Global Inequality and the Global Financial Crisis: The New Transmission Mechanism

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Global Inequality and the Global Financial

Crisis: The New Transmission Mechanism

Photis Lysandrou •

Abstract

According to Marx the root cause of crisis always lies in the inequality of wealth engendered

by the commoditisation of labour power. If he was right it follows that the globalization of

commodity relations must lead to a crisis on a corresponding global scale unless the growth in

inequality is held in check. The fact that it was not checked but allowed to reach epic

proportions by the time the global financial crisis broke out is for many people confirmation

that Marx was right. This paper seeks to give weight to this view by explaining the new

mechanism through which the effects of exploitation are transmitted into crisis: prevented

from finding expression in an excess supply of products in GDP space, these effects have

instead found expression in an excess demand for securities in capital market space. Most

economists put the major blame for the financial crisis on the banks because it was they who

created the toxic securities that caused the financial system to seize up. My interpretation is

different. The banks certainly overreached themselves in creating these securities but the

principal reason why they did so was to augment the wealth storage capacity of existing

securities stocks in order to accommodate the build-up of private wealth.

Key words: global inequality; global financial crisis; crisis transmission mechanism;

two-commodity space theory

JEL Classification: G10; P16

1. Introduction

The financial crisis that began in the US sub-prime mortgage market and then spread

to the banking sector has since mutated into the most severe international economic

crisis since the great depression of the 1930’s. As it has done so, popular interest in

the theories of Marx has increased in like measure as evidenced by the rate at which

•

Address for correspondence: Professor Photis Lysandrou, London Metropolitan Business School,

London Metropolitan University, 277-281 Holloway Rd, London N7 8 HN.

E-mail: p.lysandrou@londonmet.ac.uk

his works have been flying off the shelves in Germany and other countries 1 . It is easy

to see why. According to Marx, crisis is endemic to capitalism as a commodity

producing system, first, because the commodity form by its very nature gives rise to

the possibility of a separation between supply and demand, and, second, because

periodic realisation of this separation comes from the fact that the value of the labour

capacity is generally less than the value of the output produced by it. In other words,

the root cause of crisis in Marx’s view is always to be found in the inequality of

wealth distribution engendered by the commoditisation of labour power. It follows

from this logic that the globalization of commodity relations, now more or less

complete following the end of colonialism and the more recent collapse of

communism, must at some point lead to a crisis on a corresponding global scale

unless the inequality of wealth distribution is held in check. The fact that it was not,

but on the contrary allowed to grow to epic proportions by the time the financial crisis

broke out in the US, is for many people confirmation that Marx was right.

This paper seeks to give analytical weight to this position by directing attention to one

key question: how did sub-prime backed securities get into the financial system and

cause it to seize up with such devasting consequences? It will be shown that the

answer has exactly to do with wealth inequality and a separation between supply and

demand. Faced with an excess of global demand for ordinary ground-level securities

(those issued by governments and private corporations the cash flows on which are

serviced directly out of their revenue streams), the financial system responded not

only by expanding the supply of first-tier securities (those issued by banks the cash

flows on which are serviced by the interest payments on various types of loans) but

also the supply of second- and higher-order tier securities (securities backed by pools

of securities). The observation that it was the highly complex and opaque nature of

these financial instruments that helped to cause the complete break-down in trust

between the large commercial banks in 2007-8 is the single most important reason

why the majority of economists put the blame for the ensuing global crisis on the

financial system itself. My interpretation is different. The system certainly

overreached itself in creating and distributing structured securities that turned out to

be highly toxic, but it did so principally because of the external pressures placed upon

1

Connolly (2008)

it to supply those securities and a major source of those pressures can be traced right back to the enormous concentration of wealth ownership. The structure of this paper is as follows. Section two outlines the major explanations for the global financial crisis. Section three explains the reasons behind the emergence of a global excess demand for securities. Section four explains the pressures on the financial system to resolve this excess demand problem. Section five explains why the crisis transmission mechanism has shifted from the space of material commodities to the space of financial commodities. Section six gives some conclusions. 2. Some explanations for the global financial crisis. The global financial crisis originated in the market for collateralised debt obligations, structured financial products that were created by pooling mortgage-backed securities (mainly comprising those backed by sub-prime and other nonconforming mortgage loans) with other asset backed securities as backing collateral. The use of sophisticated credit enhancement techniques in the construction of these products was supposed to have made them safe. However, when the delinquency rate among US sub-prime borrowers began to rise sharply in the wake of the increases in the Federal Reserve rate from late 2005, not only did these sophisticated techniques not prevent a resulting fall in the prices of CDOs, they actually helped to accelerate the rate of that fall by virtue of having helped to make these products too opaque and hence too difficult to value accurately. It was the panic caused by the unexpectedly rapid collapse of the CDO market that led to the breakdown in trust between the large commercial banks (many of whom owned or sponsored investment vehicles that were directly exposed to this market), a breakdown that proved to be catastrophic insofar as it was the catalyst setting in motion a liquidity-solvency crisis spiral that eventually culminated in the paralysis of the whole financial system. According to the official view, “the root cause of the crisis was a widespread undervaluation of risk” 2 . As a matter of description, this view is correct in that the crisis would not have occurred in the form that it did had sub-prime backed securities

not entered the financial system and cause it to seize up. But the deeper question is, what led so many financial institutions to undervalue risk on so widespread a scale? The mainstream answer singles out various agency and institutional failures rather than any systemic weaknesses. These failures include: the overzealous quest for fees and commissions and the concomitant over-relaxation of lending standards on the part of the mortgage brokers and banks originating the sub-prime loans; the highly leveraged and chronically under-capitalised positions of the banks and of their investment vehicles; flaws in the risk assessment methods used by the credit rating agencies to rate the various financial products created by the investment banks; and, last but by no means least, the lack of proper oversight of the whole shadow banking system on the part of the regulatory authorities. The real economy enters into the picture in a somewhat benign way. The period spanning the last decade and a half has generally been characterised by a combination of relatively low and stable inflation with robust output growth, a phenomenon that has led both academics and policy makers to describe the period as the ‘great moderation’ or, as in the UK, the ‘great stability’ 3 . The argument is that this unusually long period of stability gave rise to complacency and lax behaviour all-round: on the part of households who over-borrowed, on the part of investors who over-lent, on the part of the banks and other financial institutions who intermediated the whole process, and on the part of the authorities who put too much trust in these institutions. The further contention is that what also served to encourage this laxity of behaviour in the Western financial markets was the continued growth of global imbalances 4 : the counterpart to excess liquidity and hence the credit expansion and over-borrowing in many of the developed economies was the ‘savings glut’ in the Emerging Market Economies, principally those of East Asia and the Middle East, a glut allegedly caused by the overcautious, even frugal, behaviour of EME governments, corporations and individuals. While mainstream economists admit that policy errors played a not insignificant role in the financial crisis, these errors tend to be seen as arising out of gaps in an 2 Jean Claude Trichet, President of the European Central Bank, Financial Times, November 13th, 2008. See also Goodhart (2007), the IMF (2008) and the Bank of England (2008) for similar statements. 3 See Bernanke (2004); Goodhart (2007)

otherwise sound macroeconomic policy framework. Heterodox economists by

contrast put the blame for the crisis squarely on that framework 5 . The contribution to

the crisis made by the many agency and institutional failures identified above is not

denied; rather, it is that the source of these failures is seen to be the neo-classical

theory inspired dogma that economic resources are allocated most efficiently when

the chief responsibility for their allocation is placed with the financial system in

general and with the capital markets in particular. This proposition is held to be

illusory because capital markets are believed to be inherently speculative in nature,

and because short term speculation is considered to be a poor basis on which to

organise resources given its potential conflict with the long term interests of industry.

National economies, it is argued, can only follow a continuously stable and efficient

growth path if the capital markets are closely monitored and controlled by

governments. On the contrary, if these markets are uncontrolled or too lightly

monitored, then speculative interests will take precedence over manufacturing

interests with the result that periods of economic stability will be punctuated by

episodes of turbulence and instability. What is more, if governments not only do not

adequately control the capital markets but also go so far as to give encouragement to

the growth in their size and weight in the economy, then it will inevitably be the case

that each episode of financial turbulence will be greater in scale and amplitude than

the previous one. From this perspective, the global financial crisis that originated in

the US mortgage market in 2007 is essentially nothing other than a culminating stage

of a process that dates back to the early late 1970’s and early1980’s, the point at

which the post-war Keynesian macro-policy framework began to give way to the neo-

liberal framework.

Although there are substantive differences between the mainstream and heterodox

explanations for the global financial crisis, there is one issue on which there is

common agreement and this is that the cause of the crisis is ultimately to be found in

the financial sector itself 6 . This agreement exists because neither camp has ever

4

See Bernanke (2005); Wolf (2009)

5

See, for example, Blackburn (2008); Wade (2008); Kregel (2008); Randall Wray (2008); Dore (2008)

6

This agreement is exemplified by the following statement by Kregel (2008): “In the current crisis, the

cushions of safety have been insufficient from the beginning – they are a structural result of how

creditworthiness is assessed in the new ‘originate and distribute’ financial system sanctioned by the

modernisation of financial services. The crisis has simply revealed the systemic inadequacy of theentertained the possibility of an excess global demand for securities the effects of

which infiltrated the financial system including that part connected with the structured

credit products. As a consequence, supply side factors are unanimously considered to

have been the driving force behind the growth of these products, while demand side

factors are seen as having played a largely passive and accommodating role. The

reality is that these latter factors played a far more active, one could even say

aggressive, role as a result of the pressures spilling over from the government and

corporate securities markets. This point is important because the moment that it is to

brought to the fore, it becomes clear that the reason for the widespread undervaluation

of risk that made the financial crisis possible had not merely to do with weaknesses in

particular financial institutions and practices, nor merely with the way that the

financial system is currently structured, but also with wider problems in the global

economy.

3. The excess demand for securities problem

The objection to the idea of demand side pressures in the global securities markets is

based partly on empirical grounds. As shown in figure 1, the rate of growth of the

world’s financial stock has outstripped that for world GDP over the past three

decades. The chief factor responsible for this growth has been the issuance of public

and private securities. Subtracting bank deposit money from the total financial stock

of $167 trillion outstanding at end-2006, this left $111 trillion worth of equities and

corporate and government bonds and $11 trillion worth of asset backed securities,

from which in turn a further $2 trillion worth of CDO’s had been constructed. (see

figure 2).

Figure 1

Growth of Global Financial Stocks

(US $Trillions)

evaluation of credit – or, what is the same thing, the undervaluation and mispricing of risk” (p.21).

Where the first half of this statement encapsulates the Minskyan critique of current financial

developments, the second half gives a characterisation of the root cause of the financial crisis that is

indistinguishable from that given by mainstream economists.(Source: McKinsey, 2008)

Figure 2

Composition of Global Securities Stocks, 2006

($trillions)

(Source: IMF, 2008)

Given the extraordinary growth of ordinary debt securities, it is difficult to see how an

excess demand for them could have risen to a point where its effects spilled over into

the other debt markets. This difficulty begins to disappear, however, when we

consider the scale and composition of the global demand for securities. As shown in

table 1, the four major sources of this demand in 2006 were: (i) the big institutional

investors: the pension funds, mutual funds and insurance companies; (ii) the

commercial banks many of whom, in response to the changes in household savingpatterns, have moved into the asset management business; (iii) governments, mainly

comprising those of Emerging Market Economies, who not only held substantial

amounts of US treasuries as currency reserves but were increasingly investing in the

securities markets through recently established Sovereign Wealth Funds; and (iv)

high net worth individuals.

Table 1

Major Holders of Securities, 2006

(US $Trillions)

Source: IMF (2008); Capgemini (2007); SWF Institute (2008); Conference Board (2008)

Empirics aside, the more important reason why an excess demand for securities is

generally considered impossible stems from the idea that the law of supply and

demand does not apply in the usual way in the financial markets because prices

respond to quantity movements here differently to the way that they respond in the

markets for goods and services. To quote from a recent article on the financial crisis

published by the Bank for International Settlements, in the real sector “an increase in

supply tends to reduce the equilibrium price and is hence self-equilibrating. By

contrast, in the financial sector, increases in the supply of funds (eg credit) will, up to

a point, create their own demand, by making financing terms more attractive, boosting

asset prices and hence aggregate demand. In a sense, a higher supply (of fundingliquidity) ultimately generates its own demand”. 7 This statement of a financial version of Say’s Law is put in flow terms; put in stock terms, the argument is that there cannot be an excess demand for securities because there will always be a corresponding level of supply due to the lowering of the cost of capital. This argument helps to explain why the sharp fall in bond yields and the tightening of yield spreads from about 2001 8 were seen as having been largely driven by psychological factors: infected by the general atmosphere of optimism and confidence in the real economy that had been stimulated by the years of the great stability, investors also became over-confident and hence overly willing to accept lower risk premiums 9 . Implicit in this argument is the assumption that investors basically view governments and corporations in the way that the latter view themselves, namely, as organisations whose function is to provide certain goods or services and who resort to external funding to help execute that function. This assumption has become an anachronism. Most investors today, if by no means all of them, view governments and corporations as organisations whose chief function is to supply securities that can serve as wealth containers, and whose ability to provide goods and services is the necessary means by which the tangibility of these wealth containers is maintained. From this standpoint, the recent developments in the global securities markets can be interpreted in a way that identifies them with those that typically occur in the product markets: just as prices of goods or services rise when the physical constraints on organisations prevent them from supplying enough quantities to match demand, so did the prices of securities rise (and yields fall) after 2001 because there were constraints on organisations preventing them from supplying securities with a sufficient enough wealth storage capacity to accommodate the build-up of global wealth. The major source of these constraints can be traced to the recent organisational changes in institutional asset management 10 . It is a general rule that whenever a 7 Borio (2008) p.13 8 High yield corporate bond spreads over US treasuries fell from 1200 basis points in 2001 to under 300 basis points in 2007 while Emerging Market bond spreads fell from 900 basis points to under 200 basis points over the same period (Borio, 2008). 9 Goodhart (2007), for example, argues that the ‘serious under-pricing of risk’ at the root of the financial crisis was in large part induced by the way that “persistent macro-economic stability led many to believe that macro-economic risks had been significantly reduced. The implication was that investment generally, and financial conditions in particular, were subject to less aggregate, macro- economic risk than in the past” ( p.3) 10 For a more detailed account of these changes see Grahl and Lysandrou (2006)

particular industry expands in scale, there is a corresponding shift towards more standardised forms of provision and the asset management industry is no exception. In place of the broad-based and discretionally managed portfolio that was previously the norm, more typical today is the narrow portfolio managed to a target risk-return ratio. Most of the big institutions now run hundreds of portfolios arranged along a risk- return continuum that begins with the giant beta factory portfolios that combine average market return with an average level of risk, while all other portfolios seek to add an extra amount of return at the cost of accepting a corresponding extra amount of risk. Through the strict separation of portfolios and their benchmarking against market indexes, the pension funds and other institutions can contain portfolio costs by matching the rewards given to individual managers to their performance; thus beta factory managers, for example, are paid substantially less than are the genuine alpha creators. As regards the retail sector, the new approach to asset management represents a cost efficient way of allowing popular access to its benefits on affordable terms; rather than personally advise retail clients on how best to invest their money, what the mutual funds now do is to make available various off-the-peg investment products and invite clients to choose the product that suits their particular risk appetite. The increasing standardisation and commoditisation of investment portfolios help to put into context the recent changes spearheaded by the institutional investors in the areas of transparency and disclosure, ratings metrics, accountancy standards, corporate law and corporate governance. Many of these changes have aroused a great deal of opposition on the grounds that the balance of power has swung too far in the direction of the investors holding securities and away from the organisations issuing them. While this reaction is understandable, it is also to some extent misplaced because it fails to take proper account of the recent change in the investor base and thus of the change in the way that securities are perceived. Where previously the typical investor was a small individual, a bank, or another corporation, none of whom had cause to see securities as anything but a means of financing the production of goods or services because none of them had cause to treat their investment portfolios as ‘products’ to be marketed to the public, the typical investor now dominating the

world’s capital markets is a pension or mutual fund or an insurance company and these investors on the contrary do have good cause to treat their portfolios as marketable products. Since the risk profiles of these products depend on the risk characteristics of their constituent securities, it follows that asset managers have to impose far stricter transparency and governance rules on security issuers if they are to carry out their basic function. This imposition is in principle no different to what goes on in other product markets: just as households and firms buying goods or services for consumption or production purposes expect them to meet with certain standards regarding material quality, so institutional investors buying securities for portfolio management purposes expect these to meet with well defined standards regarding risk quality. The problem with these new governance standards is that, while necessary to the commoditisation of securities, they at the same time exert a restraining effect on their global supply. There are two routes through which this happens. The first is through the impact on the behaviour of individual governments and corporations. There have always been certain norms regarding the amounts of securities that governments and corporations can safely issue, and these norms have always been violated to one degree or other. However, what is different today is that not only has there been a certain hardening of these norms (a process that also reflects their convergence at the global level) but also, and more importantly, that any transgression, no matter how small or trivial, can be instantly picked up and measured with forensic precision. Now when security issuers know that any idiosyncrasy on their part is certain to be factored into their ratings and thus into their capital raising costs, the more likely are they to try to conform in order to limit the costs of idiosyncrasy and this conformity includes keeping a tight rein on their external financial obligations. The second route is through the impact on regional capital market development. As shown in figure 3, the size differences across countries and regions in capital market terms are far higher than are their differences in GDP terms. It is particularly noteworthy that in 2006 the EME’s as a whole only accounted for 14% of the global stock of securities as compared with 30% of world output. Part of the story behind this is that the policy makers in these regions have deliberately held capital market growth in check because of a continuing preference for alternative, relation-based forms of finance. However, another part of the story is that the establishment of a market for securities that is

genuinely deep and liquid requires a legal, accountancy and governance framework

that is orders of magnitude stronger and more transparent than that required for the

material product markets.

Figure 3

(a) World Capital Markets: 2006

(US $Trillion)

US EU Jap EMEs Others

(b) World GDP: 2006

(US $Trillion)

US EU Jap EMEs Others

Source: IMF (2008)The differences in capital market size help to put into perspective the reasons why the

greater part of the assets managed by US and European institutional investors

continue to be assigned to domestic securities. This practice is often construed as

evidence of a continuing home or regional bias in institutional asset management, but

the word ‘bias’ implies that institutional investors have the option to diversify their

portfolios along geographical lines to a far greater extent than they do but choose not

to exercise that option 11 . The truth is that they have no such option. Faced with severe

limits on the amounts of transparent and reliable securities that are available outside

of the core capital markets, American and European institutional investors have of

necessity to concentrate their asset holdings in these core markets. This is problem

enough, but what greatly adds to it is that these investors face increased competition

in these core markets not only from other types of domestic investor but also from

foreign institutions and individuals. The scale of the increase in competition from this

direction became particularly marked in the period between 2001 and 2006 as was

evident in the volume of net capital outflows from the EMEs (see figure 4a), the

majority part of which was directed into the US markets (see figure 4b). As foreign

investors pushed into these markets thus putting more downward pressure on treasury

yields and also helping to tighten yield spreads, the greater was the corresponding

pressure on institutional investors to search for new sources of yield.

Figure 4

(a) EME Net Capital Flows

11

The observed regional ‘bias’ in institutionally held portfolios was one of the principal arguments(b) Net Capital Inflows (Av. 2001-6)

Source: McKinsey (2008)

While these capital flows in the period up to 2006 were certainly evidence of

imbalances in the global economy as has been pointed out by a number of

commentators, there are problems with the claim that these imbalances were

symptomatic of differences in regional behavioural patterns, notably, that the

Americans were not saving enough and the Asians for their part were saving too

much. It hardly makes sense to single out for special attention a ‘savings glut’ in the

Asian and other EMEs just before the outbreak of the crisis, when at that same time

the greater part of the surplus pools of capital in the world were held by US and

used by Hirst and Thompson (1999) to reject the idea of financial globalization.European institutional investors, banks and wealthy individuals. In retrospect, the

observed global imbalances had less to do with behavioural differences than with

capital market asymmetries. These asymmetries are substantive but they become even

more so when capital market size is measured in currency terms for while the US

dollar market remains the same, the eurozone market shrinks in size in the absence of

the UK sterling market and the EME markets simply disintegrate into fragments.

Given the preponderant size of the dollar market, it was inevitable that EME

governments and private investors would try to squeeze into this market for reserve

currency and other investment purposes thereby putting more downward pressure on

treasury yields and also helping to tighten yield spreads, and thus in turn forcing

domestic investors to search for new sources of yield.

The conclusion that falls out of the above is that the institutional investors were

victims of a problem that was partly of their own making: having forced through

stricter rules and codes of conduct for security issuers in the closing decades of the

last century, they then found themselves in the opening decade of this century chasing

yield because these rules made it impossible for securities stocks to grow at a rate

commensurate with the growth of global aggregate demand. However, the other

conclusion that also falls out of the above is that if the excess demand for investable

securities was a global problem, the attempts at solving it had to have a more localised

character. The observation that it was the US financial markets that were at the centre

of the financial crisis has led some commentators to say that it should be characterised

as a US crisis rather than as a truly global one 12 . This inference is in my view quite

simply wrong. Given the preponderant weight of the US capital markets in the global

financial system, and the corresponding international status of the US dollar as the

major reserve currency, it was entirely understandable why the world’s investors

looked to US financial institutions in particular to supply the extra financial products

that were needed to absorb the overflow of demand. These were the asset backed

securities.

4. The attempted resolution of the excess demand for securities problem

12

See Thompson (2009) and Nesvetailova and Palan (2009)Explanations for the growth of the US ABS market, which was particularly rapid in

the last decade (see figure 5), usually concentrate attention on the household demand

for credit. Some commentators present the expansion in this demand in terms of

cultural factors: US households, it is said, became too consumer-oriented, and thus

addicted to living on credit 13 . Others give a more plausible story that concentrates on

the material effects of globalisation, specifically those arising out of the increasing

relocation of manufacturing jobs to the relatively low wage areas of Asia and China in

particular: while helping to keep down wages and hence inflationary pressures in the

US, this relocation also meant that US low- to mid-income households had

increasingly to rely on credit as a means of survival 14 . From whatever angle the story

of consumer credit expansion is told, what tends to be backgrounded is the role played

by the global demand for asset backed securities. However, from the evidence

showing a tightening of yield spreads in the US ABS market from 2001 15 there is

good reason to believe that the demand for these securities from institutional

investors, both US and foreign, was in effect outstripping the rate of growth in their

supply. This rate, while impressive when compared with the rate for previous periods,

was still not high enough to satisfy expanding demand, and it could not be because the

bulk of the loans servicing these securities were given according to conventional

lending criteria.

13

See Manning (2000) and Langley (2006)

14

See Boushey and Weller (2006)Figure 5

Asset-backed securities issuance

(US $Billions)

Source: Bank of England (2008)

It is here that we come to the sub-prime products. Of the $11 trillion worth of asset

backed securities in 2006, about $6.5 trillion consisted of residential mortgage backed

securities, of which approximately a third consisted of securities backed by various

nonconforming loans 16 . The standard explanation for the growth of this part of the

mortgage market starts with the mortgage brokers and banks, who, in order to make

commission, gave loans to sub prime borrowers on terms that were far too easy and

then moves on to the role of the investment banks and credit rating agencies who, also

eager to make commission, were more than ready to create the sophisticated credit

products. This standard explanation then finally ends with a discussion of how

trusting and gullible investors were seduced into buying these products. This is not

quite accurate. The more accurate explanation is one that runs this story in the reverse

15

The ABS spread on US treasuries fell from 150 basis points in 2001 to under 50 basis points in 2006-

7. (IMF, 2008)

16

These broadly divided in jumbo loans (so-called because they had an above average loan to property

value ratio), alternative-A loans (alt A borrowers are just below prime borrowers in that, while having

no income documentation, they have a good credit history) and sub-prime loans (borrowers belonging

to the sub-prime category either have no credit history or an extremely poor one and include NINAs,

those with no income and no assets, and NINJAs, those with no income, no job and no assets).direction: in the frantic search for yield, investors put pressure on the investment

banks to supply structured credit products in ever greater quantities, and, in order to

be able to do this, these banks needed the mortgage originators to take whatever steps

were necessary to induce as many sub-prime borrowers as was possible to take out

mortgage loans.

Figure 6

Buyers of CDOs: 2006

(In percent)

Source: House of Commons (2008)

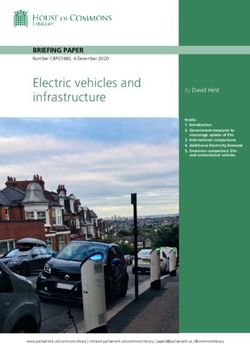

The vital clue that this reverse story is the more plausible explanation for the sudden

steep rise in sub-prime mortgage loans after 2001 is given by the composition of the

demand for CDOs (see figure 6). Approximately 52% of the CDOs outstanding at

end-2006 were held by banks, asset managers and insurance companies, while the

hedge funds held the other 48%. This ratio at first seems curious because at that same

time the hedge funds as a group held just over 1% of the world’s total stock of

securities of $122 trillion. The disparity, however, is easily explained. The basic task

of hedge funds is to generate for their clients (chief among whom were the high net

worth individuals 17 ) above average returns for which they get paid above average

fees. This task became increasingly difficult in the low-yield macro environment of

the early to mid- 2000’s because no matter how sophisticated the investmentstrategies used by the hedge funds to generate yield, there were limits to how much

could in fact be sweated and squeezed out of the existing securities and other asset

classes.

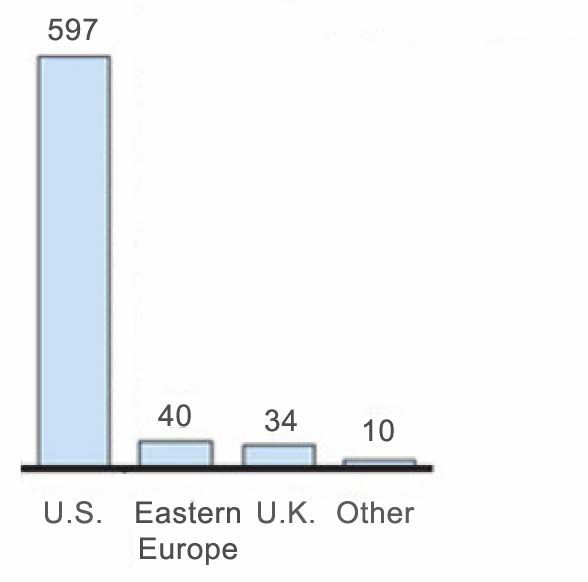

Figure 7

Growth of Hedge Funds

Source: Bank of England (2008)

Thus the hedge funds found themselves in a dilemma: on the one hand, more and

more assets were being placed under their management because other investors were

finding it difficult to generate yield (see figure 7); on the other hand, the hedge funds

were themselves finding it difficult to generate yield. It was because hedge funds

needed to resolve this dilemma that helps to explain why it was they who led the

search for alternative financial products that could give higher yields, and, when

finding that the structured credit products fitted this description, why it was they who

led the demand for them. Far from passively accepting the products provided by

suppliers, the hedge funds on the contrary pushed and prodded the suppliers into

providing these products at an ever-increasing rate. To quote from testimony given by

Gerald Corrigan of Goldman Sachs at a House of Commons hearing on the financial

17

According to the Bank of England (2008) in the period 2001-2007 wealthy individuals on average

accounted for about 50% of the assets placed with hedge funds, while banks, institutional investors and

sovereign wealth funds accounted for the other 50%.crisis: “To a significant degree it has been the reach for yield on the part of

institutional investors in particular that goes a considerable distance in explaining this

very rapid growth of structured credit products” 18 .

The growth of these products may have been very rapid, but apparently not rapid

enough to keep up with the demand for them and so the investment banks had to find

other ways of making up the shortfall. One way was by resecuritising unsold

mezzanine and other lower rated tranches of securities to create CDOs- squared, and

resecuritising any unsold mezzanine tranches of these instruments to create CDOs-

cubed. According to a recent IMF report, “These CDOs-squared and structured

finance CDOs were created almost solely to resecuritize MBS and CDO mezzanine

tranches, for which there was not sufficient demand from investors. Therefore their

value added in transferring risk is questionable” 19 . In my opinion, what is more

questionable here is the assumption that the CDOs squared and cubed were created

purely to transfer credit risk. This may have been part of their function, but their chief

purpose was to serve as wealth containers of a particular risk-return vintage. In the

whole universe of debt securities there are only a handful of banks and corporates and

about 20 to 30 sovereigns that have a triple A rating. The rest is filled with lower rated

matter. So when the banks found a way of creating thousands of extra AAA-rated

products 20 , it was only logical that investor demand would be concentrated on these

products, and it was equally logical that, rather than waste any unsold mezzanine and

equity tranches, the banks would collect all of these together to create the additional

senior tranches demanded by investors.

A further way of satisfying investor demand was through the supply of ‘synthetic’

CDOs, products created by the investment banks by taking a cash CDO as a reference

entity for two Credit Default Swaps entered into simultaneously: on the one side, the

synthetic CDO creator would sell protection to the counterparty in return for

payments of interest and principal; on the other, the creator would buy protection

from the counterparty and pay interest and principal. There were several variations on

18

House of Commons (2008; p.16)

19

IMF (2008), p.59

20

In a statement to the Council of Institutional Investors in April 2009, Lloyd Blankfein of Goldman

Sachs pointed out that “ In January 2008, there were 12 triple A- rated companies in the world. At the

same time, there were 64,000 structured finance instruments, like CDO tranches, rated triple A”.this theme. For example, cash flows in the credit default swaps would only involve the payment of interest: the ‘unfunded’ synthetic CDO. Or the reference entity for credit default swaps would be a particular tranche of a CDO rather than the whole CDO: the ‘single tranche’ synthetic CDO. It has been estimated that by 2006, the year before the crash, the supply of synthetic CDOs had grown to the point where they matched the supply of cash CDOs and what is particularly noteworthy is that among the leading institutions that had helped to drive this growth were the hedge funds, second only to the banks in the buying and selling of protection 21 . If the hedge funds were one of the principal conduits through which flowed the external pressures on the financial system to create the structured credit products, a principal source of those pressures in turn had to be the huge concentration of wealth ownership. Ultimately, it all comes down to simple arithmetic. Recall that on the eve of the crisis the global aggregate demand for securities came from four major groups: institutional investors, banks, governments and high net worth individuals. As regards the first three of these groups, there is some justification, or, at the very least, some plausible explanation, for the size of the demand for securities that was exercised. This hardly applies to the high net worth individuals who in 2006 numbered 9.5 million (a figure that represents just over 0.01% of the world’s population of 6.8 billion) and who had a combined wealth of $37 trillion, more than half of which, $19 trillion, was in securities (a figure that represents just under 10% of the total financial claims on the world’s governments and large corporations) 22 . Taking these figures in conjunction with the observation that the high net worth individuals were by far the most important suppliers of finance to the hedge funds who in turn were the chief buyers of CDOs, it follows that had the wealth of these individuals been more evenly dispersed in the global economy the pressures on the financial system to augment the wealth storage capacity of existing securities stocks would have eased sufficiently so as not to force it into creating the toxic securities on the scale that it did and the financial crisis would not have occurred when it did. 21 The hedge funds’ share of protection buying went from 16% of the total in 2004 to 28% in 2006, while their share of protection selling went from 15% to 31 % in the same period, (IMF, 2008). 22 This figure understates the degree of wealth concentration because to qualify as an HNWI one only needs assets to exceed liabilities by $1million, which is not a high hurdle in this age. The truth is that

5. The new crisis transmission mechanism Marx was right. Exploitation and wealth inequality are usually at the root of crises in a commodity producing system, and so also were they at the root of this global financial crisis. To put this argument is neither to ignore nor to excuse the many failings and errors on the part of the various financial institutions that supplied the structured credit products that were at the epicentre of the crisis. The point is that important as were these factors, they were facilitating factors nonetheless, factors that helped to bring the crisis to fruition and give it amplification. The causal factors lay outside of the financial sector, in the growth of wealth inequality that had been allowed to reach unsupportable proportions by the early part of this century. If the majority of economists refuse to give credence to this idea, it is because there appear to be insuperable difficulties with Marx’s insights into capitalist crises and exploitation that prevent them from serving as a useful framework for understanding contemporary developments. However, these difficulties are only insuperable on the assumption that Marx’s insights are inseparable from the traditional theoretical form into which they have been cast and this assumption is wrong. Consider first the crisis transmission mechanism. The standard Marxian construction of this mechanism is basically as follows 23 : the payment of wages at the value of the labour capacity is at once the primary source of profits and the source of constraints on their realisation; these constraints can never be eliminated but they can be temporarily suspended by various means, including the expansion of credit; when these means are finally exhausted and the constraints on profits again begin to tighten, the resulting cutbacks in capital investment and accompanying rise in lay-offs trigger an economic crisis. Now the opening part of this sequence does accord reasonably well with what has been happening in the global economy: the share of wages in the national incomes of the most advanced economies have been falling since the 1970s 24 , a trend that has been reinforced by the massive influx of labour into the global labour pool following the collapse of the communist systems and the the bulk of wealth is held by what are labelled as ‘ultra’ HNWIs, those with net assets in excess of $30 million. 23 For a lucid summary of the different versions of the Marxian theory of crisis see Evans (2004) 24 See Glyn (2007)

integration of China into the world market 25 , and realisation problems have accordingly become more pressing as attested by the chequered performance of profit rates in the core regions of the world capitalist system 26 and by periodic crises in its peripheral regions. By contrast, the latter part of the sequence does not accord so well with recent events. Although the realisation constraints on profits were never eliminated, they continued to be eased to a sufficient enough extent as to prevent them from being the catalyst triggering a global economic crisis. When this crisis did eventually break out, its origins lay not in the market for corporate debt or in the market for corporate equity, but in the market for mortgage-backed securities, that is to say, in that part of the financial sector that had the least connection with corporate profitability. Although a number of writers have tried to get round this peculiarity in their explanations of the global financial crisis by adding various supplementary stories to the orthodox Marxian theory of crisis (stories that essentially boil down to the same critique of financial institutions and practices as has been given by others) the fact that these explanations remain centrally focussed on corporate profitability means that it is unlikely they will command much support 27 . The reality is that a new crisis transmission mechanism has emerged following the recent changes in the size and structure of the capital markets. At the time that Marx was writing these markets were still in their infancy. In fact, they remained relatively underdeveloped until about 1980, for at no time prior to that date were the global stocks of securities anywhere near comparable to the level of world output. Since that date the reverse has been true. The world’s governments and large bank and non-bank corporations have been colonising the future to escape the constraints of the present and, as a consequence of this colonisation, the effects of global exploitation and wealth inequality have been forced to find a different form of expression: prevented from surfacing in GDP space in the form of an excess supply of material products – because the demand for these products had successfully been propped up by a number of supports that included high levels of public expenditure on the one hand and 25 For estimates of the size of this influx see IMF (2007). 26 See Brenner (2006) and Glyn (2006) 27 Explanations for the financial crisis given from an orthodox Marxian standpoint can be found in Monthly Review, International Socialism and in a host of other left wing periodicals.

increased credit to the private sector on the other – these effects have surfaced instead in capital market space in the form of an excess demand for securities. That they did so ultimately comes down to the ambivalent impact of the institutional asset management industry on securities stocks: although the growth of this industry has helped to drive the expansion in the demand for securities, thereby helping governments and corporations to transcend current income constraints on their operations to a far greater degree than would otherwise have been possible, the accompanying shift towards the commoditisation of investment portfolios has necessitated the imposition of certain rules and obligations on security issuers that, while needed to concretise the risk characteristics of portfolios, served to restrain the rate of security issuance. This restraining effect did not become a problem as long as the overall global demand for securities grew at a pace with which the global supply could keep up. However, it did become a problem after 2001 when the demand for securities began to accelerate due to the rapid accumulation of wealth seeking a suitable form of wealth storage. As already noted, the financial sector responded to this pressure of demand by creating structured credit products that were difficult to price and trade against market standards; and, as also noted, when this difficulty proved to be a critical factor in the breakdown of trust between the banks that was in turn responsible for the mutation of the sub-prime crisis into a global financial crisis, the banks took the major blame for causing the crisis. Although not without foundation, this criticism misses the essential point that had the banks stuck to the established rules for giving mortgage loans and to the conventional methods for securitising these loans, they could never have created the extra securities in the amounts needed to absorb the overspill of global demand. The only way that they could even begin to achieve this objective was precisely by breaking the established rules of lending and by resorting to highly unconventional methods of securitisation 28 . It is of course true that a great deal of money was made 28 Goodhart (2007) has stated that “the trigger for the crisis was, as everyone knows, the rising defaults in the US sub-prime mortgage market, but…the trigger could have been almost anywhere else. It was …an accident waiting and ready to happen ”. I strongly disagree with this statement. The crisis was not

out of the millions of subprime and other nonconforming borrowers whose mortgages provided the raw material from which the CDOs were constructed; but in the final analysis it was not greed, nor complacency, nor even hubris, that drove the banks and their associates to break the rules of commodity exchange so much as the attempt to out step the limits of the commodity system. Consider next the process of capitalist exploitation. The orthodox Marxian theory construes this process as a class-based one: the working class produces the surplus, while the capitalist appropriates this surplus and then distributes it within its ranks. Given the sheer diversity of today’s high net worth individuals in terms of occupation, background and social status, it is simply impossible to apply this orthodox view of exploitation as an explanation for the observed global inequality of wealth distribution. Indeed, any attempt to do so only serves to reinforce the contrary position that exploitation does not exist or that, if it does, it takes place in a way that is entirely unconnected with anything that Marx had to say. The truth of the matter is that in Marx’s own analysis of capitalism the locus of exploitation is to be found in the relation between commodities rather than in the relation between classes. Marx begins his major work Capital with the single commodity 29 . He took the commodity to be the representative unit of analysis because capitalism was the first system in history to be based on generalised commodity production, and it came to be so because the commodity principle was for the first time stretched to encompass labour power. With this unique development, all previous relations of exploitation now began to be dissolved into the relations of market exchange: while the differences between capitalists and workers in terms of their respective positions and powers are necessary to the extraction of a surplus, the sufficient condition for this extraction lies in the pricing of the different capacities possessed by these opposing groups against an ‘accident’ but an inevitability given the accumulation of wealth seeking a suitable form of storage, and the trigger could not have been anywhere other than in the US sub-prime mortgage market, first, because all other markets had already been tapped to the full for the material needed to create the securities with extra storage capacity, second, because this market was the one market which required breaking the usual rules of transparency and risk evaluation if it too was to be tapped for the necessary security building material, and, third, because had these rules not been broken the trust between the banks would have remained intact and the problems in the mortgage sector would not have led to a crisis of the whole financial system. 29 For a more detailed account of the microfoundations of Marx’s economic theory see Lysandrou (1996).

market standards 30 . Since Marx’s time, the commodity principle has been further

stretched and deepened so that it now encompasses every possible entity in the world;

not only every good or service produced in it, or even every capacity that is used to

produce them, but also every financial claim on those capacities 31 . Along with the

globalisation of the commodity principle there has been a corresponding dissolution

of all parochial relations of exploitation into the exchange relations of the global

market. In effect, a global commodity system has come into operation and every

individual on the planet occupies a point somewhere in that system. Most individuals

do so merely as possessors of a capacity for labour; others do so as possessors of other

capacities and/or of various claims on capacities. The majority of individuals put more

into the global commodity system than they take out, while a minority of individuals

take out more than they put in, and a tiny minority of this minority take out far, far

more than they put in. The problem is that, having taken out far more than they can

possibly spend on themselves in current consumption, this tiny minority of individuals

then seek to put the surplus back into the system in the form of claims on the future

income streams created by others so as to secure their own future consumption.

6. Conclusions

The global financial crisis was not caused simply because toxic assets had got into the

global financial system, but because the volume of those assets had grown to the point

where the system could no longer cope. This point of critical mass was only reached

because of the pressure of demand, and a principle source of that pressure was the

huge concentration of wealth ownership. The clear implication that falls out of this

line of argument is that the world’s wealth has to be more equitably distributed if

global financial crises are to be avoided. To give priority to this policy is not to

exclude the many other proposals that have been suggested for making the banking

sector and entire financial system more transparent, more efficient and, above all,

more accountable. On their own, however, these proposals are insufficient. No matter

how radically the financial system is reformed or restructured, as long as there remain

external pressures on it to create products or to indulge in practices that are harmful to

it, such products and practices will continue to be introduced and financial crises will

30

This argument is developed in Lysandrou (2000).continue to occur. These external pressures will only be removed when there is a

significant re-distribution of wealth, and what this entails as a first step is globally

coordinated action in key areas of tax policy that should include the closure of tax

havens to prevent tax avoidance, the harmonisation of national tax structures to

prevent the exploitation of differences between them and the realignment of tax rates

to ensure that the tax burden is again distributed on a progressive basis. In short, what

is needed is a globalised version of Keynesianism.

This proposal may seem paradoxical in the context of a paper that purports to give a

Marxist analysis of the financial crisis. There is no paradox, however, because there is

no Marxist solution to capitalist crises that is essentially different from a radical form

of Keynesianism. It used to be widely believed that there was such a solution, namely

that as put into practice in the communist systems between 1917 and 1989. As it

turned out, this proved to be no solution at all because far from progressing beyond

capitalism these systems actually regressed back to a form of feudalism albeit with

20th century structures and trappings. The cardinal lesson arising out of this regression

is that simply suspending or suppressing the commodity principle will not solve the

problems of capitalism.

In the final analysis, only three types of social system are possible: pre-commodity

systems, the commodity system, and a post- commodity system. Humanity will one

day move to a stage of development where it will no longer have to rely on markets to

allocate resources. However, to get to that stage it is necessary to work with the

present commodity system and tap its potential for generating material growth while

at the same time bringing it under democratic control so as to contain its other

potential for generating wealth inequality. If there is any one positive thing that may

come out of this global financial crisis, it is that it can possibly open the way to

establishing that democratic control.

31

This argument is developed in Lysandrou (2005).Biblography Bank of England (2008), Financial Stability Report, October Bernanke, B (2004), The great moderation, Remarks to Easter Economic Association, Washington DC, February Bernanke, B (2005), The Global Saving Glut and the US Current Account Deficit, The Sandridge Lecture, Virginia Association of Economics, Richmond, Virginia Blackburn, R (2008) The Subprime Crisis, New Left Review, No 50 Brenner, R (2006), The Economics of Global Turbulence, Verso Blankfein, Lloyd C (2009), Remarks to the Council of Institutional Investors, April Borio, C (2008), The financial turmoil of 2007 -?: a preliminary assessment and some policy considerations, BIS Working Papers No 251, March Boushey, H and Weller, Christian E (2006), Inequality and Economic Hardship in the United States of America, DESA Working Paper No 18, April Capgemini (2007), 11th World Wealth Report, June Conference Board (2008), Institutional Investment Report, September Connolly, K. (2008) Booklovers turn to Karl Marx as financial crisis bites in Germany, www.pragoti.org/node/2241, 22 December Dore, R (2008) Financialisation of the Global Economy, Industrial and Corporate Change, Volume 17, Number 6 Evans, T (2004), Marxian and post-Keynesian theories of finance and the business cycle, Capital and Class, Summer Glyn, A (2006), Capitalism Unleashed: Finance, Globalization and Welfare, Oxford University Press Glyn, A (2007), Explaining Labour’s Declining Share in National Incomes, G-24 Policy Brief No 4 Goodhart, C.A.E, The Background to the 2007 Financial Crisis, Financial Markets Group, London School of Economics Grahl, J and Lysandrou, P (2006), Capital market trading volume: an overview and some preliminary conclusions, Cambridge Journal of Economics, Vol.30, No 6 Hirst, P and Thompson, G (1999), Globalisation in Question, Polity House of Commons (2008), Treasury Committee, Report on Financial Stability and Transparency, 26th February, 2008, International Monetary Fund (2007), World Economic Outlook, April International Monetary Fund (2008), Global Financial Stability Report, April

You can also read