HSBC Asia Seminar for Investors and Analysts - Day 3 afternoon presentations - HSBC Group

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

HSBC Asia Seminar for Investors and Analysts Day 3 afternoon presentations Date: 11 April 2018

HSBC Asia Seminar for Investors and Analysts Important notice and forward-looking statements Important notice The information, statements and opinions set out in this presentation and subsequent discussion do not constitute a public offer for the purposes of any applicable law or an offer to sell or solicitation of any offer to purchase any securities or other financial instruments or any advice or recommendation in respect of such securities or other financial instruments. The information contained in this presentation and subsequent discussion, which does not purport to be comprehensive nor render any form of financial or other advice, has been provided by HSBC Holdings plc and its subsidiaries (the “Group”) and has not been independently verified by any person. No responsibility, liability or obligation (whether in tort, contract or otherwise) is accepted by the Group or any member of the Group or any of their affiliates or any of its or their officers, employees, agents or advisers (each an “Identified Person”) as to or in relation to this presentation and any subsequent discussions (including the accuracy, completeness or sufficiency thereof) or any other written or oral information made available or any errors contained therein or omissions therefrom, and any such liability is expressly disclaimed. No representations or warranties, express or implied, are given by any Identified Person as to, and no reliance should be placed on the accuracy or completeness of any information contained in this presentation, any other written or oral information provided in connection therewith or any data which such information generates. No Identified Person undertakes, or is under any obligation, to provide the recipient with access to any additional information, to update, revise or supplement this presentation or any additional information or to remedy any inaccuracies in or omissions from this presentation. Forward-looking statements This presentation and subsequent discussion may contain projections, estimates, forecasts, targets, opinions, prospects, results, returns and forward-looking statements with respect to the financial condition, results of operations, capital position and business of the Group (together, “forward-looking statements”). Any such forward-looking statements are not a reliable indicator of future performance, as they may involve significant assumptions and subjective judgements which may or may not prove to be correct and there can be no assurance that any of the matters set out in forward-looking statements are attainable, will actually occur or will be realised or are complete or accurate. Forward-looking statements are statements about the future and are inherently uncertain and generally based on stated or implied assumptions. The assumptions may prove to be incorrect and involve known and unknown risks, uncertainties, contingencies and other important factors, many of which are outside the control of the Group. Actual achievements, results, performance or other future events or conditions may differ materially from those stated, implied and/or reflected in any forward-looking statements due to a variety of risks, uncertainties and other factors (including without limitation those which are referable to general market conditions or regulatory changes). Any such forward-looking statements are based on the beliefs, expectations and opinions of the Group at the date the statements are made, and the Group does not assume, and hereby disclaims, any obligation or duty to update, revise or supplement them if circumstances or management’s beliefs, expectations or opinions should change. For these reasons, recipients should not place reliance on, and are cautioned about relying on, any forward-looking statements. No representations or warranties, expressed or implied, are given by or on behalf of the Group as to the achievement or reasonableness of any projections, estimates, forecasts, targets, prospects or returns contained herein. Additional detailed information concerning important factors that could cause actual results to differ materially is available in our Annual Report and Accounts for the fiscal year ended 31 December 2017 filed with the Securities and Exchange Commission on Form 20-F on 20 February 2018 (the “2017 20-F”). This presentation contains non-GAAP financial information. The primary non-GAAP financial measure we use is ‘adjusted performance’ which is computed by adjusting reported results for the period-on-period effects of foreign currency translation differences and significant items which distort period-on-period comparisons. Significant items are those items which management and investors would ordinarily identify and consider separately when assessing performance in order to better understand the underlying trends in the business. Reconciliations between non-GAAP financial measurements and the most directly comparable measures under GAAP are provided in the 2017 20-F and the Reconciliations of Non-GAAP Financial Measures document which are both available at www.hsbc.com. Information in this presentation was prepared as at 6 April 2018.

HSBC Asia Seminar for Investors and Analysts Day 3 afternoon presentations Business Corridors, Belt and Road 03 ASEAN introduction, panel discussion and Q&A 20 Sustainable finance 35 Closing remarks 46 Appendix 49 Glossary 52

Business Corridors, Belt and Road 11 April 2018 Mukhtar Hussain Chief Executive Officer, Malaysia

Business Corridors, Belt and Road Agenda HSBC’s network – strength of the franchise Overview of the Belt and Road Initiative HSBC’s unique positioning as the “Go to Bank” for BRI

Business Corridors, Belt and Road: HSBC’s network – strength of the franchise

Our global presence allows us access to c.90% of global trade and capital

flows

HSBC footprint

Home Priority Network Rep office

67 countries and territories

Our network covers

90

countries accounting for

more than 90% of global

GDP, trade and capital

% flows

Our international

50

> %

network supports

more than 50% of our

client revenue

Inter-connected global

4 businesses share

balance sheets and

liquidity in addition to

strong commercial links

25 China desks

5Business Corridors, Belt and Road: HSBC’s network – strength of the franchise

Trade flows increasingly centred around Asia, helped by BRI

Global 20 top trade corridors1 Key takeaways

2010 2030E

3x Further integration in ASEAN,

USD10.0tn RCEP2, as well as the Belt and

Road initiative are expected to

USD6.5tn 14

deliver additional trade growth in

USD4.0tn Asia

USD2.1tn 12

Mainland China expects its annual

Top 20 Asia at No. of Top 20 Asia at No. of trade with the more than 65

corridor value either end corridors corridor value either end corridors

countries along the Belt and Road

routes to surpass USD2.5 trillion

14 of Global 20 top trade corridors by 2030 will have Asia at either end1 in the next decade, up from about

USDbn USD1 trillion in 20153

2010-30 8% 8% 9% 5% 20% 6% 12% 9% 3% 12% 9% 10% 6% 11% Activity arising from these corridors

CAGR:

1,303

to drive urbanisation, which will

1,158 have a material impact on

640

regional economic growth

536 462

321 305 284 279 262 261 249 205 199

UAE

USA

India-

India-

China-

HK

China-

USA

China-

China-

China-

Australia-

China-

China-

USA

China-

USA

Korea-

Germany

China

Japan-

Korea

China-

Japan

India

Malaysia

Singapore

Vietnam

1. Source: Oxford Economics

2. Regional Comprehensive Economic Partnership accord is a mega-regional trade deal covering 16 countries in the Asia-Pacific region

3. Xi Jinping in 2015 Boao Forum, Xinhuanet, 29MAR15 6Business Corridors, Belt and Road: HSBC’s network – strength of the franchise

Majority of Group priority corridors are related to Asia, especially China

Corridor performance in 2017 has grown three times the rate of GDP and Asia-Pacific growth

HSBC Group priority corridors

(not ranked in terms of revenue size)

1. China ↔ Hong Kong Comparison with selected

2. China ↔ United States market growth rates2:

3. China ↔ Germany

Example

on slide 9 4. China ↔ Australia

5.

6.

China ↔

China ↔

India

Singapore

+ 15%1 GDP growth 2017:

7. China ↔ Malaysia The top 17 Asia

8. China ↔ United Kingdom

9. China ↔ United Arab Emirates

corridors have

grown 15% Y-o-Y

+ 11%1 China 6.8%

10. China ↔ Canada vs. 4.4% Asia-

11. China ↔ Saudi Arabia pacific GDP

The top 25 Hong Kong 3.7%

12. China ↔ France growth

corridors have

13. Hong Kong ↔ United States grown 11% Y-o-Y India 6.7%

14. Hong Kong ↔ United Kingdom vs. 2.9% world

15. India ↔ United Kingdom GDP growth

16. India ↔ United Arab Emirates

17. India ↔ United States Real export growth 2017:

18. United Kingdom ↔ United States

19. Canada ↔ United States China 5.6%

20. Mexico ↔ United States

21. Germany ↔ United States Hong Kong 5.3%

22. Germany ↔ United Kingdom

23. France ↔ Germany India 3.4%

24. France ↔ United Kingdom

25. Saudi Arabia ↔ United States

1. Growth rates exclude FIG

2. HSBC Global Research

7Business Corridors, Belt and Road: HSBC’s network – strength of the franchise

BRI is a part of our execution of the business corridors strategy

Asia’s international revenue growth is led by mainland …with top growth areas of China outbound coming

China…. from countries along the Belt and Road

USDbn, 20171

Y-o-Y growth (%) Y-o-Y growth (%), 2017

Asia inbound from

Saudi Arabia 16

other Regions 13%

Vietnam 12

Asia outbound to

other Regions 13% UAE 10

Indonesia 8

Intra-Asia 8%

Singapore 4

BRI Country

Asia-ex China China on one side of the corridor

1. HSBC data

8Business Corridors, Belt and Road: HSBC’s network – strength of the franchise

A business corridor offers multi-faceted opportunities for a universal bank:

a case study – Australia and China

Business corridor: two-way flows Market trends HSBC response / action

Mainland China is Australia’s top trading partner

with c.AUD155 bn trade volume1; however with

tariffs declining for many goods & services due Gaining ground in cross-border transaction

Goods & services to the ChAFTA2 DEC15 banking, especially for the middle-market8

1

trade Mainland China is a major consumer of hard Recently hired an agri-business specialist to

and soft commodities e.g. taking over half of iron target this sector

and aluminium exports where Australia is the

world’s #1 and #4 exporter, respectively3 Supporting recent expansion of Australian

pharma and med-tech companies in China

Mainland China securing access to

as well as Chinese acquisition of a private

infrastructure technology and mineral resources

healthcare services provider

via M&A

2 Capital flows Mainland China’s 5 year plan in upgrading With a retail branch network and Global

technology across many sectors, including Premier online platform, HSBC has been

healthcare4 growing the RBWM business in Australia.

Australia had c.1.4m tourists from China in Strengthened collaboration between RBWM

2017, up by 12% Y-o-Y5 referrals from China to Australia; develop

Higher education continues to be a strategic the China Australia Mortgage proposition

sector with strong demand seen from mainland

3 Wealth flows China into Australia - up to 38% of total

international students6

Introduced the ‘Significant Investment Visa’

migration scheme during 2012-137

1. Source: Australian Government Department of Foreign Affairs and Trade

2. China Australia Free Trade Agreement

3. HSBC Research; Australia Dept. of Industry, Innovation and Science reports on Aluminium (Dec 2016) and Iron (Dec 2016)

4. The State Council, The People’s Republic of China

5. Tourism Australia

6. Australia Gov Statistics - Based on government statistics, as at DEC17, international students studying Higher education from China made up 38% of total international students

7. Australia Gov

8. East & Partners 19FEB18 HSBC Bank Australia is gaining ground among the middle-market as a preferred transaction banking (TB) provider, as Corporates seek out Cross-Border Payment and International TB capabilities, new 9

research from East & Partners shows. Over the last five years, HSBC expanded its primary relationship transaction banking market share among the Corporate (annual turnover of AUD20-725 million) segment by 17%Business Corridors, Belt and Road: HSBC’s network – strength of the franchise

Case study: HSBC’s ability to support China outbound: Australia

China Communications Construction Co. Ltd (CCCC) is a long-standing GB customer of more than HSBC demonstrated strong international

25 years. Key products provided to this group include GLCM, GTRF, GM, C&L, DCM, Project structuring capability by providing a global

Finance and ECM financing solution given the cross-border nature

HSBC supported CCCC with its 100% acquisition of John Holland Group Pty of the transaction

The transaction represented one of the largest China outbound cross-border acquisitions into HSBC further strengthened itself as a key

Australia and the largest single investment for CCCC banking partner to CCCC through this

CCCC is a leading A&H dual listed company mainly engaging in design and construction of transaction. HSBC is well-positioned to leverage

transportation infrastructure, dredging and heavy machinery manufacturing business its global network and strong connectivity

among various product groups to support

John Holland is one of Australia’s leading engineering, contracting and services providers to CCCC’s future financing needs

infrastructure, energy, resources and transport services sectors

2015 2016 2017

CCCC’s acquisition of CCCC’s acquisition of GLCM provider John Holland Bonding Capital Metro PPP, Host to Host Upcoming NSW PPP

John Holland Group John Holland Group Facility ACT Connectivity Project

AUD1.1bn AUD1bn AUD1bn AUD633m AUD4bn

APR15 APR15 JUL15 MAY16 MAY16 SEP16 2018

HSBC acted as HSBC acted as HSBC was Mandated HSBC acted as HSBC acted as HSBC implemented HSBC looking to

Mandated Lead Mandated Lead as John Holland’s Mandated Lead Mandated Lead Host to Host provide PPP Project

Arranger for CCCC’s Arranger and offshore GLCM partner Arranger for the Arranger, Lender and Connectivity across all Finance and

USD1.1bn bridge loan Bookrunner for John bank. New account extension and reduction Hedge Provider on the countries to automate Receivable Financing to

facility in support of its Holland’s AUD1.0bn 3- subsequently opened in in pricing of John AUD633m project connectivity between support CCCC in its bid

100% acquisition of year syndicated Singapore, Malaysia Holland’s AUD1bn financing for the John Holland and

John Holland Group Pty performance bond to and New Zealand bonding facility AUD713m Capital HSBC

support John Holland Metro PPP in the ACT,

post acquisition to Australia. John Holland

replace bonding lines was 30% equity

available under provider drawn under

Leighton Holding’s

facilities in the

acquisition

10Business Corridors, Belt and Road: Overview of the Belt and Road Initiative

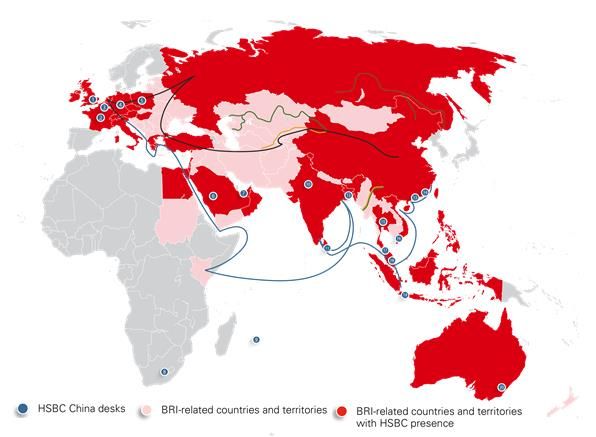

HSBC is well-positioned to capture BRI opportunities

Belt and Road Initiative is made up of “The Silk Road Economic Belt” and “The 21st Century Maritime Silk Road”

Seek to connect > 65 countries across Asia, Middle East, Africa and Europe, c.30% of global GDP and 63% of world population 1

By improving the global infrastructure and network connectivity, mainland China can better facilitate international trade and development

Mainland China’s trade with countries along the Belt and Road is expected to surpass USD2.5trn by 2025 2

BRI countries with

HSBC presence

BRI countries with

HSBC presence and

dedicated China Desk

Committed funding

by multinationals /

policy banks3

Agency Capital

(USDbn)

CDB 890

AIIB 100

SRF 55

NDB 50

CHEXIM 19

1. China Development Bank

2. Xi Jinping in 2015 Boao Forum, Xinhuanet, 29MAR15

3. CDB: China Development Bank; AIIB: Asian Infrastructure Investment Bank; SRF: Silk Road Fund’; NDB: New Development Bank; CHEXIM: Export-Import Bank of China 11Business Corridors, Belt and Road: Overview of the Belt and Road Initiative

Initial opportunities arising from BRI will be focused on significant

infrastructure investments…

USD26tn (USD1.7tn p.a.) of infra-structure

investments forecasted to 20301 in Asia HSBC strengths in infrastructure projects

Infrastructure investment, by sub-region

HSBC provides a full suite of investment banking services, including advisory

East Asia and financing solutions to our clients in the infrastructure sector

12%

South Asia 2%

Southeast Asia 0% Infrastructure and Real Estate Group (IRG) leads HSBC’s infrastructure

24% coverage and has over 200 personnel globally in key hubs, including London,

Central Asia 61% New York, Hong Kong, Singapore, Paris and Dubai

The Pacific

HSBC’s expertise is well recognised in the industry and was awarded ‘Best

BRI bank’ (AsiaMoney) and ‘Best Financial Adviser Asia Pacific’ (Infrastructure

Journal 2017)

Forecast investment spend to 2030

USDtn2 Notable transactions

Indonesia 2.7

Jul 2017 France Apr 2017 China

Phillipines 0.9

Thailand 0.8

Malaysia 0.7 EUR375m USD5bn

Financial Adviser to China Multi-tranche bond offering

Singapore 0.7 Eastern Airlines on its

acquisition of a 10% stake in Joint Global Coordinator,

Vietnam 0.7 Air France-KLM Sole Rating Adviser, Joint

Lead Manager, Joint

Others 0.5 Sole Financial Adviser Bookrunner

1. ADB estimate. Climate adjusted estimate. Without climate change mitigation and adaptation costs, USD22.6tn will be needed, or USD1.5tn per year (baseline estimate). Definitions and source data are different to those shown in

the Sustainable Finance presentation

2. Source: Mckinsey “Southeast Asia at the crossroads: Three paths to prosperity” 12

3. For 25 economies with adequate data, comprising 96% of the region’s population.

4. The difference between investment needs and current investment levelsBusiness Corridors, Belt and Road

HSBC infrastructure capabilities

HSBC provides a full suite of HSBC offers comprehensive infrastructure solutions Notable transactions

investment banking services,

Dec 2017 UK Jul 2017 France

including advisory and Infrastructure Broad knowledge of the industry and in-depth

financing solutions to our understanding of the business through our dedicated

Advisory

Power & Utilities teams

clients in the infrastructure

sector Strategic direction lead for each sub-sector globally GBP555m EUR375m

Renewables

International network providing M&A advisory and Acquisition of 30% stake in Dudgeon Financial Adviser to China Eastern

IRG Group leads HSBC’s Transport, Services & capital market solutions to our clients offshore wind farm from Statkraft Airlines on its acquisition of a 10%

Logistics stake in Air France-KLM

infrastructure coverage and

has over 200 personnel Infrastructure Acquisition

globally in key hubs, including

Sole Financial Adviser Sole Financial Adviser

London, New York, Hong Structured Bonds HSBC has a track-record of providing value-added

Kong, Singapore, Paris and advisory and arranging financing through volatile

markets Jun 2017 Indonesia Apr 2017 China

Dubai Rating Advisory

Bankers are product agnostic providing advice on best

HSBC’s expertise is well Project Finance solution be it loan, bond or private placement

Financing Solutions

recognized in the industry: Ability to provide balance sheet to support clients

Debt Advisory including underwritten and club solutions USD29.2m USD5bn

#3 APAC Financial HSBC has one of the largest global Export Finance Sinosure supported facility for the Multi-tranche bond offering

Export Finance

Advisor for infrastructure teams of any commercial bank procurement of a 1x55MW coal-fired

power

Finance 20171

Debt Capital Markets Ability to arrange Export Credit Agencies (ECAs) Coordinating Bank, Mandated Lead Joint Global Coordinator, Sole Rating

#2 APAC Bond Arranger supported facilities across diverse business sectors Arranger, Facility and Security Agent Adviser, Joint Lead Manager, Joint

worldwide with all the major ECAs, with a particularly Provider Bookrunner

for infrastructure Equity Capital Markets

strong presence in arranging Sinosure-supported

finance 20171 facilities

Aviation Finance Jan 2017 Sri Lanka Sep 2016 Indonesia

#1 Airports M&A Single global team to ensure common / integrated client

Advisor 2005 - 20171 Maritime Finance pitching

Best overall international

bank for the Belt and Green Bond

USD44m Sinosure Facility USD1.8bn

Road Initiative

Global Markets HSBC has infrastructure experts in Global Markets, Financing for the runway overlay and Jawa 7 2x1000MW IPP

solutions

associated works at Bandaranaike PT Shenhua Guohua Pembangkitan

Global Trade Receivable Financing (GTRF) and Global

Other

International Airport in Katunayake, Sri Jawa Bali; China Shenhua won the bid

Global Trade Liquidity and Cash Management (GLCM) Lanka on this project

Receivable Financing

Ability to provide Global markets, GTRF and GLCM Sole Arranger, Agent and Security Transaction Advisor to PLN

Global Liquidity and Agent

Source: IJGlobal, Dealogic solutions to support infrastructure transactions

Cash Management

1. League table ranking by deal value

13Business Corridors, Belt and Road: Overview of the Belt and Road Initiative

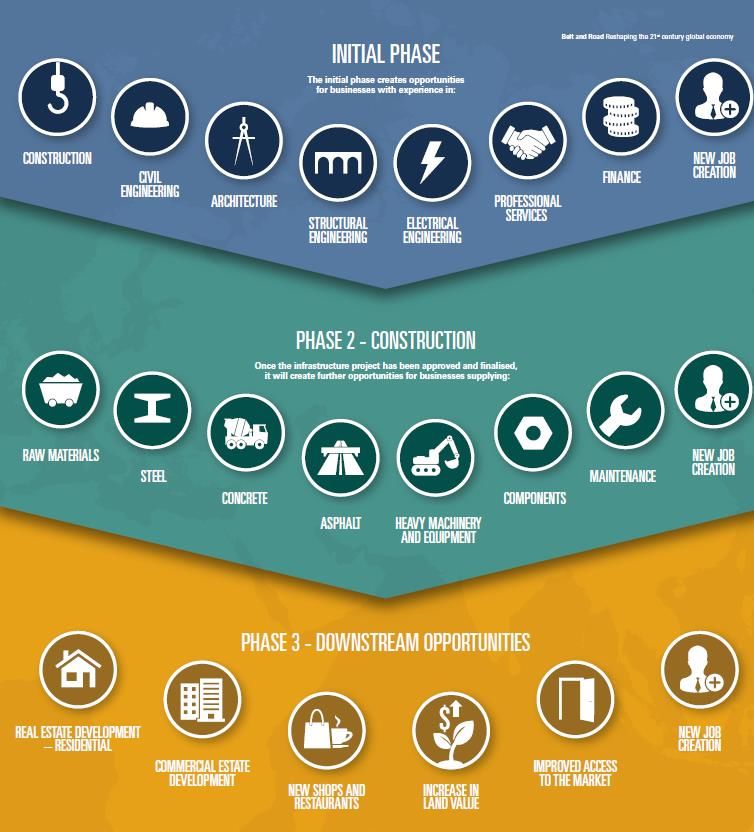

…the projects create further opportunities

In addition to the immediate opportunities, there is

tremendous potential for spillover benefits

Financial services required by participants in the immediate

supply chain associated with a project

Project development will also create local demand for

upstream / construction-related materials and services

Completed projects and enhanced connectivity will stimulate

commercial / tourism development

Follow on opportunities include

Residential Development Commercial Development

New transport routes are a Enhanced connectivity boosts

catalyst for new community relative attractiveness of sites for

development commercial / industrial users

Logistics Development Local economic multiplier

Improved connectivity will Infrastructure projects will

impact business location and stimulate local economy –

supply chain decisions generating increased local

economic activity

14Business Corridors, Belt and Road: HSBC’s unique positioning as the “Go to Bank” for BRI

Using the international network and universal banking model, HSBC can

help clients of all sizes to participate in BRI opportunities

Geographic spread Product breadth Customer depth

• HSBC’ global coverage is aligned with BRI • HSBC’s products offering provides • HSBC’s differentiated proposition

territories one-stop holistic solutions for our

• HSBC has set up 25 China desks1 around the customers

world and is the international bank with the

largest onshore network in China

Global Global

Liquidity & Banking

Securities Cash

Services Management Large

Corporates

Global

Insurance & Trade &

Receivables

Mid Market

Investments

Finance Corporates

Corporate & Business Banking

Hedging (FX, Project Upper

Interest rate) Lending

M&A

ECM

Business Banking Mass

DCM

Retail Business Banking

HSBC has a unique competitive position

1. China Desk locations: Hong Kong, Singapore, Australia, UK, USA, UAE, Germany, France, Poland, Luxembourg, Israel, Saudi Arabia, Malaysia, Macau, Thailand, India, Indonesia, Bangladesh, Vietnam, Sri Lanka, Canada,

Argentina, Mexico, South Africa, Mauritius.

15Business Corridors, Belt and Road: Overview of the Belt and Road Initiative

Increased trade flows from improved network connectivity and China’s BRI

policies will facilitate more RMB usage

Improved network connectivity across Belt and Road (BR) routes and mainland China’s trade and investment focus in key BRI countries

will lead to increased usage of RMB as a trade, payment and financing currency

70% of corporates surveyed agreed that the BRI would have a positive impact on RMB usage in the future1

With RMB now the 3rd trade finance and 5th payment currency globally, China continues to improve offshore RMB infrastructure in

partner countries and through its RMB Cross-border International Payments System (CIPS)

RMB usage along BR and within AIIB China’s trade in RMB3

50%

In 2017, China’s trade with countries along BR was 27% of its total trade at USD7.4tn2

In 2017, 12% of China’s total trade was conducted in RMB3. By 2020, HSBC estimates 4x

that China will conduct 50% of its trade in RMB 26%

22%

Of the 24 RMB clearing banks globally, 18 countries / territories are along the BR 17%

12% 12%

8%

Of the 254 markets with active RMB swap lines (c. >RMB2.2tn), 22 are along the BR

Most of China’s top trade partners are using RMB or have RMB clearing banks 2012 2013 2014 2015 2016 2017 2020F

1. HSBC RMB Internationalisation Survey 2017; Ministry of Commerce; 3. PBOC, % trade settled 4. 36 foreign central banks have signed RMB swap lines, including 11 expired swap lines; 5. CEIC goods trade, not including services;

6. SAFE; 7. HKMA, MAS, Central Bank of the Republic of China (Taiwan), City of London, BOK; 8. European Central Bank

16Business Corridors, Belt and Road: HSBC’s unique positioning as the “Go to Bank” for BRI

HSBC can reach all the business opportunities around a single BRI project

proposal

Clients’ needs / product opportunities over the Project’s life cycle

Project

Project t

• Int’l & local

Owner Ministry of Finance (MoF)

Funding (loan / bonds)

procurers

Ministry of Transport (MoT) • Financial & structuring depending on

Advice markets / Full

Government Agencies

• Hedging

Central Bank currency required Coverage

The Project’s Ecosystem

ProjectCo International Bidder A Bidder B Bidder C • Financial Advisory International Global

Bidders / investors • Intro to local partner banks’ scope network

Investors partnering with • Bid & Perf. bonds

• Funding (loan / bonds)

local large Expertise in

• Hedging (IRS, FX)

Company advising and

financing of

Lead Large International • Performance bonds infrastructure

contractors • Receivable financing

Full & local • Payable financing

Infrastructure Deliver both

Coverage • Working Capital Local

companies event and

• Hedging (FX) banks recurrent

flow

Sub Mid-size local Infrastructure products

Contractor / & logistics companies • Performance bonds

suppliers • Receivable financing

• Working Capital

Real Estate International & Local real estate • Funding (loan / bonds)

Companies investors and builders • Performance bonds

• Trade financing

• Working Capital

17Business Corridors, Belt and Road

Summary of recent examples of HSBC supporting Chinese clients going

outbound

Supply

Initial Initial event Risk

chain

advisory financing management

support

China to Australia Mandated Lead Arranger for CCCC US$1.1bn bridge loan facility in support of its 100%

acquisition of John Holland Group Pty

Mandated Lead Arranger, and Hedge Provider on the A$633m project financing for Capital Metro

PPP in the ACT

Mandated as John Holland’s offshore GLCM partner bank.

Mandated Lead Arranger for the extension and reduction in pricing of John Holland’s A$1bn

bonding facility

China to France Sole Financial Adviser for China Eastern Airlines to acquire 10% stake in Air France KLM. CEA

financed its stake acquisition through pledging of AFK and CEA (H-shares) shares owned by CEA,

where HSBC further assisted to ensure successful closing in Oct 2017

China to UK Sole Financial adviser to the China Resources Consortium for the purchase consideration of

c.£555m for the 30% equity stake in Dudgeon Holdings Limited (“Dudgeon“)

China to Sri Lanka Sole Arranger, Agent and Security Agent for the financing of runway overlay and associated

works at Bandaranaike International Airport in Katunayake, Sri Lanka.

China to Bangladesh Mandated Lead Arranger, Coordinating Arranger, Lender, Facility Agent and Security Agent, LC

Issuing Bank, Account Bank for the USD 333m financing package for the re-powering of the

210MW Ghorasal 3rd Unit involving a Swiss-Chinese consortium, comprising General Electric (ex-

Alstom) and China National Machinery Import & Export Corporation (“CMC”)

China to Switzerland Lead Financial Adviser for ChemChina on its full cash tender offer for Syngenta, the Swiss listed

world leader in crop protection, valued at USD46bn

18Business Corridors, Belt and Road

BRI is a significant long-term growth theme that will help trade, FDI and

wealth flows across the region (and globally)

1

BRI opportunities not limited to infrastructure, but also adjacent project opportunities, and downstream

opportunities

2

2017 Asian loan growth of 14%1, and 15% revenue growth for the top 17 HSBC Asian corridors highlights early

evidence of BRI benefits starting to accrue

3

BRI reaffirms our existing Business Corridor strategy

4

HSBC well-positioned to be the “go to” bank for BRI

Product capability allows to service the customer needs throughout the project lifecycle

Our presence in BRI countries combined with our customer base (SME – Large multinational corporates)

means that we are able to service multiple participants of a single project

Customer / industry has recognised our ability to finance BRI opportunities

1. Adjusted basis - same definition as shown in the HSBC Holdings plc 4Q17 results slides published on 20 February 2018

19ASEAN 11 April 2018 Matthew Lobner Head of International, Asia-Pacific and Head of Strategy and Planning, Asia-Pacific Tony Cripps Chief Executive Officer, Singapore Mukhtar Hussain Chief Executive Officer, Malaysia Sumit Dutta Chief Executive Officer, Indonesia

ASEAN

Agenda

ASEAN introduction

Opportunities arising from ASEAN integration and HSBC’s position

Singapore, Malaysia and Indonesia: Country overview and HSBC priorities

Clients’ view of ASEAN and HSBC’s structure to support their needs

Summary

21ASEAN: Introduction

Association of Southeast Asian Nations (ASEAN)

10 Countries, Combined GDP of USD2.7tn1,2, population of c.650 Population1

GDP1,2

million1 and trade of USD2.2tn1,3

Trade1,3

Priority markets

68m

Other presence

Lao PDR4 Cambodia 95m

USD423bn

Myanmar USD223bn

USD399bn

USD372bn

Thailand

Vietnam

31m

104m

USD293bn

USD333bn

Philippines USD315bn

Malaysia Brunei

Singapore USD127bn

264m

5.8m

USD1.0tn

USD304bn

Indonesia USD295bn

USD696bn

As a single entity, ASEAN ranks as world’s seventh largest economy and is expected to become fourth largest by 20305.

1. Source: Global Insight; 2017 data 4. Lao People's Democratic Republic

2. Nominal GDP 5. Source: Global Insight

3. Trade = Exports + Imports 22ASEAN: Introduction

ASEAN: Journey towards integration

ASEAN established Announced creation ASEAN pushes ASEAN to grow at a rapid pace,

to promote of ASEAN for deeper trade supported by planned initiatives to

collaboration, Economic liberalisation increase connectivity / integration

peace and stability Community (AEC) TPP-111 agreed

among members by 2015 for regional RCEP2 in final Increased investment in infrastructure

economic integration to support intra-ASEAN physical

negotiations

connectivity (e.g. Singapore Kunming

Rail Link, ASEAN Highway Network

project)

1967 1977-2003 2007 2010-15 2015-18 Growth in trade driven by further

reduction in tariffs and other trade-

distorting measures (e.g. further

strengthening of ATIGA)

1977: ASEAN Preferential 2010: ASEAN Trade in Goods

Greater mobility of skilled labour in the

Trade Agreement Agreement (ATIGA)

region (e.g. enhanced commitments

1992: ASEAN Free Trade Area 2012: ASEAN Comprehensive under Agreement on Movement of

Investment Agreement Natural Persons)

1995: ASEAN Framework

Agreement on Services 2014: ASEAN Bank

Integration Framework Deeper regional financial integration to

1997: Adopted ASEAN Vision help accelerate economic development

2015: AEC formally

2020 (e.g. ASEAN Banking Integration

established; AEC Blueprint

2003: Declared formation of 2025 was adopted Framework)

AEC

1. TPP11: Comprehensive and Progressive Agreement for Trans-Pacific Partnership

2. RCEP: Regional Comprehensive Economic Partnership

23ASEAN: Opportunities arising from ASEAN integration and HSBC’s position

Opportunities arising from ASEAN integration

Integration to accelerate economic expansion and wealth creation

across ASEAN Key opportunities

Estimated infrastructure and real estate investment, Growth of investment and corporate banking,

2014-301,2, USDtn arising from:

Infra- 2.7

0.9 ASEAN based businesses expanding across

structure 0.8 0.7 0.7 0.7 ASEAN to improve competitiveness through

needs

M&A, JVs, and upgrading regional supply chains

Indonesia Philippines Thailand Malaysia Singapore Vietnam

MNCs outside ASEAN setting up regional HQs

within ASEAN to capture opportunities across the

ASEAN trade3, USDtn Exports bloc

Imports

+7.3%4 Acceleration of infrastructure investments to

5.6

Trade enhance regional integration, supported by the

growth 2.2 2.9 Belt and Road Initiative

1.2 2.7

1.0

Growth of transaction banking, arising from:

2017 2030F

Lowering of trade tariffs and barriers to further

ASEAN per capita GDP3, USD'000

increase in trade flows

2.6x Growth of offshore wealth and individual

Wealth international banking needs, arising from:

creation

11.0

4.2 Ease of labour movement / travel throughout

ASEAN

2017 2030F

1. Source: Southeast Asia at the crossroads - Three paths to prosperity (McKinsey, 2014)

2. ID: Indonesia; PH: Philippines; TH: Thailand; MY: Malaysia; SG: Singapore; VN: Vietnam

3. Source: Global Insight 24

4. 2017-30 CAGRASEAN: Opportunities arising from ASEAN integration and HSBC’s position

HSBC well-positioned to capture ASEAN opportunities

xx Year of establishing HSBC presence

200 Priority markets

branches Other presence

10,000

For c.150 years, HSBC has

corporate clients played an active role in

development of economies

20,000 and infrastructure of ASEAN

countries

SME clients

At scale / near-scale

2,500,000 positions in three of the

largest markets

retail clients

Presence in other key

15,000 markets – Vietnam,

Thailand, Philippines

CAGR staff

2016 trade1 2016-30 Ability to capture both flows:

USDbn intra-ASEAN and ASEAN

c.88% of ASEAN’s trade is with with Rest of World / Asia

Intra-ASEAN 153 9%

rest of Asia / World. HSBC’s

global network hence puts us Strong onshore franchise

ASEAN-Rest of Asia 692 9% in a strong position against with fully functional RBWM,

regional / local banks1 CMB and GB&M in key

ASEAN countries

ASEAN-Rest of World2 404 7%

1. Export + Import; Source: Oxford Economics

2. Rest of World Ex-Asia

25ASEAN: Singapore, Malaysia and Indonesia: Country overview and HSBC priorities

Country overview: Singapore (1/2)

Country highlights

Real GDP1, USDbn Strong fundamentals

AAA credit rating from three ratings

2.1%2 2.3%2 agencies

323 USD0.7tn of One of world’s most connected economies6

289 302

Infra- investment Leading international financial centre

GDP

structure estimated between

Largest FX centre in Asia; 3rd largest

2014-20304

globally7

Expected to become the second largest

2015 2017 2020F offshore wealth centre globally by 20205

Centre of ASEAN finance and commerce

World-leading hub for container

Trade3, USDbn Offshore wealth5, USDtn transhipment, connecting ASEAN to the

Exports Imports xx CAGR (2016-21E) world

Fastest growing international 2/3rd of project financing in ASEAN is

5.7%2

1.4%2 wealth centre arranged out of Singapore8

820 3% 8% 7% Hub for regional headquarters

Trade 676 696 Wealth

454 2.4 Around 7,000 MNCs in Singapore with

380 393 1.2 c.60% having regional responsibilities9

0.8

366 Becoming the financial conduit linking

297 303 mainland China, ASEAN and the rest of the

Switzer- Singa- Hong world

2015 2017 2020F land pore Kong

1. 2010 USD basis; Source: Global Insight 6. Source: McKinsey Global Institute Connectedness Index, 2016

2. CAGR 7. Source: Bank for International Settlements (BIS)

3. Source: Global Insight 8. Source: Singapore – Asia’s infrastructure hub, Monetary Authority of Singapore & 26

4. Source: Southeast Asia at the crossroads - Three paths to prosperity (McKinsey, 2014) International Enterprise Singapore

5. Source: Global Wealth 2017, Transforming the Client Experience (BCG) 9. Source: Cushman & Wakefield (2016)ASEAN: Singapore, Malaysia and Indonesia: Country overview and HSBC priorities

Country overview: Singapore (2/2)

HSBC performance highlights1, 2017

Contribution by global business

Revenue PBT Loans and advances to

USDm

customers (net)

Revenue 1,174 44% 42%

34%

12%

6% 7% 12%

PBT 463 17% 20% 14% 20%

31% 26%

15%

USDbn

RBWM CMB GB&M GPB Corp Centre

Loans and

advances to Strategic priorities

28

customers

(net) Continue to build regional product and coverage expertise to

capture opportunities from Singapore’s role as a regional hub

Customer

41 Capture infrastructure / BRI opportunity

accounts

Capture international flows from key business corridors

Grow domestic retail and private banking business, enabled

by digital and multi-channel capabilities

Key ratios (2017)

Scale up international wealth centre to capture greater share

of wealth flows

CER 61% LICs / loans +0.03%2

Be the ‘go-to’ financial advisor and industry thought leader for

sustainable finance

1. All financials are on reported basis

2. The ratio is positive due to net loan recoveries

27ASEAN: Singapore, Malaysia and Indonesia: Country overview and HSBC priorities

Country overview: Malaysia (1/2)

Country highlights

Real GDP1, USDbn Strong and enduring economic fundamentals

Forecast GDP growth at c.5% p.a. through to

4.7%2 20203

4.2%2

411 Middle and upper middle class expected to be

330 358 USD0.7tn of more than 80% of population by 20205

Infra- investment Regional centre of excellence for Islamic

GDP

structure estimated Banking

between 2014- Growing as a major regional hub

20304 Over 3,600 MNCs with global and regional

representative offices. Further c.1,400 MNCs

2015 2017 2020F with an operating presence6

Well-developed infrastructure. 18th position

globally on ease of doing business6

Trade3, USDbn Per capita GDP3, Cost competitive, ranking 212th most expensive

USD'000 destination in the world7 (Singapore ranked 24th)

Exports Imports

Young, educated and cost effective workforce

2.6x (median age of population is c.28 years)8

+6.7%

+1.5%

24.6 Strong diplomatic, cultural and commercial

404 Wealth relations with mainland China, linking it with

Trade 323 333 ASEAN

creation

220 9.4

176 180 Over 30 inter-governmental MOUs signed

9 major Chinese corporates set up regional

148 152 184 centers in Malaysia in the last 24 months

2017 2030F Aggressive investment in ports and rail links in

2015 2017 2020F Malaysia under BRI

1. 2010 USD basis; Source: Global Insight 5. Source: Capitalizing on Asia’s Booming Upper Middle Class (BCG, 2016)

2. CAGR 6. Source: Kuala Lumpur, Asia’s regional headquarters hub (EY, 2016); Malaysian Investment Development Authority (MIDA)

3. Source: Global Insight 7. Source: Cost of Living survey published by ECA International

28

4. Source: Southeast Asia at the crossroads - Three paths to prosperity (McKinsey, 2014) 8. Source: Department of Statistics, MalaysiaASEAN: Singapore, Malaysia and Indonesia: Country overview and HSBC priorities

Country overview: Malaysia (2/2)

HSBC performance highlights1, 2017

Contribution by global business

Revenue PBT Loans and advances to

customers (net)

USDm

50%

27% 16% 34%

Revenue 836

15% 9% 44%

17% 21%

40%

PBT 325 26%

RBWM CMB GB&M Corp Centre

USDbn Strategic priorities

Loans and Build coverage and product expertise to capture opportunities

advances to from growing numbers of MNCs using or transferring to Malaysia

14 as their regional operating hub, especially from mainland China

customers

(net) Leverage early leadership in BRI investment flows, capturing

Customer both event and the flow opportunities

14 Capturing opportunities from key business corridors including

accounts

mainland China, intra-ASEAN and Japan

Grow Retail, leveraging propositions in Cards and Wealth.

Key ratios (2017) Invest in digital to enhance competitive positioning

Leverage Malaysia’s international capital markets leadership in

Shariah compliant financial services. Build out Shariah

CER 56% LICs / loans (0.32)% compliant personal financial services to capture the rapid growth

in this sector

1. All financials are on reported basis

29ASEAN: Singapore, Malaysia and Indonesia: Country overview and HSBC priorities

Country overview: Indonesia (1/2)

Country highlights

Real GDP1, USDbn Strong economic fundamentals and

demographics

5.3%2

5.0%2 ASEAN’s largest economy. Expected to become

1,272 the 7th largest (by GDP) globally by 20303

1,090 USD2.7tn of Assigned Investment Grade Credit rating by all

988

Infra- investment major rating agencies in 2017

GDP

structure estimated 4th most populous country with a young

between 2014-304 population (median age of population is c.28

years)5

GDP growth fuelled by strong domestic demand,

2015 2017 2020F supported by a growing middle class. Middle and

upper middle class expected to be more than

50% of the population by 2020 (37% in 2015)6

Trade3, USDbn Per capita GDP3, Growing trade flows

Exports Imports USD'000 Trade to grow at c.10% CAGR between 2017-

20203, with mainland China and Singapore as

3.2x

+10.0% leading partners, driven by commodities exports7

+1.9%

12.3 Investments in infrastructure

393 Wealth

Trade

284 295 creation Requires USD2.7tn in infrastructure and real

205 estate investment (between 2014 and 2030) to

149 157 3.9 support growth, the most in ASEAN4

135 138 188 Currently ongoing / planned projects amount to

c.USD300bn, expected to be supported by

2017 2030F

2015 2017 2020F funding from private sector and BRI6

1. 2010 USD basis; Source: Global Insight 5. Source: Global Insight; IMF

2. CAGR 6. Source: Capitalizing on Asia’s Booming Upper Middle Class (BCG, 2016)

3. Source: Global Insight 7. Source: Oxford Economics, HSBC Trade Connections

30

4. Source: Southeast Asia at the crossroads - Three paths to prosperity (McKinsey, 2014) 8. Source: NatixisASEAN: Singapore, Malaysia and Indonesia: Country overview and HSBC priorities

Country overview: Indonesia (2/2)

HSBC performance highlights1, 2017

Contribution by global business

Revenue PBT Loans and advances

USDm to customers (net)

1%

Revenue 564 7% 54% 8%

27%

19%

24%

17%

PBT 180

-13% 72%

42% 42%

USDbn

RBWM CMB GB&M Corp Centre

Loans and

advances to Strategic priorities

4

customers

Leverage our international network to maximise opportunities

(net)

across key Business Corridors, including mainland China,

Customer intra-ASEAN, US, UK & Germany

4

accounts

Capture infrastructure opportunity (including BRI) to drive

growth

Invest in digital to scale up Retail business

Key ratios (2017)

Grow liabilities across businesses to support asset growth

CER 56% LICs / loans (1.6)% Strengthen and grow local corporate and SME relationships

across the top cities to capture growth in domestic businesses

1. All financials are on reported basis

31ASEAN

Client viewpoints: illustrating HSBC’s ability to support MNCs expand into

ASEAN and ASEAN clients expand within and outside ASEAN

1 2 3

Expansion opportunity beyond home An attractive location to set up a Strategic location for regional

country in ASEAN manufacturing base business hubs

Indonesian Group, aiming to establish Large manufacturer in mainland China, Dutch marine engineering firm, with

a strong footprint in Asian markets, expanding production sites in ASEAN, regional sales and finance hub in

including ASEAN with regional sales hub in Malaysia Singapore

Large group in resin distribution and Vertically integrated knitwear Operates in over 50 countries,

consumer packaging business manufacturer, headquartered in Hong including 6 locations in ASEAN

Has expanded across 7 countries in Kong, with most of the production in HSBC is providing the client with a

mainland China

Asia (5 in ASEAN) regional cash management solution

Actively expanding production in to centralise its cash position

Has strong conviction in ASEAN’s

Cambodia and Vietnam to mitigate across Asia and Netherlands

growth potential, looking to expand in

rising costs in mainland China and for

the remaining ASEAN countries Obtained the mandate by delivering an

better access to the attractive ASEAN innovative liquidity management

Considers HSBC as the best partner market solution and close cooperation

to help in its expansion, with its

Have set up their regional sales hub between HSBC teams in

experience and international network

in Labuan (Malaysia) Netherlands and Singapore

HSBC Indonesia supports the client

HSBC supports the client by funding Demonstrates HSBC’s transaction

with trade facilities, FX hedging and

capital expenditure in Vietnam and banking capabilities and ability to

cash management. Client also banks

providing GLCM services in Labuan, support a corporate globally

with HSBC in Malaysia, Singapore,

where the collections are centralised

Australia, and New Zealand

32ASEAN

Structure to enable focus on ASEAN opportunities

Indonesia Malaysia Singapore

Philippines Thailand Vietnam

Strong onshore presence and coverage enhanced by regional capabilities

International wealth centre in

1 Regional coverage 2 Product specialists 3

Singapore

1. Clients’ view of ASEAN andHSBC’s structure to support their needs

33ASEAN

HSBC well positioned to capture opportunities across ASEAN

Well positioned to capture opportunities across ASEAN…

1 Deep heritage across key ASEAN markets

At scale / near-scale positions in three of the largest markets

Well positioned to support

strong economic Presence in other markets – Vietnam, Thailand and Philippines

fundamentals in ASEAN

markets, further bolstered

by ongoing integration 2

Ability to capture wealth, investment and trade flows intra-ASEAN and

activities between ASEAN with Rest of World / Asia

3

Strong onshore franchise with full coverage, supported by regional

capabilities

34Sustainable finance 11 April 2018 Daniel Klier Group Head of Strategy and Global Head of Sustainable Finance

Sustainable Finance

Sustainability and HSBC’s approach to ESG1

Sustainability at HSBC HSBC’s approach

From climate change to Support the global transition to the low-carbon economy,

wealth equality and job Environmental through our own sustainable operations and by supporting our

security, the challenges to customers with their transition

today's global economy are

unprecedented in nature We have robust climate-related risk management covering

In this changing environment, sensitive sectors, such as energy, palm oil and forestry

HSBC is committed to

develop the skills, business

innovation and low-carbon Foster a customer and employee centric approach to our

solutions to secure long-term Social business

prosperity for all

Focus on diversity and inclusion of our workforce, and strive to

Our sustainability approach

put the customer at the heart of everything we do

focuses on three main areas:

Support the transition to a

low carbon economy

Enable sustainable supply

chains and entrepreneurship Governance Maintain high standards of governance across all geographies

Provide communities,

Committed to protecting our customers and communities

customers and employees

with skills to succeed in the through our Financial Crime Risk management and cyber

future security diligence

1. Environment, Social and Governance

36Sustainable Finance

Pathway to achieve Paris Agreement is challenging; speed of change is

accelerating

Material reduction in carbon emissions required to deliver Paris Agreement1 …and stakeholders have already taken actions

Carbon emissions Carbon budget to combat climate change France and UK to ban sale of new

gigatonnes of carbon gigatonnes of carbon petrol and diesel cars by 2040

China cancelled plans of more than 100

Government

3,000 coal power plants early 2017

California to receive all of its power

from renewable energy by 2045

Investors demand reports from big

O&G companies on possible impact of

1,720 global warming policies on business

Investors

1,480 HSBC research shows that 68% of

1,300 investors plan to increase their

1,000 climate-related investment

550 A global O&G company is investing in

400 renewables for their power generation

and installing charging stations at

petrol stations

Carbon Emissions Emissions >50% >66% >50% >66% A multinational utility company

stored in at current with existing chance of chance of chance of chance of Corporates pledged to dispose EUR15bn in assets

known fossil run rate commitments achieving achieving achieving achieving to reinvest into low-carbon, distributed-

reserves this goal this goal this goal this goal energy projects

A global Original Equipment

2oC world 1.5oC world Manufacturer will produce only electric

(Paris Agreement) or hybrid cars from 2019 onwards

1. Source: Inter-governmental Panel on Climate Change, UCL, HSBC calculations, until 2050

37Sustainable Finance

Over USD100tn investment in infrastructure in the next 15 years is required

globally under 2 degree scenario, c.50% will be in Asia

Global infrastructure investment needed in the next 15 years for a 66% chance of 2°C1

USD trillion, 2016-2030

103.5 100%

16.5 c.50% of total

investment will be in

29% Mainland China

Asia, especially

9.0

emerging Asia

India

15.0 6% Other emerging Further areas of

6% Asia investment:

9.0 7% Developed Asia Energy

2% Power / electricity

7% Africa

13.5

Transport

5% Latin America

Banking Revenue pool in next 15 Middle East Mainland China’s BRI

years3: 22% US and Canada will further drive

>USD5tn global investment and

40.5

trade, especially in

the Asia-Pacific

16% Europe

region

Transport Water & Telecoms Power and Primary Energy 2016-2030 By region2

sanitation electricity energy demand/ Total

transmission/ supply efficiency

distribution chain

1. OECD, IEA, Investing in Climate, Investment in Growth, JUL17; The OECD estimates that for infrastructure to be consistent with a 2oC 66% scenario, investment needs to amount to USD6.9tn per year in the next 15 years, an

increase of about 10% in total infrastructure investment from the reference estimate of USD 6.3 trillion. Definition and source data are different to those shown in the BRI presentation

2. McKinsey, “Bridging Global Infrastructure Gaps” JUN16 38

3. HSBC estimationSustainable Finance

Asia is at the heart of the transition and key countries from Asia are

pioneering in this area

Top 100 most Changes in Gross capacity Total investment

Taking leadership

populous cities1 electricity demand2 additions2 projected2

2016 PWh, 2016-40 TW, 2016-40 USDtn, 2016-40 China

China is the world’s biggest

producer of wind energy,

Asia-Pacific 55 55% 8.4 60% 4.4 51% 4.8 47% with a total installed

capacity of c.170GW in

20164

China aims for renewables

(incl. hydro power plants) to

Americas 10 10% 1.3 9% 1.4 16% 1.5 14% contribute half of new

electricity generation by

2020, committing

RMB2.5tn5

META3 30 30% 2.5 18% 1.1 13% 1.5 14% India

India plans to increase its

solar installations from

below 5GW to 100GW by

Europe 5 5% 0.2 2% 0.9 11% 1.2 12% 2022, more than double the

present solar capacity of

China and Germany6

India aims for 57% of

installed capacity to come

Rest of World 0% 1.6 11% 0.8 9% 1.3 13%

from non-thermal energy by

20277, requiring USD200-

300bn of investment8

1. Country Disclosure, HSBC estimation 5. China to invest GBP292bn in renewable power by 2020, the Guardian, JAN17

2. Bloomberg New Energy Finance, 2017 6. Financial Times, Investors look to India as the next solar power, JAN16

3. META includes Middle East, Turkey and Africa 7. Forbes, India Coal Power Is About To Crash, JAN18 39

4. Global Wind Energy Council (GWEC), 2016 8. India needs over USD200bn of investment in renewables, Economic Times, NOV17Sustainable Finance

The transition will affect many industries and create opportunities

Transition Business opportunities Financing solutions

Risk of stranded assets Portfolio diversification Corporate Lending

Renewables will contribute at least 20% of • Transition from high-carbon to low-carbon M&A, DCM, ECM

primary energy supply by 20401 assets Trade Finance

Energy

• USD350bn of investment in wind and

solar needed to achieve the current

market share in upstream O&G3

Decentralisation of power generation system Households to install more solar panels Personal Loan

Grid health (risk of overgeneration due to New infrastructure: energy storage to provide Corporate Lending

intermittency of renewable energy systems); behind-the-meter solutions and control over- Project Finance

Utilities smart grids generation

M&A, DCM, ECM

“Green buildings” Total spending on energy-efficient products Trade Finance

Regulatory requirements to increase energy and services in buildings was USD406bn in Mortgage / Personal

efficiency 20164 Loan

Real Estate Better insulation materials / technologies in Corporate Lending

new buildings

Smart meters

Transition from Internal Combustion Engine Car makers to invest at least USD90bn in Corporate Lending

(ICE) vehicles to Electric Vehicles (EV) designing new EV models and increasing Project Finance

• Countries set target years for ban of new production5

Transportation M&A, DCM, ECM

ICE sales (e.g. France / UK by 2040) USD2.7tn investment on infrastructure

• 54% of annual global light duty vehicle needed for EV adoption6, i.e. building new

sales will be EV by 20502 charging points in petrol stations

1. Source: IEA World Energy Outlook 2017, New Policy Scenario projection, incl. hydro, bioenergy, wind, 4. UN, Global Status Report 2017; IEA

geothermal, solar photovoltaic, concentrated solar power, marine 5. Reuters Analysis, JAN18

2. BNEF, Long-Term Electric Vehicle Outlook 2017 6. Morgan Stanley Research 40

3. Wood Mackenzie 2017Sustainable Finance

HSBC is committed to leading the way to a sustainable future

Our commitments Progress so far

We are committed to financing clean USD10.5bn of GSS1 bonds facilitated in 2017

Provide USD100bn of energy, low carbon technologies and

sustainable financing and projects, which will help deliver the 2015 3 low-carbon funds launched in 2017

investment by 2025 Paris Climate Agreement and the UN

Sustainable Development Goals Applied Equator Principles to loans2 USD67.6bn

We will do this via direct investment or 27% of signed renewable power purchase agreements

Source 100% of our electricity

direct purchase agreements that in turn (2016: 23%)

from renewable sources by

help finance new renewable energy

2030 (90% by 2025)

projects

Reduce our exposure to We will reduce our exposure to thermal Restrict the development of carbon intensive sources

thermal coal and actively coal and engage with clients to actively

of energy

manage the transition for manage the transition path for other high

other high carbon sectors carbon sectors Embed climate risk in credit risk assessment

We will adopt recommendations of the

Adopt recommendations of Task Force on Climate-related Financial Reported governance, strategy and risk management

Task Force on Climate-related Disclosures report 2018. This will help us components in 2017 ARA

Financial Disclosures (TCFD) identify and disclose climate-related risks

and opportunities across our businesses

We aim to provide the thought leadership Member of 20 Sustainability-focused industry forums

Lead and shape the debate

needed to unlock the capital flows required

around sustainable finance

to address the world’s major sustainability #1 team for Climate Change research (2014-2017)

3

and investment

challenges

1. Dealogic, GSS bonds refer to green, social, sustainability bonds

2. Since 2003

3. EXEL 41You can also read