GLOBAL RESTRUCTURING TRENDS - SEPTEMBER 2020 PWC.CO.UKSERVICES/BUSINESS-RESTRUCTURING #ACTNOWTORECOVER

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Global Restructuring Trends September 2020 pwc.co.uk/services/business-restructuring #ActNowToRecover

Contents

Restructuring Trends: Ireland 24 Appendix 45

A Global View

Italy 25 Trends per

Executive Summary 01 country 46

Japan 26

Key Themes 02

Malaysia 27

Act Now to Recover 07

Middle East 28

The Netherlands 29

Themes by countries and regions

New Zealand 30

Australia 08 Norway 31

Austria 09 Philippines 32

Belgium 10 Portugal 33

Brazil 11 Russia 34

Canada 12 Singapore 35

Cayman and British Virgin Islands 13 South Africa 36

Central and Eastern Europe 14 South Korea 37

China 15 Spain 38

Denmark 16 Sweden 39

East Africa 17 Switzerland 40

Finland 18 Taiwan 41

France 19 Turkey 42

Germany 20 United Kingdom 43

Greece 21 USA 44

Hong Kong 22

India 23

Global Restructuring Trends | PwC

When facing

uncertainty, decisive

action counts.

In the face of continued uncertainty, the latest global restructuring trends explored in this

report underline the vital importance of proactive and decisive action by corporates and

restructuring practitioners.

Getting on the front foot will not only stabilise – we just don’t know how long it will be before

businesses in the short-term, but also help them pre-pandemic levels of output are restored. It is

gear up for longer term shifts in technology, therefore vital to take the initiative now – when We explore the

customer expectations and international trading facing adversity, decisive action counts. For business

arrangements. Conversely, waiting until the lifeline recovery plans to be successful, businesses need to challenges and

of government support is withdrawn could be clear about the challenges in their path and how

significantly reduce the options available and to steer through them. Some of the challenges are

public policy

increase business vulnerability. immediately obvious. Others may be harder to responses that

foresee and potentially the most critical. This isn’t are shaping

The world continues to grapple with the most just about surviving, but also maintaining control of market activity in

serious global health emergency for a generation. the business, preparing for the future and ultimately

And with lockdown, social distancing and 37 economies

thriving in the long-term.

restrictions on the movement of goods and people worldwide.

has come severe economic upheaval. As we explore in Where Next, a series of papers

looking at how COVID-19 is affecting different

As governments strive to sustain businesses and

industries and how organisations can transform to

save jobs, policy measures continue to evolve in

meet the challenges, the pandemic is accelerating

rapid and often unpredictable ways. In the first

change and providing a catalyst for innovation and

phases of the novel coronavirus (COVID-19)

operational modernisation. Prominent examples

pandemic, businesses across the world were mainly

range from the shift to digital retail to moves towards

focused on stabilising liquidity and tackling cash

a more sustainable economy. As part of a deals-led

flow erosion. Even as economies reopen, the

recovery, the plentiful dry powder ready for

trajectories of both infection rates and business

investment by private equity is set to play a key role

recovery remain uncertain. To date, both insolvency

in enabling businesses to keep pace with fast-

rates and pressure to restructure have generally

changing customer demand and seize the

been held in check by government intervention. Yet

opportunities ahead.

these lifelines are now beginning to be wound up.

Few would doubt that we’re entering a make or In order for companies to navigate the complex

break period, with businesses facing hard challenges their organisation may face and mantain

choices ahead. control, we believe that it’s important to focus on

four critical areas: operations (e.g. cost

In this, the third edition of PwC’s Restructuring

competitiveness), liquidity and cash, financial

Trends: A Global View, we explore the business

restructuring and stakeholder management

challenges and public policy responses that are

(customers, employees and suppliers, as well as

shaping market activity in 37 economies worldwide.

financial stakeholders) and strategic mechanisms

The report draws on the expert local insights of our

(e.g. consolidation or divestment of non-core

restructuring advisers and insolvency practitioners,

assets). Like the wheels on a car, each needs to be

who outline how governments and businesses have

in good working order and closely aligned to move

responded to the economic upheaval, how they

the vehicle forward.

expect the next 12 months to play out and the

priorities for restructuring ahead. If you have any queries or would like to discuss

any of the issues highlighted in more detail, please

What comes through strongly from our analysis as

feel free to get in touch with one of our local

explored later in our report is that businesses can

contacts listed in the report.

no longer rely on the cushion of government

subsidies or suspension of debt obligations. Neither

can they afford to wait for recovery to take its course

1 | Global Restructuring Trends | PwC Data sources are available on page 49

Key themes

Government support Restructuring activity Insolvency moves back

holds back insolvency is set to pick up in Q4 onto the agenda

and restructuring 2020 or Q1 2021 Insolvency activity has been curtailed

activity, for now As government support is withdrawn,

through much of Q2 2020 and Q3

2020, largely as a result of

we expect restructuring activity to

As revenues dried up and cash calls government support and restrictions

pick up. The immediate priorities will

became harder and harder to meet, on legal action. There are a few

include repairing the balance sheet

government intervention has provided exceptions to this, particularly for

and dealing with the debts

a vital lifeline for many businesses, territories with debtor in possession

accumulated during lockdown. With

even ones that had previously been processes. The USA is the most

revenues subdued and margins

strong and well-resourced. Support obvious one, as Chapter 11 provides

tight, there will also be pressure on

includes loan guarantees and wage the framework and protection to help

businesses to eliminate waste, drive

subsidies for workers put on short- with restructuring of operations, and

down costs and refocus resources

time or furlough (more than 40 million more companies have harnessed it as

on growth.

workers are on furlough in the 37 a tool to get through the emergency.

economies we cover in this report). We have also noted increasing levels We have also seen a similar trend in

Governments have also offered tax of non-performing loans in territories Canada where, whilst insolvencies

holidays and moratoria on such as Italy, Portugal, Greece and have been decreasing, corporate

insolvency action. East Africa which will drive lender led restructuring under Canada’s

restructuring activity in the coming debtor-led restructuring statute saw

This support held down insolvency a significant increase in the first

months, as banks look to dispose of

rates during the critical initial months half of 2020.

these portfolios or outsource the

of the crisis (Q2 2020 rates fell across

management of these.

many markets compared to Q2 2019). In general, insolvencies are expected

It would also appear to have eased to increase in Q4 2020 and into 2021,

the pressure to restructure and turn especially for those companies that

around troubled businesses, including operate in heavily COVID-19-affected

those that were struggling before industries that may take much longer

COVID-19. But governments can only to recover (e.g. leisure, travel,

afford to foot the bills for so long. hospitality, tourism, accommodation,

retail etc), as well as for those that

have yet to adapt their operations to

the new environment.

2 | Global Restructuring Trends | PwC Data sources are available on page 49

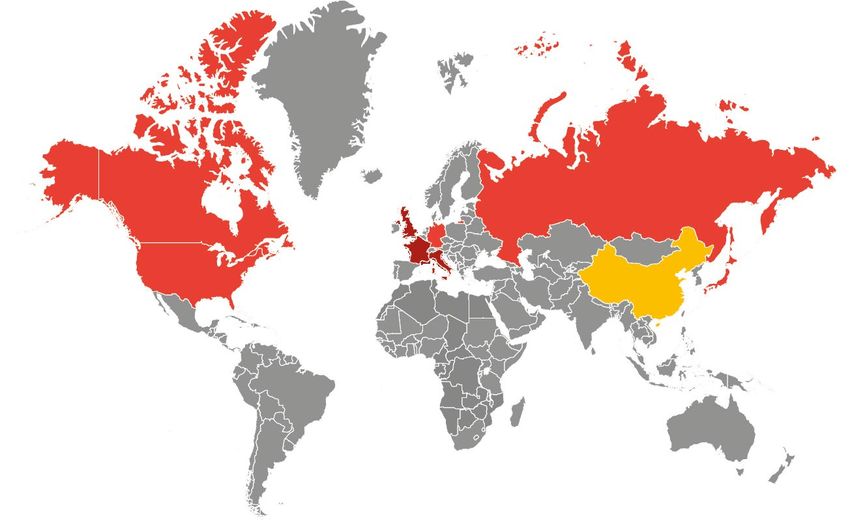

Government support Level of funding as a percentage of 2019 GDP as at August 2020 Canada 14.3% China 4.6% France 5.6% Germany 12.5% Hong Kong 10.0% Italy 4.5% Japan 42.2% Russia 3.4% United Kingdom 4.0% USA 13.9% Percentage of the national workforce on furlough as at July 2020 Canada 15.9% France 32.6% Germany 18.7% Italy 45.2% Japan 6.2% United Kingdom 31.5% USA 0.1% Note: A complete circle would represent 100% Note: No furlough data available for China, Hong Kong and Russia Note: Graphs present the G8 countries plus China and Hong Kong 3 | Global Restructuring Trends | PwC Data sources are available on page 49

-15% to -10%

-10% to -5%

-5% to 0%

0% to 5%

Pressure on GDP underlines the need to adapt

2020 Real GDP YoY now and future-proof the business for the

variation (%) shifts ahead

International Monetary Fund (IMF) projections anticipate that the

Canada Italy contraction in GDP stemming from the COVID-19 pandemic will be more

(8.4)% (12.8)% marked than the Global Financial Crisis of 2008-09 in all but a few

markets. Unemployment could also be higher, rising significantly towards

the end of 2020 as government support schemes are scaled back.

China Japan

1.2% (5.8)% The trajectory and duration of economic recovery in 2021 are still

uncertain, and are likely to vary by market and sector. Much hinges on

both a medical solution to the virus and companies’ ability to adapt to the

France Russia new environment. Further drivers of demand and growth include people’s

(12.5)% (6.6)% comfort with, and ability to, travel.

The key focal points for the coming round of restructuring include

Germany United repairing the balance sheet and creating the foundation of a healthy

(7.8)% Kingdom medium-to long-term recovery. Crucially, there will be opportunities to

make the most of rapidly developing restructuring regimes, which

(10.2)% provide new tools to work through the issues created by the crisis. These

Hong Kong include new legislation implemented or pending in the UK, Netherlands,

(4.8)% USA

Singapore, Middle East and the Cayman Islands.

(8.0)% In particular, where these regimes are more debtor friendly we expect to

see increased levels of activity as more corporates harness these tools to

get through the crisis as is the case already in the US and Canada.

Note: Map presents the G8 countries plus China and Hong Kong

4 | Global Restructuring Trends | PwC Data sources are available on page 49

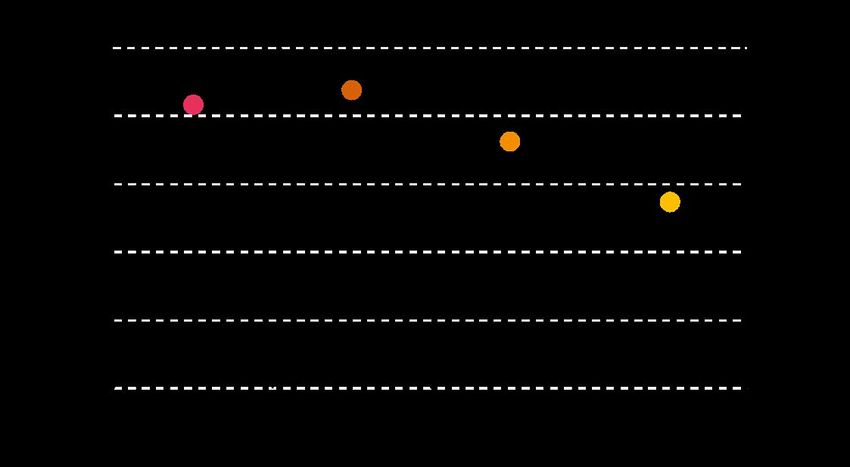

Private Markets Dry Powder ($bn)

The pandemic looks set to

accelerate longer term shifts in the

economy. This ranges from the

move to digital retail to

strengthening sustainability.

Corporate restructuring is set to

play a key role in helping businesses

to boost strategic agility and future-

proof their business models by

simplifying their structures, clearing

away non-core operations and

freeing up funds for investment.

Undeployed capital in private equity

and debt funds is at an all-time high,

significantly above the levels

available during the Global Financial

Crisis, creating a launchpad for a

fast acceleration in deals and market

recoveries. An increasing number

of companies have been able to

raise new financing without

significantly compromising existing

debts, and thereby avoided lengthy

restructuring processes.

For sources of the data presented in this report, please see page 49 at end of the report.Vestibulum venenatis eget odio quis

molestie.

5 | Global Restructuring Trends | PwC Data sources are available on page 49

Insolvency appointments

Canada China France

Germany Hong Kong Italy

Japan Russia United Kingdom

USA

Note: Q2 2020 figures for Germany,

France and Russia not included as data

was not available

Note: Graphs present the G8 countries

plus China and Hong Kong

6 | Global Restructuring Trends | PwC Data sources are available on page 49

Act now to recover

What then can you do now?

The crunch is coming for We believe that there are three key priorities:

troubled companies. Even

1. Determine what shape the business is in

those in reasonably good

The ‘health check’ should look at both the immediate

health now face fundamental state of the business and its longer term prospects.

What are the immediate threats? How is the company’s

changes ahead. As a creditor, competitive environment changing and how fit is it to

keep pace? What are the opportunities and how

sponsor or other stakeholder can the business capitalise? Is management on the

right track?

with a financial interest in a Even with the current uncertainty, there is a great deal

that can be determined by getting down to the detail in

company, how much longer areas such as customer demands, competition, supply

chains and access to investment. This not only

can you therefore afford to requires restructuring expertise, but also insights

into sector trends and how to respond, both locally

wait and see? and globally.

2. Clear the path to recovery

What is the path to recovery? What are management

The key message coming through from our Where Next teams doing to help accelerate progress? Do they have

industry perspectives is the extent to which COVID-19 has the capability to deliver the operational changes or

not only created severe strains for many businesses in the transactions required? Depending on the state of the

short-term, but also accelerated shifts in what customers business and its prospects, potential support ranges

expect and how businesses compete. Drivers of disruption from helping to shore up liquidity to divestitures, debt

and change stretch from the onward march of digitisation restructuring and facilitating access to fresh capital.

to demands for greater sustainability and social inclusion.

For the management and shareholders in the driving seat,

the shifts underline the need for plans that don’t just 3. Work through divergent interests

assume that everything will get back to where they were

Key questions include both when to step in and how.

before the pandemic, but actively prepare for the new

Sponsors may have different priorities from creditors.

environment. Wait too long and it may be too late.

Management may be wary or resistant to intervention.

Yet what does this all mean for you as one of the Different creditor groups may have different rights and

stakeholders that aren’t in the driving seat, but still have a leverage. Yet, by establishing a close relationship when

significant interest in the health and prospects of the the business is still viable rather than facing insolvency,

business? Rightly, you have offered space and support as parties have the opportunity to work effectively

businesses have sought to stabilise and stay afloat. But together to secure a better deal.

with furlough and other government lifelines being

withdrawn, the need to determine whether the business is

viable now and equipped for the changes ahead is

becoming ever more pressing. You might argue that the

trajectory of recovery is too uncertain to know whether the

business has a future and what steps are needed to

optimise its prospects. But if you do nothing, you might

find that the only option is the last resort of insolvency and

a consequential loss of value. Acting decisively now could

not only avert this, but also ensure that the business is in

the best shape to survive and thrive.

7 | Global Restructuring Trends | PwC Data sources are available on page 49

Australia

$1,393 12.3% 24.7%

2019 GDP (bn) Funding | August 2020 Furlough | July 2020

1.9% (4.5)% 4.0%

GDP YoY | 2009 GDP YoY | 2020 GDP YoY | 2021

5.6%

Unemployment | 2009

7.6%

Unemployment | 2020

8.9%

Unemployment | 2021

Australia is facing its first recession in nearly 30 years restructuring and insolvency activity to pick-up in

as a result of COVID-19. However, insolvency activity 2021 as the bulk of government support is scaled back.

has remained at historic lows. This reflects unprecedented Clearly some sectors are likely to face ongoing challenges,

levels of support for business from both the public and especially those where demand is driven by people coming

private sectors. from abroad such as the travel and tourism, tertiary

education, as well as accommodation and hospitality.

A combination of economic stimulus, the temporary

suspension of company directors’ obligations to avoid Restructuring will focus on stabilising balance sheets,

trading whilst insolvent, a moratorium on winding-up while accelerating digital transformation and reallocation

petitions and a strategic withdrawal from enforcement of resources to fast recovery and growth areas.

action by tax authorities has allowed many otherwise

‘challenged businesses’ to avoid insolvency. PwC Local contact: Stephen Longley

Restructuring activity has also remained subdued. stephen.longley@pwc.com

Many listed companies affected by the pandemic moved

quickly to raise fresh equity in March and April. Lenders +61 3 8603 3203

have also provided significant accommodation to

distressed companies in the form of covenant waivers

and principle and interest deferrals. We expect

Insolvency appointments

Note: Q2 2020 excludes June insolvency data

8 | Global Restructuring Trends | PwC Data sources are available on page 49Austria

$446 12.6% 36.8%

2019 GDP (bn) Funding | August 2020 Furlough | July 2020

(3.8)% (7.0)% 4.5%

GDP YoY | 2009 GDP YoY | 2020 GDP YoY | 2021

5.3%

Unemployment | 2009

5.5%

Unemployment | 2020

5.0%

Unemployment | 2021

In 2020, Austria’s GDP is expected to decline more sharply Despite the extension of government labour subsidies until

than during the Global Financial Crisis. While the current March 2021, we expect that the level of restructuring and

recession looks set to be short-lived, GDP is unlikely insolvency activity will increase in the remainder of 2020

to return to its pre-pandemic level by the end of 2021. and into the first half of 2021. It is clear that companies that

were already facing financial difficulties at the beginning of

Corporate insolvencies fell significantly in the first half 2020, along with those in fast-changing sectors such as

of 2020, largely due to government subsidies (liquidity retail, travel and tourism and manufacturing, are likely to

improvement actions, government-backed loans and face challenging market conditions.

short-time working). The fall also stems from new

insolvency legislation, which eliminates the over This underlines the importance of restructuring businesses

indebtedness-test until the end of Q3 2020. for long-term viability as well as near-term survival.

The main focus for businesses has been on crisis

management, securing liquidity and cost reductions.

PwC Local contact: Manfred Kvasnicka

The economic challenges have led to a rise in

unemployment. A number of initiatives to limit the manfred.kvasnicka@pwc.com

impact including short-time working have been

+43 1 501 88 29 37

introduced. We anticipate that the likelihood of an

economic recovery in 2021 will reduce the overall

impact on the employment market.

Insolvency appointments

9 | Global Restructuring Trends | PwC Data sources are available on page 49Belgium

$530 14.5% 22.5%

2019 GDP (bn) Funding | August 2020 Furlough | July 2020

(2.0)% (6.9)% 4.6%

GDP YoY | 2009 GDP YoY | 2020 GDP YoY | 2021

7.9%

Unemployment | 2009

7.3%

Unemployment | 2020

6.8%

Unemployment | 2021

In 2020, the Belgian economy is expected to experience The insolvency moratorium introduced during the first

the largest annual decline in GDP since the Second World wave of the COVID-19 lockdown has held back

War. A return to 2019 GDP levels is expected to take insolvencies. However, we expect the number of

several years. insolvencies to increase. There have already been initial

signs of this in the last few months. It is worth noting that

To date, the largest element of the increase in activity is primarily focused on businesses that were

unemployment has been among temporary and contract already facing financial distress entering 2020, with a

workers. Companies have drawn on furlough schemes in number of retail companies being especially impacted.

an effort to conserve liquidity. As these support measures

are phased out, a significant increase in overall

unemployment is expected until 2022. PwC Local contact: Thomas Deryckere

It is clear that the focus is now on cost reduction thomas.deryckere@pwc.com

initiatives, having at the outset of the pandemic been

upon conserving liquidity. +32 474 78 04 59

Insolvency appointments

10 | Global Restructuring Trends | PwC Data sources are available on page 49Brazil

$1,840 11.8% N/A

2019 GDP (bn) Funding | August 2020 Furlough | July 2020

0.1% (9.1)% 3.6%

GDP YoY | 2009 GDP YoY | 2020 GDP YoY | 2021

9.7%

Unemployment | 2009

14.7%

Unemployment | 2020

13.5%

Unemployment | 2021

Restructuring activity was limited in the first months to increase. Companies are also keen to put forward

of the pandemic. This is largely due to a combination viable business plans to support financial restructuring.

of government subsidies and greater flexibility in the

application of labour laws in areas such as reductions Pressure is coming from subdued consumer demand and

in working hours. rising unemployment. The temporary suspension of labour

regulations that has helped to protect jobs and prevent

The rapid moves by private banks to introduce covenant corporate failures also looks set to be phased out. In turn,

waivers and grace periods of between two-six months the government’s scope for further economic support may

for the payment of principal obligations contributed to the be curtailed by the pressure on public finances.

low levels of restructuring. With the end of these support

measures, we expect an increase in default rates.

As a result, banks have been raising their provisions PwC Local contact: Christine Savignon

for bad debt and increasing restrictions on new credit. christine.savignon@pwc.com

Estimates suggest that around 500,000 businesses

+55 11 3674 2710

had ceased to operate by June 2020, mainly small and

micro-enterprises. As we move into the second phase of

the economic emergency, we expect restructuring activity

Insolvency appointments

Note: No data available

11 | Global Restructuring Trends | PwC Data sources are available on page 49Canada

$1,736 14.3% 15.9%

2019 GDP (bn) Funding | August 2020 Furlough | July 2020

(2.9)% (8.4)% 4.9%

GDP YoY | 2009 GDP YoY | 2020 GDP YoY | 2021

8.4%

Unemployment | 2009

7.5%

Unemployment | 2020

7.2%

Unemployment | 2021

Corporate insolvency dipped significantly in Q2 2020. A their normal operations, as well as whether further

number of government wage subsidies, tax deferral and waves of COVID-19-related shutdowns will be ordered.

loan programmes have given companies time to review

their position and consider their options. However, some We anticipate that restructuring and insolvency activity

of these programmes are expiring or are due to be will increase through the autumn of 2020, particularly

modified. In the main, lenders have provided support as companies adjust to the new normal and the impact

to troubled debtors. of COVID-19 is more fully realised. However, Canada has

not yet seen the wave of defaults that were widely

Corporate restructuring under Canada’s debtor-led anticipated, though lenders are preparing for many new

restructuring statute saw a significant increase in the first troubled debtors in the coming quarter.

half of 2020, with as many new cases in Q2 (38 filings)

as in all of 2019. Many of these companies were already The overhang of the recession and underlying structural

facing financial issues that were exacerbated by the impact changes in the economy will result in a slow return to

of lockdown, notably in the retail sector. The economic pre-pandemic levels of economic activity across several

impact of COVID-19 in Canada has been particularly industries, including retail, travel and tourism, and

profound in the oil and gas, manufacturing, retail trade manufacturing.

and construction sectors. The dip in economic activity

was compounded by a sharp drop in oil and gas prices. PwC Local contact: Greg Prince

It is clear that economic recovery will depend heavily gregory.n.prince@pwc.com

on how quickly companies and consumers resume

+1 416 814 5752

Insolvency appointments

12 | Global Restructuring Trends | PwC Data sources are available on page 49Cayman and British Virgin Islands

$5 13.2% 7.1%

2019 GDP (bn) Funding | August 2020 Furlough | July 2020

(7.0)% (11.4)% 2.0%

GDP YoY | 2009 GDP YoY | 2020 GDP YoY | 2021

6.0%

Unemployment | 2009

11.6%

Unemployment | 2020

5.3%

Unemployment | 2021

The economies of the Cayman and British Virgin Islands liquidation process, whilst being afforded the benefits

(BVI) are dominated by tourism and hospitality and financial of a moratorium. We anticipate that this will increase

services. Tourism and hospitality have been severely restructurings substantially. In BVI, the Court has recently

affected by COVID-19-related travel restrictions. However, appointed its first ever ‘light touch’ provisional liquidator,

financial services (mainly fund and corporate activity) has similarly opening the door for substantially more financial

been buoyed by the stimulus packages put in place by restructuring processes in future.

governments worldwide.

Insolvencies have generally been subdued, though we’re PwC Local contact: Simon Conway

now seeing a steadily increasing flow of enquiries. We

anticipate a rise in fund redemptions and an increase in simon.r.conway@pwc.com

distressed insolvent scenarios into 2021, as national

+1 345 914 8688

governments start to withdraw economic support.

Restructuring activity is increasing as a number

of major corporate entities seek to restructure their

debts and avoid insolvency.

This trend is likely to continue into 2021. Legislation is

currently pending in the Cayman Islands, which will allow

debtors to appoint a restructuring officer, outside of a

Insolvency appointments

Note: No data available

13 | Global Restructuring Trends | PwC Data sources are available on page 49Central and Eastern Europe (CEE)

$2,262 5.4% N/A

2019 GDP (bn) Funding | August 2020 Furlough | July 2020

(3.0)% (5.0)% 4.8%

GDP YoY | 2009 GDP YoY | 2020 GDP YoY | 2021

9.0%

Unemployment | 2009

8.9%

Unemployment | 2020

7.6%

Unemployment | 2021

Insolvency activity has been subdued across the Central Looking ahead, we expect an uptick in restructuring activity

and Eastern Europe (CEE) region due to government across the CEE region in Q4 2020, once the institutional

measures introduced in response to COVID-19. support is ended.

These include a moratorium that has enabled banks

to adopt a collaborative approach with debtors. The key industries which remain under pressure in

The exception is Romania, which has recorded an the region are automotive, retail, tourism and hospitality.

increase in the number of insolvencies.

PwC Local contact: Petr Smutny

Restructuring activity has also remained generally

low across the region for the same reasons, though petr.smutny@pwc.com

the Czech Republic has seen an increasing trend.

+420 251 151 215

Businesses have mainly focused on preserving liquidity

by drawing on the government support structures, as

well as cost reduction and stabilisation of supply chains.

Insolvency appointments

Note: No data available

14 | Global Restructuring Trends | PwC Data sources are available on page 49China

$14,343 4.6% N/A

2019 GDP (bn) Funding | August 2020 Furlough | July 2020

9.4% 1.2% 9.2%

GDP YoY | 2009 GDP YoY | 2020 GDP YoY | 2021

4.3%

Unemployment | 2009

4.3%

Unemployment | 2020

3.8%

Unemployment | 2021

China has seen a significant deceleration in growth Signs are that the government might not prevent the

in the wake of the COVID-19 pandemic. downturn of some companies. This will lead to an increase

in insolvency activity and put pressure on businesses to

Consumer spending fell by 1.38 trillion yuan (US$199.3bn) accelerate restructuring.

in the first two months of the year due to the severe

impact of the outbreak on restaurants, hotels, tourism, Industries such as financial services, public health and

entertainment and transportation sectors. In turn, the care sector are more likely to attract foreign direct

passenger car sales saw the biggest drop in nearly investment due to relief policies introduced recently.

two decades.

PwC Local contact: Victor Jong

Chinese regulators have introduced a series of measures to

ease the financial pressures on enterprises emanating from victor.yk.jong@cn.pwc.com

the pandemic. Financial policies are geared towards certain

industries such as medical and life supplies for pandemic +852 2289 5010

prevention, aviation, agricultural and green energy vehicles.

There is also tax relief to help ease cash flow or liquidity

issues. However, despite this support, the number of

insolvencies is still higher than the comparable last year.

Insolvency appointments

15 | Global Restructuring Trends | PwC Data sources are available on page 49Denmark

$348 5.8% 9.2%

2019 GDP (bn) Funding | August 2020 Furlough | July 2020

(4.9)% (6.5)% 6.0%

GDP YoY | 2009 GDP YoY | 2020 GDP YoY | 2021

6.4%

Unemployment | 2009

6.5%

Unemployment | 2020

6.0%

Unemployment | 2021

The number of insolvencies dipped in the first half of 2020 The economic outlook in Denmark is uncertain. The Danish

despite the biggest quarterly drop in GDP in Q2 since the National Bank anticipates that recovery to pre-pandemic

Global Financial Crisis. levels of output could take several years. As Denmark is a

small and open exporting economy, it’s dependent on the

This is largely explained by government-funded relief global economy. We expect exporting companies and

initiatives such as postponement of VAT payments, salary businesses with foreign operations to be especially

compensation to furloughed employees and funding to affected by the current uncertainties. We also see an

cover pandemic-related losses. We also saw an expansion unusually high number of vacant leases in the retail sector,

of lending and guarantee capacity through state-financed and a low occupancy rate in hotels due to COVID-19.

lending entities. During lockdown, Danish courts were only

open for self-declaration of bankruptcy, which prevented We expect the support required in the near future will be

third-parties or creditors from filing. In addition, banks focused on securing financing to sustain operations. We

reported an unforeseen decrease in their lending activities, also expect restructuring support to increase, especially

due to the relief initiatives from the government. once the COVID-19 government measures are phased

out. We have also seen a focus on cash forecasting and

In line with global trends, the emphasis for businesses has working capital optimisation, and we believe this trend

been on crisis management, accessing liquidity and supply will continue in the near future.

chain resilience. The majority of the government funded

schemes are ending in Q3. We therefore expect to see an PwC Local contact: Mads Johansson

uptick in insolvency activity.

mads.johansson@pwc.com

+45 39 45 37 77

Insolvency appointments

16 | Global Restructuring Trends | PwC Data sources are available on page 49East Africa

$240 1.3% N/A

2019 GDP (bn) Funding | August 2020 Furlough | July 2020

5.2% 0.8% 5.1%

GDP YoY | 2009 GDP YoY | 2020 GDP YoY | 2021

6.4%

Unemployment | 2009

8.6%

Unemployment | 2020

9.0%

Unemployment | 2021

The adverse impact of COVID-19 on East African Given the high leverage and widespread financial distress

businesses has been severe. The region’s economies have across East African businesses before the pandemic, these

limited capacity to absorb the resultant economic shocks, steps defer rather than resolve the problems.

and governments have limited ability to offer significant

stimulus and support. Conversely, insolvency activity has dipped. This is despite

the recent implementation of insolvency-related legal and

This impact is reflected in increasing levels of regulatory reforms in a number of regional markets, aimed

non-performing loans. While this would normally at making insolvency regimes ‘business rescue’ friendly.

have led to a surge in lender-driven insolvencies, central

banks are encouraging banks to favour restructuring We expect to see comprehensive restructuring of balance

instead. The result has been an unprecedented upsurge sheets as lenders take stock of their position and the

in the volume and value of restructured facilities. In Kenya, outlook for clients in the post-pandemic period.

for example, 29% of the total banking sector loan book

PwC Local contact: George Weru

was restructured between March and June 2020.

However, this mostly comes in the form of moratoriums george.weru@pwc.com

on debt service obligations and extension of tenor rather

than a comprehensive restructuring of balance sheets. +254 727 34 15 84

Insolvency appointments

Note: No data available

17 | Global Restructuring Trends | PwC Data sources are available on page 49Finland

$269 5.2% 7.4%

2019 GDP (bn) Funding | August 2020 Furlough | July 2020

(8.1)% (6.0)% 3.1%

GDP YoY | 2009 GDP YoY | 2020 GDP YoY | 2021

8.3%

Unemployment | 2009

8.3%

Unemployment | 2020

8.4%

Unemployment | 2021

Insolvency activity in the first half of 2020 was down In line with global trends, the emphasis for businesses

from 12 month before. This is mainly due to government has been on crisis management, accessing liquidity,

moves to expand lending and guarantee capacity to supply chain resilience and rent re-negotiations.

SMEs, ensuring sufficient access to finance and reducing

the structural buffer requirements for the banking sector. We anticipate that, in the event of a renewed COVID-19

Access to capital has been gradually improving over outbreak followed by further lockdowns, there will

recent months. be a severe impact on SMEs. This contrasts with

larger companies, which are more dependent on

The government has also initiated targeted liquidity exports and global demand.

improvement actions for the most severely impacted

sectors, such as aviation and shipping. PwC Local contact: Michael Hardy

As a result of these initiatives, restructuring activity michael.hardy@pwc.com

has remained relatively quiet.

+358 20 7877442

Insolvency appointments

18 | Global Restructuring Trends | PwC Data sources are available on page 49France

$2,716 5.6% 32.6%

2019 GDP (bn) Funding | August 2020 Furlough | July 2020

(2.9)% (12.5)% 7.3%

GDP YoY | 2009 GDP YoY | 2020 GDP YoY | 2021

9.1%

Unemployment | 2009

10.4%

Unemployment | 2020

10.4%

Unemployment | 2021

The impact of lockdown on the French economy has Furthermore, these economic difficulties could also spur

been compounded by the dent to important sectors the need for refinancing of some of the lending supported

such as aerospace, automotive and tourism. Government by the guarantee programme.

support to help viable companies to ride out the impact

has included loan guarantees to encourage bank lending. The government is currently transposing the 2019 EU

restructuring directive into law. This should improve the

As a result, restructuring activity has been focused prospects for secured creditors, relative to shareholders

on two factors. The first is shoring up the balance sheets and unsecured creditors. Some temporary measures have

of otherwise viable companies applying to the guarantee also been implemented to ease the restructuring processes

programme. The second is stabilising companies that had during the post-pandemic period. Examples include flexible

already faced difficulties before the pandemic, including access to asset deals for existing shareholders, in absence

some retail businesses affected by digital competition. of other credible options.

Over the next few months, we expect the number of PwC Local contact: Sébastien Dalle

companies in financial distress or bankruptcy to increase,

resulting from the relative weakness of the economic sebastien.dalle@pwc.com

rebound across many sectors.

+33 1 56 57 80 13

Insolvency appointments

Note: Q2 2020 excludes June insolvency data

19 | Global Restructuring Trends | PwC Data sources are available on page 49Germany

$3,486 12.5% 18.7%

2019 GDP (bn) Funding | August 2020 Furlough | July 2020

(5.7)% (7.8)% 5.4%

GDP YoY | 2009 GDP YoY | 2020 GDP YoY | 2021

7.7%

Unemployment | 2009

3.9%

Unemployment | 2020

3.5%

Unemployment | 2021

The German economy faced significant headwinds We expect to see an increase in restructuring activity

from the outbreak of COVID-19 as a result of its reliance as government support is scaled back.

in exports. However, economic activity has begun to

slowly get back on track on the back of some €1.3tn The continuing impact of the pandemic is likely to spur

in government subsidies. The support includes tax restructuring within the automotive sector in particular.

reductions, furloughs and state aid in form of loans Alongside the near-term dent in consumer demand

and equity. stemming from the outbreak, carmakers face a longer-

term shift towards hybrid and fully electric vehicles.

Further relief has come from the temporary suspension

of the obligation to file for insolvency until the end of Furthermore, we expect to see increased restructuring

September 2020, with an option to extend this until the in challenged sectors such as retail, shipping and

end of March 2021. As a result, insolvency proceedings industrial manufacturing.

declined by nearly 10% in May 2020 compared to May

2019. Restructuring activity and default rates have also PwC Local contact: Daniel Judenhahn

been subdued due to government support. daniel.judenhahn@pwc.com

The main focus of businesses in the last months has

+49 69 9585 6976

been on accessing liquidity, crisis management and

supply chain stabilisation.

Insolvency appointments

Note: Q2 2020 excludes June insolvency data

20 | Global Restructuring Trends | PwC Data sources are available on page 49Greece

$210 12.8% N/A

2019 GDP (bn) Funding | August 2020 Furlough | July 2020

(4.3)% (10.0)% 5.1%

GDP YoY | 2009 GDP YoY | 2020 GDP YoY | 2021

9.6%

Unemployment | 2009

22.3%

Unemployment | 2020

19.0%

Unemployment | 2021

The impact of the COVID-19 pandemic has been A new Bankruptcy Code is about to come into effect (from

heightened by the importance of tourism to the Greek 2021) incorporating the EU restructuring directive. This will

economy (some 20% of GDP). Coordinated monetary, help to streamline bankruptcy processes, bring together

fiscal and regulatory support has helped to ease the restructuring regimes under one code and reduce the time

difficulties faced by businesses across the economy. to discharge. It will also usher in early warning mechanisms

and a truly out of court workout. as well as the digitisation

As a result, restructuring activity has been low in 2020 of procedures. We believe that the changes will make

so far. The winding down of government and bank restructuring, pre-insolvency procedures and bankruptcy

support, paired with the fact that servicers are taking more efficient.

over the majority of non-performing loans, will be

key drivers of increased restructuring activity over

PwC Local contact: Ioannis Theologitis

the next period.

ioannis.theologitis@pwc.com

+30 21 0687 4654

Insolvency appointments

Note: No data available

21 | Global Restructuring Trends | PwC Data sources are available on page 49Hong Kong

$366 10.0% N/A

2019 GDP (bn) Funding | August 2020 Furlough | July 2020

(2.5)% (4.8)% 3.9%

GDP YoY | 2009 GDP YoY | 2020 GDP YoY | 2021

5.2%

Unemployment | 2009

4.5%

Unemployment | 2020

3.9%

Unemployment | 2021

The government has supported business and jobs through We expect the hard-hit travel and aviation sectors to take

three rounds of funding totalling HKD288bn (US$37.1bn) longer to return to 2019 activity levels as the catalyst of

since the start of 2020. Moreover, in April, the Hong Kong lockdown changes people’s behaviour and priorities in the

Monetary Authority instructed all banks to grant a longer term. Accommodating these changes will require a

six-month loan repayment holiday to SMEs, which has significant rethink when it comes to liability management.

given respite to SMEs across a range of different sectors.

With economic strains continuing and new bank financing

As a result, insolvency activity has been relatively muted becoming more difficult and pricier to secure, we anticipate

this year, with only 62 compulsory winding up orders this that the number of insolvencies may go up in Q4 2020 or

year compared with 126 for the comparable period last early next year. Businesses and lenders are unable to hold

year. The lower numbers may also be attributable to the out indefinitely despite the government measures.

impact of COVID-19 on court operations.

PwC Local contact: Peter Greaves

Nonetheless, many businesses, especially those in the

consumer and retail industries, have faced significant peter.greaves@hk.pwc.com

liquidity issues, requiring them to focus on reducing their

highest outgoings – typically rental expense and +852 2289 1826

employee wages.

Insolvency appointments

22 | Global Restructuring Trends | PwC Data sources are available on page 49India

$2,876 7.0% N/A

2019 GDP (bn) Funding | August 2020 Furlough | July 2020

8.5% (4.5)% 6.0%

GDP YoY | 2009 GDP YoY | 2020 GDP YoY | 2021

5.6%

Unemployment | 2009

11.0%

Unemployment | 2020

9.8%

Unemployment | 2021

Insolvency rates have been held in check by government adjust loan arrangements in sectors under stress.

and regulatory intervention.

While unemployment rose initially, it has started to fall as

Recent regulatory action includes an increase in the businesses come out of lockdown. Business sentiment is

threshold for invoking proceedings, inclusion of a special also encouraging. PwC research has found that more than

insolvency resolution framework for SMEs and a 80% of businesses are confident that the economy can

moratorium on fresh initiation of proceedings for six return to the pre-pandemic levels by June 2021. The

months. The Reserve Bank of India (RBI) has also research underlines the importance of getting on

introduced a Resolution Framework for COVID-19 Related the front foot in seeking to restructure businesses and

Stress, which aims to revive real estate sector activities and boost viability. Respondents in our survey attribute their

mitigate the impact of financial stress on borrowers. resilience in the face of stress and confidence in their

ability to rebound to operational flexibility, robust crisis

Business agenda is primarily focused on maintaining the management and effective process/product innovation.

debt-equity ratio, reviving demand and optimising cost

management. In turn, the government has been focusing

closely on credit availability, resource utilisation and PwC Local contact: Dinesh Arora

entrepreneurship. Further interventions include the RBI

dinesh.arora@pwc.com

prudential norms, which grant banks a one-off window to

+91 98 10 19 12 91

Insolvency appointments

Note: No data available for Q2 2020

23 | Global Restructuring Trends | PwC Data sources are available on page 49Ireland

$389 7.1% 18.8%

2019 GDP (bn) Funding | August 2020 Furlough | July 2020

(5.1)% (6.8)% 6.3%

GDP YoY | 2009 GDP YoY | 2020 GDP YoY | 2021

12.6%

Unemployment | 2009

12.1%

Unemployment | 2020

7.9%

Unemployment | 2021

Restructuring activity in Ireland has remained relatively to the direct impacts of COVID-19 when assessing

subdued. The insolvency rate in the first half of 2020 was if a director acted recklessly when trading while insolvent

down by around 30% compared to the same period in on the basis they act in good faith and responsibly.

2019. Contributing factors include payment breaks for New temporary insolvency legislation is being introduced.

borrowers, together with the impact of government support The most notable changes are to extend the examinership

schemes. The acid test of viability for businesses will come period by a further 50 days if required, permit remote/

when the government aid is withdrawn. virtual creditor meetings and an increase the winding

up debt threshold to €50,000.

A key focus for businesses has been the renegotiation

of leases and the granting of forbearance. This has led We expect large multinational businesses to bounce back

to some high-profile disputes between landlords and their quickly, but the SME sector will take a number of years to

tenants. There have already been a number of liquidations recover. A lot of SMEs are already highly leveraged from

in the retail sector, driven primarily by administrations and the last downturn. They will therefore require some form of

downsizing of UK-parent companies whose difficulties restructuring, refinancing and/or change of management in

were accelerated in the COVID-19 lockdown. order to survive. Schemes such as the recently introduced

State Credit Guarantee for 80% of borrowings will be

There is likely to be an increase in restructuring and crucial to the survival of these businesses, which are the

insolvency activity in the first half of 2021. The Office of the lifeblood of the Irish economy.

Director of Corporate Enforcement issued guidance, and

some comfort, to directors that they would give due regard PwC Local contact: Declan McDonald

declan.mcdonald@pwc.com

Insolvency appointments

+353 1 792 6092

24 | Global Restructuring Trends | PwC Data sources are available on page 49Italy

$2,001 4.5% 45.2%

2019 GDP (bn) Funding | August 2020 Furlough | July 2020

(5.3)% (12.8)% 6.3%

GDP YoY | 2009 GDP YoY | 2020 GDP YoY | 2021

7.7%

Unemployment | 2009

12.7%

Unemployment | 2020

10.5%

Unemployment | 2021

Restructuring and insolvency activity was relatively A significant increase in new insolvency and restructuring

quiet in the first half of 2020 as a result of emergency is expected in the first quarter of 2021, once the existing

legislation and generally supportive approach of banks support measures have ceased. In the case of distressed

and creditors. This includes the option to suspend companies, there may be the need for capital restructuring.

payments for 6-12 months.

In both cases, investors could play a significant role,

The gathering recovery of the economy is expected with the Italian banking system involved in a new wave

to continue in the coming months. Confidence has of de-risking (through the disposal of non-performing

continued to improve in all sectors. loan portfolios and single names, as well as outsourcing

of their management to dedicated platform). Recent deal

Stronger companies have found it relatively easy activity also suggests that there is likely to be further

to access bank finance. Loans are secured by government consolidation among TIER-2 banks.

guarantees to cover losses and support short-term cash

needs. However, businesses that took advantage of last

PwC Local contact: Michele Peduzzi

year’s government-backed debt restructuring measures

have generally not been able to benefit from the current michele.peduzzi@pwc.com

guarantees. As a result, they may need to re-open

discussions with banks and look for solutions without +39 02 8064 6371

government support.

Insolvency appointments

25 | Global Restructuring Trends | PwC Data sources are available on page 49Japan

$5,082 42.2% 6.2%

2019 GDP (bn) Funding | August 2020 Furlough | July 2020

(5.4)% (5.8)% 2.4%

GDP YoY | 2009 GDP YoY | 2020 GDP YoY | 2021

5.1%

Unemployment | 2009

3.0%

Unemployment | 2020

2.3%

Unemployment | 2021

While GDP has fallen, the number of insolvencies has Other than COVID-19 related developments, there are

not increased, and the rate of unemployment has been likely to be more opportunities for business restructuring.

stable. Since the Global Financial Crisis, Japanese These include portfolio reorganisation, operational

companies have been improving their level of cash restructuring and divestments in Japanese corporations.

and shareholder equity. This is due, in part, to track record of growth in

conglomerates, sometimes retaining unprofitable

In response to the pandemic, the government and non-core businesses. Furthermore, we expect to see a

banks coordinated moves to bolster liquidity and help consolidation of the banking system, as smaller regional

corporations to protect their cash positions. Further banks have been affected by a slow economic recovery

steps include a government scheme to support SMEs, and poor interest rates. The government appears open to

with funding equivalent to more than 20% of 2019 GDP. supporting any regulatory reform required to enable the

Some specific sectors (e.g. automotive, auto-parts, consolidation process.

hospitality & leisure, retail & consumer) have been

PwC Local contact: Kiwamu Sugimoto

heavily disrupted by the COVID-19 outbreak and have

yet to recover. Consequently, if the COVID-19 outbreak kiwamu.k.sugimoto@pwc.com

continues or there is a renewed surge in cases, there

is likely to be more restructuring. +81 80 3519 9482

Insolvency appointments

26 | Global Restructuring Trends | PwC Data sources are available on page 49Malaysia

$365 4.2% N/A

2019 GDP (bn) Funding | August 2020 Furlough | July 2020

(1.5)% (1.7)% 9.0%

GDP YoY | 2009 GDP YoY | 2020 GDP YoY | 2021

3.7%

Unemployment | 2009

4.9%

Unemployment | 2020

3.4%

Unemployment | 2021

To protect jobs and stimulate the economy, the Central PwC Local contact: Victor Saw

Bank of Malaysia initiated an automatic moratorium

on all loan/financing, payments, principal and interest victor.saw.seng.kee@pwc.com

by individuals and SME borrowers for a period of six

+60 3 2173 1677

months from 1 April 2020. The moratorium was further

extended for three months to those who are directly

impacted by the pandemic.

Insolvency activity has been subdued due to various

initiatives by the government to protect companies against

collapse. This has given the businesses disrupted by the

pandemic some lifelines. However, we anticipate insolvency

activity to pick up in 2021. Especially on highly geared

companies when the government pulls the brake on

existing support measures

Insolvency appointments

Note: No data available for Q1 2020 and Q2 2020

27 | Global Restructuring Trends | PwC Data sources are available on page 49Middle East

$2,692 3.1% N/A

2019 GDP (bn) Funding | August 2020 Furlough | July 2020

0.5% (4.5)% 3.7%

GDP YoY | 2009 GDP YoY | 2020 GDP YoY | 2021

6.9%

Unemployment | 2009

10.9%

Unemployment | 2020

9.0%

Unemployment | 2021

Liquidity has come under pressure following the decline in pandemic demands a more holistic solution for borrowers

oil prices and the COVID-19 pandemic. In 2020 there have who have taken advantage of these schemes.

already been a number of high profile corporate collapses

in the region. Widespread legislative changes in the bankruptcy

and restructuring frameworks of most major regional

A combination of government support and initiatives jurisdictions could support distressed businesses in

have so far helped to delay more widespread defaults. restructurings and also provide alternative options for

For example, the UAE Central Bank has issued directives creditors. In 2020, there has already been a number of

to offer relief measures to banks, corporates and long running and high profile cases put forward under the

individuals within the country and implemented the new Kingdom of Saudi Arabia bankruptcy law where there

Targeted Economic Support Scheme (TESS), to support are now over 500 cases in total. Earlier in the year in the

banks in providing relief to corporate borrowers. The TESS UAE, the Financial Reorganisation Committee accepted

scheme is currently due to expire in Q4. Similar measures the first two applications to support multi-billion dollar

have been taken elsewhere in the region, notably by the restructurings of prominent groups in the region. These are

Saudi Arabian Monetary Authority. The support provided likely to pave the way for an increased interest in the formal

by banks has typically comprised of deferrals rather frameworks now in place to support distressed situations.

than waivers.

As the deferrals come to an end, we expect the economic PwC Local contact: Mo Farzadi

pressure created by lower oil prices and the impact of the mo.farzadi@pwc.com

+971 56 682 0649

Insolvency appointments

Note: No data available

28 | Global Restructuring Trends | PwC Data sources are available on page 49The Netherlands

$909 4.9% 28.0%

2019 GDP (bn) Funding | August 2020 Furlough | July 2020

(3.7)% (7.7)% 5.0%

GDP YoY | 2009 GDP YoY | 2020 GDP YoY | 2021

4.4%

Unemployment | 2009

6.5%

Unemployment | 2020

5.0%

Unemployment | 2021

Following sharp falls in GDP and rises in unemployment, The sectors that are likely to face increasing pressure

the Dutch economy is not expected to recover to pre-crisis include retail, travel, transportation & logistics, but also

levels until 2024 in more conservative scenarios. the construction sector. The construction sector was

already under pressure pre-COVID-19, driven by the

Nonetheless, insolvency rates have stayed remarkably so-called PFAS-crisis and nitrogen-crisis, during which

low, driven by support from the government, as well as a limited number of permits were issued by the government

the banking sector. For affected companies, the options for new building projects.

include partial payment of a company’s personnel costs

by the government, the postponement of tax payments In light of these developments, the new WHOA

and government guarantees on newly issued bank loans. restructuring law, which is expected to become

At the same time, banks have offered to suspend interest effective during the second half of 2020, is becoming

and amortisation payments. As a result, insolvencies were even more relevant. This so-called ‘Dutch scheme’

concentrated in sectors where the impact of the crisis was allows for a court-approved restructuring plan, in

most severe, such as travel and leisure. which hold-out positions are less likely to frustrate

a (consensual) restructuring. It also allows for a

As government support is expected to decrease significantly faster restructuring process.

over the coming months and tax liabilities and interest

and amortisation payments become due, a wave of

insolvencies is expected during Q4. This would be

PwC Local contact: Peter Wolterman

even more likely if there is a second wave of infections. peter.wolterman@pwc.com

+31 088 792 50 80

Insolvency appointments

29 | Global Restructuring Trends | PwC Data sources are available on page 49New Zealand

$207 21.3% 66.3%

2019 GDP (bn) Funding | August 2020 Furlough | July 2020

0.3% (7.2)% 5.9%

GDP YoY | 2009 GDP YoY | 2020 GDP YoY | 2021

5.8%

Unemployment | 2009

9.2%

Unemployment | 2020

6.8%

Unemployment | 2021

The level of formal insolvencies has remained broadly We anticipate a significant uptick in insolvency and

consistent with last year, but the rates have actually restructuring activity in Q1 2021, once the existing support

decreased since the outbreak of COVID-19. This is largely measures wind down. The main focus will be businesses

due to government initiatives that have provided in sectors such as tourism, hospitality and leisure and

businesses with additional liquidity (e.g. wage subsidies, tertiary education, along with primary industry segments

cashflow loans and tax regime changes). However, the reliant on recognised seasonal workers. As these

banking sector has also played a key role through allowing sectors look to recover, much will depend on the lifting

principal holidays, covenant waivers and the extension and of border restrictions.

re-purposing of existing loan facilities.

More broadly, we expect that many business owners

In addition, the temporary relaxation of certain directors’ will take 2020 as a ‘moment of truth’ and run a ruler across

duties is intended to give boards of viable businesses the their businesses from top to bottom. Financial, operational

confidence to trade on through the COVID-19 uncertainty. and strategic restructuring solutions (e.g. divestment of

non-core entities) will be used to create businesses that

The introduction of a new Business Debt Hibernation are more internationally competitive, environmentally

scheme provides an option for businesses to obtain a sustainable and clear on their value propositions and

seven-month standstill on existing trade debts. However, competitive advantages. This will act as a springboard

for those under greater financial pressures, this may have for long term viability and growth beyond the recovery.

to be used alongside other restructuring processes (e.g.

a creditor compromise) to be effective.

PwC Local contact: John Fisk

john.fisk@pwc.com

Insolvency appointments

+64 4 462 7486

30 | Global Restructuring Trends | PwC Data sources are available on page 49Norway

$403 4.5% 8.5%

2019 GDP (bn) Funding | August 2020 Furlough | July 2020

(1.7)% (6.3)% 2.9%

GDP YoY | 2009 GDP YoY | 2020 GDP YoY | 2021

3.3%

Unemployment | 2009

13.0%

Unemployment | 2020

7.0%

Unemployment | 2021

The economy has been hit by both COVID-19 and In comparison to other markets, Norwegian regulations

low oil prices, resulting in the lowest GDP growth in and procedures for debt negotiations have been seen

decades. Tourism, travel, entertainment, hospitality and as rigid, and rarely used. This could now change.

offshore are amongst the most heavily affected sectors.

The new legislation has similarities to Chapter 11 in

However, overall insolvency activity has remained stable the US and is expected to improve the scope for

as a result of extensive economic support packages from meaningful negotiations and solutions.

the government. Many businesses have focused on crisis

management, cash flow forecasting and securing liquidity. PwC Local contact: Per Christian Wollebæk

We expect restructuring and insolvency activity to increase per.wollebaek@pwc.com

in 2021 as government support unwinds. Moreover, a new

temporary law, expected to become permanent, may +47 952 60 318

contribute to an increased number of debt negotiations,

with the aim to avoid unnecessary bankruptcies.

Insolvency appointments

31 | Global Restructuring Trends | PwC Data sources are available on page 49You can also read