviret 32%

BAXTER 43,9 5%

CSL BEHRING 42,0 15,7%

GILEAD SCIENCES 40,3 -7 -38%

NOVO-NORDISK 38,5 +1 Novoseven 36%

ASTELLAS 32,5 -2 12%

ASTRAZENECA 32,0 Iressa, Lynparza, Tagrisso, Faslodex 19%

SHIRE PHARMACEUT. 29,4 +1 14%

Source: IQVIA Hospital Audit

49Consumer Health

50The Consumer Health market grew by 1.1% in the past year, driven by the

performance of the patient care category Consumer

Health

Consumer Health market – Belgium

(PUB Euro value; MAT December 2018)

Total Consumer Health Market €1,997m

Delta Absolute growth €21m 1yr growth +1.1% 5yr growth +1.8%

OTC €1,340m Registered €823m

15% +0.8% 1y growth +0.4% 1y growth

+1.4% 5y CAGR

18% PEC €354m

Non registered €517m

67% +0.4% 1y growth

+1.6% 1y growth

+2.1% 5y CAGR

PAC + NTR €302m

+2.8% 1y growth

+3.8% 5y CAGR

Source: IQVIA Consumer Health Services

51Most of the biggest Consumer Health classes are OTC but are

experiencing mixed performances Consumer

Health

Top 10 OTC classes in values with growing and declining – Consumer Health

(PUB Euro Value (Mio.); MAT December 2018)

01 Cough Cold 253 +4,3% Rhinathiol, Medica, Physiomer 02 Pain Relief 268 -0,3%

Promagnor, Tribvit,

04 Vit/Minerals/Nutrit.Suppl 194 +1,0% Folavit 82 Beauty Product For Women 116 -0,2%

03 Digestive/Oth Intest Rems 189 +1,0% Imodium, Movicol, Buscopan 10 Circulatory Products 81 -6,8%

06 Skin Treatment 90 +1,7% Iso-Betadine, Bepanthol, Cremicort H 07 Eye Care 62 -0,2%

83 Unisex Beauty Products 87 +7,1% Cicaplast LRP, Anthelios, Mouskito 35 Baby Foods 61 -1,5%

13 Calm Sleep Mood Enhancing 46 +5,7% Sedistress, Sediplus, Metasleep 86 Hair Products 46 -0,7%

56 Tests & Measuring Instr. 28 +1,1% One Touch Verio, Bayer Contour Next 12 Urinary And Repruduct Car 44 -2,5%

30 Spec Enteral Nutrition Pr 27 +4,1% Fortimel Com.Prote, Fresubin 2 Kcal 85 Personal Hygiene 44 -1,9%

47 Advanced Dressings 24 +8,8% Flaminal, Flamigel, Opsite 05 Tonics/Other Stimulants 42 -0,4%

57 Medical/Surgical Aids 23 +8,3% Krober Oxycure, Nexcare Coldhot 93 Oral Hygiene & Care Acce 17 -3,7%

Source: IQVIA Consumer

Health Services

52Most of the biggest Consumer Health classes are OTC but are

experiencing mixed performances Consumer

Health

Top 10 OTC classes in values with growing and declining – Consumer Health

(PUB Euro Value (Mio.); MAT December 2018)

01 Cough Cold 253 +4,3% Dafalgan, Voltaren Emulgel 02 Pain Relief 268 -0,3%

04 Vit/Minerals/Nutrit.Suppl 194 82 Beauty Product For Women 116 -0,2%

+1,0% Widmer Visage, Remederm, Widmer Yeux

03 Digestive/Oth Intest Rems 189 +1,0% Arterin, Cardioaspirine 10 Circulatory Products 81 -6,8%

06 Skin Treatment 90 +1,7% Preservision 3, Hyabak, Systane 07 Eye Care 62 -0,2%

83 Unisex Beauty Products 87 +7,1% Nutrilon (2), Nan Optipro HA, Nan 35 Baby Foods 61 -1,5%

13 Calm Sleep Mood Enhancing 46 +5,7% Nizoral-JPB, Dercos Shamp 86 Hair Products 46 -0,7%

56 Tests & Measuring Instr. 28 +1,1% 12 Urinary And Repruduct Car 44 -2,5%

Ymea, Canestene Gyn Clo., Prevalon

30 Spec Enteral Nutrition Pr 27 +4,1% Saforelle, PH5-Eucerin 85 Personal Hygiene 44 -1,9%

47 Advanced Dressings 24 +8,8% Biocure, A.Vogel (5), Tonixx 05 Tonics/Other Stimulants 42 -0,4%

57 Medical/Surgical Aids 23 +8,3% Corega, Protefix 93 Oral Hygiene & Care Acce 17 -3,7%

Source: IQVIA Consumer

Health Services

53Johnson & Johnson retains its leadership in Belgium Consumer

Health but the top 10 have overall seen negative performance Consumer

Health

Top 20 Consumer Health Companies Ranked by Sales Growth since last MAT Market growth

(PUB Prices €m, MAT December 2018) 1.1%

J&J CONS. 87,7 1,3%

GSK 75,8 -6,3% Voltaren Emulgel, Voltapatch Tissugel

BMS 66,2 +1 -2,4% Dafalgan, Sedergine, Niflugel

OMEGA PHARMA 63,0 -1 -7,9% XLS Medical, Arterin, Davitamon

SANOFI CHC 62,3 1,2%

RECKITT BENCKISER 58,8 -0,7%

TAKEDA BELGIUM 57,1 -2,8% Asaflow, Steovit, Magnecaps

MERCK CONS.HLTH 54,9 -2,3% Omnibionta

SMB LABORATOIRE 49,4 Algostase Mono, Neo-Golaseptine, Afebryl 4,6%

MEDA PHARMA 47,0 -0,4%

MELISANA 45,5 -0,2%

NUTRICIA 44,2 -2,1%

EG 40,3 Cetirizine

+1 EG, Paracetamol EG, Ibuprofen EG 11,2%

QUALIPHAR 39,7 +2 Medica, Toularynx, Mouskito 7,9%

TILMAN 39,6 -2 2,7%

LA ROCHE POSAY 39,0 -1 1,7%

METAGENICS 35,7 Probactiol, Curcudyn, Metasleep 5,5%

LOUIS WIDMER 29,8 -2,7%

NESTLE BELGILUX 29,1 OTC PEC 0,0%

VICHY 25,8 PAC NTR -4,3%

Source: IQVIA Consumer Health Services

54Biosimilars

552019 is expected to be the biggest year yet for biosimilars

Share of Sales in Belgium – Originators and Biosimilars

(MNF Euro Value (Mio.); MAT December 2018)

Therapy Area Molecule Product Share of sales Biosimilar Share of sales

Adalimumab Humira 100% Imraldi, Amgevita 0%

Etanercept Enbrel 94% Benepali 6%

Infliximab Remicade 71% Remsima, Inflectra, Flixabi 29%

Antineoplastic & Filgrastim Neupogen 73% Tevagrastim, Nivestim 27%

Immunomod. Trastuzumab Herceptin 100% Herzuma 0%

Rituxumab Mabthera 100%

Bevacizumab Avastin 100% Expected EU 2022

Nivolumab Opdivo 100% Expected in EU 2024

Insulin Glargine Toujeo, Lantus, Suliqua 98% Abasaglar 2%

Alimentary

Insulin Aspart Novorapid, Novomix 100% Expected in EU 2022

Blood Epoetin Alfa Eprex 88% Binocrit 12%

Genito, sex

Follitropin Alfa Gonal-F 76% Bemfola 24%

hormones

Hormonal Somatropin Genotonorm, Norditropin 82% Omnitrope 18%

Source: IQVIA MIDAS

56HCPs

57Amongst the General Practitioners, 4,545 of them are

responsible for 70% total market potential Prescriptions

Decile analysis

(Active GPs and Occupational GPs; prescription value (millions); MAT December 2018)

15,155 physicians

600 50%

45%

500

Prescription value (millions)

40%

35% 35%

400

Market share

30%

300 25%

555

20% 15% 20%

200 11%

15%

312

8%

228 10%

100 5%

169 3%

124 2% 1% 0% 5%

86 54 8 1

0 27 0%

D1 D2 D3 D4 D5 D6 D7 D8 D9 D10

AVERAGE prescription

value per doctor per year 366 206 151 112 82 57 36 18 6 1

(in thousands euro)

Source: IQVIA Xponent

58Digital promotional spending has slowly grown compared to traditional

spending, but levelled off in 2018 at 5%

Corporate website and mailing represent over 80% of digital spending

Digital vs. Traditional promotional Total Digital Spending

spend EU5

Total €m 144 136 137 130 116 Web advertising

GPs/Primary care Meetings

100% Detailing

4% 5% 6% 6% 5% 5% 0%

2%

Social Apps

media 1%

80% 11%

60% Mailing

20%

96% 95% 94% 94% 95%

40%

Corporate

website

20% 61%

0%

FY 2014 FY 2015 FY 2016 FY 2017 FY 2018 € 9m

Traditional Spending Digital Spending

Source: IQVIA ChannelDynamics

59When including Digital channels in the mix, it is important to target the

HCP’s who are receptive to these channels

60CONCLUSIONS

Hospital market is the key driver of the market growth, and

potentially as large as the Retail in a few years’ time

Despite the slow down and stability of the Retail market, the launch

performance and uptake will be an important driver for the Primary Care drugs

Biosimilars are part of the market pictures, with some of them

launched lately and a few others to come in the next years

Use of the Digital channels in the promotion mix will also require a

good tactical plan to be successful

61Thank you

You can also read