Implementing a Fully Effective US Child Allowance via a System of Monthly Refundable Child Tax Credits

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

“

Implementing a Fully Effective US Child

Allowance via a System of Monthly

Refundable Child Tax Credits

For CPR Seminar October 21,2021

Tim Smeeding

Lee Rainwater Distinguished Professor of Public Affairs and Economics

Member NAS Committee on Halving Child Poverty

Former Director, Institute for Research on Poverty

Research | Training | Policy | Practice

Openers • The new refundable child tax credit is a revolution in US social policy. Most families with incomes under $250,000 are now ( since July ) receiving $250 or $300 a month per child under age 17 to support their children. 3 kids? -- $750-$900 per month • The system is akin to the ‘child allowance system’ in at least 20 other rich and middle- income countries . ▪ Lecture will give some history of its creation, current effects, longer-term payoff and challenges, especially in reaching the lowest income children who would benefit most ▪ For example : many of the eligible poor who did not file taxes, like some ‘grand families’ who are raising their grandkids , and some who do, eg US born citizen children of immigrants, is much slower than expected, and complex families are always difficult • Leave time at the end for asking questions about the program as well.

Lecture Outline A. What is the US monthly refundable CTC: the current US version of a child allowance; how does it work ? B. Impacts of the CTC so far, focus on three groups: 1. Poor. greatest need, but difficult for IRS delivery; work effort, the CTC and the CDCTC 2. Working and Middle class. Success for non-college grad blue collar workers !! 3. Upper Income parents –where should the CTC phase out ? C. Where we stand: need to improve delivery & implementation D. Summary and Conclusion: What’s Next ?

A. The monthly, refundable

Child Tax Credit (CTC) in broader perspective

• Not a new idea, really, but a stunning change in the American

social policy context

• Generically called a “child allowance”, the monthly refundable

CTC, is a nearly “universal” benefit and the norm amongst 17+

other affluent countries, including Canada (‘child benefit’ of up

to $4,600 in CA cuts child poverty rate by more than 1/3 –below)

• These ‘universal’ policies are based on the idea that:

1. kids are expensive, and

2. society has a shared interest in seeing them thrive.

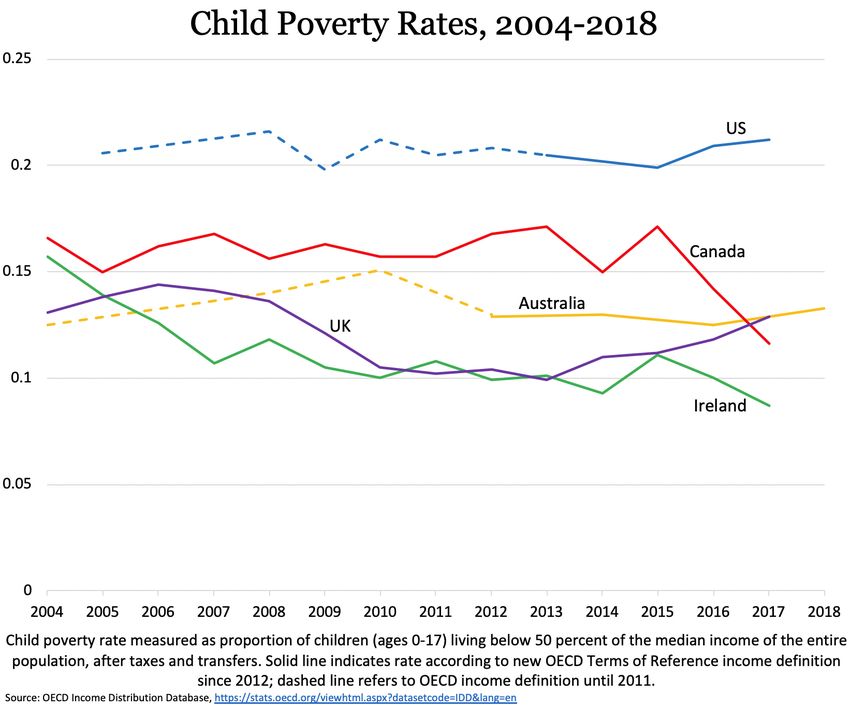

Cross-national Family Support Spending

(red arrows highlight other Anglo nations)

Effects of Spending:

Children in families

with incomers less

than half of the

median adjusted

disposable income, in

Canadian child benefit Anglophone nations

began in 2016

Source: OECD

Five Policy goals for the

USA monthly refundable CTC

• Make family life more affordable for families with children

and low incomes (esp. poor & working class)

• Reduce material hardship

• Provide stability – put a floor under monthly family income,

and reduce month to month income instability

• Cut child poverty - child poverty could be halved or for sure

reduced substantially– by about 40% by CTC alone

• Increase self-sufficiency via market work when it benefits the

family in terms of costs of childcare, schedules, etc.

How do we make a bigger dent in child poverty ? • Child poverty could be halved in two ways : 1. Monthly CTC-- rest from complementary income support policies like SNAP , with no additional work effort 2. NAS thrust-- additional work supports like the Child and Dependent Care Tax Credit (CDCTC ) and the EITC would complement the CTC and cut the “Gordian Knot” of anti- poverty programs by increasing both income support and work effort

Current and Proposed CTC Facts & Opinion • Fact: about 90% of all US kids will get credits higher than $200o per child and about 97% of all US kids will get some type of CTC benefit under current and proposed law • Fact: Total cost of expanded CTC is about $100-$110 billion a year, on top of current $125 billion, so not cheap • Opinion: targeting the CTC to ‘ those who need it’ depends heavily on implementation of a longer run, more effective CTC, administered by both the IRS and SSA, with additional administrative expenses to ease implementation

How Does the US monthly refundable

Child Tax Credit ( CTC) work ?

• US has had a CTC since 1998 ($1000 then) ; no child deductions since 2017

• In 2017 the CTC became $2000 per child, per year, available to families

with kids up to $400,00o a year, as an annual tax credit (next)

• But refundability was limited: the bottom 10% of families with no

earnings got no benefits ; and next 25% got only partial refunds (next)

• For 2021 only, the credit is fully refundable up to $3600 per year

• First half comes monthly and started in July; the second half comes as a

tax credit when 2021 taxes are filed ; the credit doesn’t begin to fade until

single parent incomes are above $112,000/ couples, above $150,000 (next)

• Higher income families (above $250,000 for couples; $150,000 for single

parents ) continue to receive the $2000 CTC from the 2017 TCJAThree rough focal groups for the CTC: • Poor and Near Poor (under ~ 100%/125% poverty ) • Working & Middle Class (~125%-200%/up to 400% pov.) • Higher Income (above 400% poverty) • Explore more below, keeping in mind: --about half of all kids under age 17 live in families with incomes below 200 % poverty (~ $60,000 / $70,000 per year ) -- only about 10 % of kids under age 17 live in families with incomes above $220,000

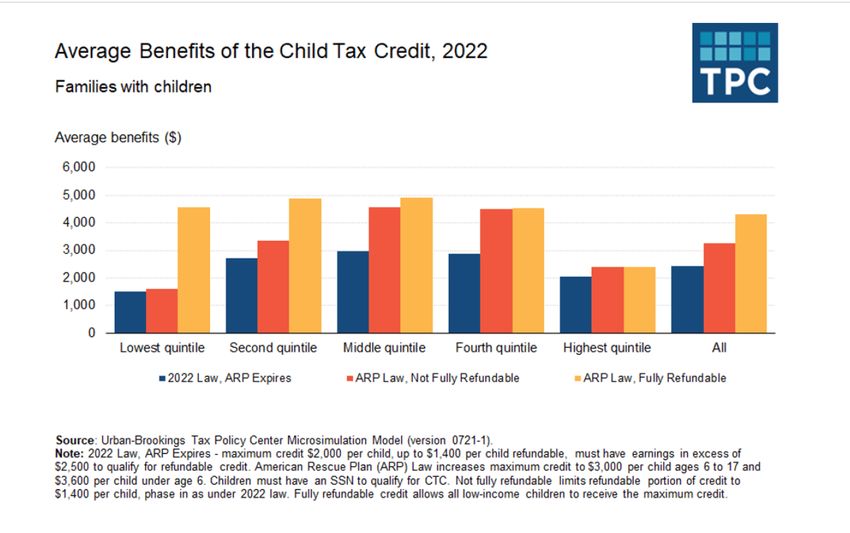

FIGURE 1

Child Tax Credit, Married Parents, One child, 2020-2021

$4,000

Credit for children ages 0–5

$3,500

Credit for children ages 6–17

$3,000

Prior law credit for children ages 0–16

$2,500

$2,000

$1,500

Poor & Working & Higher Income Families

$1,000 Near Poor Middle Class

$500

$0

$0 $50,000 $100,000 $150,000 $200,000 $250,000 $300,000 $350,000 $400,000 $450,000 $500,000

Adjusted gross income

Source: Urban-Brookings Tax Policy Center calculations.

Notes: Assumes all income comes from earnings, and child meets all tests to be a CTC-qualifying dependent. $3,000 and $3,600 credits are fully refundable; prior

law limited refunds to $1,400 out of the maximum $2,000 credit. Credit for married parents first phases out at $150,000 of income until credit reaches pre-2021

level; begins second phase out at $400,000 of income. Only citizen children qualify for the $3,000 and $3,600 credits for children under 18. Noncitizens under age

18 who meet the dependency tests of eligibility can qualify other dependent credit.

www.taxpolicycenter.org 12Other Features of the new CTC • Paid monthly to eligible parents in 2021 of all kids with SSNs , no change unless parent/guardian changes or child ages out, so low administrative burden once enrolled • Credit is not counted as income against any means tested program: not SNAP, SSI, or Medicaid -- EITC continues in same once a year refund format • Since the CTC is not reduced as earnings rise until above $112,000, it does not greatly discourage work because there is no decline in benefits until higher incomes • Result is very small negative market work effect from CTC alone ( since other benefits not reduced as earnings rise , it only has a small “income” effect—more below ) • Overall work effects of the ARP are positive and large based on NAS report , as childcare vouchers ( CCDF) are expanded, and new refundable child and development care tax credit ( CDCTC) is enacted,--both encourage market work ; plus, continuing state minimum wages increases in over half the states and tight labor markets also help

Who is helped and why it is important:

first, for poor kids per NAS report

• Childhood poverty is a big problem in the United States, affecting approximately

one-in-seven children, and one-in-five children of color; and childhood poverty

costs the country between $800 billion & $1.1 trillion each year

• Children growing up in poverty begin life at a disadvantage: they attain less

education, face greater health challenges, and are more likely to have difficulty

obtaining steady, well-paying employment in adulthood.

• There are huge longer-term benefits for poor kids and for society . Research

shows that reducing child poverty improves educational attainment, as reflected

in fewer school absences, higher standardized test scores, plus more high school

completion and college attainment. It also improves health in infancy, during

childhood, and in adulthood, as well as reducing mortality and crime.CTC is a good investment, from cost –benefit

POV, especially for poor kids

• The financial gains from reducing childhood poverty persist long past

childhood: low-income children who benefit from safety net programs are

more likely to be employed, earn more as adults and less likely to be poor.

• Long-term investment gain . Expanding the CTC leads to a long-term fiscal

payoff. Because reducing child poverty has a positive , causal, effect on

earnings in adulthood, expanding the CTC brings in more tax revenue later.

• By improving low-income families’ health , the CTC will also would reduce

government medical expenditures for this group.

• In sum, once the full effects of the CTC expansion are counted, the net cost

to taxpayers has been estimated to be as little as 16 cents for every $1 for

child beneficiaries ; & overall social benefits exceeding cost by 8 to 1B. Impacts of the CTC so far – How is it going ? • Where are we today with the CTC ? Where do we need to go ? • Start with basic delivery and benefit effect findings so far • Do it by talking about three rough CTC focal groups 1. Poor and Near Poor Families (under ~ 100/125% poverty ) 2. Working & Middle Class Families (~125%-200%/up to 400% pov.) 3. Higher Income Families (above 400% poverty) • Key issues, arguments, and findings for each group

Public Policy and the Delivery of the CTC • The IRS is now America’s largest cash anti-poverty benefit administrator for families and children • They administer the CTC, EITC and CDCTC,and pay out several hundreds of billions per year in total • But they have problems with reaching the poorest groups compared to working/ middle class and higher income families

How does one get the monthly CTC ? • Tax filers for 2020 began to get the CTC on July 15th – via direct deposit or check ( they should also have received a letter or email notice from IRS that it was coming ) • Non–filers need to determine of they are eligible ( kid SSN, residence test , support test ) and then apply online to the IRS non-filer sign up portal • There is another IRS update portal for managing changes in bank accounts, residency, child caretakers (e.g. divorce), and so on ( details in addenda)

Who gets benefits and what are the impacts ? • Look at where the $$ go and who gets them so far • Then look at reported changes in hardships, savings and other very short run effects of the CTC expansion • Longer term changes depend on reaching all groups, and making the benefits predictable and regular ( like OASDI checks)so families can plan ahead • Longer term effects on low income recipients may even include added family and residential stability

Who gets the CTC --mostly the parents of

children who are regular taxpayers

• Many more children in “working class” families (100-200% poverty

~$30,000 to $70,000 annual incomes ) than in poor families

• 38-40% kids in “working

class” vs. 9-14% who are

poor –and benefits get

to the working class

faster and more regularly

• IRS paid out credits to 59.3 million kids in July and added 1.6 million in

August ,60.9 m; in September, 61.5 million and October ~62 million

• But another 4-5 million more kids did not get the benefit yet—most of

them poorAnd annual “ blue collar” working-class (100- 200% poverty) child benefits are larger too • Their annual benefits are~ $6200 per family ( arrow) • Gain from 2020 CTC (blue) is + $3200 per family per year • Largest gains (~$4600) still for poorer kids, as post CTC, child poverty fell by 3.5 m in August • But again, only half of eligible poor kids benefit so far

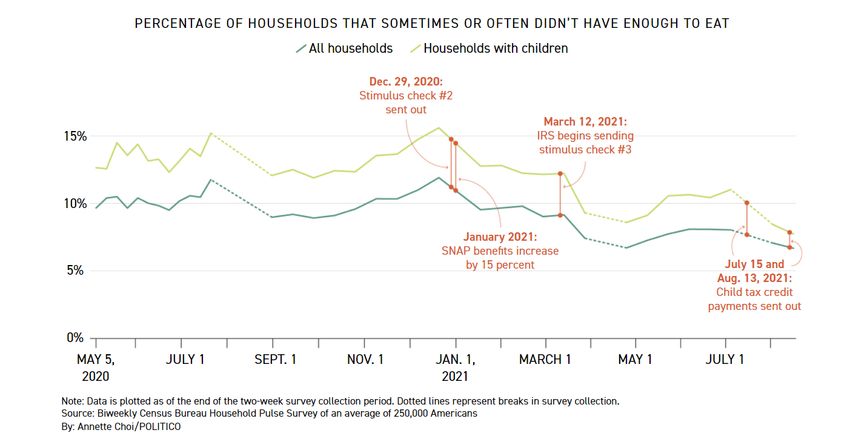

And the effects are already visible for family’s w/ kids in the “Census Pulse Survey” for July 2021 • The new CTC payment is associated with an 8-percentage point (29%) fall in food insufficiency for low-income families • Effects concentrated in families with incomes below $40,000 • So there is need to increase take up amongst the poor & many non-filers or other families still not fully connected to the IRS • Other Census reported effects included declines in families who find it difficult to afford household expenses; increased spending on debt reduction; establishing emergency savings and increased expenses on childcare.

Hunger example: importance of keeping the

CTC and the expanded SNAP beyond 2021

So far so good,

October 21 SNAP

increases and

more CTC

families will push

the line even lowerGroup#1 Poor and near-poor families with kids • So far, the CTC has helped only about half of all poor kids • IRS has had limited success with sign-up and delivery of the CTC to the poor, and other marginalized groups so far • The two CTC access portals for IRS were first designed by Intuit – tax prep firm !!! • But now IRS uses Code for America to build a better non-filer portal (Spanish +,cell-phone access, big step forward-addenda) • Some target populations still need more help : complex families, immigrant families, ‘grandfamilies’

Complex families • Many needy families are complex and unstable, with children who aren’t covered by the tax code’s extensive residency & support rules. • CTC kids need be related to the adult who claims, have their own SSN, and pass a 6-month residence and support test to meet IRS guidelines • About one-third of children are estimated to have lived with non- parent, non-sibling relatives, or unrelated adults at some point during their childhood; 3-10% in any one year (depends on dataset) • These children come from families who are both demographically , and often also residentially unstable, and are largely minority kids • As a result, some children have more than one individual who is eligible to claim them, while others may have no adult who is eligible

Immigrant families • Every citizen child in the US with an SSN is eligible for the CTC, including 6.3 million children of immigrants born here, even if many of the same kids are not eligible for the EITC because of parental tax status and use of an ITIN not an SSN • Non–filers need to determine if they are eligible and then apply online to the IRS non-filer sign up portal assistance • Issues: connect-ability, language, and “trust” issues in some cases , esp. for immigrants who fear ICE or “public charge” rules” ( plus mistaken IRS denials for some mixed status immigrants )

Grandfamilies (and children of the disabled ) • Up to 10 million children live in multigenerational units, and many of these are called “grandfamilies” where grandparents raise their grandchildren with no help from the children's parents • Many of them are struggling to raise grandchildren, and up to 40% of the 6 million children who are living primarily in these grandfamilies are poor or near poor • 4 million adults with children are disabled, with most receiving SSDI or SSI-DI , and another million kids get children’s SSI • SSA is indirectly helping to enroll these children by notifying them of their eligibility, but not directly enrolling them !

The market work issue • How big are the disincentives ? Meyer says BIG substitution effect from removing phase in leads to 1.5 million fewer parents working *) vs. others & NAS (.2-.3 million, much smaller effect ) • Other evidence shows no reduction in market work effort • Estimates of CTC alone ignore effects of new childcare subsidies • Some want work tests, but no evidence that work tests do what they are designed to do, other than harass the beneficiary * Implication from Meyer is that 1.5 m. workers with earnings $30,000-$60,000 would quit working entirely when offered $3,000-$6,000 of child tax credits (see diagram)

Child Tax Credit 2020 and 2021 SINGLE Parent -- one child

FIGURE 2

Child Tax Credit, Single Parent

$4,000 Credit for children ages 0–5

$3,500 Credit for children ages 6–17

$3,000

Prior law credit for children ages

$2,500 6–16

$2,000

$1,500 -Contested area --BIG or small

$1,000

response ?

-No evidence of bunching

$500

at kink points either

$0

$0 $50,000 $100,000 $150,000 $200,000 $250,000 $300,000

Adjusted gross income

Source: Urban-Brookings Tax Policy Center calculations.

Notes: Assumes all income comes from earnings, and child meets all tests to be a CTC-qualifying dependent.

$3,000 and $3,600 credits are fully refundable; prior law limited refunds to $1,400 out of the maximum

$2,000 credit. Credit for married parents first phases out at $150,000 of income until credit reaches pre-2021

www.taxpolicycenter.org 29More tax policy/work support benefit for

lower income workers – the refundable CDCTC

• The Child and Dependent Care Tax Credit (CDCTC)—new for 2021

• Fully refundable 50% rebate to workers w/ income under $125k

• Credit is up to $4,000, if a taxpayer has one qualifying individual;

and $8,000, for two or more qualifying individuals

• Qualifying expenses include the “formal” care of a child under

13, or other dependent unable to care for themselves, incurred

so the taxpayer can work -- or look for work ( NEED RECEIPTS)

• ~20% of CTC parents with kids under 6 use the monthly CTC &

then get a bigger refund, including the CDCTC, in Winter 2022 !Group #2 Working and middle class • We have been far more successful in getting benefits to stable working class (and middle class) families with kids who have close ties to the IRS • Working class are parents with incomes between 100 and 200% of the poverty line, representing 40% of all children. • Indeed, working class parents and their kids are the main beneficiaries of the new monthly Child Tax Credit so far, and are the ones for whom we as a nation have begun to make a big difference.

Helping the struggling working and middle class • A recent study, of the 10 plus year working-class recovery from the Great Recession found that the long recovery eventually benefited the working class—but not until 2018/2019, 9-10 years after it began. • Even then, wages and incomes remained modest at best, with workers in many low-skill professions still earning under $30,000 annually. • In fact, there were no real income gains for working class families at twice the poverty line, about $50,000-$60,000,from 2000 to 2019 , as incomes before and after taxes roughly cancelled each other ( benefits like SNAP & EITC decreased; payroll and income tax liabilities increased). • These families with children were working hard but not really getting ahead until the expanded Child Tax Credit came along in 2021.

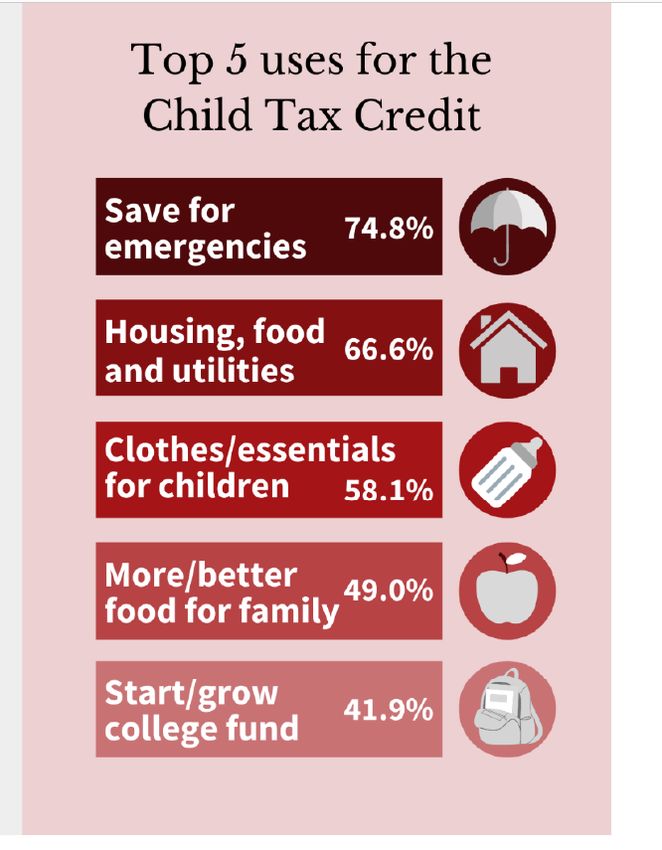

Mobility and security benefits for working and

middle class families

Asked of middle class & working

class families with incomes

below $150,000 per year in June :

“What do you plan to do with

the new monthly CTC

once you start getting it ?”

(About one in five of these

households lost all their savings

in the COVID-19 pandemic)Group # 3. Higher income families--

How fast should the CTC phase out ?

• Only about 10% of all children live in families with incomes above

~$220,000 a year and they get about 9 % of total CTC benefits

• Should CTC be “a nearly universal” or a “somewhat targeted” benefit ?

• Where should tax credits for children phase out – example focus on TCJA

$2000 credit income ceiling added by Senators Lee and Cruz ?

• Matters of equity (high score ) vs. budget savings (less so )

• For example, consider phase outs below $400,000--say about 400%

poverty, where the ACA subsidy phases out ? Or even lower at 300%

poverty as the NAS report on reducing child poverty suggests ?

• Simple example followsFIGURE 2

Child Tax Credit, Married Parents One child 2020-2021

$4,000

Credit for children ages 0–5

$3,500

Credit for children ages 6–17

Phase Out

$3,000

~$150-$215k

$2,500

Prior law credit for children ages 0–16

$2,000

$1,500

Poor & Working & Higher Income Families

$1,000 Near Poor Middle Class

$500

$0

$0 $50,000 $100,000 $150,000 $200,000 $250,000 $300,000 $350,000 $400,000 $450,000 $500,000

Adjusted gross income

Source: Urban-Brookings Tax Policy Center calculations.

Notes: Assumes all income comes from earnings, and child meets all tests to be a CTC-qualifying dependent. $3,000 and $3,600 credits are fully refundable; prior

law limited refunds to $1,400 out of the maximum $2,000 credit. Credit for married parents first phases out at $150,000 of income until credit reaches pre-2021

level; begins second phase out at $400,000 of income. Only citizen children qualify for the $3,000 and $3,600 credits for children under 18. Noncitizens under age

18 who meet the dependency tests of eligibility can qualify other dependent credit.

www.taxpolicycenter.org 35C. Where we stand with the CTC : current payments & improving implementation • Last week : -The October 15th payment was ~$15 b., to 36 m. families & 62 m. children -To date over $61 billion paid to eligible households between July & October • IRS claims that 26 million ‘lower-income children’ ( no definition ) are now receiving the full credit for the first time • BUT the October glitches are on top of the September ones and the August denials for immigrants . The Code for America help site closes November 15th ; plus multiple reports of wrong payment, stoppage for no reason, and lack of feedback are emerging • Still low income families are grateful, and enthusiastic, even if confused, sometimes even AFTER the get the benefit

Results so far for IRS • IRS often confused or non-communicative with “hard to enroll” children • What happens when one adult/parent claims the child credit and another adult/parent tries to use the same SSN to claim the credit ? • What happens when children move from place to place (& mail is not forwarded) ? • IRS is administering a system that needs to account for children moving households within a year, but lacks administrative data documenting where children live and the identity of their primary caretaker • A recent survey of families with children with incomes less than $150,000,found that approximately 80 percent reported claiming a CTC (IPSOS 2021). • Most common reason for not claiming a CTC (42 percent) was that another parent had claimed the payment instead. Contest it , payments stop, and kid loses out .

LIMITS OF IRS in complex family situations • Janet Holtzblatt, the IRS will have difficulty redefining what it means to be someone's child, because it is poorly equipped to determine things like who is supervising a child or whether he or she is living in a secure environment “--from a tax administration perspective, I think the disadvantages outweigh the benefits.” • You cannot run a program like the CTC on a website alone • You have an agency attuned to collecting taxes and striking fear into the hearts of those who are fraudulent, the IRS, not using an agency with 11,ooo offices that helps answer important questions about support, living arrangements and knows how to deliver monthly benefits, the SSA

Key implementation issues and solutions

• Administering a child benefit as a tax credit has inherent limitations (no

other nation does it this way !)

• But we have no national registry other than the SSA and SSNs , and

even here it is incomplete – so let’s get SSA involved ( 11,000 offices

where you can go ) as well as using the IRS for regular stable taxpayers

• How?

--data integration across agencies about child and guardian SSNs or ITNs

--presumptive eligibility for children when born at time SSN conferred

-- tying credit to the child and verifying living arrangements quarterly

-- in person adjustments for changes in family structure, divorce, etc.Bottom Line • A longer time frame ( at least two years ) , with a more responsive delivery system involving an office-based administrator, SSA, is needed to get to the goal of reducing child poverty by 40-45% & stabilizing and improving the lives of poor and lower income kids • SSA has experience with determining financial flows (a Representative Payee monitoring system), getting payments out on time, and having knowledgeable staff • BUT they need to have budget support too!

D. Summary and Conclusion: What’s Next ? • Extending the refundable CTC&CDCTC beyond 2021, now in Biden budget and to be decided within the next few weeks • Most desirable options: --- fewer years, from 5 to 3/2 or 1 ? -- -faster phase out for well-to do ? -- if nothing else, make the current $2000 CTC fully refundable ? • Paying for this investment with higher taxes • Extend CDCTC beyond 2021 • Use SSA , to improve delivery & help with IRS rocky start

Conclusion • NAS & Columbia U. : benefits of CTC outweigh costs 8 to 1 • Packages of benefits including the CTC and CDCTC can reduce poverty and increase market work effort at the same time • Less upward mobility & opportunity for kids now vs. past • Bottom Line: CTC is good for kids and larger society 1. USA has failed at universal health care for all 2. USA was first with universal K-12 education for all 3. Soon, USA has (almost) universal income support for kids ?

Addenda slides follow • More on Who Benefits ( rural blue collar families) • How the Code for America navigation system works • Emergency Savings vs Payday Loans • Mr Manchin is wrong, per great NYT column– but CTC delivery needs to be better executed and soon • Banking angle vs. payday loans -- another LR CTC benefit? • One more table of possible CTC alternatives from the TPC

Rural blue-collar effects largest

Improving delivery and training the navigators/

assisters via Code For America

1. Child Tax Credit (CTC) Non-filer Sign-up Tool (website – English

and Spanish). –where people sign up to for the CTC

2. CTC Non-filer Sign-up Tool Help Guide (PDF - English). Guide

for navigators & assisters, FAQs, in English and Spanish).

3. The GetCTC demo (Video – English). This video is a quick tour

of how to use GetCTC, the simplified tax filing portal.

4. There is another IRS update portal for managing changes in

bank accounts, residency, child caretakers (eg divorce), and

late/missing payments , contested claims, late paymentsEmergency Savings: 75% say this is a use of CTC • Living paycheck to paycheck creates an extreme amount of financial stress for families, frequently resulting in never being able to get ahead. • Being able to weather a financial setback such as a major or even minor car repair is the difference between keeping a job or being out of work. • Families with emergency savings have lower rates of hardship, lower housing volatility, higher food security, all of which are important for children’s development over the long term and their economic success • When faced with a financial emergency or when income falls short of usual expenses, households typically turn to credit. For households with subprime credit scores, credit options may be limited to high-cost options such as payday loans ( next )

Not Payday Loans ! • Payday loans are marketed to people with cash-flow problems. • Lenders advertise these relatively small-dollar loans as a ‘saving grace’ for people living paycheck to paycheck. Short on cash, they borrow using their next paycheck as collateral at very high interest rates and often cannot repay • If families had a reliable stream of cash in the form of advance child tax credit payments, they will avoid getting into such expensive debt.

Mr. Manchin is wrong -- take him 0n • Paying taxes is not a form of “noblesse oblige”, and the social safety net is not a philanthropic project. This nation’s prosperity is a collective achievement, and Americans are entitled to share in that prosperity. Americans also need government support to contribute to that prosperity. A basic goal of providing more help to parents with dependent children is to allow those parents to engage in paid work and to allow their children to flourish • But there is one way in which the government appears overstretched: execution --failures to get help to the right people, failures to prevent the wrong people from taking advantage, and a fair amount of general chaos. • If policy choices, like the CTC, are executed effectively, they may well become more popular, too.

TPC three alternatives for CTC in 2022

You can also read